Strategy with VWRSI and SAVE orders Long or Short or BothVWRSI is very powerful indicator coded by Algo Alpha and I Make Strategy of it

But there is no stop loss instate the Strategy is using Save orders to minimize the market manipulation

The best to used is side way market with long and short enable

The Strategy trigger long or short market order -

long - ta.crossover(rsi, 20)

short - ta.crossunder(rsi, 80)

And if is not take profit from the first trade start with the save trades until will do

the sum of the first order - base order and the save order can be adjust from the user

as well the deviation from the first order

IF some user have questions let me know

מחזורים

Capitulation Detector StrategyA multi-factor capitulation detector designed to identify exhaustion points in extended trends. It focuses on fading capitulation moves after multi-leg trends with extreme volume and price extension.

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

THE CONCEPT

Capitulation occurs when the last holders give up — panic selling into lows or euphoric buying into highs. These moments create asymmetric opportunities because:

Sentiment becomes maximally skewed

Weak hands are flushed out

Price deviates far from equilibrium

The "fuel" for continuation is exhausted

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

THE 6 FACTORS

Trend Persistence — Price stays on one side of 38 EMA for 12+ bars, confirming a sustained directional move

Acceleration — Price stays on one side of 5 EMA for 3+ bars, showing the move is accelerating into exhaustion

Volume Spike — Current bar volume ≥ 2x the 20-bar average

Body Expansion — Candle body ≥ 1.5x average, showing conviction/panic in the move

Extension — Price is 2+ ATR away from the 38 EMA, indicating overextension from equilibrium

Multi-Leg Structure — At least 3 consecutive lower lows (for longs) or higher highs (for shorts)

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

SIGNAL LOGIC

Bullish Capitulation: 4+ factors align + price below 38 EMA + down candle + volume spike

Bearish Capitulation: 4+ factors align + price above 38 EMA + up candle + volume spike

The strategy enters counter-trend, fading the exhaustion move.

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

EXIT OPTIONS

ATR-based stop loss (default: 2 ATR)

ATR-based take profit (default: 3 ATR)

Optional trailing stop

Time filter for session-specific trading

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

BEST PRACTICES

Works best on liquid instruments with clean trends

More reliable after 3+ legs in the trend

Higher conviction when daily AND intraday timeframes align

"The bigger and more extended, the better"

Consider VWAP as additional confirmation (not coded here)

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

SETTINGS GUIDE

Min Score: Increase for fewer, higher-quality signals

Volume Spike Multiplier: 2x; increase for stricter filter

Extension ATR: Higher values = more overextended setups only

Trend Bars Min: Higher values = longer established trends required

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

ALERTS

Bullish Capitulation (potential long)

Bearish Capitulation (potential short)

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

DISCLAIMER

This is a counter-trend strategy — inherently higher risk than trend-following. Always use proper position sizing and risk management. Backtest thoroughly on your specific instruments and timeframes.

Multi-MA + RSI Pullback Strategy (Jordan)1️⃣ Strategy logic I’ll code

From your screenshots:

Indicators

• EMAs: 600 / 200 / 100 / 50

• RSI: length 6, levels 80 / 20

Rules (simplified so a script can handle them):

• Use a higher-timeframe trend filter (15m or 1h) using the EMAs.

• Take entries on the chart timeframe (you can use 1m or 5m).

• Long:

• Higher-TF trend is up.

• Price is pulling back into a zone (between 50 EMA and 100 EMA on the entry timeframe – this approximates your 50–61% retrace).

• RSI crosses below 20 (oversold).

• Short:

• Higher-TF trend is down.

• Price pulls back between 50 & 100 EMAs.

• RSI crosses above 80 (overbought).

• Exits: ATR-based stop + take-profit with adjustable R:R (2:1 or 3:1).

• Max 4 trades per day.

News filter & “only trade gold” you handle manually (run it on XAUUSD and avoid news times yourself – TradingView can’t read the economic calendar from code).

Cerber Strategy ETH/BTC Cerber Strategy: High-Precision Crypto Trend Follower

The Cerber Strategy is a low-frequency, high-conviction trend following system designed to capture massive quarterly crypto moves while

filtering out 90% of consolidation noise. It combines a momentum-based "Sniper Entry" (entering only on verified breakouts) with a

"Trend Confirmation" filter (Weekly DEMA) to ensure capital is only deployed during macro bull runs.

Usage:

* Timeframe: Daily (1D) mandatory.

* Assets: Optimized for BTC and ETH, works on high-volatility alts.

* Style: Position Trading (holding for weeks/months).

* Risk: Extremely high efficiency (high Profit Factor), very low drawdown compared to Buy & Hold. Perfect for a "Set and Forget"

portfolio allocation.

SMC Pro [Stansbooth]

🔮 SMC × Fibonacci Confluence Engine — The Hidden Algorithm of the Markets

Welcome to a level of chart analysis where mathematics , market psychology , and institutional logic merge into one ultra-intelligent system.

This indicator decodes the true structure of price delivery by combining Smart Money Concepts with the timeless precision of Fibonacci ratios , revealing what retail traders can’t see — *the algorithmic heartbeat of the market*.

✨ What Makes This Indicator Different

Instead of drawing random lines or reacting to late signals, this tool **anticipates** market behavior by reading the footprints left behind by institutional algorithms. Every element is placed with purpose — every zone, every shift, every fib level — all forming a seamless narrative that explains *why* price moves the way it does.

🔥 Core Intelligence Features

Advanced BOS/CHOCH Auto-Detection — Spot structure shifts before momentum even forms.

Institutional Liquidity Mapping

— Identify liquidity pools, engineered sweeps, equal highs/lows, and trap zones designed by smart money.

Fibonacci-Aligned Precision Zones

— Auto-generated fib grids synced with SMC levels for pinpoint reversal and continuation setups.

Imbalance Engine

— FVGs, displacement, inefficiencies, and mitigation blocks displayed with crystal clarity.

Premium/Discount Algorithm

— Understand instantly whether price is in a zone of accumulation or distribution.

🚀 Designed for Traders Who Want an Edge

Whether you're scalping fast moves, capturing intraday swings, or holding higher-timeframe plays, this indicator provides a professional lens into the market. It turns complex price action into a structured, predictable system where every move has logic and every entry has confluence.

You don’t just see the chart —

you see the intention behind every push, pull, manipulation, and reversal.

💎 Why It Feels Like a Cheat Code

Because it mirrors the way institutions analyze the market:

— Identify liquidity

— Seek equilibrium

— Deliver price

— Create inefficiency

— Mitigate

— Continue the narrative

Using SMC and Fibonacci together unlocks the “algorithmic geometry” behind price movement, giving you clarity where others see chaos.

