Moon Scalper v3 + VSAMoon Scalper v3 is a high-precision scalping indicator optimized for the 15-minute chart. It delivers clean buy/sell signals with TP1 (1:1 risk-reward) exits using layered confirmations:

• **Volatility Bands** — SMA + multiplier detect expansion zones

• **EMA Filter (200)** — ensures trades align with trend

• **RSI Range Filter** — avoids extreme overbought/oversold traps (buy: 52–62, sell: 38–48)

• **Volume Spike Filter** — filters for institutional activity (vol > 1.4×SMA)

• **VSA Confirmation** — requires wide-spread, high-volume bars with reclaim (volume × 1.4, spread × 1.5, reclaim 50%)

**Usage Notes:**

Best used on 15m timeframe for liquid pairs (e.g., BTCUSDT, ETHUSDT). Signals appear as “BUY” / “SELL” labels on chart. Defaults yield high TP1 hit rate; use only during active sessions (e.g., London/NY) for best accuracy.

**Disclaimer:**

This indicator is for educational purposes only. Past performance is not a guarantee of future results. Always backtest before live trading and manage risk responsibly.

Educational

EMA inFusion Pro - Multiple SourcesEMA Fusion Pro: Dynamic Trend & Momentum Strategy with Three Exit Modes

EMA Fusion Pro is a highly customizable, multi-exit trend-following strategy designed for traders who value both precision and flexibility. By leveraging exponential moving averages (EMA), average directional index (ADX), and volume analysis, this strategy aims to capture trending market moves while offering three distinct exit modes for optimal risk management across varying market conditions.

Strategy Overview

This strategy systematically identifies potential entry points using a moving average crossover with highly configurable data sources (including price, volume, rate of change, or their Heikin Ashi versions) and filters signal quality with ADX trend strength and volume spikes. Each trade is managed with one of three advanced exit methodologies—reverse signal, ATR-based stop/take profit, or fixed percentage—giving you the control to adapt your risk profile to different market regimes.

Key Features

Customizable EMA Source: Calculate the core trend-filtering EMA from price (default), volume, rate of change, or their Heikin Ashi counterparts for unique market perspectives.

Trend Filter with ADX: Confirm entries only when the trend is strong, as measured by the user-adjustable ADX threshold.

Volume Spike Confirmation: Optional filter to only take trades with above-average volume activity, reducing false signals.

Three Exit Modes:

Reverse Signal: Exit trades when a new, opposite entry signal occurs.

ATR-Based Stop/Take Profit: Dynamic risk management using multiples of the average true range (ATR) for both take profit and stop loss.

Percent-Based Stop/Take Profit: Fixed-percentage risk management with user-defined thresholds.

Visual Annotations: Signal markers, EMA line color-coded by source, trend background coloring, and optional ATR/percent-based TP/SL levels.

Info Panel: Real-time display of all core indicators, current trading mode, exit parameters, and position status for quick oversight.

How It Works

Entry Logic: A crossover signal (above/below the EMA) triggers a new entry, but only if both ADX trend strength and (optionally) volume spike conditions are met.

Exit Logic: Three selectable modes allow you to exit trades on reverse signals, at a dynamic ATR-based profit or loss, or at a fixed percentage gain/loss.

Flexible Data Analysis: The EMA source can be chosen from six options—standard price, volume, rate of change, or their Heikin Ashi variants—allowing experimentation with different market dimensions.

Risk Management: All exits are precisely controlled, either by the next opposing signal, by volatility-adjusted levels, or by fixed risk/reward ratios.

Backtest & Optimization: The strategy is fully backtestable within TradingView’s Strategy Tester, with adjustable parameters for optimization.

Customization & Usage

Indicator Source: Select your preferred data type for EMA calculation, opening the door to creative strategy variations (e.g., volume momentum, pure price trend, rate of change divergence).

Filter Toggles: Enable/disable ADX and volume filters as desired—useful for different market environments.

Exit Mode Selection: Switch between reverse, ATR, or percent-based exits with a single parameter—ideal for adapting to ranging vs. trending markets.

Visual Clarity: The EMA line color reflects its underlying source, and the info panel summarizes all critical values for easy monitoring.

Who Should Use This Strategy?

Trend Followers seeking to ride strong moves with multiple exit options.

Experienced Traders who want to experiment with different data types (volume, momentum, Heikin Ashi) for trend analysis.

Algorithmic Traders looking for a robust, flexible base to build upon with their own ideas.

Getting Started

Apply the script to your chart and review default settings.

Customize parameters—EMA length, ADX threshold, volume settings, exit type—as desired.

Backtest on multiple instruments and timeframes to evaluate performance.

Optimize filters, exit rules, and risk parameters for your preferred trading style.

Monitor with the real-time info panel and trade alerts.

Disclaimer

This script is for educational and entertainment purposes only. It is not financial advice. Past performance is not indicative of future results. Always conduct thorough testing and consider your risk tolerance before trading real capital.

— Happy Trading —

Feel free to adapt, share, and contribute to this open-source strategy!

