EDMA Scalping & UT bot alertEDMA Scalping strategy & UT Bot Alert are the copy rights of Mighty Zinger & QuantNomad. Credit and effort for both indicators goes to respective owners. i have compiled them into one single indicator. For any information about this indicator refer to their original scripts.

ניתוח מגמה

Zig Zag + Aroon StrategyBelow is a trading strategy that combines the Zig Zag indicator and the Aroon indicator. This combination can help identify trends and potential reversal points.

Zig Zag and Aroon Strategy Overview

Zig Zag Indicator:

The Zig Zag indicator helps to identify significant price movements and eliminates smaller fluctuations. It is useful for spotting trends and reversals.

Aroon Indicator:

The Aroon indicator consists of two lines: Aroon Up and Aroon Down. It measures the time since the highest high and the lowest low over a specified period, indicating the strength of a trend.

Strategy Conditions

Long Entry Conditions:

Aroon Up crosses above Aroon Down (indicating a bullish trend).

The Zig Zag indicator shows an upward movement (indicating a potential continuation).

Short Entry Conditions:

Aroon Down crosses above Aroon Up (indicating a bearish trend).

The Zig Zag indicator shows a downward movement (indicating a potential continuation).

Exit Conditions:

Exit long when Aroon Down crosses above Aroon Up.

Exit short when Aroon Up crosses above Aroon Down.

FTMO Rules MonitorFTMO Rules Monitor: Stay on Track with Your FTMO Challenge Goals

TLDR; You can test with this template whether your strategy for one asset would pass the FTMO challenges step 1 then step 2, then with real money conditions.

Passing a prop firm challenge is ... challenging.

I believe a toolkit allowing to test in minutes whether a strategy would have passed a prop firm challenge in the past could be very powerful.

The FTMO Rules Monitor is designed to help you stay within FTMO’s strict risk management guidelines directly on your chart. Whether you’re aiming for the $10,000 or the $200,000 account challenge, this tool provides real-time tracking of your performance against FTMO’s rules to ensure you don’t accidentally breach any limits.

NOTES

The connected indicator for this post doesn't matter.

It's just a dummy double supertrends (see below)

The strategy results for this script post does not matter as I'm posting a FTMO rules template on which you can connect any indicator/strategy.

//@version=5

indicator("Supertrends", overlay=true)

// Supertrend 1 Parameters

var string ST1 = "Supertrend 1 Settings"

st1_atrPeriod = input.int(10, "ATR Period", minval=1, maxval=50, group=ST1)

st1_factor = input.float(2, "Factor", minval=0.5, maxval=10, step=0.5, group=ST1)

// Supertrend 2 Parameters

var string ST2 = "Supertrend 2 Settings"

st2_atrPeriod = input.int(14, "ATR Period", minval=1, maxval=50, group=ST2)

st2_factor = input.float(3, "Factor", minval=0.5, maxval=10, step=0.5, group=ST2)

// Calculate Supertrends

= ta.supertrend(st1_factor, st1_atrPeriod)

= ta.supertrend(st2_factor, st2_atrPeriod)

// Entry conditions

longCondition = direction1 == -1 and direction2 == -1 and direction1 == 1

shortCondition = direction1 == 1 and direction2 == 1 and direction1 == -1

// Optional: Plot Supertrends

plot(supertrend1, "Supertrend 1", color = direction1 == -1 ? color.green : color.red, linewidth=3)

plot(supertrend2, "Supertrend 2", color = direction2 == -1 ? color.lime : color.maroon, linewidth=3)

plotshape(series=longCondition, location=location.belowbar, color=color.green, style=shape.triangleup, title="Long")

plotshape(series=shortCondition, location=location.abovebar, color=color.red, style=shape.triangledown, title="Short")

signal = longCondition ? 1 : shortCondition ? -1 : na

plot(signal, "Signal", display = display.data_window)

To connect your indicator to this FTMO rules monitor template, please update it as follow

Create a signal variable to store 1 for the long/buy signal or -1 for the short/sell signal

Plot it in the display.data_window panel so that it doesn't clutter your chart

signal = longCondition ? 1 : shortCondition ? -1 : na

plot(signal, "Signal", display = display.data_window)

In the FTMO Rules Monitor template, I'm capturing this external signal with this input.source variable

entry_connector = input.source(close, "Entry Connector", group="Entry Connector")

longCondition = entry_connector == 1

shortCondition = entry_connector == -1

🔶 USAGE

This indicator displays essential FTMO Challenge rules and tracks your progress toward meeting each one. Here’s what’s monitored:

Max Daily Loss

• 10k Account: $500

• 25k Account: $1,250

• 50k Account: $2,500

• 100k Account: $5,000

• 200k Account: $10,000

Max Total Loss

• 10k Account: $1,000

• 25k Account: $2,500

• 50k Account: $5,000

• 100k Account: $10,000

• 200k Account: $20,000

Profit Target

• 10k Account: $1,000

• 25k Account: $2,500

• 50k Account: $5,000

• 100k Account: $10,000

• 200k Account: $20,000

Minimum Trading Days: 4 consecutive days for all account sizes

🔹 Key Features

1. Real-Time Compliance Check

The FTMO Rules Monitor keeps track of your daily and total losses, profit targets, and trading days. Each metric updates in real-time, giving you peace of mind that you’re within FTMO’s rules.

2. Color-Coded Visual Feedback

Each rule’s status is shown clearly with a ✓ for compliance or ✗ if the limit is breached. When a rule is broken, the indicator highlights it in red, so there’s no confusion.

3. Completion Notification

Once all FTMO requirements are met, the indicator closes all open positions and displays a celebratory message on your chart, letting you know you’ve successfully completed the challenge.

4. Easy-to-Read Table

A table on your chart provides an overview of each rule, your target, current performance, and whether you’re meeting each goal. The table adjusts its color scheme based on your chart settings for optimal visibility.

5. Dynamic Position Sizing

Integrated ATR-based position sizing helps you manage risk and avoid large drawdowns, ensuring each trade aligns with FTMO’s risk management principles.

Daveatt

PTS - Bollinger Bands with Trailing StopPTS - Bollinger Bands with Trailing Stop Strategy

Overview

The "PTS - Bollinger Bands with Trailing Stop" strategy is designed to capitalize on strong bullish market movements by combining the Bollinger Bands indicator with a dynamic trailing stop based on the Average True Range (ATR). This strategy aims to enter long positions during upward breakouts and protect profits through an adaptive exit mechanism.

Key Features

1. Bollinger Bands Indicator

Basis Moving Average Type: Choose from SMA, EMA, SMMA, WMA, or VWMA for the Bollinger Bands' basis line. Length: Adjustable period for calculating the moving average and standard deviation (default is 20). Standard Deviation Multiplier (StdDev): Determines the width of the bands (default is 2.0). Source: Select the price data used for calculations (default is the closing price).

2. Entry Conditions

The strategy enters a long position when the closing price crosses above the upper Bollinger Band , indicating strong upward momentum.

3. Exit Conditions

Trailing Stop Loss: Implemented using ATR to adjust dynamically with market volatility. ATR Length: Period for calculating ATR (default is 14). ATR Multiplier for Trailing Stop: Determines how closely the trailing stop follows the price (default is 2.0). Close Below Lower Bollinger Band: The strategy exits the long position if the closing price crosses below the lower Bollinger Band .

4. Risk Management

Commission and Slippage: Commission is set at 0.1%; slippage is set to 3. Position Sizing: Uses 100% of equity per trade (adjustable).

5. Date Range Filter

Specify the time period during which the strategy is active. Start Date: January 1, 2018. End Date: December 31, 2069.

Customizable Inputs

BB Length: Adjust the period for Bollinger Bands calculation. BB StdDev: Modify the standard deviation multiplier. Basis MA Type: Select the moving average type. Source: Choose the price data source. Offset: Shift the Bollinger Bands on the chart. ATR Length: Set the period for ATR calculation. ATR Multiplier for Trailing Stop: Adjust the trailing stop sensitivity.

Thought for 1m 7s

Description for the "PTS - Bollinger Bands with Trailing Stop" Strategy

PTS - Bollinger Bands with Trailing Stop Strategy

Overview

The "PTS - Bollinger Bands with Trailing Stop" strategy is designed to capitalize on strong bullish market movements by combining the Bollinger Bands indicator with a dynamic trailing stop based on the Average True Range (ATR). This strategy aims to enter long positions during upward breakouts and protect profits through an adaptive exit mechanism.

