ES-VIX Daily Price BandsES-VIX Daily Price Bands

This indicator plots dynamic intraday price bands for ES futures based on real-time volatility levels measured by the VIX (CBOE Volatility Index). The bands evolve throughout the trading day, providing volatility-adjusted price targets.

Formulas:

Upper Band = Daily Low + (ES Price × VIX ÷ √252 ÷ 100)

Lower Band = Daily High - (ES Price × VIX ÷ √252 ÷ 100)

The calculation uses the square root of 252 (trading days per year) to convert annualized VIX volatility into an expected daily move, then scales it as a percentage adjustment from the current day's extremes.

Features:

Real-time band calculation that updates throughout the trading session

Upper band (green) extends from the current day's low

Lower band (red) contracts from the current day's high

Shaded zone between bands for visual clarity

Information table displaying:

Current ES price and VIX level

Running daily high and low

Current upper and lower band values

חפש סקריפטים עבור "daily"

ES-VIX Expected Daily MoveThis indicator calculates the expected daily price movement for ES futures based on current volatility levels as measured by the VIX (CBOE Volatility Index).

Formula:

Expected Daily Move = (ES Price × VIX Price) / √252 / 100

The calculation converts the annualized VIX volatility into an expected daily move by dividing by the square root of 252 (the approximate number of trading days per year).

Features:

Real-time calculation using current ES futures price and VIX level

Histogram visualization in a separate pane for easy trend analysis

Information table displaying:

Current ES futures price

Current VIX level

Expected daily move in points

Expected daily move as a percentage

ORB + Fair Value Gaps (FVG/iFVG) Suite with Daily 50% MidlineA complete smart-money–focused price-action toolkit combining the New York Open Range Breakout (ORB), ICT-style Fair Value Gaps, Inverted FVGs, and a dynamic Daily 50% Midline.

Designed for traders who want a clean, fast, and highly visual way to track liquidity, imbalances, and intraday directional bias.

📌 Key Features

1. NY Session ORB (09:30–09:45 New York Time)

Automatically plots:

ORB High

ORB Low

Labels for ORB high/low

Optional 5-minute chart restriction

Lines extend forward for easy reference

Used to identify breakout conditions, liquidity sweeps, and directional bias into the morning session.

📌 2. ICT-Style Fair Value Gaps (FVGs)

Full automated detection of bullish & bearish FVGs based on the classic 3-candle displacement structure:

Bullish FVG: high < low

Bearish FVG: low > high

Each FVG is drawn as a box with:

Custom colour

Custom border style (solid, dashed, dotted)

Automatic extension to the right until filled

Optional size text showing the gap in points (font size/colour adjustable)

Adjustable max lookback for performance

📌 3. Inverted FVGs (iFVGs)

Once price fully fills an FVG, it automatically becomes an iFVG, shown with:

Custom iFVG colour

Custom border style

Extension to the right

Once price trades through the zone from the opposite side, the iFVG is considered “consumed” and:

It stops extending

And optionally auto-deletes based on user settings

This makes it easy to track meaningful imbalances that turn into liquidity pockets.

📌 4. “Show Only After ORB” Filter

Optionally hide all FVGs/iFVGs formed before the ORB completes.

This is especially useful for intraday strategies focused on NY session structure only.

📌 5. Daily 50% Midline (OHLC Midpoint)

A dynamic, always-updating midpoint of the current daily candle:

Mid = (Daily High + Daily Low) / 2

Features:

Custom colour

Dashed styling

Extends left and right as a horizontal ray

Updates live as the daily candle forms

Great for bias filters, mean reversion, and daily liquidity zones.

📌 6. Performance-Optimized (Fast!)

Built with:

Fully configurable max lookback

Memory-efficient arrays

Auto-cleaning of old FVG/iFVG objects

Lightweight daily midline recalculation

This allows extremely fast rendering even on 1-minute charts.

📌 7. Alerts

Includes a clean alert condition:

Price returned to a Fair Value Gap

Works for both bullish and bearish FVG revisits.

🎯 Who This Indicator Is For

This tool is ideal for traders who use:

ICT / SMC concepts

Liquidity-based trading

ORB strategies

Imbalance-driven price action

Intraday or NY session-focused setups

Futures, crypto, forex, and equities

🎁 Summary

This indicator gives you:

A clean ORB framework

Automatic, dynamic FVG and iFVG analysis

Real-time daily candle context

Customizable visuals

Powerful session filtering

Efficient performance

All in one clean, intuitive package built for real-time decision making.

SVE Daily ATR + SDTR Context BandsSVE Daily ATR + SDTR Context Bands is a free companion overlay from The Volatility Engine™ ecosystem.

It plots daily ATR-based expansion levels and a Standardized Deviation Threshold Range (SDTR) to give traders a clean, quantitative view of where intraday price sits relative to typical daily movement and volatility extremes.

This module is designed as an SVE-compatible context layer—using discrete, RTH-aligned daily zones, expected-move bands, and a standardized volatility shell—so traders can build situational awareness even without the full SPX Volatility Engine™ (SVE).

It does not generate trade signals.

Its sole purpose is to provide a clear volatility framework you can combine with your own structure, Fibonacci, or signal logic (including SVE, if you use it).

🔍 What It Shows

* Daily ATR Bands (expHigh / expLow)

- Expected high/low based on smoothed daily ATR

- Updates at the RTH open

* Daily SDTR Bands (expHighSDTR / expLowSDTR)

- Standard deviation threshold range for volatility extremes

- Helps identify overextended conditions

Discrete RTH-aligned Zones

- Bands reset cleanly at each RTH session

No continuous carry-over from prior days

Daily ATR & SDTR stats label

Quick-reference box showing current ATR and SDTR values

🎯 Purpose

This tool helps traders:

- Gauge intraday context relative to expected daily movement

- Assess volatility state (quiet, normal, expanded, extreme)

- Identify likely exhaustion or expansion zones

- Frame intraday price action inside daily volatility rails

- Support decision-making with objective context rather than emotion

It complements any strategy and works on any intraday timeframe.

