RISK MANAGEMENT TABLEThis updated Risk Management Indicator is a powerful and customizable tool designed to help traders effectively manage risk on every trade. By dynamically calculating position size, stop-loss, and take-profit levels, it enables traders to stay disciplined and follow predefined risk parameters directly on their charts.

Features:

Dynamic Stop-Loss and Take-Profit Levels:

Stop-loss is based on the Average True Range (ATR), offering a flexible way to account for

market volatility.

Take-profit levels can be customized as a percentage of the entry price, providing a clear

target for trade exits.

Position Sizing Calculation:

The indicator computes the maximum position size by considering:

Trade amount (montant_ligne).

Risk percentage per trade.

Transaction fees.

Visual Representation:

Displays stop-loss and take-profit levels on the chart as customizable lines.

Optional visibility of these lines through checkboxes in the settings panel.

Comprehensive Risk Table:

A table on the chart summarizes essential risk metrics:

Stop-loss value.

Distance from entry in percentage.

Position size (maximum suggested).

Take-profit price.

Customizable:

Adjust parameters like ATR length, smoothing type, risk percentage, transaction fees,

and take-profit percentage.

Modify the visual length of lines representing stop-loss and take-profit levels.

How It Works:

Stop-Loss Calculation:

The stop-loss level is calculated using ATR and a volatility factor (default: 2).

This ensures your stop-loss adapts to market conditions.

Take-Profit Calculation:

Take-profit is derived as a percentage increase from the entry price.

Position Size:

The optimal position size is computed as:

Position Size = Risk per Trade /ATR-based Stop Distance

The risk per trade deducts transaction fees to provide a more accurate calculation.

Visual Lines:

Risk Table:

The table displays updated stop-loss, position size, and take-profit metrics at a glance.

Settings Panel:

Length: ATR length for calculating market volatility.

Smoothing: Choose RMA, SMA, EMA, or WMA for ATR smoothing.

Trade Amount: The capital allocated to a single trade.

Risk by Trade (%): Define how much of your trade capital is at risk per trade.

Transaction Fees: Input fees to ensure realistic calculations.

Take Profit (%): Specify your desired take-profit percentage.

Show Entry Stop Loss: Toggle visibility of the stop-loss line.

Show Entry Take Profit: Toggle visibility of the take-profit line.

ניהול פורטפוליו

BTC Slayer 9000 - Relative Risk-adjusted performanceBTC Slayer 9000: Relative Risk-Adjusted Performance

Dear friends and fellow traders,

I am pleased to introduce the BTC Slayer 9000, a script designed to provide clear insights into risk-adjusted performance relative to a benchmark. Whether you're navigating the volatile world of cryptocurrencies or exploring opportunities in stocks, this tool helps you make informed decisions by comparing assets against your chosen benchmark.

What Does It Do?

This indicator is based on the Ulcer Index (UI), a metric that measures downside risk. It calculates the Ulcer Performance Index (UPI), which combines returns and downside risk, and compares it to a benchmark (like BTC/USDT, SPY500, or any trading pair).

The result is the Relative UPI (RUPI):

Positive RUPI (green area): The asset's risk-adjusted performance is better than the benchmark.

Negative RUPI (red area): The asset's risk-adjusted performance is worse than the benchmark.

Why Use It?

Risk vs. Reward: See if the extra risk of an asset is justified by its returns.

Customizable Benchmark: Compare any asset against BTC, SPY500, or another chart.

Dynamic Insights: Quickly identify outperforming assets for long positions and underperformers for potential shorts.

How to Use:

Inputs:

Adjust the lookback period to set the time frame for analysis. 720 Period is meant to represent 30 days. I like to use 168 period because I do not hold trades for long.

Choose your comparison chart (e.g., BTC/USDT, SPY500, AAPL, etc.).

Interpretation:

Green Area Above 0: The asset offers better risk-adjusted returns than the benchmark.

Red Area Below 0: The benchmark is a safer or more rewarding option.

Perfect for All Traders

Whether you:

Trade Cryptocurrencies: Compare altcoins to BTC.

Invest in Stocks: Compare individual stocks to indices like SPY500.

Evaluate Portfolio Options: Decide between assets like AAPL or TSLA.

This indicator equips you with a systematic way to evaluate "Is the extra risk worth it?".

The script was compiled in Collaboration with ChatGPT

Average Trading Volume per Minute & Suitable Position SizeDescription:

This indicator calculates an average trading volume per minute for the specified lookback period (default 377 bars). It then estimates a suitable position size in USD (or contracts on specific exchanges) by multiplying the average volume by a user-defined percentage (default 8%). The script discards extreme data points (top and bottom 20%) before finding the median, so it provides a more robust measure of typical volume.

How It Works:

1. Each bar’s volume is converted to a USD-based figure, either by taking volume directly (if the exchange quotes in USD) or multiplying volume by the midpoint price.

2. Values are stored in an array, which is then sorted to remove the most extreme 40% (20% from each tail). The remaining 60% is used to calculate a median.

3. You enter a position size percentage (e.g. 8%), and the script multiplies the median volume-per-minute by this percentage to get your recommended position size.

4. For certain exchanges like BitMEX/Deribit, the script adapts how it treats volume (in quotes vs. base), so it can display the final position size properly (USD or contracts).

5. The script displays the result in a small table on the chart, showing the recommended position size in USD (or, for some perpetual contracts, in contract units). If no valid data is available, it indicates “Data Invalid.”

Usage Tips:

• The default Position Size Percentage is 8%. You can adjust it higher for more aggressive trading or lower for smaller exposure.

• The default lookback (Average Calculation Period) is 377 bars. Experiment with different values (e.g. 200 or 500) to capture more or fewer historical bars.

• On certain exchanges and symbols (e.g. BitMEX or Deribit’s “.P” pairs), the script automatically switches how it calculates volume (USD vs. coin-based).

• If you see “Data Invalid,” it likely means the current symbol or timeframe lacks sufficient volume info, or you’re running it on a symbol like BTC.D.

Why This Helps:

• Many traders size positions by guesswork or a fixed fraction of their account. This script instead ties position size to actual average trading volume, ensuring your position is neither too large (risk of poor fills) nor too small (wasting leverage potential).

• Removing top/bottom outliers and using the median aims to give a stable volume measure—less influenced by sudden spikes or extremely quiet bars.

Feel free to tweak the inputs and experiment with different timeframes or pairs. By aligning your position size with typical market liquidity, you can potentially improve overall trade execution and manage risk more effectively.

