FEDFUNDS Rate Divergence Oscillator [BackQuant]FEDFUNDS Rate Divergence Oscillator

1. Concept and Rationale

The United States Federal Funds Rate is the anchor around which global dollar liquidity and risk-free yield expectations revolve. When the Fed hikes, borrowing costs rise, liquidity tightens and most risk assets encounter head-winds. When it cuts, liquidity expands, speculative appetite often recovers. Bitcoin, a 24-hour permissionless asset sometimes described as “digital gold with venture-capital-like convexity,” is particularly sensitive to macro-liquidity swings.

The FED Divergence Oscillator quantifies the behavioural gap between short-term monetary policy (proxied by the effective Fed Funds Rate) and Bitcoin’s own percentage price change. By converting each series into identical rate-of-change units, subtracting them, then optionally smoothing the result, the script produces a single bounded-yet-dynamic line that tells you, at a glance, whether Bitcoin is outperforming or underperforming the policy backdrop—and by how much.

2. Data Pipeline

• Fed Funds Rate – Pulled directly from the FRED database via the ticker “FRED:FEDFUNDS,” sampled at daily frequency to synchronise with crypto closes.

• Bitcoin Price – By default the script forces a daily timeframe so that both series share time alignment, although you can disable that and plot the oscillator on intraday charts if you prefer.

• User Source Flexibility – The BTC series is not hard-wired; you can select any exchange-specific symbol or even swap BTC for another crypto or risk asset whose interaction with the Fed rate you wish to study.

3. Math under the Hood

(1) Rate of Change (ROC) – Both the Fed rate and BTC close are converted to percent return over a user-chosen lookback (default 30 bars). This means a cut from 5.25 percent to 5.00 percent feeds in as –4.76 percent, while a climb from 25 000 to 30 000 USD in BTC over the same window converts to +20 percent.

(2) Divergence Construction – The script subtracts the Fed ROC from the BTC ROC. Positive values show BTC appreciating faster than policy is tightening (or falling slower than the rate is cutting); negative values show the opposite.

(3) Optional Smoothing – Macro series are noisy. Toggle “Apply Smoothing” to calm the line with your preferred moving-average flavour: SMA, EMA, DEMA, TEMA, RMA, WMA or Hull. The default EMA-25 removes day-to-day whips while keeping turning points alive.

(4) Dynamic Colour Mapping – Rather than using a single hue, the oscillator line employs a gradient where deep greens represent strong bullish divergence and dark reds flag sharp bearish divergence. This heat-map approach lets you gauge intensity without squinting at numbers.

(5) Threshold Grid – Five horizontal guides create a structured regime map:

• Lower Extreme (–50 pct) and Upper Extreme (+50 pct) identify panic capitulations and euphoria blow-offs.

• Oversold (–20 pct) and Overbought (+20 pct) act as early warning alarms.

• Zero Line demarcates neutral alignment.

4. Chart Furniture and User Interface

• Oscillator fill with a secondary DEMA-30 “shader” offers depth perception: fat ribbons often precede high-volatility macro shifts.

• Optional bar-colouring paints candles green when the oscillator is above zero and red below, handy for visual correlation.

• Background tints when the line breaches extreme zones, making macro inflection weeks pop out in the replay bar.

• Everything—line width, thresholds, colours—can be customised so the indicator blends into any template.

5. Interpretation Guide

Macro Liquidity Pulse

• When the oscillator spends weeks above +20 while the Fed is still raising rates, Bitcoin is signalling liquidity tolerance or an anticipatory pivot view. That condition often marks the embryonic phase of major bull cycles (e.g., March 2020 rebound).

• Sustained prints below –20 while the Fed is already dovish indicate risk aversion or idiosyncratic crypto stress—think exchange scandals or broad flight to safety.

Regime Transition Signals

• Bullish cross through zero after a long sub-zero stint shows Bitcoin regaining upward escape velocity versus policy.

• Bearish cross under zero during a hiking cycle tells you monetary tightening has finally started to bite.

Momentum Exhaustion and Mean-Reversion

• Touches of +50 (or –50) come rarely; they are statistically stretched events. Fade strategies either taking profits or hedging have historically enjoyed positive expectancy.

• Inside-bar candlestick patterns or lower-timeframe bearish engulfings simultaneously with an extreme overbought print make high-probability short scalp setups, especially near weekly resistance. The same logic mirrors for oversold.

Pair Trading / Relative Value

• Combine the oscillator with spreads like BTC versus Nasdaq 100. When both the FED Divergence oscillator and the BTC–NDQ relative-strength line roll south together, the cross-asset confirmation amplifies conviction in a mean-reversion short.

• Swap BTC for miners, altcoins or high-beta equities to test who is the divergence leader.

Event-Driven Tactics

• FOMC days: plot the oscillator on an hourly chart (disable ‘Force Daily TF’). Watch for micro-structural spikes that resolve in the first hour after the statement; rapid flips across zero can front-run post-FOMC swings.

• CPI and NFP prints: extremes reached into the release often mean positioning is one-sided. A reversion toward neutral in the first 24 hours is common.

6. Alerts Suite

Pre-bundled conditions let you automate workflows:

• Bullish / Bearish zero crosses – queue spot or futures entries.

• Standard OB / OS – notify for first contact with actionable zones.

• Extreme OB / OS – prime time to review hedges, take profits or build contrarian swing positions.

7. Parameter Playground

• Shorten ROC Lookback to 14 for tactical traders; lengthen to 90 for macro investors.

• Raise extreme thresholds (for example ±80) when plotting on altcoins that exhibit higher volatility than BTC.

• Try HMA smoothing for responsive yet smooth curves on intraday charts.

• Colour-blind users can easily swap bull and bear palette selections for preferred contrasts.

8. Limitations and Best Practices

• The Fed Funds series is step-wise; it only changes on meeting days. Rapid BTC oscillations in between may dominate the calculation. Keep that perspective when interpreting very high-frequency signals.

• Divergence does not equal causation. Crypto-native catalysts (ETF approvals, hack headlines) can overwhelm macro links temporarily.

• Use in conjunction with classical confirmation tools—order-flow footprints, market-profile ledges, or simple price action to avoid “pure-indicator” traps.

9. Final Thoughts

The FEDFUNDS Rate Divergence Oscillator distills an entire macro narrative monetary policy versus risk sentiment into a single colourful heartbeat. It will not magically predict every pivot, yet it excels at framing market context, spotting stretches and timing regime changes. Treat it as a strategic compass rather than a tactical sniper scope, combine it with sound risk management and multi-factor confirmation, and you will possess a robust edge anchored in the world’s most influential interest-rate benchmark.

Trade consciously, stay adaptive, and let the policy-price tension guide your roadmap.

M-oscillator

EchoPulse – Trend Oscillator v1 [QuayLade]Harness the Pulse. Surf the Trend.

EchoPulse™ is a precision-crafted Trend Oscillator designed to visualize the cyclic rhythm of market movements while keeping you contextually aligned with Higher Timeframe Influence Zones. Whether you're a scalper, swing trader, or systematic strategist, EchoPulse brings clarity to trend dynamics by filtering out noise and spotlighting pivotal trade opportunities.

Core Features & Innovations:

Surge Markers (Counter-Trend Oscillation Bursts):

Identify statistically unsustainable counter-trend surges with high precision. These Aqua & Orange crosses mark potential exhaustion points during pullbacks, perfect for strategic pyramiding and re-entry setups.

Exhaustion Markers (Trend Fatigue Signals):

Spot early signs of trend fatigue with Green & Red Circles. These markers appear when the market's internal cyclic rhythm shows signs of a structural unwind, assisting in managing exits or preparing for trend reversals.

Synchronized Cyclic Lines (Short, Mid, Long):

Visualize the market’s multi-speed oscillations through dynamically flowing Cycle Lines that latch to extreme zones during strong trends. Their stickiness/persistence offers valuable clues into the trend’s strength or weakening momentum.

Higher Timeframe Influence Zone (Contextual Alignment):

A soft overlay reflecting the directional bias of the Higher Timeframe, ensuring you stay aligned with macro flows without adding visual clutter. Greenish for bullish bias, reddish for bearish, and transparent during indecisive phases.

Adaptive Volatility Intelligence (Noise Suppression):

EchoPulse™ dynamically adjusts its sensitivity based on current market volatility, making it effective across various instruments and timeframes — from scalping to positional trading.

Ideal For:

Trend Traders seeking pullback confirmation within trend continuations.

Swing & Position Traders needing clear alignment with higher timeframe structures.

Scalpers] who require real-time directional cues without lag.

Systematic Traders looking to integrate a dynamic, responsive trend oscillator.

Quick User Guide

Trend Bias Confirmation:

Use the HTF Influence Zone background colour to establish directional bias. Prioritize setups aligned with this macro trend.

