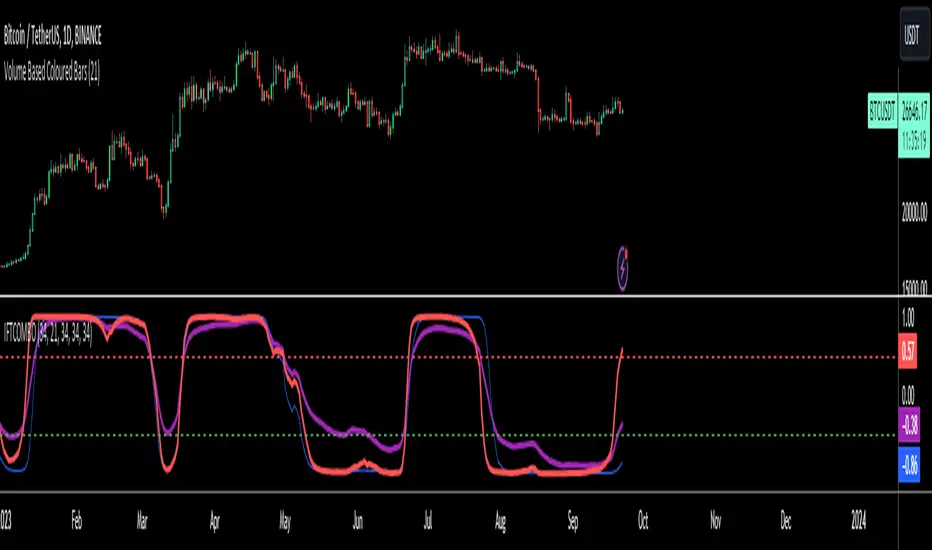

Fusion MFI RSIHello fellas,

This superb indicator summons two monsters called Relative Strength Index (RSI) and Money Flow Index (MFI) and plays the Yu-Gi-Oh! card "Polymerization" to combine them.

Overview

The Fusion MFI RSI Indicator is an advanced analytical tool designed to provide a nuanced understanding of market dynamics by combining the Relative Strength Index (RSI) and the Money Flow Index (MFI). Enhanced with sophisticated smoothing techniques and the Inverse Fisher Transform (IFT), this indicator excels in identifying key market conditions such as overbought and oversold states, trends, and potential reversal points.

Key Features (Brief Overview)

Fusion of RSI and MFI: Integrates momentum and volume for a comprehensive market analysis.

Advanced Smoothing Techniques: Employs Hann Window, Jurik Moving Average (JMA), T3 Smoothing, and Super Smoother to refine signals.

Inverse Fisher Transform (IFT) Enhances the clarity and distinctiveness of indicator outputs.

Detailed Feature Analysis

Fusion of RSI and MFI

RSI (Relative Strength Index): Developed by J. Welles Wilder Jr., the RSI measures the speed and magnitude of directional price movements. Wilder recommended using a 14-day period and identified overbought conditions above 70 and oversold conditions below 30.

MFI (Money Flow Index): Created by Gene Quong and Avrum Soudack, the MFI combines price and volume to measure trading pressure. It is typically calculated using a 14-day period, with over 80 considered overbought and under 20 as oversold.

Application in Fusion: By combining RSI and MFI, the indicator leverages RSI's sensitivity to price changes with MFI's volume-weighted confirmation, providing a robust analysis tool. This combination is particularly effective in confirming the strength behind price movements, making the signals more reliable.

Advanced Smoothing Techniques

Hann Window: Traditionally used to reduce the abrupt data discontinuities at the edges of a sample, it is applied here to smooth the price data.

Jurik Moving Average (JMA): Known for preserving the timing and smoothness of the data, JMA reduces market noise effectively without significant lag.

T3 Smoothing: Developed to respond quickly to market changes, T3 provides a smoother response to price fluctuations.

Super Smoother: Filters out high-frequency noise while retaining important trends.

Application in Fusion: These techniques are chosen to refine the output of the combined RSI and MFI values, ensuring the indicator remains responsive yet stable, providing clearer and more actionable signals.

Inverse Fisher Transform (IFT):

Developed by John Ehlers, the IFT transforms oscillator outputs to enhance the clarity of extreme values. This is particularly useful in this fusion indicator to make critical turning points more distinct and actionable.

Mathematical Calculations for the Fusion MFI RSI Indicator

RSI (Relative Strength Index)

The RSI is calculated using the following steps:

Average Gain and Average Loss: First, determine the average gain and average loss over the specified period (typically 14 days). This is done by summing all the gains and losses over the period and then dividing each by the period.

Average Gain = (Sum of Gains over the past 14 periods) / 14

Average Loss = (Sum of Losses over the past 14 periods) / 14

Relative Strength (RS): This is the ratio of average gain to average loss.

RS = Average Gain / Average Loss

RSI: Finally, the RSI is calculated using the RS value:

RSI = 100 - (100 / (1 + RS))

MFI (Money Flow Index)

The MFI is calculated using several steps that incorporate both price and volume:

Typical Price: Calculate the typical price for each period.

