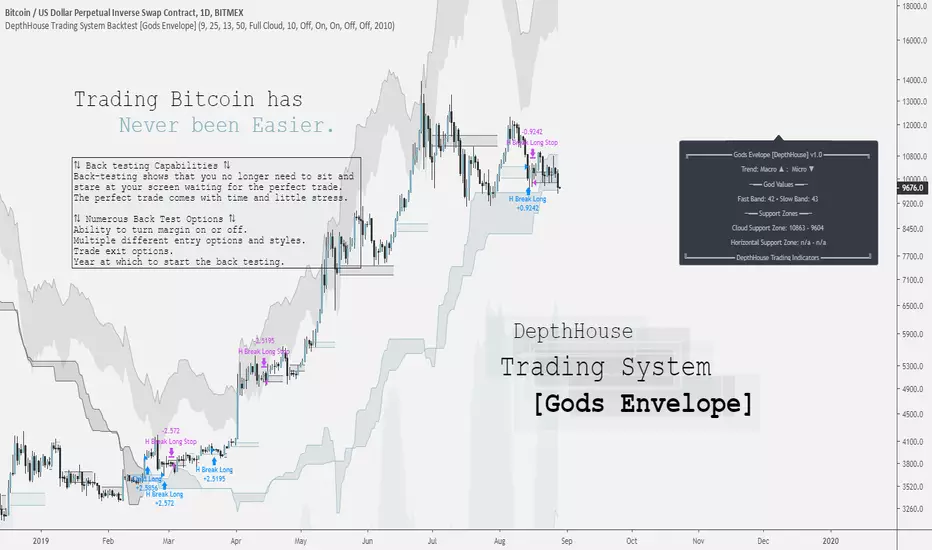

DepthHouse Trading System [Gods Envelope] Backtest StrategyCreated for Bitcoin!

*All testing has been done on the 1 Day time frame of BTC USD pairs.

Use at your own risk.

DepthHouse Trading System Basics

The Cloud:

The cloud is used in a very similar manner as the ichimoku cloud. A complete cross above or below the represents a macro trend change. The cloud then could be used as dynamic support and resistance zones.

By default there is no smoothing to the full cloud. If you wish to add smoothing, you can change the ‘Trend Base On’ option to ‘Modded Cloud Average’ to add price action and smoothing into the cloud’s calculations. The Modded Cloud can then be used in the same manner as the Full Cloud. Generally, the Full Cloud is more forgiving and has less Macro Trend changes. By default, this option is turned off. The support or resistance zone created will be shown on the info panel on the right.

Horizontal Levels:

A Horizonal zone is generated each time there is a micro level trend change. For example, as soon as a positive micro trend change occurs a green horizontal level will be plotted.

These levels then can be used as temporary support and resistance zones. The Horizontal Break Trading Strategy is entirely based on these levels. These levels are also shown on the info panel on the right.

The Envelope Itself: (by default this is off)

By selecting the Overbought and Oversold Ranges option, a cloud envelope will appear around the price action. This envelope represents the overbought and oversold ranges. If the price action should go into these zones, the info panel on the right will show ‘CAUTION’ beside the God Values as this signals that the pair is either overbought or oversold.

The God Values:

The God values are listed on the info panel on the right. These are the values created by the Godmode indicator. Generally, below 20 or above 80 it signals for caution as the price action has overextended itself.

The Back-Test Strategy Options:

⇅ - Child Fomo Positioning:

Child Fomo Positioning strategy is entirely based on the macro trend change with the center cloud. As soon as there is a complete candle close above or below the cloud and a trend change takes place. The back-test places a market order as soon as the next candle opens. By default, it then will not close this position until the price action fully crosses the cloud once again.

⇅ - Horizontal Break Trading:

Horizontal Break Trading Strategy is entirely based on the horizontal levels generated and the macro trend direction. For example, say the Macro Trend is up, and a green, positive horizontal level is formed. As soon as a complete candle closes above the upper level of the positive zone, a limit order is placed in hope that the price action comes back down and retests, filling the order. This long will not close then until a negative level is formed. As soon as a negative level is formed a stop/loss order is placed on the lower level of the horizontal support zone. It will then do the opposite in a bearish trend, and margin trading is turned on.

⇅ - Parent Positions :

Parent Positioning Strategy is based on the overall trend and the center cloud levels. This strategy has limit orders waiting on the level of the cloud that is closest to the price action. Therefore, using this strategy alone, the back-test system waits for the trend to be confirmed, and then follows the price action with limit orders waiting on the cloud to be retested. By default this order does not close until a Marco trend change occurs.

⇅ - Take 50% Partial Profits:

This options allows the back-test to take 50% profit or loss when one of the two options occur.

Horizontal Break: This would close 50% of the position in the same manner it would close a trade using the horizontal break trading system.

God Values: Once the price action enters the oversold or overbought clouds, it would then place a close order as soon as the price action exits the cloud.

⟲ - Backtest Year Start Date :

Start year of the back-testing. If set to ex. 2017, the back-test will not calculate any trades that took place before Jan. 1 of 2017.

⚖ - Margin Trading :

By default, margin trading is turned off. Simply switch this option to on the enable ‘Short Trading’ into the strategy back-test.

Notes: If you are back testing multiple strategies at the same time, you must increase the pyramiding to correspond to the number or strategies.

My Favorite Settings:

Margin = Off

Pyramiding = 2 [Settings → Properties → Pyramiding → 2 orders

Child Fomo Positioning = On

Horizontal Break Trading = On

Everything else off 😊

DISCLAIMER: Past performance does not guarantee future results.

Use at your own risk.

חפש סקריפטים עבור "range"

COIN strategy 1.0COIN strategy 1.0

Features:

Bright & Dark theme option. Choose the type that you can see clearly.

Auto finds potential Buy & Sell point.

Compatible with all time ranges.

Best accuracy for daily charts .

Helpful for Crypto/Stock/Forex

Application:

The source of this indicator is protected now for safety.

I'll appoint several followers who are active under my published ideas to evaluate this indicator.

Getting Started:

1. Add this script to your chart.

2. Try to switch to short/medium/long time ranges to find signals.

3. When there are more than two periods reported the same buy/sell signals, it would be a trustful one.

Contributing:

You can report bugs or issues under this script publication page.

Any advice would be helpful for improving this indicator's accuracy.

Invite only for valuation now.

Net Profit(净利润)

$ 137260.80

6863.04 %

Percent Profitable(胜率)

97.56 %

Max Drawdown(最大回撤)

$ 380.00

1.06 %

15分钟线共交易66笔

下面是中文介绍

特征:

明暗主题选项。 选择您可以清楚看到的类型。

Auto发现潜在的买入和卖出点。

兼容所有时间范围。

日常图表的最佳准确度。

对Crypto / Stock / Forex有帮助

应用:

为了安全起见,该指标的来源现在受到保护。

我会根据我发表的想法指定几位活跃的粉丝来评估这个指标。

入门:

1.将此脚本添加到图表中。

2.尝试切换到短/中/长时间范围以查找信号。

3.当有两个以上的期间报告相同的买入/卖出信号时,它将是一个信任的。

OKCOIN:ETHUSD1W 现在仅邀请进行评估。

DR/IDR Break .5 TPDR/IDR Extension Breakout with Custom Stop

This strategy is a systematic, counter-trend, and momentum-based system designed for intraday trading. It operates on the principle of an Opening Range Breakout (ORB), utilizing the initial market consolidation to project high-probability targets, while offering multiple methods for managing risk.

1. Market Identification (The Opening Range)

The strategy begins by defining the market's initial boundaries and volatility:

Session Window: The strategy calculates the Opening Range (OR) over a user-defined time period (default: 9:30 AM to 10:30 AM New York Time).

ORB Levels: Two key price levels are established and locked once the time window closes:

Wick High/Low: The absolute highest and lowest prices of the session. These serve as the entry trigger lines.

Body High/Low (Shaded Range): The highest and lowest open/close prices of the session. The height of this range is used to calculate the Take Profit and Stop Loss levels.

2. Entry Rule (The Breakout)

The strategy is passive until the range is violated, looking for a strong move out of the consolidation area.

Trigger Condition: A trade is signaled when a candle closes either:

Above the Wick High (for a Long entry).

Below the Wick Low (for a Short entry).

Execution: The entry is a Market Order executed on the candle that meets the trigger condition, subject to a user-defined Entry Delay (default 0 bars, meaning the entry is taken immediately upon the breakout candle's close).

Direction Control: The user can select to trade Long Only, Short Only, or Both.