Entry Triggers with Surge Markers:

Spot Surge Markers appearing against the HTF bias during pullbacks — a signal of possible exhaustion in counter-trend moves and a potential entry opportunity.

Monitor Cyclic Stickiness:

Persistent latching of Cycle Lines to extreme zones indicates a strong trend continuation. Unlatching and normalization could signal consolidation or a pause in trend momentum.

Exhaustion Markers & Reversals:

Exhaustion Markers highlight when a trend leg may be overextended. Combine them with Price Divergence or Key S/R Levels for stronger reversal signals.

Best Practices:

Use EchoPulse™ as a Trend Continuation and Exhaustion Timing Tool .

Combine with Price Action, Divergence Analysis, and Multi-Timeframe Confluence for high-probability setups.

Adjust chart timeframe based on your trading style — Intraday, Swing, or Positional.

Compliance & Acknowledgement Statement:

EchoPulse™ is an original indicator concept meticulously developed by QuayLade using proprietary techniques that visualize dynamic oscillations, adaptive latching behaviours, and multi-timeframe contextual alignment. While the indicator draws inspiration from universally known mathematical constructs such as Rate of Change (RoC) for assessing price momentum, its computational framework, signal derivations, and visualization structures are uniquely crafted and not direct derivatives of any standard or public domain indicators.

All methodologies implemented are original intellectual property, tailored to offer traders an innovative perspective on market rhythm, trend surges, and exhaustion zones. EchoPulse™ is fully committed to be compliant with TradingView’s Vendor Agreements and House Rules regarding originality, fair usage, and responsible adaptation of foundational market analysis concepts.

Script License & Usage Disclaimer:

The EchoPulse™– Trend Oscillator is a proprietary invite-only script. Unauthorized distribution, reverse engineering, or decompilation of this script is strictly prohibited.

This indicator is provided for informational and educational purposes only and does not constitute financial advice or a trading recommendation. Trading and investing involve substantial risks, and the creator assumes no responsibility for financial losses or damages resulting from its use.

By accessing this script, users agree to use it at their own discretion and understand that the author makes no guarantees regarding its performance or suitability for any specific trading objective.

Support & Assistance:

For any queries, feedback, or assistance with usage:

Contact @QuayLade via TradingView DM.

Documentation, usage guides, and walkthroughs will be provided progressively based on user feedback.

WT_CROSS Dip Buy Signal(ozkan)This script identifies potential buy opportunities based on WaveTrend (WT_CROSS) momentum crossing below the -60 level — often indicating oversold conditions.

Additional filters include price being above the Kaufman Adaptive Moving Average (KAMA) and volume below the 5-period average, which helps isolate pullbacks within an uptrend.

Buy Signal Conditions:

WT1 < -60

Price > KAMA

Volume < 5-period SMA of volume

Purpose:

To capture early entries at possible local bottoms during bullish trends while avoiding high-volume breakdown traps.

🔔 You can also set an alert based on this condition.

CUO WITH BLUE BULL// Core Ultra Oscillator (CUO) with Blue Bull

//

// The Core Ultra Oscillator (CUO) is a technical analysis tool designed to identify potential trend reversals and breakout opportunities by combining momentum, volume, and divergence analysis.

// It aims to enhance divergence-based trading by incorporating additional filters to reduce false signals during strong market trends.

// The indicator integrates WaveTrend Oscillator, regular volume and Cumulative Volume Delta (CVD), generating unique divergence signals enhanced with trend filters to allow greater flexibility in trading style and market type.

//

// Key Features:

// - WaveTrend Oscillator: Plots momentum with customizable overbought and oversold levels, displaying buy (green dots) and sell (red dots) signals for prints in extreme zones.

// - Divergence Detection: Identifies regular and hidden bullish/bearish divergences on WaveTrend and CVD, using green/red lines to connect fractal points for potential trend reversals.

// - Cumulative Volume Delta (CVD): Measures buying and selling pressure with smoothed, normalized delta, enhanced by trend and slope filters for signal reliability.

// - Trend Shift Dots:

// - Green White Dot: Indicates the end of a bearish CVD trend, suggesting a potential bullish shift.

// - Black Dot (Red Center): Signals the end of a bullish CVD trend, indicating a potential bearish shift.

// - Seven Unique Dot Signals:

// - Blue Dot (Blue Bull): Highlights potential bullish breakouts based on accumulated momentum.

// - Yellow Dot (Gold Extreme Buy): Marks potential buying opportunities near market bottoms, often following an amber dot.

// - Purple Dot (Extreme Sell): Identifies high-probability sell signals using divergence and trend weakness filters.

// - Black Dot (Yellow Center): Targets first sign of weakness after a strong bullish trend ends, aiming to capture significant selloffs.

// - Dark Blue Dot: Signals peaks in oversold regions after a bullish trend has ended and momentum has flipped towards the bears.

// - Dark Grey Dot: Warns of potential tops via CVD bearish divergences, ideally confirmed with Purple Dot or regular divergences.

// - Amber Dot: Indicates potential bottoms via CVD bullish divergences, to be confirmed with Yellow Dot or regular divergences.

// - Comprehensive Alerts: Includes 15 alert conditions for WaveTrend, CVD, and dot signals to support real-time trading decisions.

//

// How to Use:

// - Apply the indicator to any chart to monitor momentum, volume, and divergences.

// - Adjust Trend momentum, WaveTrend, CVD, and trend thinning parameters through input settings.

// - Use dot signals and divergence lines to time trade entries and exits.

// - Configure alerts for real-time notifications of key signals.

//

// Note: This indicator is for informational purposes only and does not constitute financial advice. Users are encouraged to backtest thoroughly and evaluate the indicator’s performance in their trading strategy.

MERV: Market Entropy & Rhythm Visualizer [BullByte]The MERV (Market Entropy & Rhythm Visualizer) indicator analyzes market conditions by measuring entropy (randomness vs. trend), tradeability (volatility/momentum), and cyclical rhythm. It provides traders with an easy-to-read dashboard and oscillator to understand when markets are structured or choppy, and when trading conditions are optimal.

Purpose of the Indicator

MERV’s goal is to help traders identify different market regimes. It quantifies how structured or random recent price action is (entropy), how strong and volatile the movement is (tradeability), and whether a repeating cycle exists. By visualizing these together, MERV highlights trending vs. choppy environments and flags when conditions are favorable for entering trades. For example, a low entropy value means prices are following a clear trend line, whereas high entropy indicates a lot of noise or sideways action. The indicator’s combination of measures is original: it fuses statistical trend-fit (entropy), volatility trends (ATR and slope), and cycle analysis to give a comprehensive view of market behavior.

Why a Trader Should Use It

Traders often need to know when a market trend is reliable vs. when it is just noise. MERV helps in several ways: it shows when the market has a strong direction (low entropy, high tradeability) and when it’s ranging (high entropy). This can prevent entering trend-following strategies during choppy periods, or help catch breakouts early. The “Optimal Regime” marker (a star) highlights moments when entropy is very low and tradeability is very high, typically the best conditions for trend trades. By using MERV, a trader gains an empirical “go/no-go” signal based on price history, rather than guessing from price alone. It’s also adaptable: you can apply it to stocks, forex, crypto, etc., on any timeframe. For example, during a bullish phase of a stock, MERV will turn green (Trending Mode) and often show a star, signaling good follow-through. If the market later grinds sideways, MERV will shift to magenta (Choppy Mode), warning you that trend-following is now risky.

Why These Components Were Chosen

Market Entropy (via R²) : This measures how well recent prices fit a straight line. We compute a linear regression on the last len_entropy bars and calculate R². Entropy = 1 - R², so entropy is low when prices follow a trend (R² near 1) and high when price action is erratic (R² near 0). This single number captures trend strength vs noise.

Tradeability (ATR + Slope) : We combine two familiar measures: the Average True Range (ATR) (normalized by price) and the absolute slope of the regression line (scaled by ATR). Together they reflect how active and directional the market is. A high ATR or strong slope means big moves, making a trend more “tradeable.” We take a simple average of the normalized ATR and slope to get tradeability_raw. Then we convert it to a percentile rank over the lookback window so it’s stable between 0 and 1.

Percentile Ranks : To make entropy and tradeability values easy to interpret, we convert each to a 0–100 rank based on the past len_entropy periods. This turns raw metrics into a consistent scale. (For example, an entropy rank of 90 means current entropy is higher than 90% of recent values.) We then divide by 100 to plot them on a 0–1 scale.

Market Mode (Regime) : Based on those ranks, MERV classifies the market:

Trending (Green) : Low entropy rank (<40%) and high tradeability rank (>60%). This means the market is structurally trending with high activity.

Choppy (Magenta) : High entropy rank (>60%) and low tradeability rank (<40%). This is a mostly random, low-momentum market.

Neutral (Cyan) : All other cases. This covers mixed regimes not strongly trending or choppy.