⚡ Trade With Confidence, Confluence & Control

This indicator isn’t just a tool.

It’s a complete trading framework — structured, intelligent, and deadly accurate.

Master the markets.

Decode the algorithm.

Trade like smart money .

Strategia S&P 500 vs US10Y YieldThis strategy explores the macroeconomic relationship between the equity market (S&P 500) and the debt market (10-Year Treasury Yield). Historically, rapid spikes in bond yields often exert downward pressure on equity valuations, leading to corrections or bear markets.

The goal of this strategy is capital preservation. It attempts to switch to cash when yields are rising too aggressively and re-enter the stock market when the bond market stabilizes.

Elliott Wave Full Fractal System v2.0Elliott Wave Full Fractal System v2.0 – Q.C. FINAL (Guaranteed R/R)

Elliott Wave Full Fractal System is a multi-timeframe wave engine that automatically labels Elliott impulses and ABC corrections, then builds a rule-based, ATR-driven risk/reward framework around the “W3–W4–W5” leg.

“Guaranteed R/R” here means every order is placed with a predefined stop-loss and take-profit that respect a minimum Reward:Risk ratio – it does not mean guaranteed profits.

Core Idea

This strategy turns a full fractal Elliott Wave labelling engine into a systematic trading model.

It scans fractal pivots on three wave degrees (Primary, Intermediate, Minor) to detect 5-wave impulses and ABC corrections.

A separate “Trading Degree” pivot stream, filtered by a 200-EMA trend filter and ATR-based dynamic pivots, is then used to find W4 pullback entries with a minimum, user-defined Reward:Risk ratio.

Default Properties & Risk Assumptions

The backtest uses realistic but conservative defaults:

// Default properties used for backtesting

strategy(

"Elliott Wave Full Fractal System - Q.C. FINAL (Guaranteed R/R)",

overlay = true,

initial_capital = 10000, // realistic account size

default_qty_type = strategy.percent_of_equity,

default_qty_value = 1, // 1% risk per trade

commission_type = strategy.commission.cash_per_contract,

commission_value = 0.005, // example stock commission

slippage = 0 // see notes below

)

Account size: 10,000 (can be changed to match your own account).

Position sizing: 1% of equity per trade to keep risk per idea sustainable and aligned with TradingView’s recommendations.

Commission: 0.005 cash per contract/share as a realistic example for stock trading.

Slippage: set to 0 in code for clarity of “pure logic” backtesting. Real-life trading will experience slippage, so users should adjust this according to their market and broker.

Always re-run the backtest after changing any of these values, and avoid using high risk fractions (5–10%+) as that is rarely sustainable.

1. Full Fractal Wave Engine

The script builds and maintains four pivot streams using ATR-adaptive fractals:

Primary Degree (Macro Trend):

Captures the large swings that define the major trend. Labels ①–⑤ and ⒶⒷⒸ using blue “Circle” labels and thicker lines.

Intermediate Degree (Trading Degree):

Captures the medium swings (swing-trading horizon). Uses teal labels ( (1)…(5), (A)(B)(C) ).

Minor Degree (Micro Structure):

Tracks short-term swings inside the larger waves. Uses red roman numerals (i…v, a b c).

ABC Corrections (Optional):

When enabled, the engine tries to detect standard A–B–C corrective structures that follow a completed 5-wave impulse and plots them with dashed lines.

Each degree uses a dynamic pivot lookback that expands when ATR is above its EMA, so the system naturally requires “stronger” pivots in volatile environments and reacts faster in quiet conditions.

2. Theory Rules & Strict Mode

Normal Mode: More permissive detection. Designed to show more wave structures for educational / exploratory use.

Strict Mode: Enforces key Elliott constraints:

Wave 3 not shorter than waves 1 and 5.

No invalid W4 overlap with W1 (for standard impulses).

ABC Logic: After a confirmed bullish impulse, the script expects a down-up-down corrective pattern (A,B,C). After a bearish impulse, it looks for up-down-up.

3. Trend Filter & Pivots

EMA Trend Filter: A configurable EMA (default 200) is used as a non-wave trend filter.

Price above EMA → Only long setups are considered.

Price below EMA → Only short setups are considered.

ATR-Adaptive Pivots: The pivot engine scales its left/right bars based on current ATR vs ATR EMA, making waves and trading pivots more robust in volatile regimes.

4. Dynamic Risk Management (Guaranteed R/R Engine)

The trading engine is designed around risk, not just pattern recognition:

ATR-Based Stop:

Stop-loss is placed at:

Entry ± ATR × Multiplier (user-configurable, default 2.0).

This anchors risk to current volatility.

Minimum Reward:Risk Ratio:

For each setup, the script:

Computes the distance from entry to stop (risk).

Projects a take-profit target at risk × min_rr_ratio away from entry.

Only accepts the setup if risk is positive and the required R:R ratio is achievable.

Result: Every order is created with both TP and SL at a predefined distance, so each trade starts with a known, minimum Reward:Risk profile by design.

“Guaranteed R/R” refers exclusively to this order placement logic (TP/SL geometry), not to win-rate or profitability.

5. Trading Logic – W3–W4–W5 Pattern

The Trading pivot stream (separate from visual wave degrees) looks for a simple but powerful pattern:

Bullish structure:

Sequence of pivots forms a higher-high / higher-low pattern.

Price is above the EMA trend filter.

A strong “W3” leg is confirmed with structure rules (optionally stricter in Strict mode).

Entry (Long – W4 Pullback):

The “height” of W3 is measured.

Entry is placed at a configurable Fibonacci pullback (default 50%) inside that leg.

ATR-based stop is placed below entry.

Take-profit is projected to satisfy min Reward:Risk.

Bearish structure:

Mirrored logic (lower highs/lows, price below EMA, W3 down, W4 retrace up, W5 continuation down).

Once a valid setup is found, the script draws a colored box around the entry zone and a label describing the type of signal (“LONG SETUP” or “SHORT SETUP”) with the suggested limit price.

6. Orders & Execution

Entry Orders: The strategy uses limit orders at the computed W4 level (“Sniper Long” or “Sniper Short”).

Exits: A single strategy.exit() is attached to each entry with:

Take-profit at the projected minimum R:R target.

Stop-loss at ATR-based level.

One Trade at a Time: New setups are only used when there is no open position (strategy.opentrades == 0) to keep the logic clear and risk contained.

