Trendlines & SR ZonesIt's a comprehensive indicator (Pine Script v6) that represents two powerful technical analysis tools: automatic trendline detection based on pivot points and volume delta analysis with support/resistance zone identification. This overlay indicator helps traders identify potential trend directions and key price levels where significant buying or selling pressure has occurred.

Features: =

1. Price Trendlines

The indicator automatically identifies and draws trendlines based on pivot points, creating dynamic support and resistance levels.

Key Components:

Pivot Detection: Uses configurable left and right bars to identify significant pivot highs and lows

Trendline Filtering: Only draws downward-sloping resistance trendlines and upward-sloping support trendlines

Zone Creation: Creates filled zones around trendlines based on average price volatility

Automatic Management: Maintains only the 3 most recent significant trendlines to avoid chart clutter

Customization Options:

Left/Right Bars for Pivot: Adjust sensitivity of pivot detection (default: 10 bars each side)

Extension Length: Control how far trendlines extend past the second pivot (default: 50 bars)

Average Body Periods: Set the lookback period for volatility calculation (default: 100)

Tolerance Multiplier: Adjust the width of the trendline zones (default: 1.0)

Color Customization: Separate colors for high (resistance) and low (support) trendlines and their fills

2. Volume Delta % Bars

The indicator analyzes volume distribution across price levels to identify significant supply and demand zones.

Key Components:

Volume Profile Analysis: Divides the price range into rows and calculates volume delta at each level

Delta Visualization: Displays horizontal bars showing the percentage difference between buying and selling volume

Zone Identification: Automatically identifies the most significant supply and demand zones

Visual Integration: Connects volume delta bars with corresponding support/resistance zones on the price chart

Customization Options:

Lookback Period: Set the number of bars to analyze for volume (default: 200)

Price Rows: Control the granularity of the volume analysis (default: 50 rows)

Delta Sections: Adjust the number of horizontal delta bars displayed (default: 20)

Panel Appearance: Customize width, position, and direction of the delta panel

Zone Settings: Control the number of supply/demand zones and their extension (default: 3 zones)

How It Works-

Trendline Logic:

The script continuously scans for pivot highs and lows based on the specified left and right bars

When a pivot is detected, it creates a horizontal line at that price level

The script then looks for the previous pivot of the same type (high or low)

It connects these pivots with a trendline, extending it based on the user-specified setting

A parallel line is created to form a zone, with the distance based on average price volatility

The script filters out invalid trendlines (upward-sloping resistance and downward-sloping support). Only the 3 most recent trendlines are maintained to prevent chart clutter

Volume Delta Logic:

The script divides the price range over the lookback period into the specified number of rows

For each bar in the lookback period, it categorizes volume as bullish (close > open) or bearish (close < open). This volume is assigned to the appropriate price level based on the HLC3 price.

The price levels are grouped into sections, and the net delta (bullish - bearish volume) is calculated for each Horizontal bars are drawn to represent these delta percentages.

The most significant positive and negative deltas are identified and displayed as support and resistance zones. These zones are extended to the left on the price chart and connected to the delta panel with dotted lines.

Ideal Timeframes:

The indicator is versatile and can be used across multiple timeframes, but it performs optimally on specific timeframes depending on your trading style:

For Day Trading:

Optimal Timeframes: 15-minute to 1-hour charts

Why: These timeframes provide a good balance between noise reduction and sufficient volume data. The volume delta analysis is particularly effective on these timeframes as it captures intraday accumulation/distribution patterns while the trendlines remain reliable enough for intraday trading decisions.

For Swing Trading:

Optimal Timeframes: 1-hour to 4-hour charts

Why: These timeframes offer the best combination of reliable trendline formation and meaningful volume analysis. The trendlines on these timeframes are less prone to whipsaws, while the volume delta analysis captures multi-day trading sessions and institutional activity.

For Position Trading:

Optimal Timeframes: Daily and weekly charts

Why: On these higher timeframes, trendlines become extremely reliable as they represent significant market structure points. The volume delta analysis reveals longer-term accumulation and distribution patterns that can define major support and resistance zones for weeks or months.

Timeframe-Specific Adjustments:

Lower Timeframes (1-15 minutes):

Reduce left/right bars for pivots (5-8 bars)

Decrease lookback period for volume delta (50-100 bars)

Increase tolerance multiplier (1.2-1.5) to account for higher volatility

Higher Timeframes (Daily+):

Increase left/right bars for pivots (15-20 bars)

Extend lookback period for volume delta (300-500 bars)

Consider increasing the number of price rows (70-100) for more detailed volume analysis

Usage Guidelines-

For Trendline Analysis:

Use the trendlines as dynamic support and resistance levels

Price reactions at these levels can indicate potential trend continuation or reversal points

The filled zones around trendlines represent areas of price volatility or uncertainty

Consider the slope of the trendline as an indication of trend strength

For Volume Delta Analysis:

The horizontal delta bars show where buying or selling pressure has been concentrated

Green bars indicate areas where buying volume exceeded selling volume (demand)

Red bars indicate areas where selling volume exceeded buying volume (supply)

The highlighted supply and demand zones on the price chart represent significant price levels

These zones can act as future support or resistance areas as price revisits them

Customization Tips:

Trendline Sensitivity: Decrease left/right bars values to detect more pivots (more sensitive) or increase them for fewer, more significant pivots

Zone Width: Adjust the tolerance multiplier to make trendline zones wider or narrower based on your trading style

Volume Analysis: Increase the lookback period for a longer-term volume profile or decrease it for more recent activity

Visual Clarity: Adjust colors and transparency settings to match your chart theme and preferences

Conclusion:

This indicator provides traders with a comprehensive view of both trend dynamics and volume-based support/resistance levels. With these two analytical approaches, the indicator offers valuable insights for identifying potential entry and exit points, trend strength, and key price levels where significant market activity has occurred. The extensive customization options allow traders to adapt the indicator to various trading styles and timeframes, with optimal performance on 15-minute to daily charts depending on their trading horizon.

Chart Attached: NSE HINDZINC, EoD 12/12/25

DISCLAIMER: This information is provided for educational purposes only and should not be considered financial, investment, or trading advice. Please do boost if you like it. Happy Trading.

חפש סקריפטים עבור "bar"

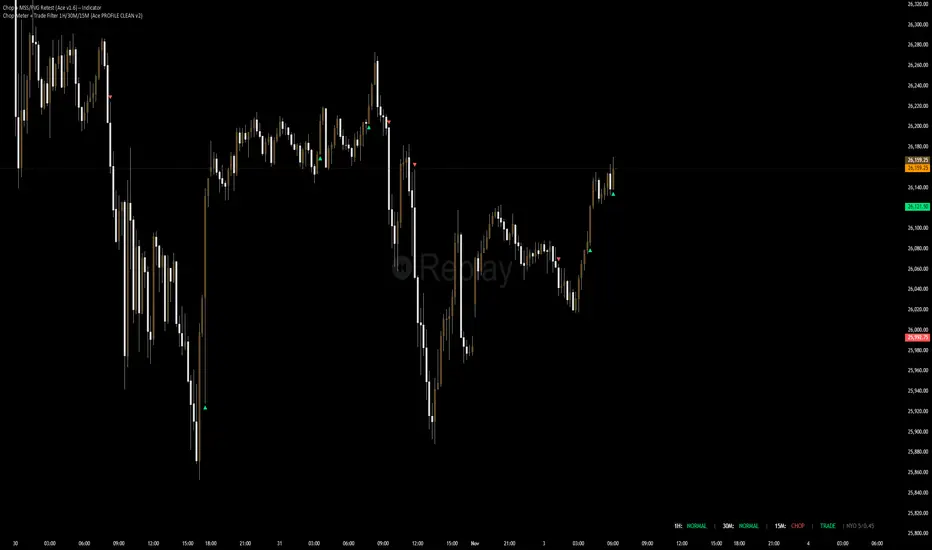

Chop + MSS/FVG Retest (Ace v1.6) – IndicatorWhat this indicator does

Name: Chop + MSS/FVG Retest (Ace v1.6) – Indicator

This is an entry model helper, not just a BOS/MSS marker.

It looks for clean trend-side setups by combining:

MSS (Market Structure Shift) using swing highs/lows

3-bar ICT Fair Value Gaps (FVG)

First retest back into the FVG

A built-in chop / trend filter based on ATR and a moving average

When everything lines up, it plots:

L below the candle = Long candidate

S above the candle = Short candidate

You pair this with a higher-timeframe filter (like the Chop Meter 1H/30M/15M) to avoid pressing the button in garbage environments.

How it works (simple explanation)

Chop / Trend filter

Computes ATR and compares each bar’s range to ATR.

If the bar is small vs ATR → more likely CHOP.

If the bar is big vs ATR → more likely TREND.