Typical Price = (High + Low + Close) / 3

Raw Money Flow: Multiply the typical price by the volume for the period.

Raw Money Flow = Typical Price * Volume

Positive and Negative Money Flow: Compare the typical price of the current period to the previous period to determine if the money flow is positive or negative.

If today's Typical Price > Yesterday's Typical Price, then Positive Money Flow = Raw Money Flow; Negative Money Flow = 0

If today's Typical Price < Yesterday's Typical Price, then Negative Money Flow = Raw Money Flow; Positive Money Flow = 0

Money Flow Ratio: Calculate the ratio of the sum of Positive Money Flows to the sum of Negative Money Flows over the past 14 periods.

Money Flow Ratio = (Sum of Positive Money Flows over 14 periods) / (Sum of Negative Money Flows over 14 periods)

MFI: Finally, calculate the MFI using the Money Flow Ratio.

MFI = 100 - (100 / (1 + Money Flow Ratio))

Fusion of RSI and MFI

The final Fusion MFI RSI value could be calculated by averaging the IFT-transformed values of RSI and MFI, providing a single oscillator value that reflects both momentum and volume-weighted price action:

Fusion MFI RSI = (MFI weight * MFI) + (RSI weight * RSI)

Suggested Settings and Trading Rules

Original Usage

RSI: Wilder suggested buying when the RSI moves above 30 from below (enter long) and selling when the RSI moves below 70 from above (enter short). He recommended exiting long positions when the RSI reaches 70 or higher and exiting short positions when the RSI falls below 30.

MFI: Quong and Soudack recommended buying when the MFI is below 20 and starts rising (enter long), and selling when it is above 80 and starts declining (enter short). They suggested exiting long positions when the MFI reaches 80 or higher and exiting short positions when the MFI falls below 20.

Fusion Application

Settings: Use a 14-day period for this indicator's calculations to maintain consistency with the original settings suggested by the inventors.

Trading Rules:

Enter Long Signal: Consider entering a long position when both RSI and MFI are below their respective oversold levels and begin to rise. This indicates strong buying pressure supported by both price momentum and volume.

Exit Long Signal: Exit the long position when either RSI or MFI reaches its respective overbought threshold, suggesting a potential reversal or decrease in buying pressure.

Enter Short Signal: Consider entering a short position when both indicators are above their respective overbought levels and begin to decline, suggesting that selling pressure is mounting.

Exit Short Signal: Exit the short position when either RSI or MFI falls below its respective oversold threshold, indicating diminishing selling pressure and a potential upward reversal.

How to Use the Indicator

Select Source and Timeframe: Choose the data source and the timeframe for analysis.

Configure Fusion Settings: Adjust the weights for RSI and MFI.

Choose Smoothing Technique: Select and configure the desired smoothing method to suit the market conditions and personal preference.

Enable Fisherization: Optionally apply the Inverse Fisher Transform to enhance signal clarity.

Customize Visualization: Set up gradient coloring, background plots, and bands according to your preferences.

Interpret the Indicator: Use the Fusion value and visual cues to identify market conditions and potential trading opportunities.

Conclusion

The Fusion MFI RSI Indicator integrates classical and modern technical analysis concepts to provide a comprehensive tool for market analysis. By combining RSI and MFI with advanced smoothing techniques and the Inverse Fisher Transform, this indicator offers enhanced insights, aiding traders in making more informed and timely trading decisions. Customize the settings to align with your trading strategy and leverage this powerful tool to navigate financial markets effectively.

Best regards,

simwai

---

Credits to:

@loxx – T3

@everget – JMA

@cheatcountry – Hann Window

Inversefishertransform

inverse_fisher_transform_adaptive_stochastic█ Description

The indicator is the implementation of inverse fisher transform an indicator transform of the adaptive stochastic (dominant cycle), as in the Cycle Analytics for Trader pg. 198 (John F. Ehlers). Indicator transformation in brief means reshaping the indicator to be more interpretable. The inverse fisher transform is achieved by compressing values near the extremes many extraneous and irrelevant wiggles are removed from the indicator, as cited.

█ Inverse Fisher Transform

input = 2*(adaptive_stoc - .5)

output = e(2*k*input) -1 / e(2*k*input) +1

█ Feature:

iFish i.e. output value

trigger i.e. previous 1 bar of iFish * 0.90

if iFish crosses above the trigger, consider a buy indicated with the green line

while, iFish crosses below the trigger, consider a sell indicate by the red line

in addition iFish needs to be greater than the previous iFish

Fisherized CCIIntroduction

This here is a non-repainting indicator where I use inverse Fisher transformation and smoothing on the well-known CCI (Commdity Channel Index) momentum indicator.

"The Inverse Fisher Transform" describes the calculation and use of the inverse Fisher transform by Dr . Ehlers in 2004. The transform is applied to any indicator with a known probability distribution function. It enables to transform an indicator signal into the range between +1 and -1. This can help to eliminate the noise of an indicator.

The CCI is an momentum indicator which describes the distance of the price to the average price.

