Double Top/Bottom Screener - Today Only v2 //@version=6

indicator("Double Top/Bottom Screener - Today Only", overlay=true, max_lines_count=500)

// Inputs

leftBars = input.int(5, "Left Bars")

rightBars = input.int(5, "Right Bars")

tolerance = input.float(0.02, "Max Difference (e.g., 0.02 for 2 cents)", step=0.01)

atrLength = input.int(14, "ATR Length for Normalized Distance", minval=1)

requiredPeaks = input.int(3, "Required Identical Peaks", minval=2, maxval=5)

// Declarations of persistent variables and arrays

var array resistanceLevels = array.new(0)

var array resistanceCounts = array.new(0)

var array supportLevels = array.new(0)

var array supportCounts = array.new(0)

var array resLines = array.new(0)

var array supLines = array.new(0)

var bool hasDoubleTop = false

var bool hasDoubleBottom = false

var float doubleTopLevel = na

var float doubleBottomLevel = na

var int todayStart = na

// Step 1: Identify Swing Highs/Lows

swingHigh = ta.pivothigh(high, leftBars, rightBars)

swingLow = ta.pivotlow(low, leftBars, rightBars)

// Today's premarket start (04:00 AM ET)

todayStart := timestamp(syminfo.timezone, year, month, dayofmonth, 4, 0, 0)

// Clear arrays and delete lines on the first bar or new day

if barstate.isfirst or (dayofmonth != dayofmonth and time >= todayStart)

// Delete all existing lines only if arrays are not empty

if array.size(resLines) > 0

for i = array.size(resLines) - 1 to 0

line.delete(array.get(resLines, i))

if array.size(supLines) > 0

for i = array.size(supLines) - 1 to 0

line.delete(array.get(supLines, i))

// Clear arrays

array.clear(resistanceLevels)

array.clear(supportLevels)

array.clear(resistanceCounts)

array.clear(supportCounts)

array.clear(resLines)

array.clear(supLines)

// Reset flags

hasDoubleTop := false

hasDoubleBottom := false

doubleTopLevel := na

doubleBottomLevel := na

// Add new swings only if today and after premarket

if not na(swingHigh) and time >= todayStart and dayofmonth == dayofmonth

bool isEqualHigh = false

int peakIndex = -1

float prevLevel = na

if array.size(resistanceLevels) > 0

for i = 0 to array.size(resistanceLevels) - 1

prevLevel := array.get(resistanceLevels, i)

if math.abs(swingHigh - prevLevel) <= tolerance

isEqualHigh := true

peakIndex := i

break

if isEqualHigh and peakIndex >= 0

array.set(resistanceCounts, peakIndex, array.get(resistanceCounts, peakIndex) + 1)

if array.get(resistanceCounts, peakIndex) == requiredPeaks

hasDoubleTop := true

doubleTopLevel := prevLevel

else

array.push(resistanceLevels, swingHigh)

array.push(resistanceCounts, 1)

line newResLine = line.new(bar_index - rightBars, swingHigh, bar_index, swingHigh, color=color.red, width=2, extend=extend.none)

array.push(resLines, newResLine)

if not na(swingLow) and time >= todayStart and dayofmonth == dayofmonth

bool isEqualLow = false

int peakIndex = -1

float prevLevel = na

if array.size(supportLevels) > 0

for i = 0 to array.size(supportLevels) - 1

prevLevel := array.get(supportLevels, i)

if math.abs(swingLow - prevLevel) <= tolerance

isEqualLow := true

peakIndex := i

break

if isEqualLow and peakIndex >= 0

array.set(supportCounts, peakIndex, array.get(supportCounts, peakIndex) + 1)

if array.get(supportCounts, peakIndex) == requiredPeaks

hasDoubleBottom := true

doubleBottomLevel := prevLevel

else

array.push(supportLevels, swingLow)

array.push(supportCounts, 1)

line newSupLine = line.new(bar_index - rightBars, swingLow, bar_index, swingLow, color=color.green, width=2, extend=extend.none)

array.push(supLines, newSupLine)

// Monitor and remove broken levels/lines; reset pattern if the equal level breaks

if array.size(resistanceLevels) > 0

for i = array.size(resistanceLevels) - 1 to 0

float level = array.get(resistanceLevels, i)

if close > level

line.delete(array.get(resLines, i))

array.remove(resLines, i)

array.remove(resistanceLevels, i)

array.remove(resistanceCounts, i)

if level == doubleTopLevel

hasDoubleTop := false

doubleTopLevel := na

if array.size(supportLevels) > 0

for i = array.size(supportLevels) - 1 to 0

float level = array.get(supportLevels, i)

if close < level

line.delete(array.get(supLines, i))

array.remove(supLines, i)

array.remove(supportLevels, i)

array.remove(supportCounts, i)

if level == doubleBottomLevel

hasDoubleBottom := false

doubleBottomLevel := na

// Limit arrays (after removals)

if array.size(resistanceLevels) > 10

line oldLine = array.shift(resLines)

line.delete(oldLine)

array.shift(resistanceLevels)

array.shift(resistanceCounts)

if array.size(supportLevels) > 10

line oldLine = array.shift(supLines)

line.delete(oldLine)

array.shift(supportLevels)

array.shift(supportCounts)

// Pattern Signal: 1 only if the exact required number of peaks is met

patternSignal = (hasDoubleTop or hasDoubleBottom) ? 1 : 0

// New: Nearest Double Level Price

var float nearestDoubleLevel = na

if hasDoubleTop and not na(doubleTopLevel)

nearestDoubleLevel := doubleTopLevel

if hasDoubleBottom and not na(doubleBottomLevel)

nearestDoubleLevel := na(nearestDoubleLevel) ? doubleBottomLevel : (math.abs(close - doubleBottomLevel) < math.abs(close - nearestDoubleLevel) ? doubleBottomLevel : nearestDoubleLevel)

// New: Distance to Nearest Level (using ATR for normalization)

var float atr = ta.atr(atrLength)

var float distanceNormalizedATR = na

if not na(nearestDoubleLevel) and not na(atr) and atr > 0

distanceNormalizedATR := math.abs(close - nearestDoubleLevel) / atr

// Optional Bounce Signal (for reference)

bounceSignal = 0

if array.size(resistanceLevels) > 0

for i = 0 to array.size(resistanceLevels) - 1

float level = array.get(resistanceLevels, i)

if low <= level and high >= level and close < level

bounceSignal := 1

if array.size(supportLevels) > 0

for i = 0 to array.size(supportLevels) - 1

float level = array.get(supportLevels, i)

if high >= level and low <= level and close > level

bounceSignal := 1

// Outputs

plot(patternSignal, title="Pattern Signal", color=patternSignal == 1 ? color.purple : na, style=plot.style_circles)

plot(bounceSignal, title="Bounce Signal", color=bounceSignal == 1 ? color.yellow : na, style=plot.style_circles)

plot(nearestDoubleLevel, title="Nearest Double Level Price", color=color.orange)

plot(distanceNormalizedATR, title="Normalized Distance (ATR)", color=color.green)

bgcolor(patternSignal == 1 ? color.new(color.purple, 80) : na)

if patternSignal == 1 and barstate.isconfirmed

alert("Double Pattern detected on " + syminfo.ticker + " at " + str.tostring(close), alert.freq_once_per_bar_close)

if barstate.islast

var table infoTable = table.new(position.top_right, 1, 4, bgcolor=color.new(color.black, 50))

table.cell(infoTable, 0, 0, "Pattern: " + str.tostring(patternSignal), bgcolor=patternSignal == 1 ? color.purple : color.gray)

table.cell(infoTable, 0, 1, "Bounce: " + str.tostring(bounceSignal), bgcolor=bounceSignal == 1 ? color.yellow : color.gray)

table.cell(infoTable, 0, 2, "Level: " + str.tostring(nearestDoubleLevel, "#.##"), bgcolor=color.orange)

table.cell(infoTable, 0, 3, "ATR Dist: " + str.tostring(distanceNormalizedATR, "#.##"), bgcolor=color.green)

חפש סקריפטים עבור "10年期国债收益率+曲线图+数据来源"

Double Top/Bottom Screener - Today Only//@version=6

indicator("Double Top/Bottom Screener - Today Only", overlay=true, max_lines_count=500)

// Inputs

leftBars = input.int(5, "Left Bars")

rightBars = input.int(5, "Right Bars")

tolerance = input.float(0.02, "Max Difference (e.g., 0.02 for 2 cents)", step=0.01)

atrLength = input.int(14, "ATR Length for Normalized Distance", minval=1)

requiredPeaks = input.int(3, "Required Identical Peaks", minval=2, maxval=5)

// Declarations of persistent variables and arrays

var array resistanceLevels = array.new(0)

var array resistanceCounts = array.new(0)

var array supportLevels = array.new(0)

var array supportCounts = array.new(0)

var array resLines = array.new(0)

var array supLines = array.new(0)

var bool hasDoubleTop = false

var bool hasDoubleBottom = false

var float doubleTopLevel = na

var float doubleBottomLevel = na

var int todayStart = na

// Step 1: Identify Swing Highs/Lows

swingHigh = ta.pivothigh(high, leftBars, rightBars)

swingLow = ta.pivotlow(low, leftBars, rightBars)

// Today's premarket start (04:00 AM ET)

todayStart := timestamp(syminfo.timezone, year, month, dayofmonth, 4, 0, 0)

