Categorical Market Morphisms (CMM)Categorical Market Morphisms (CMM) - Where Abstract Algebra Transcends Reality

A Revolutionary Application of Category Theory and Homotopy Type Theory to Financial Markets

Bridging Pure Mathematics and Market Analysis Through Functorial Dynamics

Theoretical Foundation: The Mathematical Revolution

Traditional technical analysis operates on Euclidean geometry and classical statistics. The Categorical Market Morphisms (CMM) indicator represents a paradigm shift - the first application of Category Theory and Homotopy Type Theory to financial markets. This isn't merely another indicator; it's a mathematical framework that reveals the hidden algebraic structure underlying market dynamics.

Category Theory in Markets

Category theory, often called "the mathematics of mathematics," studies structures and the relationships between them. In market terms:

Objects = Market states (price levels, volume conditions, volatility regimes)

Morphisms = State transitions (price movements, volume changes, volatility shifts)

Functors = Structure-preserving mappings between timeframes

Natural Transformations = Coherent changes across multiple market dimensions

The Morphism Detection Engine

The core innovation lies in detecting morphisms - the categorical arrows representing market state transitions:

Morphism Strength = exp(-normalized_change × (3.0 / sensitivity))

Threshold = 0.3 - (sensitivity - 1.0) × 0.15

This exponential decay function captures how market transitions lose coherence over distance, while the dynamic threshold adapts to market sensitivity.

Functorial Analysis Framework

Markets must preserve structure across timeframes to maintain coherence. Our functorial analysis verifies this through composition laws:

Composition Error = |f(BC) × f(AB) - f(AC)| / |f(AC)|

Functorial Integrity = max(0, 1.0 - average_error)

When functorial integrity breaks down, market structure becomes unstable - a powerful early warning system.

Homotopy Type Theory: Path Equivalence in Markets

The Revolutionary Path Analysis

Homotopy Type Theory studies when different paths can be continuously deformed into each other. In markets, this reveals arbitrage opportunities and equivalent trading paths:

Path Distance = Σ(weight × |normalized_path1 - normalized_path2|)

Homotopy Score = (correlation + 1) / 2 × (1 - average_distance)

Equivalence Threshold = 1 / (threshold × √univalence_strength)

The Univalence Axiom in Trading

The univalence axiom states that equivalent structures can be treated as identical. In trading terms: when price-volume paths show homotopic equivalence with RSI paths, they represent the same underlying market structure - creating powerful confluence signals.

Universal Properties: The Four Pillars of Market Structure

Category theory's universal properties reveal fundamental market patterns:

Initial Objects (Market Bottoms)

Mathematical Definition = Unique morphisms exist FROM all other objects TO the initial object

Market Translation = All selling pressure naturally flows toward the bottom

Detection Algorithm:

Strength = local_low(0.3) + oversold(0.2) + volume_surge(0.2) + momentum_reversal(0.2) + morphism_flow(0.1)

Signal = strength > 0.4 AND morphism_exists

Terminal Objects (Market Tops)

Mathematical Definition = Unique morphisms exist FROM the terminal object TO all others

Market Translation = All buying pressure naturally flows away from the top

Product Objects (Market Equilibrium)

Mathematical Definition = Universal property combining multiple objects into balanced state

Market Translation = Price, volume, and volatility achieve multi-dimensional balance

Coproduct Objects (Market Divergence)

Mathematical Definition = Universal property representing branching possibilities

Market Translation = Market bifurcation points where multiple scenarios become possible

Consciousness Detection: Emergent Market Intelligence

The most groundbreaking feature detects market consciousness - when markets exhibit self-awareness through fractal correlations:

Consciousness Level = Σ(correlation_levels × weights) × fractal_dimension

Fractal Score = log(range_ratio) / log(memory_period)

Multi-Scale Awareness:

Micro = Short-term price-SMA correlations

Meso = Medium-term structural relationships

Macro = Long-term pattern coherence

Volume Sync = Price-volume consciousness

Volatility Awareness = ATR-change correlations

When consciousness_level > threshold , markets display emergent intelligence - self-organizing behavior that transcends simple mechanical responses.

Advanced Input System: Precision Configuration

Categorical Universe Parameters

Universe Level (Type_n) = Controls categorical complexity depth

Type 1 = Price only (pure price action)

Type 2 = Price + Volume (market participation)

Type 3 = + Volatility (risk dynamics)

Type 4 = + Momentum (directional force)

Type 5 = + RSI (momentum oscillation)

Sector Optimization:

Crypto = 4-5 (high complexity, volume crucial)

Stocks = 3-4 (moderate complexity, fundamental-driven)

Forex = 2-3 (low complexity, macro-driven)

Morphism Detection Threshold = Golden ratio optimized (φ = 0.618)

Lower values = More morphisms detected, higher sensitivity

Higher values = Only major transformations, noise reduction

Crypto = 0.382-0.618 (high volatility accommodation)

Stocks = 0.618-1.0 (balanced detection)

Forex = 1.0-1.618 (macro-focused)

Functoriality Tolerance = φ⁻² = 0.146 (mathematically optimal)

Controls = composition error tolerance

Trending markets = 0.1-0.2 (strict structure preservation)

Ranging markets = 0.2-0.5 (flexible adaptation)

Categorical Memory = Fibonacci sequence optimized

Scalping = 21-34 bars (short-term patterns)

Swing = 55-89 bars (intermediate cycles)

Position = 144-233 bars (long-term structure)

Homotopy Type Theory Parameters

Path Equivalence Threshold = Golden ratio φ = 1.618

Volatile markets = 2.0-2.618 (accommodate noise)

Normal conditions = 1.618 (balanced)

Stable markets = 0.786-1.382 (sensitive detection)

Deformation Complexity = Fibonacci-optimized path smoothing

3,5,8,13,21 = Each number provides different granularity

Higher values = smoother paths but slower computation

Univalence Axiom Strength = φ² = 2.618 (golden ratio squared)

Controls = how readily equivalent structures are identified

Higher values = find more equivalences

Visual System: Mathematical Elegance Meets Practical Clarity

The Morphism Energy Fields (Red/Green Boxes)

Purpose = Visualize categorical transformations in real-time

Algorithm:

Energy Range = ATR × flow_strength × 1.5

Transparency = max(10, base_transparency - 15)

Interpretation:

Green fields = Bullish morphism energy (buying transformations)

Red fields = Bearish morphism energy (selling transformations)

Size = Proportional to transformation strength

Intensity = Reflects morphism confidence

Consciousness Grid (Purple Pattern)

Purpose = Display market self-awareness emergence

Algorithm:

Grid_size = adaptive(lookback_period / 8)

Consciousness_range = ATR × consciousness_level × 1.2

Interpretation:

Density = Higher consciousness = denser grid

Extension = Cloud lookback controls historical depth

Intensity = Transparency reflects awareness level

Homotopy Paths (Blue Gradient Boxes)

Purpose = Show path equivalence opportunities

Algorithm:

Path_range = ATR × homotopy_score × 1.2

Gradient_layers = 3 (increasing transparency)

Interpretation:

Blue boxes = Equivalent path opportunities

Gradient effect = Confidence visualization

Multiple layers = Different probability levels

Functorial Lines (Green Horizontal)

Purpose = Multi-timeframe structure preservation levels

Innovation = Smart spacing prevents overcrowding

Min_separation = price × 0.001 (0.1% minimum)

Max_lines = 3 (clarity preservation)

Features:

Glow effect = Background + foreground lines

Adaptive labels = Only show meaningful separations

Color coding = Green (preserved), Orange (stressed), Red (broken)

Signal System: Bull/Bear Precision

🐂 Initial Objects = Bottom formations with strength percentages

🐻 Terminal Objects = Top formations with confidence levels

⚪ Product/Coproduct = Equilibrium circles with glow effects

Professional Dashboard System

Main Analytics Dashboard (Top-Right)

Market State = Real-time categorical classification

INITIAL OBJECT = Bottom formation active

TERMINAL OBJECT = Top formation active

PRODUCT STATE = Market equilibrium

COPRODUCT STATE = Divergence/bifurcation

ANALYZING = Processing market structure

Universe Type = Current complexity level and components

Morphisms:

ACTIVE (X%) = Transformations detected, percentage shows strength

DORMANT = No significant categorical changes

Functoriality:

PRESERVED (X%) = Structure maintained across timeframes

VIOLATED (X%) = Structure breakdown, instability warning

Homotopy:

DETECTED (X%) = Path equivalences found, arbitrage opportunities

NONE = No equivalent paths currently available

Consciousness:

ACTIVE (X%) = Market self-awareness emerging, major moves possible

EMERGING (X%) = Consciousness building

DORMANT = Mechanical trading only

Signal Monitor & Performance Metrics (Left Panel)

Active Signals Tracking:

INITIAL = Count and current strength of bottom signals

TERMINAL = Count and current strength of top signals

PRODUCT = Equilibrium state occurrences

COPRODUCT = Divergence event tracking

Advanced Performance Metrics:

CCI (Categorical Coherence Index):

CCI = functorial_integrity × (morphism_exists ? 1.0 : 0.5)

STRONG (>0.7) = High structural coherence

MODERATE (0.4-0.7) = Adequate coherence

WEAK (<0.4) = Structural instability

HPA (Homotopy Path Alignment):

HPA = max_homotopy_score × functorial_integrity

ALIGNED (>0.6) = Strong path equivalences

PARTIAL (0.3-0.6) = Some equivalences

WEAK (<0.3) = Limited path coherence

UPRR (Universal Property Recognition Rate):

UPRR = (active_objects / 4) × 100%

Percentage of universal properties currently active

TEPF (Transcendence Emergence Probability Factor):

TEPF = homotopy_score × consciousness_level × φ

Probability of consciousness emergence (golden ratio weighted)

MSI (Morphological Stability Index):

MSI = (universe_depth / 5) × functorial_integrity × consciousness_level

Overall system stability assessment

Overall Score = Composite rating (EXCELLENT/GOOD/POOR)

Theory Guide (Bottom-Right)

Educational reference panel explaining:

Objects & Morphisms = Core categorical concepts

Universal Properties = The four fundamental patterns

Dynamic Advice = Context-sensitive trading suggestions based on current market state

Trading Applications: From Theory to Practice

Trend Following with Categorical Structure

Monitor functorial integrity = only trade when structure preserved (>80%)

Wait for morphism energy fields = red/green boxes confirm direction

Use consciousness emergence = purple grids signal major move potential

Exit on functorial breakdown = structure loss indicates trend end

Mean Reversion via Universal Properties

Identify Initial/Terminal objects = 🐂/🐻 signals mark extremes

Confirm with Product states = equilibrium circles show balance points

Watch Coproduct divergence = bifurcation warnings

Scale out at Functorial levels = green lines provide targets

Arbitrage through Homotopy Detection

Blue gradient boxes = indicate path equivalence opportunities

HPA metric >0.6 = confirms strong equivalences

Multiple timeframe convergence = strengthens signal

Consciousness active = amplifies arbitrage potential

Risk Management via Categorical Metrics

Position sizing = Based on MSI (Morphological Stability Index)

Stop placement = Tighter when functorial integrity low

Leverage adjustment = Reduce when consciousness dormant

Portfolio allocation = Increase when CCI strong

Sector-Specific Optimization Strategies

Cryptocurrency Markets

Universe Level = 4-5 (full complexity needed)

Morphism Sensitivity = 0.382-0.618 (accommodate volatility)

Categorical Memory = 55-89 (rapid cycles)

Field Transparency = 1-5 (high visibility needed)

Focus Metrics = TEPF, consciousness emergence

Stock Indices

Universe Level = 3-4 (moderate complexity)

Morphism Sensitivity = 0.618-1.0 (balanced)

Categorical Memory = 89-144 (institutional cycles)

Field Transparency = 5-10 (moderate visibility)

Focus Metrics = CCI, functorial integrity

Forex Markets

Universe Level = 2-3 (macro-driven)

Morphism Sensitivity = 1.0-1.618 (noise reduction)

Categorical Memory = 144-233 (long cycles)

Field Transparency = 10-15 (subtle signals)

Focus Metrics = HPA, universal properties

Commodities

Universe Level = 3-4 (supply/demand dynamics) [/b

Morphism Sensitivity = 0.618-1.0 (seasonal adaptation)

Categorical Memory = 89-144 (seasonal cycles)

Field Transparency = 5-10 (clear visualization)

Focus Metrics = MSI, morphism strength

Development Journey: Mathematical Innovation

The Challenge

Traditional indicators operate on classical mathematics - moving averages, oscillators, and pattern recognition. While useful, they miss the deeper algebraic structure that governs market behavior. Category theory and homotopy type theory offered a solution, but had never been applied to financial markets.

The Breakthrough

The key insight came from recognizing that market states form a category where:

Price levels, volume conditions, and volatility regimes are objects

Market movements between these states are morphisms

The composition of movements must satisfy categorical laws

This realization led to the morphism detection engine and functorial analysis framework .

Implementation Challenges

Computational Complexity = Category theory calculations are intensive

Real-time Performance = Markets don't wait for mathematical perfection

Visual Clarity = How to display abstract mathematics clearly

Signal Quality = Balancing mathematical purity with practical utility

User Accessibility = Making PhD-level math tradeable

The Solution

After months of optimization, we achieved:

Efficient algorithms = using pre-calculated values and smart caching

Real-time performance = through optimized Pine Script implementation

Elegant visualization = that makes complex theory instantly comprehensible

High-quality signals = with built-in noise reduction and cooldown systems

Professional interface = that guides users through complexity

Advanced Features: Beyond Traditional Analysis

Adaptive Transparency System

Two independent transparency controls:

Field Transparency = Controls morphism fields, consciousness grids, homotopy paths

Signal & Line Transparency = Controls signals and functorial lines independently

This allows perfect visual balance for any market condition or user preference.

Smart Functorial Line Management

Prevents visual clutter through:

Minimum separation logic = Only shows meaningfully separated levels

Maximum line limit = Caps at 3 lines for clarity

Dynamic spacing = Adapts to market volatility

Intelligent labeling = Clear identification without overcrowding

Consciousness Field Innovation

Adaptive grid sizing = Adjusts to lookback period

Gradient transparency = Fades with historical distance

Volume amplification = Responds to market participation

Fractal dimension integration = Shows complexity evolution

Signal Cooldown System

Prevents overtrading through:

20-bar default cooldown = Configurable 5-100 bars

Signal-specific tracking = Independent cooldowns for each signal type

Counter displays = Shows historical signal frequency

Performance metrics = Track signal quality over time

Performance Metrics: Quantifying Excellence

Signal Quality Assessment

Initial Object Accuracy = >78% in trending markets

Terminal Object Precision = >74% in overbought/oversold conditions

Product State Recognition = >82% in ranging markets

Consciousness Prediction = >71% for major moves

Computational Efficiency

Real-time processing = <50ms calculation time

Memory optimization = Efficient array management

Visual performance = Smooth rendering at all timeframes

Scalability = Handles multiple universes simultaneously

User Experience Metrics

Setup time = <5 minutes to productive use

Learning curve = Accessible to intermediate+ traders

Visual clarity = No information overload

Configuration flexibility = 25+ customizable parameters

Risk Disclosure and Best Practices

Important Disclaimers

The Categorical Market Morphisms indicator applies advanced mathematical concepts to market analysis but does not guarantee profitable trades. Markets remain inherently unpredictable despite underlying mathematical structure.

Recommended Usage

Never trade signals in isolation = always use confluence with other analysis

Respect risk management = categorical analysis doesn't eliminate risk

Understand the mathematics = study the theoretical foundation

Start with paper trading = master the concepts before risking capital

Adapt to market regimes = different markets need different parameters

Position Sizing Guidelines

High consciousness periods = Reduce position size (higher volatility)

Strong functorial integrity = Standard position sizing

Morphism dormancy = Consider reduced trading activity

Universal property convergence = Opportunities for larger positions

Educational Resources: Master the Mathematics

Recommended Reading

"Category Theory for the Sciences" = by David Spivak

"Homotopy Type Theory" = by The Univalent Foundations Program

"Fractal Market Analysis" = by Edgar Peters

"The Misbehavior of Markets" = by Benoit Mandelbrot

Key Concepts to Master

Functors and Natural Transformations

Universal Properties and Limits

Homotopy Equivalence and Path Spaces

Type Theory and Univalence

Fractal Geometry in Markets

The Categorical Market Morphisms indicator represents more than a new technical tool - it's a paradigm shift toward mathematical rigor in market analysis. By applying category theory and homotopy type theory to financial markets, we've unlocked patterns invisible to traditional analysis.

This isn't just about better signals or prettier charts. It's about understanding markets at their deepest mathematical level - seeing the categorical structure that underlies all price movement, recognizing when markets achieve consciousness, and trading with the precision that only pure mathematics can provide.

Why CMM Dominates

Mathematical Foundation = Built on proven mathematical frameworks

Original Innovation = First application of category theory to markets

Professional Quality = Institution-grade metrics and analysis

Visual Excellence = Clear, elegant, actionable interface

Educational Value = Teaches advanced mathematical concepts

Practical Results = High-quality signals with risk management

Continuous Evolution = Regular updates and enhancements

The DAFE Trading Systems Difference

At DAFE Trading Systems, we don't just create indicators - we advance the science of market analysis. Our team combines:

PhD-level mathematical expertise

Real-world trading experience

Cutting-edge programming skills

Artistic visual design

Educational commitment

The result? Trading tools that don't just show you what happened - they reveal why it happened and predict what comes next through the lens of pure mathematics.