⚙️ Inputs

- ATR Lookback (default: 20 days)

- RTH Session Times

- SDTR Lookback

- Show/Hide Daily Stats Label

🧩 Part of the SVE Ecosystem

This module is part of the broader SPX Volatility Engine™ framework.

The full SVE system includes:

- Composite signal scoring

- Volatility compression logic

- Histogram slope and momentum analysis

- Internals (VIX / VVIX / TICK)

- Structural zone awareness

- Real-time bias selection

- High-clarity decision support

⚠️ Disclaimer

This tool is provided for educational and informational purposes only.

No performance claims are made or implied.

Not investment advice.

ATR Daily (Classic vs Robust, NY-Fix, Spike Control)📘 What this indicator does

This tool provides an advanced view of daily market volatility by comparing two versions of the Average True Range (ATR):

• Classic ATR — standard Wilder smoothing

• Robust ATR — uses median-based filtering and spike-control logic to reduce distortion from abnormal candles

Both values are calculated using daily data aligned to the New York trading session, so volatility resets at the same moment each institutional trading day begins. This keeps readings consistent across crypto, forex and stocks, even on intraday charts.

⚙️ How it works (in simple terms)

The script evaluates each True Range (TR) value relative to a median-based threshold:

• Abnormally large ranges are either clamped to a limit or excluded from updating ATR

• A hard cap prevents single spikes from inflating the entire indicator

• The result is a smoother and more realistic representation of daily volatility

This allows ATR to reflect typical market behaviour instead of rare one-off events.

📊 What appears on the chart

• Two daily ATR lines (Classic and Robust)

• Histogram showing the percentage of daily range already completed

• Red bars when price exceeds 100% of daily ATR

• A data table with volatility metrics

• Background highlights on days with extreme values

💡 How traders can use it

• Identify when a market has already completed most of its typical daily move

• Compare Classic vs Robust ATR to spot news-driven distortion

• Use Robust ATR for more stable stop-loss and take-profit logic

• Track volatility expansion or contraction across sessions

⚙️ Key settings

Setting Purpose

ATR period Standard smoothing length (default 14)

Robust mode Clamp, Freeze or Off

MAD multiplier Sensitivity to outliers

Cap × median(TR) Maximum allowed spike size

Base for passed ATR Which ATR is used to measure daily %

Freeze weekends Keeps ATR unchanged on Sat/Sun

🧩 Unique concept

Unlike typical ATR indicators, this one combines robust statistics (median + MAD) with session-based fixation. ATR values update only once per New York session, creating stable volatility measurements that match institutional timing.

🔒 Source code

The script is published with protected source code to preserve its statistical structure and prevent unauthorized modification.

🧭 Summary

ATR Daily (Classic vs Robust, NY-Fix) provides a clearer and more reliable view of daily volatility.

It helps determine whether the market is still in the early phase of its daily range or already exhausted.

Vwap Daily By SamsungTitle

Daily VWAP with Historical Lookback (Logic Fix)

Description

This script calculates and plots the daily Volume-Weighted Average Price (VWAP), an essential tool for intraday traders.

What makes this indicator special is its robust plotting logic. Unlike many simple VWAP scripts that struggle to show data for previous days, this version includes a crucial fix that allows you to reliably display historical VWAP lines for as many days back as you need. This allows for more comprehensive backtesting and analysis of how price has interacted with the VWAP on previous trading days.

This is an indispensable tool for traders who use VWAP as a dynamic level of support/resistance, a benchmark for trade execution quality, or a gauge of the day's trend.

Key Features

Historical VWAP Display: Easily plot VWAP for multiple past days on your chart. Simply set the number of lookback days in the settings.

Accurate Daily Calculation: The VWAP calculation correctly resets at the beginning of each new trading session (00:00 server time).

Fully Customizable: You have full control over the appearance of the VWAP line, including its color, width, and style (Solid or Stepped).

Robust Plotting Engine: This script solves the common Pine Script issue where conditionally plotted historical lines fail to render. It works reliably on all intraday timeframes.

Built-in Debug Mode: For advanced users or those curious about the inner workings, a comprehensive debug mode can be enabled to display raw VWAP values, cumulative volume, and timeframe warnings.

How to Use

Add the "Daily VWAP with Historical Lookback" indicator to your chart.

IMPORTANT: Make sure you are on an intraday timeframe (e.g., 1H, 30M, 15M, 5M, 1M). This indicator is designed for intraday analysis and will display a warning if used on a daily or higher timeframe.

Open the indicator's settings.

In the "VWAP Settings" tab, adjust the "Lookback Days to Display" to set how many previous days of VWAP you want to see. (e.g., 0 for today only, 1 for today and yesterday, 10 for the last 10 days).

Customize the line's appearance in the "Line Style" tab.

The "Logic Fix" Explained (For Developers)

A common challenge in Pine Script is conditionally plotting data for historical bars. Many scripts attempt this by dynamically changing the plot color to na (transparent) for bars that shouldn't be displayed. This method is often unreliable and can result in the entire plot failing to render.

This script employs a more robust and standard approach: manipulating the data series itself.

The Problem: plot(vwap, color = shouldPlot ? color.red : na) can be buggy.

The Solution: plot(shouldPlot ? vwap : na, color = color.red) is reliable.