For smoothing I used the Hann Window and NET (Noise Elimination Technique) methods.

Additional Features

Divergence Analysis

Trend-adaptive Histogram

Timeframe selection

Usage

It is usually used to spot potential trend reverals or mean-reversion (against the trend) trades on lower timeframes. IMO it can be even used to spot trend-following trades. It always depends on which settings you have, which timeframe do you use and which indicators you combine with it.

The suggested timeframe for this indicator is 15 min (with the length setting on 50).

The histogram with adaptive mode enabled could be used as filter applied on the buy and sell signals.

The divergence analysis can help to spot additional entries/exits or confirm the buy and sell signals.

Always try to find the best settings! This indicators has a lot of customization options you should take advantage of.

Signals

The indicator uses the following logic to generate the buy and sell signals:

Normal

Buy -> When CCI and MA go above the top band (usually +100) and cross

Sell -> When CCI and MA go below the the bottom band (usually -100) and cross

Fisherized

Buy -> When CCI and MA go above the the zero line and cross

Sell -> When CCI and MA go below the the zero line and cross

Have fun with the indicator! I am open for feedback and questions. :)

Non-Lag Inverse Fisher Transform of RSX [Loxx]Non-Lag Inverse Fisher Transform of RSX is an Inverse Fisher Transform on the Non-Lagged Smoothing Filter of Jurik RSX.

What is the Inverse Fisher Transform?

The Inverse Fisher Transform was authored by John Ehlers. The IFT applies some math functions and constants to a moving average of the relative strength index (rsi) of the closing price to calculate its oscillator position. T

read more here: www.mesasoftware.com

What is RSX?

RSI is a very popular technical indicator, because it takes into consideration market speed, direction and trend uniformity. However, the its widely criticized drawback is its noisy (jittery) appearance. The Jurk RSX retains all the useful features of RSI , but with one important exception: the noise is gone with no added lag.

What is the Non-lag moving average?

The Non Lag Moving average follows price closely and gives very quick signals as well as early signals of price change. As a standalone Moving Average, it should not be used on its own, but as an additional confluence tool for early signals.

Included:

Alerts

Signals

Bar coloring

Chimpanzee V2.5 part A by joylay83Hi everyone, I am an amateur pinecoder. I would like to share my script which is coded with the intention of generating signals to send to 3commas webhook. It is still in development and revision.

This collection of indicators use:

Chart: 15m.

Inverse Fisher Transformation of the RSI to detect dips in the 15m timeframe.

Bollinger band (4H) to filter out false signals.

Triple EMA 21: to mimic price action for easier coding alerts. Currently not involved in generating signals. will be incorporated in the future.

StochRSI: As a visual filter. Currently not involved in generating signals. will be incorporated in the future.

Background will be green if stochRSI is low and red if stockRSI is high.

Candlesticks will be marked with a flag is TEMA breached BB.

One would need to play around with timeframes, BB settings and IFTRSI threshold for different signals.

There are 2 Signal Modes (with regards to IFTRSI):

Threshold: When price action falls below BB and IFTRSI hits buy threshold, a buy/sell signal is generated. Eg if IFTRSI buy threshold is set to -0.9, the buy signal will remain continuously positive as long as IFTRSI is < 0.9.

Cross: When price action falls below BB and IFTRSI hits threshold, nothing happens. It will wait until the IFTRSI cross back over the threshold before firing a signal.

There is another identical set of indicators running on a higher time frame (IFTRSI: 4H, BB: D or 3D, TEMA 21 4H) but on the same chart. This tend to generate less signals but are more reliable. A usage example would be to send a larger buy order if the signal comes from this higher time frame, or execute a sell order after multiple buys from the lower time frame.

It comes in 2 parts:

Part A: Contains overlay display. This displays BB, Triple EMA, buy/sell and StochRSI in labels. the labels are self explanatory.

Part B (please search for it): which is actually the same code but contain non-overlay display. You may also put part B overlay=true but scale to LEFT. The advantage of using overlay=true is that you can move the signal right over the candlesticks (mainly for troubleshooting/debugging). This part contains Inverse Fisher RSI, %B, Signal Line. %B is supposedly idential to Bollinger Bands in Part A.

By default, when there is a buy/sell signal:

lower time frame 15m: Signal Line in Part B will turn blue with a value 1 or -1 which corresponds to a buy or sell label in Part A

higher time frame 4H: Signal Line in Part B will turn red with a value 2 or -2 which corresponds to a HTF buy or sell label in Part A

Part A or B may be used to send signal to the webhook. You have to make sure that the settings of Part A and B are identical.

You may choose to un-display some items to reduce clutter.

Current problems:

1. Still too many buy signals

Although many times it will generate excellent buy signal at many swing lows, but there are many buy signals prior to a major swing low. This can be observed in the picture above. It also generate a couple of buy signals prior to the swing lows. I am currently experimenting with 20m and hourly timeframe to address this issue. More filters are needed eg an oscillator or detecting candlestick patterns.

2. Premature sell signals.

The sell signal is often generated at the beginning of a major bull run. My idea to solve this problem is to move to a higher timeframe and sell only when TEMA crossunder the upper bollinger band.