The mode is shown as a colored bar at the bottom: green for trending, magenta for choppy, cyan for neutral.

Optimal Regime Signal : Separately, we mark an “optimal” condition when entropy_norm < 0.3 and tradeability > 0.7 (both normalized 0–1). When this is true, a ★ star appears on the bottom line. This star is colored white when truly optimal, gold when only tradeability is high (but entropy not quite low enough), and black when neither condition holds. This gives a quick visual cue for very favorable conditions.

What Makes MERV Stand Out

Holistic View : Unlike a single-oscillator, MERV combines trend, volatility, and cycle analysis in one tool. This multi-faceted approach is unique.

Visual Dashboard : The fixed on-chart dashboard (shown at your chosen corner) summarizes all metrics in bar/gauge form. Even a non-technical user can glance at it: more “█” blocks = a higher value, colors match the plots. This is more intuitive than raw numbers.

Adaptive Thresholds : Using percentile ranks means MERV auto-adjusts to each market’s character, rather than requiring fixed thresholds.

Cycle Insight : The rhythm plot adds information rarely found in indicators – it shows if there’s a repeating cycle (and its period in bars) and how strong it is. This can hint at natural bounce or reversal intervals.

Modern Look : The neon color scheme and glow effects make the lines easy to distinguish (blue/pink for entropy, green/orange for tradeability, etc.) and the filled area between them highlights when one dominates the other.

Recommended Timeframes

MERV can be applied to any timeframe, but it will be more reliable on higher timeframes. The default len_entropy = 50 and len_rhythm = 30 mean we use 30–50 bars of history, so on a daily chart that’s ~2–3 months of data; on a 1-hour chart it’s about 2–3 days. In practice:

Swing/Position traders might prefer Daily or 4H charts, where the calculations smooth out small noise. Entropy and cycles are more meaningful on longer trends.

Day trader s could use 15m or 1H charts if they adjust the inputs (e.g. shorter windows). This provides more sensitivity to intraday cycles.

Scalpers might find MERV too “slow” unless input lengths are set very low.

In summary, the indicator works anywhere, but the defaults are tuned for capturing medium-term trends. Users can adjust len_entropy and len_rhythm to match their chart’s volatility. The dashboard position can also be moved (top-left, bottom-right, etc.) so it doesn’t cover important chart areas.

How the Scoring/Logic Works (Step-by-Step)

Compute Entropy : A linear regression line is fit to the last len_entropy closes. We compute R² (goodness of fit). Entropy = 1 – R². So a strong straight-line trend gives low entropy; a flat/noisy set of points gives high entropy.

Compute Tradeability : We get ATR over len_entropy bars, normalize it by price (so it’s a fraction of price). We also calculate the regression slope (difference between the predicted close and last close). We scale |slope| by ATR to get a dimensionless measure. We average these (ATR% and slope%) to get tradeability_raw. This represents how big and directional price moves are.

Convert to Percentiles : Each new entropy and tradeability value is inserted into a rolling array of the last 50 values. We then compute the percentile rank of the current value in that array (0–100%) using a simple loop. This tells us where the current bar stands relative to history. We then divide by 100 to plot on .

Determine Modes and Signal : Based on these normalized metrics: if entropy < 0.4 and tradeability > 0.6 (40% and 60% thresholds), we set mode = Trending (1). If entropy > 0.6 and tradeability < 0.4, mode = Choppy (-1). Otherwise mode = Neutral (0). Separately, if entropy_norm < 0.3 and tradeability > 0.7, we set an optimal flag. These conditions trigger the colored mode bars and the star line.

Rhythm Detection : Every bar, if we have enough data, we take the last len_rhythm closes and compute the mean and standard deviation. Then for lags from 5 up to len_rhythm, we calculate a normalized autocorrelation coefficient. We track the lag that gives the maximum correlation (best match). This “best lag” divided by len_rhythm is plotted (a value between 0 and 1). Its color changes with the correlation strength. We also smooth the best correlation value over 5 bars to plot as “Cycle Strength” (also 0 to 1). This shows if there is a consistent cycle length in recent price action.

Heatmap (Optional) : The background color behind the oscillator panel can change with entropy. If “Neon Rainbow” style is on, low entropy is blue and high entropy is pink (via a custom color function), otherwise a classic green-to-red gradient can be used. This visually reinforces the entropy value.

Volume Regime (Dashboard Only) : We compute vol_norm = volume / sma(volume, len_entropy). If this is above 1.5, it’s considered high volume (neon orange); below 0.7 is low (blue); otherwise normal (green). The dashboard shows this as a bar gauge and percentage. This is for context only.

Oscillator Plot – How to Read It

The main panel (oscillator) has multiple colored lines on a 0–1 vertical scale, with horizontal markers at 0.2 (Low), 0.5 (Mid), and 0.8 (High). Here’s each element:

Entropy Line (Blue→Pink) : This line (and its glow) shows normalized entropy (0 = very low, 1 = very high). It is blue/green when entropy is low (strong trend) and pink/purple when entropy is high (choppy). A value near 0.0 (below 0.2 line) indicates a very well-defined trend. A value near 1.0 (above 0.8 line) means the market is very random. Watch for it dipping near 0: that suggests a strong trend has formed.

Tradeability Line (Green→Yellow) : This represents normalized tradeability. It is colored bright green when tradeability is low, transitioning to yellow as tradeability increases. Higher values (approaching 1) mean big moves and strong slopes. Typically in a market rally or crash, this line will rise. A crossing above ~0.7 often coincides with good trend strength.

Filled Area (Orange Shade) : The orange-ish fill between the entropy and tradeability lines highlights when one dominates the other. If the area is large, the two metrics diverge; if small, they are similar. This is mostly aesthetic but can catch the eye when the lines cross over or remain close.

Rhythm (Cycle) Line : This is plotted as (best_lag / len_rhythm). It indicates the relative period of the strongest cycle. For example, a value of 0.5 means the strongest cycle was about half the window length. The line’s color (green, orange, or pink) reflects how strong that cycle is (green = strong). If no clear cycle is found, this line may be flat or near zero.

Cycle Strength Line : Plotted on the same scale, this shows the autocorrelation strength (0–1). A high value (e.g. above 0.7, shown in green) means the cycle is very pronounced. Low values (pink) mean any cycle is weak and unreliable.

Mode Bars (Bottom) : Below the main oscillator, thick colored bars appear: a green bar means Trending Mode, magenta means Choppy Mode, and cyan means Neutral. These bars all have a fixed height (–0.1) and make it very easy to see the current regime.

Optimal Regime Line (Bottom) : Just below the mode bars is a thick horizontal line at –0.18. Its color indicates regime quality: White (★) means “Optimal Regime” (very low entropy and high tradeability). Gold (★) means not quite optimal (high tradeability but entropy not low enough). Black means neither condition. This star line quickly tells you when conditions are ideal (white star) or simply good (gold star).

Horizontal Guides : The dotted lines at 0.2 (Low), 0.5 (Mid), and 0.8 (High) serve as reference lines. For example, an entropy or tradeability reading above 0.8 is “High,” and below 0.2 is “Low,” as labeled on the chart. These help you gauge values at a glance.

Dashboard (Fixed Corner Panel)

MERV also includes a compact table (dashboard) that can be positioned in any corner. It summarizes key values each bar. Here is how to read its rows:

Entropy : Shows a bar of blocks (█ and ░). More █ blocks = higher entropy. It also gives a percentage (rounded). A full bar (10 blocks) with a high % means very chaotic market. The text is colored similarly (blue-green for low, pink for high).

Rhythm : Shows the best cycle period in bars (e.g. “15 bars”). If no calculation yet, it shows “n/a.” The text color matches the rhythm line.

Cycle Strength : Gives the cycle correlation as a percentage (smoothed, as shown on chart). Higher % (green) means a strong cycle.

Tradeability : Displays a 10-block gauge for tradeability. More blocks = more tradeable market. It also shows “gauge” text colored green→yellow accordingly.

Market Mode : Simply shows “Trending”, “Choppy”, or “Neutral” (cyan text) to match the mode bar color.

Volume Regime : Similar to tradeability, shows blocks for current volume vs. average. Above-average volume gives orange blocks, below-average gives blue blocks. A % value indicates current volume relative to average. This row helps see if volume is abnormally high or low.

Optimal Status (Large Row) : In bold, either “★ Optimal Regime” (white text) if the star condition is met, “★ High Tradeability” (gold text) if tradeability alone is high, or “— Not Optimal” (gray text) otherwise. This large row catches your eye when conditions are ripe.

In short, the dashboard turns the numeric state into an easy read: filled bars, colors, and text let you see current conditions without reading the plot. For instance, five blue blocks under Entropy and “25%” tells you entropy is low (good), and a row showing “Trending” in green confirms a trend state.