// Clear arrays and delete lines on the first bar or new day

if barstate.isfirst or (dayofmonth != dayofmonth and time >= todayStart)

// Delete all existing lines

for i = array.size(resLines) - 1 to 0

line.delete(array.get(resLines, i))

for i = array.size(supLines) - 1 to 0

line.delete(array.get(supLines, i))

// Clear arrays

array.clear(resistanceLevels)

array.clear(supportLevels)

array.clear(resistanceCounts)

array.clear(supportCounts)

array.clear(resLines)

array.clear(supLines)

// Reset flags

hasDoubleTop := false

hasDoubleBottom := false

doubleTopLevel := na

doubleBottomLevel := na

// Add new swings only if today and after premarket

if not na(swingHigh) and time >= todayStart and dayofmonth == dayofmonth

bool isEqualHigh = false

int peakIndex = -1

float prevLevel = na

if array.size(resistanceLevels) > 0

for i = 0 to array.size(resistanceLevels) - 1

prevLevel := array.get(resistanceLevels, i)

if math.abs(swingHigh - prevLevel) <= tolerance

isEqualHigh := true

peakIndex := i

break

if isEqualHigh and peakIndex >= 0

array.set(resistanceCounts, peakIndex, array.get(resistanceCounts, peakIndex) + 1)

if array.get(resistanceCounts, peakIndex) == requiredPeaks

hasDoubleTop := true

doubleTopLevel := prevLevel

else

array.push(resistanceLevels, swingHigh)

array.push(resistanceCounts, 1)

line newResLine = line.new(bar_index - rightBars, swingHigh, bar_index, swingHigh, color=color.red, width=2, extend=extend.none)

array.push(resLines, newResLine)

if not na(swingLow) and time >= todayStart and dayofmonth == dayofmonth

bool isEqualLow = false

int peakIndex = -1

float prevLevel = na

if array.size(supportLevels) > 0

for i = 0 to array.size(supportLevels) - 1

prevLevel := array.get(supportLevels, i)

if math.abs(swingLow - prevLevel) <= tolerance

isEqualLow := true

peakIndex := i

break

if isEqualLow and peakIndex >= 0

array.set(supportCounts, peakIndex, array.get(supportCounts, peakIndex) + 1)

if array.get(supportCounts, peakIndex) == requiredPeaks

hasDoubleBottom := true

doubleBottomLevel := prevLevel

else

array.push(supportLevels, swingLow)

array.push(supportCounts, 1)

line newSupLine = line.new(bar_index - rightBars, swingLow, bar_index, swingLow, color=color.green, width=2, extend=extend.none)

array.push(supLines, newSupLine)

// Monitor and remove broken levels/lines; reset pattern if the equal level breaks

if array.size(resistanceLevels) > 0

for i = array.size(resistanceLevels) - 1 to 0

float level = array.get(resistanceLevels, i)

if close > level

line.delete(array.get(resLines, i))

array.remove(resLines, i)

array.remove(resistanceLevels, i)

array.remove(resistanceCounts, i)

if level == doubleTopLevel

hasDoubleTop := false

doubleTopLevel := na

if array.size(supportLevels) > 0

for i = array.size(supportLevels) - 1 to 0

float level = array.get(supportLevels, i)

if close < level

line.delete(array.get(supLines, i))

array.remove(supLines, i)

array.remove(supportLevels, i)

array.remove(supportCounts, i)

if level == doubleBottomLevel

hasDoubleBottom := false

doubleBottomLevel := na

// Limit arrays (after removals)

if array.size(resistanceLevels) > 10

line oldLine = array.shift(resLines)

line.delete(oldLine)

array.shift(resistanceLevels)

array.shift(resistanceCounts)

if array.size(supportLevels) > 10

line oldLine = array.shift(supLines)

line.delete(oldLine)

array.shift(supportLevels)

array.shift(supportCounts)

// Pattern Signal: 1 only if the exact required number of peaks is met

patternSignal = (hasDoubleTop or hasDoubleBottom) ? 1 : 0

// New: Nearest Double Level Price

var float nearestDoubleLevel = na

if hasDoubleTop and not na(doubleTopLevel)

nearestDoubleLevel := doubleTopLevel

if hasDoubleBottom and not na(doubleBottomLevel)

nearestDoubleLevel := na(nearestDoubleLevel) ? doubleBottomLevel : (math.abs(close - doubleBottomLevel) < math.abs(close - nearestDoubleLevel) ? doubleBottomLevel : nearestDoubleLevel)

// New: Distance to Nearest Level (using ATR for normalization)

var float atr = ta.atr(atrLength)

var float distanceNormalizedATR = na

if not na(nearestDoubleLevel) and not na(atr) and atr > 0

distanceNormalizedATR := math.abs(close - nearestDoubleLevel) / atr

// Optional Bounce Signal (for reference)

bounceSignal = 0

if array.size(resistanceLevels) > 0

for i = 0 to array.size(resistanceLevels) - 1

float level = array.get(resistanceLevels, i)

if low <= level and high >= level and close < level

bounceSignal := 1

if array.size(supportLevels) > 0

for i = 0 to array.size(supportLevels) - 1

float level = array.get(supportLevels, i)

if high >= level and low <= level and close > level

bounceSignal := 1

// Outputs

plot(patternSignal, title="Pattern Signal", color=patternSignal == 1 ? color.purple : na, style=plot.style_circles)

plot(bounceSignal, title="Bounce Signal", color=bounceSignal == 1 ? color.yellow : na, style=plot.style_circles)

plot(nearestDoubleLevel, title="Nearest Double Level Price", color=color.orange)

plot(distanceNormalizedATR, title="Normalized Distance (ATR)", color=color.green)

bgcolor(patternSignal == 1 ? color.new(color.purple, 80) : na)

if patternSignal == 1 and barstate.isconfirmed

alert("Double Pattern detected on " + syminfo.ticker + " at " + str.tostring(close), alert.freq_once_per_bar_close)

if barstate.islast

var table infoTable = table.new(position.top_right, 1, 4, bgcolor=color.new(color.black, 50))

table.cell(infoTable, 0, 0, "Pattern: " + str.tostring(patternSignal), bgcolor=patternSignal == 1 ? color.purple : color.gray)

table.cell(infoTable, 0, 1, "Bounce: " + str.tostring(bounceSignal), bgcolor=bounceSignal == 1 ? color.yellow : color.gray)

table.cell(infoTable, 0, 2, "Level: " + str.tostring(nearestDoubleLevel, "#.##"), bgcolor=color.orange)

table.cell(infoTable, 0, 3, "ATR Dist: " + str.tostring(distanceNormalizedATR, "#.##"), bgcolor=color.green)

Double Top/Bottom Screener V1//@version=6

indicator("Double Top/Bottom Screener", overlay=true, max_lines_count=500)

// Inputs

leftBars = input.int(5, "Left Bars")

rightBars = input.int(5, "Right Bars")

tolerance = input.float(0.02, "Max Difference (e.g., 0.02 for 2 cents)", step=0.01)

atrLength = input.int(14, "ATR Length for Normalized Distance", minval=1)

requiredPeaks = input.int(3, "Required Identical Peaks", minval=2, maxval=5)

// Declarations of persistent variables and arrays

var array resistanceLevels = array.new(0)

var array resistanceCounts = array.new(0)

var array supportLevels = array.new(0)

var array supportCounts = array.new(0)

var array resLines = array.new(0)

var array supLines = array.new(0)

var bool hasDoubleTop = false

var bool hasDoubleBottom = false

var float doubleTopLevel = na

var float doubleBottomLevel = na

var int todayStart = na

var bool isNewDay = false

// Step 1: Identify Swing Highs/Lows

swingHigh = ta.pivothigh(high, leftBars, rightBars)

swingLow = ta.pivotlow(low, leftBars, rightBars)

// Today's premarket start (04:00 AM ET)

if dayofmonth != dayofmonth

todayStart := timestamp(syminfo.timezone, year, month, dayofmonth, 4, 0, 0)

isNewDay := true

else

isNewDay := false

// Clear arrays and reset flags only once at premarket start

if isNewDay and time >= todayStart

array.clear(resistanceLevels)

array.clear(supportLevels)

array.clear(resistanceCounts)

array.clear(supportCounts)

array.clear(resLines)

array.clear(supLines)

hasDoubleTop := false

hasDoubleBottom := false

doubleTopLevel := na

doubleBottomLevel := na

// Add new swings and check for identical peaks

if not na(swingHigh) and time >= todayStart

bool isEqualHigh = false

int peakIndex = -1

float prevLevel = na

if array.size(resistanceLevels) > 0

for i = 0 to array.size(resistanceLevels) - 1

prevLevel := array.get(resistanceLevels, i)

if math.abs(swingHigh - prevLevel) <= tolerance

isEqualHigh := true

peakIndex := i

break

if isEqualHigh and peakIndex >= 0

array.set(resistanceCounts, peakIndex, array.get(resistanceCounts, peakIndex) + 1)

if array.get(resistanceCounts, peakIndex) == requiredPeaks

hasDoubleTop := true

doubleTopLevel := prevLevel

else

array.push(resistanceLevels, swingHigh)

array.push(resistanceCounts, 1)

line newResLine = line.new(bar_index - rightBars, swingHigh, bar_index, swingHigh, color=color.red, width=2, extend=extend.right)

array.push(resLines, newResLine)

if not na(swingLow) and time >= todayStart

bool isEqualLow = false

int peakIndex = -1

float prevLevel = na

if array.size(supportLevels) > 0

for i = 0 to array.size(supportLevels) - 1

prevLevel := array.get(supportLevels, i)

if math.abs(swingLow - prevLevel) <= tolerance

isEqualLow := true

peakIndex := i

break

if isEqualLow and peakIndex >= 0

array.set(supportCounts, peakIndex, array.get(supportCounts, peakIndex) + 1)

if array.get(supportCounts, peakIndex) == requiredPeaks

hasDoubleBottom := true

doubleBottomLevel := prevLevel

else

array.push(supportLevels, swingLow)

array.push(supportCounts, 1)

line newSupLine = line.new(bar_index - rightBars, swingLow, bar_index, swingLow, color=color.green, width=2, extend=extend.right)

array.push(supLines, newSupLine)