3. Exit and Risk Management

All trades are placed with simultaneous Take Profit and Stop Loss orders (a bracket order) once the entry is filled.

A. Take Profit (TP)

The Take Profit is set at the 0.5 Extension of the Shaded Range (Body Range).

Calculation: The distance from the Body High/Low to the TP level is exactly 50% of the total height of the Shaded Range.

B. Stop Loss (SL)

The Stop Loss is dynamically calculated based on a user-selected method for risk control:

Range 0.5 (Body Range): The Stop Loss is placed an equal distance (0.5 times the Body Range height) outside the opposite side of the Body Range.

Example (Long): If entry is above the Wick High, the SL is set 0.5 times the Body Range height below the Body Low.

ATR Multiple: The Stop Loss distance is determined by the asset's recent volatility.

Calculation: The distance is calculated as a user-defined Multiplier (default 2.0) times the Average True Range (ATR).

Recent Swing Low/High: The Stop Loss is placed based on a structural level defined by recent price action.

Long Entry: SL is placed at the Lowest Swing Low within a user-defined lookback period.

Short Entry: SL is placed at the Highest Swing High within a user-defined lookback period.

Summary of Workflow

The market sets the Wick and Body boundaries (e.g., 9:30–10:30 AM).

Price breaks and closes beyond a Wick boundary, triggering a signal.

The trade enters after the specified delay.

A bracket order is placed: TP is fixed at the 0.5 Extension, and SL is set based on the user's chosen risk method.

The trade is closed upon reaching either the TP or the SL level.

Strategy Builder Pro [ChartPrime]ChartPrime Strategy Creator Overview

The ChartPrime Strategy Builder offers traders an innovative, structured approach to building and testing strategies. The Strategy Creator allows users to combine, test, and automate complex strategies with many parameters.

Key Features of the ChartPrime Strategy Builder

1. Customizable Buy and Sell Conditions

The Strategy Creator provides flexibility in establishing entry and exit rules, with separate sections for long and short strategies. Traders can combine multiple conditions in each section to fine-tune when positions are opened or closed. For instance, they might choose to only buy when the indicator signals a buy and the Dynamic Reactor (a low lag filter) indicator shows a bullish trend. Users are able to pick, mix and match the following list of features:

Signal Mode: Select the type of assistive signals you are requiring. Provided are both trend following signals with self optimization using backtest results as well as reversal signals, aiming to provide real time tops and bottoms in markets. Both these signal modes can be fine tuned using the tuning input to refine signals to a trader's liking. ChartPrime Trend Signals leverage audio engineering inspired techniques and low-pass filters in order to achieve and attempt to produce lower lag response times and therefore are designed to have a uniqueness when compared to more classical trend following approaches.

The Dynamic Reactor: provides a simple band passing through the chart. This can provide assistance in support and resistance locations as well as identifying the trend direction expressed via green and red colors. Taking a moving average and applying unique adaptivity calculations gives this plot a unique and fast behavior.

Candlestick structures: analyze candlestick formation putting a spin on classical candlestick patterns and provide the most relevant formations on the chart. These are not classical and are filtered by further analyzing market activity. A trader's classic with a spin.

The Prime Trend Assistant: provides a trend following dynamic support and resistance level. This makes it perfect to use in confluence or as a filter for other supporting indicators. This is an adaptive trend following system designed to handle volatility leveraging filter kernels as opposed to low pass filters.

Money Flow: with further filters applied for early response to money flow changes in the market. This can be a great filter in trends.

Oscillator reversals: are built in leveraging an oscillator focusing on market momentum allowing users to enter based on market shifts and trends along with reversals.

Volume-Inspired Signals: determine overbought and oversold conditions, adding another layer of analysis to the oscillator. These appear as orange labels, providing a simple reading into a possible reversal.

The Volume Matrix: is a volume oscillator that shows whether money is flowing into or out of the market. Green suggests an uptrend with buyers in control, while red indicates a majority of sellers. By incorporating smoothed volume analysis, it distinguishes between bullish and bearish volumes, offering an early indication of potential trend reversals.

The True 7: is a middle-ranking system that evaluates the strength of a move and the overall trend, offering a numeric or visual representation of trend strength. It can also indicate when a trend is starting to reverse, providing leading signals for potential market shifts. Rather than using an oscillator, this offers the unique edge of falling into set categories, making understanding it simple. This can be a great confluence point when designing a strategy.

Take profits: These offer real-time suggestions from our algorithm on when it might be a good time to take profit. Using these as part of a strategy allows for great entries at bottoms and tops of trends.

Using features such as the Dynamic reactor have dual purposes. Traders can use this as both a filter and an entry condition. This allows for true interoperability when using the Strategy Builder. The above conditions are duplicated for short entries too allowing for symmetrical trading systems. By disabling all of the entry conditions on either long or short areas of the settings will create a strategy that only takes a single type of position. For example; a trader that just wants to take longs can disable all short options.

2. Layered Entries

Layered entries, a feature to enhance the uniqueness in the tool. It allows traders to average into positions as the market moves, rather than committing all capital at once. This feature is particularly useful for volatile markets where prices may fluctuate substantially. The Strategy Builder lets users adjust the number of layered entries, which can help in managing risk and optimizing entry points as well as the aggressiveness of the safety orders. With each safety order placed the system will automatically and dynamically scale into positions reducing the average entry price and hence dynamically adjust the potential take profits. Due to the potential complexities of exiting during multiple orders, a smart system is employed to automatically take profits on the layered system aiming to take profits at peaks of trends.

Users are able to override this smart TP system at the bottom of the settings instead targeting percentage profits for both short and long positions.

Entries lowering average buy price

The ability to adjust how quickly the system layers into positions can also be adjusted via the layered entries drop down between fast and slow mode where the slow mode will be more cautious when producing new orders.

3. Flexible Take Profit (TP) and Stop Loss (SL) Options

Traders can set their TP and SL levels according to various parameters, including ATR (Average True Range), risk-reward ratio, trailing stops, or specific price changes. If layered entries are active, an automatic TP method is applied by default, though traders can manually specify TP values if they prefer. This setup allows for precise control over trade exits, tailored to the strategy’s risk profile.

Provided options

The ability to use external take profits and stop losses is also provided. By loading an indicator of your choice the plots will be added to the chart. By navigating to the external sources area of the settings, users can select this plot and use it as part of a wider trading system.

Example: Let’s say a user has entries based on the inbuilt trend signals and wishes to exit whenever the RSI crosses above 70, they can add RSI to the chart, select crossing up and enter the value of 70.

4. Integrated Reinvestment for Compounding Gains

The reinvestment option allows traders to reinvest a portion of their gains into future trades, increasing trade size over time and benefiting from compounding. For example, a user might set 30% of each trade's profit to reinvest, with the remaining 70% allocated for risk management or additional safety orders. This approach can enhance long-term growth while balancing risk.

Generally in trading it can be a good approach to take profits so we suggest a healthy balance. This setting is generally best used for slow steady strategies with the long term aim of accumulating as much of the asset as possible.

5. Leverage and Position Sizing

Users can configure leverage and position sizing to simulate varying risk levels and capital allocations. A dashboard on the interface displays margin requirements based on the selected leverage, allowing traders to estimate trade sizes relative to their available capital. Whenever using leverage especially with layered entries it’s important to keep a close eye on the position sizes to avoid potential liquidations.

6. Pre-Configured Strategies for Immediate Testing

For users seeking a starting point, ChartPrime includes a range of preset strategies. These were developed and backtested by ChartPrime’s team. This allows traders to start with a stable base and adapt it to their own preferences. It is vital to understand that historical performance doesn't guarantee future success, and traders should be mindful of overfitting. These pre-built configurations offer a structured way and base to design strategies off of. These are also subject to changing results as new price action arrives and they become outdated. They serve the purpose of simply being example use cases.

7. In-Depth Specific Backtesting Ranges

The Strategy Builder includes backtesting capabilities, providing a clear view of how different setups would have performed over specified time periods. Traders can select date ranges to target specific market conditions, then review results on TradingView to see how their strategies perform across different market trends.

Example Use Case: Developing a Strategy

Consider a trader who is focused on long positions only and prefers a lower-risk strategy (note these tools can be used for all assets; we are using an undisclosed asset as an example). Using the Strategy Builder, they could:

- Disable short conditions.

- Set long entry rules to trigger when both the ChartPrime oscillator and Quantum Reactor indicators show bullish signals.

- Enable layered entries to improve average entry prices by adding to positions during market dips.

- Run a backtest over a two-year period to see historical performance trends, making adjustments as needed.

The backtest will show where entries and exits would have occurred and how layered entries may have impacted profitability.

