Fourier Extrapolator of Price w/ Projection Forecast [Loxx]Due to popular demand, I'm pusblishing Fourier Extrapolator of Price w/ Projection Forecast.. As stated in it's twin indicator, this one is also multi-harmonic (or multi-tone) trigonometric model of a price series xi, i=1..n, is given by:

xi = m + Sum( a*Cos(w*i) + b*Sin(w*i), h=1..H )

Where:

xi - past price at i-th bar, total n past prices;

m - bias;

a and b - scaling coefficients of harmonics;

w - frequency of a harmonic ;

h - harmonic number;

H - total number of fitted harmonics.

Fitting this model means finding m, a, b, and w that make the modeled values to be close to real values. Finding the harmonic frequencies w is the most difficult part of fitting a trigonometric model. In the case of a Fourier series, these frequencies are set at 2*pi*h/n. But, the Fourier series extrapolation means simply repeating the n past prices into the future.

This indicator uses the Quinn-Fernandes algorithm to find the harmonic frequencies. It fits harmonics of the trigonometric series one by one until the specified total number of harmonics H is reached. After fitting a new harmonic , the coded algorithm computes the residue between the updated model and the real values and fits a new harmonic to the residue.

see here: A Fast Efficient Technique for the Estimation of Frequency , B. G. Quinn and J. M. Fernandes, Biometrika, Vol. 78, No. 3 (Sep., 1991), pp . 489-497 (9 pages) Published By: Oxford University Press

The indicator has the following input parameters:

src - input source

npast - number of past bars, to which trigonometric series is fitted;

Nfut - number of predicted future bars;

nharm - total number of harmonics in model;

frqtol - tolerance of frequency calculations.

The indicator plots two curves: the green/red curve indicates modeled past values and the yellow/fuchsia curve indicates the modeled future values.

The purpose of this indicator is to showcase the Fourier Extrapolator method to be used in future indicators.

Fourier

Fourier Extrapolator of Price [Loxx]Fourier Extrapolator of Price is a multi-harmonic (or multi-tone) trigonometric model of a price series xi, i=1..n, is given by:

xi = m + Sum( a *Cos(w *i) + b *Sin(w *i), h=1..H )

Where:

xi - past price at i-th bar, total n past prices;

m - bias;

a and b - scaling coefficients of harmonics;

w - frequency of a harmonic;

h - harmonic number;

H - total number of fitted harmonics.

Fitting this model means finding m, a , b , and w that make the modeled values to be close to real values. Finding the harmonic frequencies w is the most difficult part of fitting a trigonometric model. In the case of a Fourier series, these frequencies are set at 2*pi*h/n. But, the Fourier series extrapolation means simply repeating the n past prices into the future.

This indicator uses the Quinn-Fernandes algorithm to find the harmonic frequencies. It fits harmonics of the trigonometric series one by one until the specified total number of harmonics H is reached. After fitting a new harmonic, the coded algorithm computes the residue between the updated model and the real values and fits a new harmonic to the residue.

see here: A Fast Efficient Technique for the Estimation of Frequency , B. G. Quinn and J. M. Fernandes, Biometrika, Vol. 78, No. 3 (Sep., 1991), pp. 489-497 (9 pages) Published By: Oxford University Press

The indicator has the following input parameters:

src - input source

npast - number of past bars, to which trigonometric series is fitted;

nharm - total number of harmonics in model;

frqtol - tolerance of frequency calculations.

The indicator plots the modeled past values

The purpose of this indicator is to showcase the Fourier Extrapolator method to be used in future indicators. While this method can also prediction future price movements, for our purpose here we will avoid doing.

OPAL - Sense→ Hi everyone, very proud to publish my unique leading oscillator ! ←

Sense is a "leading indicator" : it shows what can happen in the future, meanwhile a lagging indicator like MAs shows past sentiment.

Sense diverging with Price ? Care at the reversal !

It can be a great tool to upgrade your timings, after a divergence for example, to snipe reversals or to find Trend entries.

