Standard Deviation Models

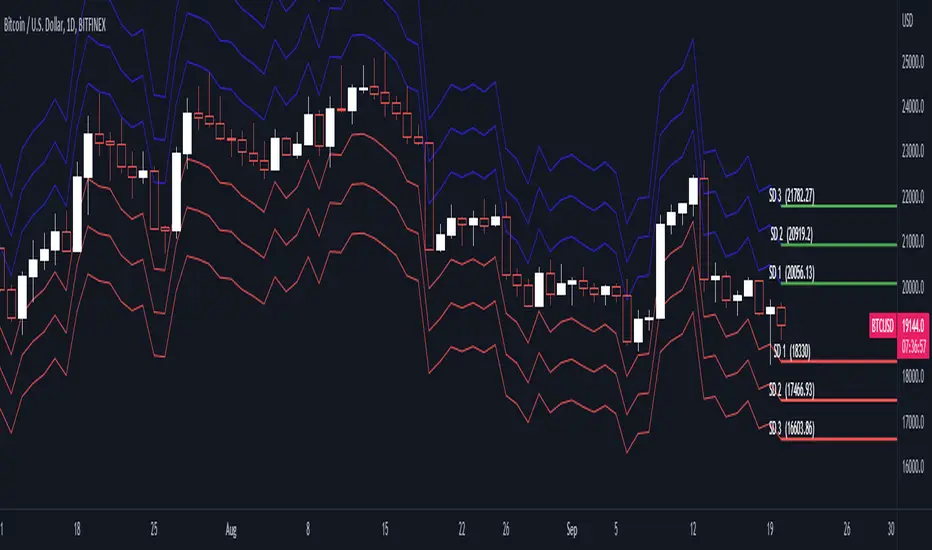

The standard deviation model can be used for options traders that are selling options contracts to collect a premium to identify a specific range of strike prices which are optimal for selling based on the underlying asset’s historical price fluctuations. Traders will be able to identify the statistical likelihood that their options contract will be in the money (ITM) or out of the money (OTM).

Basic statistics of normal distributions (probability curve):

-1 SD to +1 SD = 68% likelihood

-2 SD to + 2 SD = 95% likelihood

-3 SD to +3 SD = 99% likelihood

The standard deviation model can be used for options traders that are selling options contracts to collect a premium to identify a specific range of strike prices which are optimal for selling based on the underlying asset’s historical price fluctuations. Traders will be able to identify the statistical likelihood that their options contract will be in the money ( ITM ) or out of the money (OTM).

Basic statistics of normal distributions (probability curve):

-1 SD to +1 SD = 68% likelihood

-2 SD to + 2 SD = 95% likelihood

-3 SD to +3 SD = 99% likelihood

סקריפט להזמנה בלבד

רק משתמשים שאושרו על ידי המחבר יכולים לגשת לסקריפט הזה. יהיה עליך לשלוח בקשת גישה ולקבל אישור לשימוש. בדרך כלל, הגישה ניתנת לאחר תשלום. למידע נוסף, עקוב אחר ההוראות של היוצר בהמשך או צור קשר עם ProfessorSatoshi ישירות.

TradingView לא ממליצה לשלם עבור סקריפט או להשתמש בו אלא אם כן אתה סומך לחלוטין על המחבר שלו ומבין כיצד הוא פועל. ייתכן שתוכל גם למצוא חלופות חינמיות וקוד פתוח ב-סקריפטים הקהילתיים שלנו.

הוראות המחבר

כתב ויתור

סקריפט להזמנה בלבד

רק משתמשים שאושרו על ידי המחבר יכולים לגשת לסקריפט הזה. יהיה עליך לשלוח בקשת גישה ולקבל אישור לשימוש. בדרך כלל, הגישה ניתנת לאחר תשלום. למידע נוסף, עקוב אחר ההוראות של היוצר בהמשך או צור קשר עם ProfessorSatoshi ישירות.

TradingView לא ממליצה לשלם עבור סקריפט או להשתמש בו אלא אם כן אתה סומך לחלוטין על המחבר שלו ומבין כיצד הוא פועל. ייתכן שתוכל גם למצוא חלופות חינמיות וקוד פתוח ב-סקריפטים הקהילתיים שלנו.