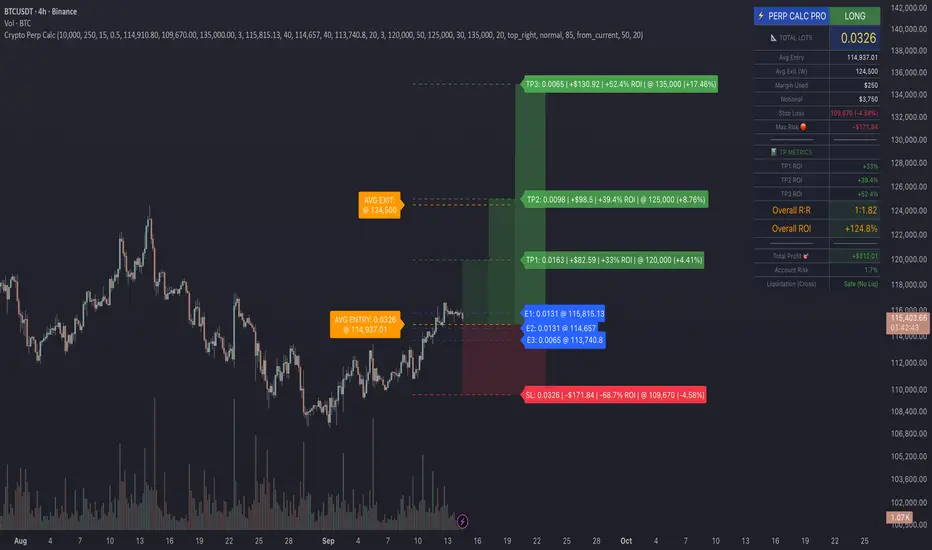

Crypto Perp Calc v1Advanced Perpetual Position Calculator for TradingView

Description

A comprehensive position sizing and risk management tool designed specifically for perpetual futures trading. This indicator eliminates the confusion of calculating leveraged positions by providing real-time position metrics directly on your chart.

Key Features:

Interactive Price Selection: Click directly on chart to set entry, stop loss, and take profit levels

Accurate Lot Size Calculation: Instantly calculates the exact position size needed for your margin and leverage

Multiple Entry Support: DCA into positions with up to 3 entry points with customizable allocation

Multiple Take Profit Levels: Scale out of positions with up to 3 TP targets

Comprehensive Risk Metrics: Shows dollar P&L, account risk percentage, and liquidation price

Visual Risk/Reward: Color-coded boxes and lines display your trade setup clearly

Real-time Info Table: All critical position data in one organized panel

Perfect for traders using perpetual futures who need precise position sizing with leverage.

---------

How to Use

Quick Start (3 Clicks)

1. Add the indicator to your chart

2. Click three times when prompted:

First click: Set your entry price

Second click: Set your stop loss

Third click: Set your take profit

3. Read the TOTAL LOTS value from the info table (highlighted in yellow)

4. Use this lot size in your exchange when placing the trade

Detailed Setup

Step 1: Configure Your Account

Enter your account balance (total USDT in account)

Set your margin amount (how much USDT to risk on this trade)

Choose your leverage (1x to 125x)

Select Long or Short position

Step 2: Set Price Levels

Main levels use interactive clicking (Entry, SL, TP)

For multiple entries or TPs, use the settings panel to manually input prices and percentages

Step 3: Read the Results

The info table shows:

TOTAL LOTS - The position size to enter on your exchange

Margin Used - Your actual capital at risk

Notional - Total position value (margin × leverage)

Max Risk - Dollar amount you'll lose at stop loss

Total Profit - Dollar amount you'll gain at take profit

R:R Ratio - Risk to reward ratio

Account Risk - Percentage of account at risk

Liquidation - Price where position gets liquidated

Step 4: Advanced Features (Optional)

Multiple Entries (DCA):

Enable "Use Multiple Entries"

Set up to 3 entry prices

Allocate percentage for each (must total 100%)

See individual lot sizes for each entry

Multiple Take Profits:

Enable "Use Multiple TPs"

Set up to 3 TP levels

Allocate percentage to close at each level (must total 100%)

View profit at each target

Visual Elements

Blue lines/labels: Entry points

Red lines/labels: Stop loss

Green lines/labels: Take profit targets

Colored boxes: Visual risk (red) and reward (green) zones

Info table: Can be positioned anywhere on screen

Alerts

Set price alerts for:

Entry zones reached

Stop loss approached

Take profit levels hit

Works with TradingView's alert system

Tips for Best Results

Always verify the lot size matches your intended risk

Check the liquidation price stays far from your stop loss

Monitor the account risk percentage (recommended: keep under 2-3%)

Use the warning indicators if risk exceeds margin

For quick trades, use single entry/TP; for complex strategies, use multiple levels

Example Workflow

Find your trade setup using your analysis

Add this indicator and click to set levels

Check risk metrics in the table

Copy the TOTAL LOTS value

Enter this exact position size on your exchange

Set alerts for key levels if desired

This tool bridges the gap between TradingView charting and exchange execution, ensuring your position sizing is always accurate when trading with leverage.

Disclaimer, this was coded with help of AI, double check calculations if they are off.

BTC_Hull Suite StrategyOverview

BTC_Hull Suite Strategy is a trend-following system designed to keep drawdowns modest while staying exposed during genuine uptrends. It uses the Hull Moving Average (HMA) for fast, low-lag trend turns, a long-term SMA filter to avoid chop, and a percentage trailing stop to protect gains.

🔧 What the strategy includes

- Hull Moving Average (HMA) with configurable length (default 55)

- SMA filter (default 130) to trade only with higher-timeframe bias

- Trailing stop in percent (default 5%) based on the running peak of close

- Execution model: signals are evaluated on the previous bar and entries are placed at the next bar’s open (TradingView default)

📈 How it works:

✅ Entry (Long):

Detects a bullish Hull turn by comparing the current HMA to its value 3 bars ago:

h > h3 and h <= h3 → HMA just turned up on the prior bar

The SMA filter must confirm: close > sma

If both are true (and within the date window), a long is opened next bar at the open

❌ Exit:

Hull turn down: h < h3 and h >= h3 , or

Trailing stop: price closes below peak * (1 – trailingPct)

Either condition closes the position at the current bar’s close

Notes:

pyramiding = 1 → allows one add-on (maximum two concurrent long positions)

Position sizing defaults to 20% of equity per entry (adjustable in Properties)

Who is this for?

This strategy is tailored for Bitcoin traders (spot or perpetuals) who want a rules-based, low-lag trend system with built-in drawdown protection.

It works best on Daily or 4H charts, but parameters can be adapted for other timeframes.

⚠️ Disclaimer

This strategy is provided for educational and research purposes only.

It is not financial advice. Markets are risky — always test on your own data, include realistic fees/slippage, and forward-test before using real capital.