8. Iterative design

Strategy builders and creating a strategy is often an iterative process. By experimenting and using logic; a trader can arrive at a more sustainable system. Analyzing the shortcomings of your strategy and iteratively designing and filtering them out is the goal. For example; let’s say a strategy has high drawdown, a user would want to tighten stop losses for example to reduce this and find a balance point between optimizing winning trades and reducing the drawdown. When designing a strategy there are generally tradeoffs and optimizing taking into consideration a wide range of factors is key. This also applies to filtering techniques, entries and exits and every variable in the strategy.

Let’s say a strategy was taking too many long positions in a downtrend and after you’ve analyzed the data, you come to the conclusion this needs to be solved. Filtering these using built in trend following tools can be a great approach and refining with logic is a great approach.

The Strategy Builder also takes into consideration those who seek to automate especially via reinvesting and leverage features.

Considerations

The ChartPrime Strategy Builder aims to help traders build clear, rule-based strategies without excessive complexity. As with all backtesting tools, it's crucial to understand that historical performance doesn't guarantee future success, and traders should be mindful of overfitting. This tool offers a structured way to test strategies against various market conditions, helping traders refine their approaches with data-driven insights. Traders should also ensure they enter the correct fees when designing strategies and ensure usage on standard candle types.

Gabriel's Witcher Strategy [65 Minute Trading Bot]Strategy Description: Gabriel's Witcher Strategy

Author: Gabriel

Platform: TradingView Pine Script (Version 5)

Backtested Asset: Avalanche (Coinbase Brokage for Volume adjustment)

Timeframe: 65 Minutes

Strategy Type: Comprehensive Trend-Following and Momentum Strategy with Scalping and Risk Management Features

Overview

Gabriel's Witcher Strategy is an advanced trading bot designed for the Avalanche pair on a 65-minute timeframe. This strategy integrates a multitude of technical indicators to identify and execute high-probability trading opportunities. By combining trend-following, momentum, volume analysis, and range filtering, the strategy aims to capitalize on both long and short market movements. Additionally, it incorporates scalping mechanisms and robust risk management features, including take-profit (TP) levels and commission considerations, to optimize trade performance and profitability.

====Key Components====

Source Selection:

Custom Source Flexibility: Allows traders to select from a wide range of price and volume sources (e.g., Close, Open, High, Low, HL2, HLC3, OHLC4, VWAP, On-Balance Volume, etc.) for indicator calculations, enhancing adaptability to various trading styles.

Various curves of Volume Analysis are employed:

Tick Volume Calculation: Utilizes tick volume as a fallback when actual volume data is unavailable, ensuring consistency across different data feeds.

Volume Indicators: Incorporates multiple volume-based indicators such as On-Balance Volume (OBV), Accumulation/Distribution (AccDist), Negative Volume Index (NVI), Positive Volume Index (PVI), and Price Volume Trend (PVT) for comprehensive market analysis.

Trend Indicators:

ADX (Average Directional Index): Measures trend strength using either the Classic or Masanakamura method, with customizable length and threshold settings. It's used to open positions when the mesured trend is strong, or exit when its weak.

Jurik Moving Average (JMA): A smooth moving average that reduces lag, configurable with various parameters including source, resolution, and repainting options.

Parabolic SAR: Identifies potential reversals in market trends with adjustable start, increment, and maximum settings.

Custom Trend Indicator: Utilizes highest and lowest price points over a specified timeframe to determine current and previous trend bases, visually represented with color-filled areas.

Momentum Indicators:

Relative Strength Index (RSI): Evaluates the speed and change of price movements, smoothed with a custom length and source. It's used to not enter the market for shorts in oversold or longs for overbought conditions, and to enter for long in oversold or shorts for overboughts.

Momentum-Based Calculations: Employs both Double Exponential Moving Averages (DEMA) on a MACD-based RSI to enhance momentum signal accuracy which is then further accelerated by a Hull MA. This is the technical analysis tool that determines bearish or bullish momentum.

OBV-Based Momentum Conditions: Uses two exponential moving averages of OBV to determine bullish or bearish momentum shifts, anomalities, breakouts where banks flow their funds in or Smart Money Concepts trade.

Moving Averages (MA):

Multiple MA Types: Includes Simple Moving Average (SMA), Exponential Moving Average (EMA), Weighted Moving Average (WMA), Hull Moving Average (HMA), and Volume-Weighted Moving Average (VWMA), selectable via input parameters.

MA Speed Calculation: Measures the percentage change in MA values to determine the direction and speed of the trend.

Range Filtering:

Variance-Based Filter: Utilizes variance and moving averages to filter out trades during low-volatility periods, enhancing trade quality.

Color-Coded Range Indicators: Visualizes range filtering with color changes on the chart for quick assessment.

Scalping Mechanism:

Heikin-Ashi Candles: Optionally uses Heikin-Ashi candles for smoother price action analysis.

EMA-Based Trend Detection: Employs fast, medium, and slow EMAs to determine trend direction and potential entry points.

Fractal-Based Filtering: Detects regular or BW (Black & White) fractals to confirm trade signals.

Take Profit (TP) Management:

Dynamic TP Levels: Calculates TP levels based on the number of consecutive long or short entries, adjusting targets to maximize profits.

TP Signals and Re-Entry: Plots TP signals on the chart and allows for automatic re-entry upon TP hit, maintaining continuous trade flow.

Risk Management:

Commission Integration: Accounts for trading commissions to ensure net profitability.

Position Sizing: Configured to use a percentage of equity for each trade, adjustable via input parameters.

Pyramiding: Allows up to one additional position per direction to enhance gains during strong trends.

Alerts and Visual Indicators:

Buy/Sell Signals: Plots visual indicators (triangles and flags) on the chart to signify entry and TP points.

Bar Coloring: Changes bar colors based on ADX and trend conditions for immediate visual cues.

Price Levels: Marks significant price levels related to TP and position entries with cross styles.

Input Parameters

Source Settings:

Custom Sources (srcinput): Choose from various price and volume sources to tailor indicator calculations.

ADX Settings:

ADX Type (ADX_options): Select between 'CLASSIC' and 'MASANAKAMURA' methods.

ADX Length (ADX_len): Defines the period for ADX calculation.

ADX Threshold (th): Sets the minimum ADX value to consider a strong trend.

RSI Settings:

RSI Length (len_3): Period for RSI calculation.

RSI Source (src_3): Source data for RSI.

Trend Strength Settings:

Channel Length (n1): Period for trend channel calculation.

Average Length (n2): Period for smoothing trend strength.

Jurik Moving Average (JMA) Settings:

JMA Source (inp): Source data for JMA.

JMA Resolution (reso): Timeframe for JMA calculation.

JMA Repainting (rep): Option to allow JMA to repaint.

JMA Length (lengths): Period for JMA.

Parabolic SAR Settings:

SAR Start (start): Initial acceleration factor.

SAR Increment (increment): Acceleration factor increment.

SAR Maximum (maximum): Maximum acceleration factor.

SAR Point Width (width): Visual width of SAR points.

Trend Indicator Settings:

Trend Timeframe (timeframe): Period for trend indicator calculations.

Momentum Settings:

Source Type (srcType): Select between 'Price' and 'VWAP'.

Momentum Source (srcPrice): Source data for momentum calculations.

RSI Length (rsiLen): Period for momentum RSI.

Smooth Length (sLen): Smoothing period for momentum RSI.

OBV Settings:

OBV Line 1 (e1): EMA period for OBV line 1.

OBV Line 2 (e2): EMA period for OBV line 2.

Moving Average (MA) Settings:

MA Length (length): Period for MA calculations.

MA Type (matype): Select MA type (1: SMA, 2: EMA, 3: HMA, 4: WMA, 5: VWMA).

Range Filter Settings:

Range Filter Length (length0): Period for range filtering.

Range Filter Multiplier (mult): Multiplier for range variance.

Take Profit (TP) Settings:

TP Long (tp_long0): Percentage for long TP.

TP Short (tp_short0): Percentage for short TP.

Scalping Settings:

Scalping Activation (ACT_SCLP): Enable or disable scalping.

Scalping Length (HiLoLen): Period for scalping indicators.

Fast EMA Length (fastEMAlength): Period for fast EMA in scalping.

Medium EMA Length (mediumEMAlength): Period for medium EMA in scalping.

Slow EMA Length (slowEMAlength): Period for slow EMA in scalping.

Filter (filterBW): Enable or disable additional fractal filtering.

Pullback Lookback (Lookback): Number of bars for pullback consideration.

