ניהול פורטפוליו

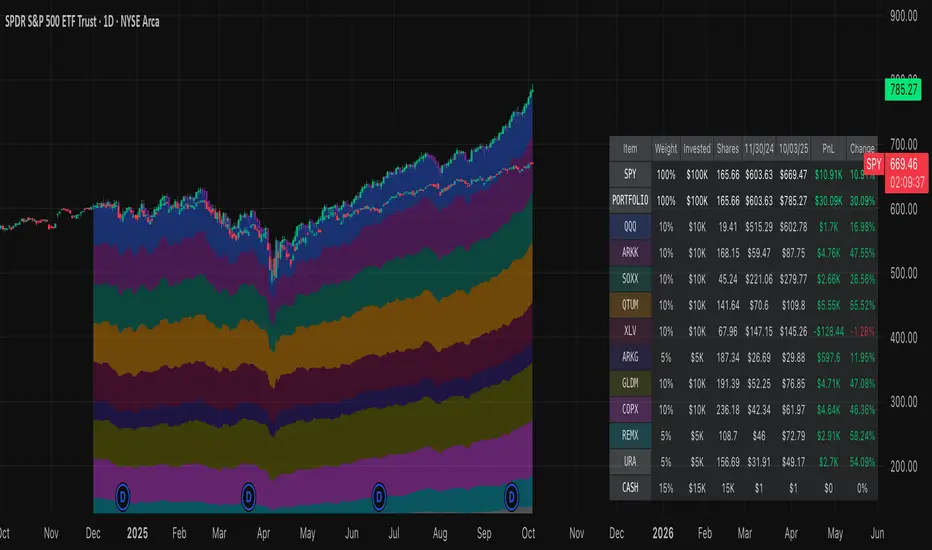

Normalized Portfolio TrackerThis script lets you create, visualize, and track a custom portfolio of up to 15 assets directly on TradingView.

It calculates a synthetic "portfolio index" by combining multiple tickers with user-defined weights, automatically normalizing them so the total allocation always equals 100%.

All assets are scaled to a common starting point, allowing you to compare your portfolio’s performance versus any benchmark like SPY, QQQ, or BTC.

🚀 Goal

This script helps traders and investors:

• Understand the combined performance of their portfolio.

• Normalize diverse assets into a single synthetic chart .

• Make portfolio-level insights without relying on external spreadsheets.

🎯 Use Cases

• Backtest your portfolio allocations directly on the chart.

• Compare your portfolio vs. benchmarks like SPY, QQQ, BTC.

• Track thematic baskets (commodities, EV supply chain, regional ETFs).

• Visualize how each component contributes to overall performance.

📊 Features

• Weighted Portfolio Performance : Combines selected assets into a synthetic value series.

• Base Price Alignment : Each asset is normalized to its starting price at the chosen date.

• Dynamic Portfolio Table : Displays symbols, normalized weights (%), equivalent shares (based on each asset’s start price, sums to 100 shares), and a total row that always sums to 100%.

• Multi-Asset Support : Works with stocks, ETFs, indices, crypto, or any TradingView-compatible symbol.

⚙️ Configuration

Flexible Portfolio Setup

• Add up to 15 assets with custom weight inputs.

• You can enter any arbitrary numbers (e.g. 30, 15, 55).

• The script automatically normalizes all weights so the total allocation always equals 100%.

Start Date Selection

• Choose any custom start date to normalize all assets.

• The portfolio value is then scaled relative to the main chart symbol, so you can directly compare portfolio performance against benchmarks like SPY or QQQ.

Chart Styles

• Candlestick chart

• Heikin Ashi chart

• Line chart

Custom Display

• Adjustable colors and line widths

• Optionally display asset list, normalized weights, and equivalent shares

⚙️ How It Works

• Fetch OHLC data for each asset.

• Normalizes weights internally so totals = 100%.

• Stores each asset’s base price at the selected start date.

• Calculates equivalent “shares” for each allocation.

• Builds a synthetic portfolio value series by summing weighted contributions.

• Renders as Candlestick, Heikin Ashi, or Line chart.

• Adds a portfolio info table for clarity.

⚠️ Notes

• This script is for visualization only . It does not place trades or auto-rebalance.

• Weight inputs are automatically normalized, so you don’t need to enter exact percentages.

DCA vs One-ShotCompare a DCA strategy by choosing the payment frequency (daily, weekly, or monthly), and by choosing whether or not to pay on weekends for cryptocurrency. You can add fees and the reference price (opening, closing, etc.).

LB PortLag Exit IndicatorAllows you to compare a benchmark against any asset over the last X candles. Simple.