Lot size calculator for futuresEasily and quickly calculate lot sizes with this unique indicator for futures trading. Whether you're dealing with full contracts or micro contracts, this tool simplifies the process by allowing you to input your account balance, risk percentage, and stop loss in pips. The indicator then automatically calculates the optimal number of contracts to trade based on your risk parameters. Designed for both novice and experienced traders, it ensures precise risk management and enhances your trading strategy. Experience the ease and efficiency of lot size calculation like never before!

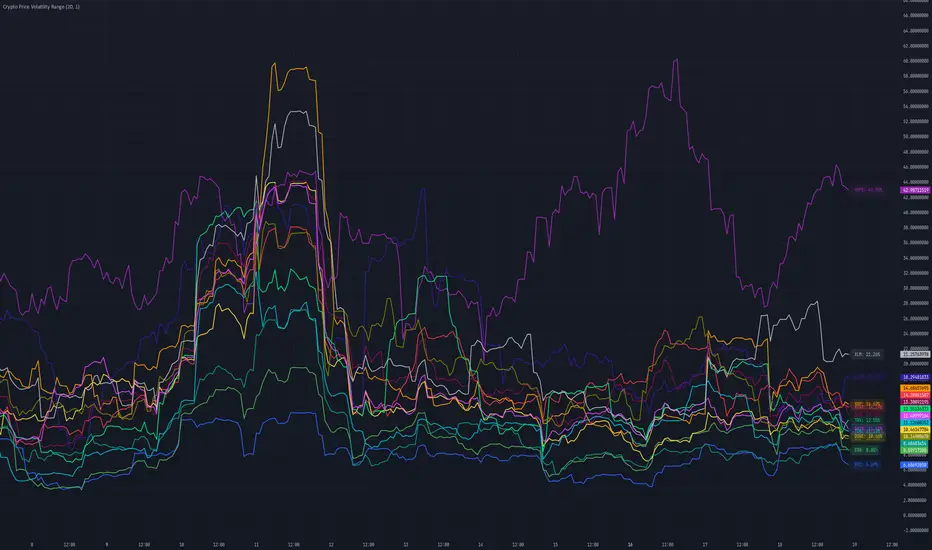

Crypto Price Volatility Range# Cryptocurrency Price Volatility Range Indicator

This TradingView indicator is a visualization tool for tracking historical volatility across multiple major cryptocurrencies.

## Features

- Real-time volatility tracking for 14 major cryptocurrencies

- Customizable period and standard deviation multiplier

- Individual color coding for each currency pair

- Optional labels showing current volatility values in percentage

## Supported Cryptocurrencies

- Bitcoin (BTC)

- Ethereum (ETH)

- Avalanche (AVAX)

- Dogecoin (DOGE)

- Hype (HYPE)

- Ripple (XRP)

- Binance Coin (BNB)

- Cardano (ADA)

- Tron (TRX)

- Chainlink (LINK)

- Shiba Inu (SHIB)

- Toncoin (TON)

- Sui (SUI)

- Stellar (XLM)

## Settings

- **Period**: Timeframe for volatility calculation (default: 20)

- **Standard Deviation Multiplier**: Multiplier for standard deviation (default: 1.0)

- **Show Labels**: Toggle label display on/off

## Calculation Method

The indicator calculates volatility using the following method:

1. Calculate daily logarithmic returns

2. Compute standard deviation over the specified period

3. Annualize (multiply by √252)

4. Convert to percentage (×100)

## Usage

1. Add the indicator to your TradingView chart

2. Adjust parameters as needed

3. Monitor volatility lines for each cryptocurrency

4. Enable labels to see precise current volatility values

## Notes

- This indicator displays in a separate window, not as an overlay

- Volatility values are annualized

- Data for each currency pair is sourced from USD pairs

Highest Volume FuturesScript tracks the volume of futures contracts which are not expired for the current and next year. Provides a label at the real-time bar and when a different contract has higher volume in the last bar of the timeframe input as long as it is different from the current ticker. It should display on continuous and lower volume contract charts.

Intended to be used with a higher timeframe input.

Currently supports ES, MES, NQ, MNQ, RTY, M2K, YM, MYM, BTC, MBT, CL, MCL, GC, MGC, E7 and J7. If you'd like to add your own, then include the syminfo.root of your ticker and the appropriate month codes for that contract in the validMonthCodes switch list.

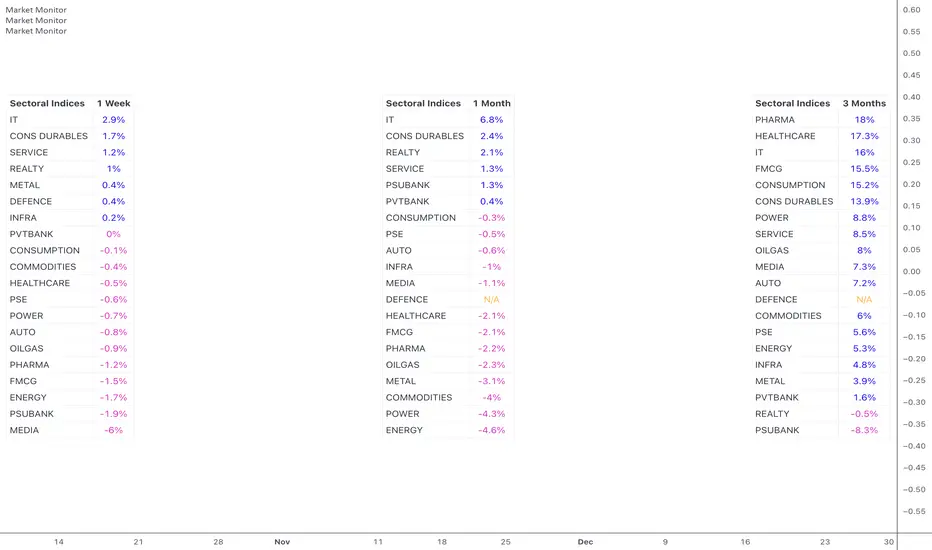

Market MonitorOverview

The Market Monitor Indicator provides a customisable view of dynamic percentage changes across selected indices or sectors, calculated by comparing current and previous closing prices over the chosen timeframe.

Key Features

Choose up to 20 predefined indices or your own selected indices/stocks.

Use checkboxes to show or hide individual entries.

Monitor returns over daily, weekly, monthly, quarterly, half-yearly, or yearly timeframes

Sort by returns (descending) to quickly identify top-performing indices or alphabetically for an organised and systematic review.

Customisation

Switch between Light Mode (Blue or Green themes) and Dark Mode for visual clarity.

Adjust the table’s size, position, and location.