Uses a moving average:

Above MA + TREND → trendLong zone

Below MA + TREND → trendShort zone

MSS (Market Structure Shift)

Uses swing highs/lows (left/right bars) to track the last significant high/low.

Bullish MSS: close breaks above last swing high with displacement.

Bearish MSS: close breaks below last swing low with displacement.

Those events are marked as tiny triangles (MSS up/down).

A MSS only stays “valid” for a certain number of bars (Bars after MSS allowed).

3-bar ICT FVG

Bullish FVG: low > high

→ gap between bar 3 high and bar 2 low.

Bearish FVG: high < low

→ gap between bar 3 low and bar 2 high.

The indicator stores the FVG boundaries (top/bottom).

Retest of FVG

Watches for price to trade back into that gap (first touch).

That retest is the “entry zone” after the MSS.

Final Long / Short condition

Long (L) prints when:

Recent bullish MSS

Bullish FVG has formed

Price retests the bullish FVG

Environment = trendLong (ATR + above MA)

Not CHOP

Short (S) prints when:

Recent bearish MSS

Bearish FVG has formed

Price retests the bearish FVG

Environment = trendShort (ATR + below MA)

Not CHOP

So the L/S markers are “model-approved entry candles”, not just any random BOS.

Inputs / Settings

Key inputs you’ll see:

ATR length (chop filter)

How many bars to use for ATR in the chop / trend filter.

Lower = more sensitive, twitchy

Higher = smoother, slower to change

Max chop ratio

If barRange / ATR is below this → treat as CHOP.

Min trend ratio

If barRange / ATR is above this → treat as TREND.

Hide MSS/BOS marks in CHOP?

ON = MSS triangles disappear when the bar is classified as CHOP

Keeps your chart cleaner in consolidation

Swing left / right bars

Controls how tight or wide the swing highs/lows are for MSS:

Smaller = more sensitive, more MSS points

Larger = fewer, more significant swings

Bars after MSS allowed

How many bars after a MSS the indicator will still allow FVG entries.

Small value (e.g. 10) = MSS must deliver quickly or it’s ignored.

Larger (e.g. 20) = MSS idea stays “in play” longer.

Visual RR (for info only)

Just for plotting relative risk-reward in your head.

This is not a strategy tester; it doesn’t manage positions.

What you see on the chart

Small green triangle up = Bullish MSS

Small red triangle down = Bearish MSS

“L” triangle below a bar = Long idea (MSS + FVG retest + trendLong + not chop)

“S” triangle above a bar = Short idea (MSS + FVG retest + trendShort + not chop)

Faint circle plots on price:

When the filter sees CHOP

When it sees Trend Long zone

When it sees Trend Short zone

You do not have to trade every L or S.

They’re there to show “this is where the model would have considered an entry.”

How to use it in your trading

1. Use it with a higher-timeframe filter

Best practice:

Use this with the Chop Meter 1H/30M/15M or some other HTF filter.

Only consider L/S when:

Chop Meter = TRADE / NORMAL, and

This indicator prints L or S in the right location (premium/discount, near OB/FVG, etc.)

If higher-timeframe says NO TRADE, you ignore all L/S.

2. Location > Signal

Treat L/S as confirmation, not the whole story.

For shorts (S):

Look for premium zones (previous highs, OBs, fair value ranges above mid).

Want purge / raid of liquidity + MSS down + bearish FVG retest → then S.

For longs (L):

Look for discount zones (previous lows, OBs/FVGs below mid).

Want stop raid / purge low + MSS up + bullish FVG retest → then L.

If you see L/S firing in the middle of a bigger range, that’s where you skip and let it go.

3. Instrument presets (example)

You can tune the ATR/chop settings per instrument:

MNQ (noisy, 1m chart):

ATR length: 21

Max chop ratio: 0.90

Min trend ratio: 1.40

Bars after MSS allowed: 10

GOLD (cleaner, 3m chart):

ATR length: 14

Max chop ratio: 0.80

Min trend ratio: 1.30

Bars after MSS allowed: 20

You can save those as presets in the TV settings for quick switching.

4. How to practice with it

Open replay on a couple of days.

Check Chop Meter → if NO TRADE, just observe.

When Chop Meter says TRADE:

Mark where L/S printed.

Ask:

Was this in premium/discount?

Was there SMT / purge on HTF?

Did the move actually deliver, or did it die?

Screenshot the A+ L/S and the ugly ones; refine:

ATR length

Chop / trend thresholds

MSS lookback

Your goal is to get it to where:

The L/S marks show up mostly in the same places your eye already likes,

and you ignore the rest.

Pinbar MTF - No Repaint# Pinbar MTF - No Repaint Indicator

## Complete Technical Documentation

---

## 📊 Overview

**Pinbar MTF (Multi-Timeframe) - No Repaint** is a professional-grade TradingView Pine Script indicator designed to detect high-probability pinbar reversal patterns with advanced filtering systems. The indicator is specifically engineered to be **100% non-repainting**, making it reliable for both live trading and backtesting.

### Key Features

✅ **Non-Repainting** - Signals only appear AFTER bar closes, never disappear

✅ **Three-Layer Filter System** - ATR, SWING, and RSI filters

✅ **Automatic SL/TP Calculation** - Based on risk:reward ratios

✅ **Real-time Alerts** - TradingView notifications for all signals

✅ **Visual Trade Management** - Lines, labels, and areas for entries, stops, and targets

✅ **Backtesting Ready** - Reliable historical data for strategy testing

---

## 🎯 What is a Pinbar?

A **Pinbar (Pin Bar/Pinocchio Bar)** is a single candlestick pattern that indicates a potential price reversal:

### Bullish Pinbar (BUY Signal)

- **Long lower wick** (rejection of lower prices)

- **Small body at the top** of the candle

- Shows buyers rejected sellers' attempt to push price down

- Forms at support levels or swing lows

- Entry signal for LONG positions

### Bearish Pinbar (SELL Signal)

- **Long upper wick** (rejection of higher prices)

- **Small body at the bottom** of the candle

- Shows sellers rejected buyers' attempt to push price up

- Forms at resistance levels or swing highs

- Entry signal for SHORT positions

---

## 🔧 How the Indicator Works

### 1. **Pinbar Detection Logic**

The indicator analyzes the **previous closed bar ** to identify pinbar patterns:

```

Bullish Pinbar Requirements:

- Lower wick > 72% of total candle range (adjustable)

- Upper wick < 28% of total candle range

- Close > Open (bullish candle body)

Bearish Pinbar Requirements:

- Upper wick > 72% of total candle range (adjustable)

- Lower wick < 28% of total candle range

- Close < Open (bearish candle body)

```

**Why check ?** By analyzing the previous completed bar, we ensure the pattern is fully formed and won't change, preventing repainting.

---

### 2. **Three-Layer Filter System**

#### 🔍 **Filter #1: ATR (Average True Range) Filter**

- **Purpose**: Ensures the pinbar has significant size

- **Function**: Only signals if pinbar range ≥ ATR value

- **Benefit**: Filters out small, insignificant pinbars

- **Settings**:

- Enable/Disable toggle

- ATR Period (default: 7)

**Example**: If ATR = 50 pips, only pinbars with 50+ pip range will signal.

---

#### 🔍 **Filter #2: SWING Filter** (Always Active)

- **Purpose**: Confirms pinbar forms at swing highs/lows

- **Function**: Validates the pinbar is an absolute high/low

- **Benefit**: Identifies true reversal points

- **Settings**:

- Swing Candles (default: 3)

**How it works**:

- For bullish pinbar: Checks if low is lowest of past 3 bars

- For bearish pinbar: Checks if high is highest of past 3 bars

**Example**: With 3 swing candles, a bullish pinbar must have the lowest low among the last 3 bars.

---

#### 🔍 **Filter #3: RSI (Relative Strength Index) Filter**

- **Purpose**: Confirms momentum conditions

- **Function**: Prevents signals in extreme momentum zones

- **Benefit**: Avoids counter-trend trades

- **Settings**:

- Enable/Disable toggle

- RSI Period (default: 7)

- RSI Source (Close, Open, High, Low, HL2, HLC3, OHLC4)

- Overbought Level (default: 70)

- Oversold Level (default: 30)

**Logic**:

- Bullish Pinbar: Only signals if RSI < 70 (not overbought)

- Bearish Pinbar: Only signals if RSI > 30 (not oversold)

---

### 3. **Stop Loss Calculation**

Two methods available:

#### Method A: ATR-Based Stop Loss (Recommended)

```

Bullish Pinbar:

SL = Pinbar Low - (1 × ATR)

Bearish Pinbar:

SL = Pinbar High + (1 × ATR)