Dynamic Levels This indicator plots key price levels (Open, High, Low, Mid, Close) from multiple higher timeframes (Monday, Daily, Weekly, Monthly, Yearly).

It allows you to track how price interacts with important reference levels without switching timeframes.

🔑 Features

✅ Monday levels (MO, MH, MM)

By default: shows the last completed Monday (fixed values).

Option: “live mode” to update Monday High/Low/Mid while Monday’s candle is forming.

✅ Daily levels (DO, DH, DL, DM, DC)

Live: Daily High/Low/Mid update dynamically while today’s candle is forming.

Previous Daily Close (DC) is always fixed.

✅ Weekly levels (WO, WH, WL, WM)

Live: Weekly High/Low/Mid update dynamically while this week’s candle is forming.

Weekly Open is fixed.

✅ Monthly levels (MO(n), MH(n-1), ML(n-1), MM(n-1), MC(n-1))

Shows last completed month’s values (constant, never changing).

Current Monthly Open is also shown (naturally fixed).

✅ Yearly levels (YO(n), YH(n-1), YL(n-1), YM(n-1), YC(n-1))

Shows last completed year’s values (constant, never changing).

Current Yearly Open is also shown (naturally fixed).

🎨 Customization

Toggle each level (on/off) in indicator settings.

Individual color settings for Monday, Daily, Weekly, Monthly, and Yearly.

Adjustable line width and transparency.

Optional short labels (MO, DO, WM, etc.) displayed on the right side of the chart.

🔄 Dynamic Logic

Daily and Weekly → update dynamically while their candle is forming.

Monday, Monthly, and Yearly → use fixed values from the last completed bar (do not “breathe”).

📌 Use cases

Quickly see where price stands relative to previous close, current open, or mid-levels.

Use Monday Open/High/Mid as strong intraday references.

Use Monthly/Yearly levels as long-term support/resistance zones.

Dynamic Levels: Mon + D/W/M/Y (O/H/L/C/Mid)Purpose!

This Pine Script plots key reference levels (Open,High,Low,Close,Mid) for Monday,Daily,Weekly, Monthly, and Yearly timeframes.

All levels update live while the bar is forming. ( intrabar updates).

USAGE

Add the script to Pine Editor on TradingView (desktop Web)

Save - Add to chart

On mobile app: Find it under indicators - My scripts.

Great for identifying key reaction zones (opens,mids,previous closes).

Interval Price AlertsInterval Price Alerts

A versatile indicator that creates horizontal price levels with customizable alerts. Perfect for tracking multiple price levels simultaneously without having to create individual horizontal lines manually.

Features:

• Create evenly spaced price levels between a start and end price

• Customizable price interval spacing

• Optional price labels with flexible positioning

• Alert capabilities for both price crossovers and crossunders

• Highly customizable visual settings

Settings Groups:

1. Price Settings

• Start Price: The lower boundary for price levels

• End Price: The upper boundary for price levels

• Price Interval: The spacing between price levels

2. Line Style

• Line Color: Choose any color for the price level lines

• Line Style: Choose between Solid, Dashed, or Dotted lines

• Line Width: Adjustable from 2-4 pixels (optimized for opacity)

• Line Opacity: Control the transparency of lines (0-100%)

3. Label Style

• Show Price Labels: Toggle price labels on/off

• Label Color: Customize label text color

• Label Size: Choose from Tiny, Small, Normal, or Large

• Label Position: Place labels on Left or Right side

• Label Background: Set the background color

• Background Opacity: Control label background transparency

• Text Opacity: Adjust label text transparency

4. Alert Settings

• Alert on Crossover: Enable/disable upward price cross alerts

• Alert on Crossunder: Enable/disable downward price cross alerts

Usage Tips:

• Great for marking key price levels, support/resistance zones

• Useful for tracking multiple entry/exit points

• Perfect for scalping when you need to monitor multiple price levels

• Ideal for pre-market planning and level setting

Notes:

• Line width starts at 2 for optimal opacity rendering

• Labels can be fully customized or hidden completely

• Alert messages include the symbol and price level crossed

Fed Rate Change Impact📊 Fed Rate Change Impact — Macro Event-Driven Indicator

Fed Rate Change Impact is an advanced indicator designed to analyze the impact of Federal Reserve interest rate changes on financial markets. It integrates event-driven logic with dynamic visualization, percentage diagnostics, and multi-asset selection, offering a clear and customizable view of post-event effects.

🔍 Key Features 📅 Preloaded Fed Events : Includes over 30 historical rate cut (↓) and hike (↑) dates from 2008 to 2024.