Real-Life Example

Example : Consider a daily chart of a trending stock (e.g. “AAPL, 1D”). During a strong uptrend, recent prices fit a clear upward line, so Entropy would be low (blue line near bottom, perhaps below the 0.2 line). Volatility and slope are high, so Tradeability is high (green-yellow line near top). In the dashboard, Entropy might show only 1–2 blocks (e.g. 10%) and Tradeability nearly full (e.g. 90%). The Market Mode bar turns green (Trending), and you might see a white ★ on the optimal line if conditions are very good. The Volume row might light orange if volume is above average during the rally. In contrast, imagine the same stock later in a tight range: Entropy will rise (pink line up, more blocks in dashboard), Tradeability falls (fewer blocks), and the Mode bar turns magenta (Choppy). No star appears in that case.

Consolidated Use Case : Suppose on XYZ stock the dashboard reads “Entropy: █░░░░░░░░ 20%”, “Tradeability: ██████████ 80%”, Mode = Trending (green), and “★ Optimal Regime.” This tells the trader that the market is in a strong, low-noise trend, and it might be a good time to follow the trend (with appropriate risk controls). If instead it reads “Entropy: ████████░░ 80%”, “Tradeability: ███▒▒▒▒▒▒ 30%”, Mode = Choppy (magenta), the trader knows the market is random and low-momentum—likely best to sit out until conditions improve.

Example: How It Looks in Action

Screenshot 1: Trending Market with High Tradeability (SOLUSD, 30m)

What it means:

The market is in a clear, strong trend with excellent conditions for trading. Both trend-following and active strategies are favored, supported by high tradeability and strong volume.

Screenshot 2: Optimal Regime, Strong Trend (ETHUSD, 1h)

What it means:

This is an ideal environment for trend trading. The market is highly organized, tradeability is excellent, and volume supports the move. This is when the indicator signals the highest probability for success.

Screenshot 3: Choppy Market with High Volume (BTC Perpetual, 5m)

What it means:

The market is highly random and choppy, despite a surge in volume. This is a high-risk, low-reward environment, avoid trend strategies, and be cautious even with mean-reversion or scalping.

Settings and Inputs

The script is fully open-source; here are key inputs the user can adjust:

Entropy Window (len_entropy) : Number of bars used for entropy and tradeability (default 50). Larger = smoother, more lag; smaller = more sensitivity.

Rhythm Window (len_rhythm ): Bars used for cycle detection (default 30). This limits the longest cycle we detect.

Dashboard Position : Choose any corner (Top Right default) so it doesn’t cover chart action.

Show Heatmap : Toggles the entropy background coloring on/off.

Heatmap Style : “Neon Rainbow” (colorful) or “Classic” (green→red).

Show Mode Bar : Turn the bottom mode bar on/off.

Show Dashboard : Turn the fixed table panel on/off.

Each setting has a tooltip explaining its effect. In the description we will mention typical settings (e.g. default window sizes) and that the user can move the dashboard corner as desired.

Oscillator Interpretation (Recap)

Lines : Blue/Pink = Entropy (low=trend, high=chop); Green/Yellow = Tradeability (low=quiet, high=volatile).

Fill : Orange tinted area between them (for visual emphasis).

Bars : Green=Trending, Magenta=Choppy, Cyan=Neutral (at bottom).

Star Line : White star = ideal conditions, Gold = good but not ideal.

Horizontal Guides : 0.2 and 0.8 lines mark low/high thresholds for each metric.

Using the chart, a coder or trader can see exactly what each output represents and make decisions accordingly.

Disclaimer

This indicator is provided as-is for educational and analytical purposes only. It does not guarantee any particular trading outcome. Past market patterns may not repeat in the future. Users should apply their own judgment and risk management; do not rely solely on this tool for trading decisions. Remember, TradingView scripts are tools for market analysis, not personalized financial advice. We encourage users to test and combine MERV with other analysis and to trade responsibly.

-BullByte

Swing Strategy MTF with Auto SL/TP + Weekly Pivotsested and Working Notes:

Works on any intraday chart (like 1H or 4H)

Uses Daily trend for confirmation by default

Adjust trend EMAs or pivot TF if needed

Wait for a signal label after candle close

Targets and SL are drawn automatically

—

TFPS - TradFi Pressure ScoreThe Data-Driven Answer to a New Market Reality.

This indicator quantifies the pressure exerted by Wall Street on the crypto market across four critical dimensions: Risk Appetite, Fear, Liquidity Flows, and the Opportunity Cost of Capital. Our research has found that the correlation between this 4-dimensional pressure vector and crypto price action reaches peak values of 0.87. This is your decisive macro edge, delivered in real-time.

The Irreversible Transformation

A fundamental analysis of the last five years of market data proves an irreversible transformation: The crypto market has matured into a high-beta risk asset, its fate now inextricably linked to Traditional Finance (TradFi).

The empirical data is clear:

Bitcoin increasingly behaves like a leveraged version of the S&P 500.

The correlation to major stock indices is statistically significant and persistent.

The "digital gold" narrative is refuted by the data; the correlation to gold is virtually non-existent.

This means standard technical indicators are no longer sufficient. Tools like RSI or MACD are blind to the powerful, external macro context that now dominates price action. They see the effect, but not the cause.

The Solution: A 4-Dimensional Macro-Lens

The TradFi Pressure Score (TFPS) is the answer. It is an institutional-grade dashboard that aggregates the four most dominant external forces into a single, actionable score:

S&P 500 (SPY): The Pulse of Risk Appetite. A rising S&P signals a "risk-on" environment, fueling capital flows into crypto.

VIX: The Market's Fear Gauge. A rising VIX signals a "risk-off" flight to safety, draining liquidity from crypto.

DXY (US-Dollar Index): The Anchor of Global Liquidity. A strong Dollar (rising DXY) tightens financial conditions, creating powerful headwinds for risk assets like Bitcoin.

US 10Y Yield: The Opportunity Cost of Capital. Rising yields make risk-free assets more attractive, pulling capital away from non-yielding assets like crypto.

What makes the TFPS truly unique?

1. Dynamic Weighting (The Secret Weapon):

Which macro factor matters most right now? Is it a surging Dollar or a collapsing stock market? The TFPS answers this automatically. It continuously analyzes the correlation of all four components to your chosen asset (e.g., Bitcoin) and adjusts their influence in real-time. The dashboard shows you the exact live weights, ensuring you are always focused on the factor that is currently driving the market.

2. Adaptive Engine:

The forces driving a 15-minute chart are different from those driving a daily chart. The TFPS engine automatically recalibrates its internal lookback periods to your chosen timeframe. This ensures the score is always optimally relevant, whether you are a day trader or a swing trader.

3. Designed for Actionable Insights

The Pressure Line: The indicator's core output. Is its value > 0 (tailwind) or < 0 (headwind)? This provides an instant, unambiguous read on the macro environment for your trade.

The Z-Score (The Contrarian Signal): The background "Stress Cloud" and the discrete dots provide early warnings of extreme macro greed or fear. Readings above +2 or below -2 have historically pinpointed moments of market exhaustion that often precede major trend reversals.

Lead/Lag Status: Gain a critical edge by knowing who is in the driver's seat. The dashboard tells you if TradFi is leading the price action or if crypto is moving independently, allowing you to validate your trade thesis against the dominant market force.

This is a public indicator with protected source code

Access is now available for traders who understand the new market reality at the intersection of crypto and traditional finance.

You are among the first to leverage what is a new standard for macro analysis in crypto trading. Your feedback is highly valued as I continue to refine this tool.

Follow for updates and trade with the full context!

MACD Signal with Williams %R ColoringA simple fused indicator of 2, 1) MACD signal lines made colouring when 2) Williams % R is in overbought or oversold. not my own coding, just took two readily available indicators and coded them together.

Gold 3min Trading Pro [XAU/USD]# Gold 3min Trading Pro - User Guide

## Overview

This is a professional scalping indicator specifically designed for Gold (XAU/USD) trading on 3-minute timeframes. It combines multiple technical analysis methods to provide high-probability entry signals for short-term trading.