Instead of changing the color, we create a new data series (plotVwap). This series contains the vwapValue only on the bars that meet our date criteria. On all other bars, its value is na (Not a Number). The plot() function is designed to handle na values by simply "lifting the pen," creating a clean break in the line. This ensures that the VWAP is drawn only for the selected days, with 100% reliability across all historical data.

Settings Explained

Lookback Days to Display: Sets the number of past days (from the last visible bar) for which to display the VWAP.

Line Color, Width, and Style: Standard cosmetic settings for the VWAP line.

Enable Debug Mode (Master Switch): Toggles all debugging features on or off. It is enabled by default to help new users.

Display Debug: Cumulative Volume: When enabled, it shows the daily cumulative volume in a gray area on a separate pane.

Display Debug: Raw VWAP Value: When enabled, it plots the raw, unfiltered VWAP calculation for all days on the chart, helping to verify the core logic.

This script is provided for educational and informational purposes. Trading involves significant risk. Always conduct your own research and analysis before making any trading decisions.

If you find this script useful, a 'Like' is always appreciated! Happy trading

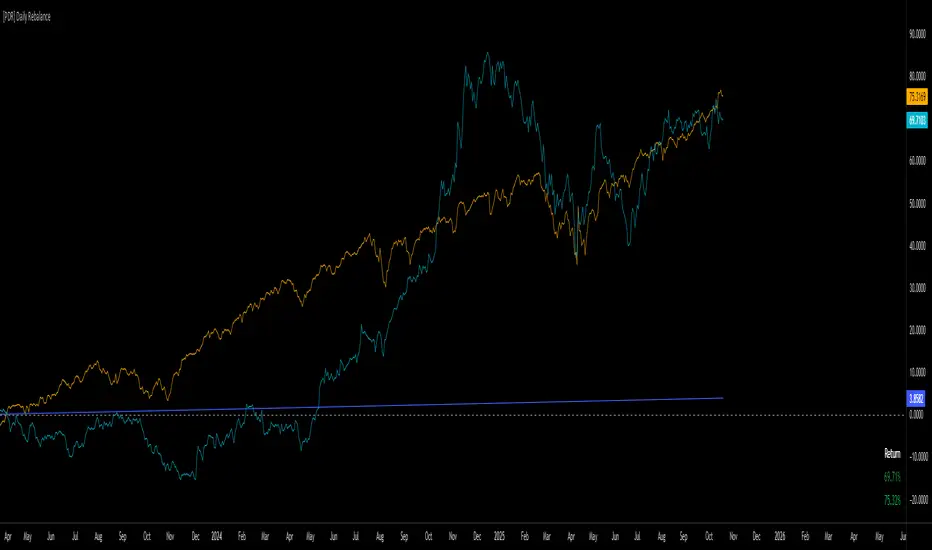

[PDR] Daily Rebalance█ OVERVIEW

This indicator is a powerful portfolio backtesting tool designed to simulate the performance of a static-weight, daily rebalancing strategy. It allows you to define a portfolio of up to 10 assets, set their target weights, and track its cumulative return against a user-defined benchmark and a risk-free rate.

The core of the script is its daily rebalancing logic, which calculates and logs every trade needed to bring the portfolio back to its target allocations at the close of each day. This provides a transparent and detailed view of how a static portfolio would have performed historically, including the impact of trading costs.

█ KEY FEATURES

Daily Rebalancing: Simulates a portfolio that is rebalanced at the close of every day to maintain target asset allocations.

Customizable Portfolio: Configure up to 10 different assets with specific weights. If all weights are left at 0, the script automatically creates an equal-weight portfolio from the selected assets.

Performance Comparison: Plots the portfolio's equity curve against a user-defined benchmark (e.g., SET:SET50 ) and a risk-free return, allowing for easy relative performance analysis.

Realistic Simulation: Accounts for trading costs like broker commission and minimum lot sizes for more accurate and grounded backtesting results.

Detailed Performance Metrics: An on-chart table displays real-time statistics, including Current Drawdown, Max Drawdown, and Total Return for both your portfolio and the benchmark.

Trade-by-Trade Logs: For full transparency, every rebalancing trade (BUY/SELL), including shares, price, notional value, and fees, is logged in the Pine Logs panel.

█ HOW TO USE

**Apply to a Daily Chart:** This script is designed to work exclusively on the daily ( 1D ) timeframe. Applying it to any other timeframe will result in a runtime error.

**Configure Settings:** Open the indicator's settings. Set your `Initial Capital`, `Start Time`, and the `Benchmark` symbol you wish to compare against.

**Define Your Assets:** In the 'Assets' group, check the box to enable each asset you want to include, select the symbol, and define its target `Weight (%)`.

**Set Trading Costs:** Adjust the `Broker Commission (%)` and `Minimal Buyable Lot` to match your expected trading conditions.

**Analyze the Results:** The performance curves are plotted in the indicator pane below your main chart. The key metrics table is displayed on the bottom-right of your chart.

**View Rebalancing Trades:** This is a crucial step for understanding the simulation. To see the detailed daily trades, you **must** open the **Pine Logs**. You can find this panel at the bottom of your TradingView window, next to the "Pine Editor" and "Strategy Tester" tabs. The logs provide a complete breakdown of every rebalancing action.

█ DISCLAIMER

This is a backtesting and simulation tool, not a trading signal generator. Its purpose is for research and performance analysis. Past performance is not indicative of future results. Always conduct your own research before making any investment decisions.

ATR DAILY PROGRESSION)Indicator: ATR Daily Progression — Final Compact Edition

1. Indicator Objective

The ATR Daily Progression indicator measures the progression of intraday volatility as a percentage of the daily Average True Range (ATR).