📈 Post-Event Analysis : Calculates the percentage change of the selected asset 5, 10, and 30 days after each event.

📌 Vertical Chart Lines : Visually highlights each event directly on the chart, with dynamic coloring (red for hikes, green for cuts).

📋 Diagnostic Table : Displays real-time impact for each event, with color-coded values and a compact layout.

🧠 Interactive Filter: Choose to display only hikes, only cuts, or both.

🧭 Flexible Asset Selection : Analyze the current chart asset, pick from a predefined list, or manually input any ticker via input.symbol().

🎯 Contextual Highlighting : The table highlights the analyzed asset if it matches the active chart symbol.

⚙️ Customizable Parameters lookahead5, lookahead10, lookahead30: Define the time horizon for measuring post-event impact.

eventFilter : Choose which type of events to display.

presetAsset / customAsset : Select or input the asset to analyze.

🧪 Recommended Use Cases Macroeconomic analysis on indices, commodities, crypto, and forex

Studying delayed effects of rate changes on sensitive assets

Building event-driven strategies or diagnostic overlays

Visual backtesting and cross-asset comparison

🧠 Technical Notes The indicator is compatible with overlay=true and works best on Daily timeframe.

The table automatically adapts to the number of events and includes visual padding for improved readability.

All calculations are performed in real time and require no external data.

Expected Value Monte CarloI created this indicator after noticing that there was no Expected Value indicator here on TradingView.

The EVMC provides statistical Expected Value to what might happen in the future regarding the asset you are analyzing.

It uses 2 quantitative methods:

Historical Backtest to ground your analysis in long-term, factual data.

Monte Carlo Simulation to project a cone of probable future outcomes based on recent market behavior.

This gives you a data-driven edge to quantify risk, and make more informed trading decisions.

The indicator includes:

Dual analysis: Combines historical probability with forward-looking simulation.

Quantified projections: Provides the Expected Value ($ and %), Win Rate, and Sharpe Ratio for both methods.

Asset-aware: Automatically adjusts its calculations for Stocks (252 trading days) and Crypto (365 days) for mathematical accuracy.

The projection cone shows the mean expected path and the +/- 1 standard deviation range of outcomes.

No repainting

Calculation:

1. Historical Expected Value:

This is a systematic backtest over thousands of bars. It calculates the return Rᵢ for N past trades (buy-and-hold). The Historical EV is the simple average of these returns, giving a baseline performance measure.

Historical EV % = (Σ Rᵢ) / N

2. Monte Carlo Projection:

This projection uses the Geometric Brownian Motion (GBM) model to simulate thousands of future price paths based on the market's recent behavior.

It first measures the drift (μ), or recent trend, and volatility (σ), or recent risk, from the Projection Lookback period. It then projects a final return for each simulation using the core GBM formula:

Projected Return = exp( (μ - σ²/2)T + σ√T * Z ) - 1

(Where T is the time horizon and Z is a random variable for the simulation.)

The purple line on the chart is the average of all simulated outcomes (the Monte Carlo EV). The cone represents one standard deviation of those outcomes.

The dashed lines represent one standard deviation (+/- 1σ) from the average, forming a cone of probable outcomes. Roughly 68% of the simulated paths ended within this cone.

This projection answers the question: "If the recent trend and volatility continue, where is the price most likely to go?"

Here's how to read the indicator

Expected Value ($/%): Is my average trade profitable?

Win Rate: How often can I expect to be right?

Sharpe Ratio: Am I being adequately compensated for the risk I'm taking?

User Guide

Max trade duration (bars): This is your analysis timeframe. Are you interested in the probable outcome over the next month (21 bars), quarter (63 bars), or year (252 bars)?

Position size ($): Set this to your typical trade size to see the Expected Value in real dollar terms.

Projection lookback (bars): This is the most important input for the Monte Carlo model. A short lookback (e.g., 50) makes the projection highly sensitive to recent momentum. Use this to identify potential recency bias. A long lookback (e.g., 252) provides a more stable, long-term projection of trend and volatility.

Historical Lookback (bars): For the historical backtest, more data is always better. Use the maximum that your TradingView plan allows for the most statistically significant results.

Use TP/SL for Historical EV: Check this box to see how the historical performance would have changed if you had used a simple Take Profit and Stop Loss, rather than just holding for the full duration.

I hope you find this indicator useful and please let me know if you have any suggestions. 😊

DCA Cost Basis (with Lump Sum)DCA Cost Basis (with Lump Sum) — Pine Script v6

This indicator simulates a Dollar Cost Averaging (DCA) plan directly on your chart. Pick a start date, choose how often to buy (daily/weekly/monthly), set the per-buy amount, optionally add a one-time lump sum on the first date, and visualize your evolving average cost as a VWAP-style line.