```

**Benefit**: Dynamic stops that adapt to market volatility

#### Method B: Fixed Pips Stop Loss

```

Bullish Pinbar:

SL = Pinbar Low - (Fixed Pips)

Bearish Pinbar:

SL = Pinbar High + (Fixed Pips)

```

**Settings**:

- Calculate Stop with ATR (toggle)

- Stop Pips without ATR (default: 5)

---

### 4. **Take Profit Calculation**

Take Profit is calculated based on Risk:Reward ratio:

```

Bullish Trade:

TP = Entry + (Entry - SL) × Risk:Reward Ratio

Bearish Trade:

TP = Entry - (SL - Entry) × Risk:Reward Ratio

```

**Example**:

- Entry: 1.2000

- SL: 1.1950 (50 pip risk)

- RR: 2:1

- TP: 1.2100 (100 pip reward = 50 × 2)

**Settings**:

- Risk:Reward Ratio (default: 1.0, range: 0.1 to 10.0)

---

## 📈 Visual Elements

### On-Chart Displays

1. **Signal Markers**

- 🟢 **Green Triangle Up** = Bullish Pinbar (BUY)

- 🔴 **Red Triangle Down** = Bearish Pinbar (SELL)

- Placed directly on the pinbar candle

2. **Entry Labels**

- Green "BUY" label with entry price

- Red "SELL" label with entry price

- Shows exact entry level

3. **Stop Loss Lines**

- 🔴 Red horizontal line

- "SL" label

- Extends 20 bars forward

4. **Take Profit Lines**

- 🟢 Green horizontal line

- "TP" label

- Extends 20 bars forward

5. **Risk/Reward Areas** (Optional)

- Red shaded box = Risk zone (Entry to SL)

- Green shaded box = Reward zone (Entry to TP)

- Visual risk:reward visualization

6. **Info Table** (Top Right)

- Displays current settings

- Shows filter status (ON/OFF)

- Real-time RSI value

- Quick reference panel

---

## 🔔 Alert System

Three alert types available:

### 1. Combined Alert: "Pinbar Signal (Any Direction)"

- Fires for BOTH bullish and bearish pinbars

- **Best for**: General monitoring

- **Message**: "Pinbar Signal Detected on {TICKER} at {PRICE}"

### 2. Bullish Alert: "Bullish Pinbar Alert"

- Fires ONLY for BUY signals

- **Best for**: Long-only strategies

- **Message**: "BUY Signal on {TICKER} at {PRICE}"

### 3. Bearish Alert: "Bearish Pinbar Alert"

- Fires ONLY for SELL signals

- **Best for**: Short-only strategies

- **Message**: "SELL Signal on {TICKER} at {PRICE}"

---

## ⚙️ Input Parameters Reference

### **Filters Group**

| Parameter | Default | Range | Description |

|-----------|---------|-------|-------------|

| ATR Filter on Pinbar Range? | ✅ ON | Boolean | Enable/disable ATR filter |

| ATR Period | 7 | 1+ | Lookback period for ATR calculation |

| Swing Candles | 3 | 1+ | Bars to check for swing high/low |

| RSI Filter on Pinbar? | ❌ OFF | Boolean | Enable/disable RSI filter |

| RSI Period | 7 | 2+ | Lookback period for RSI calculation |

| RSI Source | Close | Multiple | Price data for RSI (Close/Open/High/Low/etc) |

| RSI Overbought Level | 70 | 50-100 | Upper threshold for RSI filter |

| RSI Oversold Level | 30 | 0-50 | Lower threshold for RSI filter |

### **Pinbar Detection Group**

| Parameter | Default | Range | Description |

|-----------|---------|-------|-------------|

| Shadow % vs Body | 72 | 50-95 | Minimum wick size as % of total range |

### **Visualization Group**

| Parameter | Default | Range | Description |

|-----------|---------|-------|-------------|

| Show SL and TP Lines? | ✅ ON | Boolean | Display stop loss and take profit lines |

| Show SL and TP Area? | ❌ OFF | Boolean | Show shaded risk/reward boxes |

### **Risk Management Group**

| Parameter | Default | Range | Description |

|-----------|---------|-------|-------------|

| Risk:Reward Ratio | 1.0 | 0.1-10.0 | Target profit vs risk (1.0 = 1:1, 2.0 = 1:2) |

| Calculate Stop with ATR? | ✅ ON | Boolean | Use ATR for stop calculation |

| Stop Pips without ATR | 5 | 1+ | Fixed pip stop when ATR disabled |

---

## 🚫 Non-Repainting Architecture

### What is Repainting?

**Repainting** occurs when an indicator's historical signals differ from what appeared in real-time. This makes backtesting unreliable and can lead to false confidence in a strategy.

### How This Indicator Prevents Repainting

1. **Closed Bar Analysis**

- All calculations use ` ` offset (previous bar)

- Only analyzes COMPLETED candles

- Signals appear on the bar AFTER the pinbar closes

2. **Confirmed Swing Points**

- Waits for sufficient bar history before signaling

- Only checks historical bars that cannot change

- Prevents premature swing detection

3. **Static Alert Timing**

- Alerts fire only after bar completion

- No conditional logic that changes historically

- Same results in replay mode and live trading

### Verification Method

To verify non-repainting behavior:

1. Apply indicator to chart

2. Note signal locations and prices

3. Refresh browser / reload chart

4. **Signals remain in exact same locations**

---

## 💼 Trading Strategy Guidelines

### Entry Rules

**For Bullish Pinbar (LONG):**

1. Wait for green triangle to appear

2. Enter at close of pinbar (shown in label)

3. Alternative: Enter on break of pinbar high

4. Place stop loss at red SL line

5. Set target at green TP line

**For Bearish Pinbar (SHORT):**

1. Wait for red triangle to appear

2. Enter at close of pinbar (shown in label)

3. Alternative: Enter on break of pinbar low

4. Place stop loss at red SL line

5. Set target at green TP line

### Risk Management

- **Position Sizing**: Risk only 1-2% of account per trade

- **Stop Loss**: Always use the calculated SL (never move it wider)

- **Take Profit**: Use calculated TP or trail stop after 1:1 RR

- **Multiple Timeframes**: Confirm signals on higher timeframe

### Best Practices

✅ **DO:**

- Wait for bar to close before entering

- Trade in direction of higher timeframe trend

- Use on liquid markets with clear support/resistance

- Combine with price action analysis

- Keep a trading journal

❌ **DON'T:**

- Enter before bar closes (prevents seeing full pattern)

- Trade against strong trends

- Ignore the filters (they improve win rate)

- Risk more than 2% per trade

- Trade every signal (be selective)

---

## 📊 Backtesting & Data Export

### Available Data Points

The indicator exports these values for strategy development:

| Output | Description |

|--------|-------------|

| Bullish Signal | 1 = BUY signal, 0 = No signal |

| Bearish Signal | 1 = SELL signal, 0 = No signal |

| Bull SL | Stop loss level for long trades |

| Bull TP | Take profit level for long trades |

| Bull Entry | Entry price for long trades |

| Bear SL | Stop loss level for short trades |

| Bear TP | Take profit level for short trades |

| Bear Entry | Entry price for short trades |

### How to Use in Strategy

These values can be accessed by Pine Script strategies using:

```pine

indicator_values = request.security(syminfo.tickerid, timeframe.period,

)

```

---

## 🎓 Understanding the Filters

### Why Use Multiple Filters?

Single-indicator systems often generate too many false signals. This indicator uses a **confluence approach**:

1. **Pinbar Pattern** = Price rejection detected

2. **+ SWING Filter** = Rejection at key level

3. **+ ATR Filter** = Significant move

4. **+ RSI Filter** = Favorable momentum

**Result**: Higher probability setups with better risk:reward

### Filter Optimization

**Conservative Settings** (Fewer, Higher Quality Signals):

- ATR Filter: ON

- Swing Candles: 5

- RSI Filter: ON

- Shadow %: 75%

**Aggressive Settings** (More Signals, More Noise):

- ATR Filter: OFF

- Swing Candles: 2

- RSI Filter: OFF

- Shadow %: 65%

**Balanced Settings** (Recommended):

- ATR Filter: ON

- Swing Candles: 3

- RSI Filter: OFF (or ON for trending markets)

- Shadow %: 72%

---

## 🔍 Troubleshooting

### "No Signals Appearing"

**Possible Causes:**

1. Filters are too strict

2. No pinbars forming on chart

3. Insufficient bar history

**Solutions:**

- Reduce Shadow % to 65%

- Reduce Swing Candles to 2

- Disable ATR or RSI filters temporarily

- Check that chart has enough data loaded

### "Too Many Signals"

**Solutions:**

- Enable ATR filter

- Increase Swing Candles to 4-5

- Enable RSI filter

- Increase Shadow % to 75-80%

### "Signals Appearing Late"

**This is normal behavior!** The indicator:

- Analyzes previous closed bar

- Signals appear on the bar AFTER the pinbar

- This is what prevents repainting

- Signal latency is 1 bar (by design)