## Key Features

### 1. Multi-Timeframe Trend Analysis

- **Major Trend**: Analyzes 15min, 1H, and 4H timeframes using moving averages

- **Short-term Trend**: Focuses on 3-minute price action and moving average alignment

- **Trend Strength**: Rated from 1-3 based on timeframe agreement

### 2. Core Indicators

- **RSI (9-period)**: Momentum oscillator for overbought/oversold conditions

- **Stochastic (9-period)**: %K and %D lines for entry timing

- **MACD**: Additional trend confirmation

- **Volume Analysis**: Detects volume spikes for signal validation

- **ATR-based Volatility Filter**: Ensures adequate market movement

### 3. Signal Types

- **Primary Signals**: Green triangles (LONG) and Red triangles (SHORT)

- **Enhanced Signals**: Stronger signals with multiple confirmations

- **Confirmation Signals**: Small circles for stochastic crossovers

## How to Use

### 1. Setup

- **Timeframe**: Use on 3-minute charts for Gold (XAU/USD)

- **Settings**: Default settings are optimized for Gold scalping

- **Session Filter**: Enable for London/New York sessions (recommended)

### 2. Entry Conditions

#### LONG Entry:

- Major trend is bullish (green background)

- Short-term trend is up or neutral

- RSI shows bullish momentum

- Stochastic indicates oversold recovery

- Volume spike confirmation

- Strong price action (bullish candle)

#### SHORT Entry:

- Major trend is bearish (red background)

- Short-term trend is down or neutral

- RSI shows bearish momentum

- Stochastic indicates overbought reversal

- Volume spike confirmation

- Strong price action (bearish candle)

### 3. Trade Management

- **Quick Target**: 50% of ATR-based calculation

- **Main Target**: Full ATR-based target

- **Stop Loss**: 60% of ATR below/above entry

- **Time Limit**: Exit if no progress within 20 bars (60 minutes)

### 4. Risk Management

- **Position Size**: Risk 1-2% of account per trade

- **Maximum Trades**: 3-5 trades per session

- **Avoid**: Low volatility periods and major news events

## Visual Elements

### Background Colors

- **Light Green**: Bullish major trend

- **Light Red**: Bearish major trend

- **Yellow**: Volume spike detected

- **Intense Colors**: Very strong trend alignment

### Chart Indicators

- **RSI Line (Blue)**: Main momentum indicator

- **Stochastic %K (Orange)**: Fast stochastic line

- **Stochastic %D (Yellow)**: Slow stochastic line

- **Horizontal Lines**: 70 (overbought), 30 (oversold), 50 (midline)

### Information Table (Top Right)

- Total signal count and performance statistics

- Current market conditions and trend strength

- RSI levels and volatility status

- Trading session information

- Last signal timing

## Alert System

### Standard Alerts

- **Scalp Long Signal**: Basic long entry signal

- **Scalp Short Signal**: Basic short entry signal

- **Premium Signals**: High-quality signals with strong confirmation

- **Trend Reversal**: Major trend change notifications

### Alert Setup

1. Right-click on chart → "Add Alert"

2. Select desired alert condition

3. Configure notification method (popup, email, webhook)

4. Set alert frequency to "Once Per Bar Close"

## Best Practices

### 1. Trading Sessions

- **Optimal**: London-NY overlap (3:00-5:00 PM EST)

- **Good**: London session (2:00-11:00 AM EST)

- **Avoid**: Asian session and major news releases

### 2. Market Conditions

- **Best**: Trending markets with normal to high volatility

- **Moderate**: Ranging markets during active sessions

- **Avoid**: Extremely low volatility or choppy conditions

### 3. Confirmation Rules

- Wait for signal triangle to appear

- Check that major trend aligns with signal direction

- Verify volume spike (yellow background)

- Ensure volatility is adequate (check info table)

### 4. Entry Timing

- Enter immediately after signal confirmation

- Use market orders for scalping speed

- Set stop loss and take profit levels immediately

## Settings Customization

### Essential Settings

- **MA Type**: EMA (recommended) or SMA

- **RSI Length**: 9 (default, can adjust 5-14)

- **Volume Threshold**: 1.8 (higher = fewer but stronger signals)

- **Volatility Filter**: Keep enabled for better signal quality

### Display Options

- **Show Scalping Signals**: Main entry signals

- **Show Performance Stats**: Information table

- **Show Trend Filter**: Background trend colors

- **Use Time Filter**: Session-based filtering

## Performance Optimization

### 1. Backtesting Tips

- Test on different market conditions

- Analyze win rate and average profit/loss

- Adjust settings based on historical performance

### 2. Signal Quality

- Higher trend strength (2-3) = better signals

- Volume confirmation improves success rate

- Enhanced signals have higher probability

### 3. Risk Control

- Never risk more than 2% per trade

- Use proper position sizing

- Stop trading after 3 consecutive losses

## Troubleshooting

### Common Issues

1. **No Signals**: Check volatility filter and session timing

2. **Too Many Signals**: Increase volume threshold or enable filters

3. **Poor Performance**: Verify timeframe (must be 3-minute) and symbol (XAU/USD)

### Support

- Ensure TradingView Pro+ subscription for multi-timeframe data

- Verify Gold symbol matches your broker's format

- Update to latest TradingView version

This indicator is designed for experienced traders familiar with scalping techniques and risk management. Always practice on demo accounts before live trading.

MACD-RSI Divergence OscillatorMACD-RSI Divergence Oscillator: Dual Confirmation with Momentum + Divergence Signals

This powerful oscillator combines MACD and RSI into a single normalized visual tool, enriched with automatic divergence detection and smart signal alerts. It’s designed to give traders advanced insights into momentum shifts and trend reversals.

Key Features:

• MACD + RSI Combo: Both indicators are scaled and merged into one oscillator for clearer interpretation.

• Automatic Divergence Detection:

• Bullish & Bearish divergences on both MACD and RSI

• Highlights strong divergences when both confirm

• Trading Signals:

• Detects MACD crossovers and RSI reversals

• Smart buy/sell signals based on momentum + divergence

• Custom Oscillator View:

• Plots MACD and RSI on the same scale

• Visual zero-line, overbought/oversold levels, and customizable colors

• Optional Dashboard Table:

• Displays live indicator values, signal states, and divergence status

Ideal For:

• Spotting early trend reversals

• Confirming trade entries/exits

• Avoiding false signals using dual indicator logic

Highly customizable and suitable for all timeframes and asset types.

ATR%The time period can be customized, which is suitable for finding short-term high-volatility trading pairs, and may be suitable for finding grid trading.

Smart Price Divergence (MACD Filter) + EMA📌 Purpose

This indicator detects Price Divergences with MACD filtered by a 200 EMA trend condition.

It helps identify high-probability reversal zones aligned with market trend context.

🧠 How It Works

1. MACD Divergence Logic

Bearish Divergence:

Price makes a higher high.

MACD makes a lower high.

Price is above EMA (indicating possible exhaustion in bullish trend).

Bullish Divergence:

Price makes a lower low.

MACD makes a higher low.

Price is below EMA (indicating possible exhaustion in bearish trend).

2. EMA Trend Filter

EMA(200) is used as a directional filter:

Bearish divergences considered above EMA (extended bullish conditions).

Bullish divergences considered below EMA (extended bearish conditions).

3. Visual & Alerts

EMA(200) plotted on chart in orange.

Red triangles for Bearish Divergence.

Green triangles for Bullish Divergence.

Alerts fire for both divergence types.

📈 How to Use

Look for divergence signals as potential reversal alerts.

Combine with support/resistance or price action for confirmation.

EMA ensures signals occur in extended zones, increasing reliability.

Recommended Timeframes: 1h, 4h, D.

Markets: Forex, Crypto, Stocks.

⚙️ Inputs

MACD Fast / Slow / Signal Length

EMA Length (default 200)

⚠️ Disclaimer

This script is for educational purposes only. It does not constitute financial advice.

Always test thoroughly before live trading.

Smart RSI Divergence PRO | Auto Lines + Alerts📌 Purpose

This indicator automatically detects Regular and Hidden RSI Divergences between price action and the RSI oscillator.

It plots divergence lines directly on the chart, labels signals, and includes alerts for automated monitoring.

🧠 How It Works

1. RSI Calculation

RSI is calculated using the selected Source (default: Close) and RSI Length (default: 14).

2. Divergence Detection via Fractals

Swing points on both price and RSI are detected using fractal logic (5-bar patterns).

Regular Divergence:

Bearish: Price forms a higher high, RSI forms a lower high.

Bullish: Price forms a lower low, RSI forms a higher low.

Hidden Divergence:

Bearish: Price forms a lower high, RSI forms a higher high.

Bullish: Price forms a higher low, RSI forms a lower low.

3. Auto Drawing Lines

Lines are drawn automatically between divergence points:

Red = Regular Bearish

Green = Regular Bullish

Orange = Hidden Bearish

Blue = Hidden Bullish

Line width and transparency are adjustable.

4. Labels and Alerts

Labels mark divergence points with up/down arrows.

Alerts trigger for each divergence type.

📈 How to Use

Use Regular Divergences to anticipate trend reversals.

Use Hidden Divergences to confirm trend continuation.

Combine with support/resistance, trendlines, or volume for higher probability setups.

Recommended Timeframes: Works on all timeframes; more reliable on 1h, 4h, and Daily.

Markets: Forex, Crypto, Stocks.

⚙️ Inputs

Source (Close, HL2, etc.)

RSI Length

Toggle Regular / Hidden Divergence visibility

Toggle Lines / Labels

Line Width & Line Transparency

⚠️ Disclaimer

This script is for educational purposes only. It does not constitute financial advice.