// Monitor and remove broken levels/lines; reset pattern if the equal level breaks

if array.size(resistanceLevels) > 0

for i = array.size(resistanceLevels) - 1 to 0

float level = array.get(resistanceLevels, i)

if close > level

line.delete(array.get(resLines, i))

array.remove(resLines, i)

array.remove(resistanceLevels, i)

array.remove(resistanceCounts, i)

if level == doubleTopLevel

hasDoubleTop := false

doubleTopLevel := na

if array.size(supportLevels) > 0

for i = array.size(supportLevels) - 1 to 0

float level = array.get(supportLevels, i)

if close < level

line.delete(array.get(supLines, i))

array.remove(supLines, i)

array.remove(supportLevels, i)

array.remove(supportCounts, i)

if level == doubleBottomLevel

hasDoubleBottom := false

doubleBottomLevel := na

// Limit arrays (after removals)

if array.size(resistanceLevels) > 10

line oldLine = array.shift(resLines)

line.delete(oldLine)

array.shift(resistanceLevels)

array.shift(resistanceCounts)

if array.size(supportLevels) > 10

line oldLine = array.shift(supLines)

line.delete(oldLine)

array.shift(supportLevels)

array.shift(supportCounts)

// Pattern Signal: 1 only if the exact required number of peaks is met

patternSignal = (hasDoubleTop or hasDoubleBottom) and (array.size(resistanceCounts) > 0 and array.get(resistanceCounts, array.size(resistanceCounts) - 1) == requiredPeaks or array.size(supportCounts) > 0 and array.get(supportCounts, array.size(supportCounts) - 1) == requiredPeaks) ? 1 : 0

// New: Nearest Double Level Price

var float nearestDoubleLevel = na

if hasDoubleTop and not na(doubleTopLevel)

nearestDoubleLevel := doubleTopLevel

if hasDoubleBottom and not na(doubleBottomLevel)

nearestDoubleLevel := na(nearestDoubleLevel) ? doubleBottomLevel : (math.abs(close - doubleBottomLevel) < math.abs(close - nearestDoubleLevel) ? doubleBottomLevel : nearestDoubleLevel)

// New: Distance to Nearest Level (using ATR for normalization)

var float atr = ta.atr(atrLength)

var float distanceNormalizedATR = na

if not na(nearestDoubleLevel) and not na(atr) and atr > 0

distanceNormalizedATR := math.abs(close - nearestDoubleLevel) / atr

// Optional Bounce Signal (for reference)

bounceSignal = 0

if array.size(resistanceLevels) > 0

for i = 0 to array.size(resistanceLevels) - 1

float level = array.get(resistanceLevels, i)

if low <= level and high >= level and close < level

bounceSignal := 1

if array.size(supportLevels) > 0

for i = 0 to array.size(supportLevels) - 1

float level = array.get(supportLevels, i)

if high >= level and low <= level and close > level

bounceSignal := 1

// Outputs

plot(patternSignal, title="Pattern Signal", color=patternSignal == 1 ? color.purple : na, style=plot.style_circles)

plot(bounceSignal, title="Bounce Signal", color=bounceSignal == 1 ? color.yellow : na, style=plot.style_circles)

plot(nearestDoubleLevel, title="Nearest Double Level Price", color=color.orange)

plot(distanceNormalizedATR, title="Normalized Distance (ATR)", color=color.green)

bgcolor(patternSignal == 1 ? color.new(color.purple, 80) : na)

if patternSignal == 1 and barstate.isconfirmed

alert("Double Pattern detected on " + syminfo.ticker + " at " + str.tostring(close), alert.freq_once_per_bar_close)

if barstate.islast

var table infoTable = table.new(position.top_right, 1, 4, bgcolor=color.new(color.black, 50))

table.cell(infoTable, 0, 0, "Pattern: " + str.tostring(patternSignal), bgcolor=patternSignal == 1 ? color.purple : color.gray)

table.cell(infoTable, 0, 1, "Bounce: " + str.tostring(bounceSignal), bgcolor=bounceSignal == 1 ? color.yellow : color.gray)

table.cell(infoTable, 0, 2, "Level: " + str.tostring(nearestDoubleLevel, "#.##"), bgcolor=color.orange)

table.cell(infoTable, 0, 3, "ATR Dist: " + str.tostring(distanceNormalizedATR, "#.##"), bgcolor=color.green)

Double Top/Bottom Screener 3-5 peaks //@version=6

indicator("Double Top/Bottom Screener", overlay=true, max_lines_count=500)

// Inputs

leftBars = input.int(5, "Left Bars")

rightBars = input.int(5, "Right Bars")

tolerance = input.float(0.02, "Max Difference (e.g., 0.02 for 2 cents)", step=0.01)

atrLength = input.int(14, "ATR Length for Normalized Distance", minval=1)

maxPeaks = input.int(5, "Max Identical Peaks", minval=2, maxval=5)

// Declarations of persistent variables and arrays

var array resistanceLevels = array.new(0)

var array resistanceCounts = array.new(0)

var array supportLevels = array.new(0)

var array supportCounts = array.new(0)

var array resLines = array.new(0)

var array supLines = array.new(0)

var bool hasDoubleTop = false

var bool hasDoubleBottom = false

var float doubleTopLevel = na

var float doubleBottomLevel = na

var int todayStart = na

var bool isNewDay = false

// Step 1: Identify Swing Highs/Lows

swingHigh = ta.pivothigh(high, leftBars, rightBars)

swingLow = ta.pivotlow(low, leftBars, rightBars)

// Today's premarket start (04:00 AM ET)

if dayofmonth != dayofmonth

todayStart := timestamp(syminfo.timezone, year, month, dayofmonth, 4, 0, 0)

isNewDay := true

else

isNewDay := false

// Clear arrays and reset flags only once at premarket start

if isNewDay and time >= todayStart

array.clear(resistanceLevels)

array.clear(supportLevels)

array.clear(resistanceCounts)

array.clear(supportCounts)

array.clear(resLines)

array.clear(supLines)

hasDoubleTop := false

hasDoubleBottom := false

doubleTopLevel := na

doubleBottomLevel := na

// Add new swings and check for identical peaks

if not na(swingHigh) and time >= todayStart

bool isEqualHigh = false

int peakIndex = -1

float prevLevel = na // Declare prevLevel with initial value

if array.size(resistanceLevels) > 0

for i = 0 to array.size(resistanceLevels) - 1

prevLevel := array.get(resistanceLevels, i)

if math.abs(swingHigh - prevLevel) <= tolerance

isEqualHigh := true

peakIndex := i

break

if isEqualHigh and peakIndex >= 0

array.set(resistanceCounts, peakIndex, array.get(resistanceCounts, peakIndex) + 1)

if array.get(resistanceCounts, peakIndex) >= maxPeaks

hasDoubleTop := true

doubleTopLevel := prevLevel

else

array.push(resistanceLevels, swingHigh)

array.push(resistanceCounts, 1)

line newResLine = line.new(bar_index - rightBars, swingHigh, bar_index, swingHigh, color=color.red, width=2, extend=extend.right)

array.push(resLines, newResLine)

if not na(swingLow) and time >= todayStart

bool isEqualLow = false

int peakIndex = -1

float prevLevel = na // Declare prevLevel with initial value

if array.size(supportLevels) > 0

for i = 0 to array.size(supportLevels) - 1

prevLevel := array.get(supportLevels, i)

if math.abs(swingLow - prevLevel) <= tolerance

isEqualLow := true

peakIndex := i

break

if isEqualLow and peakIndex >= 0

array.set(supportCounts, peakIndex, array.get(supportCounts, peakIndex) + 1)

if array.get(supportCounts, peakIndex) >= maxPeaks

hasDoubleBottom := true

doubleBottomLevel := prevLevel

else

array.push(supportLevels, swingLow)

array.push(supportCounts, 1)

line newSupLine = line.new(bar_index - rightBars, swingLow, bar_index, swingLow, color=color.green, width=2, extend=extend.right)

array.push(supLines, newSupLine)