This tool is used for sniping in our levels trading setup (in our trading community)

Sense is made of everything you know about common indicators :

RSI/STOCH/STOCHRSI/MFI/RVSI/PZO/VZO/MOMENTUM/VOLUMES/UO

>>> Basically shows situations where almost all the known indicators reach interesting points in Overbought and Oversold zones

Signals provided :

*Visible and Hidden Minor OB/OS Crosses (Small Arrows)

*Visible and Hidden Major OB/OS Crosses (Bigger Arrows)

*Visible and Hidden Major and Minor Confluence in OB/OS Zones (Rockets/Blood)

*Background Smart Coloring when price reaches OB/OS Zones :

- blue/purple = entering OB/OS Zones

- green/red = extrem multiple OB/OS situation

*Coloration of Middle Line based on std Price Deviation

*Smart Divergences spotting : applied level filter to get divergences that reached OB/OS Zones at least once.

Divergences are scanned twice for confirmation<

*Full alerting system on :

- Full signals = blood and rockets

- Half signals = bigger arrows

- Minor signals = small arrows

- Dual Divergences = on both oscillators (slow & fast)

1) What is the curve i see on Sense ? => It is my homemade oscillator, described above

2) What are thoses Zones around the curve ? => Overbought/Oversold Zones

3) What are those dots on the curve ? => When the oscillator crosses its Triggerline

4) What are those little arrows ? => Printing minor Overbought/Oversold situations

5) What are those bigger arrows ? => Printing major Overbought/Oversold situations

6) What are those Blood dots/ Rockets ? => Printing Confluence situations in Overbought/Oversold Zones

7) Why is background coloring ? => I applied smart coloration based on oscillators location (see above coloration meaning)

8) What are those lines between curve spikes ? => Situations when Price and oscillator are doing different moves, basically divergences, meaning a correction can happen sooner or later

Should be strong on almost every timeframe !

Always backtest, watch, then use or not in your trading strategy.

If you like my work, leave a like :)

Hoping you success !

Function Sawtooth WaveThis is an indicator to draw a sawtooth wave on the chart.

It can be a useful perspective, as decaying markets tend to oscillate in reverse sawtooth waves, and bullish markets can oscillate in conventional sawtooth waves. With the right inputs, it can be an early warning signal for potential movements.

Something I've noted is that large waves cause a ripple effect and sets the frequency for the market until a change occurs. Sawtooth waves may help in capturing ripple waves.

Useful inputs are:

- Average True Range as wave height (amplitude)

- Periodicity of market as wave duration (frequency)

(Inputs will change the wave from conventional to reverse)

I hope that it is helpful.

GLHF

- DPT

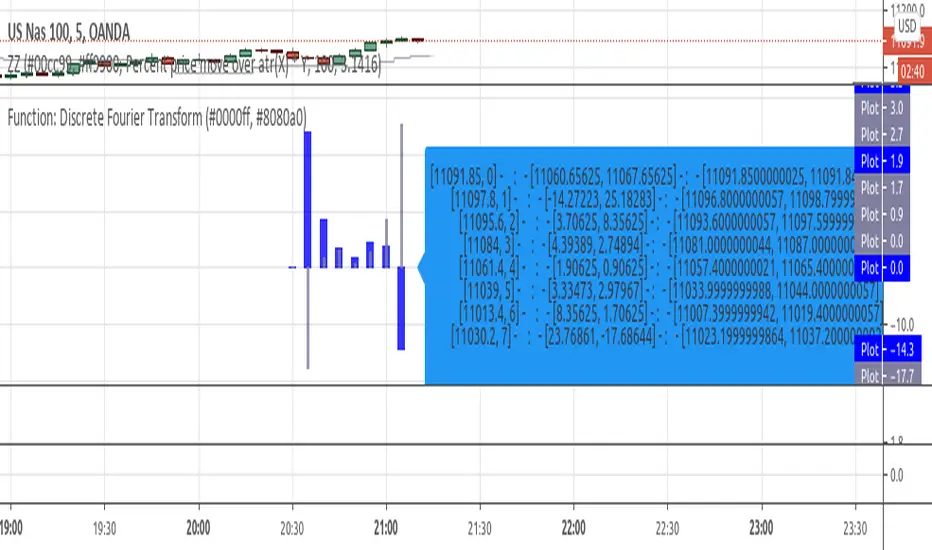

Function: Discrete Fourier TransformExperimental:

function for inverse and discrete fourier transform in one, if you notice errors please let me know! use at your own risk...