Key Features

1. Bollinger Bands Indicator

Basis Moving Average Type: Choose from SMA, EMA, SMMA, WMA, or VWMA for the Bollinger Bands' basis line. Length: Adjustable period for calculating the moving average and standard deviation (default is 20). Standard Deviation Multiplier (StdDev): Determines the width of the bands (default is 2.0). Source: Select the price data used for calculations (default is the closing price).

2. Entry Conditions

The strategy enters a long position when the closing price crosses above the upper Bollinger Band , indicating strong upward momentum.

3. Exit Conditions

Trailing Stop Loss: Implemented using ATR to adjust dynamically with market volatility. ATR Length: Period for calculating ATR (default is 14). ATR Multiplier for Trailing Stop: Determines how closely the trailing stop follows the price (default is 2.0). Close Below Lower Bollinger Band: The strategy exits the long position if the closing price crosses below the lower Bollinger Band .

4. Risk Management

Commission and Slippage: Commission is set at 0.1%; slippage is set to 3. Position Sizing: Uses 100% of equity per trade (adjustable).

5. Date Range Filter

Specify the time period during which the strategy is active. Start Date: January 1, 2018. End Date: December 31, 2069.

Customizable Inputs

BB Length: Adjust the period for Bollinger Bands calculation. BB StdDev: Modify the standard deviation multiplier. Basis MA Type: Select the moving average type. Source: Choose the price data source. Offset: Shift the Bollinger Bands on the chart. ATR Length: Set the period for ATR calculation. ATR Multiplier for Trailing Stop: Adjust the trailing stop sensitivity.

How the Strategy Works

1. Initialization

Calculates Bollinger Bands and ATR based on selected parameters.

2. Entry Logic

Opens a long position when the closing price exceeds the upper Bollinger Band.

3. Exit Logic

Uses a trailing stop loss based on ATR. Exits if the closing price drops below the lower Bollinger Band.

4. Date Filtering

Executes trades only within the specified date range.

Advantages

Adaptive Risk Management: Trailing stop adjusts to market volatility. Simplicity: Clear entry and exit signals. Customizable Parameters: Tailor the strategy to different assets or conditions.

Considerations

Aggressive Position Sizing: Using 100% equity per trade is high-risk. Market Conditions: Best in trending markets; may produce false signals in sideways markets. Backtesting: Always test on historical data before live trading.

Disclaimer

This strategy is intended for educational and informational purposes only. Trading involves significant risk, and past performance is not indicative of future results. Assess your financial situation and consult a financial advisor if necessary.

Usage Instructions

1. Apply the Strategy: Add it to your TradingView chart. 2. Configure Inputs: Adjust parameters to suit your style and asset. 3. Analyze Backtest Results: Use the Strategy Tester. 4. Optimize Parameters: Experiment with input values. 5. Risk Management: Evaluate position sizing and incorporate risk controls.

Final Notes

The "PTS - Bollinger Bands with Trailing Stop" strategy provides a framework to leverage momentum breakouts while managing risk through adaptive trailing stops. Customize and test thoroughly to align with your trading objectives.

Fibonacci ATR Fusion - Strategy [presentTrading]Open-script again! This time is also an ATR-related strategy. Enjoy! :)

If you have any questions, let me know, and I'll help make this as effective as possible.

█ Introduction and How It Is Different

The Fibonacci ATR Fusion Strategy is an advanced trading approach that uniquely integrates Fibonacci-based weighted averages with the Average True Range (ATR) to identify and capitalize on significant market trends.

Unlike traditional strategies that rely on single indicators or static parameters, this method combines multiple timeframes and dynamic volatility measurements to enhance precision and adaptability. Additionally, it features a 4-step Take Profit (TP) mechanism, allowing for systematic profit-taking at various levels, which optimizes both risk management and return potential in long and short market positions.

BTCUSD 6hr Performance

█ Strategy, How It Works: Detailed Explanation

The Fibonacci ATR Fusion Strategy utilizes a combination of technical indicators and weighted averages to determine optimal entry and exit points. Below is a breakdown of its key components and operational logic.

🔶 1. Enhanced True Range Calculation

The strategy begins by calculating the True Range (TR) to measure market volatility accurately.

TR = max(High - Low, abs(High - Previous Close), abs(Low - Previous Close))

High and Low: Highest and lowest prices of the current trading period.

Previous Close: Closing price of the preceding trading period.

max: Selects the largest value among the three calculations to account for gaps and limit movements.

🔶 2. Buying Pressure (BP) Calculation

Buying Pressure (BP) quantifies the extent to which buyers are driving the price upwards within a period.

BP = Close - True Low

Close: Current period's closing price.

True Low: The lower boundary determined in the True Range calculation.

🔶 3. Ratio Calculation for Different Periods

To assess the strength of buying pressure relative to volatility, the strategy calculates a ratio over various Fibonacci-based timeframes.

Ratio = 100 * (Sum of BP over n periods) / (Sum of TR over n periods)

n: Length of the period (e.g., 8, 13, 21, 34, 55).

Sum of BP: Cumulative Buying Pressure over n periods.

Sum of TR: Cumulative True Range over n periods.

This ratio normalizes buying pressure, making it comparable across different timeframes.

🔶 4. Weighted Average Calculation

The strategy employs a weighted average of ratios from multiple Fibonacci-based periods to smooth out signals and enhance trend detection.

Weighted Avg = (w1 * Ratio_p1 + w2 * Ratio_p2 + w3 * Ratio_p3 + w4 * Ratio_p4 + Ratio_p5) / (w1 + w2 + w3 + w4 + 1)

w1, w2, w3, w4: Weights assigned to each ratio period.

Ratio_p1 to Ratio_p5: Ratios calculated for periods p1 to p5 (e.g., 8, 13, 21, 34, 55).

This weighted approach emphasizes shorter periods more heavily, capturing recent market dynamics while still considering longer-term trends.

🔶 5. Simple Moving Average (SMA) of Weighted Average

To further smooth the weighted average and reduce noise, a Simple Moving Average (SMA) is applied.

Weighted Avg SMA = SMA(Weighted Avg, m)

- m: SMA period (e.g., 3).

This smoothed line serves as the primary signal generator for trade entries and exits.

🔶 6. Trading Condition Thresholds

The strategy defines specific threshold values to determine optimal entry and exit points based on crossovers and crossunders of the SMA.

Long Condition = Crossover(Weighted Avg SMA, Long Entry Threshold)

Short Condition = Crossunder(Weighted Avg SMA, Short Entry Threshold)

Long Exit = Crossunder(Weighted Avg SMA, Long Exit Threshold)

Short Exit = Crossover(Weighted Avg SMA, Short Exit Threshold)

Long Entry Threshold (T_LE): Level at which a long position is triggered.

Short Entry Threshold (T_SE): Level at which a short position is triggered.

Long Exit Threshold (T_LX): Level at which a long position is exited.

Short Exit Threshold (T_SX): Level at which a short position is exited.

These conditions ensure that trades are only executed when clear trends are identified, enhancing the strategy's reliability.

Previous local performance

🔶 7. ATR-Based Take Profit Mechanism

When enabled, the strategy employs a 4-step Take Profit system to systematically secure profits as the trade moves in the desired direction.

TP Price_1 Long = Entry Price + (TP1ATR * ATR Value)

TP Price_2 Long = Entry Price + (TP2ATR * ATR Value)

TP Price_3 Long = Entry Price + (TP3ATR * ATR Value)

TP Price_1 Short = Entry Price - (TP1ATR * ATR Value)

TP Price_2 Short = Entry Price - (TP2ATR * ATR Value)

TP Price_3 Short = Entry Price - (TP3ATR * ATR Value)

- ATR Value: Calculated using ATR over a specified period (e.g., 14).

- TPxATR: User-defined multipliers for each take profit level.

- TPx_percent: Percentage of the position to exit at each TP level.

This multi-tiered exit strategy allows for partial position closures, optimizing profit capture while maintaining exposure to potential further gains.

█ Trade Direction

The Fibonacci ATR Fusion Strategy is designed to operate in both long and short market conditions, providing flexibility to traders in varying market environments.

Long Trades: Initiated when the SMA of the weighted average crosses above the Long Entry Threshold (T_LE), indicating strong upward momentum.

Short Trades: Initiated when the SMA of the weighted average crosses below the Short Entry Threshold (T_SE), signaling robust downward momentum.

Additionally, the strategy can be configured to trade exclusively in one direction—Long, Short, or Both—based on the trader’s preference and market analysis.

█ Usage

Implementing the Fibonacci ATR Fusion Strategy involves several steps to ensure it aligns with your trading objectives and market conditions.

1. Configure Strategy Parameters:

- Trading Direction: Choose between Long, Short, or Both based on your market outlook.