---

## 📝 Technical Specifications

**Indicator Type:** Overlay (displays on price chart)

**Pine Script Version:** 5

**Max Labels:** 500

**Max Lines:** 500

**Repainting:** None (100% non-repainting)

**Data Window Values:** 8 exported values

**Alert Types:** 3 (Combined, Bullish, Bearish)

**Performance:**

- Lightweight script (fast execution)

- Works on all timeframes

- Compatible with all markets (Forex, Crypto, Stocks, Futures)

- No data snooping bias

---

## 🎯 Use Cases

### 1. **Swing Trading**

- Timeframe: Daily, 4H

- Filter Settings: All enabled

- Best for: Catching major reversals

### 2. **Day Trading**

- Timeframe: 15m, 1H

- Filter Settings: ATR + SWING only

- Best for: Intraday reversals

### 3. **Scalping**

- Timeframe: 5m, 15m

- Filter Settings: SWING only (aggressive)

- Best for: Quick reversals (requires experience)

### 4. **Position Trading**

- Timeframe: Weekly, Daily

- Filter Settings: All enabled + high RR (2:1 or 3:1)

- Best for: Long-term trend reversal catches

---

## 🏆 Advantages Over Other Pinbar Indicators

✅ **Guaranteed Non-Repainting** - Many pinbar indicators repaint; this one never does

✅ **Automatic SL/TP** - No manual calculation needed

✅ **Multi-Layer Filtering** - Reduces false signals significantly

✅ **Visual Trade Management** - Clear entry, stop, and target levels

✅ **Flexible Configuration** - Adaptable to any trading style

✅ **Alert System** - Never miss a setup

✅ **Backtesting Ready** - Reliable historical data

✅ **Professional Grade** - Suitable for live trading

---

## 📚 Educational Resources

### Recommended Reading on Pinbars

- "The Pin Bar Trading Strategy" by Nial Fuller

- "Price Action Trading" by Al Brooks

- TradingView Education: Price Action Patterns

### Practice Recommendations

1. Paper trade signals for 20+ trades before live trading

2. Backtest on different timeframes and markets

3. Keep detailed records of all trades

4. Analyze winning vs losing setups

5. Refine filter settings based on results

---

## ⚖️ Disclaimer

This indicator is a tool for technical analysis and does not guarantee profits. Trading involves substantial risk of loss. Past performance is not indicative of future results.

- Always use proper risk management

- Never risk more than you can afford to lose

- Consider your trading experience and objectives

- Seek independent financial advice if needed

---

## 📧 Version Information

**Current Version:** 1.0

**Last Updated:** 2024

**Compatibility:** TradingView Pine Script v5

**Status:** Production Ready

---

## 🔄 Future Enhancements (Potential)

Possible future additions:

- Multi-timeframe confirmation option

- Volume filter integration

- Customizable color schemes

- Win rate statistics display

- Partial profit taking levels

- Trailing stop functionality

---

## 📖 Quick Start Guide

### 5-Minute Setup

1. **Add to Chart**

- Open TradingView

- Go to Pine Editor

- Paste the code

- Click "Add to Chart"

2. **Configure Settings**

- Open indicator settings (gear icon)

- Start with default settings

- Enable "Show SL and TP Lines"

3. **Set Alert**

- Right-click indicator name

- Click "Add Alert"

- Select "Pinbar Signal (Any Direction)"

- Configure notification method

4. **Test**

- Scroll back on chart

- Verify signals make sense

- Check that signals don't repaint

5. **Trade** (After Practice!)

- Wait for alert

- Verify signal quality

- Enter, place SL/TP

- Manage trade

---

## 🎯 Final Thoughts

The **Pinbar MTF - No Repaint** indicator is designed for serious traders who value:

- **Reliability** over flashy signals

- **Quality** over quantity

- **Honesty** over false promises

This indicator will NOT:

- Make you rich overnight

- Win every trade

- Replace proper trading education

This indicator WILL:

- Identify high-probability reversal setups

- Save you analysis time

- Provide consistent, non-repainting signals

- Help you develop a systematic trading approach

**Success in trading comes from:**

1. Proper education (60%)

2. Risk management (30%)

3. Technical tools like this indicator (10%)

Use this tool as part of a complete trading plan, not as a standalone solution.

Historical Matrix Analyzer [PhenLabs]📊Historical Matrix Analyzer

Version: PineScriptv6

📌Description

The Historical Matrix Analyzer is an advanced probabilistic trading tool that transforms technical analysis into a data-driven decision support system. By creating a comprehensive 56-cell matrix that tracks every combination of RSI states and multi-indicator conditions, this indicator reveals which market patterns have historically led to profitable outcomes and which have not.

At its core, the indicator continuously monitors seven distinct RSI states (ranging from Extreme Oversold to Extreme Overbought) and eight unique indicator combinations (MACD direction, volume levels, and price momentum). For each of these 56 possible market states, the system calculates average forward returns, win rates, and occurrence counts based on your configurable lookback period. The result is a color-coded probability matrix that shows you exactly where you stand in the historical performance landscape.

The standout feature is the Current State Panel, which provides instant clarity on your active market conditions. This panel displays signal strength classifications (from Strong Bullish to Strong Bearish), the average return percentage for similar past occurrences, an estimated win rate using Bayesian smoothing to prevent small-sample distortions, and a confidence level indicator that warns you when insufficient data exists for reliable conclusions.

🚀Points of Innovation

Multi-dimensional state classification combining 7 RSI levels with 8 indicator combinations for 56 unique trackable market conditions

Bayesian win rate estimation with adjustable smoothing strength to provide stable probability estimates even with limited historical samples

Real-time active cell highlighting with “NOW” marker that visually connects current market conditions to their historical performance data

Configurable color intensity sensitivity allowing traders to adjust heat-map responsiveness from conservative to aggressive visual feedback

Dual-panel display system separating the comprehensive statistics matrix from an easy-to-read current state summary panel

Intelligent confidence scoring that automatically warns traders when occurrence counts fall below reliable thresholds

🔧Core Components

RSI State Classification: Segments RSI readings into 7 distinct zones (Extreme Oversold <20, Oversold 20-30, Weak 30-40, Neutral 40-60, Strong 60-70, Overbought 70-80, Extreme Overbought >80) to capture momentum extremes and transitions

Multi-Indicator Condition Tracking: Simultaneously monitors MACD crossover status (bullish/bearish), volume relative to moving average (high/low), and price direction (rising/falling) creating 8 binary-encoded combinations

Historical Data Storage Arrays: Maintains rolling lookback windows storing RSI states, indicator states, prices, and bar indices for precise forward-return calculations

Forward Performance Calculator: Measures price changes over configurable forward bar periods (1-20 bars) from each historical state, accumulating total returns and win counts per matrix cell

Bayesian Smoothing Engine: Applies statistical prior assumptions (default 50% win rate) weighted by user-defined strength parameter to stabilize estimated win rates when sample sizes are small

Dynamic Color Mapping System: Converts average returns into color-coded heat map with intensity adjusted by sensitivity parameter and transparency modified by confidence levels

🔥Key Features

56-Cell Probability Matrix: Comprehensive grid displaying every possible combination of RSI state and indicator condition, with each cell showing average return percentage, estimated win rate, and occurrence count for complete statistical visibility

Current State Info Panel: Dedicated display showing your exact position in the matrix with signal strength emoji indicators, numerical statistics, and color-coded confidence warnings for immediate situational awareness

Customizable Lookback Period: Adjustable historical window from 50 to 500 bars allowing traders to focus on recent market behavior or capture longer-term pattern stability across different market cycles

Configurable Forward Performance Window: Select target holding periods from 1 to 20 bars ahead to align probability calculations with your trading timeframe, whether day trading or swing trading

Visual Heat Mapping: Color-coded cells transition from red (bearish historical performance) through gray (neutral) to green (bullish performance) with intensity reflecting statistical significance and occurrence frequency

Intelligent Data Filtering: Minimum occurrence threshold (1-10) removes unreliable patterns with insufficient historical samples, displaying gray warning colors for low-confidence cells

Flexible Layout Options: Independent positioning of statistics matrix and info panel to any screen corner, accommodating different chart layouts and personal preferences

Tooltip Details: Hover over any matrix cell to see full RSI label, complete indicator status description, precise average return, estimated win rate, and total occurrence count

🎨Visualization

Statistics Matrix Table: A 9-column by 8-row grid with RSI states labeling vertical axis and indicator combinations on horizontal axis, using compact abbreviations (XOverS, OverB, MACD↑, Vol↓, P↑) for space efficiency