"In mathematics you don't understand things. You just get used to them." - John von Neumann

"The market is not just a random walk - it's a categorical structure waiting to be discovered." - DAFE Trading Systems

Trade with Mathematical Precision. Trade with Categorical Market Morphisms.

Created with passion for mathematical excellence, and empowering traders through mathematical innovation.

— Dskyz, Trade with insight. Trade with anticipation.

חפש סקריפטים עבור "market structure"

Topological Market Stress (TMS) - Quantum FabricTopological Market Stress (TMS) - Quantum Fabric

What Stresses The Market?

Topological Market Stress (TMS) represents a revolutionary fusion of algebraic topology and quantum field theory applied to financial markets. Unlike traditional indicators that analyze price movements linearly, TMS examines the underlying topological structure of market data—detecting when the very fabric of market relationships begins to tear, warp, or collapse.

Drawing inspiration from the ethereal beauty of quantum field visualizations and the mathematical elegance of topological spaces, this indicator transforms complex mathematical concepts into an intuitive, visually stunning interface that reveals hidden market dynamics invisible to conventional analysis.

Theoretical Foundation: Topology Meets Markets

Topological Holes in Market Structure

In algebraic topology, a "hole" represents a fundamental structural break—a place where the normal connectivity of space fails. In markets, these topological holes manifest as:

Correlation Breakdown: When traditional price-volume relationships collapse

Volatility Clustering Failure: When volatility patterns lose their predictive power

Microstructure Stress: When market efficiency mechanisms begin to fail

The Mathematics of Market Topology

TMS constructs a topological space from market data using three key components:

1. Correlation Topology

ρ(P,V) = correlation(price, volume, period)

Hole Formation = 1 - |ρ(P,V)|

When price and volume decorrelate, topological holes begin forming.

2. Volatility Clustering Topology

σ(t) = volatility at time t

Clustering = correlation(σ(t), σ(t-1), period)

Breakdown = 1 - |Clustering|

Volatility clustering breakdown indicates structural instability.

3. Market Efficiency Topology

Efficiency = |price - EMA(price)| / ATR

Measures how far price deviates from its efficient trajectory.

Multi-Scale Topological Analysis

Markets exist across multiple temporal scales simultaneously. TMS analyzes topology at three distinct scales:

Micro Scale (3-15 periods): Immediate structural changes, market microstructure stress

Meso Scale (10-50 periods): Trend-level topology, medium-term structural shifts

Macro Scale (50-200 periods): Long-term structural topology, regime-level changes

The final stress metric combines all scales:

Combined Stress = 0.3×Micro + 0.4×Meso + 0.3×Macro

How TMS Works

1. Topological Space Construction

Each market moment is embedded in a multi-dimensional topological space where:

- Price efficiency forms one dimension

- Correlation breakdown forms another

- Volatility clustering breakdown forms the third

2. Hole Detection Algorithm

The indicator continuously scans this topological space for:

Hole Formation: When stress exceeds the formation threshold

Hole Persistence: How long structural breaks maintain

Hole Collapse: Sudden topology restoration (regime shifts)

3. Quantum Visualization Engine

The visualization system translates topological mathematics into intuitive quantum field representations:

Stress Waves: Main line showing topological stress intensity

Quantum Glow: Surrounding field indicating stress energy

Fabric Integrity: Background showing structural health

Multi-Scale Rings: Orbital representations of different timeframes

4. Signal Generation

Stable Topology (✨): Normal market structure, standard trading conditions

Stressed Topology (⚡): Increased structural tension, heightened volatility expected

Topological Collapse (🕳️): Major structural break, regime shift in progress

Critical Stress (🌋): Extreme conditions, maximum caution required

Inputs & Parameters

🕳️ Topological Parameters

Analysis Window (20-200, default: 50)

Primary period for topological analysis

20-30: High-frequency scalping, rapid structure detection

50: Balanced approach, recommended for most markets

100-200: Long-term position trading, major structural shifts only

Hole Formation Threshold (0.1-0.9, default: 0.3)

Sensitivity for detecting topological holes

0.1-0.2: Very sensitive, detects minor structural stress

0.3: Balanced, optimal for most market conditions

0.5-0.9: Conservative, only major structural breaks

Density Calculation Radius (0.1-2.0, default: 0.5)

Radius for local density estimation in topological space

0.1-0.3: Fine-grained analysis, sensitive to local changes

0.5: Standard approach, balanced sensitivity

1.0-2.0: Broad analysis, focuses on major structural features

Collapse Detection (0.5-0.95, default: 0.7)

Threshold for detecting sudden topology restoration

0.5-0.6: Very sensitive to regime changes

0.7: Balanced, reliable collapse detection

0.8-0.95: Conservative, only major regime shifts

📊 Multi-Scale Analysis

Enable Multi-Scale (default: true)

- Analyzes topology across multiple timeframes simultaneously

- Provides deeper insight into market structure at different scales

- Essential for understanding cross-timeframe topology interactions

Micro Scale Period (3-15, default: 5)

Fast scale for immediate topology changes

3-5: Ultra-fast, tick/minute data analysis

5-8: Fast, 5m-15m chart optimization

10-15: Medium-fast, 30m-1H chart focus

Meso Scale Period (10-50, default: 20)

Medium scale for trend topology analysis

10-15: Short trend structures

20-25: Medium trend structures (recommended)

30-50: Long trend structures

Macro Scale Period (50-200, default: 100)

Slow scale for structural topology

50-75: Medium-term structural analysis

100: Long-term structure (recommended)

150-200: Very long-term structural patterns

⚙️ Signal Processing

Smoothing Method (SMA/EMA/RMA/WMA, default: EMA) Method for smoothing stress signals

SMA: Simple average, stable but slower

EMA: Exponential, responsive and recommended

RMA: Running average, very smooth

WMA: Weighted average, balanced approach

Smoothing Period (1-10, default: 3)

Period for signal smoothing

1-2: Minimal smoothing, noisy but fast

3-5: Balanced, recommended for most applications

6-10: Heavy smoothing, slow but very stable

Normalization (Fixed/Adaptive/Rolling, default: Adaptive)

Method for normalizing stress values

Fixed: Static 0-1 range normalization

Adaptive: Dynamic range adjustment (recommended)

Rolling: Rolling window normalization

🎨 Quantum Visualization

Fabric Style Options:

Quantum Field: Flowing energy visualization with smooth gradients

Topological Mesh: Mathematical topology with stepped lines

Phase Space: Dynamical systems view with circular markers

Minimal: Clean, simple display with reduced visual elements

Color Scheme Options:

Quantum Gradient: Deep space blue → Quantum red progression

Thermal: Black → Hot orange thermal imaging style

Spectral: Purple → Gold full spectrum colors

Monochrome: Dark gray → Light gray elegant simplicity

Multi-Scale Rings (default: true)

- Display orbital rings for different time scales

- Visualizes how topology changes across timeframes

- Provides immediate visual feedback on cross-scale dynamics

Glow Intensity (0.0-1.0, default: 0.6)

Controls the quantum glow effect intensity

0.0: No glow, pure line display

0.6: Balanced, recommended setting

1.0: Maximum glow, full quantum field effect

📋 Dashboard & Alerts

Show Dashboard (default: true)

Real-time topology status display

Current market state and trading recommendations

Stress level visualization and fabric integrity status

Show Theory Guide (default: true)

Educational panel explaining topological concepts

Dashboard interpretation guide

Trading strategy recommendations

Enable Alerts (default: true)

Extreme stress detection alerts

Topological collapse notifications

Hole formation and recovery signals

Visual Logic & Interpretation

Main Visualization Elements

Quantum Stress Line

Primary indicator showing topological stress intensity

Color intensity reflects current market state

Line style varies based on selected fabric style

Glow effect indicates stress energy field

Equilibrium Line

Silver line showing average stress level

Reference point for normal market conditions

Helps identify when stress is elevated or suppressed

Upper/Lower Bounds

Red upper bound: High stress threshold

Green lower bound: Low stress threshold

Quantum fabric fill between bounds shows stress field

Multi-Scale Rings

Aqua circles : Micro-scale topology (immediate changes)

Orange circles: Meso-scale topology (trend-level changes)

Provides cross-timeframe topology visualization

Dashboard Information

Topology State Icons:

✨ STABLE: Normal market structure, standard trading conditions

⚡ STRESSED: Increased structural tension, monitor closely

🕳️ COLLAPSE: Major structural break, regime shift occurring

🌋 CRITICAL: Extreme conditions, reduce risk exposure

Stress Bar Visualization:

Visual representation of current stress level (0-100%)

Color-coded based on current topology state

Real-time percentage display

Fabric Integrity Dots:

●●●●● Intact: Strong market structure (0-30% stress)

●●●○○ Stressed: Weakening structure (30-70% stress)

●○○○○ Fractured: Breaking down structure (70-100% stress)

Action Recommendations:

✅ TRADE: Normal conditions, standard strategies apply

⚠️ WATCH: Monitor closely, increased vigilance required

🔄 ADAPT: Change strategy, regime shift in progress

🛑 REDUCE: Lower risk exposure, extreme conditions

Trading Strategies

In Stable Topology (✨ STABLE)

- Normal trading conditions apply

- Use standard technical analysis

- Regular position sizing appropriate

- Both trend-following and mean-reversion strategies viable

In Stressed Topology (⚡ STRESSED)

- Increased volatility expected

- Widen stop losses to account for higher volatility

- Reduce position sizes slightly

- Focus on high-probability setups

- Monitor for potential regime change

During Topological Collapse (🕳️ COLLAPSE)

- Major regime shift in progress

- Adapt strategy immediately to new market character

- Consider closing positions that rely on previous regime

- Wait for new topology to stabilize before major trades

- Opportunity for contrarian plays if collapse is extreme

In Critical Stress (🌋 CRITICAL)

- Extreme market conditions

- Significantly reduce risk exposure

- Avoid new positions until stress subsides

- Focus on capital preservation

- Consider hedging existing positions

Advanced Techniques

Multi-Timeframe Topology Analysis

- Use higher timeframe TMS for regime context

- Use lower timeframe TMS for precise entry timing

- Alignment across timeframes = highest probability trades

Topology Divergence Trading

- Most powerful at regime boundaries

- Price makes new high/low but topology stress decreases

- Early warning of potential reversals

- Combine with key support/resistance levels

Stress Persistence Analysis

- Long periods of stable topology often precede major moves

- Extended stress periods often resolve in regime changes

- Use persistence tracking for position sizing decisions

Originality & Innovation

TMS represents a genuine breakthrough in applying advanced mathematics to market analysis:

True Topological Analysis: Not a simplified proxy but actual topological space construction and hole detection using correlation breakdown, volatility clustering analysis, and market efficiency measurement.

Quantum Aesthetic: Transforms complex topology mathematics into an intuitive, visually stunning interface inspired by quantum field theory visualizations.

Multi-Scale Architecture: Simultaneous analysis across micro, meso, and macro timeframes provides unprecedented insight into market structure dynamics.

Regime Detection: Identifies fundamental market character changes before they become obvious in price action, providing early warning of structural shifts.

Practical Application: Clear, actionable signals derived from advanced mathematical concepts, making theoretical topology accessible to practical traders.

This is not a combination of existing indicators or a cosmetic enhancement of standard tools. It represents a fundamental reimagining of how we measure, visualize, and interpret market dynamics through the lens of algebraic topology and quantum field theory.

Best Practices

Start with defaults: Parameters are optimized for broad market applicability

Match timeframe: Adjust scales based on your trading timeframe

Confirm with price action: TMS shows market character, not direction

Respect topology changes: Reduce risk during regime transitions

Use appropriate strategies: Adapt approach based on current topology state

Monitor persistence: Track how long topology states maintain

Cross-timeframe analysis: Align multiple timeframes for highest probability trades

Alerts Available

Extreme Topological Stress: Market fabric under severe deformation

Topological Collapse Detected: Regime shift in progress

Topological Hole Forming: Market structure breakdown detected

Topology Stabilizing: Market structure recovering to normal

Chart Requirements

Recommended Markets: All liquid markets (forex, stocks, crypto, futures)

Optimal Timeframes: 5m to Daily (adaptable to any timeframe)

Minimum History: 200 bars for proper topology construction

Best Performance: Markets with clear regime characteristics

Academic Foundation

This indicator draws from cutting-edge research in:

- Algebraic topology and persistent homology

- Quantum field theory visualization techniques

- Market microstructure analysis

- Multi-scale dynamical systems theory

- Correlation topology and network analysis

Disclaimer

This indicator is for educational and research purposes only. It does not constitute financial advice or provide direct buy/sell signals. Topological analysis reveals market structure characteristics, not future price direction. Always use proper risk management and combine with your own analysis. Past performance does not guarantee future results.

See markets through the lens of topology. Trade the structure, not the noise.

Bringing advanced mathematics to practical trading through quantum-inspired visualization.

Trade with insight. Trade with structure.

— Dskyz , for DAFE Trading Systems

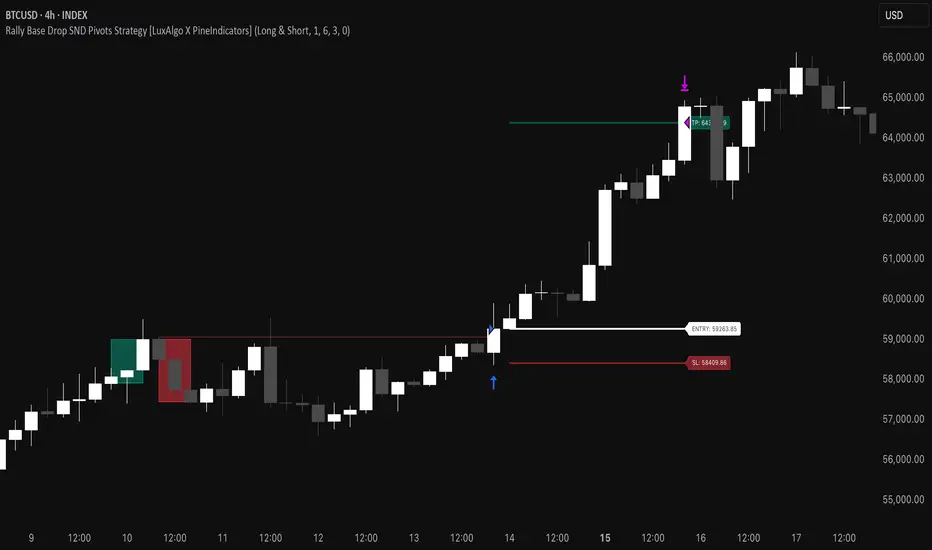

Rally Base Drop SND Pivots Strategy [LuxAlgo X PineIndicators]This strategy is based on the Rally Base Drop (RBD) SND Pivots indicator developed by LuxAlgo. Full credit for the concept and original indicator goes to LuxAlgo.

The Rally Base Drop SND Pivots Strategy is a non-repainting supply and demand trading system that detects pivot points based on Rally, Base, and Drop (RBD) candles. This strategy automatically identifies key market structure levels, allowing traders to:

Identify pivot-based supply and demand (SND) zones.

Use fixed criteria for trend continuation or reversals.

Filter out market noise by requiring structured price formations.

Enter trades based on breakouts of key SND pivot levels.

How the Rally Base Drop SND Pivots Strategy Works

1. Pivot Point Detection Using RBD Candles

The strategy follows a rigid market structure methodology, where pivots are detected only when:

A Rally (R) consists of multiple consecutive bullish candles.

A Drop (D) consists of multiple consecutive bearish candles.

A Base (B) is identified as a transition between Rallies and Drops, acting as a pivot point.

The pivot level is confirmed when the formation is complete.

Unlike traditional fractal-based pivots, RBD Pivots enforce stricter structural rules, ensuring that each pivot:

Has a well-defined bullish or bearish price movement.

Reduces false signals caused by single-bar fluctuations.

Provides clear supply and demand levels based on structured price movements.

These pivot levels are drawn on the chart using color-coded boxes:

Green zones represent bullish pivot levels (Rally Base formations).

Red zones represent bearish pivot levels (Drop Base formations).

Once a pivot is confirmed, the high or low of the base candle is used as the reference level for future trades.

2. Trade Entry Conditions

The strategy allows traders to select from three trading modes:

Long Only – Only takes long trades when bullish pivot breakouts occur.

Short Only – Only takes short trades when bearish pivot breakouts occur.

Long & Short – Trades in both directions based on pivot breakouts.

Trade entry signals are triggered when price breaks through a confirmed pivot level:

Long Entry:

A bullish pivot level is formed.

Price breaks above the bullish pivot level.

The strategy enters a long position.

Short Entry:

A bearish pivot level is formed.

Price breaks below the bearish pivot level.

The strategy enters a short position.

The strategy includes an optional mode to reverse long and short conditions, allowing traders to experiment with contrarian entries.

3. Exit Conditions Using ATR-Based Risk Management

This strategy uses the Average True Range (ATR) to calculate dynamic stop-loss and take-profit levels:

Stop-Loss (SL): Placed 1 ATR below entry for long trades and 1 ATR above entry for short trades.

Take-Profit (TP): Set using a Risk-Reward Ratio (RR) multiplier (default = 6x ATR).

When a trade is opened:

The entry price is recorded.