- Trading Condition Thresholds: Set the Long Entry, Short Entry, Long Exit, and Short Exit thresholds to define when to enter and exit trades.

2. Set Take Profit Levels (if enabled):

- ATR Multipliers: Define how many ATRs away from the entry price each take profit level is set.

- Take Profit Percentages: Allocate what percentage of the position to close at each TP level.

3. Apply to Desired Chart:

- Add the strategy to the chart of the asset you wish to trade.

- Observe the plotted Fibonacci ATR and SMA Fibonacci ATR indicators for visual confirmation.

4. Monitor and Adjust:

- Regularly review the strategy’s performance through backtesting.

- Adjust the input parameters based on historical performance and changing market dynamics.

5. Risk Management:

- Ensure that the sum of take profit percentages does not exceed 100% to avoid over-closing positions.

- Utilize the ATR-based TP levels to adapt to varying market volatilities, maintaining a balanced risk-reward ratio.

█ Default Settings

Understanding the default settings is crucial for optimizing the Fibonacci ATR Fusion Strategy's performance. Here's a precise and simple overview of the key parameters and their effects:

🔶 Key Parameters and Their Effects

1. Trading Direction (`tradingDirection`)

- Default: Both

- Effect: Determines whether the strategy takes both long and short positions or restricts to one direction. Selecting Both allows maximum flexibility, while Long or Short can be used for directional bias.

2. Trading Condition Thresholds

Long Entry (long_entry_threshold = 58.0): Higher values reduce false positives but may miss trades.

Short Entry (short_entry_threshold = 42.0): Lower values capture early short trends but may increase false signals.

Long Exit (long_exit_threshold = 42.0): Exits long positions early, securing profits but potentially cutting trends short.

Short Exit (short_exit_threshold = 58.0): Delays short exits to capture favorable movements, avoiding premature exits.

3. Take Profit Configuration (`useTakeProfit` = false)

- Effect: When enabled, the strategy employs a 4-step TP mechanism to secure profits at multiple levels. By default, it is disabled to allow users to opt-in based on their trading style.

4. ATR-Based Take Profit Multipliers

TP1 (tp1ATR = 3.0): Sets the first TP at 3 ATRs for initial profit capture.

TP2 (tp2ATR = 8.0): Targets larger trends, though less likely to be reached.

TP3 (tp3ATR = 14.0): Optimizes for extreme price moves, seldom triggered.

5. Take Profit Percentages

TP Level 1 (tp1_percent = 12%): Secures 12% at the first TP.

TP Level 2 (tp2_percent = 12%): Exits another 12% at the second TP.

TP Level 3 (tp3_percent = 12%): Closes an additional 12% at the third TP.

6. Weighted Average Parameters

Ratio Periods: Fibonacci-based intervals (8, 13, 21, 34, 55) balance responsiveness.

Weights: Emphasizes recent data for timely responses to market trends.

SMA Period (weighted_avg_sma_period = 3): Smoothens data with minimal lag, balancing noise reduction and responsiveness.

7. ATR Period (`atrPeriod` = 14)

Effect: Sets the ATR calculation length, impacting TP sensitivity to volatility.

🔶 Impact on Performance

- Sensitivity and Responsiveness:

- Shorter Ratio Periods and Higher Weights: Make the weighted average more responsive to recent price changes, allowing quicker trade entries and exits but increasing the likelihood of false signals.

- Longer Ratio Periods and Lower Weights: Provide smoother signals with fewer false positives but may delay trade entries, potentially missing out on significant price moves.

- Profit Taking:

- ATR Multipliers: Higher multipliers set take profit levels further away, targeting larger price movements but reducing the probability of reaching these levels.

- Fixed Percentages: Allocating equal percentages at each TP level ensures consistent profit realization and risk management, preventing overexposure.

- Trade Direction Control:

- Selecting Specific Directions: Restricting trades to Long or Short can align the strategy with market trends or personal biases, potentially enhancing performance in trending markets.

- Risk Management:

- Take Profit Percentages: Dividing the position into smaller percentages at multiple TP levels helps lock in profits progressively, reducing risk and allowing the remaining position to ride further trends.

- Market Adaptability:

- Weighted Averages and ATR: By combining multiple timeframes and adjusting to volatility, the strategy adapts to different market conditions, maintaining effectiveness across various asset classes and timeframes.

---

If you want to know more about ATR, can also check "SuperATR 7-Step Profit".

Enjoy trading.

The Most Powerful TQQQ EMA Crossover Trend Trading StrategyTQQQ EMA Crossover Strategy Indicator

Meta Title: TQQQ EMA Crossover Strategy - Enhance Your Trading with Effective Signals

Meta Description: Discover the TQQQ EMA Crossover Strategy, designed to optimize trading decisions with fast and slow EMA crossovers. Learn how to effectively use this powerful indicator for better trading results.

Key Features

The TQQQ EMA Crossover Strategy is a powerful trading tool that utilizes Exponential Moving Averages (EMAs) to identify potential entry and exit points in the market. Key features of this indicator include:

**Fast and Slow EMAs:** The strategy incorporates two EMAs, allowing traders to capture short-term trends while filtering out market noise.

**Entry and Exit Signals:** Automated signals for entering and exiting trades based on EMA crossovers, enhancing decision-making efficiency.

**Customizable Parameters:** Users can adjust the lengths of the EMAs, as well as take profit and stop loss multipliers, tailoring the strategy to their trading style.

**Visual Indicators:** Clear visual plots of the EMAs and exit points on the chart for easy interpretation.

How It Works

The TQQQ EMA Crossover Strategy operates by calculating two EMAs: a fast EMA (default length of 20) and a slow EMA (default length of 50). The core concept is based on the crossover of these two moving averages:

- When the fast EMA crosses above the slow EMA, it generates a *buy signal*, indicating a potential upward trend.

- Conversely, when the fast EMA crosses below the slow EMA, it produces a *sell signal*, suggesting a potential downward trend.

This method allows traders to capitalize on momentum shifts in the market, providing timely signals for trade execution.

Trading Ideas and Insights

Traders can leverage the TQQQ EMA Crossover Strategy in various market conditions. Here are some insights:

**Scalping Opportunities:** The strategy is particularly effective for scalping in volatile markets, allowing traders to make quick profits on small price movements.

**Swing Trading:** Longer-term traders can use this strategy to identify significant trend reversals and capitalize on larger price swings.

**Risk Management:** By incorporating customizable stop loss and take profit levels, traders can manage their risk effectively while maximizing potential returns.

How Multiple Indicators Work Together

While this strategy primarily relies on EMAs, it can be enhanced by integrating additional indicators such as:

- **Relative Strength Index (RSI):** To confirm overbought or oversold conditions before entering trades.

- **Volume Indicators:** To validate breakout signals, ensuring that price movements are supported by sufficient trading volume.

Combining these indicators provides a more comprehensive view of market dynamics, increasing the reliability of trade signals generated by the EMA crossover.

Unique Aspects

What sets this indicator apart is its simplicity combined with effectiveness. The reliance on EMAs allows for smoother signals compared to traditional moving averages, reducing false signals often associated with choppy price action. Additionally, the ability to customize parameters ensures that traders can adapt the strategy to fit their unique trading styles and risk tolerance.

How to Use

To effectively utilize the TQQQ EMA Crossover Strategy:

1. **Add the Indicator:** Load the script onto your TradingView chart.

2. **Set Parameters:** Adjust the fast and slow EMA lengths according to your trading preferences.

3. **Monitor Signals:** Watch for crossover points; enter trades based on buy/sell signals generated by the indicator.

4. **Implement Risk Management:** Set your stop loss and take profit levels using the provided multipliers.

Regularly review your trading performance and adjust parameters as necessary to optimize results.

Customization

The TQQQ EMA Crossover Strategy allows for extensive customization:

- **EMA Lengths:** Change the default lengths of both fast and slow EMAs to suit different time frames or market conditions.

- **Take Profit/Stop Loss Multipliers:** Adjust these values to align with your risk management strategy. For instance, increasing the take profit multiplier may yield larger gains but could also increase exposure to market fluctuations.

This flexibility makes it suitable for various trading styles, from aggressive scalpers to conservative swing traders.

Conclusion

The TQQQ EMA Crossover Strategy is an effective tool for traders seeking an edge in their trading endeavors. By utilizing fast and slow EMAs, this indicator provides clear entry and exit signals while allowing for customization to fit individual trading strategies. Whether you are a scalper looking for quick profits or a swing trader aiming for larger moves, this indicator offers valuable insights into market trends.

Incorporate it into your TradingView toolkit today and elevate your trading performance!