Active Cell Indicator: The current market state cell displays “⦿ NOW ⦿” in yellow text with enhanced color saturation to immediately draw attention to relevant historical performance

Signal Strength Visualization: Info panel uses emoji indicators (🔥 Strong Bullish, ✅ Bullish, ↗️ Weak Bullish, ➖ Neutral, ↘️ Weak Bearish, ⛔ Bearish, ❄️ Strong Bearish, ⚠️ Insufficient Data) for rapid interpretation

Histogram Plot: Below the price chart, a green/red histogram displays the current cell’s average return percentage, providing a time-series view of how historical performance changes as market conditions evolve

Color Intensity Scaling: Cell background transparency and saturation dynamically adjust based on both the magnitude of average returns and the occurrence count, ensuring visual emphasis on reliable patterns

Confidence Level Display: Info panel bottom row shows “High Confidence” (green), “Medium Confidence” (orange), or “Low Confidence” (red) based on occurrence counts relative to minimum threshold multipliers

📖Usage Guidelines

RSI Period

Default: 14

Range: 1 to unlimited

Description: Controls the lookback period for RSI momentum calculation. Standard 14-period provides widely-recognized overbought/oversold levels. Decrease for faster, more sensitive RSI reactions suitable for scalping. Increase (21, 28) for smoother, longer-term momentum assessment in swing trading. Changes affect how quickly the indicator moves between the 7 RSI state classifications.

MACD Fast Length

Default: 12

Range: 1 to unlimited

Description: Sets the faster exponential moving average for MACD calculation. Standard 12-period setting works well for daily charts and captures short-term momentum shifts. Decreasing creates more responsive MACD crossovers but increases false signals. Increasing smooths out noise but delays signal generation, affecting the bullish/bearish indicator state classification.

MACD Slow Length

Default: 26

Range: 1 to unlimited

Description: Defines the slower exponential moving average for MACD calculation. Traditional 26-period setting balances trend identification with responsiveness. Must be greater than Fast Length. Wider spread between fast and slow increases MACD sensitivity to trend changes, impacting the frequency of indicator state transitions in the matrix.

MACD Signal Length

Default: 9

Range: 1 to unlimited

Description: Smoothing period for the MACD signal line that triggers bullish/bearish state changes. Standard 9-period provides reliable crossover signals. Shorter values create more frequent state changes and earlier signals but with more whipsaws. Longer values produce more confirmed, stable signals but with increased lag in detecting momentum shifts.

Volume MA Period

Default: 20

Range: 1 to unlimited

Description: Lookback period for volume moving average used to classify volume as “high” or “low” in indicator state combinations. 20-period default captures typical monthly trading patterns. Shorter periods (10-15) make volume classification more reactive to recent spikes. Longer periods (30-50) require more sustained volume changes to trigger state classification shifts.

Statistics Lookback Period

Default: 200

Range: 50 to 500

Description: Number of historical bars used to calculate matrix statistics. 200 bars provides substantial data for reliable patterns while remaining responsive to regime changes. Lower values (50-100) emphasize recent market behavior and adapt quickly but may produce volatile statistics. Higher values (300-500) capture long-term patterns with stable statistics but slower adaptation to changing market dynamics.

Forward Performance Bars

Default: 5

Range: 1 to 20

Description: Number of bars ahead used to calculate forward returns from each historical state occurrence. 5-bar default suits intraday to short-term swing trading (5 hours on hourly charts, 1 week on daily charts). Lower values (1-3) target short-term momentum trades. Higher values (10-20) align with position trading and longer-term pattern exploitation.

Color Intensity Sensitivity

Default: 2.0

Range: 0.5 to 5.0, step 0.5

Description: Amplifies or dampens the color intensity response to average return magnitudes in the matrix heat map. 2.0 default provides balanced visual emphasis. Lower values (0.5-1.0) create subtle coloring requiring larger returns for full saturation, useful for volatile instruments. Higher values (3.0-5.0) produce vivid colors from smaller returns, highlighting subtle edges in range-bound markets.

Minimum Occurrences for Coloring

Default: 3

Range: 1 to 10

Description: Required minimum sample size before applying color-coded performance to matrix cells. Cells with fewer occurrences display gray “insufficient data” warning. 3-occurrence default filters out rare patterns. Lower threshold (1-2) shows more data but includes unreliable single-event statistics. Higher thresholds (5-10) ensure only well-established patterns receive visual emphasis.

Table Position

Default: top_right

Options: top_left, top_right, bottom_left, bottom_right

Description: Screen location for the 56-cell statistics matrix table. Position to avoid overlapping critical price action or other indicators on your chart. Consider chart orientation and candlestick density when selecting optimal placement.

Show Current State Panel

Default: true

Options: true, false

Description: Toggle visibility of the dedicated current state information panel. When enabled, displays signal strength, RSI value, indicator status, average return, estimated win rate, and confidence level for active market conditions. Disable to declutter charts when only the matrix table is needed.

Info Panel Position

Default: bottom_left

Options: top_left, top_right, bottom_left, bottom_right

Description: Screen location for the current state information panel (when enabled). Position independently from statistics matrix to optimize chart real estate. Typically placed opposite the matrix table for balanced visual layout.

Win Rate Smoothing Strength

Default: 5

Range: 1 to 20

Description: Controls Bayesian prior weighting for estimated win rate calculations. Acts as virtual sample size assuming 50% win rate baseline. Default 5 provides moderate smoothing preventing extreme win rate estimates from small samples. Lower values (1-3) reduce smoothing effect, allowing win rates to reflect raw data more directly. Higher values (10-20) increase conservatism, pulling win rate estimates toward 50% until substantial evidence accumulates.

✅Best Use Cases

Pattern-based discretionary trading where you want historical confirmation before entering setups that “look good” based on current technical alignment

Swing trading with holding periods matching your forward performance bar setting, using high-confidence bullish cells as entry filters

Risk assessment and position sizing, allocating larger size to trades originating from cells with strong positive average returns and high estimated win rates

Market regime identification by observing which RSI states and indicator combinations are currently producing the most reliable historical patterns

Backtesting validation by comparing your manual strategy signals against the historical performance of the corresponding matrix cells

Educational tool for developing intuition about which technical condition combinations have actually worked versus those that feel right but lack historical evidence

⚠️Limitations

Historical patterns do not guarantee future performance, especially during unprecedented market events or regime changes not represented in the lookback period

Small sample sizes (low occurrence counts) produce unreliable statistics despite Bayesian smoothing, requiring caution when acting on low-confidence cells

Matrix statistics lag behind rapidly changing market conditions, as the lookback period must accumulate new state occurrences before updating performance data

Forward return calculations use fixed bar periods that may not align with actual trade exit timing, support/resistance levels, or volatility-adjusted profit targets

💡What Makes This Unique

Multi-Dimensional State Space: Unlike single-indicator tools, simultaneously tracks 56 distinct market condition combinations providing granular pattern resolution unavailable in traditional technical analysis

Bayesian Statistical Rigor: Implements proper probabilistic smoothing to prevent overconfidence from limited data, a critical feature missing from most pattern recognition tools

Real-Time Contextual Feedback: The “NOW” marker and dedicated info panel instantly connect current market conditions to their historical performance profile, eliminating guesswork

Transparent Occurrence Counts: Displays sample sizes directly in each cell, allowing traders to judge statistical reliability themselves rather than hiding data quality issues

Fully Customizable Analysis Window: Complete control over lookback depth and forward return horizons lets traders align the tool precisely with their trading timeframe and strategy requirements

🔬How It Works

1. State Classification and Encoding

Each bar’s RSI value is evaluated and assigned to one of 7 discrete states based on threshold levels (0: <20, 1: 20-30, 2: 30-40, 3: 40-60, 4: 60-70, 5: 70-80, 6: >80)

Simultaneously, three binary conditions are evaluated: MACD line position relative to signal line, current volume relative to its moving average, and current close relative to previous close

These three binary conditions are combined into a single indicator state integer (0-7) using binary encoding, creating 8 possible indicator combinations

The RSI state and indicator state are stored together, defining one of 56 possible market condition cells in the matrix

2. Historical Data Accumulation

As each bar completes, the current state classification, closing price, and bar index are stored in rolling arrays maintained at the size specified by the lookback period

When the arrays reach capacity, the oldest data point is removed and the newest added, creating a sliding historical window

This continuous process builds a comprehensive database of past market conditions and their subsequent price movements

3. Forward Return Calculation and Statistics Update

On each bar, the indicator looks back through the stored historical data to find bars where sufficient forward bars exist to measure outcomes

For each historical occurrence, the price change from that bar to the bar N periods ahead (where N is the forward performance bars setting) is calculated as a percentage return

This percentage return is added to the cumulative return total for the specific matrix cell corresponding to that historical bar’s state classification

Occurrence counts are incremented, and wins are tallied for positive returns, building comprehensive statistics for each of the 56 cells

The Bayesian smoothing formula combines these raw statistics with prior assumptions (neutral 50% win rate) weighted by the smoothing strength parameter to produce estimated win rates that remain stable even with small samples

💡Note:

The Historical Matrix Analyzer is designed as a decision support tool, not a standalone trading system. Best results come from using it to validate discretionary trade ideas or filter systematic strategy signals. Always combine matrix insights with proper risk management, position sizing rules, and awareness of broader market context. The estimated win rate feature uses Bayesian statistics specifically to prevent false confidence from limited data, but no amount of smoothing can create reliable predictions from fundamentally insufficient sample sizes. Focus on high-confidence cells (green-colored confidence indicators) with occurrence counts well above your minimum threshold for the most actionable insights.