3. Lack of a backtester that can test multiple concurrent deals.

Buy -> Buy (average down) -> Buy (average down) -> Buy (average down) -> Sell

4. Lack of the ability to calculate average purchase price

Probably have to code it as a strategy

5. Display lag

As the browser is running 2 copies of the idential script, it tends to lag when you drag your chart around. So far there are no timeouts or delay in firing alerts to 3commas.

I do welcome any suggestion for improvement and constructive criticism. tqvm.

Credits : Thank you for doing an awesome job. I learnt a lot from your codes and tutorials.

Credits not listed in any order. If your code is used here and did not receive due credit, kindly drop me a note. tq.

Blessing 3 by JTA Today

@ZenAndTheArtOfTrading (extremely-easy-to-understand tutorials eg fixing repainting)

@LazyBear (various codes)

@Galactus-B Argo I

@TheTradingParrot (Inverse Fisher RSI and Gavin's backtester)

@zendog123 (backtester and various codes)

@ydeniz2000 (Bollinger Bands)

TradingView built-in scripts

Inverse Fisher Transform on Williams %RInverse Fisher Transform On Williams %R

Since Williams R indicator produces negative values, I preferred to add 50 instead of subtracting 50.

It produces values between 0.5 and -0.5.

Generates clear buy and sell signals.

Williams %R determines overbought and oversold levels.

You can see more softly.

[GJ]IFRSITHE INVERSE FISHER TRANSFORM STOCH RSI

HOW IT WORKS

This indicator uses the inverse fisher transform on the stoch RSI for clear buying and selling signals. The stoch rsi is used to limit it in the range of 0 and 100. We subtract 50 from this to get it into the range of -50 to +50 and multiply by .1 to get it in the range of -5 to +5. We then use the 9 period weighted MA to remove some "random" trade signals before we finally use the inverse fisher transform to get the output between -1 and +1

HOW TO USE

Buy when the indicator crosses over –0.5 or crosses over +0.5 if it has not previously crossed over –0.5.

Sell when the indicator crosses under +0.5 or crosses under –0.5 if it has not previously crossed under +0.5.

We can see multiple examples of good buy and sell signals from this indicator on the attached chart for QCOM. Let me know if you have any suggestions or thoughts!

[blackcat] L2 Ehlers Inverse Fisher Cyber CycleLevel: 2

Background

John F. Ehlers introuced the Inverse Fisher Transform of Cyber Cycle in May, 2004.

Function

"The Inverse Fisher Transform ," describes the calculation and use of the inverse Fisher transform by Dr . Ehlers in 2004. The transform is applied to any indicator with a known probability distribution function, but this script offers a sample transforms: Cyber Cycle . I have created inputs for the trigger levels for entry and exit so that the user may adjust these levels as desired.

In his article, Dr . Ehlers states the inverse Fisher transform can work with any oscillator, and that values between -1 and 1 are more suited for the transform calculations. Here is one version of the inverse Fisher transform of Cyber Cycle . This version takes the highest and lowest value of the Cyber Cycle and normalizes the scale to a range of -1 to 1. John Ehlers shows how to use the inverse Fisher transform ( IFT ) to compress oscillator-type indicators to give clear trading indications of when to buy or sell. The IFT is a nonlinear transformation that changes the probability distribution, so for example, unbounded indicators can be transformed into bounded indicators with a high probability of being either +1 or -1.

Key Signal

ICycle--> Inverse Fisher Transform of Cyber Cycle fast line

Trigger--> Inverse Fisher Transform of Cyber Cycle slow line

Pros and Cons

100% John F. Ehlers definition translation, even variable names are the same. This help readers who would like to use pine to read his book.

Remarks

The 69th script for Blackcat1402 John F. Ehlers Week publication.

Readme

In real life, I am a prolific inventor. I have successfully applied for more than 60 international and regional patents in the past 12 years. But in the past two years or so, I have tried to transfer my creativity to the development of trading strategies. Tradingview is the ideal platform for me. I am selecting and contributing some of the hundreds of scripts to publish in Tradingview community. Welcome everyone to interact with me to discuss these interesting pine scripts.

The scripts posted are categorized into 5 levels according to my efforts or manhours put into these works.

Level 1 : interesting script snippets or distinctive improvement from classic indicators or strategy. Level 1 scripts can usually appear in more complex indicators as a function module or element.

Level 2 : composite indicator/strategy. By selecting or combining several independent or dependent functions or sub indicators in proper way, the composite script exhibits a resonance phenomenon which can filter out noise or fake trading signal to enhance trading confidence level.

Level 3 : comprehensive indicator/strategy. They are simple trading systems based on my strategies. They are commonly containing several or all of entry signal, close signal, stop loss, take profit, re-entry, risk management, and position sizing techniques. Even some interesting fundamental and mass psychological aspects are incorporated.

Level 4 : script snippets or functions that do not disclose source code. Interesting element that can reveal market laws and work as raw material for indicators and strategies. If you find Level 1~2 scripts are helpful, Level 4 is a private version that took me far more efforts to develop.