Use Heikin-Ashi Candles (UseHAcandles): Option to use Heikin-Ashi candles for smoother trend analysis.

Strategy Logic

Indicator Calculations:

Volume and Source Selection: Determines the primary data source based on user input, ensuring flexibility and adaptability.

ADX Calculation: Computes ADX using either the Classic or Masanakamura method to assess trend strength.

RSI Calculation: Evaluates market momentum using RSI, further smoothed with custom periods.

Trend Strength Assessment: Utilizes trend channel and average lengths to gauge the robustness of current trends.

Jurik Moving Average (JMA): Smooths price data to reduce lag and enhance trend detection.

Parabolic SAR: Identifies potential trend reversals with adjustable parameters for sensitivity.

Momentum Analysis: Combines RSI with DEMA and OBV-based conditions to confirm bullish or bearish momentum.

Moving Averages: Employs multiple MA types to determine trend direction and speed.

Range Filtering: Filters out low-volatility periods to focus on high-probability trades.

Trade Conditions:

Long Entry Conditions:

ADX Confirmation: ADX must be above the threshold, indicating a strong uptrend.

RSI and Momentum: RSI below 70 and positive momentum signals.

JMA and SAR: JMA indicates an uptrend, and Parabolic SAR is below the price.

Trend Indicator: Confirms the current trend direction.

Range Filter: Ensures market is in an upward range.

Scalping Option: If enabled, additional scalping conditions must be met.

Short Entry Conditions:

ADX Confirmation: ADX must be above the threshold, indicating a strong downtrend.

RSI and Momentum: RSI above 30 and negative momentum signals.

JMA and SAR: JMA indicates a downtrend, and Parabolic SAR is above the price.

Trend Indicator: Confirms the current trend direction.

Range Filter: Ensures market is in a downward range.

Scalping Option: If enabled, additional scalping conditions must be met.

Position Management:

Entry Execution: Places long or short orders based on the identified conditions and user-selected position types (Longs, Shorts, or Both).

Take Profit (TP): Automatically sets TP levels based on predefined percentages, adjusting dynamically with consecutive trades.

Re-Entry Mechanism: Allows for automatic re-entry upon TP hit, maintaining active trading positions.

Exit Conditions: Closes positions when TP levels are reached or when opposing trend signals are detected.

Visual Indicators:

Bar Coloring: Highlights bars in green for bullish conditions, red for bearish, and orange for neutral.

Plotting Price Levels: Marks significant price levels related to TP and trade entries with cross symbols.

Signal Shapes: Displays triangle and flag shapes on the chart to indicate trade entries and TP hits.

Alerts:

Custom Alerts: Configured to notify traders of long entries, short entries, and TP hits, enabling timely trade management and execution.

Usage Instructions

Setup:

Apply the Strategy: Add the script to your TradingView chart set to BTCUSDT with a 65-minute timeframe.

Configure Inputs: Adjust the input parameters under their respective groups (e.g., Source Settings, ADX, RSI, Trend Strength, etc.) to match your trading preferences and risk tolerance.

Position Selection:

Choose Position Type: Use the Position input to select Longs, Shorts, or Both based on your market outlook.

Execution: The strategy will automatically execute and manage positions according to the selected type, ensuring targeted trading actions.

Signal Interpretation:

Buy Signals: Blue triangles below the bars indicate potential long entry points.

Sell Signals: Red triangles above the bars indicate potential short entry points.

Take Profit Signals: Flags above or below the bars signify TP hits for long and short positions, respectively.

Bar Colors: Green bars suggest bullish conditions, red bars indicate bearish conditions, and orange bars represent neutral or consolidating markets.

Risk Management:

Default Position Size: Set to 100% of equity. Adjust the default_qty_value as needed for your risk management strategy.

Commission: Accounts for a 0.1% commission per trade. Adjust the commission_value to match your broker's fees.

Pyramiding: Allows up to one additional position per direction to enhance gains during strong trends.

Backtesting and Optimization:

Historical Testing: Utilize TradingView's backtesting features to evaluate the strategy's performance over historical data.

Parameter Tuning: Optimize input parameters to align the strategy with current market dynamics and personal trading objectives.

Alerts Configuration:

Set Up Alerts: Enable and configure alerts based on the predefined alertcondition statements to receive real-time notifications of trade signals and TP hits.

Additional Features

Comprehensive Indicator Integration: Combines multiple technical indicators to provide a holistic view of market conditions, enhancing trade signal accuracy.

Scalping Options: Offers an optional scalping mechanism to capitalize on short-term price movements, increasing trading flexibility.

Dynamic Take Profit Levels: Adjusts TP targets based on the number of consecutive trades, maximizing profit potential during favorable trends.

Advanced Volume Analysis: Utilizes various volume indicators to confirm trend strength and validate trade signals.

Customizable Range Filtering: Filters trades based on market volatility, ensuring trades are taken during optimal conditions.

Heikin-Ashi Candle Support: Optionally uses Heikin-Ashi candles for smoother price action analysis and reduced noise.

====Recommendations====

Thorough Backtesting:

Historical Performance: Before deploying the strategy in a live trading environment, perform comprehensive backtesting to understand its performance under various market conditions. These are the premium settings for Avalanche Coinbase.

Optimization: Regularly review and adjust input parameters to ensure the strategy remains effective amidst changing market volatility and trends. Backtest the strategy for each crypto and make sure you are in the right brokage when using the volume sources as it will affect the overall outcome of the trading strategy.

Risk Management:

Position Sizing: Adjust the default_qty_value to align with your risk tolerance and account size.

Stop-Loss Implementation: Although the strategy includes TP levels, they're also consided to be a stop-loss mechanisms to protect against adverse market movements.

Commission Adjustment: Ensure the commission_value accurately reflects your broker's fees to maintain realistic backtesting results. Generally, 0.1~0.3% are most of the average broker's comission fees.

Slipage: The slip comssion is 1 Tick, since the strategy is adjusted to only enter/exit on bar close where most positions are available.

Continuous Monitoring:

Strategy Performance: Regularly monitor the strategy's performance to ensure it operates as expected and make adjustments as needed. A max-drawndown hit has been added to operate in case the premium Avalanche settings go wrong, but you can turn it off an adjust the equity percentage to 50% if you are confortable with the high volatile max-drown or even 100% if your account allows you to borrow cash.

Customization:

Indicator Parameters: Tailor indicator settings (e.g., ADX length, RSI period, MA types) to better fit your specific trading style and market conditions.

Scalping Options: Enable or disable scalping based on your trading preferences and risk appetite.

Conclusion

Gabriel's Witcher Strategy is a robust and versatile trading solution designed to navigate the complexities of the Crypto market. By integrating a wide array of technical indicators and providing extensive customization options, this strategy empowers traders to execute informed and strategic trades. Its comprehensive approach, combining trend analysis, momentum detection, volume evaluation, and range filtering, ensures that trades are taken during optimal market conditions. Additionally, the inclusion of scalping features and dynamic take-profit management enhances the strategy's adaptability and profitability potential. Unlike any trading strategy, with both diligent testing and continuous monitoring under the strategy tester, it's possible to achieve sustained success by adjusting the settings to the individual Crypto that need it, for example this one is preset for Avalanche Coinbase 65 Miinutes but it can be adjust for BTCUSD or Etherium if you backtest and search for the right settings.

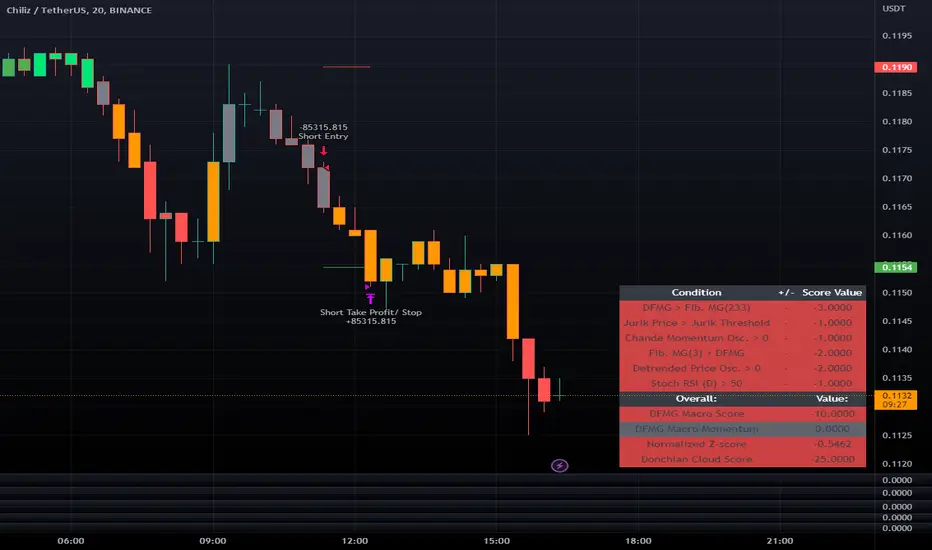

LeafAlgo Premium Macro StrategiesA "macro score", as defined here, is created by giving various weights to different signals and adding them together to get one smooth score. Positive or negative values are assigned to each of the signals depending on if the statement is true or false (e.g. DPO > 0: +1, DPO < 0: -1). This manner of strategy allows for a subset of the available signals to be present at one time as opposed to every technical signal having to be active in order for a long/short signal to trigger.