Features

Customizable DCA Plan — Set Start Date , buy Frequency (Daily / Weekly / Monthly), and Recurring Amount (in quote currency, e.g., USD).

Lump Sum Option — Add a one-time lump sum on the very first eligible date; recurring DCA continues automatically after that.

Cost Basis Line — Plots the live average price (Total Cost / Total Units) as a smooth, VWAP-style line for instant breakeven awareness.

Buy Markers — Optional triangles below bars to show when simulated buys occur.

Performance Metrics — Tracks:

Total Invested (quote)

Total Units (base)

Cost Basis (avg entry)

Current Value (mark-to-market)

CAGR (Annualized) from first buy to current bar

On-Chart Summary Table — Displays Start Date, Plan Type (Lump + DCA or DCA only), Total Invested, and CAGR (Annualized).

Data Window Integration — All key values also appear in the Data Window for deeper inspection.

Why use it?

Visualize long-term strategies for Bitcoin, crypto, or stocks.

See how a lump sum affects your average entry over time.

Gauge breakeven at a glance and evaluate historical performance.

Note: This tool is for educational/simulation purposes. Results are based on bar closes and do not represent live orders or fees.

Market Order Risk CalculatorObviously the Long/Short Position tool does this, but when you are scalping, 10 - 15 seconds matters. What matters more than that is defined risk, you dont want your losses being scattered, 300 here 145 there, you want consistent risk to have consistent data.

What this does is when you are framing a trade, it provides a hands off tool that tells you exactly how many contracts to enter with, that way if you have bracket orders on, your stop will be exactly where you want it to be without going over your defined risk.

IU Trade ManagementDESCRIPTION

IU Trade Management is a powerful utility tool designed to help traders manage their trades with precision and clarity. It provides automated Stop Loss, Take Profit, and Break Even calculations using multiple customizable methods. Along with clear SL/TP plotting on the chart, it also displays a detailed trade status table that tracks every important detail including entry price, SL/TP levels, break-even, PNL, and trade duration. This tool is perfect for traders who want to manage risk and rewards visually and systematically.

USER INPUTS :

-Entry Candle Time: Default 20 Jul 2021 00:00 +0300 (select the candle from which the trade begins)

- Entry Price: Default 2333 (define the price at which the trade is executed)

- Trade Direction: Default Long (choose between Long or Short)

- SL/TP Method: Default ATR (options: ATR, Points/Pips, Percentage %, Standard Deviation, Highest/Lowest, Previous High/Low)

- Risk to Reward: Default 3 (set custom risk-to-reward ratio)

- Use Break Even: Default false (option to enable break-even)

- Plot Break Even Line: Default false (option to display BE line)

- RTR of Break Even Point: Default 2 (factor used for BE calculation)

SL/TP Method Specific Inputs:

- ATR Length: Default 14

- ATR Factor: Default 2

- Points/Pips: Default 100

- Percentage: Default 1%

- Standard Deviation Length: Default 20

- Standard Deviation Factor: Default 2

- Highest/Lowest Length: Default 10

Trade Status Table Settings:

- Show Trade Status: Default true

- Table Size: Default small (options: normal, tiny, small, large)

- Table Position: Default top right

- Frame Width: Default 2

- Table Color: Default black

- Frame Color: Default gray

- Border Width: Default 2

- Border Color: Default gray

- Text Color: Default purple (RGB 212, 0, 255)

HOW TO USE THE INDICATOR:

1. Set the entry candle time and entry price manually.

2. Select whether the trade is Long or Short.

3. Choose the preferred SL/TP calculation method (ATR, Percentage, Points, STD, High/Low, Previous High/Low).

4. Define your risk-to-reward ratio and enable break-even if required.

5. The indicator will automatically plot your Entry, Stop Loss, Take Profit, and Break Even levels on the chart.

6. A detailed trade management table will appear, showing trade direction, SL, TP, PNL (points and %), SL/TP method, and total trade time.

WHY IT IS UNIQUE:

- Offers multiple methods to calculate SL and TP (ATR, Percentage, Points, Standard Deviation, High/Low, Previous High/Low)

- Built-in Break Even functionality for risk-free trade management

- Real-time PNL tracking in both points and percentage

- Trade status table for complete transparency on all trade details

- Visual plotting of SL, TP, and Entry with color-coded zones for clarity

HOW USER CAN BENEFIT FROM IT :

- Helps traders manage risk and reward with discipline

- Eliminates guesswork by automating SL and TP levels

- Provides clear visual guidance on trade exits and risk management

- Enhances decision-making with live trade tracking and performance statistics

- Suitable for manual traders as a trade manager and for strategy developers as a risk management reference

Stop Loss vs Take Profit Probability and EVThis stop loss and take profit calculator uses a Monte Carlo simulation to calculate the probability of hitting your Stop Loss or Take Profit levels across different time horizons (expressed in bars).