Money Flow | Lyro RSMoney Flow | Lyro RS

The Money Flow is a momentum and volume-driven oscillator designed to highlight market strength, exhaustion, and potential reversal points. By combining smoothed Money Flow Index readings with volatility, momentum, and RVI-based logic, it offers traders a deeper perspective on money inflow/outflow, divergences, and overbought/oversold dynamics.

Key Features

Smoothed Money Flow Line

EMA-smoothed calculation of the MFI for noise reduction.

Clear thresholds for overbought and oversold zones.

Normalized Histogram

Histogram plots show bullish/bearish money flow pressure.

Color-coded cross logic for quick trend assessment.

Relative Volatility Index (RVI) Signals

Detects overbought and oversold conditions using volatility-adjusted RVI.

Plots ▲ and ▼ markers at exhaustion points.

Momentum Strength Gauge

Calculates normalized momentum strength from ROC and volume activity.

Displays percentage scale of current momentum force.

Divergence Detection

Bullish divergence: Price makes lower lows while money flow makes higher lows.

Bearish divergence: Price makes higher highs while money flow makes lower highs.

Plotted as diamond markers on the oscillator.

Signal Dashboard (Table Overlay)

Displays real-time status of Money Flow signals, volatility, and momentum.

Color-coded readouts for instant clarity (Long/Short/Neutral + Momentum Bias).

How It Works

Money Flow Calculation – Applies EMA smoothing to MFI values.

Normalization – Scales oscillator between relative high/low values.

Trend & Signals – Generates bullish/bearish signals based on midline and histogram cross logic.

RVI Integration – Confirms momentum exhaustion with overbought/oversold markers.

Divergences – Identifies hidden market imbalances between price and money flow.

Practical Use

Trend Confirmation – Use midline crossovers with histogram direction for money flow bias.

Overbought/Oversold Reversals – Watch RVI ▲/▼ markers for exhaustion setups.

Momentum Tracking – Monitor momentum percentage to gauge strength of current trend.

Divergence Alerts – Spot early reversal opportunities when money flow diverges from price action.

Customization

Adjust length, smoothing, and thresholds for different markets.

Enable/disable divergence detection as needed.

Personalize visuals and dashboard display for cleaner charts.

⚠️ Disclaimer

This indicator is a tool for technical analysis and does not provide guaranteed results. It should be used alongside other methods and proper risk management. The creator is not responsible for financial decisions made using this script.

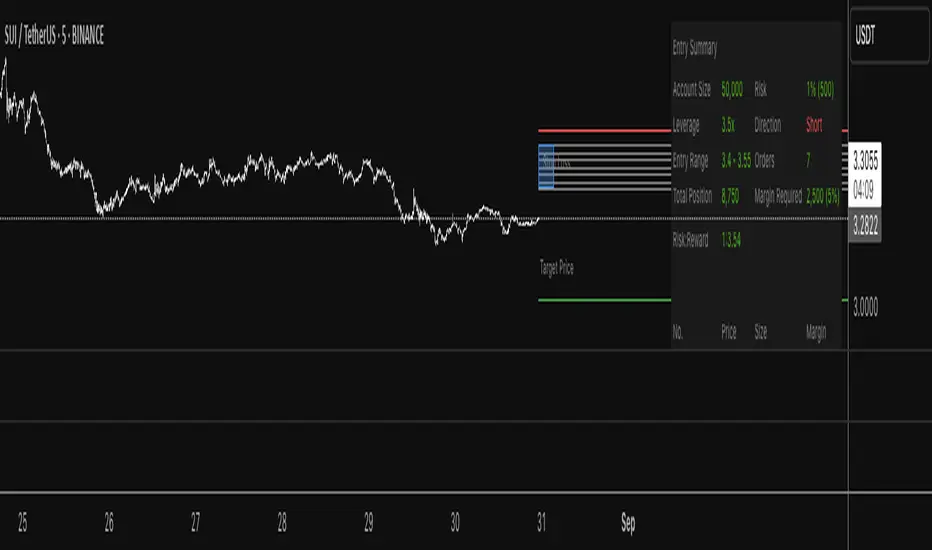

Progressive Entry Position Sizer v3Progressive Entry Position Sizer (PEPS) - DEVELOPMENT VERSION

⚠️ IMPORTANT DISCLAIMER: This indicator is currently in development and should NOT be relied upon for trading accuracy. Use at your own risk and always verify calculations independently before making any trading decisions.

Overview:

The Progressive Entry Position Sizer (PEPS) is a risk management tool designed to help traders plan multiple entry positions with progressive scaling. This indicator calculates position sizes and margin requirements across multiple entry levels while maintaining consistent risk exposure.

Key Features:

Progressive Risk Scaling: Uses a token-based system (1, 2, 3, 4, 5...) to progressively increase position sizes at each entry level

Leverage Support: Accommodates leverage up to 50x with proper margin calculations

Dollar-Based Position Sizing: Displays position values in dollar amounts rather than share quantities

Visual Entry Planning: Shows entry zones, target, and stop loss levels with extended lines

Comprehensive Risk Table: Detailed breakdown of each entry with position values and margin requirements

How It Works:

Set your account balance, risk percentage, and leverage

Define primary entry, final entry, target, and stop loss prices

Choose number of limit orders (2-8)

The indicator calculates evenly distributed entry prices with progressive position sizing

Each subsequent entry receives more "risk tokens" resulting in larger position sizes

Use Cases:

Planning DCA (Dollar Cost Averaging) strategies

Risk management for leveraged positions

Visualizing multi-entry trading setups

Educational purposes for understanding progressive scaling

⚠️ Development Status:

This script is actively being developed and may contain bugs or calculation errors. Always:

Verify all calculations manually

Test thoroughly on paper trades first

Consult with financial professionals

Never risk more than you can afford to lose

Feedback Welcome:

As this is a development version, user feedback and suggestions for improvements are greatly appreciated.

This indicator is for educational and planning purposes only. Not financial advice.