This strategy contains SIX different macro score strategies -- "Base DFMA", "Base DFMG", "Ichimoku", "TSI", "Donchian DFMA", and "Donchian DFMG". These strategies have the signals and weights pre-determined in the code. The "Base DFMA" strategy is based on our Democratic Fibonacci Moving Average (DFMA) indicator; the "Donchian DFMA" is the same as the base DFMA strategy, but with a signal from our Donchian Cloud Score indicator as added confluence. The "Base DFMG" strategy is based on our Democratic Fibonacci McGinley Dynamics (DFMG) indicator; the "Donchian DFMG" is the same, but with the Donchian Cloud Score as added confluence. The "Ichimoku" strategy is based on the major sub-indicators found within an Ichimoku Cloud in addition to our Donchian Cloud Score. The "TSI" strategy is based on the True Strength Index.

The ability to select your strategy of choice can be found at the top of the strategy settings under "Strategy Options", then in the drop-down menu labeled "Strategy Choice".

The DFMA - Democratic Fibonacci Moving Average - is a separate indicator that we have released that takes 10 different Fibonacci MAs (lengths of 3 to 233, at Fibonacci intervals) and averages them to form the DFMA line. This helps by creating a consensus on the trend based on moving averages alone. Crossovers of the DFMA with the various Fib MA lengths as well as a cross of the price source and these lines can provide adequate long and short signals. In the two DFMA strategies, the heaviest weights have been given to crosses of the DFMA line/Fib MA (233) as well as the crosses of the Fib MA (3)/DFMA. Additionally, there are thresholds for DPO ( Detrended Price Oscillator , above or below 0), CMO ( Chande Momentum Oscillator , above or below 0), Jurik Volatility Bands (above or below 0), and Stoch RSI (above or below 50). These four signals hold a lighter weight than the MA cross signals. The macro score itself ranges between -10 and 10. In addition to the macro score line, a momentum line (sourced by the macro score itself) has been included. A crossover/crossunder of the macro score and the macro momentum line is included into the long/short signal syntax in addition to a threshold for the macro score.

The DFMG - Democratic Fibonacci McGinley Dynamics - is a separate indicator that we have released that takes 10 different Fibonacci McGinley Dynamic liness (lengths of 3 to 233, at Fibonacci intervals) and averages them to form the DFMG line. This helps by creating a consensus on the trend based on moving averages alone. Crossovers of the DFMG with the various Fib MG lengths as well as a cross of the price source and these lines can provide adequate long and short signals. This strategy has the signals and weights pre-determined in the code. Heaviest weights have been given to crosses of the DFMG line/ McGinley (233) as well as the crosses of the McGinley (3)/DFMG. Additionally, there are thresholds for DPO ( Detrended Price Oscillator , above or below 0), CMO ( Chande Momentum Oscillator , above or below 0), Jurik Volatility Bands (above or below 0), and Stoch RSI (above or below 50). These four signals hold a lighter weight than the McGinley cross signals. The macro score itself ranges between -10 and 10. In addition to the macro score line, a momentum line (sourced by the macro score itself) has been included. A crossover/crossunder of the macro score and the macro momentum line is included into the long/short signal syntax in addition to a threshold for the macro score.

For the Ichimoku macro score, five signals were considered and weighted equally:

- Kijun-sen < Ichimoku Source

- Tenkan-sen < Ichimoku Source

- Kijun-sen > Chikou-span

- Tenkan-sen > Kijun-sen

- Senkou Span A > Senkou Span B

In addition to these factors, the Ichimoku strategy utilizes the Donchian Cloud Score in the long and short entry signals. Thus, the Donchian Cloud settings are applicable to this strategy.

For the True Strength Index strategy, the heaviest weights have been given to various TSI signals, including a crossover/crossunder of TSI signal and TSI value, a threshold for the TSI Signal (above or below 0), and a crossover/crossunder of the CMO ( Chande Momentum Oscillator ) and the TSI signal line. Additionally, there are thresholds for DPO ( Detrended Price Oscillator , above or below 0), Jurik Volatility Bands (above or below 0), and Stoch RSI (above or below 50). These three signals hold a lighter weight than the three TSI signals. The macro score itself ranges between -10 and 10. In addition to the macro score line, a momentum line (sourced by the macro score itself) has been included. A crossover/crossunder of the macro score and the macro momentum line is included into the long/short signal syntax in addition to a threshold for the macro score.

The Donchian Cloud Score is derived from a set of 5 Donchian channels (upper, lower, and basis plotted) defaulted to lengths of 25, 50, 100, 150, and 200. A set of conditions associated with the channels aims to determine ranging versus trending markets. Weights are given to these conditions accordingly, then tallied up to determine the "cloud score", ranging between -25 and 25. In general, a ranging market is determined by a cloud score between -10 and 10, while a positive trending market has a score higher than 10 and a negative trending market has a score lower than -10. That said, long and short thresholds similar to the macro score itself are included in the user settings and set to a default of 5 or -5. The cloud score is plotted as a line in the underlay with coloration reflecting ranging or trending markets (green color above the long threshold, gray between the thresholds, and red below the short threshold). The cloud score is incorporated into the strategy syntax for long and short positions in that the score must be above or below the set threshold for a trade to be placed. A breakdown for the Donchian scoring is as follows:

- Broke the 25-length DC (DC(25)) upper band in the previous 3 bars - +1 if true, 0 if false

- Broke the DC(50) upper band in the previous 3 bars - +2 if true, 0 if false

- Broke the DC(100) upper band in the previous 3 bars - +3 if true, 0 if false

- Broke the DC(150) upper band in the previous 3 bars - +4 if true, 0 if false

- Broke the DC(200) upper band in the previous 3 bars - +5 if true, 0 if false

- Broke the DC(25) lower band in the previous 3 bars - -1 if true, 0 if false

- Broke the DC(50) lower band in the previous 3 bars - -2 if true, 0 if false

- Broke the DC(100) lower band in the previous 3 bars - -3 if true, 0 if false

- Broke the DC(150) lower band in the previous 3 bars - -4 if true, 0 if false

- Broke the DC(200) lower band in the previous 3 bars - -5 if true, 0 if false

- DC(25) basis line above the DC(50) basis line - +1 if true, -1 if false

- DC(25) basis line above the DC(100) basis line - +1 if true, -1 if false

- DC(25)basis line above the DC(150) basis line - +1 if true, -1 if false

- DC(25) basis line above the DC(200) basis line - +1 if true, -1 if false

- DC(50) basis line above the DC(100) basis line - +1 if true, -1 if false

- DC(50) basis line above the DC(150) basis line - +1 if true, -1 if false

- DC(50) basis line above the DC(200) basis line - +1 if true, -1 if false

- DC(100) basis line above the DC(150) basis line - +1 if true, -1 if false

- DC(100) basis line above the DC(200) basis line - +1 if true, -1 if false

- DC(150) basis line above the DC(200) basis line - +1 if true, -1 if false

Thresholds for both the respective macro score and the Donchian Cloud score have been included. Entry signals for each strategy require the score to be >= the respective thresholds for longs and <= the respective thresholds for shorts.

Additionally, a normalized z-score has been included. The z-score does not affect the entry and exit signals, however, it is displayed on the chart in the form of bar coloration. The z-score has been normalized to a range of -1 to +1. A z-score under -0.60 is displayed as a red bar color, a score between -0.60 and -0.2 is displayed as an orange bar color, a score between -0.2 and 0.2 is displayed as a gray bar color, a score between 0.2 and 0.6 is displayed as a lime bar color, and a score over 0.6 is displayed in green.

Data for each respective strategy will be displayed in an overlaid table. This includes the factors that comprise the macro score of choice, the values of each signal that adds up to the macro score, the macro score itself, the value of the momentum line of the macro score, the normalized z-score value, and the Donchian Cloud score (if applicable). Green coloration notes bullish sentiment within the signals or values, gray coloration is neutral, and red coloration notes bearish sentiment.