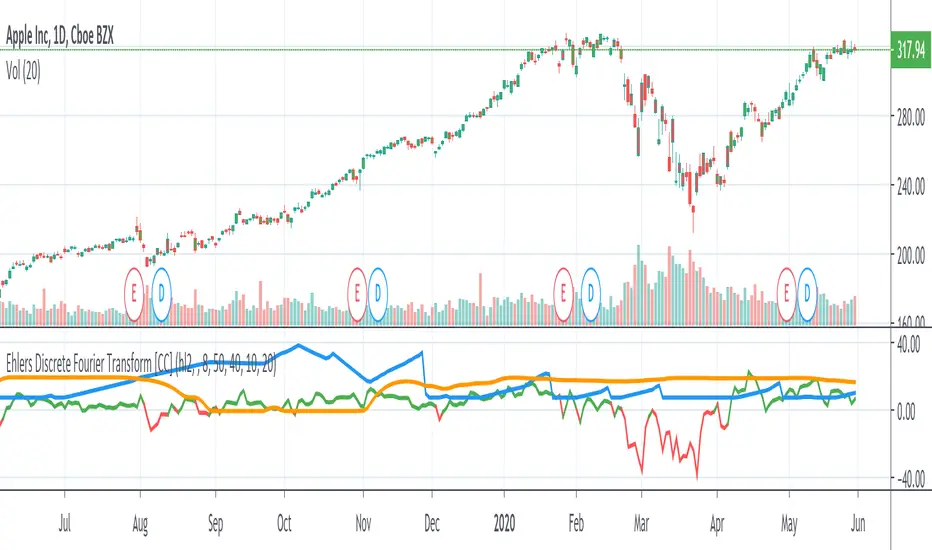

Ehlers Discrete Fourier TransformThe Discrete Fourier Transform Indicator was written by John Ehlers and more details can be found at www.mesasoftware.com

I have color coded everything as follows: blue line is the dominant cycle, orange line is the power converted to decibels, and I have marked the other line as red if you should sell or green if you should buy

Let me know if you would like to see me write any other scripts!

Low Frequency Fourier TransformThis Study uses the Real Discrete Fourier Transform algorithm to generate 3 sinusoids possibly indicative of future price.

I got information about this RDFT algorithm from "The Scientist and Engineer's Guide to Digital Signal Processing" By Steven W. Smith, Ph.D.

It has not been tested thoroughly yet, but it seems that that the RDFT isn't suited for predicting prices as the Frequency Domain Representation shows that the signal is similar to white noise, showing no significant peaks, indicative of very low periodicity of price movements.

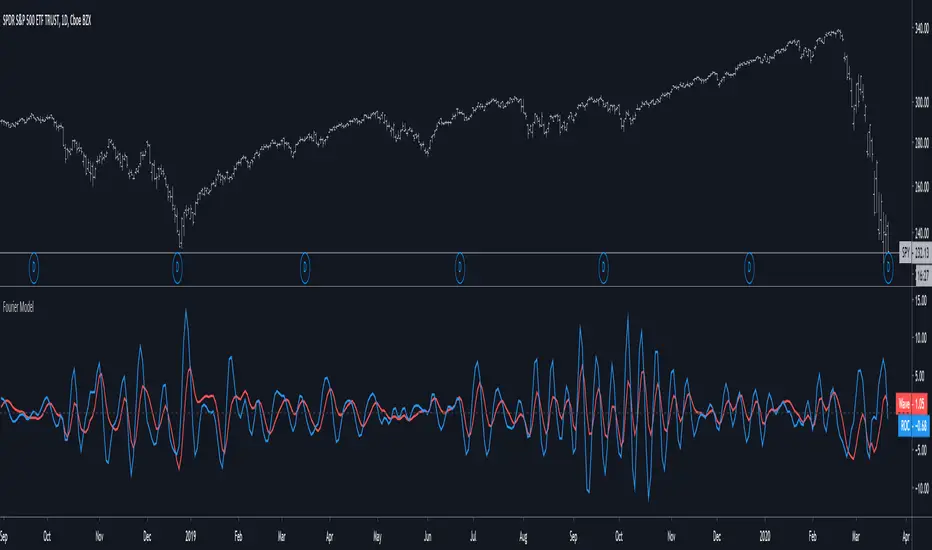

[e2] Fourier series Model Of The MarketFourier series Model Of The Market

John F. Ehlers

TASC Jun 2019

Regularized Volume Zone Oscillator FSVZORegularized VZO

Vanilla in link below

White noise and 1 confirm auto divs included