Always test thoroughly before using in live trading.

Smart Impulse Exhaustion Finder (ATR + ADX Filter)📌 Purpose

This indicator detects potential exhaustion of strong bullish or bearish impulses at fresh swing highs/lows by combining multiple price action and volatility-based filters.

🧠 How It Works

A signal is triggered only when all core conditions are satisfied:

1. Swing High/Low Detection

Current high (or low) must be the highest (or lowest) over the last Extremum Lookback bars (default: 50).

This ensures the move is significant relative to recent price action.

2. Impulse Confirmation

Price must extend by at least 1 × ATR from the previous swing point.

This filters out minor fluctuations.

3. Exhaustion Conditions (at least 2 out of 3 must be met)

RSI Extreme: RSI > Overbought Level (default: 80) for bearish signals, RSI < Oversold Level (default: 20) for bullish signals.

Volume Spike: Volume > SMA(Volume, Volume SMA Length) × Volume Spike Multiplier.

Candle Wick Rejection: Upper wick ≥ Wick Threshold % for bearish setups, Lower wick ≥ Wick Threshold % for bullish setups.

4. Trend Filter

ADX > ADX Threshold ensures the market is trending and filters out sideways conditions.

5. Candle Body Filter

Candle body must be ≥ Body Size ATR Factor × ATR.

This avoids weak signals from small candles or doji formations.

📈 How to Use

Bearish Signal:

Appears at fresh swing highs with exhaustion conditions met. Useful for tightening stops, taking partial profits, or counter-trend shorts.

Bullish Signal:

Appears at fresh swing lows with exhaustion conditions met. Useful for trailing stops, profit-taking, or counter-trend longs.

Recommended Timeframes: Works best on 1h, 4h, and Daily charts.

Markets: Crypto, Forex, Stocks — wherever volatility and trends are present.

⚙️ Inputs

RSI Length / Overbought / Oversold

Volume SMA Length & Volume Spike Multiplier

Wick Threshold %

Extremum Lookback (bars for highs/lows)

ADX Length & Threshold

Body Size ATR Factor

⚠️ Disclaimer

This script is for educational purposes only and does not constitute financial advice.

Always test thoroughly and apply proper risk management before live trading.

💡 Tip: Combine this tool with your own market context and confluence factors for higher probability setups.

JHW Volume Based Buy and Sell MomentumThe JHW Volume-Based Buy and Sell Momentum indicator is a custom momentum oscillator designed to capture market sentiment based on volume dynamics and price rate of change (ROC). It aims to identify bullish or bearish momentum by analyzing how price reacts to increasing or decreasing trading volume.

Core Logic:

The indicator calculates the Rate of Change (ROC) of the closing price.

It then accumulates this ROC separately based on whether the current volume is lower or higher than the previous bar:

If volume decreases, the ROC is added to a "negative volume index" accumulator.

If volume increases, the ROC is added to a "positive volume index" accumulator.

These two accumulators are combined to form a net momentum line.

Smoothing:

A Simple Moving Average (SMA) is applied to both accumulators over a user-defined period (default: 25 bars).

The sum of these smoothed values forms the signal line.

Visualization:

The indicator plots:

The net momentum line (yellow).

The smoothed signal line (blue).

The area between the two lines is filled with color:

Yellow when momentum is above the signal (bullish).

Blue when momentum is below the signal (bearish).

Bar colors are also adjusted to reflect the current momentum state.

Use Case:

This indicator helps traders:

Detect volume-driven momentum shifts.

Identify potential buy or sell zones based on volume behavior.

Confirm trends or spot early reversals.

XRSI-Momentum IndexThe XRSI Momentum Index is an enhanced, presentation‑ready implementation of the classic Relative Strength Index (RSI) for TradingView.

It retains the mathematical simplicity of J. Welles Wilder’s RSI while adding a modern visual layer and alert framework that makes momentum assessment faster and less error‑prone on intraday as well as swing charts.

Interpretation Guide

Momentum confirmation

RSI above the Neutral (50) → bullish bias; below → bearish bias.

Noise filters

When RSI oscillates only between OB Noise & OS Noise, ignore whipsaw and stay flat or trend‑follow with reduced size.

Reversal scout

A full cross into the OB or OS band (beyond the noise area) followed by a cross back into the Noise band signals early exhaustion.

EMA overlay

• RSI > EMA RSI → momentum acceleration.

• RSI < EMA RSI → momentum cooling.

Combine with price structure (higher‑highs / lower‑lows) for divergence detection.

Quick‑Start

Add to Chart

Indicators → Invite‑only scripts → XRSI Momentum Index (or paste the source into Pine editor).

Tune Zones

For volatile pairs (e.g., GBPJPY), widen OB/OS to 80 / 20.

For range‑bound assets (e.g., EURCHF), tighten to 60 / 40.

Set Alerts

Right‑click indicator → Add alert → choose condition (e.g., “Entry Into Oversold Area”) → route to webhook or app.

Optional EMA Strategy

Overlay price 50/200 EMA on chart; trade only when XRSI and price trend agree.

Trigonometric StochasticTrigonometric Stochastic - Mathematical Smoothing Oscillator

Overview

A revolutionary approach to stochastic oscillation using sine wave mathematical smoothing. This indicator transforms traditional stochastic calculations through trigonometric functions, creating an ultra-smooth oscillator that reduces noise while maintaining sensitivity to price changes.

Mathematical Foundation

Unlike standard stochastic oscillators, this version applies sine wave smoothing:

• Raw Stochastic: (close - lowest_low) / (highest_high - lowest_low) × 100

• Trigonometric Smoothing: 50 + 50 × sin(2π × raw_stochastic / 100)

• Result: Naturally smooth oscillator with mathematical precision

Key Features

Advanced Smoothing Technology

• Sine Wave Filter: Eliminates choppy movements while preserving signal integrity

• Natural Boundaries: Mathematically constrained between 0-100

• Reduced False Signals: Trigonometric smoothing filters market noise effectively

Traditional Stochastic Levels

• Overbought Zone: 80 level (dashed line)

• Oversold Zone: 20 level (dashed line)

• Midline: 50 level (dotted line) - equilibrium point

• Visual Clarity: Clean oscillator panel with clear level markings

Smart Signal Generation

• Anti-Repaint Logic: Uses confirmed previous bar values

• Buy Signals: Generated when crossing above 30 from oversold territory

• Sell Signals: Generated when crossing below 70 from overbought territory

• Crossover Detection: Precise entry/exit timing

Professional Presentation

• Separate Panel: Dedicated oscillator window (overlay=false)

• Price Format: Formatted as price indicator with 2-decimal precision

• Theme Adaptive: Automatically matches your chart color scheme

Parameters

• Cycle Length (5-200): Period for highest/lowest calculations

- Shorter periods = more sensitive, more signals

- Longer periods = smoother, fewer but stronger signals

Trading Applications

Momentum Analysis

• Overbought/Oversold: Clear visual identification of extreme levels

• Momentum Shifts: Early detection of momentum changes

• Trend Strength: Monitor oscillator position relative to midline

Signal Trading

• Long Entries: Buy when crossing above 30 (oversold bounce)

• Short Entries: Sell when crossing below 70 (overbought rejection)

• Confirmation Tool: Use with trend indicators for higher probability trades

Divergence Detection

• Bullish Divergence: Price makes lower lows, oscillator makes higher lows

• Bearish Divergence: Price makes higher highs, oscillator makes lower highs

• Early Warning: Spot potential trend reversals before they occur

Trading Strategies

Scalping (5-15min timeframes)

• Use cycle length 10-14 for quick signals

• Focus on 20/80 level bounces

• Combine with price action confirmation

Swing Trading (1H-4H timeframes)

• Use cycle length 20-30 for reliable signals

• Wait for clear crossovers with momentum

• Monitor divergences for reversal setups

Position Trading (Daily+ timeframes)

• Use cycle length 50+ for major signals

• Focus on extreme readings (below 10, above 90)

• Combine with fundamental analysis

Advantages Over Standard Stochastic

1. Smoother Action: Sine wave smoothing reduces whipsaws

2. Mathematical Precision: Trigonometric functions provide consistent behavior

3. Maintained Sensitivity: Smoothing doesn't compromise signal quality

4. Reduced Noise: Cleaner signals in volatile markets

5. Visual Appeal: More aesthetically pleasing oscillator movement

Best Practices

• Market Context: Consider overall trend direction

• Multiple Timeframe: Confirm signals on higher timeframes

• Risk Management: Always use proper position sizing

• Backtesting: Test parameters on your preferred instruments

• Combination: Works excellently with trend-following indicators

Built-in Alerts

• Buy Alert: Trigonometric stochastic oversold crossover

• Sell Alert: Trigonometric stochastic overbought crossunder

Technical Specifications

• Pine Script Version: v6

• Panel: Separate oscillator window

• Format: Price indicator with 2-decimal precision

• Performance: Optimized for all timeframes

• Compatibility: Works with all instruments

Free and open-source indicator. Modify, improve, and share with the community!