Level 5 : indicator/strategy that do not disclose source code. private version of Level 3 script with my accumulated script processing skills or a large number of custom functions. I had a private function library built in past two years. Level 5 scripts use many of them to achieve private trading strategy.

[blackcat] L2 Ehlers Inverse Fisher RSILevel: 2

Background

John F. Ehlers introuced the Inverse Fisher Transform of RSI in May, 2004.

Function

"The Inverse Fisher Transform," describes the calculation and use of the inverse Fisher transform by Dr. Ehlers in 2004. The transform is applied to any indicator with a known probability distribution function, but this script offers a sample transforms: RSI. I have created inputs for the trigger levels for entry and exit so that the user may adjust these levels as desired.

In his article, Dr. Ehlers states the inverse Fisher transform can work with any oscillator, and that values between -1 and 1 are more suited for the transform calculations. Here is one version of the inverse Fisher transform of RSI. This version takes the highest and lowest value of the RSI and normalizes the scale to a range of -1 to 1. John Ehlers shows how to use the inverse Fisher transform (IFT) to compress oscillator-type indicators to give clear trading indications of when to buy or sell. The IFT is a nonlinear transformation that changes the probability distribution, so for example, unbounded indicators can be transformed into bounded indicators with a high probability of being either +1 or -1.

Key Signal

IFish--> Ehlers Inverse Fisher RSI fast line

Trigger--> Ehlers Inverse Fisher RSI slow line

Pros and Cons

100% John F. Ehlers definition translation, even variable names are the same. This help readers who would like to use pine to read his book.

Remarks

The 68th script for Blackcat1402 John F. Ehlers Week publication.

Readme

In real life, I am a prolific inventor. I have successfully applied for more than 60 international and regional patents in the past 12 years. But in the past two years or so, I have tried to transfer my creativity to the development of trading strategies. Tradingview is the ideal platform for me. I am selecting and contributing some of the hundreds of scripts to publish in Tradingview community. Welcome everyone to interact with me to discuss these interesting pine scripts.

The scripts posted are categorized into 5 levels according to my efforts or manhours put into these works.

Level 1 : interesting script snippets or distinctive improvement from classic indicators or strategy. Level 1 scripts can usually appear in more complex indicators as a function module or element.

Level 2 : composite indicator/strategy. By selecting or combining several independent or dependent functions or sub indicators in proper way, the composite script exhibits a resonance phenomenon which can filter out noise or fake trading signal to enhance trading confidence level.

Level 3 : comprehensive indicator/strategy. They are simple trading systems based on my strategies. They are commonly containing several or all of entry signal, close signal, stop loss, take profit, re-entry, risk management, and position sizing techniques. Even some interesting fundamental and mass psychological aspects are incorporated.

Level 4 : script snippets or functions that do not disclose source code. Interesting element that can reveal market laws and work as raw material for indicators and strategies. If you find Level 1~2 scripts are helpful, Level 4 is a private version that took me far more efforts to develop.

Level 5 : indicator/strategy that do not disclose source code. private version of Level 3 script with my accumulated script processing skills or a large number of custom functions. I had a private function library built in past two years. Level 5 scripts use many of them to achieve private trading strategy.

Inverse Fisher Transform of NWMA Aroon Oscillator As originally described by Manfred G. Dürschner. Applies an inverse fisher transform to an aroon oscillator calculated using smoothed price. Smoothing is done via NWMA or "Moving Average 3.0".

Signals are Buy > 0 and Sell < 0

length 1 must be at least twice length 2 (lambda >= 2.0)

Inverse Fisher Transform of SMI and sto. RSI, MTF confirmedThe system uses 1 hour and 15 min timeframe data. Signals coming from 15 min Inverse Fisher Transform of SMI and stochastic RSI are confirmed by 1 hour Inverse Fisher Transform SMI, according to the following rules:

long cond.: 15 min IFTSMI crosses ABOVE -0.5 or SRSI k-line crosses ABOVE 50 while 1-hour IFTSMI is already ABOVE -0.5

short cond.:15 min IFTSMI crosses BELOW 0.5 or SRSI k-line crosses BELOW 50 while 1-hour IFTSMI is already BELOW 0.5

SMI and Inverse Fisher Transform of SMI codes belong to @kivancozbilgic.

Hancock - IFT RSI T3MAThis is a version of the Inverse Fisher Transform Relative Strength Index with T3MA smoothing and histogram difference based on EMA signal line.

Configurable parameters:

RSI length - This is the period used for the RSI .

RSI Smooth Length - This is the smoothing period of the Weighted Moving Average used for the smoothing in Inverse Fisher Transform .

RSI Signal - This is the period used for EMA signal line.

RSI Overbought - Configures the overbought threshold (0.5 default).

RSI Oversold - Configures the oversold threshold (-0.5 default).

T3 Smoothing - Enabling this applies T3MA smoothing to the RSI .

T3 Length - This is the period used for the T3MA smoothing of the RSI .