Relative Strength Index Remastered [CHE]Relative Strength Index Remastered — Enhanced RSI with robust divergence detection using price-based pivots and line-of-sight validation to reduce false signals compared to the standard RSI indicator.

Summary

RSI Remastered builds on the classic Relative Strength Index by adding a more reliable divergence detection system that relies on price pivots rather than RSI pivots alone, incorporating a line-of-sight check to ensure the RSI path between points remains clear. This approach filters out many false divergences that occur in the original RSI indicator due to its volatile pivot detection on the RSI line itself. Users benefit from clearer reversal and continuation signals, especially in noisy markets, with optional hidden divergence support for trend confirmation. The core RSI calculation and smoothing options remain familiar, but the divergence logic provides materially fewer alerts while maintaining sensitivity.

Motivation: Why this design?

The standard RSI indicator often generates misleading divergence signals because it detects pivots directly on the RSI values, which can fluctuate erratically in volatile conditions, leading to frequent false positives that confuse traders during ranging or choppy price action. RSI Remastered addresses this by shifting pivot detection to the underlying price highs and lows, which are more stable, and adding a validation step that confirms the RSI line does not cross the direct path between pivot points. This design targets the real problem of over-signaling in the original, promoting more actionable insights without altering the RSI's core momentum measurement.

What’s different vs. standard approaches?

- Reference baseline: The classical TradingView RSI indicator, which uses simple RSI-based pivot detection for divergences.

- Architecture differences:

- Pivot identification on price extremes (highs and lows) instead of RSI values, extracting RSI levels at those points for comparison.

- Addition of a line-of-sight validation that checks the RSI path bar by bar between pivots to prevent signals where the line is interrupted.

- Inclusion of hidden divergence types alongside regular ones, using the same robust framework.

- Configurable drawing of connecting lines between validated pivot RSI points for visual clarity.

- Practical effect: Charts show fewer but higher-quality divergence markers and lines, reducing clutter from the original's frequent RSI pivot triggers; this matters for avoiding whipsaws in intraday trading, where the standard version might flag dozens of invalid setups per session.

Key Comparison Aspects

Aspect: Title/Shorttitle

Original RSI: "Relative Strength Index" / "RSI"

Robust Variant: "Relative Strength Index Remastered " / "RSI RM"

Aspect: Max. Lines/Labels

Original RSI: No specification (Standard: 50/50)

Robust Variant: max_lines_count=200, max_labels_count=200 (for more lines/markers in divergences)

Aspect: RSI Calculation & Plots

Original RSI: Identical: RSI with RMA, Plots (line, bands, gradient fills)

Robust Variant: Identical: RSI with RMA, Plots (line, bands, gradient fills)

Aspect: Smoothing (MA)

Original RSI: Identical: Inputs for MA types (SMA, EMA etc.), Bollinger Bands optional

Robust Variant: Identical: Inputs for MA types (SMA, EMA etc.), Bollinger Bands optional

Aspect: Divergence Activation

Original RSI: input.bool(false, "Calculate Divergence") (disabled by default)

Robust Variant: input.bool(true, "Calculate Divergence") (enabled by default, with tooltip)

Aspect: Pivot Calculation

Original RSI: Pivots on RSI (ta.pivotlow/high on RSI values)

Robust Variant: Pivots on price (ta.pivotlow/high on low/high), RSI values then extracted

Aspect: Lookback Values

Original RSI: Fixed: lookbackLeft=5, lookbackRight=5

Robust Variant: Input: L=5 (Pivot Left), R=5 (Pivot Right), adjustable (min=1, max=50)

Aspect: Range Between Pivots

Original RSI: Fixed: rangeUpper=60, rangeLower=5 (via _inRange function)

Robust Variant: Input: rangeUpper=60 (Max Bars), rangeLower=5 (Min Bars), adjustable (min=1–6, max=100–300)

Aspect: Divergence Types

Original RSI: Only Regular Bullish/Bearish: - Bull: Price LL + RSI HL - Bear: Price HH + RSI LH

Robust Variant: Regular + Hidden (optional via showHidden=true): - Regular Bull: Price LL + RSI HL - Regular Bear: Price HH + RSI LH - Hidden Bull: Price HL + RSI LL - Hidden Bear: Price LH + RSI HH

Aspect: Validation

Original RSI: No additional check (only pivot + range check)

Robust Variant: Line-of-Sight Check: RSI line must not cross the connecting line between pivots (line_clear function with slope calculation and loop for each bar in between)

Aspect: Signals (Plots/Shapes)

Original RSI: - Plot of pivot points (if divergence) - Shapes: "Bull"/"Bear" at RSI value, offset=-5

Robust Variant: - No pivot plots, instead shapes at RSI , offset=-R (adjustable) - Shapes: "Bull"/"Bear" (Regular), "HBull"/"HBear" (Hidden) - Colors: Lime/Red (Regular), Teal/Orange (Hidden)

Aspect: Line Drawing

Original RSI: No lines

Robust Variant: Optional (showLines=true): Lines between RSI pivots (thick for regular, dashed/thin for hidden), extend=none

Aspect: Alerts

Original RSI: Only Regular Bullish/Bearish (with pivot lookback reference)

Robust Variant: Regular Bullish/Bearish + Hidden Bullish/Bearish (specific "at latest pivot low/high")

Aspect: Robustness

Original RSI: Simple, prone to false signals (RSI pivots can be volatile)

Robust Variant: Higher: Price pivots are more stable, line-of-sight filters "broken" divergences, hidden support for trend continuations

Aspect: Code Length/Structure

Original RSI: ~100 lines, simple if-blocks for bull/bear

Robust Variant: ~150 lines, extended helper functions (e.g., inRange, line_clear), var group for inputs

How it works (technical)

The indicator first computes the core RSI value based on recent price changes, separating upward and downward movements over the specified length and smoothing them to derive a momentum reading scaled between zero and one hundred. This value is then plotted in a separate pane with fixed upper and lower reference lines at seventy and thirty, along with optional gradient fills to highlight overbought and oversold zones.

For smoothing, a moving average type is applied to the RSI if enabled, with an option to add bands around it based on the variability of recent RSI values scaled by a multiplier. Divergence detection activates on confirmed price pivots: lows for bullish checks and highs for bearish. At each new pivot, the system retrieves the bar index and values (price and RSI) for the current and prior pivot, ensuring they fall within a configurable bar range to avoid unrelated points.

Comparisons then assess whether the price has made a lower low (or higher high) while the RSI at those points moves in the opposite direction—higher for bullish regular, lower for bearish regular. For hidden types, the directions reverse to capture trend strength. The line-of-sight check calculates the straight path between the two RSI points and verifies that the actual RSI values in between stay entirely above (for bullish) or below (for bearish) that path, breaking the signal if any bar violates it. Valid signals trigger shapes at the RSI level of the new pivot and optional lines connecting the points. Initialization uses built-in functions to track prior occurrences, with states persisting across bars for accurate historical comparisons. No higher timeframe data is used, so confirmation occurs after the right pivot bars close, minimizing live-bar repaints.

Parameter Guide

Length — Controls the period for measuring price momentum changes — Default: 14 — Trade-offs/Tips: Shorter values increase responsiveness but add noise and more false signals; longer smooths trends but delays entries in fast markets.

Source — Selects the price input for RSI calculation — Default: Close — Trade-offs/Tips: Use high or low for volatility focus, but close works best for most assets; mismatches can skew overbought/oversold reads.

Calculate Divergence — Enables the enhanced divergence logic — Default: True — Trade-offs/Tips: Disable for pure RSI view to save computation; essential for signal reliability over the standard method.

Type (Smoothing) — Chooses the moving average applied to RSI — Default: SMA — Trade-offs/Tips: None for raw RSI; EMA for quicker adaptation, but SMA reduces whipsaws; Bollinger Bands option adds volatility context at cost of added lines.