Educational Value: Perfect for traders wanting to understand how mathematical smoothing improves oscillators and trigonometric applications in technical analysis.

COT Comm OsciDescription

The COT Comm Osci is a sentiment oscillator based on net positions from the weekly Commitments of Traders (COT) report.

It transforms net positions of Commercials, Noncommercials, or Nonreportables into a 0–100 index.

A value of 100 = highest net position within the selected timeframe.

A value of 0 = lowest net position.

You can define three historical intervals (e.g. 26/ 52 / 156 weeks).

Tip

To improve your analysis, it's recommended to add a separate COT indicator that visualizes raw Long/Short or net positions directly. This helps interpret the oscillator in context.

This script is based on “Commercial Index–Buschi” by MagicEins and has been extended with new features and error handling.

Features

Select between Commercial, Noncommercial, or Nonreportable trader groups

Proper handling of HG Futures (Copper)

Displays a warning if the root code is invalid (unsupported market symbol)

Assets Correlation AnalyzerAssets Correlation Analyzer

---------------------------------------------

What is it?

The Assets Correlation Analyzer is a technical indicator that measures and visualizes the statistical relationship between any two financial assets (a 'Base Asset' vs. a 'Comparison Asset', example Gold vs. SPY or Nasdaq vs. Bitcoin). The indicator calculates dynamic correlation tracking using statistical methods, confidence intervals, and category-wide analysis capabilities.

---------------------------------------------

Why was it built? / Potential Benefits

This indicator was developed to help analyze inter-asset relationships in portfolio management and trading strategies. The indicator can be used for:

Risk Assessment: Identify when assets begin moving together

Diversification Analysis: Monitor portfolio component relationships

Pairs Trading: Identify when correlated assets diverge

Market Analysis: Recognize shifts in market conditions through correlation patterns

Asset Analysis: Support decision-making based on correlation dynamics

Hedging Analysis: Identify relationships between different instruments

---------------------------------------------

How it Works

The indicator employs established statistical methods to calculate rolling correlations between two selected assets:

Data Collection: Retrieves price data for both selected assets using TradingView's security function

Returns Calculation: Computes logarithmic or simple returns based on user preference

Outlier Filtering: Optionally removes extreme price movements (beyond 2.5 standard deviations) to improve accuracy

Correlation Computation: Calculates either Pearson or Spearman rank correlation over the specified period

Signal Generation: Applies smoothing and generates a signal line (EMA) for momentum detection

Confidence Assessment: Evaluates data quality and provides confidence metrics

---------------------------------------------

How to Read the Oscillator

Main Correlation Line

Values Range: -1.0 to +1.0

+1.0: Perfect positive correlation (assets move identically)

+0.7 to +0.99: Strong positive correlation

+0.3 to +0.69: Moderate positive correlation

-0.3 to +0.29: Weak/No significant correlation

-0.69 to -0.31: Moderate negative correlation

-0.99 to -0.7: Strong negative correlation

-1.0: Perfect negative correlation (assets move oppositely)

Color Coding System

Green shades: Positive correlation levels, with brighter green indicating stronger positive correlation

Red shades: Negative correlation levels, with brighter red indicating stronger negative correlation

Gray: Insufficient data or transitional periods

The color intensity reflects both correlation strength and momentum relative to the signal line.

Signal Line (Gray)

The EMA-based signal line helps identify momentum changes:

Correlation above signal: Positive momentum in correlation

Correlation below signal: Negative momentum in correlation

Crossovers: Potential turning points in the relationship

Background Fills

Gradient fills provide a quick visual assessment of correlation strength, with intensity indicating the degree of correlation.

---------------------------------------------

Correlation Calculation Methods and Options

Calculation Methods

Spearman Rank Correlation (Default)

Uses ranked values rather than raw prices

Less sensitive to outliers and non-linear relationships

Suitable for volatile or non-normally distributed assets

Pearson Correlation (Traditional)

Standard linear correlation method

More sensitive to outliers

Suitable for assets with normal distribution patterns

---------------------------------------------

Customization Options

Correlation Period (7-500 bars): Determines the lookback window for calculation

Signal Line Period (1-200 bars): Controls the smoothing of the signal line

Outlier Removal: Automatically filters extreme price movements

Return Type: Choose between logarithmic (recommended) or simple returns

Smoothing Period: Reduces noise in correlation readings

---------------------------------------------

Asset Categories

The indicator includes 80+ pre-configured assets across multiple categories:

Metals: Gold, Silver, Copper, Platinum, Palladium, Nickel, Zinc, Aluminum

Energy: WTI/Brent Crude, Natural Gas, Uranium

Agriculture: Corn, Soybeans, Wheat, Coffee

ETFs: Major indices, sector, geographic, and specialty ETFs

Bonds: Government and corporate bond instruments

Financial: Currency pairs, treasury yields, volatility indices

Cryptocurrencies: Major digital assets and market cap indices

Real Estate: REITs and real estate focused instruments

---------------------------------------------

For Whom This Indicator Is Designed

Intended Users

Portfolio Managers: Asset allocation and risk assessment

Quantitative Traders: Correlation-based strategy development

Risk Analysts: Correlation monitoring and analysis

Institutional Investors: Diversification analysis

Active Traders: Pairs trading and arbitrage analysis

Skill Level

Intermediate to Advanced: Requires understanding of correlation concepts and statistical interpretation

Experience with Statistics: Users should be familiar with correlation analysis concepts

---------------------------------------------

Information Tables

Main Analysis Table

Displays current correlation value, data confidence percentage, and selected asset information.

Category Correlation Table

Shows correlation strength between the selected 'Base Asset' (in the chart, Gold) and all assets in the comparison asset's category.

---------------------------------------------

Alert Conditions

Four built-in alert types:

Strong Stable Positive Correlation: Triggers when correlation exceeds +0.8 with low volatility

Strong Stable Negative Correlation: Triggers when correlation falls below -0.8 with low volatility

Bullish Correlation Momentum: Signals when correlation crosses above the signal line

Bearish Correlation Momentum: Signals when correlation crosses below the signal line

---------------------------------------------

Usage Notes

Longer periods (30-50 bars) provide more stable analysis

Shorter periods (10-20 bars) provide more responsive signals

Monitor confidence levels - correlations with <75% confidence should be interpreted cautiously

Correlations tend to increase during market stress periods

Should be used in conjunction with other analysis tools

---------------------------------------------

Important Disclaimer

This indicator is for educational and informational purposes only. It should not be considered as financial advice or a recommendation to buy, sell, or hold any financial instrument. Past correlation patterns do not guarantee future relationships between assets. Users should conduct their own research and consider consulting with a qualified financial advisor before making investment decisions. Trading and investing involve substantial risk of loss, and correlation analysis cannot eliminate these risks. The accuracy of correlation calculations depends on data quality and market conditions, which can change rapidly.

Blue Dot Pullback with Bollinger BonusKey FeaturesCore Blue Dot Condition:ATH Pulse: Checks if the highest high in the lookback period (default: 60 bars) is within 1% of the all-time high (over 5000 bars), using recentHigh >= allTimeHigh * 0.99.

Pullback: Price must be below the recent high (close < recentHigh ) but above a 10-period SMA (close > sma10) to ensure a bullish context.

Stochastic Crossover: Stochastic %K must cross above 20 (ta.crossover(k, stochOverSold)).

When these conditions are met, a blue dot is plotted below the bar.

Purple Dot Condition (Bollinger Band Bonus):Includes all blue dot conditions plus the price being within 2% of the lower Bollinger Band (close <= lowerBB * bbProximity).

When met, a purple dot is plotted instead of a blue dot to highlight the stronger signal.

Plotting Logic:Blue dots are plotted only when blueDotCondition is true and purpleDotCondition is false to avoid overlap.

Purple dots are plotted when purpleDotCondition is true (includes Bollinger Band proximity).

Alerts:Added separate alertcondition calls for blue and purple dots, allowing you to set up notifications in TradingView for each signal type.

Visualization:Stochastic %K and %D are plotted in a separate pane for reference, along with the oversold line (20).

You can disable the Stochastic plot by setting display=display.none in the plot functions.

Why This Should WorkCore Setup Alignment: The blue dot condition focuses on the core requirements (ATH, pullback, Stochastic crossover), which should produce signals similar to or more frequently than the ChatGPT script, as it omits the Bollinger Band requirement unless the purple dot condition is met.

Bollinger Band Bonus: The purple dot incorporates the Bollinger Band proximity check (bbNear), matching the ChatGPT script’s additional filter, ensuring purple dots appear when the price is near the lower Bollinger Band.