It provides a quick visual overview of whether the market has reached or exceeded its average daily range of movement.

This helps traders avoid entering low-probability continuation trades once the day’s ATR is already completed.

2. Visual Presentation

Horizontal bar ranging from 0% to 150% of the ATR.

Green color up to 100%, then red beyond that point.

Main ticks: 0, 25, 50, 75, 90, 100, and 150%.

Full-height white vertical lines at 0%, 100%, and 150%.

A floating badge displaying the current ATR completion percentage, always visible.

Compact Height mode enabled by default for optimal visual integration.

3. Key Features

Function Description

Precise alignment The transition from green to red occurs exactly after the 100% tick.

Audio & visual alerts Triggered at 75%, 90%, 100%, and 150%.

Session flash effects The filled bar blinks when the ATR is reached (100%) or exceeded (150%).

Dynamic badge Displays the current ATR %, green before 100%, red after.

Compact layout Three-line table format for better chart integration.

4. Recommended Settings

ATR Length (Daily): 14

Bar width (steps): 32–40 (depending on chart size)

Always green below 100%: enabled

Show floating % badge: enabled

Compact Height: enabled by default

Flash at 75% and 90%: enabled

Flash at 100% and 150%: enabled

5. Strategic Use

The ATR Done Today is a visual discipline tool designed to help traders:

Identify when the market has likely completed its daily move.

Avoid late-session counter-trend trades.

Visualize volatility compression or expansion.

Determine optimal times to take profits or pause trading.

Dynamic Levels This indicator plots key price levels (Open, High, Low, Mid, Close) from multiple higher timeframes (Monday, Daily, Weekly, Monthly, Yearly).

It allows you to track how price interacts with important reference levels without switching timeframes.

🔑 Features

✅ Monday levels (MO, MH, MM)

By default: shows the last completed Monday (fixed values).

Option: “live mode” to update Monday High/Low/Mid while Monday’s candle is forming.

✅ Daily levels (DO, DH, DL, DM, DC)

Live: Daily High/Low/Mid update dynamically while today’s candle is forming.

Previous Daily Close (DC) is always fixed.

✅ Weekly levels (WO, WH, WL, WM)

Live: Weekly High/Low/Mid update dynamically while this week’s candle is forming.

Weekly Open is fixed.

✅ Monthly levels (MO(n), MH(n-1), ML(n-1), MM(n-1), MC(n-1))

Shows last completed month’s values (constant, never changing).

Current Monthly Open is also shown (naturally fixed).

✅ Yearly levels (YO(n), YH(n-1), YL(n-1), YM(n-1), YC(n-1))

Shows last completed year’s values (constant, never changing).

Current Yearly Open is also shown (naturally fixed).

🎨 Customization

Toggle each level (on/off) in indicator settings.

Individual color settings for Monday, Daily, Weekly, Monthly, and Yearly.

Adjustable line width and transparency.

Optional short labels (MO, DO, WM, etc.) displayed on the right side of the chart.

🔄 Dynamic Logic

Daily and Weekly → update dynamically while their candle is forming.

Monday, Monthly, and Yearly → use fixed values from the last completed bar (do not “breathe”).

📌 Use cases

Quickly see where price stands relative to previous close, current open, or mid-levels.

Use Monday Open/High/Mid as strong intraday references.

Use Monthly/Yearly levels as long-term support/resistance zones.

Key Levels: Daily, Weekly, Monthly [BackQuant]Key Levels: Daily, Weekly, Monthly

Map the market’s “memory” in one glance—yesterday’s range, this week’s chosen day high/low, and D/W/M opens—then auto-clean levels once they break.

What it does

This tool plots three families of high-signal reference lines and keeps them tidy as price evolves:

Chosen Day High/Low (per week) — Pick a weekday (e.g., Monday). For each past week, the script records that day’s session high and low and projects them forward for a configurable number of bars. These act like “memory levels” that price often revisits.

Daily / Weekly / Monthly Opens — Plots the opening price of each new day, week, and month with separate styling. These opens frequently behave like magnets/flip lines intraday and anchors for regime on higher timeframes.

Auto-pruning — When price breaks a stored level, the script can automatically remove it to reduce clutter and refocus you on still-active lines. See: (broken levels removed).

Why these levels matter

Liquidity pockets — Prior day’s high/low and the daily open concentrate stops and pending orders. Mapping them quickly reveals likely sweep or fade zones. Example: previous day highs + daily open highlighting liquidity:

Context & regime — Monthly opens frame macro bias; trading above a rising cluster of monthly opens vs. below gives a clean top-down read. Example: monthly-only “macro outlook” view:

Cleaner charts — Auto-remove broken lines so you focus on what still matters right now.

What it plots (at a glance)

Past Chosen Day High/Low for up to N prior weeks (your choice), extended right.

Current Daily Open , Weekly Open , and Monthly Open , each with its own color, label, and forward extension.

Optional short labels (e.g., “Mon High”) or full labels (with week/month info).

How breaks are detected & cleaned

You control both the evidence and the timing of a “break”:

Break uses — Choose Close (more conservative) or Wick (more sensitive).

Inclusive? — If enabled, equality counts (≥ high or ≤ low). If disabled, you need a strict cross.

Allow intraday breaks? — If on, a level can break during the tracked day; if off, the script only counts breaks after the session completes.

Remove Broken Levels — When a break is confirmed, the line/label is deleted automatically. (See the demo: )

Quick start

Pick a Day of Week to Track (e.g., Monday).

Set how many weeks back to show (e.g., 8–10).

Choose how far to extend each family (bars to the right for chosen-day H/L and D/W/M opens).