Length (Smoothing) — Period for the smoothing average — Default: 14 — Trade-offs/Tips: Match RSI length for consistency; shorter boosts signal speed but amplifies noise in the smoothed line.

BB StdDev — Multiplier for band width around smoothed RSI — Default: 2.0 — Trade-offs/Tips: Lower narrows bands for tighter signals, risking more touches; higher widens for fewer but stronger breakouts.

Pivot Left — Bars to the left for confirming price pivots — Default: 5 — Trade-offs/Tips: Increase for stricter pivots in noisy data, reducing signals; too high delays confirmation excessively.

Pivot Right — Bars to the right for confirming price pivots — Default: 5 — Trade-offs/Tips: Balances with left for symmetry; longer right ensures maturity but shifts signals backward.

Max Bars Between Pivots — Upper limit on distance for valid pivot pairs — Default: 60 — Trade-offs/Tips: Tighten for short-term trades to focus recent action; widen for swing setups but risks unrelated comparisons.

Min Bars Between Pivots — Lower limit to avoid clustered pivots — Default: 5 — Trade-offs/Tips: Raise to filter micro-moves; too low invites overlapping signals like the original RSI.

Detect Hidden — Includes trend-continuation hidden types — Default: True — Trade-offs/Tips: Enable for full trend analysis; disable simplifies to reversals only, akin to basic RSI.

Draw Lines — Shows connecting lines between valid pivots — Default: True — Trade-offs/Tips: Turn off for cleaner charts; helps visually confirm line-of-sight in backtests.

Reading & Interpretation

The main RSI line oscillates between zero and one hundred, crossing above fifty suggesting building momentum and below indicating weakness; touches near seventy or thirty flag potential extremes. The optional smoothed line and bands provide a filtered view—price above the upper band on the RSI pane hints at overextension. Divergence shapes appear as upward labels for bullish (lime for regular, teal for hidden) and downward for bearish (red regular, orange hidden) at the pivot's RSI level, signaling a mismatch only after validation. Connecting lines, if drawn, slope between points without RSI interference, their color matching the shape type; a dashed style denotes hidden. Fewer shapes overall compared to the standard RSI mean higher conviction, but always confirm with price structure.

Practical Workflows & Combinations

- Trend following: Enter longs on regular bullish shapes near support with higher highs in price; filter hidden bullish for pullback buys in uptrends, pairing with a rising smoothed RSI above fifty.

- Exits/Stops: Use bearish regular as reversal warnings to tighten stops; hidden bearish in downtrends confirms continuation—exit if lines show RSI crossing the path.

- Multi-asset/Multi-TF: Defaults suit forex and stocks on one-hour charts; for crypto volatility, widen pivot ranges to ten; scale min/max bars proportionally on daily for swings, avoiding the original's intraday spam.

Behavior, Constraints & Performance

Signals confirm only after the right pivot bars close, so live bars may show tentative pivots that vanish on close, unlike the standard RSI's immediate RSI-pivot triggers—plan for this delay in automation. No higher timeframe calls, so no security-related repaints. Resources include up to two hundred lines and labels for dense charts, with a loop in validation scanning up to three hundred bars between pivots, which is efficient but could slow on very long histories. Known limits: Slight lag at pivot confirmation in trending markets; volatile RSI might rarely miss fine path violations; not ideal for gap-heavy assets where pivots skip.

Sensible Defaults & Quick Tuning

Start with defaults for balanced momentum and divergence on most timeframes. For too many signals (like the original), raise pivot left/right to eight and min bars to ten to filter noise. If sluggish in trends, shorten RSI length to nine and enable EMA smoothing for faster adaptation. In high-volatility assets, widen max bars to one hundred but disable hidden to focus essentials. For clean reversal hunts, set smoothing to none and lines on.

What this indicator is—and isn’t

RSI Remastered serves as a refined momentum and divergence visualization tool, enhancing the standard RSI for better signal quality in technical analysis setups. It is not a standalone trading system, nor does it predict price moves—pair it with volume, structure breaks, and risk rules for decisions. Use alongside position sizing and broader context, not in isolation.

Disclaimer

The content provided, including all code and materials, is strictly for educational and informational purposes only. It is not intended as, and should not be interpreted as, financial advice, a recommendation to buy or sell any financial instrument, or an offer of any financial product or service. All strategies, tools, and examples discussed are provided for illustrative purposes to demonstrate coding techniques and the functionality of Pine Script within a trading context.

Any results from strategies or tools provided are hypothetical, and past performance is not indicative of future results. Trading and investing involve high risk, including the potential loss of principal, and may not be suitable for all individuals. Before making any trading decisions, please consult with a qualified financial professional to understand the risks involved.

By using this script, you acknowledge and agree that any trading decisions are made solely at your discretion and risk.

Do not use this indicator on Heikin-Ashi, Renko, Kagi, Point-and-Figure, or Range charts, as these chart types can produce unrealistic results for signal markers and alerts.

Best regards and happy trading

Chervolino

Volume Sampled Supertrend [BackQuant]Volume Sampled Supertrend

A Supertrend that runs on a volume sampled price series instead of fixed time. New synthetic bars are only created after sufficient traded activity, which filters out low participation noise and makes the trend much easier to read and model.

Original Script Link

This indicator is built on top of my volume sampling engine. See the base implementation here:

Why Volume Sampling

Traditional charts print a bar every N minutes regardless of how active the tape is. During quiet periods you accumulate many small, low information bars that add noise and whipsaws to downstream signals.

Volume sampling replaces the clock with participation. A new synthetic bar is created only when a pre-set amount of volume accumulates (or, in Dollar Bars mode, when pricevolume reaches a dollar threshold). The result is a non-uniform time series that stretches in busy regimes and compresses in quiet regimes. This naturally:

filters dead time by skipping low volume chop;

standardizes the information content per bar, improving comparability across regimes;

stabilizes volatility estimates used inside banded indicators;

gives trend and breakout logic cleaner state transitions with fewer micro flips.

What this tool does

It builds a synthetic OHLCV stream from volume based buckets and then applies a Supertrend to that synthetic price. You are effectively running Supertrend on a participation clock rather than a wall clock.

Core Features

Sampling Engine - Choose Volume buckets or Dollar Bars . Thresholds can be dynamic from a rolling mean or median, or fixed by the user.

Synthetic Candles - Plots the volume sampled OHLC candles so you can visually compare against regular time candles.

Supertrend on Synthetic Price - ATR bands and direction are computed on the sampled series, not on time bars.

Adaptive Coloring - Candle colors can reflect side, intensity by volume, or a neutral scheme.

Research Panels - Table shows total samples, current bucket fill, threshold, bars-per-sample, and synthetic return stats.

Alerts - Long and Short triggers on Supertrend direction flips for the synthetic series.

How it works

Sampling

Pick Sampling Method = Volume or Dollar Bars.

Set the dynamic threshold via Rolling Lookback and Filter (Mean or Median), or enable Use Fixed and type a constant.

The script accumulates volume (or pricevolume) each time bar. When the bucket reaches the threshold, it finalizes one or more synthetic candles and resets accumulation.

Each synthetic candle stores its own OHLCV and is appended to the synthetic series used for all downstream logic.

Supertrend on the sampled stream

Choose Supertrend Source (Open, High, Low, Close, HLC3, HL2, OHLC4, HLCC4) derived from the synthetic candle.

Compute ATR over the synthetic series with ATR Period , then form upperBand = src + factorATR and lowerBand = src - factorATR .

Apply classic trailing band and direction rules to produce Supertrend and trend state.

Because bars only come when there is sufficient participation, band touches and flips tend to align with meaningful pushes, not idle prints.

Reading the display

Synthetic Volume Bars - The non-uniform candles that represent equal information buckets. Expect more candles during active sessions and fewer during lulls.

Volume Sampled Supertrend - The main line. Green when Trend is 1, red when Trend is -1.

Markers - Small dots appear when a new synthetic sample is created, useful for aligning activity cycles.

Time Bars Overlay (optional) - Plot regular time candles to compare how the synthetic stream compresses quiet chop.

Settings you will use most

Data Settings

Sampling Method - Volume or Dollar Bars.

Rolling Lookback and Filter - Controls the dynamic threshold. Median is robust to outliers, Mean is smoother.

Use Fixed and Fixed Threshold - Force a constant bucket size for consistent sampling across regimes.

Max Stored Samples - Ring buffer limit for performance.

Indicator Settings

SMA over last N samples - A moving average computed on the synthetic close series. Can be hidden for a cleaner layout.

Supertrend Source - Price field from the synthetic candle.

ATR Period and Factor - Standard Supertrend controls applied on the synthetic series.

Visuals and UI

Show Synthetic Bars - Turn synthetic candles on or off.

Candle Color Mode - Green/Red, Volume Intensity, Neutral, or Adaptive.