Customise the table title to your own choice e.g. Sectoral, Broad, Portfolio etc.

Use Cases

Use multiple instances of the script with varying timeframes to study sectoral rotation and trends.

Customise the stocks to see your portfolio returns for the day or over the past week, or longer.

IPO Lifecycle Sell Strategy [JARUTIR]IPO Lifecycle Sell Strategy with Dynamic Buy Date and Multiple Sell Rules

This custom TradingView script is designed for traders looking to capitalize on dynamic strategies for IPOs and growth stocks, by implementing several sell rules based on price action and technical indicators. It provides a set of sell rules that are applied dynamically depending on the stock's lifecycle and price action, allowing users to lock in profits and minimize drawdowns based on key technical thresholds.

The four sell strategies incorporated into this script are inspired by the book "The Lifecycle Trade", a resource that focuses on capturing profits while managing risk in different phases of a stock's lifecycle, from IPO to high-growth stages.

Key Features:

Buy Price and Buy Date: You can either manually input your buy price and date or let the script automatically detect the buy date based on the specified buy price.

Multiple Sell Strategies: Choose from 4 predefined sell strategies:

Ascender Rule : Captures strong momentum from IPO stocks by selling portions at specific price levels or technical conditions.

Midterm Rule : Focuses on holding for longer periods, with defensive sell signals triggered when the stock deviates significantly from peak price or key moving averages.

40 Week Rule : Designed for long-term holds, this rule triggers a sell when the stock closes below the 40-week moving average.

Everest Rule : Aggressive strategy for selling into strength based on parabolic moves or gap downs, ideal for high momentum stocks.

Interactive Features:

Horizontal Green Line showing the buy price level from the buy date.

Visual Sell Signals appear only after the buy date to ensure that your analysis is relevant to the stock lifecycle.

Customizable settings, allowing you to choose your preferred sell rule strategy and automate buy date detection.

This script is perfect for traders using a strategic, systematic approach to IPOs and high-growth stocks, whether you're looking for quick exits during momentum phases or holding for longer-term growth.

Usage:

Input your Buy Price and Buy Date, or allow the script to automate the buy date detection.

Select a Sell Rule strategy based on your risk profile and trading style.

View visual signals for selling when specific conditions are met.

Frequently Asked Questions (FAQs):

Q1: How do I input my Buy Price and Buy Date?

The script allows you to either manually input the Buy Price and Buy Date or use the automated detection. If you choose automated detection, the script will automatically assign the buy date when the price crosses above your set Buy Price.

Q2: What is the purpose of the "Sell Rules"?

The script offers four sell strategies to help manage different types of stocks in varying phases of their lifecycle:

Ascender Rule: Targets IPO stocks showing positive momentum.

Midterm Rule: A defensive strategy for stocks in a steady uptrend.

40 Week Rule: Long-term hold strategy designed to ride stocks through extended growth.

Everest Rule: Aggressive strategy to capture profits during parabolic price moves.

Q3: What is the significance of the Green Line at Buy Price?

The Green Line represents your entry point (Buy Price) on the chart. It will appear from the buy date onwards, helping you track the performance of your stock relative to your entry.

Q4: Can I customize the Sell Strategy?

Yes! You can choose from the available Sell Rules (Ascender Rule, Midterm Rule, 40 Week Rule, Everest Rule) via an input option in the script. Each strategy has its own unique triggers based on price action, moving averages, and time-based conditions.

Q5: Does this script work for stocks and crypto?

Yes, this script is designed for both stocks and cryptocurrencies. It works on any asset where price data and timeframes are available.

Q6: How do the Weekly Moving Averages (WSMA) work in this strategy?

The script uses weekly moving averages (WSMA) to track longer-term trends. These are essential for some of the sell rules, such as the Midterm Rule and 40 Week Rule, which rely on the stock's movement relative to the 40-week moving average.

Q7: Will the script plot a Sell Signal immediately after the Buy Date?

No, sell signals will only be plotted after the Buy Date. This ensures that the sell strategy is relevant to your actual holding period and avoids premature triggers.

Q8: How do I interpret the Sell Signal?

The script will plot a Red Sell Signal above the bar when the sell conditions are met, based on the selected strategy. This indicates that it may be a good time to exit the position according to your chosen rule.

Q9: Can I use this strategy on different timeframes?

Yes, you can apply the script to any timeframe. However, some sell strategies, like the Midterm Rule and 40 Week Rule, are designed to work best with weekly data, so it's recommended to use these strategies with longer timeframes.

Q10: Does this script have any alerts?

Yes! The script supports alert conditions that will notify you when the sell conditions are met according to your selected rule. You can set up alerts to stay informed without needing to watch the chart constantly.

Q11: What if I want to disable some of the sell rules?

You can select your preferred sell rule using the "Select Sell Rule" dropdown. If you don’t want to use a particular rule, simply choose a different strategy or leave it inactive.

------------------------------

Disclaimer:

This strategy is intended for educational purposes only. It should not be considered financial advice. Always perform your own research and consult with a professional before making any trading decisions. Trading involves significant risk, and you should never trade with money you cannot afford to lose.

Employee Portfolio Generator [By MUQWISHI]▋ INTRODUCTION :

The “Employee Portfolio Generator” simplifies the process of building a long-term investment portfolio tailored for employees seeking to build wealth through investments rather than traditional bank savings. The tool empowers employees to set up recurring deposits at customizable intervals, enabling to make additional purchases in a list of preferred holdings, with the ability to define the purchasing investment weight for each security. The tool serves as a comprehensive solution for tracking portfolio performance, conducting research, and analyzing specific aspects of portfolio investments. The output includes an index value, a table of holdings, and chart plots, providing a deeper understanding of the portfolio's historical movements.

_______________________

▋ OVERVIEW:

● Scenario (The chart above can be taken as an example) :

Let say, in 2010, a newly employed individual committed to saving $1,000 each month. Rather than relying on a traditional savings account, chose to invest the majority of monthly savings in stable well-established stocks. Allocating 30% of monthly saving to AMEX:SPY and another 30% to NASDAQ:QQQ , recognizing these as reliable options for steady growth. Additionally, there was an admired toward innovative business models of NASDAQ:AAPL , NASDAQ:MSFT , NASDAQ:AMZN , and NASDAQ:EBAY , leading to invest 10% in each of those companies. By the end of 2024, after 15 years, the total monthly deposits amounted to $179,000, which would have been the result of traditional saving alone. However, by sticking into long term invest, the value of the portfolio assets grew, reaching nearly $900,000.