T3 Factor - This is the factor used for the T3MA smoothing of the RSI .

I've added a histogram plotting the difference between the signal line and RSI to make it easier to make trades. Oversold and Overbought thresholds are indicated by the red and green horizontal lines. Signal line is coloured for trade direction.

Happy trading folks!

Hancock

Hancock - Floating O/B O/S IFT RSI T3MAThis is a version of the Inverse Fisher Transform Relative Strength Index with floating oversold and overbought thresholds.

Configurable parameters:

RSI length - This is the period used for the RSI .

RSI Smooth Length - This is the smoothing period of the Weighted Moving Average used for the smoothing in Inverse Fisher Transform .

RSI Threshold Period - This is the period used for calculating the floating oversold and overbought thresholds.

RSI Overbought - Configures the overbought threshold (80% default).

RSI Oversold - Configures the oversold threshold (20% default).

T3 Smoothing - Enabling this applies T3MA smoothing to the RSI.

T3 Length - This is the period used for the T3MA smoothing of the RSI.

T3 Factor - This is the factor used for the T3MA smoothing of the RSI.

RSI line breaching the thresholds are clearly indicated by filled chart plots.

An inverse Fisher transform of RSI is designed to enhance the extremes (overbought and oversold zones), in combination with floating thresholds this version allows faster and cleaner trend detection and identification. With additional smoothing, false signals can be avoided. As with any other indicator some experimenting with parameters is advised (in order to find optimal settings for symbol/time frame pair).

Happy trading folks!

Hancock

Fisher Least Squares Moving AverageIntroduction

I already estimated the least-squares moving average numerous times, one of the most elegant ways was by rescaling a linear function to the price by using the z-score, today i will propose a new smoother (FLSMA) based on the line rescaling approach and the inverse fisher transform of a scaled moving average error with the goal to provide an alternative least-squares smoother, the indicator won't use the correlation coefficient and will try to adresses problems such as overshoots and lag reduction.

Line Rescaling Method

For those who did not see my least squares moving average estimation using the line rescaling method here is a resume, we want to fit a polynomial function of degree 1 to the price by reducing the sum of squares between the price and the filter, squares is a term meaning the squared difference between the price and its estimation. The line rescaling technique work as follow :

1 - get the z-score of a line.

2 - multiply this z-score with the correlation between the price and a line.

3 - multiply the precedent result with the standard deviation of the price, then sum that to a simple moving average.

This process is shorter than the classical least-squares moving average method.

Z-Score Derivation And The Inverse Fisher Transform

The FLSMA will use a similar approach to the line rescaling technique but instead of using the correlation during step 2 we will use an alternative calculated from the error between the estimate and the price.

In order to do so we must use the inverse fisher transform, the inverse fisher transform can take a z-score and scale it in a range of (1,-1), it is possible to estimate the correlation with it. First lets create our modified z-score in the form of : Z = ma((y - Y)/e) where y is the price, Y our output estimate and e the moving average absolute error between the price and Y and lets call it scaled smoothed error , then apply the inverse fisher transform : r = IFT(Z) = tanh(Z) , we then multiply the z-score of the line with it.

Performance

The FLSMA greatly reduce the overshoots, this mean that the maximas of abs(r) are lower than the maxima's of the absolute correlation, such case is not "bad" but we can see that the filter is not closer to the price than the LSMA during trending periods, we can assume the filter don't reduce least-squares as well as the LSMA.

The image above is the running mean of the absolute error of each the FLSMA (in red) and the LSMA (in blue), we could fix this problem by multiplying the smooth scaled error by p where p can be any number, for example :

z = sma(src - nz(b ,src),length)/e * p where p = 2

In red the FLSMA and in blue the FLSMA with p = 2 , the greater p is the less lag the FLSMA will have.

Conclusion

It could be possible to get better results than the LSMA with such design, the presented indicator use its own correlation replacement but it is possible to use anything in a range of (1,-1) to multiply the line z-score. Although the proposed filter only reduce overshoots without keeping the accuracy of the LSMA i believe the code can be useful for others.

Thanks for reading.