Decide if a break uses Close or Wick , and whether equality counts.

Toggle Remove Broken Levels to keep the chart clean automatically.

Tips by use-case

Intraday bias — Watch the Daily Open as a magnet/flip. If price gaps above and holds, pullbacks to the daily open often decide direction. Pair with last day’s high/low for sweep→reversal or true breakout cues. See:

Weekly structure — Track the week’s chosen day (e.g., Monday) high/low across prior weeks. If price stalls near a cluster of old “Monday Highs,” look for sweep/reject patterns or continuation on reclaim.

Macro regime — Hide daily/weekly lines and keep only Monthly Opens to read bigger cycles at a glance (BTC/crypto especially). Example:

Customization

Use wicks or bodies for highs/lows (wicks capture extremes; bodies are stricter).

Line style & thickness — solid/dashed/dotted, width 1–5, plus global transparency.

Labels — Abbreviated (“Mon High”, “D Open”) or full (month/week/day info).

Color scheme — Separate colors for highs, lows, and each of D/W/M opens.

Capacity controls — Set how many daily/weekly/monthly opens and how many weeks of chosen-day H/L to keep visible.

What’s under the hood

On your selected weekday, the script records that session’s true high and true low (using wicks or body-based extremes—your choice), then projects a horizontal line forward for the next bars.

At each new day/week/month , it records the opening price and projects that line forward as well.

Each bar, the script checks your “break” rules; once broken, lines/labels are removed if auto-cleaning is on.

Everything updates in real time; past levels don’t repaint after the session finishes.

Recommended presets

Day trading — Weeks back: 6–10; extend D/W opens: 50–100 bars; Break uses: Close ; Inclusive: off; Auto-remove: on.

Swing — Fewer daily opens, more weekly opens (2–6), and 8–12 weeks of chosen-day H/L.

Macro — Show only Monthly Opens (1–6 months), dashed style, thicker lines for clarity.

Reading the examples

Broken lines disappear — decluttering in action:

Macro outlook — monthly opens as cycle rails:

Liquidity map — previous day highs + daily open:

Final note

These are not “signals”—they’re reference points that many participants watch. By standardising how you draw them and automatically clearing the ones that no longer matter, you turn a noisy chart into a focused map: where liquidity likely sits, where price memory lives, and which lines are still in play.

Spiderlines BTCUSD - daily/weekly📘 Documentation – Daily and Weekly Spider Lines for Bitcoin

🔹 Purpose of the Script

This script draws dynamic “Spider Lines” in the Bitcoin chart.

The lines connect certain historical candles with a reference candle and extend to the right.

These act as guideline levels that can serve as potential support or resistance zones.

🔹 How It Works

The script operates in two modes, depending on the active chart timeframe:

Weekly Mode (timeframe.isweekly)

The reference date is July 1, 2019.

The number of weeks since that date is calculated.

This defines the connection candle (connection_candle).

Several predefined offsets (e.g., +32, +34, +36 …) are added to the reference to determine starting candles.

Lines are drawn from these candles toward the connection candle.

→ Line color: green

Daily Mode (timeframe.isdaily)

Same reference date: July 1, 2019.

The number of days since that date is calculated.

Again, a connection candle is set.

A different set of offsets (e.g., +224, +238, +252 …) defines the starting candles.

Lines are drawn accordingly.

→ Line color: red

🔹 Line Logic

Each line connects:

Start → bar_index at high

End → bar_index at close

Lines are extended indefinitely to the right (extend.right).

Appearance: dashed style, width 2.

🔹 Error Handling

If a calculated candle index does not exist in the chart history (e.g., chart data does not go back far enough),

a label is plotted in the chart showing the message:

"Daily idx out of range: 252"

This way, missing lines can be diagnosed easily.

🔹 Color Convention

Weekly Spider Lines → Green

Daily Spider Lines → Red

🔹 Use Cases

Visualization of historical cyclic line patterns.

Helps in technical chart analysis: spotting potential reaction zones in price movement.

Designed mainly for long-term traders and analysts observing Bitcoin in Daily or Weekly timeframes.

🔹 Limitations

Works only on Daily and Weekly charts.

Requires chart data going back to July 1, 2019.

Based purely on fixed offsets → not a classical indicator like Moving Averages or RSI.

Emre AOI Zonen Daily & Weekly (mit Alerts, max 60 Pips)This TradingView indicator automatically highlights Areas of Interest (AOI) for Forex or other markets on Daily and Weekly timeframes. It identifies zones based on the high and low of the previous period, but only includes zones with a width of 60 pips or less.

Features:

Daily AOI Zones in blue, Weekly AOI Zones in yellow with 20% opacity, so candlesticks remain visible.

Persistent zones: AOI boxes stay on the chart until the price breaks the zone.

Multiple zones: Supports storing multiple Daily and Weekly AOIs simultaneously.

Break Alerts: Sends alerts whenever a Daily or Weekly AOI is broken, helping traders spot key levels in real-time.

Fully automated: No manual drawing needed; zones are updated and extended automatically.

Use Case:

Ideal for traders using a top-down approach, combining Weekly trend analysis with Daily entry signals. Helps identify support/resistance, supply/demand zones, and critical price levels efficiently.

Close Above/Below Prev 2 Candle (Daily Close)This strategy identifies potential trend continuation or breakout signals by analyzing the daily candle closes relative to the previous two daily candles. It generates clear alerts and trade signals only after the daily candle has fully closed, reducing false intraday triggers.

How it works:

Long Entry (Bullish Signal): Triggered when the daily candle closes above the highs of the previous two daily candles.

Short Entry (Bearish Signal): Triggered when the daily candle closes below the lows of the previous two daily candles.