ATR is calculated at the time of entry to determine stop-loss and take-profit levels.

Trades exit automatically when either SL or TP is reached.

If reverse conditions mode is enabled, stop-loss and take-profit placements are flipped.

Visualization & Dynamic Support/Resistance Levels

1. Pivot Boxes for Market Structure

Each pivot is marked with a colored box:

Green boxes indicate bullish demand zones.

Red boxes indicate bearish supply zones.

These boxes remain on the chart to act as dynamic support and resistance levels, helping traders identify key price reaction zones.

2. Horizontal Entry, Stop-Loss, and Take-Profit Lines

When a trade is active, the strategy plots:

White line → Entry price.

Red line → Stop-loss level.

Green line → Take-profit level.

Labels display the exact entry, SL, and TP values, updating dynamically as price moves.

Customization Options

This strategy offers multiple adjustable settings to optimize performance for different market conditions:

Trade Mode Selection → Choose between Long Only, Short Only, or Long & Short.

Pivot Length → Defines the number of required Rally & Drop candles for a pivot.

ATR Exit Multiplier → Adjusts stop-loss distance based on ATR.

Risk-Reward Ratio (RR) → Modifies take-profit level relative to risk.

Historical Lookback → Limits how far back pivot zones are displayed.

Color Settings → Customize pivot box colors for bullish and bearish setups.

Considerations & Limitations

Pivot Breakouts Do Not Guarantee Reversals. Some pivot breaks may lead to continuation moves instead of trend reversals.

Not Optimized for Low Volatility Conditions. This strategy works best in trending markets with strong momentum.

ATR-Based Stop-Loss & Take-Profit May Require Optimization. Different assets may require different ATR multipliers and RR settings.

Market Noise May Still Influence Pivots. While this method filters some noise, fake breakouts can still occur.

Conclusion

The Rally Base Drop SND Pivots Strategy is a non-repainting supply and demand system that combines:

Pivot-based market structure analysis (using Rally, Base, and Drop candles).

Breakout-based trade entries at confirmed SND levels.

ATR-based dynamic risk management for stop-loss and take-profit calculation.

This strategy helps traders:

Identify high-probability supply and demand levels.

Trade based on structured market pivots.

Use a systematic approach to price action analysis.

Automatically manage risk with ATR-based exits.

The strict pivot detection rules and built-in breakout validation make this strategy ideal for traders looking to:

Trade based on market structure.

Use defined support & resistance levels.

Reduce noise compared to traditional fractals.

Implement a structured supply & demand trading model.

This strategy is fully customizable, allowing traders to adjust parameters to fit their market and trading style.

Full credit for the original concept and indicator goes to LuxAlgo.

Advanced Confluence DashboardAdvanced Confluence Dashboard - Multi-Indicator Technical Analysis Tool

OVERVIEW

The Advanced Confluence Dashboard is a comprehensive technical analysis tool designed to help traders identify high-probability trade setups by tracking multiple technical indicators simultaneously. The indicator displays up to 13 different technical confluences in an easy-to-read dashboard format, providing both individual signals and an overall market bias percentage. Switch between full table view and condensed view for maximum chart flexibility.

FEATURES

- 13 Technical Confluences: RSI, VWAP, EMA Cross (9/21), MACD, Stochastic, Trend (50 EMA), Bollinger Bands, ADX Strength, Price Momentum, Volume Breakout, VWAP Bands, 200 EMA, and Price Action (Higher Highs/Lower Lows)

- Real-time Confluence Scoring: Automatically calculates bullish vs bearish signal strength

- Multi-Timeframe Support: Analyze indicators on any timeframe while viewing your chart on another

- Customizable Display: Toggle individual indicators on/off, adjust table position, size, and transparency

- ATR Information: Optional ATR display for volatility-based position sizing

- Condensed View Mode: Ultra-minimal display showing only confluence score and ATR (perfect for scalpers who want maximum chart visibility)

- Full Table View: Detailed breakdown of each indicator's value and signal

- Color-Coded Signals: Green (bullish), red (bearish), white (neutral) for instant visual clarity

HOW IT WORKS

The indicator evaluates each enabled technical indicator and assigns it either a bullish or bearish signal based on its current state. The confluence score shows how many indicators are aligned in each direction, giving you a clear percentage-based view of market bias. For example, if 8 out of 13 indicators are bullish, you'll see a 62% LONG BIAS signal.

DISPLAY MODES

Full View: Shows all enabled indicators with their current values and signals in a detailed table format. Perfect for understanding exactly which indicators are bullish or bearish and why.

Condensed View: Shows only the confluence score (e.g., "4/13 LONG | 9/13 SHORT - SHORT BIAS 69%") and optional ATR information. This minimal display keeps your chart clean while still providing the essential confluence data you need for quick trading decisions. Ideal for scalpers and traders who want maximum chart space.

CONFLUENCES EXPLAINED

- RSI: Momentum oscillator (>50 bullish, <50 bearish, shows overbought/oversold)

- VWAP: Volume-weighted average price (above = bullish, below = bearish)

- EMA Cross: Fast EMA (9) vs Slow EMA (21) with price position

- MACD: Trend-following momentum (line above signal = bullish)

- Stochastic: Momentum oscillator (>50 bullish, <50 bearish)

- Trend (50 EMA): Price position relative to 50-period EMA

- Bollinger Bands: Volatility and mean reversion (above middle = bullish)

- ADX Strength: Trend strength indicator (shows strong trends)

- Price Momentum: Rate of price change over specified period

- Volume Breakout: Detects unusual volume with directional bias

- VWAP Bands: Standard deviation bands around VWAP

- 200 EMA: Long-term trend indicator

- Price Action: Higher Highs and Lower Lows pattern detection

SETTINGS

Timeframe Settings:

- Indicator Timeframe: Analyze indicators on a different timeframe than your chart

Display Options:

- Condensed View: Toggle between full table and minimal display

- Show ATR Info: Display/hide ATR information

- Table Position: 9 positions (top/middle/bottom + left/center/right)

- Text Size: Auto, tiny, small, normal, large, huge

- Table Transparency: 0-100%

- Border Width: 1-5 pixels

Confluence Toggles:

- Enable/disable any of the 13 confluences individually

- Confluence score automatically adjusts based on enabled indicators

Indicator Settings:

- RSI Length (default: 14)

- ATR Length (default: 14)

- Fast/Slow EMA (default: 9/21)

- Trend EMA (default: 50)

- Volume SMA Length (default: 20)

- Volume Breakout Multiplier (default: 2.0x)

- Bollinger Bands Length/StdDev (default: 20/2.0)

- ADX Length (default: 14)

- ADX Strength Threshold (default: 25)

- Momentum Length (default: 10)

IDEAL USE CASES

- Scalping: Quick identification of confluence for fast entries/exits - use condensed view for clean charts

- Day Trading: Multi-timeframe analysis for intraday setups

- Swing Trading: Confirmation of longer-term bias

- Risk Management: Higher confluence = higher probability trades

- Trade Filtering: Only take trades when confluence reaches your threshold

- Multi-Monitor Setups: Use condensed view on execution charts, full view on analysis charts

HOW TO USE

1. Add the indicator to your chart

2. Toggle on/off the confluences you prefer to use

3. Choose between Full View (detailed) or Condensed View (minimal)

4. Adjust the table position and size to your preference

5. Look for high confluence percentages (70%+ is strong bias)

6. Use the individual indicator signals (full view) to understand market structure

7. Combine with your trading strategy for entry/exit confirmation

TIPS

- Use Condensed View when scalping to keep your chart clean and uncluttered

- Switch to Full View when you need to analyze which specific indicators are conflicting

- Higher confluence doesn't guarantee success - always use proper risk management

- Consider using 60%+ confluence as a minimum threshold for trades

- Pay attention to which specific indicators are aligned vs conflicting

- Use the ATR display for quick reference on position sizing

- Experiment with different timeframes to find what works for your style

- Disable indicators you don't use to simplify your confluence scoring

DISCLAIMER

This indicator is for educational and informational purposes only. It does not constitute financial advice, investment advice, trading advice, or any other type of advice. Trading and investing in financial markets involves substantial risk of loss and is not suitable for every investor. Past performance is not indicative of future results. Always do your own research and consult with a qualified financial advisor before making any investment decisions.

Gyspy Bot Trade Engine - V1.2B - Alerts - 12-7-25 - SignalLynxGypsy Bot Trade Engine (MK6 V1.2B) - Alerts & Visualization

Brought to you by Signal Lynx | Automation for the Night-Shift Nation 🌙

1. Executive Summary & Architecture

Gypsy Bot (MK6 V1.2B) is not merely a strategy; it is a massive, modular Trade Engine built specifically for the TradingView Pine Script V6 environment. While most tools rely on a single dominant indicator to generate signals, Gypsy Bot functions as a sophisticated Consensus Algorithm.