It provides data-driven insights to optimize your risk management and position sizing by showing Expected Value for each scenario.

As a quant, I love using statistical data to help my decisions and get better EV from my trades.

🔬 How It's Calculated

Monte Carlo Simulation: Runs 1,000-10,000 price simulations using a random walk model

Volatility Analysis: Combines ATR-based and Historical Volatility for accurate price movement modeling

Expected Value: Calculates profit/loss expectation using formula: (TP_Probability × Reward) - (SL_Probability × Risk)

Time Horizons: Tests multiple timeframes (1, 5, 10, 20, 50 bars) to find optimal holding periods

Risk/Reward Ratios: Automatically calculates and displays R:R ratios for quick assessment

💡 Use Cases

Position Sizing - Determine optimal risk per trade based on Expected Value

Time Horizon Optimization - Find the best holding period for your strategy

Stop Loss Placement - Validate SL levels using probability analysis

Take Profit Optimization - Set TP levels with statistical backing

Strategy Backtesting - Compare different R:R setups before entering trades

Risk Management - Avoid trades with negative Expected Value

Swing vs Day Trading - Choose timeframes with highest success probability

🎯 How to Use

Setup Trade: Enter your entry price, stop loss, and take profit levels

You can add or remove time horizons denominated in bars. Say you are looking at 1h candles, adding a 24-bar time horizon means you are looking into 24 hours

Choose Direction: Select Long or Short position

Review Table

Analyze Expected Value: Focus on positive EV scenarios (green background)

Optimize Timing: Select time horizons with best risk/reward profile

Adjust Parameters: Modify volatility calculation method and simulation count if needed

Examples

Here's how you can read the tables.

Example 1:

In this chart, we are analyzing the TP and SL probabilities as well as the EV (expected value) for a stock. I want to check what the likelihood is that my SL and TP get triggered over the next 5 days. The stock market is open for 6.5 hours per day, which is 13 bars in this 30-minute bar chart. 26 bars is 2 days, 39 bars is 3 days and so on.

Although this trade is more likely to trigger my SL than my TP, in some of the time horizons we have a positive expected value because of the risk/reward of our trade (i.e. distance of the SL and TP from the price) and the probability of hitting SL and TP.

Example 2:

In this example, we have applied the indicator to gold. Because the TP is much closer to the price, the probability of hitting the TP is much higher.

We can also observe that the expected Value in the shorter time frames is better than in the longer ones. This can give us some clues to set up our trade. If we know that the EV is positive, we can allocate more to that specific trade.

Enjoy, and please let me know your feedback! 😊🥂

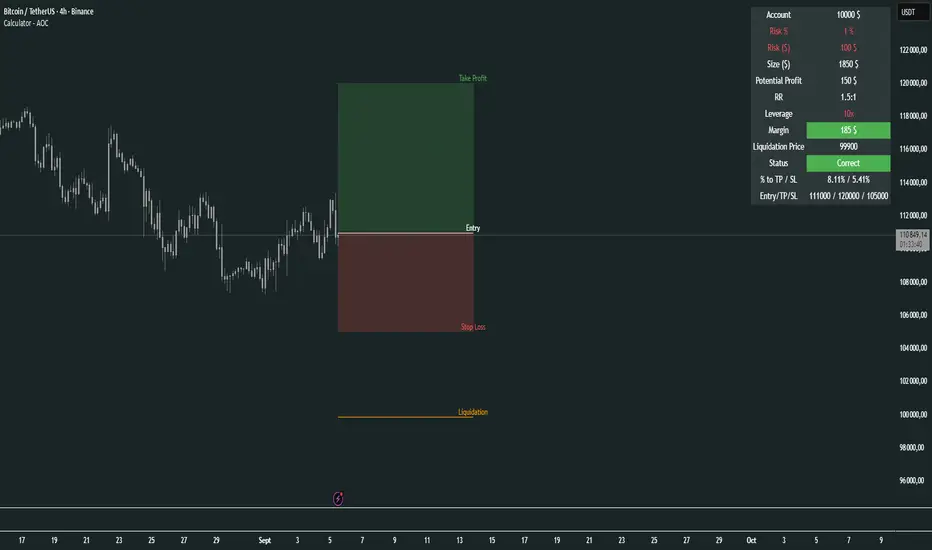

Calculator - AOC📊 Calculator - AOC Indicator 🚀

The Calculator - AOC indicator is a powerful and user-friendly tool designed for TradingView to help traders plan and visualize trades with precision. It calculates key trade metrics, displays entry, take-profit (TP), stop-loss (SL), and liquidation levels, and provides a clear overview of risk management and potential profits. Perfect for both novice and experienced traders! 💡

✨ Features

📈 Trade Planning: Input your Entry Price, Take Profit (TP), Stop Loss (SL), and Trade Direction (Long/Short) to visualize your trade setup on the chart.