Visual Indicators: Green triangles indicate bullish signals, red triangles indicate bearish signals.

Strategy Features:

Optional long and short entries with configurable risk/reward ratio.

Automatic stop-loss and take-profit calculation based on candle structure.

Works on intraday charts using daily candle analysis.

Alerts:

Alerts trigger only after the daily candle closes above/below the previous two daily candles.

Helps traders receive precise notifications for potential breakout trades.

Benefits:

Reduces noise by using daily candle closes.

Easy to integrate with other swing or trend strategies.

Provides clear visual and alert signals for both bullish and bearish setups.

Moving Average Exponential (Daily Frozen EMA)This script plots an Exponential Moving Average (EMA) based on the daily timeframe, but with a unique twist:

✅ The EMA value is frozen for the entire current daily session, only updating when a new daily candle begins.

🔍 How it works:

The EMA is calculated using the 1-day timeframe, regardless of the chart's current timeframe.

This EMA value remains fixed throughout the day — it doesn't fluctuate intrabar.

It updates only once the daily candle has closed, providing a stable and reliable reference point during the trading day.

The default is the 5 day EMA but can be changed to any EMA timeframe you desire such as 9, 21, 50, 100. 200, etc.

✨ Additional Features:

✅ Optional smoothing with various moving average types (SMA, EMA, WMA, SMMA, VWMA).

✅ Optional Bollinger Bands on top of the smoothed EMA.

✅ Adjustable settings for EMA length, smoothing type, Bollinger Band deviation, and display options.

🛠️ Use Cases:

Ideal for traders who want a non-reactive EMA during intraday trading.

Helps reduce signal noise by anchoring EMA to higher timeframe structure.

Useful for strategy development where EMA should represent confirmed daily bias only.

Hope this helps, happy trading!

Average Daily Range in TicksPurpose: The ADR Ticks Indicator calculates and displays the average daily price range of a financial instrument, expressed in ticks, over a user-specified number of days. It provides traders with a measure of average daily volatility, which can be used for position sizing, setting stop-loss/take-profit levels, or assessing market activity.

Calculation: Computes the average daily range by taking the difference between the daily high and low prices, averaging this range over a customizable number of days, and converting the result into ticks (using the instrument's minimum tick size).

Customization: Includes a user input to adjust the number of days for the average calculation and a toggle to show/hide the ADR Ticks value in the table.

Risk Management: Helps traders estimate typical daily price movement to set appropriate stop-loss or take-profit levels.

Market Analysis: Offers insight into average daily volatility, useful for day traders or swing traders assessing whether a market is trending or ranging.

Technical Notes:

The indicator uses barstate.islast to update the table only on the last bar, reducing computational load and preventing overlap.

The script handles different chart timeframes by pulling daily data via request.security, making it robust across various instruments and timeframes.

1H & 2H Candle Panel + Daily Grid v1.2Indicator: "1H & 2H Candle Panel + Daily Grid v1.2"

This powerful indicator combines two key features into one tool:

Daily Grid anchored to the previous day’s close

Multi-Timeframe Candle Panel for comprehensive market analysis

1. Daily Grid Logic

Input:

Grid Distance (Points): Adjustable spacing between grid lines (default: 5.0 pts).

How It Works:

Detects the start of a new trading day using ta.change(time("D")).

Fetches the prior day’s close via request.security().

Draws the following elements at each new session:

Thick Red Line: Previous day’s closing price (key reference level).

8-Point Grid:

4 blue lines above the close (+1x to +4x the grid distance).

4 gold lines below the close (-1x to -4x the grid distance).

Info Label: Displays the exact prior close value.

Automatically clears and redraws all elements daily to avoid clutter.

2. Multi-Timeframe Candle Panel

Timeframes Analyzed:

Current chart TF, 30M, 1H, 2H, 3H, 4H, 6H, 12H, and Daily (1D).

Data Displayed per TF:

Open, Close, High, Low

Price Difference (Close − Open)

Candle Type (Bullish/Bearish)

Time remaining until candle close (hh:mm:ss format)

Visual Output:

A right-aligned table with conditional coloring:

Bullish candles: Green background

Bearish candles: Red background

Current timeframe highlighted in purple.

Optimized Updates:

Uses request.security() for efficient cross-TF data fetching.

Tracks candle closing times via TradingView’s native time_close.

Updates only on the last bar or in real-time (barstate.islast/isrealtime).

3. Confluence Signals

Full Confluence:

Triggers when all timeframes align:

Buy Signal: All candles bullish → Green arrow + alert.

Sell Signal: All candles bearish → Red arrow + alert.

1H Special Confluence:

Activates 30 minutes after the 1H candle opens.

Requires alignment between 1H, 4H, and 6H candles.

Marks entries with price-level arrows (no alerts).

4. Technical Optimizations

Performance:

Dynamically manages graphic objects (no redundant redrawing).

Uses arrays to track grid lines efficiently.

Precision:

Leverages TradingView’s time_close for accurate countdowns.

Formats prices with format.mintick for asset-specific precision.

How to Use

Adjust Grid Distance based on asset volatility.

Monitor the panel for multi-TF trend strength.

Use the daily grid as support/resistance reference.

Confluence signals highlight high-probability setups.

Pro Tip: Combine with volume analysis or RSI for confirmation!

Last Week's APM & Daily % Move(Corrected)Last Week's Average Price Movement + Daily Percentage Move (based on NY time)

This indicator accurately displays last week's Average Pip Movement (APM) consistently across all timeframes and tracks the true daily percentage move relative to that APM in a clear table in the top-right corner.