7. Visual Guide on the Chart

Wave Labels:

Primary: ①,②,③,④,⑤, ⒶⒷⒸ

Intermediate: (1)…(5), (A)(B)(C)

Minor: i…v, a b c

Trend EMA: Single blue EMA showing the dominant trend.

Setup Boxes:

Green transparent box → long entry zone.

Red transparent box → short entry zone.

Labels: “LONG SETUP / SHORT SETUP” labels mark the proposed limit entry with price.

8. How to Use This Strategy

Attach the strategy to your chart

Choose your market (stocks, indices, FX, crypto, futures, etc.) and timeframe (for example 1h, 4h, or Daily). Then add the strategy to the chart from your Scripts list.

Start with the default settings

Leave all inputs on their defaults first. This lets you see the “intended” behaviour and the exact properties used for the published backtest (account size, 1% risk, commission, etc.).

Study the wave map

Zoom in and out and look at the three wave degrees:

Blue circles → Primary degree (big picture trend).

Teal (1)…(5) → Intermediate degree (swing structure).

Red i…v → Minor degree (micro waves).

Use this to understand how the engine is interpreting the Elliott structure on your symbol.

Watch for valid setups

Look for the coloured boxes and labels:

Green box + “LONG SETUP” label → potential W4 pullback long in an uptrend.

Red box + “SHORT SETUP” label → potential W4 pullback short in a downtrend.

Only trades in the direction of the EMA trend filter are allowed by the strategy.

Check the Reward:Risk of each idea

For each setup, inspect:

Limit entry price.

ATR-based stop level.

Projected take-profit level.

Make sure the minimum Reward:Risk ratio matches your own rules before you consider trading it.

Backtest and evaluate

Open the Strategy Tester:

Verify you have a decent sample size (ideally 100+ trades).

Check drawdowns, average trade, win-rate and R:R distribution.

Change markets and timeframes to see where the logic behaves best.

Adapt to your own risk profile

If you plan to use it live:

Set Initial Capital to your real account size.

Adjust default_qty_value to a risk level you are comfortable with (often 0.5–2% per trade).

Set commission and slippage to realistic broker values.

Re-run the backtest after every major change.

Use as a framework, not a signal machine

Treat this as a structured Elliott/R:R framework:

Filter signals by higher-timeframe trend, major S/R, volume, or fundamentals.

Optionally hide some wave degrees or ABC labels if you want a cleaner chart.

Combine the system’s structure with your own trade management and discretion.

Best Practices & Limitations

This is an approximate Elliott Wave engine based on fractal pivots. It does not replace a full discretionary Elliott analysis.

All wave counts are algorithmic and can differ from a manual analyst’s interpretation.

Like any backtest, results depend heavily on:

Symbol and timeframe.

Sample size (more trades are better).

Realistic commission/slippage settings.

The 0-slippage default is chosen only to show the “raw logic”. In real markets, slippage can significantly impact performance.

No strategy wins all the time. Losing streaks and drawdowns will still occur even with a strict R:R framework.

Disclaimer

This script is for educational and research purposes only and does not constitute financial advice or a recommendation to buy or sell any security. Past performance, whether real or simulated, is not indicative of future results. Always test on multiple symbols/timeframes, use conservative risk, and consult your financial advisor before trading live capital.

Keltner Channels Strategy NewThe strategy is chenging the same as an original copy, but this one is for tests, so I will publish it and check results

Trend Flow & Breakout Professional [Strategy]Description:

🌪️ Overview

Stop guessing. Start following the flow.

The Trend Flow & Breakout Professional is a high-precision visual trading system designed to solve the biggest problem traders face: Choppy Markets & Fakeouts.

Instead of relying on lagging indicators that generate false signals, this engine uses a proprietary "Momentum Alignment Algorithm" to identify when price action is entering a genuine expansion phase. It transforms complex trend data into a clean, easy-to-read visual roadmap, allowing you to catch the meat of the move while filtering out the noise.

🔮 Key Features

1. The "Traffic Light" Visual System Trading is 90% psychology. This script reduces mental fatigue by coloring the chart background to reflect the dominant market state:

🟢 Green Zone (Bullish Flow): Momentum is accelerating upwards. The system suggests holding long positions and ignoring minor pullbacks.

🔴 Red Zone (Bearish Flow): Structure has broken down. The system suggests defensive measures or short entries.

Note: The background remains active as long as the trend structure holds, preventing you from exiting trades too early.

2. Smart Noise Filtering Unlike standard crossover strategies that get destroyed in sideways ranges, this system includes a Multi-Layer Trend Filter. It only triggers a signal when:

Short-term momentum aligns perfectly with the medium-term direction.

Volatility expands significantly (breakout confirmation).

Price successfully clears key long-term structural resistance (The "Blue Sky" Zone).

3. Built-in "Smart Strategy" Backtester We have integrated a professional-grade position management module. You can customize how the strategy executes trades in the settings:

Mode A: Sniper (Trend Reversal): Enters heavily on the first confirmed breakout and holds until the trend reverses. Ideal for swing traders.

Mode B: Builder (Pyramiding): Adds to the position incrementally as the trend confirms its strength, maximizing profit during strong runs.

4. Cooldown Mechanism To prevent over-trading, the algorithm includes a smart "Cooldown Period" that prevents signal spamming during high-volatility consolidations.

⚙️ How to Trade This System

Wait for the Signal:

Look for the "Buy" / "Sell" labels accompanied by a bright Neon Candle.

Ensure the background color shifts (e.g., from Grey/Red to Green).

Ride the Zone:

Do not exit just because of one red candle. As long as the Background remains Green, the trend is healthy.

The background color acts as your "psychological anchor," helping you let profits run.

Exit / Reversal:

A complete background color flip (e.g., Green to Red) indicates a structural trend failure. This is your signal to close positions or flip directions.

⚠️ Disclaimer

This tool is for educational and technical analysis purposes only. Past performance does not guarantee future results. Always use proper risk management.

N1E_UTBOATN1E_UTBOAT

ATR trailing stop

Optional Heikin Ashi source

Buy/Sell signals based on a crossover of price vs ATR trailing stop

Strategy long/short entries

小諾的Lazy Bot這是個市場上所有人都懂得邏輯

指標往往是越簡單越好

只做高勝率的順勢交易,並利用指標幫我們克服人性的恐懼與貪婪。

風險免責聲明

過往績效不代表未來表現。請務必先在模擬倉進行回測與熟悉。

此腳本僅供輔助與學習使用,不構成任何投資建議 。

建議配合自身的風險管理使用。

Strategy Philosophy The logic behind this strategy is universal and widely understood: often, the simpler the indicator, the better. We focus exclusively on high-probability trend-following trades, using this indicator to help us overcome human fear and greed.