Take profit, stop loss, and trailing percentages are also included, found at the bottom of the Input tab under “TT and TTP” as well as “Stop Loss”. The take profit and stop loss levels will be reflected as green and red lines respectively on the chart as they occur. Make sure to understand the TP/SL ratio that you desire before use, as the desired hit rate/profitability percentage will be affected accordingly. The option for adding in a trailing stop has also been included, with options to choose between an ATR-based trail or a percentage-based trail. This strategy does NOT guarantee future returns. Apply caution in trading regardless of discretionary or algorithmic. Understand the concepts of risk/reward and the intricacies of each strategy choice before utilizing them in your personal trading.

Profitview/Pineconnector Settings:

If you wish to utilize Profitview’s automation system, find the included “Profitview Settings” under the Input tab of the strategy settings menu. If not, skip this section entirely as it can be left blank. Options will be “OPEN LONG TITLE”, “OPEN SHORT TITLE”, “CLOSE LONG TITLE”, and “CLOSE SHORT TITLE”. If you wished to trade SOL, for example, you would put “SOL LONG”, “SOL SHORT”, “SOL CLOSE LONG”, and “SOL CLOSE SHORT” in these areas. Within your Profitview extension, ensure that your Alerts all match these titles. To set an alert for use with Profitview, go to the “Alerts” tab in TradingView, then create an alert. Make sure that your desired asset and timeframe are currently displayed on your screen when creating the alert. Under the “Condition” option of the alert, select the strategy, then select the expiration time. If using TradingView Premium, this can be open-ended. Otherwise, select your desired expiration time and date. This can be updated whenever desired to ensure the strategy does not expire. Under “Alert actions”, nothing necessarily needs to be selected unless so desired. Leave the “Alert name” option empty. For the “Message”, delete the generated message and replace it with {{strategy.order.alert_message}} and nothing else. If using Pineconnector, follow the same directions for setting up an alert, but use the ",buy,,risk=" syntax as noted in the tooltips.

3Commas Bot DCA Backtester & Signals FREEThis is a DCA Strategy backtester + signals, built to emulate the 3Commas DCA bots. It uses your choice of 4 different buy signals, 2 of which can be adjusted in the settings. Everything is customizable so you can backtest specific settings with different buy signals and find the best performing strategy for your risk tolerance and capital. It can be used to backtest strategies on stocks as well, but just make sure your base order is larger than the share price for the entire backtesting range or it will not calculate properly.

You can use this template to code your own buy signals and then backtest them as a DCA strategy if you know some basic pine script.

The indicator shows all of your backtesting orders on the chart. The red line is your take profit level, the blue line is your average price level, the white line is your first order and the green lines are your average down orders. If you enable a stop loss in the settings your stop loss will be shown as an orange line once all of your average down orders have been hit, it will not be set until price has dipped below your covered trading range.

These levels update when things change during backtesting so you can visualize your strategy and how it would perform as well as see if your percentage deviation is large enough to cover dips. When backtesting trades are taken, the chart will show where they were taken(in backtesting) along with info on those trades such as the number each order is, the size of that order and the percentage deviation that order is from the initial buy.

SENDING SIGNALS TO 3COMMAS

Tradingview cannot sync this backtester to 3Commas and with the way alerts are setup for strategies on Tradingview, the best option for you to give signals to your bot would be to use this backtester to figure out what trigger you want to use and then setup that indicator separately to send alerts to your bot. All of the indicators used for signals in this backtester are available for free and can be configured to match this backtester and send alerts to 3Commas for you. Just make sure you set your alerts to once per bar close and don’t use less than a 15 second timeframe because then you could trigger the Tradingview threshold for alerts and get your alerts shut off.

You can also use this backtester with your own buy triggers if you know a little pine script. Just make copy of the script and code in your own buy signals and see how it backtests.

INFO PANEL FOR ANALYZING YOUR STRATEGY

The right hand side of the screen will show an info panel that shows a lot of different information so you can quickly see your bot settings and how it performed right on the screen.

In the top right corner you will see in purple your bot settings. These include your stoploss % if turned on, take profit %, average down order %, average down order % multiplier, volume multiplier, max number of orders allowed and size of your base order.

The top section of the first column “Current Trade” shows these stats: the open trade’s average price, the open trade’s take profit price, the open trade’s PNL, how far price is from your open tarde’s take profit level in percentage, your open position size and number of open orders.

The bottom section of the first column “Overall Performance” shows these stats: total number of trades taken during backtesting range, the largest amount of trades that were open at one time during backtesting, the max drawdown, the average number of bars per trade, gross profit, net profit, percent profit from your initial capital, current portfolio value and your initial capital.

CUSTOMIZABLE OPTIONS TO FIND THE PERFECT STRATEGY

Stoploss On/Off

This will turn your stoploss on or off. By default it is set to off and will not affect anything unless turned on.

Stoploss Percentage

This is the percentage below your final average down order price that will be set as a stoploss to keep your account from going too far in the red on big dips.

Take Profit Percentage - This is the percentage of profit you want the trade to hit before taking profit on your entire DCA trade. This level updates everytime you average down.

Average Down Percentage - This is the percentage that price has to drop from your initial order to initiate your first safety order. If the Average Down Percent Multiplier is set to 1 then this percentage will be the same for every average down order.

Average Down Percentage Multiplier - This multiplies your Average Down Percentage so each safety order needs a larger percentage deviation than the previous one. This keeps your buys closer together at the beginning and further apart when you hit more orders so you can extend your trading range but still be aggressive when price is going sideways.

Volume Multiplier Per New Order - This multiplies the size of each trade based on your base order. If you set it to a 2x multiplier then each average down order will be 2 times the size of the last one. So for example, a $100 base order with a 2x multiplier would have these values for the first 3 average down orders: 200, 400, 800.

Size Of Base Order - This is the size of your first position entry and will be used as a starting point for the volume multiplier. If your base order is $100 then it will buy $100 worth of whatever crypto you are backtesting this on. If you are looking at stock charts, you need to make sure your base order is higher than the share price across the entire backtesting range or it will not perform correctly.

Max Number Of Orders - This is the maximum number of orders the bot can take, including your base order. Adjust this to suit the amount of capital you are willing to allocate to your bot based on how much money it will require to run according to your bot settings.

TIPS ON HOW TO USE FOR BEST RESULTS

If you don’t have a lot of capital to work with, then use longer timeframes with a reasonable take profit percentage so that you don’t need a lot of average down orders. You can also try keeping the volume multiplier close to 1.

You can use the 3Commas dca bot settings page to see how much capital you will need for your strategy if you match it to the settings you have on this indicator. You can also check to see how much of a percentage deviation your bot is covering to make sure you have a reasonable range to trade in and orders to cover big dips. You can also check your coverage by seeing how far down the chart the green lines cover, which are your average down orders.

Make sure the initial capital in the properties tab of the settings has enough to cover all of your orders otherwise you will get unrealistic backtesting results. Also, make sure you leave the order size in the properties tab on contracts so it calculates your trades correctly. The only settings you need to touch in the properties tab is the initial capital. Unless you are trading somewhere that has lower commission fees, then you can change that to match, but leave all the other settings as is for it to function properly.

Increasing the volume multiplier will make your average price and take profit target follow the price action a lot closer as price falls, but it can also lead to having very large orders very quickly once you get into the 1.5-3x multiple range. Try using a high volume multiplier with less safety orders and you will get better results, however you need to have money on the sidelines to add on major dips to keep your bot turning a profit. Be very careful with this as greed and impatience will hurt your overall performance. This bot is meant to make money with lots of small wins so don’t get greedy and make sure you have enough money to cover large dips. If you are being aggressive with your bot, then I recommend only using 25% or less of your portfolio to trade aggressively and then use the smart trade feature on 3commas to add chunks of funds to your trades when price dips below your last safety order. Or if you want it to run without any supervision, then use lower volume multipliers and have lots of safety orders that can cover entire bear markets and still keep buying lower.

It’s a good idea to have some capital on the sidelines that you can add in when price dips quickly. This will help lower your average price and allow your bot to get out in profit quicker. 3Commas bot has a smart trade feature that will allow you to track your average price when adding extra funds and it will automatically update your other orders which is very convenient. Look at the longer timeframes when price dips and only add chunks at major areas where price is very likely to bounce. Or you can be aggressive when trading and add to your position when price dips and is at a likely bounce zone to maximize profits.