// Monitor and remove broken levels/lines; reset pattern if the equal level breaks

if array.size(resistanceLevels) > 0

for i = array.size(resistanceLevels) - 1 to 0

float level = array.get(resistanceLevels, i)

if close > level

line.delete(array.get(resLines, i))

array.remove(resLines, i)

array.remove(resistanceLevels, i)

array.remove(resistanceCounts, i)

if level == doubleTopLevel

hasDoubleTop := false

doubleTopLevel := na

if array.size(supportLevels) > 0

for i = array.size(supportLevels) - 1 to 0

float level = array.get(supportLevels, i)

if close < level

line.delete(array.get(supLines, i))

array.remove(supLines, i)

array.remove(supportLevels, i)

array.remove(supportCounts, i)

if level == doubleBottomLevel

hasDoubleBottom := false

doubleBottomLevel := na

// Limit arrays (after removals)

if array.size(resistanceLevels) > 10

line oldLine = array.shift(resLines)

line.delete(oldLine)

array.shift(resistanceLevels)

array.shift(resistanceCounts)

if array.size(supportLevels) > 10

line oldLine = array.shift(supLines)

line.delete(oldLine)

array.shift(supportLevels)

array.shift(supportCounts)

// Pattern Signal: 1 if any pattern with maxPeaks is active and unbroken

patternSignal = (hasDoubleTop or hasDoubleBottom) ? 1 : 0

// New: Nearest Double Level Price

var float nearestDoubleLevel = na

if hasDoubleTop and not na(doubleTopLevel)

nearestDoubleLevel := doubleTopLevel

if hasDoubleBottom and not na(doubleBottomLevel)

nearestDoubleLevel := na(nearestDoubleLevel) ? doubleBottomLevel : (math.abs(close - doubleBottomLevel) < math.abs(close - nearestDoubleLevel) ? doubleBottomLevel : nearestDoubleLevel)

// New: Distance to Nearest Level (using ATR for normalization)

var float atr = ta.atr(atrLength)

var float distanceNormalizedATR = na

if not na(nearestDoubleLevel) and not na(atr) and atr > 0

distanceNormalizedATR := math.abs(close - nearestDoubleLevel) / atr

// Optional Bounce Signal (for reference)

bounceSignal = 0

if array.size(resistanceLevels) > 0

for i = 0 to array.size(resistanceLevels) - 1

float level = array.get(resistanceLevels, i)

if low <= level and high >= level and close < level

bounceSignal := 1

if array.size(supportLevels) > 0

for i = 0 to array.size(supportLevels) - 1

float level = array.get(supportLevels, i)

if high >= level and low <= level and close > level

bounceSignal := 1

// Outputs

plot(patternSignal, title="Pattern Signal", color=patternSignal == 1 ? color.purple : na, style=plot.style_circles)

plot(bounceSignal, title="Bounce Signal", color=bounceSignal == 1 ? color.yellow : na, style=plot.style_circles)

plot(nearestDoubleLevel, title="Nearest Double Level Price", color=color.orange)

plot(distanceNormalizedATR, title="Normalized Distance (ATR)", color=color.green)

bgcolor(patternSignal == 1 ? color.new(color.purple, 80) : na)

if patternSignal == 1 and barstate.isconfirmed

alert("Double Pattern detected on " + syminfo.ticker + " at " + str.tostring(close), alert.freq_once_per_bar_close)

if barstate.islast

var table infoTable = table.new(position.top_right, 1, 4, bgcolor=color.new(color.black, 50))

table.cell(infoTable, 0, 0, "Pattern: " + str.tostring(patternSignal), bgcolor=patternSignal == 1 ? color.purple : color.gray)

table.cell(infoTable, 0, 1, "Bounce: " + str.tostring(bounceSignal), bgcolor=bounceSignal == 1 ? color.yellow : color.gray)

table.cell(infoTable, 0, 2, "Level: " + str.tostring(nearestDoubleLevel, "#.##"), bgcolor=color.orange)

table.cell(infoTable, 0, 3, "ATR Dist: " + str.tostring(distanceNormalizedATR, "#.##"), bgcolor=color.green)

MA Pack + Cross Signals (Short vs Long)Overview

A flexible moving average pack that lets you switch between short-term trend detection and long-term trend confirmation .

Short-term mode: plots 5, 10, 20, and 50 MAs with early crossovers (10/50, 20/50).

Long-term mode: plots 50, 100, 200 MAs with Golden Cross and Death Cross signals.

Choice of SMA or EMA .

Alerts included for all crossovers.

Why Use It

Catch early trend shifts in short-term mode.

Confirm institutional trend levels in long-term mode.

Visual signals (triangles + labels) make spotting setups easy.

Alert-ready for automated trade monitoring.

Usage

Add to chart.

In settings, choose Short-term or Long-term .

Watch for markers:

Green triangles = bullish cross

Red triangles = bearish cross

Green label = Golden Cross

Red label = Death Cross

Optional: enable alerts for notifications.

Market Pressure Oscillator█ OVERVIEW

The Market Pressure Oscillator is an advanced technical indicator for TradingView, enabling traders to identify potential trend reversals and momentum shifts through candle-based pressure analysis and divergence detection. It combines a smoothed oscillator with moving average signals, overbought/oversold levels, and divergence visualization, enhanced by customizable gradients, dynamic band colors, and alerts for quick decision-making.

█ CONCEPT

The indicator measures buying or selling pressure based on candle body size (open-to-close difference) and direction, with optional smoothing for clarity and divergence detection between price action and the oscillator. It relies solely on candle data, offering insights into trend strength, overbought/oversold conditions, and potential reversals with a customizable visual presentation.

█ WHY USE IT?

- Divergence Detection: Identifies bullish and bearish divergences to reinforce signals, especially near overbought/oversold zones.

- Candle Pressure Analysis: Measures pressure based on candle body size, normalized to a ±100 scale.

- Signal Generation: Provides buy/sell signals via overbought/oversold crossovers, zero-line crossovers, moving average zero-line crossovers, and dynamic band color changes.

- Visual Clarity: Uses dynamic colors, gradients, and fill layers for intuitive chart analysis.

Flexibility: Extensive settings allow customization to individual trading preferences.

█ HOW IT WORKS?

- Candle Pressure Calculation: Computes candle body size as math.abs(close - open), normalized against the average body size over a lookback period (avgBody = ta.sma(body, len)). - Candle direction (bullish: +1, bearish: -1, neutral: 0) is multiplied by body weight to derive pressure.

- Cumulative Pressure: Sums pressure values over the lookback period (Lookback Length) and normalizes to ±100 relative to the maximum possible value.

- Smoothing: Optionally applies EMA (Smoothing Length) to normalized pressure.

- Moving Average: Calculates SMA (Moving Average Length) for trend confirmation (Moving Average (SMA)).

- Divergence Detection: Identifies bullish/bearish divergences by comparing price and oscillator pivot highs/lows within a specified range (Pivot Length). Divergence signals appear with a delay equal to the Pivot Length.

- Signals: Generates signals for:

Crossing oversold upward (buy) or overbought downward (sell).

Crossing the zero line by the oscillator or moving average (buy/sell).

Bullish/bearish divergences, marked with labels, enhancing signals, especially near overbought/oversold zones.

Dynamic band color changes when the moving average crosses MA overbought/oversold thresholds (green for oversold, red for overbought).

- Visualization: Plots the oscillator and moving average with dynamic colors, gradient fills, transparent bands, and labels, with customizable overbought/oversold levels.

Alerts: Built-in alerts for divergences, overbought/oversold crossovers, and zero-line crossovers (oscillator and moving average).

█ SETTINGS AND CUSTOMIZATION

- Lookback Length: Period for aggregating candle pressure (default: 14).

- Smoothing Length (EMA): EMA length for smoothing the oscillator (default: 1). Higher values smooth the signal but may reduce signal frequency; adjust overbought/oversold levels accordingly.

- Moving Average Length (SMA): SMA length for the moving average (default: 14, minval=1). Higher values make SMA a trend indicator, requiring adjusted MA overbought/oversold levels.

- Pivot Length (Left/Right): Candles for detecting pivot highs/lows in divergence calculations (default: 2, minval=1). Higher values reduce noise but add delay equal to the set value.

- Enable Divergence Detection: Enables divergence detection (default: true).

- Overbought/Oversold Levels: Thresholds for the oscillator (default: 30/-30) and moving average (default: 10/-10). For the moving average, no arrows appear; bands change color from gray to green (oversold) or red (overbought), reinforcing entry signals.

- Signal Type: Select signals to display: "None", "Overbought/Oversold", "Zero Line", "MA Zero Line", "All" (default: "Overbought/Oversold").

- Colors and Gradients: Customize colors for bullish/bearish oscillator, moving average, zero line, overbought/oversold levels, and divergence labels.

- Transparency: Adjust gradient fill transparency (default: 70, minval=0, maxval=100) and band/label transparency (default: 40, minval=0, maxval=100) for consistent visuals.

- Visualizations: Enable/disable moving average, gradients for zero/overbought/oversold levels, and gradient fills.

█ USAGE EXAMPLES

- Momentum Analysis: Observe the MPO Oscillator above 0 for bullish momentum or below 0 for bearish momentum. The SMA, being smoother, reacts slower and can confirm trend direction as a noise filter.

- Reversal Signals: Look for buy triangles when the oscillator crosses oversold upward, especially when the SMA is below the MA oversold threshold and the band turns green. Similarly, seek sell triangles when crossing overbought downward, with the SMA above the MA overbought threshold and the band turning red.

- Using Divergences: Treat bullish (green labels) and bearish (red labels) divergences as reinforcement for other signals, especially near overbought/oversold zones, indicating stronger potential trend reversals.

- Customization: Adjust lookback length, smoothing, and moving average length to specific instruments and timeframes to minimize false signals.

█ USER NOTES

Combine the indicator with tools like Fibonacci levels or pivot points to enhance accuracy.