_______________________

▋ OUTPUTS:

The table can be displayed in three formats:

1. Portfolio Index Title: displays the index name at the top, and at the bottom, it shows the index value, along with the chart timeframe, e.g., daily change in points and percentage.

2. Specifications: displays the essential information on portfolio performance, including the investment date range, total deposits, free cash, returns, and assets.

3. Holdings: a list of the holding securities inside a table that contains the ticker, last price, entry price, return percentage of the portfolio's total deposits, and latest weighted percentage of the portfolio. Additionally, a tooltip appears when the user passes the cursor over a ticker's cell, showing brief information about the company, such as the company's name, exchange market, country, sector, and industry.

4. Indication of New Deposit: An indication of a new deposit added to the portfolio for additional purchasing.

5. Chart: The portfolio's historical movements can be visualized in a plot, displayed as a bar chart, candlestick chart, or line chart, depending on the preferred format, as shown below.

_______________________

▋ INDICATOR SETTINGS:

Section(1): Table Settings

(1) Naming the index.

(2) Table location on the chart and cell size.

(3) Sorting Holdings Table. By securities’ {Return(%) Portfolio, Weight(%) Portfolio, or Ticker Alphabetical} order.

(4) Choose the type of index: {Assets, Return, or Return (%)}, and the plot type for the portfolio index: {Candle, Bar, or Line}.

(5) Positive/Negative colors.

(6) Table Colors (Title, Cell, and Text).

(7) To show/hide any of selected indicator’s components.

Section(2): Recurring Deposit Settings

(1) From DateTime of starting the investment.

(2) To DateTime of ending the investment

(3) The amount of recurring deposit into portfolio and currency.

(4) The frequency of recurring deposits into the portfolio {Weekly, 2-Weeks, Monthly, Quarterly, Yearly}

(5) The Depositing Model:

● Fixed: The amount for recurring deposits remains constant throughout the entire investment period.

● Increased %: The recurring deposit amount increases at the selected frequency and percentage throughout the entire investment period.

(5B) If the user selects “ Depositing Model: Increased % ”, specify the growth model (linear or exponential) and define the rate of increase.

Section(3): Portfolio Holdings

(1) Enable a ticker in the investment portfolio.

(2) The selected deposit frequency weight for a ticker. For example, if the monthly deposit is $1,000 and the selected weight for XYZ stock is 30%, $300 will be used to purchase shares of XYZ stock.

(3) Select up to 6 tickers that the investor is interested in for long-term investment.

Please let me know if you have any questions

Ticker Tape with Multiple Inputs# Ticker Tape

A customizable multi-symbol price tracker that displays real-time price information in a scrolling ticker format, similar to financial news tickers.

This indicator is inspired from Tradingciew's default tickertape indicator with changes in the way inputs are given.

### Overview

This indicator allows you to monitor up to 15 different symbols simultaneously across any supported exchanges on TradingView. It displays essential price information including current price, price change, and percentage change in an easy-to-read format at the bottom of your chart.

### Features

• Monitor up to 15 different symbols simultaneously

• Support for any exchange available on TradingView

• Real-time price updates

• Color-coded price changes (green for increase, red for decrease)

• Smooth scrolling animation (can be disabled)

• Customizable scroll speed and position offset

### Input Parameters

#### Ticker Tape Controls

• Running: Enable/disable the scrolling animation

• Offset: Adjust the starting position of the ticker tape

#### Symbol Settings

• Exchange (1-15): Enter the exchange name (e.g., NSE, BINANCE, NYSE)

• Symbol (1-15): Enter the symbol name (e.g., BANKNIFTY, RELIANCE, BTCUSDT)

### Display Format

For each symbol, the ticker shows:

1. Symbol Name

2. Current Price

3. Price Change (Absolute and Percentage)

### Example Usage

Input Settings:

Exchange 1: NSE

Symbol 1: BANKNIFTY

Exchange 2: NSE

Symbol 2: RELIANCE

The ticker tape will display:

`NIFTY BANK 46750.00 +350.45 (0.75%) | RELIANCE 2456.85 -12.40 (-0.50%) |`

### Use Cases

1. Multi-Market Monitoring: Track different markets simultaneously without switching between charts

2. Portfolio Tracking: Monitor all your positions in real-time

### Tips for Best Use

1. Group related symbols together for easier monitoring

2. Use the offset parameter to position important symbols in your preferred viewing area

3. Disable scrolling if you prefer a static display

4. Leave exchange field empty for default exchange symbols

### Notes

• Price updates occur in real-time during market hours

• Color coding helps quickly identify price direction

• The indicator adapts to any chart timeframe

• Empty input pairs are automatically skipped

### Performance Considerations

The indicator is optimized for efficiency, but monitoring too many high-frequency symbols might impact chart performance. It's recommended to use only the symbols you actively need to monitor.

Version: 2.0 Stock_Cloud

Last Updated: December 2024

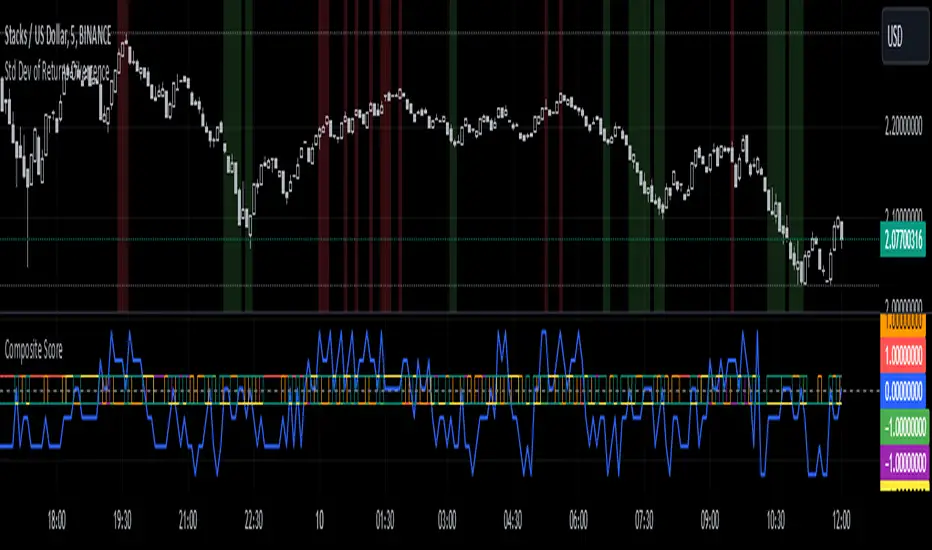

Standard Deviation of Returns: DivergencePurpose:

The "Standard Deviation of Returns: Divergence" indicator is designed to help traders identify potential trend reversals or continuation signals by analyzing divergences between price action and the statistical volatility of returns. Divergences can signal weakening momentum in the prevailing trend, offering insight into potential buying or selling opportunities.