Only trade coins that have a good amount of liquidity as the larger your orders get, the harder it will be to sell if there isn’t much liquidity. Also, beware of how large your first order is as it will usually be a market order and can move the market if there is not much liquidity.

Since this bot takes a lot of trades and performs best when taking small profits consistently, you will need to factor in exchange fees. The bot is set to .5% commission(you can change this) on the buy and sell orders as most exchanges charge that amount. Some exchanges offer no fee trading on certain coins so be sure to look around for those so you can keep the commissions and maximize profits.

I strongly encourage you to try out a lot of different setting combinations across multiple different coins and do it across a few months to see how it would have performed under various market conditions. This will help you get a better idea of how much of a percentage deviation you’ll need to be able to cover to keep your bot running and making constant profits. You can also use the deep backtesting feature of the strategy panel to see how it would have done, but just beware that the info panel of the indicator will not reflect deep backtesting results, only the normal backtesting range.

MARKETS

This backtester can be used on any market including crypto, stocks, forex & futures. You just need to make sure your base order is larger than the share price when using this on things besides crypto.

TIMEFRAMES

This backtester can be used on all timeframes.

Rosebud Trend Backtest [DepthHouse]*Past Performance Does Not Guarantee Future Results*

*Strategy created for backtesting purposes only.

*Backtesting assesses the viability of a trading strategy or pricing model by discovering how it would have played out retrospectively using historical data.

* Please be sure to read all updates below as the information below could change with future updates.

Rosebud Trend Indicator uses complex range calculations to easily detect trend changes, critical support and resistance levels, and even aid in spotting reversals. The Critical Support & Resistance Zones are plotted via the red and green cloud. This cloud not only visually displays the expected trend direction but often acts as major support and resistance zones. The outer band measures the expected range in which the assets trade over longer periods of time.

The Rosebud Trend Backtest combines the calculations of the ATR Auto Oscillator & the Rosebud Trend Indicator to demonstrate backtest performance.

// Settings //

Users can switch the ‘ Trend Sensitivity ’ between ‘ Low ', ' Med ', and ‘ High ’ to increase or decrease the rate at which the cloud changes.

By altering the S/R Band Thickness users can furthermore increase or decrease the rate at which a trend changes by altering the thickness of the cloud. Default is .50 however this can be lowered if needed.

Bar colors are generated by a combination of Rosebuds primary function and our ATR AUTO Oscillator base functions. Users have 3 bar color options to select from: Simple, Complex, and Off.

Simple: Bars colors alternate between shades of red and green based on the trend direction and the ATR Auto strength. The stronger the shade, the stronger the trend.

Complex: This adds a few extra variables to the script which generates a more complex bar color display. Using this option, Rosebud will generate light red bars in a bull trend if downward movement is strong and vice versa in a bear trend. It also will generate a purple bar if the candle successfully closes above or below the Top & Bottom Range Bands; We call this a range break, and it could be an early sign of strong upward or downward movement.

Off: In case you like to keep things even simpler, this option hides all overlay bar colors.

ATR Options: Used for Light & Strong Entries/Exits // Bar Colors also based on these settings

ATR Smoothed Signal Option: Turns advance smoothing on or off. On will reduce signal noise, while Off could land you that perfect bottom signal with a lower success rate.

ATR Candlestick Length: Default factor for bar color and shape generation, the higher the number the fewer signals that will generate.

ATR Candlestick Smoothing: Default smoothing for the Candlestick Length

Signal Lookback: Adjust the factor at which Bull, Bear, Up, and Down. Lower this to 2 for more signals.

// ⇅ BackTest Settings ⇅ //

Short Trading: Option to see backtest results for both long and short positions. Default is Long Only.

Strategy Entry Options:

Trend Only: Positions are entered right as there is a cloud trend change.

Light Entry: This enters a trade as soon as there is a breakout or breakdown signal generated from the ATR settings.

Strong Entry: Multiple conditions must be met; Price action must be near the Trend Base and must receive either a bullish or bearish crossover in the oversold or overbought range of the ATR Settings.

Strategy Exit Options:

Trend Only: Exits all positions after there is a primary trend change.

Light Exit: Exits a user set percentage of open positions when the ATR generates a breakdown or breakout. Will continue to do this at each occurrence. Presets are built in to keep these from triggering too often in volatile conditions.

Strong Exit: Exits a user set percentage of open positions when the ATR generates a bullish or bearish crossover in the overbought or oversold ranges. Will continue to do this with each occurrence. Presets are built in to keep these from triggering too often in volatile conditions.

Profit Points: Exits a set percentage of the position up to 3 times at a user set percentage gap from the entry. Any remaining amount in the position exits upon a trend change.

Profit QTY Percent: Percent of the position to exit when an exit condition triggers. This does not apply to the “Trend Only” exit option.

Profit Percent Gap: Percent gap for Profit Point Exits. Recommend adjusting based on timeframe. See example below.

Strategy - DMI Indicator with DPO Indicator as a GuardThe Directional Movement Index Indicator is one of my favorite indicators in tradingview's built-in library. It is free to use for all

For more information on what the DMI is, please visit: www.tradingview.com

The only problem I've come across with the DMI is that when it hits a 'trade range zone' it triggers false new trends (this is the case with almost every indicator I've ever tested).

This script modifies the DMI by removing the need for the ADX logic. It only focuses on the +DI and the -DI.

In order to remove the 'noise' generated during a trade range zone I have added another powerful indicator called the Detrended Price Oscillator.

The DPO is also a 'built-in' indicator on tradingview. www.tradingview.com

The DPO is used in conjunction with the DMI to stop trade ranges from wrecking your profits.

This strategy logic simply checks for the DMI indicator to cross itself. If the +DI crosses over the -DI this is a bullish cross and visa versa, if the -DI crosses over the +DI then it could mean bearish sentiment is building.

But then strategy logic uses the DPO to check if the DPO is above 0 or below 0 value

If the +DI crosses over the -DI and the DPO is above 0 value, then it's a Long entry point.

However, if the +DI crosses over the -DI and the DPO is below 0 value, then the Long signal is void.

And visa versa, if the -DI crosses over the +DI and the DPO is below 0 value, then it's a Short entry point (unless the DPO is greater than 0)

With this DPO 'guard' in place, it helps us keep the total trades executed to a minimum.

This is vital to push through trade ranges that can wreck your profit potential.

I wish I could create a better plotting mechanism for this indicator so you can better see the visuals. But combining the DMI to scale with the DPO is not possible.

The best solution is to simply add another DMI indicator to your chart so you can compare the DMI to this script that is dominated by the DPO (yellow line).

Enjoy! Likes are much appreciated!

Intraday Market Structure Research Tool (Reversal + Breakout)This script is a fully rule-based intraday strategy designed for research and backtesting purposes, not financial advice. It is intended to help traders study market behavior, time-based price patterns, and statistical trade outcomes under realistic trading assumptions.

What the Strategy Does

This strategy operates in two selectable trade modes:

1. Reversal Mode

Identifies statistically large candles relative to recent volatility

Enters counter-direction trades when price shows exhaustion behavior

Designed to study fade-type behavior around session extremes

2. Breakout Mode

Tracks recent swing highs/lows over a user-defined lookback

Executes trades only after confirmed price expansion beyond these levels

Designed to test momentum continuation behavior

Time & Session Filtering

Trades are only taken during user-defined market sessions, including:

New York 1

New York 2

London

Asia

This allows users to analyze performance differences between global trading sessions.

9:30 AM Opening Range Logic

The script captures the 9:30 AM (Eastern) one-minute candle high/low and uses that as an Opening Range:

Breakout trades can be confirmed above or below this range

The range is visualized for clarity

Risk Management & Realism Controls

This script includes realistic execution mechanics:

Fixed stop-loss and take-profit defined by the user (points or ticks)

Built-in slippage modeling

Commission assumptions included

Position sizing designed to keep risk per trade under 5–10% of account equity when used with realistic account sizes

Users are responsible for choosing realistic account sizes and risk values when running backtests.

Statistical Performance Tracking

The strategy records and displays performance data including:

Win rate

Average win and loss

Maximum drawdown per trade series

Expectancy

Trade distribution by:

Time of day

Session

Market classification

This allows users to study market tendencies and structural behavior over large sample sizes.

Visual Tools

The script displays:

Entry and exit markers

Blocked trade labels (when conditions are not met)

Opening range box

Breakout levels

Use Case Disclaimer

This script is designed for:

Backtesting

Market structure research

Statistical study

It is not guaranteed to be profitable, and results depend heavily on user-selected settings, market conditions, and realistic brokerage assumptions.