Risk Disclaimer

Past performance is not indicative of future results. Please ensure you backtest and familiarize yourself with the script in a demo account first.

This script is provided for educational and assistive purposes only and does not constitute investment advice .

It is strongly recommended to use this tool in conjunction with your own risk management strategies.

2026 CHRISTMAS PRESENT CHRISTMAS PRESENT

Overview

The Cash Detector is a comprehensive trading strategy that combines momentum analysis with price action confirmation to identify high-probability entry points. This strategy is designed to capture trend reversals and continuation moves by requiring multiple confirming signals before entry, significantly reducing false signals common in single-indicator systems.

Strategy Background

The strategy is built on the principle of confluence trading requiring multiple technical factors to align before taking a position. It focuses on two critical phases of market rotation:

Q2 Momentum Phase: Uses MACD crossovers to identify shifts in market momentum, signaling when bulls or bears are gaining control.

Q4 Trigger Phase: Employs engulfing candlestick patterns to confirm strong directional pressure and validate the momentum signal with actual price action.

By combining these elements, the strategy filters out weak signals and focuses only on setups where both momentum AND price action agree on direction.

Key Features

Dual Confirmation System: Requires both MACD momentum shift and engulfing candle pattern

RSI Filter: Optional overbought/oversold filter to avoid extreme conditions

Built-in Risk Management: Configurable stop loss and take profit levels

Performance Dashboard: Real-time ROI metrics displayed on chart

Full Backtesting: Strategy mode allows historical performance analysis

Trading Rules

LONG ENTRY BUY

All conditions must occur on the same candle:

1. Momentum Confirmation:

MACD line crosses above signal line bullish crossover

2. Price Action Confirmation:

Bullish engulfing pattern forms:

Current close greater than previous open

Current open less than previous close

Current close greater than current open

3. RSI Filter Optional:

RSI less than 70 not overbought

Visual Signal: Green LONG label appears below the candle

SHORT ENTRY SELL

All conditions must occur on the same candle:

1. Momentum Confirmation:

MACD line crosses below signal line bearish crossover

2. Price Action Confirmation:

Bearish engulfing pattern forms:

Current close less than previous open

Current open greater than previous close

Current close less than current open

3. RSI Filter Optional:

RSI greater than 30 not oversold

Visual Signal: Red SHORT label appears above the candle

Exit Rules

Stop Loss Default 2 percent

Long: Exit if price drops 2 percent below entry

Short: Exit if price rises 2 percent above entry

Take Profit Default 4 percent

Long: Exit if price rises 4 percent above entry

Short: Exit if price drops 4 percent below entry

Input Parameters

Indicator Settings

MACD Fast Length: 12 default

MACD Slow Length: 26 default

RSI Length: 14 default

Risk Management

Use Stop Loss: Enable or disable stop loss

Stop Loss percent: Percentage risk per trade default 2 percent

Use Take Profit: Enable or disable take profit

Take Profit percent: Target profit per trade default 4 percent

Filters

Use RSI Filter: Enable or disable RSI overbought oversold filter

RSI Overbought: Upper threshold default 70

RSI Oversold: Lower threshold default 30

Performance Metrics

The built-in dashboard displays:

Net Profit: Total profit loss in currency and percentage

Total Trades: Number of completed trades

Win Rate: Percentage of profitable trades

Profit Factor: Ratio of gross profit to gross loss

Average Win Loss: Mean profit per winning losing trade

Max Drawdown: Largest peak to trough decline

Best Practices

1. Timeframe Selection: Works on multiple timeframes test on 15min 1H 4H and daily

2. Market Conditions: Most effective in trending markets with clear momentum

3. Risk Reward Ratio: Default 1:2 ratio 2 percent risk 4 percent reward is conservative adjust based on backtesting

4. Combine with Context: Consider overall market trend and support resistance levels

5. Backtest First: Always backtest on your specific instrument and timeframe before live trading

Risk Disclaimer

This strategy is for educational purposes. Past performance does not guarantee future results. Always:

Backtest thoroughly on historical data

Paper trade before using real capital

Use proper position sizing and risk management

Never risk more than you can afford to lose

Customization Tips

Aggressive traders: Reduce stop loss to 1.5 percent increase take profit to 5 percent

Conservative traders: Increase stop loss to 3 percent reduce take profit to 3 percent

Ranging markets: Enable RSI filter to avoid false breakouts

Strong trends: Disable RSI filter to catch all momentum shifts

Technical Details

Indicators Used:

Moving Average Convergence Divergence MACD

Relative Strength Index RSI

Candlestick Pattern Recognition

Strategy Type: Trend following with momentum confirmation

Best Suited For: Stocks Forex Crypto Indices

Version 1.0

Compatible with Pine Script v5

ALT Risk Metric StrategyHere's a professional write-up for your ALT Risk Strategy script:

ALT/BTC Risk Strategy - Multi-Crypto DCA with Bitcoin Correlation Analysis

Overview

This strategy uses Bitcoin correlation as a risk indicator to time entries and exits for altcoins. By analyzing how your chosen altcoin performs relative to Bitcoin, the strategy identifies optimal accumulation periods (when alt/BTC is oversold) and profit-taking opportunities (when alt/BTC is overbought). Perfect for traders who want to outperform Bitcoin by strategically timing altcoin positions.

Key Innovation: Why Alt/BTC Matters

Most traders focus solely on USD price, but Alt/BTC ratios reveal true altcoin strength:

When Alt/BTC is low → Altcoin is undervalued relative to Bitcoin (buy opportunity)

When Alt/BTC is high → Altcoin has outperformed Bitcoin (take profits)

This approach captures the rotation between BTC and alts that drives crypto cycles

Key Features

📊 Advanced Technical Analysis

RSI (60% weight): Primary momentum indicator on weekly timeframe

Long-term MA Deviation (35% weight): Measures distance from 150-period baseline

MACD (5% weight): Minor confirmation signal

EMA Smoothing: Filters noise while maintaining responsiveness

All calculations performed on Alt/BTC pairs for superior market timing

💰 3-Tier DCA System

Level 1 (Risk ≤ 70): Conservative entry, base allocation

Level 2 (Risk ≤ 50): Increased allocation, strong opportunity

Level 3 (Risk ≤ 30): Maximum allocation, extreme undervaluation

Continuous buying: Executes every bar while below threshold for true DCA behavior

