OPEN-SOURCE SCRIPT

3HMA

Introduction

The Hull smoothing method aim to reduce the lag of a moving average by using a simple calculation involving smoothing with a moving average of period √p the subtraction of a moving average of period p/2 multiplied by 2 with another moving average of period p, however it is possible to extend this calculation by introducing more terms thus reducing both the lag and overshoot of the classical HMA.

Comparison

The proposed filter add 1 more term to the classical hull moving average thus ending with : sma(sma(p/3) * 3 - sma(p/2) - sma(p),p), this can be developed as long as every terms add to total unity, more terms will often require more smoothing, this is why i replace √p by p.

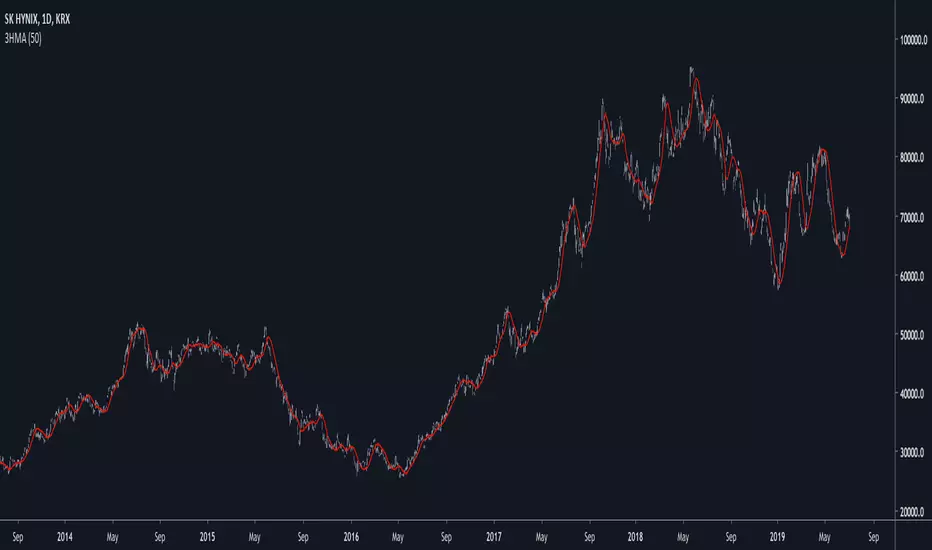

In blue a HMA and in red the proposed filter of both period 50. The third term added allow for more reactivity which sometimes allow for overshoots with lower amplitudes.

Conclusions

Adding more terms to certain filtering methods can correct certain behaviours as well as reducing lag or increasing smoothing.

The Hull smoothing method aim to reduce the lag of a moving average by using a simple calculation involving smoothing with a moving average of period √p the subtraction of a moving average of period p/2 multiplied by 2 with another moving average of period p, however it is possible to extend this calculation by introducing more terms thus reducing both the lag and overshoot of the classical HMA.

Comparison

The proposed filter add 1 more term to the classical hull moving average thus ending with : sma(sma(p/3) * 3 - sma(p/2) - sma(p),p), this can be developed as long as every terms add to total unity, more terms will often require more smoothing, this is why i replace √p by p.

In blue a HMA and in red the proposed filter of both period 50. The third term added allow for more reactivity which sometimes allow for overshoots with lower amplitudes.

Conclusions

Adding more terms to certain filtering methods can correct certain behaviours as well as reducing lag or increasing smoothing.

סקריפט קוד פתוח

ברוח האמיתית של TradingView, יוצר הסקריפט הזה הפך אותו לקוד פתוח, כך שסוחרים יוכלו לעיין בו ולאמת את פעולתו. כל הכבוד למחבר! אמנם ניתן להשתמש בו בחינם, אך זכור כי פרסום חוזר של הקוד כפוף ל־כללי הבית שלנו.

Check out the indicators we are making at luxalgo: tradingview.com/u/LuxAlgo/

"My heart is so loud that I can't hear the fireworks"

"My heart is so loud that I can't hear the fireworks"

כתב ויתור

המידע והפרסומים אינם מיועדים להיות, ואינם מהווים, ייעוץ או המלצה פיננסית, השקעתית, מסחרית או מכל סוג אחר המסופקת או מאושרת על ידי TradingView. קרא עוד ב־תנאי השימוש.

סקריפט קוד פתוח

ברוח האמיתית של TradingView, יוצר הסקריפט הזה הפך אותו לקוד פתוח, כך שסוחרים יוכלו לעיין בו ולאמת את פעולתו. כל הכבוד למחבר! אמנם ניתן להשתמש בו בחינם, אך זכור כי פרסום חוזר של הקוד כפוף ל־כללי הבית שלנו.

Check out the indicators we are making at luxalgo: tradingview.com/u/LuxAlgo/

"My heart is so loud that I can't hear the fireworks"

"My heart is so loud that I can't hear the fireworks"

כתב ויתור

המידע והפרסומים אינם מיועדים להיות, ואינם מהווים, ייעוץ או המלצה פיננסית, השקעתית, מסחרית או מכל סוג אחר המסופקת או מאושרת על ידי TradingView. קרא עוד ב־תנאי השימוש.