Mark new samples - Puts a dot when a bucket closes.

Show Time Bars - Overlay regular candles for comparison.

Paint candles according to Trend - Colors chart candles using current synthetic Supertrend direction.

Line Width , Colors , and Stats Table toggles.

Some workflow notes:

Trend Following

Set Sampling Method = Volume, Filter = Median, and a reasonable Rolling Lookback so busy regimes produce more samples.

Trade in the direction of the Volume Sampled Supertrend. Because flips require real participation, you tend to avoid micro whipsaws seen on time bars.

Use the synthetic SMA as a bias rail and trailing reference for partials or re-entries.

Breakout and Continuation

Watch for rapid clustering of new sample markers and a clean flip of the synthetic Supertrend.

The compression of quiet time and expansion in busy bursts often makes breakouts more legible than on uniform time charts.

Mean Reversion

In instruments that oscillate, faded moves against the synthetic Supertrend are easier to time when the bucket cadence slows and Supertrend flattens.

Combine with the synthetic SMA and return statistics in the table for sizing and expectation setting.

Stats table (top right)

Method and Total Samples - Sampling regime and current synthetic history length.

Current Vol or Dollar and Threshold - Live bucket fill versus the trigger.

Bars in Bucket and Avg Bars per Sample - How much time data each synthetic bar tends to compress.

Avg Return and Return StdDev - Simple research metrics over synthetic close-to-close changes.

Why this reduces noise

Time based bars treat a 5 minute print with 1 percent of average participation the same as one with 300 percent. Volume sampling equalizes bar information content. By advancing the bar only when sufficient activity occurs, you skip low quality intervals that add variance but little signal. For banded systems like Supertrend, this often means fewer false flips and cleaner runs.

Notes and tips

Use Dollar Bars on assets where nominal price varies widely over time or across symbols.

Median filter can resist single burst outliers when setting dynamic thresholds.

If you need a stable research baseline, set Use Fixed and keep the threshold constant across tests.

Enable Show Time Bars occasionally to sanity check what the synthetic stream is compressing or stretching.

Link again for reference

Original Volume Based Sampling engine:

Bottom line

When you let participation set the clock, your Supertrend reacts to meaningful flow instead of idle prints. The result is a cleaner state machine, fewer micro whipsaws, and a trend read that respects when the market is actually trading.

Magic Volume - Projected [MW]Magic Volume – Projected

This lower-pane volume tool estimates the full-bar volume before the bar closes by measuring the current bar’s elapsed time and the rate of incoming volume. It then contrasts that “expected volume” against typical activity and recent momentum to spotlight potential burst conditions (breakout/acceleration), color-codes the live volume stream, and annotates when the projected surge is likely bullish or bearish based on bar structure and recent highs/lows.

Settings

Projected / Expected Volume

Moving Average: EMA length used for volume baseline comparisons. (Default: 14)

Minimum Volume: Hard floor the bar’s raw volume must exceed to qualify as notable. (Default: 10,000)

Consecutive Volume Above 14 EMA: Count required for “sustained” high-volume context. (Default: 3)

Stochastic Volume Burst

Stochastic Length: Window for the Stochastic calculation on volume. (Default: 8)

Smoothing: Smoothing applied to Stochastic volume and its signal. (Default: 3)

Stochastic Volume Breakout Threshold: Level above which Stochastic volume is considered a breakout. (Default: 20)

Volume Bar Increase Amount: Multiplier the current bar’s volume must exceed vs. prior bar to be considered a “burst.” (Default: 1.618)

Plotted Items

Expected Volume (columns): Magenta columns projecting the full-bar volume from intrabar rate. Turns lime when a high expected-volume condition aligns with bullish bar structure; turns red under analogous bearish conditions.

Actual Volume (columns): Live volume columns, color-coded by state:

• Blue = baseline;

• Orange = “burst” (volume rising fast above prior × factor and above baseline);

• Yellow = “burst at breakout” (burst + Stochastic volume breakout);

• Light Blue = Stochastic breakout only.

Volume EMA (line): Yellow EMA for baseline comparison (default 14).

Calculations

Compute elapsed time in the current bar (ms → seconds) and convert the current bar’s accumulated volume into a rate (volume per second).

Project full-bar Expected Volume = (volume so far / seconds elapsed) × bar-seconds.

Compute Volume EMA (default 14) for baseline; derive Stochastic(volume, length) and smoothed signal for momentum.

Define “Burst” conditions:

• Volume > prior volume × Volume Bar Increase Amount;

• Volume > Minimum Volume;

• Volume > Volume EMA;

• Stochastic(volume) rising and/or above threshold.

Classify “Burst at Breakout” when Burst aligns with Stochastic crossover above the Breakout Threshold.

Classify Bullish/Bearish Expected Volume: if Expected Volume is ≥ 1.618 × prior bar volume and prior volume > Volume EMA, then:

• Bullish if bar is green with a rising low;

• Bearish if bar is red with a falling high.

Color-map actual volume columns by state; overlay Expected Volume columns (magenta) and paint conditional overlays (lime/red) when directional context is detected.

How to Use

Spot the Surge Early

When Expected Volume spikes well above typical (and especially above ~1.618× the prior bar) before the bar closes, it often precedes a volatile move. Use this to prepare entries with tight, structure-based risk (e.g., just beyond the current bar’s wick) and asymmetric targets.

Confirm with Momentum

Yellow/orange volume columns indicate burst/breakout behavior in the live tape. When this aligns with a lime (bullish) or red (bearish) Expected Volume column, the probability of follow-through improves—particularly if aligned with prevailing trend or key levels.

Context Matters

Combine with your preferred S/R or structure tools (e.g., order blocks, channels, VWAP) to avoid chasing into obvious supply/demand. The projected surge can mark both continuations and sharp reversals depending on location and broader context.

Alerts

High Expected Volume – Bullish: When projected volume surges and the price action meets bullish conditions (green body with rising low).

High Expected Volume – Bearish: When projected volume surges and the price action meets bearish conditions (red body with falling high).

Other Usage Notes and Limitations

Projected volume depends on intrabar pace; abrupt pauses/flushes can change the projection quickly, especially on very small timeframes.

Minimum Volume and EMA baselines help filter thin markets; adjust upward on illiquid symbols to reduce noise.

A rising projection does not pick direction on its own—directional coloring (lime/red) requires price-action confirmation; otherwise treat magenta projections as “heads-up” only.

As with any single indicator, use within a broader plan (risk management, structure, confluence) to mitigate false positives and improve selectivity.

Inputs (Quick Reference)

Moving Average (int, default 14)

Stochastic Length (int, default 8)

Smoothing (int, default 3)

Stochastic Volume Breakout Threshold (int, default 20)

Volume Bar Increase Amount (float, default 1.618)

Minimum Volume (int, default 10,000)

Consecutive Volume Above 14 EMA (int, default 3)

US Opening 5-Minute Candle HighlighterUS Opening 5-Minute Candle Highlighter — True RVOL (Two-Tier + Label)

What it does (in plain English)

This indicator finds the first 5-minute bar of the US cash session (09:30–09:35 ET) and highlights it when the candle has the specific “strong open” look you want:

Opens near the low of its own range, and

Closes near the high of its own range, and

Has a decisive real body (not a wick-y doji), and

(Optionally) is a green candle, and

Meets a TRUE opening-bar RVOL filter (compares today’s 09:30–09:35 volume only to prior sessions’ 09:30–09:35 volumes).

You get two visual intensities based on opening RVOL:

Tier-1 (≥ threshold 1, default 1.0×) → light green highlight + lime arrow

Tier-2 (≥ threshold 2, default 1.5×) → darker green highlight + green arrow

An RVOL label (e.g., RVOL 1.84x) can be shown above or below the opening bar.

Designed for 5-minute charts. On other timeframes the “opening bar” will be the bar that starts at 09:30 on that timeframe (e.g., 15-minute 09:30–09:45). For best results keep the chart on 5m.

How the pattern is defined

For the opening 5-minute bar, we compute:

Range = high − low

Body = |close − open|

Then we measure where the open and close sit within the bar’s own range on a 0→1 scale:

0 means exactly at the low

1 means exactly at the high

Using two quantiles:

Open ≤ position in range (0–1) (default 0.20)

Example: 0.20 means “open must be in the lowest 20% of the bar’s range.”

Close ≥ position in range (0–1) (default 0.80)

Example: 0.80 means “close must be in the top 20% of the bar’s range.”

This keeps the logic range-normalized so it adapts across different tickers and vol regimes (you’re not using fixed cents or % of price).

Body ≥ fraction of range (0–1) (default 0.55)

Requires the real body to be at least that fraction of the total range.

0.55 = body fills ≥ 55% of the candle.

Purpose: filter out indecisive, wick-heavy bars.