How to avoid repainting when using security() - viewing optionsHow to avoid repainting when using the security() - Edited PineCoders FAQ with more viewing options

This may be of value to a limited few, but I've introduced a set of Boolean inputs to PineCoders' original script because viewing all the various security lines at once was giving me a brain cramp. I wanted to study each behavior one-by-one. This version (also updated to PineScript v6) will allow users to selectively display each, or any combination, of the security plots. Each plot was updated to include a condition tied to its corresponding input, ensuring it only appears when explicitly enabled. The label-rendering logic only displays when its related plot is active; however, I've also added an input that allows you to remove all labels, enabling you to see the price action more clearly (the labels can sometimes obscure what you want to see). Run this script in replay mode to view the nuanced differences between the 12 methods while selecting/deselecting the desired plots (selecting all at once can be overcrowded and confusing).

All thanks and credit to PineCoders--these changes I made only provide more control over what’s shown on the chart without altering the core structure or intent of the original script. It helped me, so I thought I should share it. If I inadvertently messed something up, please let me know, and I will try to fix it.

I set the defaults for viewing monthly security functions on the daily timeframe. Only the first 2 security functions plot with the default settings, so change the settings as needed. Be sure to read the original notes and detailed explanations in the PineCoders posting "How to avoid repainting when using security() - PineCoders FAQ."

Bottom line, you should use one of the two functions: f_secureSecurity or f_security, depending on what you are trying to do. Hopefully, this script will make it a little easier for the visual learner to understand why (use replay mode or watch live price action on a lower timeframe).

Gap Detector (Body and Candle)Finds/Detects gaps between candles and candle bodies for any chart/timeframe with O(n+delta) performance.

Candle Gaps (between wicks) act as strong support or resistance. They are drawn as solid boxes.

Body Gaps (ignores wicks) act as mild support or resistance. They are depicted with lines.

Adjust the settings for candle/body gap width, smaller the time frame, smaller the gap.

Adjust max historical bars to fine tune performance on your system/setup. The more historical bars the script scans, more time required to load the chart. At times based on system configuration, TradingView may timeout the script due to too many bars. Reducing the max bars helps in this scenario.

This is a revamped version of "Body Gap Detector".

Happy charting !

Balanced Big Wicks (50/50) HighlighterThis open-source indicator highlights candles with balanced long wicks (50/50 style)—that is, candles where both upper and lower shadows are each at least 30–60% of the full range and within ~8% of each other, while retaining a substantial body. This specific structure often reflects indecision or liquidity sweeps and can precede strong breakout moves.

How It Works (Inputs and Logic)

Min wick % (each side): 30–60% of candle range

Max body %: up to 60% of range (preserves strong body presence)

Equality tolerance: wicks within 8% of each other

ATR filter (multiples of ATR14): ensures only significant-range candles are flagged

When a “50/50” candle forms, it’s visually colored and labeled; audibly alertable.

How to Use It

Long setup: price closes above the wick-high → potential long entry (SL below wick-low, TP = 1:1).

Short setup: price closes below wick-low → potential short entry (SL above wick-high, TP = 1:1).

Especially effective on 5–15 minute scalping charts when aligned with high-volume sessions or HTF trend context.

Why This Indicator Is Unique

Unlike standard wick or doji voters, this script specifically filters for candles with a strong body and symmetrical wicks, paired with a range filter, reducing noise significantly.

Important Notes

No unrealistic claims: backtested setups indicate high occurrence of clean breakouts, though performance depends on market structure.

Script built responsibly: uses real-time calculations only, no future-data lookahead.

Visuals on the published chart reflect default input values exactly.

TCLC - Multi TimeFrame VWAPVWAP :

VWAP, or Volume Weighted Average Price, is a trading indicator that represents the average price of a security over a specific period, weighted by the volume of trades at each price level. It is calculated by taking the sum of the product of price and volume and dividing it by the total volume for the period. Essentially, VWAP shows the average price at which most trades occurred, giving more weight to prices with higher trading volumes.

The Indicator Plots the VWAP in Daily, WEEKLY , MONTHLY , YEARLY which helps to gauage the trend where the Volume vs Price exists....

Break Point Record Table — GSK-VIZAG-AP-INDIA "Break Point Record Table — GSK-VIZAG-AP-INDIA" indicator captures key break points during each trading session and presents a clear, color-coded table overlay on the chart for quick visual reference. Specifically, it logs sessions' open price and monitors subsequent price action for notable breaks in the session high or low prices. Each break event is recorded with the time, price, and percentage change from the previous break, helping traders identify significant price movements within the session at a glance.

Key Features:

Records the session start time and opening price for context.

Tracks every intraday break above the previous session high or below the previous session low.

Calculates and displays the percentage change at each break event.

Highlights breaks with descriptive text including break time and values to aid trade decision-making.

Displays a table with columns for Time, Open, High, Low, and a Description of the event.

Uses color-coded cells to differentiate between session start, highs, lows, and break descriptions for better readability.

Maintains performance and readability by limiting the table to the latest 30 break events.

Usage & Benefits:

This indicator is ideal for intraday traders who want reliable visual cues to monitor momentum shifts and breakout/breakdown points during the trading day. By capturing these break points as discrete events and organizing the data into an easily accessible, visually intuitive table, it improves situational awareness and supports timely trading decisions.

Session Based Liquidity# Session Based Liquidity Indicator - Educational Open Source

## 📊 Overview

The Session Based Liquidity indicator is a comprehensive educational tool designed to help traders understand and visualize liquidity concepts across major trading sessions. This indicator identifies Buy-Side Liquidity (BSL) and Sell-Side Liquidity (SSL) levels created during Asia, London, and New York trading sessions, providing insights into institutional order flow and potential market reversal zones.