Test different settings for lookback length, smoothing, and moving average length on your chosen instrument and timeframe to find optimal values.

TA█ TA Library

📊 OVERVIEW

TA is a Pine Script technical analysis library. This library provides 25+ moving averages and smoothing filters , from classic SMA/EMA to Kalman Filters and adaptive algorithms, implemented based on academic research.

🎯 Core Features

Academic Based - Algorithms follow original papers and formulas

Performance Optimized - Pre-calculated constants for faster response

Unified Interface - Consistent function design

Research Based - Integrates technical analysis research

🎯 CONCEPTS

Library Design Philosophy

This technical analysis library focuses on providing:

Academic Foundation

Algorithms based on published research papers and academic standards

Implementations that follow original mathematical formulations

Clear documentation with research references

Developer Experience

Unified interface design for consistent usage patterns

Pre-calculated constants for optimal performance

Comprehensive function collection to reduce development time

Single import statement for immediate access to all functions

Each indicator encapsulated as a simple function call - one line of code simplifies complexity

Technical Excellence

25+ carefully implemented moving averages and filters

Support for advanced algorithms like Kalman Filter and MAMA/FAMA

Optimized code structure for maintainability and reliability

Regular updates incorporating latest research developments

🚀 USING THIS LIBRARY

Import Library

//@version=6

import DCAUT/TA/1 as dta

indicator("Advanced Technical Analysis", overlay=true)

Basic Usage Example

// Classic moving average combination

ema20 = ta.ema(close, 20)

kama20 = dta.kama(close, 20)

plot(ema20, "EMA20", color.red, 2)

plot(kama20, "KAMA20", color.green, 2)

Advanced Trading System

// Adaptive moving average system

kama = dta.kama(close, 20, 2, 30)

= dta.mamaFama(close, 0.5, 0.05)

// Trend confirmation and entry signals

bullTrend = kama > kama and mamaValue > famaValue

bearTrend = kama < kama and mamaValue < famaValue

longSignal = ta.crossover(close, kama) and bullTrend

shortSignal = ta.crossunder(close, kama) and bearTrend

plot(kama, "KAMA", color.blue, 3)

plot(mamaValue, "MAMA", color.orange, 2)

plot(famaValue, "FAMA", color.purple, 2)

plotshape(longSignal, "Buy", shape.triangleup, location.belowbar, color.green)

plotshape(shortSignal, "Sell", shape.triangledown, location.abovebar, color.red)

📋 FUNCTIONS REFERENCE

ewma(source, alpha)

Calculates the Exponentially Weighted Moving Average with dynamic alpha parameter.

Parameters:

source (series float) : Series of values to process.

alpha (series float) : The smoothing parameter of the filter.

Returns: (float) The exponentially weighted moving average value.

dema(source, length)

Calculates the Double Exponential Moving Average (DEMA) of a given data series.

Parameters:

source (series float) : Series of values to process.

length (simple int) : Number of bars for the moving average calculation.

Returns: (float) The calculated Double Exponential Moving Average value.

tema(source, length)

Calculates the Triple Exponential Moving Average (TEMA) of a given data series.

Parameters:

source (series float) : Series of values to process.

length (simple int) : Number of bars for the moving average calculation.

Returns: (float) The calculated Triple Exponential Moving Average value.

zlema(source, length)

Calculates the Zero-Lag Exponential Moving Average (ZLEMA) of a given data series. This indicator attempts to eliminate the lag inherent in all moving averages.

Parameters:

source (series float) : Series of values to process.

length (simple int) : Number of bars for the moving average calculation.

Returns: (float) The calculated Zero-Lag Exponential Moving Average value.

tma(source, length)

Calculates the Triangular Moving Average (TMA) of a given data series. TMA is a double-smoothed simple moving average that reduces noise.

Parameters:

source (series float) : Series of values to process.

length (simple int) : Number of bars for the moving average calculation.

Returns: (float) The calculated Triangular Moving Average value.

frama(source, length)

Calculates the Fractal Adaptive Moving Average (FRAMA) of a given data series. FRAMA adapts its smoothing factor based on fractal geometry to reduce lag. Developed by John Ehlers.

Parameters:

source (series float) : Series of values to process.

length (simple int) : Number of bars for the moving average calculation.

Returns: (float) The calculated Fractal Adaptive Moving Average value.

kama(source, length, fastLength, slowLength)

Calculates Kaufman's Adaptive Moving Average (KAMA) of a given data series. KAMA adjusts its smoothing based on market efficiency ratio. Developed by Perry J. Kaufman.

Parameters:

source (series float) : Series of values to process.

length (simple int) : Number of bars for the efficiency calculation.

fastLength (simple int) : Fast EMA length for smoothing calculation. Optional. Default is 2.

slowLength (simple int) : Slow EMA length for smoothing calculation. Optional. Default is 30.

Returns: (float) The calculated Kaufman's Adaptive Moving Average value.

t3(source, length, volumeFactor)

Calculates the Tilson Moving Average (T3) of a given data series. T3 is a triple-smoothed exponential moving average with improved lag characteristics. Developed by Tim Tillson.

Parameters:

source (series float) : Series of values to process.

length (simple int) : Number of bars for the moving average calculation.

volumeFactor (simple float) : Volume factor affecting responsiveness. Optional. Default is 0.7.

Returns: (float) The calculated Tilson Moving Average value.

ultimateSmoother(source, length)

Calculates the Ultimate Smoother of a given data series. Uses advanced filtering techniques to reduce noise while maintaining responsiveness. Based on digital signal processing principles by John Ehlers.

Parameters:

source (series float) : Series of values to process.

length (simple int) : Number of bars for the smoothing calculation.

Returns: (float) The calculated Ultimate Smoother value.

kalmanFilter(source, processNoise, measurementNoise)

Calculates the Kalman Filter of a given data series. Optimal estimation algorithm that estimates true value from noisy observations. Based on the Kalman Filter algorithm developed by Rudolf Kalman (1960).

Parameters:

source (series float) : Series of values to process.

processNoise (simple float) : Process noise variance (Q). Controls adaptation speed. Optional. Default is 0.05.

measurementNoise (simple float) : Measurement noise variance (R). Controls smoothing. Optional. Default is 1.0.

Returns: (float) The calculated Kalman Filter value.

mcginleyDynamic(source, length)

Calculates the McGinley Dynamic of a given data series. McGinley Dynamic is an adaptive moving average that adjusts to market speed changes. Developed by John R. McGinley Jr.

Parameters:

source (series float) : Series of values to process.

length (simple int) : Number of bars for the dynamic calculation.

Returns: (float) The calculated McGinley Dynamic value.

mama(source, fastLimit, slowLimit)

Calculates the Mesa Adaptive Moving Average (MAMA) of a given data series. MAMA uses Hilbert Transform Discriminator to adapt to market cycles dynamically. Developed by John F. Ehlers.

Parameters:

source (series float) : Series of values to process.

fastLimit (simple float) : Maximum alpha (responsiveness). Optional. Default is 0.5.

slowLimit (simple float) : Minimum alpha (smoothing). Optional. Default is 0.05.

Returns: (float) The calculated Mesa Adaptive Moving Average value.

fama(source, fastLimit, slowLimit)

Calculates the Following Adaptive Moving Average (FAMA) of a given data series. FAMA follows MAMA with reduced responsiveness for crossover signals. Developed by John F. Ehlers.

Parameters:

source (series float) : Series of values to process.

fastLimit (simple float) : Maximum alpha (responsiveness). Optional. Default is 0.5.

slowLimit (simple float) : Minimum alpha (smoothing). Optional. Default is 0.05.

Returns: (float) The calculated Following Adaptive Moving Average value.

mamaFama(source, fastLimit, slowLimit)

Calculates Mesa Adaptive Moving Average (MAMA) and Following Adaptive Moving Average (FAMA).

Parameters:

source (series float) : Series of values to process.

fastLimit (simple float) : Maximum alpha (responsiveness). Optional. Default is 0.5.

slowLimit (simple float) : Minimum alpha (smoothing). Optional. Default is 0.05.

Returns: ( ) Tuple containing values.

laguerreFilter(source, length, gamma, order)

Calculates the standard N-order Laguerre Filter of a given data series. Standard Laguerre Filter uses uniform weighting across all polynomial terms. Developed by John F. Ehlers.

Parameters:

source (series float) : Series of values to process.

length (simple int) : Length for UltimateSmoother preprocessing.

gamma (simple float) : Feedback coefficient (0-1). Lower values reduce lag. Optional. Default is 0.8.

order (simple int) : The order of the Laguerre filter (1-10). Higher order increases lag. Optional. Default is 8.

Returns: (float) The calculated standard Laguerre Filter value.

laguerreBinomialFilter(source, length, gamma)

Calculates the Laguerre Binomial Filter of a given data series. Uses 6-pole feedback with binomial weighting coefficients. Developed by John F. Ehlers.

Parameters:

source (series float) : Series of values to process.

length (simple int) : Length for UltimateSmoother preprocessing.

gamma (simple float) : Feedback coefficient (0-1). Lower values reduce lag. Optional. Default is 0.5.

Returns: (float) The calculated Laguerre Binomial Filter value.

superSmoother(source, length)

Calculates the Super Smoother of a given data series. SuperSmoother is a second-order Butterworth filter from aerospace technology. Developed by John F. Ehlers.

Parameters:

source (series float) : Series of values to process.

length (simple int) : Period for the filter calculation.