Cumulative sizing: L3 triggers = L1 + L2 + L3 amounts combined

📈 Smart Profit Management

Sequential selling: Must complete L1 before L2, L2 before L3

Percentage-based exits: Sell portions of position, not fixed amounts

Auto-reset on re-entry: New buy signals reset sell progression

Prevents premature full exits during volatile conditions

🤖 3Commas Automation

Pre-configured JSON webhooks for Custom Signal Bots

Multi-exchange support: Binance, Coinbase, Kraken, Bitfinex, Bybit

Flexible quote currency: USD, USDT, or BUSD

Dynamic order sizing: Automatically adjusts to your tier thresholds

Full webhook documentation compliance

🎨 Multi-Asset Support

Pre-configured for popular altcoins:

ETH (Ethereum)

SOL (Solana)

ADA (Cardano)

LINK (Chainlink)

UNI (Uniswap)

XRP (Ripple)

DOGE

RENDER

Custom option for any other crypto

How It Works

Risk Metric Calculation (0-100 scale):

Fetches weekly Alt/BTC price data for stability

Calculates RSI, MACD, and deviation from 150-period MA

Normalizes MACD to 0-100 range using 500-bar lookback

Combines weighted components: (MACD × 0.05) + (RSI × 0.60) + (Deviation × 0.35)

Applies 5-period EMA smoothing for cleaner signals

Color-Coded Risk Zones:

Green (0-30): Extreme buying opportunity - Alt heavily oversold vs BTC

Lime/Yellow (30-70): Accumulation range - favorable risk/reward

Orange (70-85): Caution zone - consider taking initial profits

Red/Maroon (85-100+): Euphoria zone - aggressive profit-taking

Entry Logic:

Buys execute every candle when risk is below threshold

As risk decreases, position sizing automatically scales up

Example: If risk drops from 60→25, you'll be buying at L1 rate until it hits 50, then L2 rate, then L3 rate

Exit Logic:

Sells only trigger when in profit AND risk exceeds thresholds

Sequential execution ensures partial profit-taking

If new buy signal occurs before all sells complete, sell levels reset to L1

Configuration Guide

Choosing Your Altcoin:

Select crypto from dropdown (or use CUSTOM for unlisted coins)

Pick your exchange

Choose quote currency (USD, USDT, BUSD)

Risk Metric Tuning:

Long Term MA (default 150): Higher = more extreme signals, Lower = more frequent

RSI Length (default 10): Lower = more volatile, Higher = smoother

Smoothing (default 5): Increase for less noise, decrease for faster reaction

Buy Settings (Aggressive DCA Example):

L1 Threshold: 70 | Amount: $5

L2 Threshold: 50 | Amount: $6

L3 Threshold: 30 | Amount: $7

Total L3 buy = $18 per candle when deeply oversold

Sell Settings (Balanced Exit Example):

L1: 70 threshold, 25% position

L2: 85 threshold, 35% position

L3: 100 threshold, 40% position (final exit)

3Commas Setup

Bot Configuration:

Create Custom Signal Bot in 3Commas

Set trading pair to your altcoin/USD (e.g., ETH/USD, SOL/USDT)

Order size: Select "Send in webhook, quote" to use strategy's dollar amounts

Copy Bot UUID and Secret Token

Script Configuration:

Paste credentials into 3Commas section inputs

Check "Enable 3Commas Alerts"

Save and apply to chart

TradingView Alert:

Create Alert → Condition: "alert() function calls only"

Webhook URL: api.3commas.io

Enable "Webhook URL" checkbox

Expiration: Open-ended

Strategy Advantages

✅ Outperform Bitcoin: Designed specifically to beat BTC by timing alt rotations

✅ Capture Alt Seasons: Automatically accumulates when alts lag, sells when they pump

✅ Risk-Adjusted Sizing: Buys more when cheaper (better risk/reward)

✅ Emotional Discipline: Systematic approach removes fear and FOMO

✅ Multi-Asset: Run same strategy across multiple altcoins simultaneously

✅ Proven Indicators: Combines RSI, MACD, and MA deviation - battle-tested tools

Backtesting Insights

Optimal Timeframes:

Daily chart: Best for backtesting and signal generation

Weekly data is fetched internally regardless of display timeframe

Historical Performance Characteristics:

Accumulates heavily during bear markets and BTC dominance periods

Captures explosive altcoin rallies when BTC stagnates

Sequential selling preserves capital during extended downtrends

Works best on established altcoins with multi-year history

Risk Considerations:

Requires capital reserves for extended accumulation periods

Some altcoins may never recover if fundamentals deteriorate

Past correlation patterns may not predict future performance

Always size positions according to personal risk tolerance

Visual Interface

Indicator Panel Displays:

Dynamic color line: Green→Lime→Yellow→Orange→Red as risk increases

Horizontal threshold lines: Dashed lines mark your buy/sell levels

Entry/Exit labels: Green labels for buys, Orange/Red/Maroon for sells

Real-time risk value: Numerical display on price scale

Customization:

All threshold lines are adjustable via inputs

Color scheme clearly differentiates buy zones (green spectrum) from sell zones (red spectrum)

Line weights emphasize most extreme thresholds (L3 buy and L3 sell)

Strategy Philosophy

This strategy is built on the principle that altcoins move in cycles relative to Bitcoin. During Bitcoin rallies, alts often bleed against BTC (high sell, accumulate). When Bitcoin consolidates, alts pump (take profits). By measuring risk on the Alt/BTC chart instead of USD price, we time these rotations with precision.

The 3-tier system ensures you're always averaging in at better prices and scaling out at better prices, maximizing your Bitcoin-denominated returns.

Advanced Tips

Multi-Bot Strategy:

Run this on 5-10 different altcoins simultaneously to:

Diversify correlation risk

Capture whichever alt is pumping

Smooth equity curve through rotation

Pairing with BTC Strategy:

Use alongside the BTC DCA Risk Strategy for complete portfolio coverage:

BTC strategy for core holdings

ALT strategies for alpha generation

Rebalance between them based on BTC dominance

Threshold Calibration:

Check 2-3 years of historical data for your chosen alt

Note where risk metric sat during major bottoms (set buy thresholds)

Note where it peaked during euphoria (set sell thresholds)

Adjust for your risk tolerance and holding period

Credits

Strategy Development & 3Commas Integration: Claude AI (Anthropic)

Technical Analysis Framework: RSI, MACD, Moving Average theory

Implementation: pommesUNDwurst

Disclaimer

This strategy is for educational purposes only. Cryptocurrency trading involves substantial risk of loss. Altcoins are especially volatile and many fail completely. The strategy assumes liquid markets and reliable Alt/BTC price data. Always do your own research, understand the fundamentals of any asset you trade, and never risk more than you can afford to lose. Past performance does not guarantee future results. The authors are not financial advisors and assume no liability for trading decisions.