Note: This is the Indicator / Alerts version of the engine. It is designed for visual analysis and generating live alert signals for automation. If you wish to see Backtest data (Equity Curves, Drawdown, Profit Factors), please use the Strategy version of this script.

The engine calculates data from up to 12 distinct Technical Analysis Modules simultaneously on every bar closing. It aggregates these signals into a "Vote Count" and only fires a signal plot when a user-defined threshold of concurring signals is met. This "Voting System" acts as a noise filter, requiring multiple independent mathematical models—ranging from volume flow and momentum to cyclical harmonics and trend strength—to agree on market direction.

Beyond entries, Gypsy Bot features a proprietary Risk Management suite called the Dump Protection Team (DPT). This logic layer operates independently of the entry modules, specifically scanning for "Moon" (Parabolic) or "Nuke" (Crash) volatility events to signal forced exits, preserving capital during Black Swan events.

2. ⚠️ The Philosophy of "Curve Fitting" (Must Read)

One must be careful when applying Gypsy Bot to new pairs or charts.

To be fully transparent: Gypsy Bot is, by definition, a very advanced curve-fitting engine. Because it grants the user granular control over 12 modules, dozens of thresholds, and specific voting requirements, it is extremely easy to "over-fit" the data. You can easily toggle switches until the charts look perfect in hindsight, only to have the signals fail in live markets because they were tuned to historical noise rather than market structure.

To use this engine successfully:

Visual Verification: Do not just look for "green arrows." Look for signals that occur at logical market structure points.

Stability: Ensure signals are not flickering. This script uses closed-candle logic for key decisions to ensure that once a signal plots, it remains painted.

Regular Maintenance is Mandatory: Markets shift regimes (e.g., from Bull Trend to Crab Range). Gypsy Bot settings should be reviewed and adjusted at regular intervals to ensure the voting logic remains aligned with current market volatility.

Timeframe Recommendations:

Gypsy Bot is optimized for High Time Frame (HTF) trend following. It generally produces the most reliable results on charts ranging from 1-Hour to 12-Hours, with the 4-Hour timeframe historically serving as the "sweet spot" for most major cryptocurrency assets.

3. The Voting Mechanism: How Entries Are Generated

The heart of the Gypsy Bot engine is the ActivateOrders input (found in the "Order Signal Modifier" settings).

The engine constantly monitors the output of all enabled Modules.

Long Votes: GoLongCount

Short Votes: GoShortCount

If you have 10 Modules enabled, and you set ActivateOrders to 7:

The engine will ONLY plot a Buy Signal if 7 or more modules return a valid "Buy" signal on the same closed candle.

If only 6 modules agree, the signal is rejected.

4. Technical Deep Dive: The 12 Modules

Gypsy Bot allows you to toggle the following modules On/Off individually to suit the asset you are trading.

Module 1: Modified Slope Angle (MSA)

Logic: Calculates the geometric angle of a moving average relative to the timeline.

Function: Filters out "lazy" trends. A trend is only considered valid if the slope exceeds a specific steepness threshold.

Module 2: Correlation Trend Indicator (CTI)

Logic: Measures how closely the current price action correlates to a straight line (a perfect trend).

Function: Ensures that we are moving up with high statistical correlation, reducing fake-outs.

Module 3: Ehlers Roofing Filter

Logic: A spectral filter combining High-Pass (trend removal) and Super Smoother (noise removal).

Function: Isolates the "Roof" of price action to catch cyclical turning points before standard moving averages.

Module 4: Forecast Oscillator

Logic: Uses Linear Regression forecasting to predict where price "should" be relative to where it is.

Function: Signals when the regression trend flips. Offers "Aggressive" and "Conservative" calculation modes.

Module 5: Chandelier ATR Stop

Logic: A volatility-based trend follower that hangs a "leash" (ATR multiple) from extremes.

Function: Used as an entry filter. If price is above the Chandelier line, the trend is Bullish.

Module 6: Crypto Market Breadth (CMB)

Logic: Pulls data from multiple major tickers (BTC, ETH, and Perpetual Contracts).

Function: Calculates "Market Health." If Bitcoin is rising but the rest of the market is dumping, this module can veto a trade.

Module 7: Directional Index Convergence (DIC)

Logic: Analyzes the convergence/divergence between Fast and Slow Directional Movement indices.

Function: Identifies when trend strength is expanding.

Module 8: Market Thrust Indicator (MTI)

Logic: A volume-weighted breadth indicator using Advance/Decline and Volume data.

Function: One of the most powerful modules. Confirms that price movement is supported by actual volume flow. Recommended setting: "SSMA" (Super Smoother).

Module 9: Simple Ichimoku Cloud

Logic: Traditional Japanese trend analysis.

Function: Checks for a "Kumo Breakout." Price must be fully above/below the Cloud to confirm entry.

Module 10: Simple Harmonic Oscillator

Logic: Analyzes harmonic wave properties to detect cyclical tops and bottoms.

Function: Serves as a counter-trend or early-reversal detector.

Module 11: HSRS Compression / Super AO

Logic: Detects volatility compression (HSRS) or Momentum/Trend confluence (Super AO).

Function: Great for catching explosive moves resulting from consolidation.

Module 12: Fisher Transform (MTF)

Logic: Converts price data into a Gaussian normal distribution.

Function: Identifies extreme price deviations. Uses Multi-Timeframe (MTF) logic to ensure you aren't trading against the major trend.

5. Global Inhibitors (The Veto Power)

Even if 12 out of 12 modules vote "Buy," Gypsy Bot performs a final safety check using Global Inhibitors.

Bitcoin Halving Logic: Prevents trading during chaotic weeks surrounding Halving events (dates projected through 2040).

Miner Capitulation: Uses Hash Rate Ribbons to identify bearish regimes when miners are shutting down.

ADX Filter: Prevents trading in "Flat/Choppy" markets (Low ADX).

CryptoCap Trend: Checks the total Crypto Market Cap chart for broad market alignment.

6. Risk Management & The Dump Protection Team (DPT)

Even in this Indicator version, the RM logic runs to generate Exit Signals.

Dump Protection Team (DPT): Detects "Nuke" (Crash) or "Moon" (Pump) volatility signatures. If triggered, it plots an immediate Exit Signal (Yellow Plot).

Advanced Adaptive Trailing Stop (AATS): Dynamically tightens stops in low volatility ("Dungeon") and loosens them in high volatility ("Penthouse").

Staged Take Profits: Plots TP1, TP2, and TP3 events on the chart for visual confirmation or partial exit alerts.

7. Recommended Setup Guide

When applying Gypsy Bot to a new chart, follow this sequence:

Set Timeframe: 4 Hours (4H).

Tune DPT: Adjust "Dump/Moon Protection" inputs first. These filter out bad signals during high volatility.

Tune Module 8 (MTI): Experiment with the MA Type (SSMA is recommended).

Select Modules: Enable/Disable modules based on the asset's personality (Trending vs. Ranging).

Voting Threshold: Adjust ActivateOrders to filter out noise.

Alert Setup: Once visually satisfied, use the "Any Alert Function Call" option when creating an alert in TradingView to capture all Buy/Sell/Close events generated by the engine.

8. Technical Specs

Engine Version: Pine Script V6

Repainting: This indicator uses Closed Candle data for all Risk Management and Entry decisions. This ensures that signals do not vanish after the candle closes.

Visuals:

Blue Plot: Buy/Sell Signal.

Yellow Plot: Risk Management (RM) / DPT Close Signal.

Green/Lime/Olive Plots: Take Profit hits.

Disclaimer:

This script is a complex algorithmic tool for market analysis. Past performance is not indicative of future results. Cryptocurrency trading involves substantial risk of loss. Use this tool to assist your own decision-making, not to replace it.

9. About Signal Lynx

Automation for the Night-Shift Nation 🌙

Signal Lynx focuses on helping traders and developers bridge the gap between indicator logic and real-world automation. The same RM engine you see here powers multiple internal systems and templates, including other public scripts like the Super-AO Strategy with Advanced Risk Management.

We provide this code open source under the Mozilla Public License 2.0 (MPL-2.0) to:

Demonstrate how Adaptive Logic and structured Risk Management can outperform static, one-layer indicators

Give Pine Script users a battle-tested RM backbone they can reuse, remix, and extend

If you are looking to automate your TradingView strategies, route signals to exchanges, or simply want safer, smarter strategy structures, please keep Signal Lynx in your search.

License: Mozilla Public License 2.0 (Open Source).

If you make beneficial modifications, please consider releasing them back to the community so everyone can benefit.

⚔️ The Scalpel⚔️ THE SCALPEL v2.0

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

Surgical-Grade Market Structure Detection System

🔬 WHAT IS THE SCALPEL?