Returns: (float) The calculated Super Smoother value.

rangeFilter(source, length, multiplier)

Calculates the Range Filter of a given data series. Range Filter reduces noise by filtering price movements within a dynamic range.

Parameters:

source (series float) : Series of values to process.

length (simple int) : Number of bars for the average range calculation.

multiplier (simple float) : Multiplier for the smooth range. Higher values increase filtering. Optional. Default is 2.618.

Returns: ( ) Tuple containing filtered value, trend direction, upper band, and lower band.

qqe(source, rsiLength, rsiSmooth, qqeFactor)

Calculates the Quantitative Qualitative Estimation (QQE) of a given data series. QQE is an improved RSI that reduces noise and provides smoother signals. Developed by Igor Livshin.

Parameters:

source (series float) : Series of values to process.

rsiLength (simple int) : Number of bars for the RSI calculation. Optional. Default is 14.

rsiSmooth (simple int) : Number of bars for smoothing the RSI. Optional. Default is 5.

qqeFactor (simple float) : QQE factor for volatility band width. Optional. Default is 4.236.

Returns: ( ) Tuple containing smoothed RSI and QQE trend line.

sslChannel(source, length)

Calculates the Semaphore Signal Level (SSL) Channel of a given data series. SSL Channel provides clear trend signals using moving averages of high and low prices.

Parameters:

source (series float) : Series of values to process.

length (simple int) : Number of bars for the moving average calculation.

Returns: ( ) Tuple containing SSL Up and SSL Down lines.

ma(source, length, maType)

Calculates a Moving Average based on the specified type. Universal interface supporting all moving average algorithms.

Parameters:

source (series float) : Series of values to process.

length (simple int) : Number of bars for the moving average calculation.

maType (simple MaType) : Type of moving average to calculate. Optional. Default is SMA.

Returns: (float) The calculated moving average value based on the specified type.

atr(length, maType)

Calculates the Average True Range (ATR) using the specified moving average type. Developed by J. Welles Wilder Jr.

Parameters:

length (simple int) : Number of bars for the ATR calculation.

maType (simple MaType) : Type of moving average to use for smoothing. Optional. Default is RMA.

Returns: (float) The calculated Average True Range value.

macd(source, fastLength, slowLength, signalLength, maType, signalMaType)

Calculates the Moving Average Convergence Divergence (MACD) with customizable MA types. Developed by Gerald Appel.

Parameters:

source (series float) : Series of values to process.

fastLength (simple int) : Period for the fast moving average.

slowLength (simple int) : Period for the slow moving average.

signalLength (simple int) : Period for the signal line moving average.

maType (simple MaType) : Type of moving average for main MACD calculation. Optional. Default is EMA.

signalMaType (simple MaType) : Type of moving average for signal line calculation. Optional. Default is EMA.

Returns: ( ) Tuple containing MACD line, signal line, and histogram values.

dmao(source, fastLength, slowLength, maType)

Calculates the Dual Moving Average Oscillator (DMAO) of a given data series. Uses the same algorithm as the Percentage Price Oscillator (PPO), but can be applied to any data series.

Parameters:

source (series float) : Series of values to process.

fastLength (simple int) : Period for the fast moving average.

slowLength (simple int) : Period for the slow moving average.

maType (simple MaType) : Type of moving average to use for both calculations. Optional. Default is EMA.

Returns: (float) The calculated Dual Moving Average Oscillator value as a percentage.

continuationIndex(source, length, gamma, order)

Calculates the Continuation Index of a given data series. The index represents the Inverse Fisher Transform of the normalized difference between an UltimateSmoother and an N-order Laguerre filter. Developed by John F. Ehlers, published in TASC 2025.09.

Parameters:

source (series float) : Series of values to process.

length (simple int) : The calculation length.

gamma (simple float) : Controls the phase response of the Laguerre filter. Optional. Default is 0.8.

order (simple int) : The order of the Laguerre filter (1-10). Optional. Default is 8.

Returns: (float) The calculated Continuation Index value.

📚 RELEASE NOTES

v1.0 (2025.09.24)

✅ 25+ technical analysis functions

✅ Complete adaptive moving average series (KAMA, FRAMA, MAMA/FAMA)

✅ Advanced signal processing filters (Kalman, Laguerre, SuperSmoother, UltimateSmoother)

✅ Performance optimized with pre-calculated constants and efficient algorithms

✅ Unified function interface design following TradingView best practices

✅ Comprehensive moving average collection (DEMA, TEMA, ZLEMA, T3, etc.)

✅ Volatility and trend detection tools (QQE, SSL Channel, Range Filter)

✅ Continuation Index - Latest research from TASC 2025.09

✅ MACD and ATR calculations supporting multiple moving average types

✅ Dual Moving Average Oscillator (DMAO) for arbitrary data series analysis

alangari EMA Crossoverإذا كان عندك متوسطين متحركين أسيين (EMA) بفترات مختلفة (مثلاً 10 و 21).

التقاطع الصاعد (Bullish Crossover): لما الـ EMA القصير (10) يقطع الـ EMA الطويل (21) من تحت لفوق → إشارة شراء.

التقاطع الهابط (Bearish Crossover): لما الـ EMA القصير يقطع الطويل من فوق لتحت → إشارة بيع.

Exponential Moving Averages (EMA) Crossover

An EMA crossover strategy uses two exponential moving averages with different periods (e.g., a fast EMA and a slow EMA).

Bullish Crossover: Occurs when the fast EMA crosses above the slow EMA, often interpreted as a buy signal indicating upward momentum.

Bearish Crossover: Occurs when the fast EMA crosses below the slow EMA, often interpreted as a sell signal indicating downward momentum.

This technique helps traders identify trend reversals and confirm the strength or weakness of the current price direction.

Simple Turnover (Enhanced v2)📊 Simple Turnover (Enhanced)

🔹 Overview

The Simple Turnover Indicator calculates a stock’s turnover by combining both price and volume, and then compares it against quarterly highs. This helps traders quickly gauge whether market participation in a move is strong enough to confirm a breakout, or weak and likely to be false.

Unlike volume alone, turnover considers both traded volume and price level, giving a truer reflection of capital flow in/out of a stock.

________________________________________

🔹 Formulae Used

1. Average Price (SMA)

AvgPrice=SMA(Close,n)

2. Average Volume (SMA)

AvgVol=SMA(Volume,n)

3. Turnover (Raw)

Turnover raw=AvgPrice × AvgVol

4. Unit Adjustment

• If Millions → Turnover = Turnover raw × 10^−6

• If Crores → Turnover = Turnover raw × 10^−7

• If Raw → Turnover = Turnover raw

5. Quarterly High Turnover (qHigh)

Within each calendar quarter (Jan–Mar, Apr–Jun, Jul–Sep, Oct–Dec), we track the maximum turnover seen:

qHigh=max (Turnover within current quarter)

________________________________________

🔹 Visualization

• Bars → Color follows price candle:

o Green if Close ≥ Open

o Red if Close < Open

• Blue Line → Rolling Quarterly High Turnover (qHigh)

________________________________________

🔹 Strategy Use Case

The Simple Turnover Indicator is most effective for confirming true vs false breakouts.

• A true breakout should be supported by increasing turnover, showing real capital backing the move.

• A false breakout often occurs with weak or declining turnover, suggesting lack of conviction.

📌 Example Strategy (3H timeframe):

1. Identify a demand zone using your preferred supply-demand indicator.

2. From this demand zone, monitor turnover bars.

3. A potential long entry is validated when:

o The current turnover bar is at least 20% higher than the previous one or two bars.

o Example setting: SMA length = 5 (i.e., turnover = 5-bar average close × 5-bar average volume).

4. This confirms strong participation in the move, increasing probability of a sustained breakout.

________________________________________

🔹 Disclaimer

⚠️ This indicator/strategy does not guarantee 100% accurate results.

It is intended to improve the probability of identifying true breakouts.

The actual success of the strategy will depend on price action, market momentum, and prevailing market conditions.

Always use this as a supporting tool along with broader trading analysis and risk management.

Irrationality Index by CRYPTO_ADA_BTC"The market can be irrational longer than you can stay solvent" ~ John Maynard Keynes

This indicator, the Irrationality Index, measures how far the current market price has deviated from a smoothed estimate of its "fair value," normalized for recent volatility. It provides traders with a visual sense of when the market may be behaving irrationally, without giving direct buy or sell signals.

How it works:

1. Fair Value Calculation

The indicator estimates a "fair value" for the asset using a combination of a long-term EMA (exponential moving average) and a linear regression trend over a configurable period. This fair value serves as a smoothed baseline for price, balancing trend-following and mean-reversion.

2. Volatility-Adjusted Z-Score

The deviation between price and fair value is measured in standard deviations of recent log returns:

Z = (log(price) - log(fairValue)) / volatility

This standardization accounts for different volatility environments, allowing comparison across assets.

3. Irrationality Score (0–100)

The Z-score is transformed using a logistic mapping into a 0–100 scale:

- 50 → price near fair value (rational zone)

- >75 → high irrationality, price stretched above fair value

- >90 → extreme irrationality, unsustainable extremes

- <25 → high irrationality, price stretched below fair value

- <10 → extreme bearish irrationality

4. Price vs Fair Value (% deviation)

The indicator plots the percentage difference between price and fair value:

pctDiff = (price - fairValue) / fairValue * 100

- Positive values → Percentage above fair value (optimistic / overvalued)

- Negative values → Percentage below fair value (pessimistic / undervalued)

Visuals:

- Irrationality (%) Line (0–100) shows irrationality level.