Bullish B's - RSI Divergence StrategyThis indicator strategy is an RSI (Relative Strength Index) divergence trading tool designed to identify high-probability entry and exit points based on trend shifts. It utilizes both regular and hidden RSI divergence patterns to spot potential reversals, with signals for both bullish and bearish conditions.

Key Features

Divergence Detection:

Bullish Divergence: Signals when RSI indicates momentum strengthening at a lower price level, suggesting a reversal to the upside.

Bearish Divergence: Signals when RSI shows weakening momentum at a higher price level, indicating a potential downside reversal.

Hidden Divergences: Looks for hidden bullish and bearish divergences, which signal trend continuation points where price action aligns with the prevailing trend.

Volume-Adjusted Entry Signals:

The strategy enters long trades when RSI shows bullish or hidden bullish divergence, indicating an upward momentum shift.

An optional volume filter ensures that only high-volume, high-conviction trades trigger a signal.

Exit Signals:

Exits long positions when RSI reaches a customizable overbought level, typically indicating a potential reversal or profit-taking opportunity.

Also closes positions if bearish divergence signals appear after a bullish setup, providing protection against trend reversals.

Trailing Stop-Loss:

Uses a trailing stop mechanism based on ATR (Average True Range) or a percentage threshold to lock in profits as the price moves in favor of the trade.

Alerts and Custom Notifications:

Integrated with TradingView alerts to notify the user when entry and exit conditions are met, supporting timely decision-making without constant monitoring.

Customizable Parameters:

Users can adjust the RSI period, pivot lookback range, overbought level, trailing stop type (ATR or percentage), and divergence range to fit their trading style.

Ideal Usage

This strategy is well-suited for trend traders and swing traders looking to capture reversals and trend continuations on medium to long timeframes. The divergence signals, paired with trailing stops and volume validation, make it adaptable for multiple asset classes, including stocks, forex, and crypto.

Summary

With its focus on RSI divergence, trailing stop-loss management, and volume filtering, this strategy aims to identify and capture trend changes with minimized risk. This allows traders to efficiently capture profitable moves and manage open positions with precision.

This Strategy BEST works with GLD!

Z-Score RSI StrategyOverview

The Z-Score RSI Indicator is an experimental take on momentum analysis. By applying the Relative Strength Index (RSI) to a Z-score of price data, it measures how far prices deviate from their mean, scaled by standard deviation. This isn’t your traditional use of RSI, which is typically based on price data alone. Nevertheless, this unconventional approach can yield unique insights into market trends and potential reversals.

Theory and Interpretation

The RSI calculates the balance between average gains and losses over a set period, outputting values from 0 to 100. Typically, people look at the overbought or oversold levels to identify momentum extremes that might be likely to lead to a reversal. However, I’ve often found that RSI can be effective for trend-following when observing the crossover of its moving average with the midline or the crossover of the RSI with its own moving average. These crossovers can provide useful trend signals in various market conditions.

By combining RSI with a Z-score of price, this indicator estimates the relative strength of the price’s distance from its mean. Positive Z-score trends may signal a potential for higher-than-average prices in the near future (scaled by the standard deviation), while negative trends suggest the opposite. Essentially, when the Z-Score RSI indicates a trend, it reflects that the Z-score (the distance between the average and current price) is likely to continue moving in the trend’s direction. Generally, this signals a potential price movement, though it’s important to note that this could also occur if there’s a shift in the mean or standard deviation, rather than a meaningful change in price itself.

While the Z-Score RSI could be an insightful addition to a comprehensive trading system, it should be interpreted carefully. Mean shifts may validate the indicator’s predictions without necessarily indicating any notable price change, meaning it’s best used in tandem with other indicators or strategies.

Recommendations

Before putting this indicator to use, conduct thorough backtesting and avoid overfitting. The added parameters allow fine-tuning to fit various assets, but be careful not to optimize purely for the highest historical returns. Doing so may create an overly tailored strategy that performs well in backtests but fails in live markets. Keep it balanced and look for robust performance across multiple scenarios, as overfitting is likely to lead to disappointing real-world results.

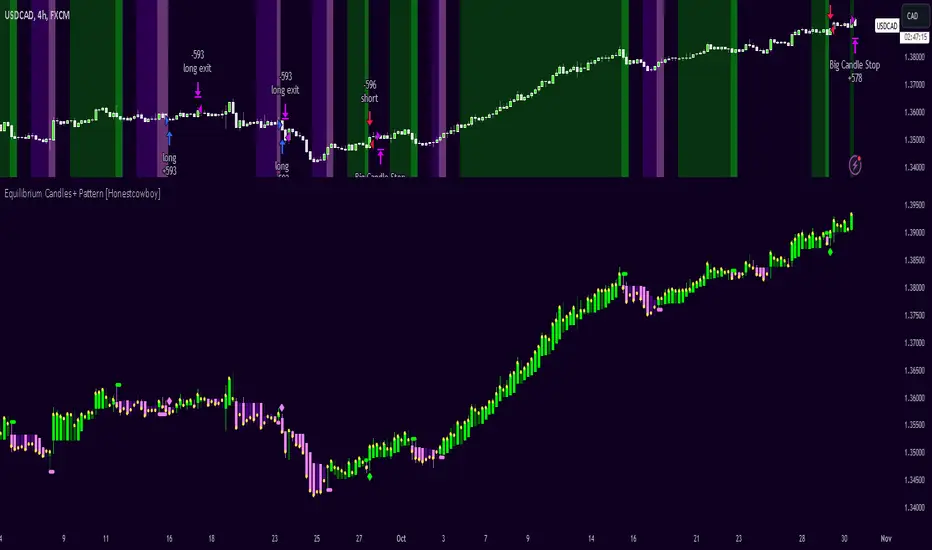

Equilibrium Candles + Pattern [Honestcowboy]The Equilibrium Candles is a very simple trend continuation or reversal strategy depending on your settings.

How an Equilibrium Candle is created:

We calculate the equilibrium by measuring the mid point between highest and lowest point over X amount of bars back.

This now is the opening price for each bar and will be considered a green bar if price closes above equilibrium.

Bars get shaded by checking if regular candle close is higher than open etc. So you still see what the normal candles are doing.

Why are they useful?

The equilibrium is calculated the same as Baseline in Ichimoku Cloud. Which provides a point where price is very likely to retrace to. This script visualises the distance between close and equilibrium using candles. To provide a clear visual of how price relates to this equilibrium point.

This also makes it more straightforward to develop strategies based on this simple concept and makes the trader purely focus on this relationship and not think of any Ichimoku Cloud theories.

Script uses a very simple pattern to enter trades:

It will count how many candles have been one directional (above or below equilibrium)

Based on user input after X candles (7 by default) script shows we are in a trend (bg colors)

On the first pullback (candle closes on other side of equilibrium) it will look to enter a trade.

Places a stop order at the high of the candle if bullish trend or reverse if bearish trend.

If based on user input after X opposite candles (2 by default) order is not filled will cancel it and look for a new trend.

Use Reverse Logic:

There is a use reverse logic in the settings which on default is turned on. It will turn long orders into short orders making the stop orders become limit orders. It will use the normal long SL as target for the short. And TP as stop for the short. This to provide a means to reverse equity curve in case your pair is mean reverting by nature instead of trending.

ATR Calculation:

Averaged ATR, which is using ta.percentile_nearest_rank of 60% of a normal ATR (14 period) over the last 200 bars. This in simple words finds a value slightly above the mean ATR value over that period.

Big Candle Exit Logic:

Using Averaged ATR the script will check if a candle closes X times that ATR from the equilibrium point. This is then considered an overextension and all trades are closed.

This is also based on user input.

Simple trade management logic:

Checks if the user has selected to use TP and SL, or/and big candle exit.

Places a TP and SL based on averaged ATR at a multiplier based on user Input.

Closes trade if there is a Big Candle Exit or an opposite direction signal from indicator.

Script can be fully automated to MT5

There are risk settings in % and symbol settings provided at the bottom of the indicator. The script will send alert to MT5 broker trying to mimic the execution that happens on tradingview. There are always delays when using a bridge to MT5 broker and there could be errors so be mindful of that. This script sends alerts in format so they can be read by tradingview.to which is a bridge between the platforms.

Use the all alert function calls feature when setting up alerts and make sure you provide the right webhook if you want to use this approach.

There is also a simple buy and sell alert feature if you don't want to fully automate but still get alerts. These are available in the dropdown when creating an alert.

Almost every setting in this indicator has a tooltip added to it. So if any setting is not clear hover over the (?) icon on the right of the setting.