Key Components

1. Returns Calculation:

* The indicator uses logarithmic returns (log(close / close )) to measure relative price changes in a normalized manner.

* Log returns are more effective than simple price differences when analyzing data across varying price levels, as they account for percentage-based changes.

2. Standard Deviation of Returns:

* The script computes the standard deviation of returns over a user-defined lookback period (ta.stdev(returns, lookback)).

* Standard deviation measures the dispersion of returns around their average, effectively quantifying market volatility.

* A higher standard deviation indicates increased volatility, while lower standard deviation reflects a calmer market.

3. Price Action:

* Detects higher highs (new peaks in price) and lower lows (new troughs in price) over the lookback period.

* Price trends are compared to the behavior of the standard deviation.

4. Divergence Detection:

A divergence occurs when price action (higher highs or lower lows) is not confirmed by a corresponding movement in standard deviation:

Bullish Divergence: Price makes a lower low, but the standard deviation does not, signaling potential upward momentum.

Bearish Divergence: Price makes a higher high, but the standard deviation does not, signaling potential downward momentum.

5. Visual Cues:

The script highlights divergence regions directly on the chart:

Green Background: Indicates a bullish divergence (potential buy signal).

Red Background: Indicates a bearish divergence (potential sell signal).

How It Works

Inputs:

* The user specifies the lookback period (lookback) for calculating the standard deviation and detecting divergences.

Calculation:

* Each bar’s returns are computed and used to calculate the standard deviation over the specified lookback period.

* The indicator evaluates price highs/lows and compares these with the highest and lowest values of the standard deviation within the same lookback period.

Highlight of Divergences:

When divergences are detected:

Bullish Divergence: The background of the chart is shaded green.

Bearish Divergence: The background of the chart is shaded red.

Trading Application

Bullish Divergence:

* Occurs when the market is oversold, or downward momentum is weakening.

* Suggests a potential reversal to an uptrend, signaling a buying opportunity.

Bearish Divergence:

* Occurs when the market is overbought, or upward momentum is weakening.

* Suggests a potential reversal to a downtrend, signaling a selling opportunity.

Contextual Use:

* Use this indicator in conjunction with other technical tools like RSI, MACD, or moving averages to confirm signals.

* Effective in volatile or ranging markets to help anticipate shifts in momentum.

Summary

The "Standard Deviation of Returns: Divergence" indicator is a robust tool for spotting divergences that can signal weakening market trends. It combines statistical volatility with price action analysis to highlight key areas of potential reversals. By integrating this tool into your trading strategy, you can gain additional confirmation for entries or exits while keeping a close watch on momentum shifts.

Disclaimer: This is not a financial advise; please consult your financial advisor for personalized advice.

US Recessions OverlayThe US Recessions Overlay indicator highlights the periods of US economic recessions directly on your TradingView chart. Using historical data from the Great Depression to the present, it provides a visual representation of recessions as transparent red backgrounds. This can help traders and analysts correlate market movements with historical economic downturns.

Features:

- Displays US recessions since the Great Depression (1929) as shaded areas.

- Automatically adjusts the background shading to match the date ranges of historical recessions.

- A simple and effective way to observe market behavior during recessionary periods.

- Fully customizable to include new recession periods or modify transparency levels.

How to Use:

Apply the indicator to any chart. Recession periods will appear as red-shaded backgrounds, providing a clear visual cue for market behavior during those times.

Use Case:

Ideal for traders, economists, and market historians who wish to study the impact of recessions on financial markets.

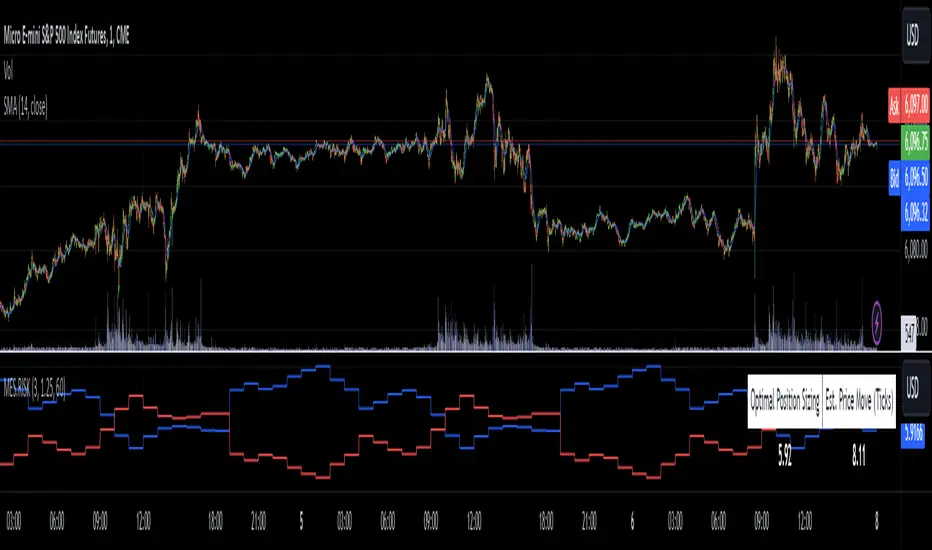

MES Position Sizing EstimatorDescription and Use:

Here is an indicator which aims to help all Micro-ES futures traders who struggle with risk management! I created this indicator designed as a general guideline to help short term traders (designed for 1 minute candles) determine how many contracts to trade on the MES for their desired profit target.

To use the indicator, simply go to MES on the 1 minute timeframe, apply the indicator, and enter your Holding Period (how long you want to have your position open for), Value Per Tick

(usually 1.25 for MES since one point is $5) and your target PnL for the trade in the inputs tab.

It will then show in a table the recommended position sizing, as well as the estimated price change for your holding period. Additionally, there are two plotted lines also showing the position sizing and estimated price change historically.

How the indicator works

On the technical level, I made calculations for this indicator using Python. I downloaded 82 days of 1 minute OHLC data from TradingView, and then ran regression (log-transformed linear regression specifically) to calculate how the average price change in MES futures scales with the amount of time a position is held for, and then ran these regressions for every hour of the day. I then copied the equations from those regressions into Pinescript, and used the assumption that:

position size = target PnL / (estimated price change for time * tick value)

Therefore, Choosing the number of contracts to trade position sizing for Micro E-mini S&P 500 Futures (MES) based on time of day, holding period, and tick value. This tool leverages historical volatility patterns and log-transformed linear regression models to provide precise recommendations tailored to your trading strategy.