- Background Colors: Yellow= high bullish irrationality, Green= extreme bullish irrationality, Orange= high bearish irrationality, Red= extreme bearish irrationality.

- Price - FairValue (%) plot: price deviation vs fair value (%), Colored green above 0 and red below 0.

- Label: display actual price, estimated fair value, and Z-score for the latest bar.

- Alerts: configurable thresholds for high and extreme irrationality.

How to read it:

- 50 → Market trading near fair value.

- >75 / >90 → Price may be irrationally high; risk of pullback increases.

- <25 / <10 → Price may be irrationally low; potential rebound zones, but trends can continue.

- Price - FairValue (%) plot → visual guide for % price stretch relative to fair value.

Notes / Warnings:

- Measures relative deviation, not fundamental value!

- High irrationality scores do not automatically indicate trades; markets can remain can be irrational longer than you can stay solvent .

- Best used with other tools: momentum, volume, divergence, and multi-timeframe analysis.

Supertrend DashboardOverview

This dashboard is a multi-timeframe technical indicator dashboard based on Supertrend. It combines:

Trend detection via Supertrend

Momentum via RSI and OBV (volume)

Volatility via a basic candle-based metric (bs)

Trend strength via ADX

Multi-timeframe analysis to see whether the trend is bullish across different timeframes

It then displays this info in a table on the chart with colors for quick visual interpretation.

2️⃣ Inputs

Dashboard settings:

enableDashboard: Toggle the dashboard on/off

locationDashboard: Where the table appears (Top right, Bottom left, etc.)

sizeDashboard: Text size in the table

strategyName: Custom name for the strategy

Indicator settings:

factor (Supertrend factor): Controls how far the Supertrend lines are from price

atrLength: ATR period for Supertrend calculation

rsiLength: Period for RSI calculation

Visual settings:

colorBackground, colorFrame, colorBorder: Control dashboard style

3️⃣ Core Calculations

a) Supertrend

Supertrend is a trend-following indicator that generates bullish or bearish signals.

Logic:

Compute ATR (atr = ta.atr(atrLength))

Compute preliminary bands:

upperBand = src + factor * atr

lowerBand = src - factor * atr

Smooth bands to avoid false flips:

lowerBand := lowerBand > prevLower or close < prevLower ? lowerBand : prevLower

upperBand := upperBand < prevUpper or close > prevUpper ? upperBand : prevUpper

Determine direction (bullish / bearish):

dir = 1 → bullish

dir = -1 → bearish

Supertrend line = lowerBand if bullish, upperBand if bearish

Output:

st → line to plot

bull → boolean (true = bullish)

b) Buy / Sell Trigger

Logic:

bull = ta.crossover(close, supertrend) → close crosses above Supertrend → buy signal

bear = ta.crossunder(close, supertrend) → close crosses below Supertrend → sell signal

trigger → checks which signal was most recent:

trigger = ta.barssince(bull) < ta.barssince(bear) ? 1 : 0

1 → Buy

0 → Sell

c) RSI (Momentum)

rsi = ta.rsi(close, rsiLength)

Logic:

RSI > 50 → bullish

RSI < 50 → bearish

d) OBV / Volume Trend (vosc)

OBV tracks whether volume is pushing price up or down.

Manual calculation (safe for all Pine versions):

obv = ta.cum( math.sign( nz(ta.change(close), 0) ) * volume )

vosc = obv - ta.ema(obv, 20)

Logic:

vosc > 0 → bullish

vosc < 0 → bearish

e) Volatility (bs)

Measures how “volatile” the current candle is:

bs = ta.ema(math.abs((open - close) / math.max(high - low, syminfo.mintick) * 100), 3)

Higher % → stronger candle moves

Displayed on dashboard as a number

f) ADX (Trend Strength)

= ta.dmi(14, 14)

Logic:

adx > 20 → Trending

adx < 20 → Ranging

g) Multi-Timeframe Supertrend

Timeframes: 1m, 3m, 5m, 10m, 15m, 30m, 1H, 2H, 4H, 12H, 1D

Logic:

for tf in timeframes

= request.security(syminfo.tickerid, tf, f_supertrend(ohlc4, factor, atrLength))

array.push(tf_bulls, bull_tf ? 1.0 : 0.0)

bull_tf ? 1.0 : 0.0 → converts boolean to number

Then we calculate user rating:

userRating = (sum of bullish timeframes / total timeframes) * 10

0 → Strong Sell, 10 → Strong Buy

4️⃣ Dashboard Table Layout

Row Column 0 (Label) Column 1 (Value)

0 Strategy strategyName

1 Technical Rating textFromRating(userRating) (color-coded)

2 Current Signal Buy / Sell (based on last Supertrend crossover)

3 Current Trend Bullish / Bearish (based on Supertrend)

4 Trend Strength bs %

5 Volume vosc → Bullish/Bearish

6 Volatility adx → Trending/Ranging

7 Momentum RSI → Bullish/Bearish

8 Timeframe Trends 📶 Merged cell

9-19 1m → Daily Bullish/Bearish for each timeframe (green/red)

5️⃣ Color Logic

Green shades → bullish / trending / buy

Red / orange → bearish / weak / sell

Yellow → neutral / ranging

Example:

dashboard_cell_bg(1, 1, colorFromRating(userRating))

dashboard_cell_bg(1, 2, trigger ? color.green : color.red)

dashboard_cell_bg(1, 3, superBull ? color.green : color.red)

Makes the dashboard visually intuitive

6️⃣ Key Logic Flow

Calculate Supertrend on current timeframe

Detect buy/sell triggers based on crossover

Calculate RSI, OBV, Volatility, ADX

Request Supertrend on multiple timeframes → convert to 1/0

Compute user rating (percentage of bullish timeframes)

Populate dashboard table with colors and values

✅ The result: You get a compact, fast, multi-timeframe trend dashboard that shows:

Current signal (Buy/Sell)

Current trend (Bullish/Bearish)

Momentum, volatility, and volume cues

Trend across multiple timeframes

Overall technical rating

It’s essentially a full trend-strength scanner directly on your chart.

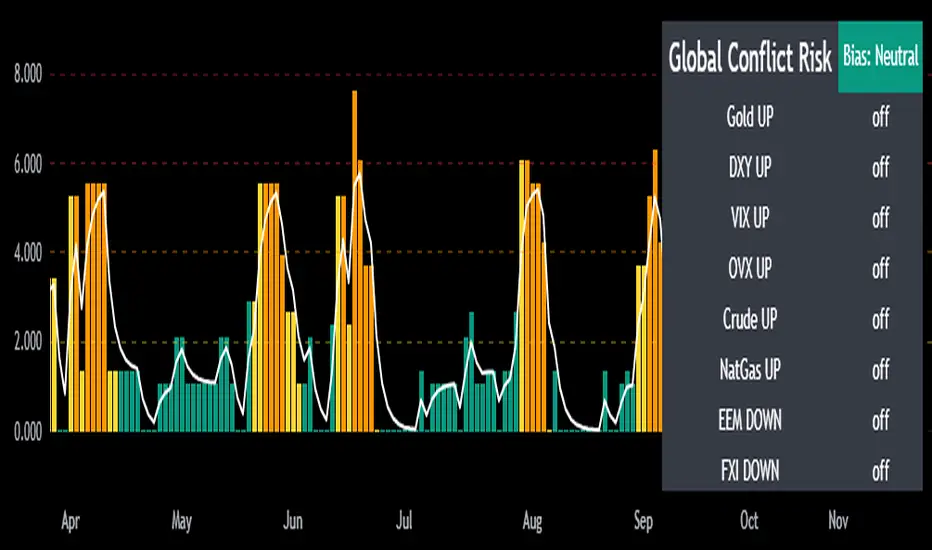

Mongoose Global Conflict Risk Index v1Overview

The Mongoose Global Conflict Risk Index v1 is a multi-asset composite indicator designed to track the early pricing of geopolitical stress and potential conflict risk across global markets. By combining signals from safe havens, volatility indices, energy markets, and emerging market equities, the index provides a normalized 0–10 score with clear bias classifications (Neutral, Caution, Elevated, High, Shock).

This tool is not predictive of headlines but captures when markets are clustering around conflict-sensitive assets before events are widely recognized.

Methodology

The indicator calculates rolling rate-of-change z-scores for eight conflict-sensitive assets:

Gold (XAUUSD) – classic safe haven

US Dollar Index (DXY) – global reserve currency flows

VIX (Equity Volatility) – S&P 500 implied volatility

OVX (Crude Oil Volatility Index) – energy stress gauge

Crude Oil (CL1!) – WTI front contract

Natural Gas (NG1!) – energy security proxy, especially Europe

EEM (Emerging Markets ETF) – global risk capital flight

FXI (China ETF) – Asia/China proxy risk

Rules:

Safe havens and vol indices trigger when z-score > threshold.

Energy triggers when z-score > threshold.

Risk assets trigger when z-score < –threshold.

Each trigger is assigned a weight, summed, normalized, and scaled 0–10.

Bias classification:

0–2: Neutral

2–4: Caution

4–6: Elevated

6–8: High

8–10: Conflict Risk-On

How to Use

Timeframes:

Daily (1D) for strategic signals and early warnings.

4H for event shocks (missiles, sanctions, sudden escalations).