The backtest uses a 4% exposure per trade and a 10 point slippage. I did not include a commission cause I'm not personaly aware what the commissions are on most forex brokers. I'm only aware of minimal slippage to use in a backtest. Trading conditions vary per broker you use so always pay close attention to trading costs on your own broker. Use a full automation at your own risk and discretion and do proper backtesting.

SuperATR 7-Step Profit - Strategy [presentTrading] Long time no see!

█ Introduction and How It Is Different

The SuperATR 7-Step Profit Strategy is a multi-layered trading approach that integrates adaptive Average True Range (ATR) calculations with momentum-based trend detection. What sets this strategy apart is its sophisticated 7-step take-profit mechanism, which combines four ATR-based exit levels and three fixed percentage levels. This hybrid approach allows traders to dynamically adjust to market volatility while systematically capturing profits in both long and short market positions.

Traditional trading strategies often rely on static indicators or single-layered exit strategies, which may not adapt well to changing market conditions. The SuperATR 7-Step Profit Strategy addresses this limitation by:

- Using Adaptive ATR: Enhances the standard ATR by making it responsive to current market momentum.

- Incorporating Momentum-Based Trend Detection: Identifies stronger trends with higher probability of continuation.

- Employing a Multi-Step Take-Profit System: Allows for gradual profit-taking at predetermined levels, optimizing returns while minimizing risk.

BTCUSD 6hr Performance

█ Strategy, How It Works: Detailed Explanation

The strategy revolves around detecting strong market trends and capitalizing on them using an adaptive ATR and momentum indicators. Below is a detailed breakdown of each component of the strategy.

🔶 1. True Range Calculation with Enhanced Volatility Detection

The True Range (TR) measures market volatility by considering the most significant price movements. The enhanced TR is calculated as:

TR = Max

Where:

High and Low are the current bar's high and low prices.

Previous Close is the closing price of the previous bar.

Abs denotes the absolute value.

Max selects the maximum value among the three calculations.

🔶 2. Momentum Factor Calculation

To make the ATR adaptive, the strategy incorporates a Momentum Factor (MF), which adjusts the ATR based on recent price movements.

Momentum = Close - Close

Stdev_Close = Standard Deviation of Close over n periods

Normalized_Momentum = Momentum / Stdev_Close (if Stdev_Close ≠ 0)

Momentum_Factor = Abs(Normalized_Momentum)

Where:

Close is the current closing price.

n is the momentum_period, a user-defined input (default is 7).

Standard Deviation measures the dispersion of closing prices over n periods.

Abs ensures the momentum factor is always positive.

🔶 3. Adaptive ATR Calculation

The Adaptive ATR (AATR) adjusts the traditional ATR based on the Momentum Factor, making it more responsive during volatile periods and smoother during consolidation.

Short_ATR = SMA(True Range, short_period)

Long_ATR = SMA(True Range, long_period)

Adaptive_ATR = /

Where:

SMA is the Simple Moving Average.

short_period and long_period are user-defined inputs (defaults are 3 and 7, respectively).

🔶 4. Trend Strength Calculation

The strategy quantifies the strength of the trend to filter out weak signals.

Price_Change = Close - Close

ATR_Multiple = Price_Change / Adaptive_ATR (if Adaptive_ATR ≠ 0)

Trend_Strength = SMA(ATR_Multiple, n)

🔶 5. Trend Signal Determination

If (Short_MA > Long_MA) AND (Trend_Strength > Trend_Strength_Threshold):

Trend_Signal = 1 (Strong Uptrend)

Elif (Short_MA < Long_MA) AND (Trend_Strength < -Trend_Strength_Threshold):

Trend_Signal = -1 (Strong Downtrend)

Else:

Trend_Signal = 0 (No Clear Trend)

🔶 6. Trend Confirmation with Price Action

Adaptive_ATR_SMA = SMA(Adaptive_ATR, atr_sma_period)

If (Trend_Signal == 1) AND (Close > Short_MA) AND (Adaptive_ATR > Adaptive_ATR_SMA):

Trend_Confirmed = True

Elif (Trend_Signal == -1) AND (Close < Short_MA) AND (Adaptive_ATR > Adaptive_ATR_SMA):

Trend_Confirmed = True

Else:

Trend_Confirmed = False

Local Performance

🔶 7. Multi-Step Take-Profit Mechanism

The strategy employs a 7-step take-profit system

█ Trade Direction

The SuperATR 7-Step Profit Strategy is designed to work in both long and short market conditions. By identifying strong uptrends and downtrends, it allows traders to capitalize on price movements in either direction.

Long Trades: Initiated when the market shows strong upward momentum and the trend is confirmed.

Short Trades: Initiated when the market exhibits strong downward momentum and the trend is confirmed.

█ Usage

To implement the SuperATR 7-Step Profit Strategy:

1. Configure the Strategy Parameters:

- Adjust the short_period, long_period, and momentum_period to match the desired sensitivity.

- Set the trend_strength_threshold to control how strong a trend must be before acting.

2. Set Up the Multi-Step Take-Profit Levels:

- Define ATR multipliers and fixed percentage levels according to risk tolerance and profit goals.

- Specify the percentage of the position to close at each level.

3. Apply the Strategy to a Chart:

- Use the strategy on instruments and timeframes where it has been tested and optimized.

- Monitor the positions and adjust parameters as needed based on performance.

4. Backtest and Optimize:

- Utilize TradingView's backtesting features to evaluate historical performance.

- Adjust the default settings to optimize for different market conditions.

█ Default Settings

Understanding default settings is crucial for optimal performance.

Short Period (3): Affects the responsiveness of the short-term MA.

Effect: Lower values increase sensitivity but may produce more false signals.

Long Period (7): Determines the trend baseline.

Effect: Higher values reduce noise but may delay signals.

Momentum Period (7): Influences adaptive ATR and trend strength.

Effect: Shorter periods react quicker to price changes.

Trend Strength Threshold (0.5): Filters out weaker trends.

Effect: Higher thresholds yield fewer but stronger signals.

ATR Multipliers: Set distances for ATR-based exits.

Effect: Larger multipliers aim for bigger moves but may reduce hit rate.

Fixed TP Levels (%): Control profit-taking on smaller moves.

Effect: Adjusting these levels affects how quickly profits are realized.

Exit Percentages: Determine how much of the position is closed at each TP level.

Effect: Higher percentages reduce exposure faster, affecting risk and reward.

Adjusting these variables allows you to tailor the strategy to different market conditions and personal risk preferences.

By integrating adaptive indicators and a multi-tiered exit strategy, the SuperATR 7-Step Profit Strategy offers a versatile tool for traders seeking to navigate varying market conditions effectively. Understanding and adjusting the key parameters enables traders to harness the full potential of this strategy.

DSL Strategy [DailyPanda]

Overview

The DSL Strategy by DailyPanda is a trading strategy that synergistically combines the idea from indicators to create a more robust and reliable trading tool. By integrating these indicators, the strategy enhances signal accuracy and provides traders with a comprehensive view of market trends and momentum shifts. This combination allows for better entry and exit points, improved risk management, and adaptability to various market conditions.

Combining ideas from indicators adds value by:

Enhancing Signal Confirmation : The strategy requires alignment between trend and momentum before generating trade signals, reducing false entries.

Improving Accuracy : By integrating price action with momentum analysis, the strategy captures more reliable trading opportunities.

Providing Comprehensive Market Insight : The combination offers a better perspective on the market, considering both the direction (trend) and the strength (momentum) of price movements.

How the Components Work Together

1. Trend Identification with DSL Indicator

Dynamic Signal Lines : Calculates upper and lower DSL lines based on a moving average (SMA) and dynamic thresholds derived from recent highs and lows with a specified offset. These lines adapt to market conditions, providing real-time trend insights.

ATR-Based Bands : Adds bands around the DSL lines using the Average True Range (ATR) multiplied by a width factor. These bands account for market volatility and help identify potential stop-loss levels.

Trend Confirmation : The relationship between the price, DSL lines, and bands determines the current trend. For example, if the price consistently stays above the upper DSL line, it indicates a bullish trend.

2. Momentum Analysis

RSI Calculation : Computes the RSI over a specified period to measure the speed and change of price movements.

Zero-Lag EMA (ZLEMA) : Applies a ZLEMA to the RSI to minimize lag and produce a more responsive oscillator.

DSL Application on Oscillator : Implements the DSL concept on the oscillator by calculating dynamic upper and lower levels. This helps identify overbought or oversold conditions more accurately.

Signal Generation : Detects crossovers between the oscillator and its DSL lines. A crossover above the lower DSL line signals potential bullish momentum, while a crossover below the upper DSL line signals potential bearish momentum.