Key Features:

-Consistent Last Week's APM: Calculates the average pip movement from Monday to Friday of the previous trading week (based on daily wick-to-wick ranges, divided by 5). This APM value is now stable and the same across all chart timeframes.

-Accurate Live Daily % Move: Tracks the maximum percentage the price has moved (either up or down) since the 5 PM New York time daily open, compared to last week's APM. The percentage holds the maximum value reached during the day and resets at the next 5 PM NY open.

-NY Time Alignment: All time-based calculations are aligned with the New York time zone

Pip Adjustment: Automatically adjusts for JPY pairs.

⚠️ Important: For the intended display and relevance of the daily percentage move, this indicator is best used on timeframes 4-hour and under. On Daily and Weekly timeframes, the APM display will show a message indicating this.

We hope this indicator enhances your trading analysis.

Enhanced Daily Sentiment & Auction Area Trading StrategyDetermine Daily Sentiment (Anchor Chart - Daily TF):

Analyze Yesterday's Daily Candle: Look at the previous day's daily candlestick (high, low, open, close). This is the "most important information."

Establish Bias: If yesterday's candle was bullish (closed higher), the bias for today is generally long (approx. 80% of the time). If bearish, the bias is short.

Moving Average Context: Note if the daily price is above or below its short-term moving average (e.g., 21 or 50 MA). This should align with the candle's bias (e.g., bullish daily candle above its MA).

Pre-Market & Opening Analysis (Information Gathering):

Check for Gaps: Observe if the market is gapping up or down in the pre-market session relative to yesterday's close. This provides an early clue to current sentiment.

Consider Overall Sentiment: Briefly factor in relevant news or overarching market sentiment (e.g., data releases, overall market feeling from yields, gold etc.). Trading Window: Focus primarily on trading within the first hour of the U.S. market open, as this is when volatility is typically highest, which the strategy relies on.

Setup 5-Minute Chart for Execution (Trading TF - 5-min):

Apply Moving Average: Use the same short-term moving average (e.g., 21 or 50 MA) as on the daily chart.

Seek Alignment (Crucial): The 5-minute chart's trend and price action relative to its MA must align with the daily chart's bias and MA relationship.

If Daily bias is LONG (price above daily MA), the 5-minute chart should also show price establishing itself above its 5-min MA, ideally with a similar "45-degree angle" uptrend.

If Daily bias is SHORT (price below daily MA), the 5-minute chart should also show price establishing itself below its 5-min MA, with a similar downtrend. If there's no clear alignment between the daily and 5-minute chart structure/MA, do not trade.

Identify the "Auction Area" (Value/Congestion) on the 5-Minute Chart:

This is a recent area of congestion, a small support/resistance flip, or where price has paused, consolidated, and is retesting, often near the 5-minute MA.

Uptrend (Long Bias): Look for a pullback (a small "V" shape dip) towards the 5-minute MA or a recent small resistance-turned-support area. This is the "auction retest" before a potential breakout higher.

Downtrend (Short Bias): Look for a pullback rally (an inverted "V" shape) towards the 5-minute MA or a recent small support-turned-resistance area.

10 Monday's 1H Avg Range + 30-Day Daily RangeWhat This Script Does

This indicator is designed for traders who want to monitor volatility and range behavior at the start of the trading week . It focuses specifically on the first four 15-minute candles of each Monday and tracks their combined high-low range over time.

How It Works

Monday 1H Range Detection:

Each week, it automatically detects and highlights the first 4 candles of Monday on a 15-minute chart (1 hour total). It calculates the range between the highest high and lowest low of these candles.

10-Week Average of Monday 1H Ranges:

It stores and averages the last 10 such ranges, displaying this average in a table for weekly comparison.

30-Day Daily Range Average:

Separately, it calculates the average daily range (high – low) of the last 30 daily candles. This value helps put the Monday 1H range into broader context and can guide Stop Loss or TP planning.

Dynamic Labeling & Visual Highlights:

The script visually highlights the first 4 candles of Monday and places a label showing the pip range once the 4 candles have completed. It also updates a small table with the two averages described above.

How to Use It

Use it on the 15-minute timeframe to activate the Monday 1H logic.

Compare the current week’s Monday range to the 10-week average to see if volatility is increasing or decreasing.

Use the 30-day daily range to determine if the Monday opening movement is unusually large or small.

Consider adjusting trade entries, stops, or targets if the Monday range is disproportionately large compared to recent historical behavior.

What Makes It Original?

This is not a typical volatility indicator like ATR or standard deviation. Instead, it’s a purpose-built tool combining:

Time-specific behavior (first hour of the week),

Historical contextualization (10-week average tracking),

A dual-timeframe analysis (15-min + daily),

A user-friendly table and visual interface.

This script helps intraday or swing traders spot abnormal volatility early in the week and adjust their strategies accordingly—especially in fast-moving Forex or Index markets.

BTC Daily DCA CalculatorThe BTC Daily DCA Calculator is an indicator that calculates how much Bitcoin (BTC) you would own today by investing a fixed dollar amount daily (Dollar-Cost Averaging) over a user-defined period. Simply input your start date, end date, and daily investment amount, and the indicator will display a table on the last candle showing your total BTC, total invested, portfolio value, and unrealized yield (in USD and percentage).

Features

Customizable Inputs: Set the start date, end date, and daily dollar amount to simulate your DCA strategy.

Results Table: Displays on the last candle (top-right of the chart) with:

Total BTC: The accumulated Bitcoin from daily purchases.

Total Invested ($): The total dollars invested.

Portfolio Value ($): The current value of your BTC holdings.

Unrealized Yield ($): Your profit/loss in USD.

Unrealized Yield (%): Your profit/loss as a percentage.

Visual Markers: Green triangles below the chart mark each daily investment.