Weekly (1W) for sustained trends and macro build-ups.

What to Look For:

A single trigger (for example, Gold ON) may be noise.

A cluster of 2–3 triggers across Gold, USD, VIX, and Energy often marks early stress pricing.

Elevated readings (>4) = caution; High (>6) = rotation into havens; Shock (>8) = market conviction of conflict risk.

Practical Application:

Monitor as a heatmap of global stress.

Combine with fundamental or headline tracking.

Use alert conditions at ≥4, ≥6, ≥8 for systematic monitoring.

Notes

This indicator is for informational and educational purposes only.

It is not financial advice and should be used in conjunction with other analysis methods.

Simple Technicals Table📊 Simple Technicals Table

🎯 A comprehensive technical analysis dashboard displaying key pivot points and moving averages across multiple timeframes

📋 OVERVIEW

The Simple Technicals Table is a powerful indicator that organizes essential trading data into a clean, customizable table format. It combines Fibonacci-based pivot points with critical moving averages for both daily and weekly timeframes, giving traders instant access to key support/resistance levels and trend information.

Perfect for:

Technical analysts studying multi-timeframe data

Chart readers needing quick reference levels

Market researchers analyzing price patterns

Educational purposes and data visualization

🚀 KEY FEATURES

📊 Dual Timeframe Analysis

Daily (D1) and Weekly (W1) data side-by-side

Real-time updates as market conditions change

Seamless comparison between timeframes

🎯 Fibonacci Pivot Points

R3, R2, R1 : Resistance levels using Fibonacci ratios (38.2%, 61.8%, 100%)

PP : Central pivot point from previous period's data

S1, S2, S3 : Support levels with same methodology

📈 Complete EMA Suite

EMA 10 : Short-term trend identification

EMA 20 : Popular swing trading reference

EMA 50 : Medium-term trend confirmation

EMA 100 : Institutional support/resistance

EMA 200 : Long-term trend determination

📊 Essential Indicators

RSI 14 : Momentum for overbought/oversold conditions

ATR 14 : Volatility measurement for risk management

🎨 Full Customization

9 table positions : Place anywhere on your chart

5 text sizes : Tiny to huge for optimal visibility

Custom colors : Background, headers, and text

Optional pivot lines : Visual weekly levels on chart

⚙️ HOW IT WORKS

Fibonacci Pivot Calculation:

Pivot Point (PP) = (High + Low + Close) / 3

Range = High - Low

Resistance Levels:

R1 = PP + (Range × 0.382)

R2 = PP + (Range × 0.618)

R3 = PP + (Range × 1.000)

Support Levels:

S1 = PP - (Range × 0.382)

S2 = PP - (Range × 0.618)

S3 = PP - (Range × 1.000)

Smart Price Formatting:

< $1: 5 decimal places (crypto-friendly)

$1-$10: 4 decimal places

$10-$100: 3 decimal places

> $100: 2 decimal places

📊 TECHNICAL ANALYSIS APPLICATIONS

⚠️ EDUCATIONAL PURPOSE ONLY

This indicator is designed solely for technical analysis and educational purposes . It provides data visualization to help understand market structure and price relationships.

📈 Data Analysis Uses

Support & Resistance Identification : Visualize Fibonacci-based pivot levels

Trend Analysis : Study EMA relationships and price positioning

Multi-Timeframe Study : Compare daily and weekly technical data

Market Structure : Understand key technical levels and indicators

📚 Educational Benefits

Learn about Fibonacci pivot point calculations

Understand moving average relationships

Study RSI and ATR indicator values

Practice multi-timeframe technical analysis

🔍 Data Visualization Features

Organized table format for easy data reading

Color-coded levels for quick identification

Real-time technical indicator values

Historical data integrity maintained

🛠️ SETUP GUIDE

1. Installation

Search "Simple Technicals Table" in indicators

Add to chart (appears in middle-left by default)

Table displays automatically on any timeframe

2. Customization

Table Position : Choose from 9 locations

Text Size : Adjust for screen resolution

Colors : Match your chart theme

Pivot Lines : Toggle weekly level visualization

3. Optimization Tips

Use larger text on mobile devices

Dark backgrounds work well with light text

Enable pivot lines for visual reference

✅ BEST PRACTICES

Recommended Usage:

Use for technical analysis and educational study only

Combine with other analytical methods for comprehensive analysis

Study multi-timeframe data relationships

Practice understanding technical indicator values

Important Notes:

Levels based on previous period's data

Most effective in trending markets

No repainting - uses confirmed data only

Works on all instruments and timeframes

🔧 TECHNICAL SPECS

Performance:

Pine Script v5 optimized code

Minimal CPU/memory usage

Real-time data updates

No lookahead bias

Compatibility:

All chart types (Candlestick, Bar, Line)

Any instrument (Stocks, Forex, Crypto, etc.)

All timeframes supported

Mobile and desktop friendly

Data Accuracy:

Precise floating-point calculations

Historical data integrity maintained

No future data leakage

📱 DEVICE SUPPORT

✅ Desktop browsers (Chrome, Firefox, Safari, Edge)

✅ TradingView mobile app (iOS/Android)

✅ TradingView desktop application

✅ Light and dark themes

✅ All screen resolutions

📋 VERSION INFO

Version 1.0 - Initial Release

Fibonacci-based pivot calculations

Dual timeframe support (Daily/Weekly)

Complete EMA suite (10, 20, 50, 100, 200)

RSI and ATR indicators

Fully customizable interface

Optional pivot line visualization

Smart price formatting

Mobile-optimized display

⚠️ DISCLAIMER

This indicator is designed for technical analysis, educational and informational purposes ONLY . It provides data visualization and technical calculations to help users understand market structure and price relationships.

⚠️ NOT FOR TRADING DECISIONS

This tool does NOT provide trading signals or investment advice

All data is for analytical and educational purposes only

Users should not base trading decisions solely on this indicator

Always conduct thorough research and analysis before making any financial decisions

📚 Educational Use Only

Use for learning technical analysis concepts

Study market data and indicator relationships

Practice chart reading and data interpretation

Understand mathematical calculations behind technical indicators

The Simple Technicals Table provides technical data visualization to assist in market analysis education. It does not constitute financial advice, trading recommendations, or investment guidance. Users are solely responsible for their own research and decisions.

Author: ToTrieu

Version: 1.0

Category: Technical Analysis / Support & Resistance

License: Open source for educational use

💬 Questions? Comments? Feel free to reach out!

Volume Bubbles & Liquidity Heatmap [LuxAlgo]The Volume Bubbles & Liquidity Heatmap indicator highlights volume and liquidity clearly and precisely with its volume bubbles and liquidity heat map, allowing to identify key price areas.

Customize the bubbles with different time frames and different display modes: total volume, buy and sell volume, or delta volume.

🔶 USAGE

The primary objective of this tool is to offer traders a straightforward method for analyzing volume on any selected timeframe.

By default, the tool displays buy and sell volume bubbles for the daily timeframe over the last 2,000 bars. Traders should be aware of the difference between the timeframe of the chart and that of the bubbles.

The tool also displays a liquidity heat map to help traders identify price areas where liquidity accumulates or is lacking.

🔹 Volume Bubbles

The bubbles have three possible display modes:

Total Volume: Displays the total volume of trades per bubble.

Buy & Sell Volume: Each bubble is divided into buy and sell volume.

Delta Volume: Displays the difference between buy and sell volume.

Each bubble represents the trading volume for a given period. By default, the timeframe for each bubble is set to daily, meaning each bubble represents the trading volume for each day.

The size of each bubble is proportional to the volume traded; a larger bubble indicates greater volume, while a smaller bubble indicates lower volume.

The color of each bubble indicates the dominant volume: green for buy volume and red for sell volume.

One of the tool's main goals is to facilitate simple, clear, multi-timeframe volume analysis.

The previous chart shows Delta Volume bubbles with various chart and bubble timeframe configurations.

To correctly visualize the bubbles, traders must ensure there is a sufficient number of bars per bubble. This is achieved by using a lower chart timeframe and a higher bubble timeframe.

As can be seen in the image above, the greater the difference between the chart and bubble timeframes, the better the visualization.

🔹 Liquidity Heatmap

The other main element of the tool is the liquidity heatmap. By default, it divides the chart into 25 different price areas and displays the accumulated trading volume on each.

The image above shows a 4-hour BTC chart displaying only the liquidity heatmap. Traders should be aware of these key price areas and observe how the price behaves in them, looking for possible opportunities to engage with the market.

The main parameters for controlling the heatmap on the settings panel are Rows and Cell Minimum Size. Rows modifies the number of horizontal price areas displayed, while Cell Minimum Size modifies the minimum size of each liquidity cell in each row.

As can be seen in the above BTC hourly chart, the cell size is 24 at the top and 168 at the bottom. The cells are smaller on top and bigger on the bottom.

The color of each cell reflects the liquidity size with a gradient; this reflects the total volume traded within each cell. The default colors are:

Red: larger liquidity

Yellow: medium liquidity

Blue: lower liquidity

🔹 Using Both Tools Together

This indicator provides the means to identify directional bias and market timing.

The main idea is that if buyers are strong, prices are likely to increase, and if sellers are strong, prices are likely to decrease. This gives us a directional bias for opening long or short positions. Then, we combine our directional bias with price rejection or acceptance of key liquidity levels to determine the timing of opening or closing our positions.

Now, let's review some charts.