3. Integrated Signal Filtering

Confluence Requirement : A trade signal is generated only when both the DSL indicator and oscillator agree. For instance, a long entry requires both an uptrend confirmation from the DSL indicator and a bullish momentum signal from the oscillator.

Risk Management Integration : The strategy uses the DSL indicator's bands for setting stop-loss levels and calculates take-profit levels based on a user-defined risk-reward ratio. This ensures that every trade has a predefined risk management plan.

--------------------------------------------------------------------------------------------

Originality and Value Added to the Community

Unique Synergy : While both indicators are available individually, this strategy is original in how it combines them to enhance their strengths and mitigate their weaknesses, offering a novel approach not present in existing scripts.

Enhanced Reliability : By requiring confirmation from both trend and momentum indicators, the strategy reduces false signals and increases the likelihood of successful trades.

Versatility : The customizable parameters allow traders to adapt the strategy to different instruments, timeframes, and trading styles, making it a valuable tool for a wide range of trading scenarios.

Educational Contribution : The script demonstrates an effective method of combining indicators for improved trading performance, providing insights that other traders can learn from and apply to their own strategies.

--------------------------------------------------------------------------------------------

How to Use the Strategy

Adding the Strategy to Your Chart

Apply the DSL Strategy to your desired trading instrument and timeframe on TradingView.

--------------------------------------------------------------------------------------------

Configuring Parameters

DSL Indicator Settings :

Length (len) : Adjusts the sensitivity of the DSL lines (default is 34).

Offset : Determines the look-back period for threshold calculations (default is 30).

Bands Width (width) : Changes the distance of the ATR-based bands from the DSL lines (default is 1).

DSL-BELUGA Oscillator Settings :

Beluga Length (len_beluga) : Sets the period for the RSI calculation in the oscillator (default is 10).

DSL Lines Mode (dsl_mode) : Chooses between "Fast" (more responsive) and "Slow" (smoother) modes for the oscillator's DSL lines.

Risk Management :

Risk Reward (risk_reward) : Defines your desired risk-reward ratio for calculating take-profit levels (default is 1.5).

--------------------------------------------------------------------------------------------

Interpreting Signals

Long Entry Conditions :

Trend Confirmation : Price is above the upper DSL line and the upper DSL band (dsl_up1 > dsl_dn).

Price Behavior : The last three candles have both their opens and closes above the upper DSL line.

Momentum Signal : The DSL-BELUGA oscillator crosses above its lower DSL line (up_signal), indicating bullish momentum.

Short Entry Conditions :

Trend Confirmation : Price is below the lower DSL line and the lower DSL band (dsl_dn < dsl_up1).

Price Behavior : The last three candles have both their opens and closes below the lower DSL band.

Momentum Signal : The DSL-BELUGA oscillator crosses below its upper DSL line (dn_signal), indicating bearish momentum.

Exit Conditions :

Stop-Loss : Automatically set at the DSL indicator's band level (upper band for longs, lower band for shorts).

Take-Profit : Calculated based on the risk-reward ratio and the initial risk determined by the stop-loss distance.

Visual Aids

Signal Arrows : Upward green arrows for long entries and downward blue arrows for short entries appear on the chart when conditions are met.

Stop-Loss and Take-Profit Lines : Red and green lines display the calculated stop-loss and take-profit levels for active trades.

Background Highlighting : The chart background subtly changes color to indicate when a signal has been generated.

Backtesting and Optimization

Use TradingView's strategy tester to backtest the strategy over historical data.

Adjust parameters to optimize performance for different instruments or market conditions.

Regularly review backtesting results to ensure the strategy remains effective.

RVI Crossover Strategy[Kopottaja]Overview of the RVI Crossover Strategy

Strategy Name: RVI Crossover Strategy

Purpose: The RVI Crossover Strategy is based on the crossover signals between the Relative Vigor Index (RVI) and its moving average signal line. This strategy aims to identify potential buy and sell signals by evaluating the market’s directional trend.

Key Indicator Features

Relative Vigor Index (RVI): This indicator measures the momentum of price changes over a specified period and helps identify the market’s current trend. The RVI is based on the idea that prices generally close higher than they open in an uptrend (and lower in a downtrend). The RVI helps provide an indication of the strength and direction of a trend.

Signal Line: A moving average (e.g., SMA) is applied to the RVI values, creating a "signal line." When the RVI crosses above or below this line, it signals a potential trading opportunity.

Calculations and Settings

Calculating the RVI: The RVI is calculated by comparing the difference between the close and open prices to the difference between high and low prices. This provides information about the direction and momentum of price movement:

RVI= Sum(SWMA(high−low))Sum(SWMA(close−open))

where SWMA is a smoothed weighted moving average over a specified period.

Signal Line Calculation: The RVI value is smoothed by applying a simple moving average (SMA) to create the signal line. This signal line helps filter crossover signals for improved accuracy.

Buy and Sell Conditions: Buy and sell conditions are identified based on crossovers between the RVI and its signal line.

Buy Signal: A buy condition is triggered when the RVI crosses above the signal line, provided that the "Bearish" condition (trend confirmation) is met.

Sell Signal: A sell condition occurs when the RVI crosses below the signal line, alongside the "Bullish" trend confirmation.

Volume-Weighted Moving Averages (VWMA): VWMA indicators are used to assess price-volume relationships over different timeframes:

Fast VWMA: A short-period volume-weighted moving average.

Slow VWMA: A longer-period volume-weighted moving average. These values are used to strengthen the buy and sell conditions by confirming trend directions (Bullish or Bearish).

Disclaimer: This is an educational and informational tool. Past performance is not indicative of future results. Always backtest before using in live markets

Price Action StrategyThe **Price Action Strategy** is a tool designed to capture potential market reversals by utilizing classic reversal candlestick patterns such as Hammer, Shooting Star, Doji, and Pin Bar near dinamic support and resistance levels.

***Note to moderators

- The moving average was removed from the strategy because it was not suitable for the strategy and not participating in the entry or exit criteria.

- The moving average length has been replaced/renamed by the support/resistance lenght.

- The bullish engulfing and bearish engulfing patterns were also removed because in practice they were not working as entry criteria, since the candle price invariably closes far from the support/resistance level even considering the sensitivity range. There was no change in the backtest results after removing these patterns.

### Key Elements of the Strategy

1. Support and Resistance Levels

- Support and resistance are pivotal price levels where the asset has previously struggled to move lower (support) or higher (resistance). These levels act as psychological barriers where buying interest (at support) or selling interest (at resistance) often increases, potentially causing price reversals.

- In this strategy, support is calculated as the lowest low and resistance as the highest high over a 16-period length. When the price nears these levels, it indicates possible zones for a reversal, and the strategy looks for specific candlestick patterns to confirm an entry.

2. Candlestick Patterns

- This strategy uses classic reversal patterns, including:

- **Hammer**: Indicates a buy signal, suggesting rejection of lower prices.

- **Shooting Star**: Suggests a sell signal, showing rejection of higher prices.

- **Doji**: Reflects indecision and potential reversal.

- **Pin Bar**: Represents price rejection with a long shadow, often signaling a reversal.

By combining these reversal patterns with the proximity to dinamic support or resistance levels, the strategy aims to capture potential reversal movements.

3. Sensitivity Level

- The sensitivity parameter adjusts the acceptable range (Default 0.018 = 1.8%) around support and resistance levels within which reversal patterns can trigger trades (i.e. the closing price of the candle must occur within the specified range defined by the sensitivity parameter). A higher sensitivity value expands this range, potentially leading to less accurate signals, as it may allow for more false positives.

4. Entry Criteria

- **Buy (Long)**: A Hammer, Doji, or Pin Bar pattern near support.

- **Sell (Short)**: A Shooting Star, Doji, or Pin Bar near resistance.

5. Exit criteria

- Take profit = 9.5%

- Stop loss = 16%

6. No Repainting

- The Price Action Strategy is not subject to repainting.

7. Position Sizing by Equity and risk management

- This strategy has a default configuration to operate with 35% of the equity. The stop loss is set to 16% from the entry price. This way, the strategy is putting at risk about 16% of 35% of equity, that is, around 5.6% of equity for each trade. The percentage of equity and stop loss can be adjusted by the user according to their risk management.

8. Backtest results

- This strategy was subjected to deep backtest and operations in replay mode on **1000000MOGUSDT.P**, with the inclusion of transaction fees at 0.12% and slipagge of 5 ticks, and the past results have shown consistent profitability. Past results are no guarantee of future results. The strategy's backtest results may even be due to overfitting with past data.