If you want to check out how the regression code worked in python, it is all open source and available on my Github repository for it .

Notes:

The script assumes a log-normal distribution of price movements and is intended as an educational tool to aid in risk management.

It is not a standalone trading system and should be used in conjunction with other trading strategies and risk assessments.

Past performance is not indicative of future results, and traders should exercise caution and adjust their strategies based on personal risk tolerance.

This script is open-source and available for use and modification by the TradingView community. It aims to provide a valuable resource for traders seeking to enhance their risk management practices through data-driven insights.

DCA Valuation & Unrealized GainsThis Pine Script for TradingView calculates and visualizes the relationship between a Dollar Cost Average (DCA) price and the All-Time High (ATH) price for over 50 different cryptocurrencies. Here's what it does:

1. Inputs for DCA Prices:

- Users can manually input DCA prices for specific cryptocurrencies (e.g., BTC, ETH, BNB).

2. Dynamic ATH Calculation:

- Dynamically calculates the ATH price for the current asset using the highest price in the chart's loaded data and persists this value across bars.

3. Percentage Change from DCA to ATH:

- Computes the percentage gain from the DCA price to the ATH price.

4. Visualizations:

- Draws a line at the DCA price and the ATH price, both extended to the right.

- Adds an arrow pointing from the DCA price to the ATH, offset by 10 bars into the future.

- Displays labels for:

- The percentage gain from DCA to ATH.

- "No DCA Configured" if no valid DCA price is set for the asset.

5. Color Coding:

- Labels and arrows are color-coded to indicate positive or negative percentage changes:

- Green for gains.

- Red for losses.

6. Adaptability:

- The script dynamically adjusts to the current asset based on its ticker and uses the corresponding DCA price.

This functionality provides traders with clear insights into their investment's performance relative to its ATH, aiding in decision-making.

-----

To add a new asset to the script:

1. Define the DCA Input: Add a new input for the asset's DCA price using the `input.float` function. For example:

dcaPriceNEW = input.float(title="NEW DCA Price", defval=0.1, tooltip="Set the DCA price for NEW")

2. Add the Asset Logic: Include a conditional check for the new asset in the ticker matching logic:

if str.contains(currentAsset, "NEW") and dcaPriceNEW != 0

dcaPrice := dcaPriceNEW

Where NEW is the ticker symbol of the asset you're adding.

NOTE: SOLO had to be put before SOL because otherwise the indicator was pulling the DCA price from SOL even on the SOLO chart. If you have a similar issue, try that fix.

Adding an asset requires only these two changes. Once done, the script dynamically incorporates the new asset into its calculations and visualizations.

IU VaR (Value at Risk) Historical MethodThis Pine Script indicator calculates the **Value at Risk (VaR)** using the **Historical Method** to help traders understand potential losses during a given period( Chart Timeframe) with a specific level of confidence.

What is Value at Risk (VaR) ?

Value at Risk (VaR) is a measure used in finance to estimate the potential loss in value of an asset, portfolio, or investment over a specific time period, given normal market conditions, and at a certain confidence level.

Example:

Suppose you invest ₹1,00,000 in stocks. A VaR of 5% at a 95% confidence level means:

- There is a **95% chance** that you won’t lose more than **₹5,000** in a day.

- Conversely, there is a **5% chance** that your loss could exceed ₹5,000 in a day.

VaR is a helpful tool for understanding risk and making informed investment decisions!

How It Works:

1. The indicator calculates the percentage difference between consecutive bars.

2. The differences are sorted, and the VaR is determined based on the assurance level you specify.

3. A label displays the VaR value on the chart, indicating the potential maximum loss with the selected assurance level within one period eg - ( 1h, 4h , 1D, 1W, 1M etc as per your chart timeframe )

Key Features:

- Customizable Assurance Level:

Set the confidence level (e.g., 95%) to determine the probability of loss.

-Historical Approach:

Uses the past percentage changes in price to calculate the risk.

-Clear Insights:

Displays the calculated VaR value on the chart with an informative tooltip explaining the risk.

Use this tool to better understand your market exposure and manage risk!

Adaptive ATR Trailing Stops█ Introduction

This script is based on the average true range (ATR) and has been improved with the HHV or LLV. The script supports the trader to have his stoploss trailed. In this case, the stoploss is dynamic and can be adjusted with each candleclose.

█ What Does This Indicator Do?

The ATR SL Trailing Indicator helps you dynamically adjust your stop-loss levels based on market movements. It uses market volatility to calculate trailing stop-loss levels, ensuring you can secure profits or minimize losses. The indicator creates two lines:

A green/red line for long positions (when you’re betting on prices going up).

A green/red line for short positions (when you’re betting on prices going down).

█ Key Concepts: How Does the Indicator Work?

The Average True Range (ATR) measures market volatility, showing how much the price moves over a specific period.

A high ATR indicates a volatile market (large price swings), while a low ATR indicates a quiet market (smaller price changes).

Why is ATR important? ATR helps dynamically adjust the distance between your stop-loss and the current price. In volatile markets, the stop-loss is placed further away to avoid being triggered by short-term fluctuations. In quieter markets, the stop-loss is set closer to the price.

The HHV is the highest price over a specific period. For long positions, the indicator uses the highest price minus an ATR-based value to determine the stop-loss level.

Why is HHV important? HHV ensures the stop-loss for long positions only moves up when the price reaches new highs. Once the price starts falling, the stop-loss remains unchanged to lock in profits or minimize losses.

The LLV is the lowest price over a specific period. For short positions, the indicator uses the lowest price plus an ATR-based value to determine the stop-loss level.

Why is LLV important? LLV ensures the stop-loss for short positions only moves down when the price reaches new lows. Once the price starts rising, the stop-loss remains unchanged to lock in profits or minimize losses.

█ How Does the Indicator Work?

For Long Positions:

The indicator sets the stop-loss below the current price, based on:

Market volatility (ATR).

The highest price over a specific period (HHV).

The line turns green when the current price is above the stop-loss.

The line turns red when the price drops below the stop-loss, signaling you may need to exit the trade.

For Short Positions:

The indicator sets the stop-loss above the current price, based on:

*Market volatility (ATR).

*The lowest price over a specific period (LLV).

*The line turns green when the current price is below the stop-loss.

*The line turns red when the price moves above the stop-loss, signaling you may need to exit the trade.

█ Advantages of the ATR SL Trailing Indicator

*Dynamic and adaptive: Automatically adjusts stop-loss levels based on market volatility.