ORB Breakout Strategy w/ Filters - Dynamic Sizing - MTFHere is a comprehensive description of the strategy, written in a clear and structured format. You can use this for your script's "how-to-use" guide or documentation.

---

## 📈 Opening Range Breakout (ORB) Strategy

This is a comprehensive, multi-timeframe strategy built for trading opening range breakouts. It is designed with a "filters-first" approach, allowing you to validate a breakout with trend, volume, and volatility.

The strategy's core power comes from its flexibility. You can trade on a low timeframe (like a 1-minute chart) while basing your breakout levels on a higher timeframe's opening bar (e.g., the first 15-minute bar). It includes dynamic position sizing based on risk and a wide array of advanced exit management options.

### Key Features

* **Multi-Timeframe Opening Range:** The core of the strategy. You can define the "Opening Range" timeframe (5, 10, 15, 30, or 60 min) *independently* of your chart timeframe.

* **Custom Trading Session:** Define the exact session (e.g., "0930-1600" in "America/New_York") you want to trade.

* **One Trade Per Session:** The strategy will only take the *first valid breakout* signal per day to avoid over-trading.

---

### 🚦 Entry Signals & Filters

A trade is only initiated when the price closes above the Session High or below the Session Low **AND** all active filters are passed.

* **Trend Filter:** (Optional) Requires price to be above a long-term MA (e.g., 100 EMA) for long trades and below it for short trades.

* **Volume Filter:** (Optional) Requires the breakout bar's volume to be a specified multiplier (e.g., 1.5x) of the recent average volume.

* **Volatility Filter:** (Optional) Requires the current ATR to be higher than its long-term average, ensuring you only trade during periods of expanding volatility.

* **Direction Filter:** Allows you to isolate the strategy to **Long Only**, **Short Only**, or **Both**.

---

### 💰 Dynamic Position Sizing

The strategy includes a robust "Risk %" sizing model.

* **Risk-Based Sizing:** Instead of fixed contracts, it calculates the position size based on your **Account Size**, **Risk % per Trade**, and the **Stop Loss distance**.

* **Auto-Detect Point Value:** It automatically detects the correct point value for popular futures contracts (ES, NQ, MES, MNQ) and provides a manual override for other assets.

---

### 📤 Exit & Risk Management

This strategy features a multi-layered exit system, giving you complete control over how trades are managed.

#### 1. Stop Loss (SL)

Your initial stop loss can be calculated using a fixed **Tick** offset or an **ATR** multiplier. It can be anchored from two different points:

* **Breakout Level:** The stop is placed relative to the `sessionHigh` or `sessionLow` level.

* **Entry Bar:** The stop is placed relative to the high/low of the bar that *triggered* the entry.

#### 2. Take Profit (TP)

A standard Take Profit can be set using a fixed **Tick** offset or an **ATR** multiplier.

#### 3. Advanced Exit Logic

These options override the standard Take Profit to allow for more dynamic trade management:

* **Trailing Take Profit (TTP):**

* **Fixed/ATR Trail:** A standard trailing stop that activates after price moves a certain amount in your favor.

* **MA Price Cross:** Exits the trade as soon as the price closes across a fast-moving average (e.g., 9-EMA).

* **MA Crossover:** Exits the trade as soon as a fast MA crosses below a slow MA (for longs) or above (for shorts).

* **Close on Reversal:** (Optional) Exits immediately if the **very next bar** after entry closes back *inside* the opening range (a "failed breakout" signal).

* **Close on Opposite Range Cross:** (Optional) Exits a long trade if the price ever closes below the `sessionLow` (and vice-versa for shorts).

* **End of Session Exit:** All open positions are automatically closed at the end of the defined trading session.

NY ORB - Full Dynamic SystemNY ORB - Full Dynamic Strategy Summary

1. Opening Range and Session Timing

Opening Range (ORB) Calculation: The strategy identifies the ORB High and ORB Low by tracking the highest high and lowest low during the specified New York pre-market window, which is set by default from 8:30 to 8:45 (New York time).

Entry Window: Trading activity is restricted to a specific entry period, typically starting shortly after the ORB is established (default: 8:50 to 12:00).

Hard Exit Time: Any remaining open positions are automatically closed at a fixed exit time (default: 13:25).

2. Trade Entry Logic and Filters

An entry (Long or Short) is generated when the price breaks out of the established ORB, provided it passes a series of optional filters:

Direction Control: The user can restrict the strategy to trade Long Only, Short Only, or Both.

Second Breakout Logic: An optional filter that requires the price to break out, reverse back into the range, and then break out again, confirming momentum after a consolidation.

Confirmation Candle Count: An optional filter that checks the close of a previous candle (e.g., 1 or 2 candles ago) to ensure the price was still inside the range, preventing premature entry.

Technical Filters (Optional): The entry is only executed if it aligns with selected indicators:

RSI: Filters for non-overbought (Long) or non-oversold (Short) conditions.

MACD: Requires the MACD line to be above/below the Signal line for alignment.

VWAP: Requires the price to be above/below the Volume-Weighted Average Price.

Trend Filter (SMMA): Requires the price to be above/below a 50-period Simple Moving Average.

3. Dynamic Risk and Exit Management

This strategy features highly configurable stop-loss and profit-taking mechanics:

Primary Stop Loss Methods: The Stop Loss distance can be dynamically chosen from four types:

Fixed: A fixed number of ticks.

ATR: Based on a multiple of the Average True Range (ATR).

Capped ATR: ATR-based, but with a hard maximum tick limit.

OR-Based: Based on a multiple of the actual ORB High-to-Low range.

Dynamic Profit Target: The Take Profit level is calculated dynamically based on a multiplier of either the ATR or the ORB Range.

Breakeven Stop:

If enabled, the Stop Loss automatically moves to the entry price (Breakeven) once the price moves a predetermined distance in the profitable direction.

An Adaptive Breakeven option allows the trigger distance to be calculated as a percentage of the overall ATR Profit Target.

Trailing Stop: The strategy uses a trailing stop, which can be custom-set (fixed ticks) or dynamically tied to the ATR. An optional feature Auto Tighten Trailing reduces the trailing multiplier once the breakeven level is hit.

MA Cross Exit: An alternative, counter-trend exit mechanism that closes the trade if the price crosses back over the chosen Moving Average (either SMMA or VWAP), overriding the pending profit target.

4. Daily Account Management

The strategy includes crucial daily risk controls to protect capital and lock in profits:

Daily Profit Limit: If the total daily PnL (realized and unrealized) hits a predefined maximum profit threshold (in ticks), all trades are closed, and new entries are blocked for the remainder of the trading day.

Daily Loss Limit: Conversely, if the total daily PnL hits a predefined maximum loss threshold, all trades are closed, and new entries are blocked for the remainder of the day.

Cybertrading-Insidebar hunter pro robotThe Cybertrading-Inside Pro strategy is an advanced version of Cyber-Inside.

It automates ATR-based inside-bar trading with optional pullback entries, full risk/reward visualization, time filtering, pending-order handling, and fixed chart watermark branding (“CollegePips / CyberTrading”).

⚙️ Technical Overview

1. Core Structure

Uses ATR(14) to measure volatility and classify candle ranges.

Candles are labeled as Spinning, Standard, Long, or Huge based on their range vs. ATR.

Only valid candles (Standard or Long) qualify to confirm a setup.

2. Inside-Bar Logic

The setup requires the current candle’s high/low to be fully contained inside the previous candle (an inside bar).

A wick-break must occur — the wick slightly breaks the previous inside bar’s range while the body remains inside.

This pattern forms a Pierce-Only signal.

Direction:

Wick down → potential Long entry

Wick up → potential Short entry

3. Timing and Entry Conditions

With the time filter enabled, trades trigger only between defined hours (e.g., 07–22).

If Enable Pullback is on, the entry is placed using a limit order offset by pullbackATR × ATR from the signal candle.

If the pullback entry isn’t triggered within pullbackMaxBars, the pending order is canceled automatically.

You can also enable display-only entries without execution (Enable Entry Without Pullback).

4. Risk & Target Management

Stop loss is placed beyond the second-previous candle’s high/low ± stopBuffer × ATR.

Take-profit is based on the chosen risk/reward multiple (RR) or the previous candle’s high/low.

Position size auto-adjusts to keep total risk equal to riskPercent of equity.

5. Visual Components

Dynamic chart objects include:

Red box: risk zone (entry → stop)

Green/blue box: reward zone (entry → target)

Dotted diagonal line: risk-to-reward path

Arrows: actual fill points

6. Order Management System

Each signal creates a unique order ID (pendingId) and exit ID (planExitId).