💰 Risk Management: Set your Initial Capital and Risk per Trade (%) to calculate the optimal Position Size and Risk Amount for each trade.

⚖️ Leverage Support: Define your Leverage to compute the Required Margin and Liquidation Price, ensuring you stay aware of potential risks.

📊 Risk/Reward Ratio: Automatically calculates the Risk-to-Reward Ratio to evaluate trade profitability.

🎨 Visuals: Displays Entry, TP, SL, and Liquidation levels as lines and boxes on the chart, with customizable Line Width, Line Style, and Label Size.

✅ Trade Validation: Checks if your trade setup is valid (e.g., correct TP/SL placement) and highlights issues like potential liquidation risks with color-coded statuses (Correct ✅, Incorrect ❌, or Liquidation ⚠️).

📋 Summary Table: A clean, top-right table summarizes key metrics: Capital, Risk %, Risk Amount, Position Size, Potential Profit, Risk/Reward, Margin, Liquidation Price, Trade Status, and % to TP/SL.

🖌️ Customization: Adjust Line Extension (Bars) for how far lines extend, and choose from Solid, Dashed, or Dotted line styles for a personalized chart experience.

🛠️ How to Use

Add to Chart: Apply the indicator to your TradingView chart.

Configure Inputs:

Accountability: Set your Initial Capital and Risk per Trade (%).

Target: Enter Entry Price, TP, and SL prices.

Leverage: Specify your leverage (e.g., 10x).

Direction: Choose Long or Short.

Display Settings: Customize Line Width, Line Style, Label Size, and Line Extension.

Analyze: The indicator plots Entry, TP, SL, and Liquidation levels on the chart and displays a table with all trade metrics.

Validate: Check the Trade Status in the table to ensure your setup is valid or if adjustments are needed.

🎯 Why Use It?

Plan Smarter: Visualize your trade setup and understand your risk/reward profile instantly.

Stay Disciplined: Precise position sizing and risk calculations help you stick to your trading plan.

Avoid Mistakes: Clear validation warnings prevent costly errors like incorrect TP/SL placement or liquidation risks.

User-Friendly: Intuitive visuals and a summary table make trade analysis quick and easy.

📝 Notes

Ensure Entry, TP, and SL prices align with your trade direction to avoid "Incorrect" or "Liquidation" statuses.

The indicator updates dynamically on the latest bar, ensuring real-time visuals.

Best used with proper risk management to maximize trading success! 💪

Happy trading! 🚀📈

SP500 Weekly Posture Ribbon (EMA10W)Check if the SP500 is bullish or bearish. Do not buy stocks when SP500 is bearish.