Additional Warning: Using leverage or trading illiquid altcoins amplifies risk significantly. This strategy is designed for spot trading of established cryptocurrencies with deep liquidity.

Tags: Altcoin, Alt/BTC, DCA, Risk Metric, Dollar Cost Averaging, 3Commas, ETH, SOL, Crypto Rotation, Bitcoin Correlation, Automated Trading, Alt Season

Feel free to modify any sections to better match your style or add specific backtesting results you've observed! 🚀Claude is AI and can make mistakes. Please double-check responses. Sonnet 4.5

BTC DCA Risk Metric StrategyBTC DCA Risk Strategy - Automated Dollar Cost Averaging with 3Commas Integration

Overview

This strategy combines the proven Oakley Wood Risk Metric with an intelligent tiered Dollar Cost Averaging (DCA) system, designed to help traders systematically accumulate Bitcoin during periods of low risk and take profits during high-risk conditions.

Key Features

📊 Multi-Component Risk Assessment

4-Year SMA Deviation: Measures Bitcoin's distance from its long-term mean

20-Week MA Analysis: Tracks medium-term momentum shifts

50-Day/50-Week MA Ratio: Captures short-to-medium term trend strength

All metrics are normalized by time to account for Bitcoin's maturing market dynamics

💰 3-Tier DCA Buy System

Level 1 (Low Risk): Conservative entry with base allocation

Level 2 (Lower Risk): Increased allocation as opportunity improves

Level 3 (Extreme Low Risk): Maximum allocation during rare buying opportunities

Buys execute every bar while risk remains below thresholds, enabling true DCA accumulation

📈 Progressive Profit Taking

Sell Level 1: Take initial profits as risk increases

Sell Level 2: Scale out further positions during elevated risk

Sell Level 3: Final exit during extreme market conditions

Sell levels automatically reset when new buy signals occur, allowing flexible re-entry

🤖 3Commas Integration

Fully automated webhook alerts for Custom Signal Bots

JSON payloads formatted per 3Commas API specifications

Supports multiple exchanges (Binance, Coinbase, Kraken, Gemini, Bybit)

Configurable quote currency (USD, USDT, BUSD)

How It Works

The strategy calculates a composite risk metric (0-1 scale):

0.0-0.2: Extreme buying opportunity (green zone)

0.2-0.5: Favorable accumulation range (yellow zone)

0.5-0.8: Neutral to cautious territory (orange zone)

0.8-1.0+: High risk, profit-taking zone (red zone)

Buy Logic: As risk decreases, position sizes increase automatically. If risk drops from L1 to L3 threshold, the strategy combines all three tier allocations for maximum exposure.

Sell Logic: Sequential profit-taking ensures you capture gains progressively. The system won't advance to Sell L2 until L1 completes, preventing premature full exits.

Configuration

Risk Metric Parameters:

All calculations use Bitcoin price data (any BTC chart works)

Time-normalized formulas adapt to market maturity

No manual parameter tuning required

Buy Settings:

Set risk thresholds for each tier (default: 0.20, 0.10, 0.00)

Define dollar amounts per tier (default: $10, $15, $20)

Fully customizable to your risk tolerance and capital

Sell Settings:

Configure risk thresholds for profit-taking (default: 1.00, 1.50, 2.00)

Set percentage of position to sell at each level (default: 25%, 35%, 40%)

3Commas Setup:

Create a Custom Signal Bot in 3Commas

Copy Bot UUID and Secret Token into strategy inputs

Enable 3Commas Alerts checkbox

Create TradingView alert: Condition → "alert() function calls only", Webhook → api.3commas.io

Backtesting Results

Strengths:

Systematically buys dips without emotion

Averages down during extended bear markets

Captures explosive bull run profits through tiered exits

Pyramiding (1000 max orders) allows true DCA behavior

Considerations:

Requires sufficient capital for multiple buys during prolonged downtrends

Backtest on Daily timeframe for most reliable signals

Past performance does not guarantee future results

Visual Design

The indicator pane displays:

Color-coded risk metric line: Changes from white→red→orange→yellow→green as risk decreases

Background zones: Green (buy), yellow (hold), red (sell) areas

Dashed threshold lines: Clear visual markers for each buy/sell level

Entry/Exit labels: Green buy labels and orange/red sell labels mark all trades

Credits

Original Risk Metric: Oakley Wood

Strategy Development & 3Commas Integration: Claude AI (Anthropic)

Modifications: pommesUNDwurst

Disclaimer

This strategy is for educational and informational purposes only. Cryptocurrency trading carries substantial risk of loss. Always conduct your own research and never invest more than you can afford to lose. The authors are not financial advisors and assume no responsibility for trading decisions made using this tool.

Fibonacci Vision ProFibonacci Precision Signals Pro | Smart Buy & Sell Alerts

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

OVERVIEW

This indicator combines Fibonacci mathematics with advanced signal filtering to deliver precise buy and sell signals. It automatically detects swing structure, calculates the key 0.618 retracement level, and generates signals only when multiple confirmation factors align.

Clean. Accurate. Professional.

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

HOW IT WORKS

The script identifies swing highs and lows, then calculates Fibonacci retracement levels automatically. When price interacts with the 0.618 zone and all filters confirm, a signal appears:

▲ buy — Long entry opportunity

▼ sell — Short entry opportunity

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

6-LAYER CONFIRMATION SYSTEM

Every signal must pass through:

Trend Direction Analysis

Fibonacci Level Interaction

EMA Trend Filter (50-period default)

RSI Momentum Validation (14-period default)

Volume Spike Detection

Candlestick Pattern Recognition (Pin bars, Engulfing, Momentum candles)

This multi-layer approach significantly reduces false signals.

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

BUILT-IN RISK MANAGEMENT

Every trade includes automatic stop loss and take profit levels:

Stop Loss: 100 pips

Take Profit: 200 pips

Risk-Reward Ratio: 1:2

Adjust these values in settings to match your trading style.