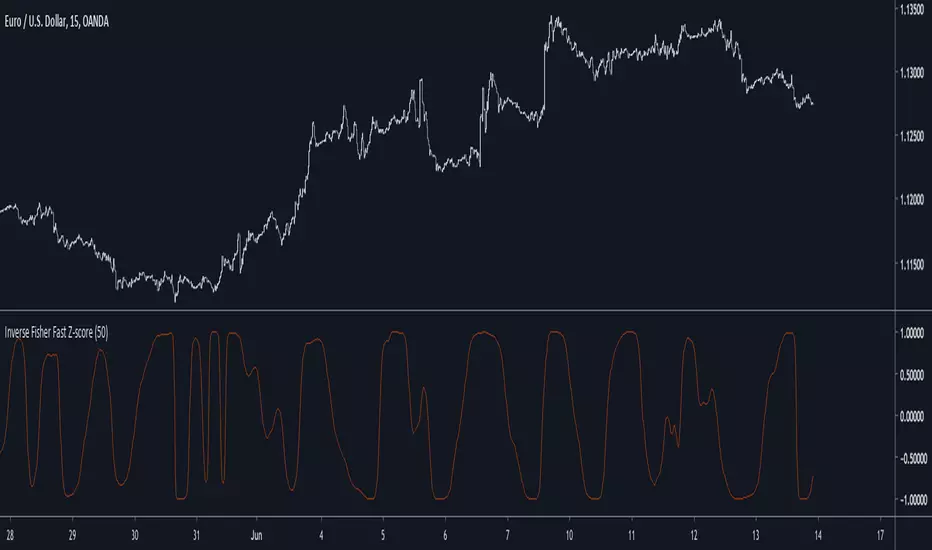

Inverse Fisher Fast Z-scoreIntroduction

The fast z-score is a modification of the classic z-score that allow for smoother and faster results by using two least squares moving averages, however oscillators of this kind can be hard to read and modifying its shape to allow a better interpretation can be an interesting thing to do.

The Indicator

I already talked about the fisher transform, this statistical transform is originally applied to the correlation coefficient, the normal transform allow to get a result similar to a smooth z-score if applied to the correlation coefficient, the inverse transform allow to take the z-score and rescale it in a range of (1,-1), therefore the inverse fisher transform of the fast z-score can rescale it in a range of (1,-1).

inverse = (exp(k*fz) - 1)/(exp(k*fz) + 1)

Here k will control the squareness of the output, an higher k will return heavy side step shapes while a lower k will preserve the smoothness of the output.

Conclusion

The fisher transform sure is useful to kinda filter visual information, it also allow to draw levels since the rescaling is in a specific range, i encourage you to use it.

Notes

During those almost 2 weeks i was even lazier and sadder than ever before, so i think its no use to leave, i also have papers to publish and i need tv for that.

Thanks for reading !

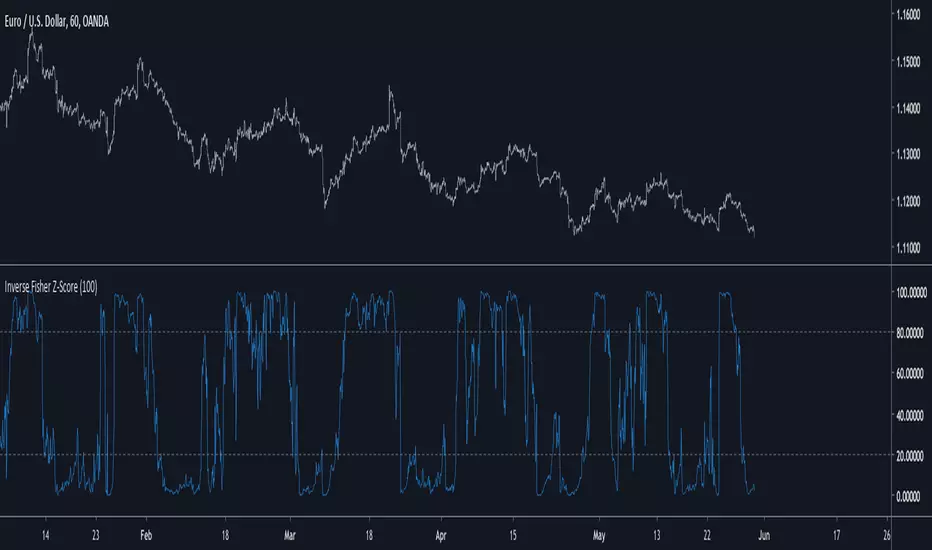

Inverse Fisher Z-Score Introduction

The inverse fisher transform or hyperbolic tangent function is a type os sigmoid function (sometime called squashing function) , those types of functions can rescale a result in a certain range and are widely used in artificial intelligence. More in depth the fisher transform can make the correlation coefficient of a time series normally distributed, in practice if you apply the fisher transform to the correlation coefficient between a time series and a linear function you will end up with an estimate of the z-score of the time series. The inverse transform however can do the contrary, it can take the z-score and transform it into a rough estimate of the correlation coefficient, if your z-score is not smooth then you will have a non-smooth estimate of the correlation coefficient, that's quite nice no ?

The Indicator

The inverse fisher transform of the z-score will produce results in a range of 1/-1, here however i will rescale in a range of 100/0 because its a standard range for oscillators in technical analysis. Values over 80 indicate an overbought market, under 20 an oversold market. The smooth option in the indicator settings will make the indicator use a linearly weighted moving average as input thus resulting in a smoother result.

The indicator with smooth option.

Conclusion

I presented a new oscillator indicator who use the inverse fisher transform of a z-score. Using the fisher transform and its inverse can give a new shape to your indicator, make sure to control the scale of your indicator before applying the fisher transform, the inverse transform should be applied to values in range of 1/-1 but you can use higher limits (2/-2,3/-3...) , however remember that higher limits will approximate an heavy side step function (square shape) . I hope you will find an use to this indicator.

Thanks for reading !

rsiD new form RSI This indicator is based on inverse fisher rsi with some modification

so in this way we can create RSI that if cross the zero its bullish and fall bellow zero is bearish.