## 🎯 Key Features

### 📈 Multi-Session Tracking

- **Asia Session**: Tokyo/Sydney overlap (20:00-02:00 EST)

- **London Session**: European markets (03:00-07:30 EST)

- **New York Session**: US markets (09:30-16:00 EST)

- Individual session toggle controls for focused analysis

### 💧 Liquidity Level Detection

- **Buy-Side Liquidity (BSL)**: Identifies stop losses above swing highs where short positions get stopped out

- **Sell-Side Liquidity (SSL)**: Identifies stop losses below swing lows where long positions get stopped out

- Advanced filtering algorithm to identify only significant liquidity zones

- Configurable pivot strength for sensitivity adjustment

### 🎨 Visual Management System

- **Unclaimed Levels**: Active liquidity zones that haven't been hit (default: black lines)

- **Claimed Levels**: Swept liquidity zones showing historical interaction (default: red lines)

- Customizable line styles, colors, and widths for both states

- Dynamic label system showing session origin and level significance

- Real-time line extension and label positioning

### ⚙️ Advanced Configuration

- **Pivot Strength**: Adjust sensitivity (1-20) for liquidity detection

- **Max Levels Per Side**: Control number of tracked levels (1-10) per session

- **Label Offset**: Customize label positioning

- **Style Customization**: Full control over visual appearance

## 📚 Educational Value

### Core Concepts Explained

- **Liquidity Pools**: Areas where stop losses and pending orders cluster

- **Liquidity Sweeps**: When price moves through levels to trigger stops, then reverses

- **Session-Based Analysis**: How different market sessions create distinct liquidity characteristics

- **Institutional Order Flow**: Understanding how large players interact with retail liquidity

### Trading Applications

- Identify high-probability reversal zones after liquidity sweeps

- Understand where stop losses are likely clustered

- Avoid trading into obvious liquidity traps

- Use session context for timing entries and exits

- Recognize institutional accumulation and distribution patterns

### Code Learning Opportunities

- **Pine Script v6 Best Practices**: Modern syntax and efficient coding patterns

- **Object-Oriented Design**: Custom types and methods for clean code organization

- **Array Management**: Dynamic data structure handling for performance

- **Visual Programming**: Line, label, and styling management

- **Session Detection**: Time-based filtering and timezone handling

## 🔧 Technical Implementation

### Performance Optimized

- Efficient memory management with automatic cleanup

- Limited historical level tracking to maintain responsiveness

- Optimized array operations for smooth real-time updates

- Smart filtering to reduce noise and focus on significant levels

### Code Architecture

- **Modular Design**: Clean separation of concerns with dedicated methods

- **Type Safety**: Custom SessionLiquidity type for organized data management

- **Extensible Structure**: Easy to modify and enhance for specific needs

- **Educational Comments**: Comprehensive documentation throughout

## 💡 Usage Guide

### Basic Setup

1. Add indicator to chart

2. Configure session times for your timezone

3. Adjust pivot strength based on timeframe (higher for lower timeframes)

4. Enable/disable sessions based on your trading focus

### Interpretation

- **Unclaimed levels**: Watch for price interaction and potential reversals

- **Claimed levels**: Use as potential support/resistance after sweep

- **External levels**: Beyond session range, higher significance

- **Internal levels**: Within session range, may indicate ranging conditions

### Best Practices

- Use higher timeframes (15m+) for cleaner signals

- Combine with price action analysis for confirmation

- Consider session overlap periods for increased significance

- Monitor multiple sessions for comprehensive market view

## 🎓 Educational Goals

This open-source project aims to:

- Demystify liquidity concepts for retail traders

- Provide practical coding examples in Pine Script v6

- Encourage understanding of institutional trading behavior

- Foster community learning and collaboration

- Bridge the gap between theory and practical application

## 📄 License & Usage

Released under Mozilla Public License 2.0 - free for educational and commercial use with proper attribution.

## 🤝 Contributing

As an open-source educational tool, contributions are welcome! Whether it's bug fixes, feature enhancements, or educational improvements, your input helps the trading community learn and grow.

## ⚠️ Disclaimer

This indicator is for educational purposes only. All trading involves risk, and past performance does not guarantee future results. Always practice proper risk management and never risk more than you can afford to lose.

---

*By studying and using this indicator, traders can develop a deeper understanding of market microstructure and improve their ability to read institutional order flow patterns.*

Previous Day OHLC Dashboard (Last N Days)Indicator: Previous Day OHLC Dashboard (Multi-Day)

This indicator displays a dashboard-style table on your chart that shows the Open, High, Low, and Close (OHLC) of the previous trading days. It’s designed to help traders quickly reference key daily levels that often act as important support and resistance zones.

🔑 Features:

Dashboard Table: Shows OHLC data for the last N trading days (default = 3, up to 10).

Customizable Appearance:

Change the position of the dashboard (Top-Right, Top-Left, Bottom-Right, Bottom-Left).

Adjust text size (Tiny → Huge).

Customize colors for header, labels, and each OHLC column.

Yesterday’s OHLC Lines (optional): Plots horizontal lines on the chart for the previous day’s Open, High, Low, and Close.

Intraday & Multi-Timeframe Compatible: Works on all timeframes below Daily — values update automatically from the daily chart.

📊 Use Cases:

Quickly identify yesterday’s key levels for intraday trading.

Track how current price reacts to previous day’s support/resistance.

Keep a multi-day reference for trend bias and range context.

⚙️ How it Works:

The indicator pulls daily OHLC values using request.security() with lookahead_on to ensure prior day’s values are extended across the next session.

These values are displayed in a compact table for quick reference.

Optionally, the most recent daily levels (D-1) are plotted as chart lines.

✅ Perfect for day traders, scalpers, and swing traders who rely on yesterday’s price action to plan today’s trades.

OSOK KatxumotoThe OSOK Dynamic Box Enhanced is designed for scalpers and traders using the OSOK (One Shot, One Kill) method on futures like the NQ.

Features include:

A midline that dynamically follows the current price in real-time.

Upper (LS) and lower (LI) protection lines at configurable distances from the current price, representing stop or protection levels.

Target lines offset from LS and LI according to your risk/reward strategy, also fully configurable.

Customizable colors and thickness for all lines, allowing you to adapt the visualization to your trading style.