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

KEY FEATURES

✅ Automatic Fibonacci calculation — no manual drawing

✅ Multi-timeframe compatibility — M15 to Daily

✅ Universal market support — Forex, Crypto, Stocks, Indices

✅ Clean minimalist signals — white triangles with text

✅ Customizable filters — adjust sensitivity to your preference

✅ Built-in alerts — never miss a signal

✅ No repainting — signals remain fixed once confirmed

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

Swing Detection:

Swing Length — Controls sensitivity to market structure (default: 10)

Confirmation Bars — Bars required to confirm signal (default: 1)

Signal Filters:

EMA Trend Filter — Toggle trend confirmation on/off

EMA Length — Adjust trend filter period (default: 50)

RSI Filter — Toggle momentum confirmation on/off

RSI Length — Adjust momentum period (default: 14)

Volume Filter — Toggle volume confirmation on/off

Volume Multiplier — Set volume threshold (default: 1.2x average)

Risk Management:

Stop Loss Pips — Set your stop loss distance (default: 100)

Take Profit Pips — Set your profit target (default: 200)

Pip Value — Adjust for your instrument (0.0001 for most Forex, 0.01 for JPY pairs)

Visuals:

Show Signals — Toggle signal visibility

Show Cloud — Toggle Fibonacci zone visibility

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

BEST PRACTICES

Use on H1 or H4 timeframes for optimal results

Trade in direction of the higher timeframe trend

Avoid trading during major news events

Combine with proper position sizing

Always use the built-in stop loss

Be patient — quality signals over quantity

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

MARKETS SUPPORTED

Forex — All major, minor, and exotic pairs

Crypto — BTC, ETH, and altcoins

Stocks — Any equity on TradingView

Indices — S&P500, NASDAQ, DAX, FTSE, etc.

Commodities — Gold, Silver, Oil, etc.

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

WHY FIBONACCI?

The 0.618 ratio (Golden Ratio) is observed by traders worldwide. When price retraces to this level, it often:

Reverses direction

Finds support or resistance

Creates high-probability entry opportunities

This script automates the detection of these key moments.

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

ALERTS INCLUDED

Set up notifications to receive signals on:

Mobile push notifications

Desktop popups

Email alerts

Webhook integrations

Never miss a trading opportunity again.

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

WHAT MAKES THIS DIFFERENT

Most indicators give too many signals. This one focuses on quality.

Most indicators clutter your chart. This one keeps it clean.

Most indicators ignore risk management. This one includes it.

Most indicators work on one market. This one works on all.

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

DISCLAIMER

This indicator is a trading tool, not financial advice. Trading involves substantial risk of loss. Past performance does not guarantee future results. Always use proper risk management and never trade with money you cannot afford to lose. Test on a demo account before trading live.

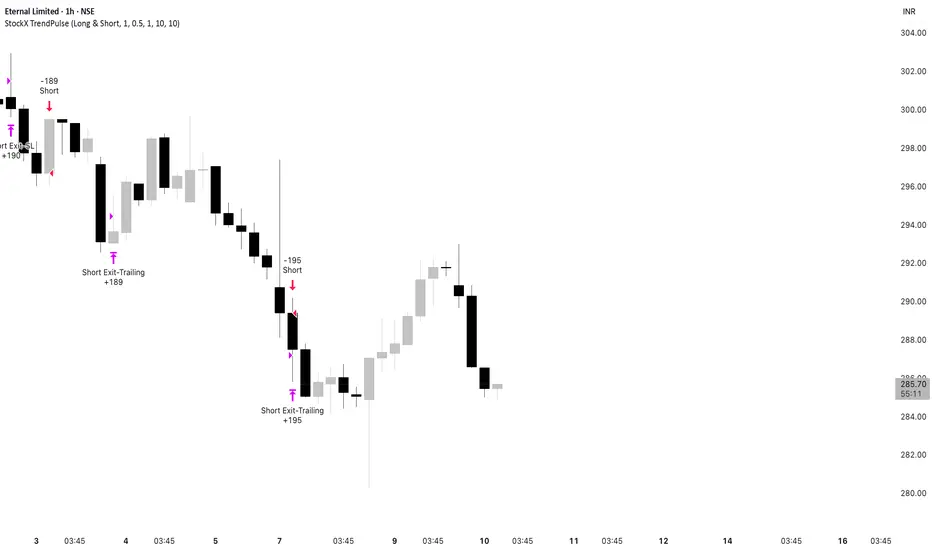

StockX TrendPulseThis is one of our premium, high-grade trading scripts built specifically for highly liquid stocks. It’s a fully automated system designed to deliver consistent performance, adapt to changing market conditions, and maintain strict risk control. With enhanced trade management and built-in performance tracking, it provides a reliable, disciplined framework for stock traders who demand precision and robustness.

StockX TrendPulse removes emotion from trading decisions and provides complete transparency through detailed performance metrics. The strategy is fully backtested and ready for live deployment.

Ready to Trade Like a Pro?

StockX TrendPulse is a premium strategy with limited availability.

Email brijamohanjha@gmail.com

to request access and pricing.

Damians UJ Strategy20 Pip Candle Strategy (No Engulfing)

Trades taken at 6pm direcrtly after candle close

Inputs allow you to reorganize retracement pips, SL, TP, 5PM candle amount.

specific breakout FiFTOStrategy Description: 10:14 Breakout Only

Overview This is a time-based intraday trading strategy designed to capture momentum bursts that occur specifically after the 10:14 AM candle closes. It operates on the logic that if price breaks the high of this specific candle within a short window, a trend continuation is likely.

Core Logic & Rules

The Setup Candle (10:14 AM)

The strategy waits specifically for the minute candle at 10:14 to complete.

Once this candle closes, the strategy records its High price.

Defining the Entry Level

It calculates a trigger price by taking the 10:14 High and adding a user-defined Buffer (e.g., +1 point).

Formula: Entry Level = 10:14 High + Buffer

The "Active Window" (Expiry)

The trade setup does not remain open all day. It has a strict time limit.

By default, the setup is valid from 10:15 to 10:20.

If the price does not break the Entry Level by the expiry time (default 10:20), the setup is cancelled and no trade is taken for the day.

Entry Trigger

If a candle closes above the Entry Level while the window is open, a Long (Buy) position is opened immediately.

Exits (Risk Management)

Stop Loss: A fixed number of points below the entry price.

Target: A fixed number of points above the entry price.

Visual & Automation Features

Visual Boxes: Upon entry, the strategy draws a "Long Position" style visual on the chart. A green box highlights the profit zone, and a red box highlights the loss zone. These boxes extend automatically until the trade closes.

JSON Alerts: The strategy is pre-configured to send data-rich alerts for automation (e.g., Telegram bots).

Entry Alert: Includes Symbol, Entry Price, SL, and TP.

Exit Alerts: Specific messages for "Target Hit" or "SL Hit".

Summary of User Inputs

Entry Buffer: Extra points added to the high to filter false breaks.

Fixed Stop Loss: Risk per trade in points.