*Visual clarity: Green and red lines clearly indicate whether your position is safe or at risk.

*Effective risk management: Helps you lock in profits and minimize losses without the need for constant manual adjustments.

█ When Should You Use This Indicator?

*If you practice trend-based trading and want your stop-losses to automatically adapt to market movements.

*In volatile markets, to avoid being stopped out by short-term fluctuations.

*When you want to implement efficient risk management without manually adjusting your positions.

█ Inputs

The user can set the indicator for both longs and shorts. This is particularly important because the calculation is different. The HHV is used for longs and the LLV for shorts. The user can therefore set the period/length for the ATR on the one hand and the HHV/LLV on the other. He also has a multiplier, which can also be customized. The multiplier multiplies the price change of each individual candle.

█ Color Change

If the SL is trailed and the price breaks a line, the color changes. In this case, it would have executed the SL on an open trade.

ETF-Benchmark AnalyzerHave you ever wondered which ETF performs the best? Which one is the most volatile, or which one has the smallest drawdown?

This Pine Script™ "ETF-Benchmark Analyzer" compares the performance of an ETF (such as SPY, the S&P 500 ETF) against a benchmark, which can also be adjusted by the user. It provides several key financial metrics, such as:

Performance (%): Displays the total return over a specified lookback period (e.g., 1 year). It compares the performance of the ETF against the benchmark and shows the difference.

Alpha (%): Measures the excess return of the ETF over the expected return, which is calculated using the benchmark’s return. Positive alpha indicates that the ETF has outperformed the benchmark, while negative alpha suggests underperformance. This metric is important because it isolates performance that cannot be explained by exposure to the benchmark's movements.

Sharpe Ratio: A risk-adjusted measure of return. It is calculated by dividing the excess return of the ETF (above the risk-free rate) by its standard deviation (volatility). A higher Sharpe ratio indicates better risk-adjusted returns. The Sharpe ratio is calculated for both the ETF and the benchmark, and their difference is displayed as well.

Drawdown: The percentage decrease from the highest price to the lowest price over the lookback period. This is a critical measure of risk, as it shows the largest potential loss an investor might face during a specific period.

Beta: Measures the ETF’s sensitivity to movements in the benchmark. A beta of 1 means the ETF moves in line with the benchmark; greater than 1 means it is more volatile, while less than 1 means it is less volatile.

These metrics provide a holistic view of the ETF’s performance compared to the benchmark, allowing traders to assess the risk and return profile more effectively.

Scientific Sources

Sharpe Ratio: Sharpe, W. F. (1994). The Sharpe Ratio. Journal of Portfolio Management, 21(1), 49-58. This paper defines and develops the Sharpe ratio as a measure of risk-adjusted return.

Alpha and Beta: Jensen, M. C. (1968). The Performance of Mutual Funds in the Period 1945–1964. The Journal of Finance, 23(2), 389-416. This paper discusses the concepts of alpha and beta in the context of mutual fund performance.

Correlation Coefficient [Giang]### **Introduction to the "Correlation Coefficient" Indicator**

#### **Idea behind the Indicator**

The "Correlation Coefficient" indicator was developed to analyze the linear relationship between Bitcoin (**BTCUSD**) and other important economic indices or financial assets, such as:

- **SPX** (S&P 500 Index): Represents the U.S. stock market.

- **DXY** (Dollar Index): Reflects the strength of the USD against major currencies.

- **SPY** (ETF representing the S&P 500): A popular trading instrument.

- **GOLD** (Gold price): A traditional safe-haven asset.

The correlation between these assets can help traders understand how Bitcoin reacts to market movements of traditional financial instruments, providing opportunities for more effective trading decisions.

Additionally, the indicator allows users to **customize asset symbols for comparison**, not limited to the default indices (SPX, DXY, SPY, GOLD). This flexibility enables traders to tailor their analysis to specific goals and portfolios.

---

#### **Significance and Use of Correlation in Trading**

**Correlation** is a measure of the linear relationship between two data series. In the context of this indicator:

- **The correlation coefficient ranges from -1 to 1**:

- **1**: Perfect positive relationship (both increase or decrease together).

- **0**: No linear relationship.

- **-1**: Perfect negative relationship (one increases while the other decreases).

- **Use in trading**:

- Identify **strong relationships or unusual divergences** between Bitcoin and other assets.

- Help determine **market sentiment**: For example, if Bitcoin has a negative correlation with DXY, traders might expect Bitcoin to rise when the USD weakens.

- Provide a foundation for hedging strategies or investments based on inter-asset relationships.

---

#### **Components of the Indicator**

The "Correlation Coefficient" indicator consists of the following key components:

1. **Main Data (BTCUSD)**:

- The closing price of Bitcoin is used as the central asset for calculations.

2. **Comparison Data**:

- Users can select different asset symbols for comparison. By default, the indicator supports:

- **SPX**: Stock market index.

- **DXY**: Dollar Index.

- **SPY**: Popular ETF.

- **GOLD**: Gold price.

3. **Correlation Coefficients**:

- Calculated between BTC and each comparison index, based on a Weighted Moving Average (WMA) over a user-defined period.

4. **Graphical Representation**:

- Displays individual correlation coefficients with each comparison index, making it easier for traders to track and analyze.

---

#### **How to Analyze and Use the Indicator**

**1. Identify Key Correlations:**

- Observe the correlation lines between BTC and the indices to determine positive or negative relationships.

- Example:

- If the **Correlation Coefficient (BTC-DXY)** sharply declines to -1, this indicates that when USD strengthens, Bitcoin tends to weaken.

**2. Analyze the Strength of Correlations:**

- **Strong Correlations**: If the coefficient is close to 1 or -1, the relationship between the two assets is very clear.

- **Weak Correlations**: If the coefficient is near 0, Bitcoin may be influenced by other factors outside the compared index.

**3. Develop Trading Strategies:**

- Use correlations to predict Bitcoin's price movements:

- If BTC has an inverse relationship with **DXY**, traders might consider selling BTC when the USD strengthens.

- If BTC and **SPX** are strongly correlated, traders can monitor the stock market to predict Bitcoin's trend.

**4. Evaluate Changes Over Time:**

- Use different timeframes (daily, weekly) to track the correlation's fluctuations.

- Look for unusual signals, such as a breakdown or shift from positive to negative relationships.

---

#### **Conclusion**

The "Correlation Coefficient" indicator is a powerful tool that helps traders analyze the relationship between Bitcoin and major financial indices. The ability to customize asset symbols for comparison makes the indicator flexible and suitable for various trading strategies. When used correctly, this indicator not only provides insights into market sentiment but also supports the development of intelligent trading strategies and optimized profits.