All lines automatically extend to the right from the current price, keeping the chart clean without accumulating old lines.

This indicator helps traders quickly visualize key levels, manage risk, and set objectives efficiently—perfect for scalping and high-precision setups.

Configurable parameters:

Protection distance (LS/LI) in points

Target distance from LS/LI in points

Line colors and thickness

Line extension to the right

Relative Strength Heat [InvestorUnknown]The Relative Strength Heat (RSH) indicator is a relative strength of an asset across multiple RSI periods through a dynamic heatmap and provides smoothed signals for overbought and oversold conditions. The indicator is highly customizable, allowing traders to adjust RSI periods, smoothing methods, and visual settings to suit their trading strategies.

The RSH indicator is particularly useful for identifying momentum shifts and potential reversal points by aggregating RSI data across a range of periods. It presents this data in a visually intuitive heatmap, with color-coded bands indicating overbought (red), oversold (green), or neutral (gray) conditions. Additionally, it includes signal lines for overbought and oversold indices, which can be smoothed using RAW, SMA, or EMA methods, and a table displaying the current index values.

Features

Dynamic RSI Periods: Calculates RSI across 31 periods, starting from a user-defined base period and incrementing by a specified step.

Heatmap Visualization: Displays RSI strength as a color-coded heatmap, with red for overbought, green for oversold, and gray for neutral zones.

Customizable Smoothing: Offers RAW, SMA, or EMA smoothing for overbought and oversold signals.

Signal Lines: Plots scaled overbought (purple) and oversold (yellow) signal lines with a midline for reference.

Information Table: Displays real-time overbought and oversold index values in a table at the top-right of the chart.

User-Friendly Inputs: Allows customization of RSI source, period ranges, smoothing length, and colors.

How It Works

The RSH indicator aggregates RSI calculations across 31 periods, starting from the user-defined Starting Period and incrementing by the Period Increment. For each period, it computes the RSI and determines whether the asset is overbought (RSI > threshold_ob) or oversold (RSI < threshold_os). These states are stored in arrays (ob_array for overbought, os_array for oversold) and used to generate the following outputs:

Heatmap: The indicator plots 31 horizontal bands, each representing an RSI period. The color of each band is determined by the f_col function:

Red if the RSI for that period is overbought (>threshold_ob).

Green if the RSI is oversold (

Indian market session on Gift Nifty chartsGift Nifty Market Session Highlighter

This indicator highlights the official Indian market session on Gift Nifty charts — from 9:15 AM to 3:30 PM IST. It shades the background during this time window so traders can instantly identify when the local market is open.

Features:

Marks 9:15 AM to 3:30 PM (IST) session on intraday charts.

Adjustable highlight color and transparency.

Works seamlessly across lower timeframes (1m, 5m, 15m, etc.).

Helps traders align Gift Nifty activity with NSE market hours.

Use Cases:

Quickly distinguish active market hours from overnight or global sessions.

Backtest trading strategies specific to Indian session volatility.

Improv

e focus on expiry-day setups and intraday opportunities.

Disclaimer:

This tool is provided for educational and informational purposes only. It is not financial advice, nor does it guarantee trading success. Always do your own research and consult a licensed financial professional before making investment decisions.

Globex Trap w/ percentage [SLICKRICK]Globex Trap w/ Percentage

Overview

The Globex Trap w/ Percentage indicator is a powerful tool designed to help traders identify high-probability trading opportunities by analyzing price action during the Globex (overnight) session and regular trading hours. By combining Globex session ranges with Supply & Demand zones, this indicator highlights potential "trap" areas where significant price reactions may occur. Additionally, it calculates the Globex session range as a percentage of the daily Average True Range (ATR), providing valuable context for assessing market volatility.

This indicator is ideal for traders in futures markets or other instruments traded during Globex sessions, offering a visual and analytical edge for spotting key price levels and potential reversals or breakouts.

Key Features

Globex Session Tracking:

Visualizes the high and low of the Globex session (default: 3:00 PM to 6:30 AM PST) with customizable time settings.

Displays a semi-transparent box to mark the Globex range, with labels for "Globex High" and "Globex Low."

Calculates the Globex range as a percentage of the daily ATR, displayed as a label for quick reference.

Supply & Demand Zones:

Identifies Supply & Demand zones during regular trading hours (default: 6:00 AM to 8:00 AM PST) with customizable time settings.

Draws semi-transparent boxes to highlight these zones, aiding in the identification of key support and resistance areas.

Trap Area Identification:

Highlights potential trap zones where Globex ranges and Supply & Demand zones overlap, indicating areas where price may reverse or consolidate due to trapped traders.

Customizable Settings:

Adjust Globex and Supply & Demand session times to suit your trading preferences.

Toggle visibility of Globex and Supply & Demand zones independently.

Customize box colors for better chart readability.

Set the lookback period (default: 10 days) to control how many historical zones are displayed.

Configure the ATR length (default: 14) for the percentage calculation.

PST Timezone Default:

All times are based on Pacific Standard Time (PST) by default, ensuring accurate session tracking for users in this timezone or those aligning with U.S. West Coast market hours.

Recommended Usage

Timeframes: Best used on 1-hour charts or lower (e.g., 15-minute, 5-minute) for precise entry and exit points.

Markets: Optimized for futures (e.g., ES, NQ, CL) and other instruments traded during Globex sessions.

Historical Data: Ensure at least 10 days of historical data for optimal visualization of zones.

Strategy Integration: Use the indicator to identify potential reversals or breakouts at Globex highs/lows or Supply & Demand zones. The ATR percentage provides context for whether the Globex range is significant relative to typical daily volatility.

How It Works

Globex Session:

Tracks the high and low prices during the user-defined Globex session (default: 3:00 PM to 6:30 AM PST).

When the session ends, a box is drawn from the start to the end of the session, capturing the high and low prices.

Labels are placed at the midpoint of the session, showing "Globex High," "Globex Low," and the range as a percentage of the daily ATR (e.g., "75.23% of Daily ATR").