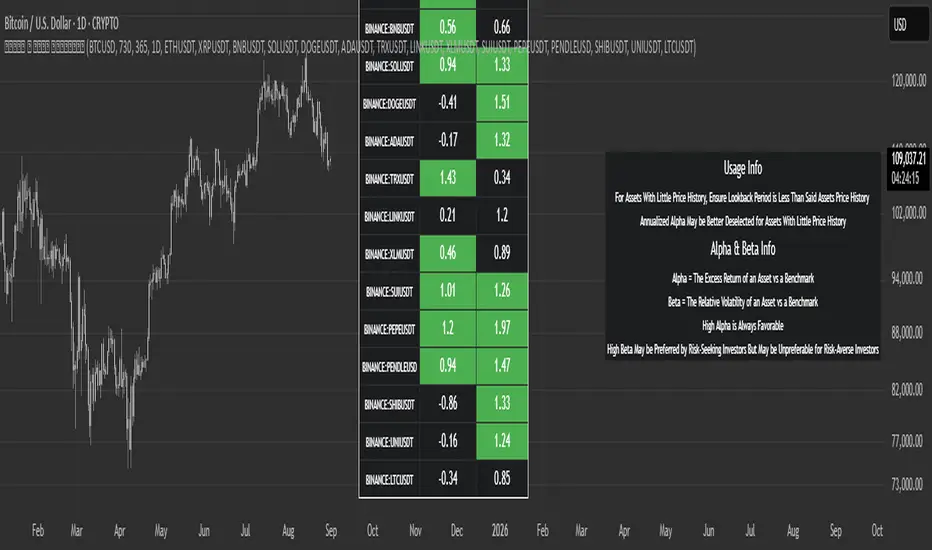

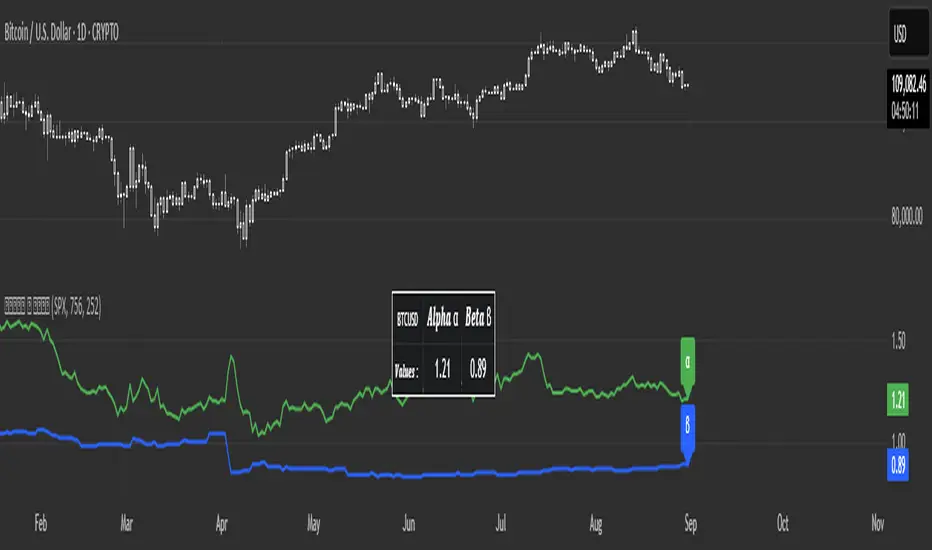

Rolling Performance Toolkit (Returns, Correlation and Sharpe)This script provides a flexible toolkit for evaluating rolling performance metrics between any asset and a benchmark.

Features:

Library-based: Built on a custom utilities library for consistent return and statistics calculations.

Rolling Window Control: Choose the lookback period (in days) to calculate metrics.

Multiple Modes: Toggle between Rolling Returns, Rolling Correlation, and Rolling Sharpe Ratio.

Benchmark Comparison: Compare your selected ticker against a benchmark (default: S&P 500 / SPX), but you can easily switch to any symbol.

Risk-Free Rate Options: Choose from zero, a constant annual % rate, or a proxy symbol (default: US03M – 3-Month Treasury Yield).

Annualized Sharpe: Sharpe ratios are annualized by default (×√252) for intuitive interpretation.

This tool is useful for traders and investors who want to monitor relative performance, diversification benefits, or risk-adjusted returns over time.

RDT Buy/Sell Signals Scalp 1MExit alerts for scalps for the 1m chart.

An alert is triggered, if a 1m candle ended and a 3/8 EMA cross was created in the according direction (depending on whether Long or Short Exit alert is set).

Entry alerts basically work the same. I've never ever used them so far though, since it never made sense the way I trade.

More infos: www.reddit.com

15/30M Alerts"X Candle Close":

Same as in 5m Enter alert: it's really helpful to wait for a 15m/30m candle to be confirmed, to see f. e. whether a candle really broke a support / resistance or not - and to prevent making bad decisions.

More infos: www.reddit.com

1D Exit Alerts"A Daily Exit LONG" + "B Daily Exit SHORT":

I'm not using this one anymore since they often make me worry more than necessary, and I focus more on aiming to reach specific price targets, or using the 5m Exit alerts instead.

Also swing trades require less time-sensitive operations than day trades, so for me personally they felt a bit redundant.

But maybe it helps some of you:

There are 4 conditions that trigger it. As with 5m Exit Alerts, the triggering reasons show up in the exit alert message (unfortunately only as a number, since alert messages can't have "dynamic text" in TradingView).

Here are the conditions sorted from best to worst:

Gap Up / Down. Better check SPY and the stock whether a Gap Reversal is likely to happen (aka get out) or whether the stock will keep going higher / lower.

Earnings: End of day or Tomorrow morning. Alert is triggered at beginning of morning before earnings, and then again 15m before market close.

Mental stop loss: Broke daily EMA 8 or SMA - in the wrong direction....