Flexible ATH Detection: Using recentHigh >= allTimeHigh * 0.99 makes the ATH condition less strict, increasing the likelihood of signals compared to my original script.

How to UseAdd to TradingView:Open the Pine Editor in TradingView.

Copy and paste the script.

Click "Add to Chart" to apply it.

Interpret Dots:Blue Dot: Indicates a stock near an ATH, in a pullback (above 10-period SMA), with a Stochastic crossover above 20. This is the core Dr. Wish setup.

Purple Dot: Same as blue dot but with the price also within 2% of the lower Bollinger Band, suggesting a stronger pullback signal.

Test and Compare:Apply the script to the same stock and timeframe where the ChatGPT script showed blue dots (e.g., NVDA or TSLA on a daily chart).

Check if blue dots appear at similar points and if purple dots appear when the price is near the lower Bollinger Band.

Adjust lookbackATH (e.g., 60 to 100) or bbProximity (e.g., 1.02 to 1.05) if signals are too rare or frequent.

Set Alerts:Use TradingView’s alert feature to create notifications for “Blue Dot Alert” or “Purple Dot Alert” when signals occur.

TroubleshootingIf you’re still not seeing blue or purple dots:Check the Chart: Ensure the stock has recently hit an ATH and pulled back. Test on volatile stocks like NVDA, TSLA, or AAPL on daily or weekly timeframes.

Timeframe Sensitivity: The script may produce fewer signals on lower timeframes (e.g., 1-hour) due to fewer ATH occurrences. Try a daily or weekly chart.

Parameter Tuning: Increase bbProximity (e.g., to 1.05) to allow purple dots for prices slightly further from the lower Bollinger Band, or increase lookbackATH to capture more ATHs.

Compare with ChatGPT Script: Run both scripts on the same chart to identify where signals differ. Share the ticker, timeframe, or a screenshot if you need help debugging specific cases.

Additional NotesThe 10-period SMA in the pullback condition (isPullback) is a simple bullish context filter. You can replace it with another condition (e.g., 20-period SMA or trend filter) if preferred.

The Bollinger Band parameters (bbLength=20, bbMult=2.0) are standard but can be adjusted to match your trading style.

The script uses a 5000-bar lookback for allTimeHigh to approximate a true ATH. If your chart has limited historical data, reduce this value (e.g., to 1000).

EMA-VWAP Super Reversal (Final Advanced Version)EMA-VWAP Super Reversal – User Guide

This indicator is designed for high-probability reversal trading setups on futures such as NQ1! and ES1!, following strict confluence conditions.

✅ Signal Types

🟢 / 🔴 Mean Reversion Dots

Appear when all 4 stochastics (15m, 5m, 1m) are extreme (>80 or <20)

AND price is far (>0.05% by default, adjustable) from EMA21 on the 15m.

Indicates potential snapback to EMAs.

🔺 Green / Orange EMA Reversal Triangles

Appear when stochastics are extreme

AND price pulls back into EMAs while the EMAs are correctly postured (bullish or bearish).

Indicates a high-probability reversal.

💎 Purple Diamond Super Reversal

Appears when EMA reversal conditions are met

AND there is divergence on the fast stochastic (Stoch1).

Strongest reversal signal.

✅ Confluence Checks Built In

✔ Multi-timeframe stochastic alignment (15m, 5m, 1m)

✔ EMA posture (bullish or bearish stack)

✔ EMA pullback logic or EMA distance check

✔ VWAP reversion point consideration

✔ Divergence detection for strongest signals

✅ How to Use

Use on a 15-minute chart (optimal).

Look for Super Reversal diamonds first (highest conviction).

Confirm with price action and key levels before entry.

Combine with order flow, liquidity sweeps, or market structure for best results.

⚙ Settings

EMA Distance Threshold (%) → Default 0.05 (for Mean Reversion Dots).

Increase for fewer, stronger signals.

Decrease for more sensitivity.

📌 Best Practices

Focus on reversals during London & NY sessions.

Avoid trading against strong higher timeframe trends without extra confirmation.

Use tight stops and let winners run when the setup is strong.

💡 This tool is built to highlight only the cleanest reversal setups with layered confluence. Use it to filter noise and stay disciplined with your entries.

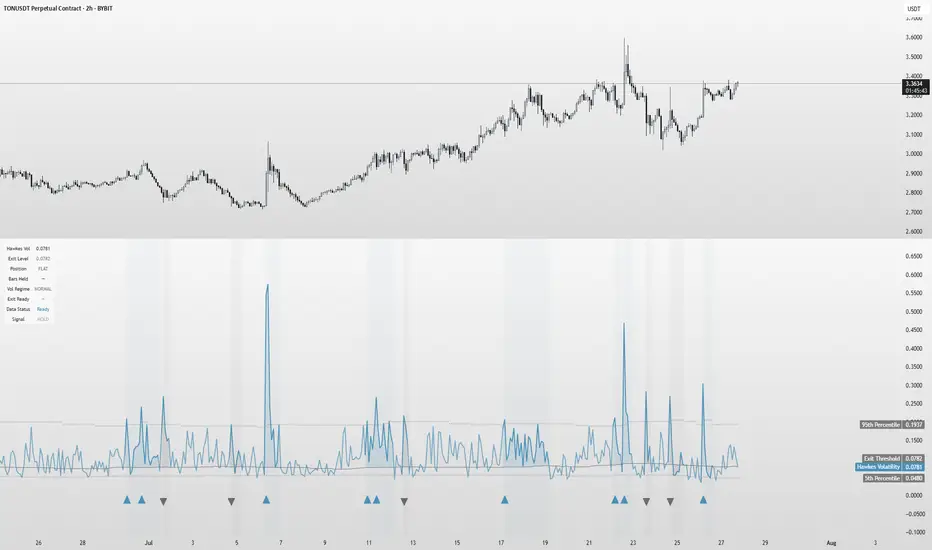

Hawkes Volatility Exit IndicatorOverview

The Hawkes Volatility Exit Indicator is a powerful tool designed to help traders capitalize on volatility breakouts and exit positions when momentum fades. Built on the Hawkes process, it models volatility clustering to identify optimal entry points after quiet periods and exit signals during volatility cooling. Designed to be helpful for swing traders and trend followers across markets like stocks, forex, and crypto.

Key Features Volatility-Based Entries: Detects breakouts when volatility spikes above the 95th percentile (adjustable) after quiet periods (below 5th percentile).

This indicator is probably better on exits than entries.

Smart Exit Signals: Triggers exits when volatility drops below a customizable threshold (default: 30th percentile) after a minimum hold period.

Hawkes Process: Uses a decay-based model (kappa) to capture volatility clustering, making it responsive to market dynamics.

Visual Clarity: Includes a volatility line, exit threshold, percentile bands, and intuitive markers (triangles for entries, X for exits).

Status Table: Displays real-time data on position (LONG/SHORT/FLAT), volatility regime (HIGH/LOW/NORMAL), bars held, and exit readiness.

Customizable Alerts: Set alerts for breakouts and exits to stay on top of trading opportunities.

How It Works Quiet Periods: Identifies low volatility (below 5th percentile) that often precede significant moves.

Breakout Entries: Signals bullish (triangle up) or bearish (triangle down) entries when volatility spikes post-quiet period.

Exit Signals: Suggests exiting when volatility cools below the exit threshold after a minimum hold (default: 3 bars).

Visuals & Table: Tracks volatility, position status, and signals via lines, shaded zones, and a detailed status table.

Settings

Hawkes Kappa (0.1): Adjusts volatility decay (lower = smoother, higher = more sensitive).

Volatility Lookback (168): Sets the period for percentile calculations.

ATR Periods (14): Normalizes volatility using Average True Range.

Breakout Threshold (95%): Volatility percentile for entries.

Exit Threshold (30%): Volatility percentile for exits.

Quiet Threshold (5%): Defines quiet periods.

Minimum Hold Bars (3): Ensures positions are held before exiting.

Alerts: Enable/disable breakout and exit alerts.

How to Use

Entries: Look for triangle markers (up for long, down for short) and confirm with the status table showing "ENTRY" and "LONG"/"SHORT."

Exits: Exit on X cross markers when the status table shows "EXIT" and "Exit Ready: YES."

Monitoring: Use the status table to track position, bars held, and volatility regime (HIGH/LOW/NORMAL).

Combine: Pair with price action, support/resistance, or other indicators for better context.

Tips : Adjust thresholds for your market: lower breakout thresholds for more signals, higher exit thresholds for earlier exits.

Test on your asset to ensure compatibility (best for markets with volatility clustering).

Use alerts to automate signal detection.

Limitations Requires sufficient data (default: 168 bars) for reliable signals. Check "Data Status" in the table.

Focuses on volatility, not price direction—combine with trend tools.

May lag slightly due to the smoothing nature of the Hawkes process.

Why Use It?