Supply & Demand Zones:

Tracks the high and low prices during the user-defined regular trading hours (default: 6:00 AM to 8:00 AM PST).

Draws a box to mark these zones, which often act as key support or resistance levels.

ATR Percentage:

Calculates the Globex range (high minus low) and divides it by the daily ATR to express it as a percentage.

This metric helps traders gauge whether the overnight price movement is significant compared to the instrument’s typical volatility.

Time Handling:

Uses PST (UTC-8) for all time calculations, ensuring accurate session timing for users aligning with this timezone.

Properly handles overnight sessions that cross midnight, ensuring seamless tracking.

Input Settings

Globex Session Settings:

Show Globex Session: Enable/disable Globex session visualization (default: true).

Globex Start/End Time: Set the start and end times for the Globex session (default: 3:00 PM to 6:30 AM PST).

Globex Box Color: Customize the color of the Globex session box (default: semi-transparent gray).

Supply & Demand Zone Settings:

Show Supply & Demand Zone: Enable/disable zone visualization (default: true).

Zone Start/End Time: Set the start and end times for Supply & Demand zones (default: 6:00 AM to 8:00 AM PST).

Zone Box Color: Customize the color of the zone box (default: semi-transparent aqua).

General Settings:

Days to Look Back: Number of historical days to display zones (default: 10).

ATR Length: Period for calculating the daily ATR (default: 14).

Notes

All times are in Pacific Standard Time (PST). Adjust the start and end times if your market operates in a different timezone or if you prefer different session windows.

The indicator is optimized for instruments with active Globex sessions, such as futures. Results may vary for non-24/5 markets.

A typo in the label "Globe Low" (should be "Globex Low") will be corrected in future updates.

Ensure your TradingView chart is set to display sufficient historical data to view the full lookback period.

Why Use This Indicator?

The Globex Trap w/ Percentage indicator provides a unique combination of session-based range analysis, Supply & Demand zone identification, and volatility context via the ATR percentage. Whether you’re a day trader, swing trader, or scalper, this tool helps you:

Pinpoint key price levels where institutional traders may act.

Assess the significance of overnight price movements relative to daily volatility.

Identify potential trap zones for high-probability setups.

Customize the indicator to fit your trading style and market preferences.

Statistical FootprintStatistical Footprint - Behavioral Support & Resistance

This indicator identifies key price levels based on actual market behavior rather than traditional pivot calculations. It analyzes how bulls and bears have historically moved price from session opens, creating statistical zones where future reactions are most likely.

The concept is simple: track how far bullish candles typically push above the open versus how far bearish candles drop below it. These patterns reveal the market's behavioral "footprint" - showing where momentum typically stalls and reverses.

Key Features:

- Separate analysis for daily and weekly timeframes

- Smart zone merging when levels cluster together (within 5 points)

- Uses both mean and median calculations for more robust levels

- XGBoost-optimized lookback periods for maximum statistical significance

- Clean zone-only display focused on actionable price areas

How it Works:

The code separates bullish and bearish sessions, measuring their typical range extensions from the open. It then projects these statistical ranges forward from current session opens, creating "behavioral zones" where the market has historically shown consistent reactions.

When daily and weekly levels align closely, they merge into combined zones with enhanced significance. Labels show both the mean and median values when they differ meaningfully.

Best Used For:

- Identifying high-probability reversal zones

- Setting profit targets based on historical behavior

- Understanding market sentiment shifts at key levels

- Confluence analysis between different timeframes

The lookback periods have been optimized using machine learning to find the most predictive historical sample sizes for current market conditions.

Prev RTH FibsThis study captures the previous day’s Regular Trading Hours (RTH) range (default 09:30–16:00 America/New_York), then projects it onto the current session. It draws HIGH, LOW, and an optional 50% midpoint, plus a configurable set of inside fib-style percentages measured from the HIGH downward. Every level extends a short distance to the right of the current price and shows a clean numeric label (no box) on the right edge.

Key features

Prev-day RTH range tracked automatically; plotted each new session.

Inside levels (from HIGH ↓): 11%, 25%, 29.5%, 38.2%, 45%, 55%, 62% (OTE), 70.5%, 75%, 78.6%, 85% (toggle any on/off).

Clean right-side labels: numbers only, resizable (Tiny → Huge) with transparent background.

Line styling: HIGH/LOW and 50% are solid; inside levels can be Solid/Dashed/Dotted with independent color/width.

Smart right padding: lines/labels extend a few bars past the latest candle, so annotations stay beside price without violating TradingView’s “>500 bars in future” rule.

Works on any symbol/timeframe; RTH window and timezone are adjustable.

Inputs you control

Session: RTH session string and timezone.

Right-side padding (bars) and number size.

Visibility & style for HIGH, LOW, and 50%.

Which inside levels to show, plus their style/color/width.

Goldbach Time Indicator🔧 Key Fixes Applied:

1. Time Validation & Bounds Checking:

Hour/Minute Bounds: Ensures hours stay 0-23, minutes stay 0-59

Edge Case Handling: Prevents invalid time calculations from causing missing data

UTC Conversion Safety: Better handling of timezone edge cases

2. Enhanced Value Validation:

NA Checking: Validates all calculated values before using them

Goldbach Detection: Only flags valid, non-NA values as Goldbach hits

Plot Safety: Prevents plotting invalid or NA values that could cause gaps

3. Improved Plot Logic:

Core Level Colors: Blue for core levels (29,35,71,77), yellow/lime/orange for regular hits

Debug Mode Enhanced: Shows all calculations with gray dots when enabled

Better Filtering: Only plots positive, valid values for minus calculations

4. Background vs Dots Issue:

The large green/blue background you see suggests the indicator is detecting Goldbach times correctly, but the dots weren't plotting due to validation issues. This should now be fixed.