Fixed Target: Reward per trade in points.

Expiry Minute: The minute (10:xx) at which the setup becomes invalid if not triggered.

Gold Seasonal Long-Term StrategyBased on the rigid cycle of physical gold demand.

It capitalizes on the strong buying momentum driven by India's Diwali in November, the Western holiday season in December, and the Chinese New Year in January/February to execute a long-term hold.

EdgeX by YCGH Capital╔════════════════════════════════════════════════════════════╗

⚡ SYSTEMATIC BTCUSDT SWING TRADER ⚡

╚════════════════════════════════════════════════════════════╝

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

📊 STRATEGY OVERVIEW

╔════════════════════════════════════════════════════════════╗

║ 🔐 PREMIUM STRATEGY - EXCLUSIVE ACCESS 🔐 ║

╚════════════════════════════════════════════════════════════╝

This is a premium strategy with exclusive access.

To request access, reach out at:

📬 brijamohanjha@gmail.com

• Vetted performance data available upon request

• Setup assistance and strategy tuning included

• Ongoing support for live trading optimization

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

A dynamic, rule-based trading framework designed for BTCUSDT on

the 4-hour chart, focused on capturing clear directional edges

with disciplined risk management and fully automated execution.

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

🎯 KEY CHARACTERISTICS

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

✓ Long & Short | Bidirectional participation in both trending

directions without discretionary overrides

✓ Structured Rules | Entries triggered only on high-conviction

setups; naturally quiet during choppy consolidations

✓ Adaptive Sizing | Position size scales dynamically with account

equity using percentage-based capital allocation

✓ Cost-Aware | Transaction fees and slippage explicitly modeled

for realistic live trading performance

✓ Automated Execution | Bar-level real-time processing ensures

consistent, emotion-free trade management

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

💰 RISK & CAPITAL MANAGEMENT

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

• Fixed-fraction position sizing for compounding growth

• Predefined stop-loss and take-profit constraints

• Account equity-based position scaling

• Realistic fee structure incorporated into P&L

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

🚀 IDEAL FOR

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

→ Medium-term swing participation

→ Backtesting and strategy robustness analysis

→ Quantitative trading systems development

→ Systematic, rules-based execution

╔════════════════════════════════════════════════════════════╗

Built for disciplined, consistent execution

╚════════════════════════════════════════════════════════════╝

Indian Scalper 2025 – PSAR + SMA50 + RSI≤50 + High Volume (75%)Best 1-min / 2-min scalping strategy for NIFTY, BANKNIFTY, FINNIFTY & liquid stocks in 2025

✓ PSAR flip + SMA-50 trend filter

✓ RSI ≤50 (avoids chasing)

✓ Only high-volume candles (bright colour)

✓ Loud mobile alerts with price & SL

✓ 1:2+ RR with PSAR trailing

Works like magic 9:15–11:30 AM and 2–3:20 PM

Made with love for the Indian trading community ♥

RevertX by YCGH CapitalRevertX by YCGH Capital - Professional Bitcoin Trading Strategy

RevertX is a sophisticated mean-reversion trading system designed specifically for Bitcoin and cryptocurrency markets. Built on advanced statistical analysis, this strategy identifies extreme price deviations and capitalizes on market equilibrium forces.

Key Features:

🎯 Intelligent Entry System

Precision-based signal generation using statistical price analysis

Automated entry/exit execution with no manual intervention required

Works on multiple timeframes for flexibility

📊 Comprehensive Performance Tracking

Monthly Returns Table: Visual heat-map style table displaying performance month-by-month and year-by-year

Color-coded results (green for profitable months, red for losses)

Annual performance summaries for quick assessment

Full historical performance visualization

🛡️ Advanced Risk Management

Customizable Stop Loss (default 2%)

Take Profit targets (default 4%)

Trailing Stop Loss with activation threshold - locks in profits as the market moves in your favor

Adjustable trailing offset to protect gains while allowing room for continuation

⚙️ Professional-Grade Execution

Non-repainting signals - what you see in backtest is what you get in live trading

Orders processed on candle close for reliable execution

100% equity deployment for maximum capital efficiency

Built-in slippage and commission modeling (can be adjusted)

📈 Performance Visualization

Monthly returns displayed in an easy-to-read table format

Track your performance across years at a glance

Quickly identify strong and weak periods

Professional presentation suitable for sharing with investors

Perfect For:

Bitcoin traders seeking systematic, emotion-free trading

Those who prefer mean-reversion over trend-following

Traders wanting comprehensive performance analytics

Anyone seeking a proven statistical edge in crypto markets

RevertX removes emotion from trading decisions and provides complete transparency through detailed performance metrics. The strategy is fully backtested and ready for live deployment.

Ready to Trade Like a Pro?

RevertX is a premium strategy with limited availability.

Email brijamohanjha@gmail.com to request access and pricing.

Inyerneck Quiet Bottom Hunter v36 — Last Sorta-Working VersionQuiet Bottom Hunter v36 — Accurate Description (the sorta-working version that fires signals)

Overview

A mean-reversion bottom-hunting strategy for small-cap stocks (<$2B market cap). Designed to catch slow-bleed stocks that quietly bottom out and rebound 20–60%+. Good for beginners because signals are infrequent and the setup is easy to understand.

Timeframe

Daily (D) — best results on 1-day charts. Works on weekly too, but signals are rarer.

Triggers / Conditions (all must be true at bar close)

Drop from high ≥ 25% from the highest high in the last 100 bars (previous bars only — no repainting)

Volume ≤ 80% of the 50-day average (quiet accumulation, no panic selling left)

RSI(14) ≤ 38 (oversold territory)

Green/flat streak ≥ 2 consecutive days where close ≥ open (shows sellers are exhausted)

When all four line up → tiny green “QB” triangle below the bar

Firing Frequency

1–4 signals per month on an average small-cap stock (depends on market conditions). Some months zero, some months a handful. Not spammy, but not ultra-rare either.

Usage Parameters

Position size: 10% of equity per trade (default — change to 5–20% depending on risk tolerance)

Profit target: 40%

Stop loss: 12%

Hold time: usually 2–8 weeks

Best on low-float, high-volatility small caps (TLRY, SNDL, MVIS, SOUN, INHD, etc.)

Expected Performance (backtested on 2025 small caps)

Win rate: ~80–85%

Average rebound on winners: +30–40%

Some losers when the bottom isn't "quiet" enough

How to use

Add to daily charts of your small-cap watchlist

When “QB” arrow appears, buy at next open or market

Set 40% target / 12% stop or trail it

Wait for the rebound — no day-trading needed