Overlay on Chart: The table and markers appear directly on the BTCUSD price chart for easy reference.

Daily Timeframe: Designed for Daily (1D) charts to ensure accurate calculations.

How to Use

Add the Indicator: Apply the indicator to a BTCUSD chart (e.g., Coinbase:BTCUSD, Binance:BTCUSDT).

Set Daily Timeframe: Ensure your chart is on the Daily (1D) timeframe, or the script will display an error.

Configure Inputs: Open the indicator’s Settings > Inputs tab and set:

Start Date: When to begin the DCA strategy (e.g., 2024-01-01).

End Date: When to end the strategy (e.g., 2025-04-27 or earlier).

Daily Investment ($): The fixed dollar amount to invest daily (e.g., $100).

View Results: Scroll to the last candle in your date range to see the results table in the top-right corner of the chart. Green triangles below the bars indicate investment days.

Settings

Start Date: Choose the start date for your DCA strategy (default: 2024-01-01).

End Date: Choose the end date (default: 2025-04-27). Must be after the start date and within available chart data.

Daily Investment ($): Set the daily investment amount (default: $100). Minimum is $0.01.

Notes

Timeframe: The indicator requires a Daily (1D) chart. Other timeframes will trigger an error.

Data: Ensure your BTCUSD chart has historical data for the selected date range. Use reliable pairs like Coinbase:BTCUSD or Binance:BTCUSDT.

Limitations: Does not account for trading fees or slippage. Future dates (beyond the current date) will not display results.

Performance: Works best with historical data. Free TradingView accounts may have limited historical data; consider premium for longer ranges.

Key Levels (4H and Daily)Key Levels (4H and Daily)

This indicator highlights important key price levels derived from the 4-hour (4H) and daily (D) timeframes, providing traders with critical support and resistance areas. The levels are calculated using the highest highs and lowest lows over a customizable lookback period, offering a dynamic view of significant price points that could influence market movement.

Key Features:

Key Levels for 4H and Daily Timeframes:

The indicator calculates and displays the highest high and lowest low over a user-defined period for both the 4-hour and daily timeframes. This helps traders identify key support and resistance levels that could dictate the market's behavior.

Customizable Lookback Period:

Traders can adjust the lookback period (in days) for both the 4-hour and daily timeframes to reflect different market conditions. This flexibility ensures the levels are tailored to your preferred trading style and market conditions.

Horizontal Lines:

The indicator plots horizontal lines at the high and low levels for both timeframes. These levels serve as dynamic support and resistance areas and help traders monitor price action near these critical points.

Real-Time Updates:

The lines adjust automatically with each new bar, providing up-to-date key levels based on the most recent price action and trading session.

Alert Conditions:

Alerts are built-in to notify traders when the price breaks above or below these key levels. Traders can set up notifications to stay informed when significant market moves occur.

How to Use:

Support and Resistance: Use the levels as potential support and resistance areas where price could reverse. Price often reacts at these levels, providing potential trading opportunities.

Breakouts: Pay attention to breakouts above the high or below the low of these levels. A break above the 4H or daily high could indicate bullish momentum, while a break below could signal bearish trends.

Trend Confirmation: Combine these levels with other technical analysis tools to confirm the overall market trend and enhance your trading strategy.

Perfect for:

Day Traders: Use the 4-hour levels for intraday trading setups, such as potential reversals or breakouts.

Swing Traders: The daily levels provide longer-term insights, helping to identify key zones where price might pause, reverse, or break out.

Market Context: Ideal for those who want to contextualize their trades within broader timeframes, helping to understand the market’s structure at multiple time scales.

This description conveys the utility and functionality of the indicator, focusing on how it helps traders identify and monitor key levels that influence market action.

Custom Daily % Levels Table📘 Indicator Description

"Custom Daily % Levels – table" is a dynamic and customizable tool designed to help traders visualize daily percentage-based price ranges and key metrics in a compact, table-style format.

🧩 Key Features:

📐 Custom Percent Levels: Automatically calculates upper and lower price levels based on a user-defined base percentage and number of levels, relative to the previous daily close.

🟢🔴 Color Gradient Highlighting: Positive levels are shown with a green gradient, negative levels with red, and the level labels with a neutral tone for easy reference.

📊 Live Asset Info: Displays the current symbol, percentage change from the previous daily close, and 14-period RSI, all color-coded for quick interpretation.

⚙️ Header Control: Toggle the visibility of the main info headers and level headers independently.

📌 Position Customization: Choose where the table appears on your chart (top/bottom, left/right, center).

📈 Clean Layout: Makes it easy to visually track price movement relative to daily expected ranges.

This indicator is especially useful for intraday traders, scalpers, or anyone needing a clear visual of short-term price expansion and contraction based on predefined volatility zones.

Average Daily Range ProjectionsCreates a trailing high and low projection based on the Average Daily Range.

Track the Session High and Low to determine the Daily Range.

Average the Daily Range by a fixed Period to create an Average Daily Range .

Track the Prior Daily Range .

Track the Current Daily Range .

Track the % of Range completion relative to the CDR & ADR(P).

From the Session Low, project an Average Daily Range High by adding the ADR.

From the Session High, project an Average Daily Range Low by subtracting the ADR.

When %R reaches 100% or greater, the ADR HI & LO will lock, showing the range break out or break down. As the Session High and Low create the Daily Range, observe the reaction of price as it reaches the limit of the expected daily range.

On strongly trending days, CDR is likely greater than PDR and ADR(P). Price can break away.

On ranging days, %R may fail to reach 100% and CDR may be lesser than PDR and ADR(P). Price can bounce around within the bounds of ADR HI & LO.