Wrong direction: Broke below / above yesterday's Low / High. It's not immediately triggered, but only after re-touching VWAP again, to prevent too impulsive exits.

As with 5m Exit alerts: Always consider how the market and stock looks like, then decide whether to exit or not! These are meant to make you look at the chart, not to FOMO-exit.

"X Candle Close":

Same as in 1D Enter alert: Is triggered 15m before market close (I put it in here as well because I kept forgetting whether I put this one into Enter or Exit alerts...)

More infos: www.reddit.com

1D Enter AlertsThis is only a remaining of an experiment. I had real swing enter alerts, but it just made more sense to use classic TradingView alerts for horizontal / trendline / SMA breaks.

(Btw you can set up a horizontal alert in TradingView just by hovering the mouse on the chart so it's at the price point you aim for, and pressing "Alt + A").

Once this horizontal alert triggered I would usually wait for confirmation of the move on the 5m. If it's f. e. a break of an SMA and I'm not convinced yet, I might wait until end of the day. For exactly that purpose the following alert comes in handy:

"X Candle Close":

Is triggered 15m before market close - good reminder to check a stock again to see whether a resistance / support break was valid - and the stock should be entered as a swing, or maybe whether it should be closed as a loss.

"Z Trend Change: UP" + "Z Trend Change: DOWN":

Same as on 5m Exit Alert: meant to be only applied on SPY, and to have it set up to never end!

Criteria:

SPY broke through daily EMA 8 or daily SMA today, indicating an important short-term change on the daily chart.

Is triggered 15m before market close

More infos: www.reddit.com

5m Exit AlertsThese can help a lot with Daytrading if you don't have a price target in mind when there's no clear resistance / support nearby, and you don't trust the market enough to hold it as a swing trade.

Keep in mind that its main purpose is to give you a "warning" that it might be good to look at your screen, instead of guaranteeing you "now is the best time to exit". You won't reach high winning stats by blindly following this alert.

"A Exit LONG":

(I'm using letters instead of numbers for all Exit alerts to make sure I don't accidentally confuse Enter and Exit alerts).

There are 4 conditions that might trigger it. The reasons show up in the exit alert message (unfortunately only as a number, since alert messages can't have "dynamic text" in TradingView), and can also be displayed as symbols in the chart (see image above - make sure to enable "Show Signals" in the indicator settings first though).

Here are the conditions sorted from best to worst:

Technical reversal: Bearish Hammer candle with Volume > 2 * avg volume (of last 30 candles), when 5m candle closed. Reversal very likely. This is usually the best time to take your gains for the rest of the day.

EMA 3/8 cross: standard 5m EMA 3/8 cross, indicating a trend reversal, or at least a pullback. Can also be helpful to detect double tops / double bottoms.

Trailing Stop Loss: Crossed below 30m EMA 8, 5m candle closed. This is a "fallback" alert in case EMA 3 was already below EMA 8 before you set up the alert. It's not unlikely that the stock might go further down to VWAP, so depending on the chart and market this might be a good opportunity to save the gains you have left.

"Final" Stop Loss: Crossed below VWAP. Usually not a good sign. If you entered around VWAP your losses shouldn't be big yet, but if you plan on holding the stock the Daily chart and market outlook should better be quite convincing, and you wouldn't have needed to use this alert in the first place.

Keep in mind these work of course best if you picked a "good" stock: clear movement, tidy price action, high volume. Otherwise alerts are more likely to be triggered redundantly.

Always consider how the market and stock looks like, then decide whether to exit or not! Usually it makes sense to wait a bit to see f. e. whether the stock bounces off the 30m EMA 8, and it's just a pullback.

"B Enter SHORT":

Similar, but for shorts...

"C 1m Scalp LONG" + "D 1m Scalp SHORT":

Simple Scalping alert for EMA 3/8 cross on a 1m chart - but without needing to use a 1m chart to set it up!

Unfortunately it's not as accurate as manually setting this alert up on a 1m chart. It might be an advantage though that it sometimes is triggered 1-2 min later, since this means there are less redundant triggerings.

It can be useful esp. on high momentum trades, but I honestly haven't used it in a looong while.

"X Candle Close":

same as in 5m Entry indicator: triggered when 5m candle is confirmed

"Z Trend Change: UP" + "Z Trend Change: DOWN":

This one is meant to be used only on SPY: It alerts you when SPY is changing its trending direction, which might mean entering or closing existing trades.

I have therefore set it up to never end (by setting it to "Once Per Bar Close" in the alert settings).

It's based on DMI positive or negative being > 25. I had it based on VWAP at the beginning, but there were days where it was triggered every 5 minutes...

More infos: www.reddit.com