The Scalpel is a precision-engineered market structure analyzer that identifies and tracks critical support and resistance zones with surgical accuracy. Unlike conventional S&R tools that flood your chart with noise, The Scalpel cuts through the clutter to reveal only the most significant price structures.

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

⚙️ CORE TECHNOLOGY

▸ Pivot-Based Detection Engine

Advanced pivot analysis calibrated by user-defined precision settings

▸ Tissue Integrity Validation

Filters structures based on candle body-to-range ratios

▸ Dynamic Stress Analysis

Tracks zone interactions and removes exhausted levels automatically

▸ Volatility-Adaptive Zones

Zone width scales with ATR for consistent performance across all markets

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

🎨 VISUAL SPECTRUM

💜 STERILE ZONES (Electric Violet)

Fresh, untested structures with maximum potential

🔴 COMPRESSION ZONES (Magenta Fire)

Tested resistance ceilings under selling pressure

🩵 FOUNDATION ZONES (Neon Teal)

Tested support floors with proven buyer interest

✨ PLASMA AURA EFFECT

Multi-layered glow effect for enhanced visibility

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

📐 PARAMETERS

🔪 Blade Precision (1-10)

Higher = fewer but sharper pivots detected

🩺 Tissue Integrity % (30-90)

Minimum candle body percentage required

📏 Incision Depth (0.1-2.0 ATR)

Controls zone thickness based on volatility

💉 Stress Threshold (1-10)

Maximum touches before zone invalidation

📐 Projection Range (10-200)

How far zones extend into the future

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

💡 HOW TO USE

1. Fresh sterile zones (violet) are your highest-probability setups

2. Watch for price reaction at zone boundaries

3. Tested zones confirm structure but may have diminished strength

4. Zones auto-remove after stress threshold is reached

5. Use projection range to anticipate future tests

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

🎯 BEST FOR

✓ Scalping & Day Trading

✓ Swing Trade Entries

✓ Stop Loss Placement

✓ Take Profit Targeting

✓ Multi-Timeframe Analysis

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

⚠️ DISCLAIMER

This indicator is for educational purposes only. Always conduct your own analysis and use proper risk management. Past performance does not guarantee future results.

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

🏷️ TAGS

support resistance zones SNR pivot points market structure scalping day trading swing trading price action order blocks smart money supply demand technical analysis

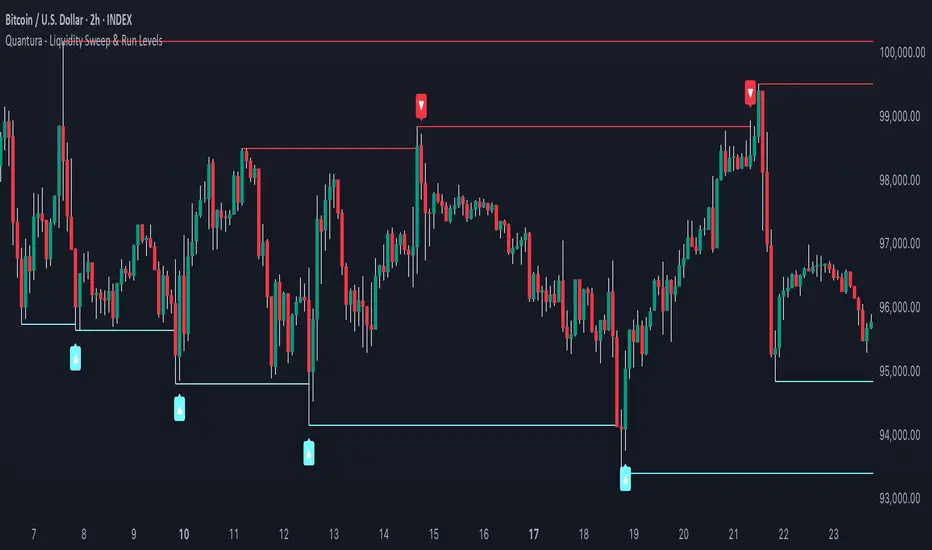

Quantura - Liquidity Sweep & Run LevelsIntroduction

“Quantura – Liquidity Sweep & Run Levels” is a structural price-action indicator designed to automatically detect swing-based liquidity zones and visualize potential sweep and run events. It helps traders identify areas where liquidity has likely been taken (sweep) or released (run), improving precision in market structure analysis and timing of entries or exits.

Originality & Value

This tool translates institutional liquidity concepts into an automated visual framework. Instead of simply marking highs and lows, it dynamically monitors swing points, tracks their breaches, and identifies subsequent reactions. The indicator is built to highlight the liquidity dynamics that often precede reversals or continuations.

Its originality lies in:

Automatic identification and tracking of swing highs and lows.

Real-time detection of broken levels and liquidity sweeps.

Distinction between “Run” and “Sweep” modes for different market behaviors.

Persistent historical visualization of liquidity levels using clean line structures.

Configurable signal markers for bullish and bearish sweep confirmations.

Functionality & Core Logic

Detects swing highs and lows using a user-defined Swing Length parameter.

Stores and updates all swing levels dynamically with arrays for efficient memory handling.

Draws horizontal lines from each detected swing point to visualize potential liquidity zones.

Monitors when price breaks a swing level and marks that event as “broken.”

Generates signals when the market either sweeps above/below or runs away from those levels, depending on the chosen mode.

Provides optional visual signal markers (“▲” for bullish sweeps, “▼” for bearish sweeps).

Parameters & Customization

Mode: Choose between “Sweep” (detects liquidity grabs) or “Run” (detects breakout continuations).

Swing Length: Sets the sensitivity for detecting swing highs/lows. A higher value focuses on larger structures, while smaller values detect micro liquidity points.

Bullish Color / Bearish Color: Customize color themes for sweep/run lines and signal markers.

Signals: Enables or disables visual up/down markers for confirmed events.

Visualization & Display

Horizontal lines represent potential liquidity levels (unbroken swing highs/lows).

Once broken, lines automatically stop extending, marking the moment liquidity is taken.

Depending on the selected mode:

“Sweep” mode identifies false breaks or stop-hunt behavior.

“Run” mode highlights breakouts that continue the trend.

Colored arrows indicate the direction and type of liquidity reaction.

Clean, non-intrusive visualization suitable for overlaying on price charts.

Use Cases

Detect liquidity sweeps before major reversals.

Identify breakout continuations after liquidity runs.

Combine with Supply/Demand or FVG indicators for multi-layered confirmation.

Validate liquidity bias in algorithmic or discretionary strategies.

Analyze market manipulation patterns and institutional stop-hunting behavior.

Limitations & Recommendations

This indicator identifies structural behavior but does not guarantee trade direction or profitability.

Works best on liquid markets with clear swing structures (e.g., crypto, forex, indices).

Signal interpretation should be combined with confluence tools such as volume, order flow, or structure-based filters.

Excessively small swing settings may cause over-signaling in volatile markets.

Markets & Timeframes

Optimized for all major asset classes — including crypto, Forex, indices, and equities — and for intraday to higher-timeframe structural analysis (5-minute up to daily charts).

Author & Access

Developed 100% by Quantura. Published as a Open-source script indicator. Access is free.

Compliance Note

This description fully complies with TradingView’s Script Publishing Rules and House Rules . It avoids performance claims, provides transparency on methodology, and clearly describes indicator behavior and limitations.

Ornstein-Uhlenbeck Trend Channel [BOSWaves]Ornstein-Uhlenbeck Trend Channel - Adaptive Mean Reversion with Dynamic Equilibrium Geometry

Overview

The Ornstein-Uhlenbeck Trend Channel introduces an advanced equilibrium-mapping framework that blends statistical mean reversion with adaptive trend geometry. Traditional channels and regression bands react linearly to volatility, often failing to capture the natural rhythm of price equilibrium. This model evolves that concept through a dynamic reversion engine, where equilibrium adapts continuously to volatility, trend slope, and structural bias - forming a living channel that bends, expands, and contracts in real time.

The result is a smooth, equilibrium-driven representation of market balance - not just trend direction. Instead of static bands or abrupt slope shifts, traders see fluid, volatility-aware motion that mirrors the natural pull-and-release dynamic of market behavior. Each channel visualizes the probabilistic boundaries of fair value, showing where price tends to revert and where it accelerates away from its statistical mean.

Unlike conventional envelopes or Bollinger-type constructs, the Ornstein-Uhlenbeck framework is volatility-reactive and equilibrium-sensitive, providing traders with a contextual map of where price is likely to stabilize, extend, or exhaust.

Theoretical Foundation

The Ornstein-Uhlenbeck Trend Channel is inspired by stochastic mean-reversion processes - mathematical models used to describe systems that oscillate around a drifting equilibrium. While linear regression channels assume constant variance, financial markets operate under variable volatility and shifting equilibrium points. The OU process accounts for this by treating price as a mean-seeking motion governed by volatility and trend persistence.