9. Chart Visualization

- Support and resistance levels are displayed as green (support) and red (resistance) lines.

- Only the candlestick pattern that generated the entry signal to triger the trade is identified and labeled on the chart. During the operation, the occurrence of new Doji, Pin Bar, Hammer and Shooting Star patterns will not be demonstrated on the chart, since the exit criteria are based on percentage take profit and stop loss.

Doji:

Pin Bar and Doji

Shooting Star and Doji

Hammer

10. Default settings

Chart timeframe: 20 min

Moving average lenght: 16

Sensitivity: 0.018

Stop loss (%): 16

Take Profit (%): 9.5

BYBIT:1000000MOGUSDT.P

Supertrend StrategyThe Supertrend Strategy was created based on the Supertrend and Relative Strength Index (RSI) indicators, widely respected tools in technical analysis. This strategy combines these two indicators to capture market trends with precision and reliability, looking for optimizing exit levels at oversold or overbought price levels.

The Supertrend indicator identifies trend direction based on price and volatility by using the Average True Range (ATR). The ATR measures market volatility by calculating the average range between an asset’s high and low prices over a set period. It provides insight into price fluctuations, with higher ATR values indicating increased volatility and lower values suggesting stability. The Supertrend Indicator plots a line above or below the price, signaling potential buy or sell opportunities: when the price closes above the Supertrend line, an uptrend is indicated, while a close below the line suggests a downtrend. This line shifts as price movements and volatility levels change, acting as both a trailing stop loss and trend confirmation.

To enhance the Supertrend strategy, the Relative Strength Index (RSI) has been added as an exit criterion. As a momentum oscillator, the RSI indicates overbought (usually above 70) or oversold (usually below 30) conditions. This integration allows trades to close when the asset is overbought or oversold, capturing gains before a possible reversal, even if the percentage take profit level has not been reached. This mechanism aims to prevent losses due to market reversals before the Supertrend signal changes.

### Key Features

1. **Entry criteria**:

- The strategy uses the Supertrend indicator calculated by adding or subtracting a multiple of the ATR from the closing price, depending on the trend direction.

- When the price crosses above the Supertrend line, the strategy signals a long (buy) entry. Conversely, when the price crosses below, it signals a short (sell) entry.

- The strategy performs a reversal if there is an open position and a change in the direction of the supertrend occurs

2. **Exit criteria**:

- Take profit of 30% (default) on the average position price.

- Oversold (≤ 5) or overbought (≥ 95) RSI

- Reversal when there is a change in direction of the Supertrend

3. **No Repainting**:

- This strategy is not subject to repainting, as long as the timeframe configured on your chart is the same as the supertrend timeframe .

4. **Position Sizing by Equity and risk management**:

- This strategy has a default configuration to operate with 35% of the equity. At the time of opening the position, the supertrend line is typically positioned at about 12 to 16% of the entry price. This way, the strategy is putting at risk about 16% of 35% of equity, that is, around 5.6% of equity for each trade. The percentage of equity can be adjusted by the user according to their risk management.

5. **Backtest results**:

- This strategy was subjected to deep backtesting and operations in replay mode, including transaction fees of 0.12%, and slippage of 5 ticks.

- The past results in deep backtest and replay mode were compatible and profitable (Variable results depending on the take profit used, supertrend and RSI parameters). However, it should be noted that few operations were evaluated, since the currency in question has been created for a short time and the frequency of operations is relatively small.

- Past results are no guarantee of future results. The strategy's backtest results may even be due to overfitting with past data.

Default Settings

Chart timeframe: 2h

Supertrend Factor: 3.42

ATR period: 14

Supertrend timeframe: 2 h

RSI timeframe: 15 min

RSI Lenght: 5 min

RSI Upper limit: 95

RSI Lower Limit: 5

Take Profit: 30%

BYBIT:1000000MOGUSDT.P

Wolfpack Elite - Liquidation Sniper - by 9123416916### Strategy: **Wolfpack Elite - Liquidation Sniper by Md Arif**

**Overview:**

This is a technical analysis strategy designed for trading, which combines two popular technical indicators: **Relative Strength Index (RSI)** and **Moving Averages (MA)**. It identifies potential buy (long) and sell (short) signals based on oversold and overbought conditions in the market, along with crossovers between two moving averages. The strategy also incorporates a risk management system by setting **take profit** and **stop loss** levels to protect against large losses and lock in gains.

---

**Key Components:**

1. **Indicators Used:**

- **RSI (Relative Strength Index):**

- Measures the speed and change of price movements.

- Used to identify **overbought** (above 70) and **oversold** (below 30) conditions.

- **Short and Long Moving Averages:**

- The strategy uses two simple moving averages (SMA) to detect trends and potential entry points.

- Short MA (9-period) and Long MA (21-period) are used for crossovers.

2. **Entry Signals:**

- **Bullish Entry (Long Position):**

- Triggered when the RSI falls below the oversold level (30) and the **short MA** crosses above the **long MA** (bullish crossover).

- This suggests that the market might be oversold and ready to rebound.

- **Bearish Entry (Short Position):**

- Triggered when the RSI rises above the overbought level (70) and the **short MA** crosses below the **long MA** (bearish crossover).

- This suggests that the market might be overbought and due for a correction.

3. **Risk Management:**

- **Take Profit and Stop Loss:**

- The strategy calculates the take profit and stop loss levels as percentages of the entry price.

- **Take Profit:** Set at 5% above the entry price for long positions and 5% below the entry price for short positions.

- **Stop Loss:** Set at 3% below the entry price for long positions and 3% above the entry price for short positions.

4. **Position Sizing:**

- The position size is calculated as a percentage of the trader's total equity (default set to 100% of equity).

5. **Exit Conditions:**

- **For Long Positions:**

- Exit the trade if the price hits the take profit level (5% above entry) or the stop loss level (3% below entry).

- **For Short Positions:**

- Exit the trade if the price hits the take profit level (5% below entry) or the stop loss level (3% above entry).

6. **Visualization:**

- The strategy visually plots the short and long moving averages on the chart.

- It also marks **bullish crossovers** with green upward triangles and **bearish crossovers** with red downward triangles, making it easier to spot potential entry points.

---

**How the Strategy Works:**

- The strategy starts by calculating the **RSI** and **moving averages**.

- It waits for specific conditions to trigger buy or sell signals. If the RSI indicates that the market is oversold and a bullish crossover occurs, it initiates a **long trade**. Similarly, if the RSI shows an overbought condition and a bearish crossover occurs, it opens a **short trade**.

- Once a trade is open, the strategy monitors the price and automatically exits the trade if the price reaches the set take profit or stop loss level.

---

This strategy is designed for active traders who seek to capitalize on short-term price movements and want clear entry/exit points with built-in risk management.

Ultimate Oscillator Trading StrategyThe Ultimate Oscillator Trading Strategy implemented in Pine Script™ is based on the Ultimate Oscillator (UO), a momentum indicator developed by Larry Williams in 1976. The UO is designed to measure price momentum over multiple timeframes, providing a more comprehensive view of market conditions by considering short-term, medium-term, and long-term trends simultaneously. This strategy applies the UO as a mean-reversion tool, seeking to capitalize on temporary deviations from the mean price level in the asset’s movement (Williams, 1976).

Strategy Overview:

Calculation of the Ultimate Oscillator (UO):

The UO combines price action over three different periods (short-term, medium-term, and long-term) to generate a weighted momentum measure. The default settings used in this strategy are:

Short-term: 6 periods (adjustable between 2 and 10).

Medium-term: 14 periods (adjustable between 6 and 14).

Long-term: 20 periods (adjustable between 10 and 20).

The UO is calculated as a weighted average of buying pressure and true range across these periods. The weights are designed to give more emphasis to short-term momentum, reflecting the short-term mean-reversion behavior observed in financial markets (Murphy, 1999).

Entry Conditions:

A long position is opened when the UO value falls below 30, indicating that the asset is potentially oversold. The value of 30 is a common threshold that suggests the price may have deviated significantly from its mean and could be due for a reversal, consistent with mean-reversion theory (Jegadeesh & Titman, 1993).

Exit Conditions:

The long position is closed when the current close price exceeds the previous day’s high. This rule captures the reversal and price recovery, providing a defined point to take profits.

The use of previous highs as exit points aligns with breakout and momentum strategies, as it indicates sufficient strength for a price recovery (Fama, 1970).