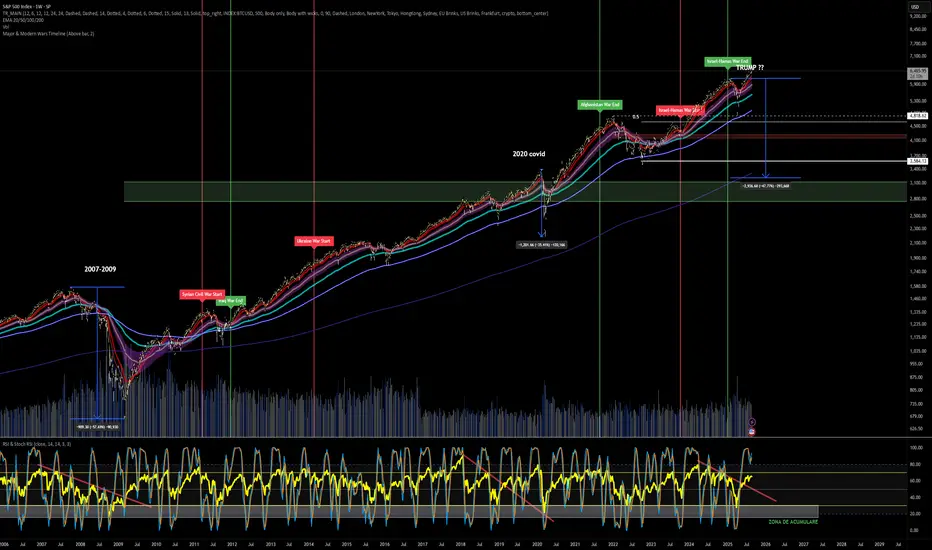

Major & Modern Wars TimelineDescription:

This indicator overlays vertical lines and labels on your chart to mark the start and end dates of major global wars and modern conflicts.

Features:

Displays start (red line + label) and end (green line + label) for each war.

Covers 20th century wars (World War I, World War II, Korean War, Vietnam War, Gulf War, Afghanistan, Iraq).

Includes modern conflicts: Syrian Civil War, Ukraine War, and Israel–Hamas War.

For ongoing conflicts, the end date is set to 2025 for timeline visualization.

Customizable: label position (above/below bar), line width.

Works on any chart timeframe, overlaying events on financial data.

Use case:

Useful for historical market analysis (e.g., gold, oil, S&P 500), helping traders and researchers see how wars and conflicts align with market movements.

Daily Start Vertical Lines (≤1H)This indicator automatically plots vertical lines at the start of each new trading day, based on the selected chart’s timezone. Unlike the default daily session boundaries (which often start at 17:00 New York time), this tool ensures that lines are drawn precisely at 00:00 midnight of the chart’s timezone.

🔹 Features:

Plots a vertical line at every new day start (midnight).

Fully time-zone aware → lines adjust automatically when you change the chart’s timezone.

Customizable line style, width, and color.

Option to limit plotting to specific timeframes (e.g., show only on ≤ 1H charts).

Lightweight & optimized (does not clutter higher-timeframe charts).

🔹 Use Cases:

Quickly identify daily boundaries for intraday analysis.

Helps scalpers and day traders align trades with new day opens.

Useful for strategies that depend on daily session resets.

This tool is especially helpful for traders who want clarity when working across different time zones.

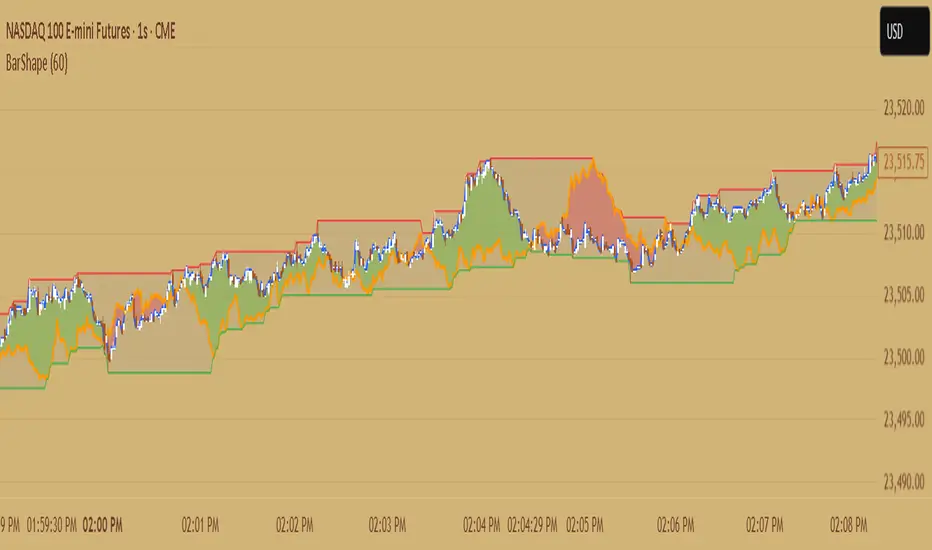

Candle ShapeCandle Shape

This indicator visualizes rolling candles that aggregate price action over a chosen lookback period, allowing you to see how OHLC dynamics evolve in real time.

Instead of waiting for a higher timeframe (HTF) bar to close, you can track its development directly from a lower timeframe chart.

For example, view how a 1-hour candle is forming on a 1-minute chart — complete with rolling open, high, low, and close levels, as well as colored body and wick areas.

---

🔹 How it works

- Lookback Period (n) → sets the bucket size, defining how many bars are merged into a “meta-candle.”

- The script continuously updates the meta-open, meta-high, meta-low, and meta-close.

- Body and wick areas are filled with color , making bullish/bearish transitions easy to follow.

---

🔹 Use cases

- Monitor the intra-development of higher timeframe candles.

- Analyze rolling OHLC structures to understand how price dynamics shift across different aggregation windows.

- Explore unique perspectives for strategy confirmation, breakout anticipation, and market structure analysis.

---

✨ Candle Shape bridges the gap between timeframes and uncovers new layers of price interaction.