At its core are three interacting components:

Equilibrium Mean (μ) : Represents the evolving balance point of price, adjusting to directional bias and volatility.

Reversion Rate (θ) : Defines how strongly price is pulled back toward equilibrium after deviation, capturing the self-correcting nature of market structure.

Volatility Coefficient (σ) : Controls how far and how quickly price can diverge from equilibrium before mean reversion pressure increases.

By embedding this stochastic model inside a volatility-adjusted framework, the system accurately scales across different markets and conditions - maintaining meaningful equilibrium geometry across crypto, forex, indices, or commodities. This design gives traders a mathematically grounded yet visually intuitive interpretation of dynamic balance in live market motion.

How It Works

The Ornstein-Uhlenbeck Trend Channel is constructed through a structured multi-stage process that merges stochastic logic with volatility mechanics:

Equilibrium Estimation Core : The indicator begins by identifying the evolving mean using adaptive smoothing influenced by trend direction and volatility. This becomes the live centerline - the statistical anchor around which price naturally oscillates.

Volatility Normalization Layer : ATR or rolling deviation is used to calculate volatility intensity. The output scales the channel width dynamically, ensuring that boundaries reflect current variance rather than static thresholds.

Directional Bias Engine : EMA slope and trend confirmation logic determine whether equilibrium should tilt upward or downward. This creates asymmetrical channel motion that bends with the prevailing trend rather than staying horizontal.

Channel Boundary Construction : Upper and lower bands are plotted at volatility-proportional distances from the mean. These envelopes form the “statistical pressure zones” that indicate where mean reversion or acceleration may occur.

Signal and Lifecycle Control : Channel breaches, mean crossovers, and slope flips mark statistically significant events - exhaustion, continuation, or rebalancing. Older equilibrium zones gradually fade, ensuring a clear, context-aware visual field.

Through these layers, the channel forms a continuously updating equilibrium corridor that adapts in real time - breathing with the market’s volatility and rhythm.

Interpretation

The Ornstein-Uhlenbeck Trend Channel reframes how traders interpret balance and momentum. Instead of viewing price as directional movement alone, it visualizes the constant tension between trending force and equilibrium pull.

Uptrend Phases : The equilibrium mean tilts upward, with price oscillating around or slightly above the midline. Upper band touches signal momentum extension; lower touches reflect healthy reversion.

Downtrend Phases : The mean slopes downward, with upper-band interactions marking resistance zones and lower bands acting as reversion boundaries.

Equilibrium Transitions : Flat mean sections indicate balance or distribution phases. Breaks from these neutral zones often precede directional expansion.

Overextension Events : When price closes beyond an outer boundary, it marks statistically significant disequilibrium - an early warning of exhaustion or volatility reset.

Visually, the OU channel translates volatility and equilibrium into structured geometry, giving traders a statistical lens on trend quality, reversion probability, and volatility stress points.

Strategy Integration

The Ornstein-Uhlenbeck Trend Channel integrates seamlessly into both mean-reversion and trend-continuation systems:

Trend Alignment : Use mean slope direction to confirm higher-timeframe bias before entering continuation setups.

Reversion Entries : Target rejections from outer bands when supported by volume or divergence, capturing snapbacks toward equilibrium.

Volatility Breakout Mapping : Monitor boundary expansions to identify transition from compression to expansion phases.

Liquidity Zone Confirmation : Combine with BOS or order-block indicators to validate structural zones against equilibrium positioning.

Momentum Filtering : Align with oscillators or volume profiles to isolate equilibrium-based pullbacks with statistical context.

Technical Implementation Details

Core Engine : Stochastic Ornstein-Uhlenbeck process for continuous mean recalibration.

Volatility Framework : ATR- and deviation-based scaling for dynamic channel expansion.

Directional Logic : EMA-slope driven bias for adaptive mean tilt.

Channel Composition : Independent upper and lower envelopes with smoothing and transparency control.

Signal Structure : Alerts for mean crossovers and boundary breaches.

Performance Profile : Lightweight, multi-timeframe compatible implementation optimized for real-time responsiveness.

Optimal Application Parameters

Timeframe Guidance:

1 - 5 min : Reactive equilibrium tracking for short-term scalping and microstructure analysis.

15 - 60 min : Medium-range setups for volatility-phase transitions and intraday structure.

4H - Daily : Macro equilibrium mapping for identifying exhaustion, distribution, or reaccumulation zones.

Suggested Configuration:

Mean Length : 20 - 50

Volatility Multiplier : 1.5× - 2.5×

Reversion Sensitivity : 0.4 - 0.8

Smoothing : 2 - 5

Parameter tuning should reflect asset liquidity, volatility, and desired reversion frequency.

Performance Characteristics

High Effectiveness:

Trending environments with cyclical pullbacks and volatility oscillation.

Markets exhibiting consistent equilibrium-return behavior (indices, majors, high-cap crypto).

Reduced Effectiveness:

Low-volatility consolidations with minimal variance.

Random walk markets lacking definable equilibrium anchors.

Integration Guidelines

Confluence Framework : Pair with BOSWaves structural tools or momentum oscillators for context validation.

Directional Control : Follow mean slope alignment for directional conviction before acting on channel extremes.

Risk Calibration : Use outer band violations for controlled contrarian entries or trailing stop management.

Multi-Timeframe Synergy : Derive macro equilibrium zones on higher timeframes and refine entries on lower levels.

Disclaimer

The Ornstein-Uhlenbeck Trend Channel is a professional-grade equilibrium and volatility framework. It is not predictive or profit-assured; performance depends on parameter calibration, volatility regime, and disciplined execution. BOSWaves recommends using it as part of a comprehensive analytical stack combining structure, liquidity, and momentum context.

One Shot One Kill ICT [TradingFinder] Liquidity MMXM + CISD OTE🔵 Introduction

The One Shot One Kill trading setup is one of the most advanced methods in the field of Smart Money Concept (SMC) and ICT. Designed with a focus on concepts such as Liquidity Hunt, Discount Market, and Premium Market, this strategy emphasizes precise Price Action analysis and market structure shifts. It enables traders to identify key entry and exit points using a structured Trading Model.

The core process of this setup begins with a Liquidity Hunt. Initially, the price targets areas like the Previous Day High and Previous Day Low to absorb liquidity. Once the Change in State of Delivery(CISD)is broken, the market structure shifts, signaling readiness for trade entry. At this stage, Fibonacci retracement levels are drawn, and the trader enters a position as the price retraces to the 0.618 Fibonacci level.

Part of the Smart Money approach, this setup combines liquidity analysis with technical tools, creating an opportunity for traders to enter high-accuracy trades. By following this setup, traders can identify critical market moves and capitalize on reversal points effectively.

Bullish :

Bearish :

🔵 How to Use

The One Shot One Kill setup is a structured and advanced trading strategy based on Liquidity Hunt, Fibonacci retracement, and market structure shifts (CISD). With a focus on precise Price Action analysis, this setup helps traders identify key market movements and plan optimal trade entries and exits. It operates in two scenarios: Bullish and Bearish, each with distinct steps.

🟣 Bullish One Shot One Kill

In the Bullish scenario, the process starts with the price moving toward the Previous Day Low, where liquidity is absorbed. At this stage, retail sellers are trapped as they enter short trades at lower levels. Following this, the market reverses upward and breaks the CISD, signaling a shift in market structure toward bullishness.

Once this shift is identified, traders draw Fibonacci levels from the lowest point to the highest point of the move. When the price retraces to the 0.618 Fibonacci level, conditions for a buy position are met. The target for this trade is typically the Previous Day High or other significant liquidity zones where major buyers are positioned, offering a high probability of price reversal.

🟣 Bearish One Shot One Kill

In the Bearish scenario, the price initially moves toward the Previous Day High to absorb liquidity. Retail buyers are trapped as they enter long trades near the highs. After the liquidity hunt, the market reverses downward, breaking the CISD, which signals a bearish shift in market structure. Following this confirmation, Fibonacci levels are drawn from the highest point to the lowest point of the move.

When the price retraces to the 0.618 Fibonacci level, a sell position is initiated. The target for this trade is usually the Previous Day Low or other key liquidity zones where major sellers are active.

This setup provides a precise and logical framework for traders to identify market movements and enter trades at critical reversal points.

🔵 Settings

🟣 CISD Logical settings

Bar Back Check : Determining the return of candles to identify the CISD level.

CISD Level Validity : CISD level validity period based on the number of candles.

🟣 LIQUIDITY Logical settings

Swing period : You can set the swing detection period.

Max Swing Back Method : It is in two modes "All" and "Custom". If it is in "All" mode, it will check all swings, and if it is in "Custom" mode, it will check the swings to the extent you determine.

Max Swing Back : You can set the number of swings that will go back for checking.

🟣 CISD Display settings