Scientific Basis and Rationale:

Momentum and Mean-Reversion:

The strategy leverages two well-established phenomena in financial markets: momentum and mean-reversion. Momentum, identified in earlier studies like those by Jegadeesh and Titman (1993), describes the tendency of assets to continue in their direction of movement over short periods. Mean-reversion, as discussed by Poterba and Summers (1988), indicates that asset prices tend to revert to their mean over time after short-term deviations. This dual approach aims to buy assets when they are temporarily oversold and capitalize on their return to the mean.

Multi-timeframe Analysis:

The UO’s incorporation of multiple timeframes (short, medium, and long) provides a holistic view of momentum, unlike single-period oscillators such as the RSI. By combining data across different timeframes, the UO offers a more robust signal and reduces the risk of false entries often associated with single-period momentum indicators (Murphy, 1999).

Trading and Market Efficiency:

Studies in behavioral finance, such as those by Shiller (2003), show that short-term inefficiencies and behavioral biases can lead to overreactions in the market, resulting in price deviations. This strategy seeks to exploit these temporary inefficiencies, using the UO as a signal to identify potential entry points when the market sentiment may have overly pushed the price away from its average.

Strategy Performance:

Backtests of this strategy show promising results, with profit factors exceeding 2.5 when the default settings are optimized. These results are consistent with other studies on short-term trading strategies that capitalize on mean-reversion patterns (Jegadeesh & Titman, 1993). The use of a dynamic, multi-period indicator like the UO enhances the strategy’s adaptability, making it effective across different market conditions and timeframes.

Conclusion:

The Ultimate Oscillator Trading Strategy effectively combines momentum and mean-reversion principles to trade on temporary market inefficiencies. By utilizing multiple periods in its calculation, the UO provides a more reliable and comprehensive measure of momentum, reducing the likelihood of false signals and increasing the profitability of trades. This aligns with modern financial research, showing that strategies based on mean-reversion and multi-timeframe analysis can be effective in capturing short-term price movements.

References:

Fama, E. F. (1970). Efficient Capital Markets: A Review of Theory and Empirical Work. The Journal of Finance, 25(2), 383-417.

Jegadeesh, N., & Titman, S. (1993). Returns to Buying Winners and Selling Losers: Implications for Stock Market Efficiency. The Journal of Finance, 48(1), 65-91.

Murphy, J. J. (1999). Technical Analysis of the Financial Markets: A Comprehensive Guide to Trading Methods and Applications. New York Institute of Finance.

Poterba, J. M., & Summers, L. H. (1988). Mean Reversion in Stock Prices: Evidence and Implications. Journal of Financial Economics, 22(1), 27-59.

Shiller, R. J. (2003). From Efficient Markets Theory to Behavioral Finance. Journal of Economic Perspectives, 17(1), 83-104.

Williams, L. (1976). Ultimate Oscillator. Market research and technical trading analysis.

VIDYA ProTrend Multi-Tier ProfitHello! This time is about a trend-following system.

VIDYA is quite an interesting indicator that adjusts dynamically to market volatility, making it more responsive to price changes compared to traditional moving averages. Balancing adaptability and precision, especially with the more aggressive short trade settings, challenged me to fine-tune the strategy for a variety of market conditions.

█ Introduction and How it is Different

The "VIDYA ProTrend Multi-Tier Profit" strategy is a trend-following system that combines the VIDYA (Variable Index Dynamic Average) indicator with Bollinger Bands and a multi-step take-profit mechanism.

Unlike traditional trend strategies, this system allows for more adaptive profit-taking, adjusting for long and short positions through distinct ATR-based and percentage-based targets. The innovation lies in its dynamic multi-tier approach to profit-taking, especially for short trades, where more aggressive percentages are applied using a multiplier. This flexibility helps adapt to various market conditions by optimizing trade management and profit allocation based on market volatility and trend strength.

BTCUSD 6hr performance

█ Strategy, How it Works: Detailed Explanation

The core of the "VIDYA ProTrend Multi-Tier Profit" strategy lies in the dual VIDYA indicators (fast and slow) that analyze price trends while accounting for market volatility. These indicators work alongside Bollinger Bands to filter trade entries and exits.

🔶 VIDYA Calculation

The VIDYA indicator is calculated using the following formula:

Smoothing factor (𝛼):

alpha = 2 / (Length + 1)

VIDYA formula:

VIDYA(t) = alpha * k * Price(t) + (1 - alpha * k) * VIDYA(t-1)

Where:

k = |Chande Momentum Oscillator (MO)| / 100

🔶 Bollinger Bands as a Volatility Filter

Bollinger Bands are calculated using a rolling mean and standard deviation of price over a specified period:

Upper Band:

BB_upper = MA + (K * stddev)

Lower Band:

BB_lower = MA - (K * stddev)

Where:

MA is the moving average,

K is the multiplier (typically 2), and

stddev is the standard deviation of price over the Bollinger Bands length.

These bands serve as volatility filters to identify potential overbought or oversold conditions, aiding in the entry and exit logic.

🔶 Slope Calculation for VIDYA

The slopes of both fast and slow VIDYAs are computed to assess the momentum and direction of the trend. The slope for a given VIDYA over its length is:

Slope = (VIDYA(t) - VIDYA(t-n)) / n

Where:

n is the length of the lookback period. Positive slope indicates bullish momentum, while negative slope signals bearish momentum.

LOCAL picture

🔶 Entry and Exit Conditions

- Long Entry: Occurs when the price moves above the slow VIDYA and the fast VIDYA is trending upward. Bollinger Bands confirm the signal when the price crosses the upper band, indicating bullish strength.

- Short Entry: Happens when the price drops below the slow VIDYA and the fast VIDYA trends downward. The signal is confirmed when the price crosses the lower Bollinger Band, showing bearish momentum.

- Exit: Based on VIDYA slopes flattening or reversing, or when the price hits specific ATR or percentage-based profit targets.

🔶 Multi-Step Take Profit Mechanism

The strategy incorporates three levels of take profit for both long and short trades:

- ATR-based Take Profit: Each step applies a multiple of the ATR (Average True Range) to the entry price to define the exit point.

The first level of take profit (long):

TP_ATR1_long = Entry Price + (2.618 * ATR)

etc.

█ Trade Direction

The strategy offers flexibility in defining the trading direction:

- Long: Only long trades are considered based on the criteria for upward trends.

- Short: Only short trades are initiated in bearish trends.

- Both: The strategy can take both long and short trades depending on the market conditions.

█ Usage

To use the strategy effectively:

- Adjust the VIDYA lengths (fast and slow) based on your preference for trend sensitivity.

- Use Bollinger Bands as a filter for identifying potential breakout or reversal scenarios.

- Enable the multi-step take profit feature to manage positions dynamically, allowing for partial exits as the price reaches specified ATR or percentage levels.

- Leverage the short trade multiplier for more aggressive take profit levels in bearish markets.

This strategy can be applied to different asset classes, including equities, forex, and cryptocurrencies. Adjust the input parameters to suit the volatility and characteristics of the asset being traded.

█ Default Settings

The default settings for this strategy have been designed for moderate to trending markets:

- Fast VIDYA Length (10): A shorter length for quick responsiveness to price changes. Increasing this length will reduce noise but may delay signals.

- Slow VIDYA Length (30): The slow VIDYA is set longer to capture broader market trends. Shortening this value will make the system more reactive to smaller price swings.

- Minimum Slope Threshold (0.05): This threshold helps filter out weak trends. Lowering the threshold will result in more trades, while raising it will restrict trades to stronger trends.

Multi-Step Take Profit Settings

- ATR Multipliers (2.618, 5.0, 10.0): These values define how far the price should move before taking profit. Larger multipliers widen the profit-taking levels, aiming for larger trend moves. In higher volatility markets, these values might be adjusted downwards.

- Percentage Levels (3%, 8%, 17%): These percentage levels define how much the price must move before taking profit. Increasing the percentages will capture larger moves, while smaller percentages offer quicker exits.

- Short TP Multiplier (1.5): This multiplier applies more aggressive take profit levels for short trades. Adjust this value based on the aggressiveness of your short trade management.

Each of these settings directly impacts the performance and risk profile of the strategy. Shorter VIDYA lengths and lower slope thresholds will generate more trades but may result in more whipsaws. Higher ATR multipliers or percentage levels can delay profit-taking, aiming for larger trends but risking partial gains if the trend reverses too early.

Adaptive MA Scalping StrategyAdaptive MA Scalping Strategy

The Adaptive MA Scalping Strategy is an innovative trading approach that merges the strengths of the Kaufman's Adaptive Moving Average (KAMA) with the Moving Average Convergence Divergence (MACD) histogram. This combination results in a momentum-adaptive moving average that dynamically adjusts to market conditions, providing traders with timely and reliable signals.

How It Works