Also in this way it easy to create more accurate signal based on the RSI

I set it on 14 length , if you want it more active set it on 5

Inverse Fisher RSI-MTF2 alertsThis is the study with allerts of the RSI-MTF2

if there is repainting then I suggest to go to lower time frame and graph of 1 hour or half hour then it will not repaint. the issue i think exist only in 24 hours time frame when you build it on shorter graph

still the results will be great (test it in strategy that i put before this one)

have fun

Inverse Fisher Transform COMBOThis indicator is the one scripted and published by KIVANCfr3762 (fr3762 @twitter), only difference is the IFT Stochastic Momentum line to be added and also included for average IFT line calculation. Both IFT CCI and IFT CCI V2 lines are included within this script. With the options/settings menu, the lines can be added/removed for displaying on the chart up to preferences.

İndikatör , Kıvanç ( KIVANCfr3762 (fr3762 @twitter) ) hocamızın daha önceden yayınladığı indikatördür, Buna, IFT Stochastic Momentumu ekledim, ve tabi bu hesaplamayı ortalama IFT çizgisi hesabına da dahil ettim. IFT CCI ve IFT CCI V2 iki çizgi de ayrı ayrı indikatörün içinde bulunmaktadır. İstenilenler ayarlar kısmındaki kutucuklardan işaretlenerek/kaldırılarak grafiğin üzerinde gösterimi sağlanabilir.

Fisher Multi-Pack [DW]This is an experimental study designed to visualize price activity using John Ehlers Fisher Transform and Inverse Fisher Transform methods.

The Ehlers Fisher Transform is a variation of R. A. Fisher's Z transformation.

In this study, there are five oscillator types to choose from:

-Fisher Transform Indicator - A conversion of price's probability distribution to a Gaussian normal distribution with a smoother output

-Inverse Fisher Relative Strength Index - Converts the RSI's distribution to a bounded distribution between 1 and -1 with a smoother output

-Inverse Fisher Stochastic Oscillator - Converts the Stochastic's distribution to a bounded distribution between 1 and -1 with a smoother output

-Inverse Fisher Commodity Channel Index - Converts the CCI's distribution to a bounded distribution between 1 and -1 with a smoother output

-Inverse Fisher Blast Off Momentum - Converts the BOM's distribution to a bounded distribution between 1 and -1 with a smoother output

The study uses a modified set of Bollinger Bands applied to the chosen oscillator to determine trend and impulse activity, which are highlighted by the color scheme.

Custom bar colors are included.

Inverse Fisher Transform COMBO STO+RSI+CCIv2 by KIVANÇ fr3762A combined 3in1 version of pre shared INVERSE FISHER TRANSFORM indicators on RSI , on STOCHASTIC and on CCIv2 to provide space for 2 more indicators for users...

About John EHLERS:

From California, USA, John is a veteran trader. With 35 years trading experience he has seen it all. John has an engineering background that led to his technical approach to trading ignoring fundamental analysis (with one important exception).

John strongly believes in cycles. He’d rather exit a trade when the cycle ends or a new one starts. He uses the MESA principle to make predictions about cycles in the market and trades one hundred percent automatically.

In the show John reveals:

• What is more appropriate than trading individual stocks

• The one thing he relies upon in his approach to the market

• The detail surrounding his unique trading style

• What important thing underpins the market and gives every trader an edge

About INVERSE FISHER TRANSFORM:

The purpose of technical indicators is to help with your timing decisions to buy or

sell. Hopefully, the signals are clear and unequivocal. However, more often than

not your decision to pull the trigger is accompanied by crossing your fingers.

Even if you have placed only a few trades you know the drill.

In this article I will show you a way to make your oscillator-type indicators make

clear black-or-white indication of the time to buy or sell. I will do this by using the

Inverse Fisher Transform to alter the Probability Distribution Function ( PDF ) of

your indicators. In the past12 I have noted that the PDF of price and indicators do

not have a Gaussian, or Normal, probability distribution. A Gaussian PDF is the

familiar bell-shaped curve where the long “tails” mean that wide deviations from

the mean occur with relatively low probability. The Fisher Transform can be

applied to almost any normalized data set to make the resulting PDF nearly

Gaussian, with the result that the turning points are sharply peaked and easy to

identify. The Fisher Transform is defined by the equation

1)

Whereas the Fisher Transform is expansive, the Inverse Fisher Transform is

compressive. The Inverse Fisher Transform is found by solving equation 1 for x

in terms of y. The Inverse Fisher Transform is:

2)

The transfer response of the Inverse Fisher Transform is shown in Figure 1. If

the input falls between –0.5 and +0.5, the output is nearly the same as the input.

For larger absolute values (say, larger than 2), the output is compressed to be no

larger than unity . The result of using the Inverse Fisher Transform is that the

output has a very high probability of being either +1 or –1. This bipolar

probability distribution makes the Inverse Fisher Transform ideal for generating

an indicator that provides clear buy and sell signals.

Creator: John EHLERS