Volatility and Tick Size DataThis indicator, titled "Tick Information & Standard Deviation Table," provides detailed insights into market microstructure, including tick size, point value, and standard deviation values calculated based on the True Range. It helps visualize essential trading parameters that influence transaction costs, risk management, and portfolio performance, including volatility measures that can guide investment strategies.

Why These Data Points Are Important for Portfolio Management

Tick Size and Point Value:

Tick size refers to the smallest possible price movement in a given asset. It defines the granularity of the price changes, affecting how precise the market price can be at any moment. Point value reflects the monetary value of a single price movement (one tick). These two data points are essential for understanding transaction costs and for evaluating how much capital is at risk per price movement. Smaller tick sizes may lead to more efficient pricing in high-frequency trading strategies (Hasbrouck, 2009).

Reference: Hasbrouck, J. (2009). Empirical Market Microstructure. Foundations and Trends® in Finance, 3(4), 169-272.

Standard Deviations and Volatility:

Standard deviation measures the variability or volatility of an asset's price over a set period. This data point is critical for portfolio management, as it helps to quantify risk and predict potential price movements. True Range and its standard deviations provide a more comprehensive measure of market volatility than just price fluctuations, as they include gaps and extreme price changes. Investors use volatility data to assess the potential risk and adjust portfolio allocations accordingly (Ang, 2006).

Reference: Ang, A. (2006). Asset Management: A Systematic Approach to Factor Investing. Oxford University Press.

Risk Management:

The ability to quantify risk through metrics like the 1st, 2nd, and 3rd standard deviations of the true range is essential for implementing risk controls within a portfolio. By incorporating volatility data, portfolio managers can adjust their strategies for different market conditions, potentially reducing exposure to high-risk environments. These volatility measures help in setting stop-loss levels, optimizing position sizes, and managing the portfolio’s overall risk-return profile (Black & Scholes, 1973).

Reference: Black, F., & Scholes, M. (1973). The Pricing of Options and Corporate Liabilities. Journal of Political Economy, 81(3), 637-654.

Portfolio Diversification and Hedging:

Understanding asset volatility and transaction costs is critical when constructing a diversified portfolio. By using the standard deviations from this indicator, investors can better identify assets that may provide diversification benefits, potentially reducing the overall portfolio risk. Moreover, the point values and tick sizes help assess the cost-effectiveness of various assets, enabling portfolio managers to implement more efficient hedging strategies (Markowitz, 1952).

Reference: Markowitz, H. (1952). Portfolio Selection. The Journal of Finance, 7(1), 77-91.

Conclusion

The Tick Information & Standard Deviation Table provides critical market data that informs the risk management, diversification, and pricing strategies used in portfolio management. By incorporating tick size, point value, and volatility metrics, investors can make more informed decisions, better manage risk, and optimize the returns on their portfolios. The data serves as an essential tool for aligning asset selection and portfolio allocations with the investor's risk tolerance and market conditions.

Confluence ChecklistHOW DOES IT WORK?

The "Confluence Checklist" indicator helps you to stick to your trading plan with your set rules. You have a total of 8 rules that can be set up manually. Using the checkbox, you can check during trading whether your rules are followed or not. You can change the colors of the table on the one hand, and the size and width of the table columns on the other.

█ WHAT MAKES IT UNIQUE?

It is the only checklist indicator on Tradingview that has an integrated checkbox. Thus, you can always check your trading plan.

█ HOW TO USE IT?

The best way to start is to create your personal trading plan based on your trading strategy. Then you can display the trading plan digitally in Tradingview. This way you don't have to write and check your rules on paper anymore. This is very important for scalping, because sometimes you only have a few seconds left for the execution. After creating the trading plan, you can integrate it into the checklist. Before placing an order, you can check the checklist to see if the trade is really valid.

Z The Good Stuff +I created this script to have a couple datapoints that I want to look at when going through charts to find trade ideas. Qullamaggie is one of my biggest inspirations and I built in a couple of his concepts with a touch to help me with sizing properly, all explained below:

Box 1: ADR %, Average Daily Range, gives and indication of how volatile the stock is. It uses the 20 day average % move of the current stock on the chart.

Box 2: LOD Distance, low of day distance is a quality of life element I created. It calculates the low for the current candle and color codes it red or green depending on if it's higher or lower than the daily ADR. The logic is that if a stock has an average speed, buying on a setup it is preferred if the stop distance (assuming a low of day stop) should be less than the ADR to improve the odds of more upside.

Box 3: Todays DV, this shows a rough estimate of how much money was traded on the particular day.

Box 4: ADV 20 days, similar to above this shows the 20 day $ traded average. The point to look at it is to have a better idea what position size is possible to not get stuck in something too illiquid.

Box 5: Market cap, just shows the market cap of the stock to know what size the company is.

Box 6: Number of shares, this is an additional quality of life aspect. If using low of day stops, this part calculates based on the users' inputted portfolio size and portfolio risk preference and then calculates how many stocks to buy to stay within the risk parameters. It is obviously not a sole decision making parameter nor does it guarantee any execution, but if a stock is showing an entry you want to take you can use the number of shares to help you know how many to buy. The preset is a portfolio of 10000 and a risk of 0.25%. This means that the number of shares to buy will be at the current price with lod stop that would result in a 0.25% portfolio loss. OF COURSE the actual loss depends on the execution and if the user places a stop loss order.

Hope you find it useful and feel free to give feedback! Cheers!

Position Sizing Calculator (Real-Time)█ SUMMARY

The following indicator is a Position Sizing Calculator based on Average True Range (ATR), originally developed by market technician J. Welles Wilder Jr., intended for real-time trading.

This script utilizes the user's account size, acceptable risk percentage, and a stop-loss distance based on ATR to dynamically calculate the appropriate position size for each trade in real time.

█ BACKGROUND

Developed for use on the 5-minute timeframe, this script provides traders with continuously updated, dynamic position sizes. It enables traders to instantly determine the exact number of shares and dollar amount to use for entering a trade within their acceptable risk tolerance whenever a trade opportunity arises.

This real-time position sizing tool helps traders make well-informed decisions when planning trade entries and calculating maximum stop-loss levels, ultimately enhancing risk management.

█ USER INPUTS

Trading Account Size: Total dollar value of the user's trading account.

Acceptable Risk (%): Maximum percentage of the trading account that the user is willing to risk per trade.

ATR Multiplier for Stop-Loss: Multiplier used to determine the distance of the stop-loss from the current price, based on the ATR value.

ATR Length: The length of the lookback period used to calculate the ATR value.