Volume Spike Alert & Overlay"Volume Spike Alert & Overlay" highlights unusually high trading volume on a chart. It calculates whether the current volume exceeds a user-defined percentage above the historical average and triggers an alert if it does. The information is also displayed in a customizable on-screen table.

What It Does

Monitors volume for each bar and compares it to an average over a user-defined lookback period.

Supports multiple smoothing methods (SMA, EMA, WMA, RMA) for calculating the average volume.

Triggers an alert when current volume exceeds the threshold percentage above the average.

Displays a table on the chart with:

Current Volume

Average Volume

Threshold Percentage

Optional empty row for spacing/formatting

How It Works

User Inputs:

lookbackPeriods: Number of bars used to calculate the average volume.

thresholdPercent: % above the average that triggers a volume spike alert.

smoothingType: Type of moving average used for volume calculation.

textColor, bgColor: Formatting for the display table.

tablePositionInput: Where the table appears on the chart (e.g., Bottom Right).

Toggles for showing/hiding parts of the table.

Volume Calculations:

Calculates current bar's volume.

Calculates average volume using the selected smoothing method.

Computes the threshold: avgVol * (1 + thresholdPercent / 100).

Compares current volume to threshold.

Table Display:

Dynamically creates a table with volume stats.

Adds rows based on user preferences.

Alerts:

alertcondition fires when currentVol crosses above the calculated threshold.

Message: "Volume Threshold Exceeded"

Usage Examples

Example 1: Spotting High Activity

Apply the script to a stock like AAPL on a 5-minute chart.

Set lookbackPeriods to 20 and thresholdPercent to 30.

Use EMA for more reactive volume tracking.

When volume spikes more than 30% above the 20-period EMA, an alert triggers.

Example 2: Day Trading Filter

For scalpers, apply it to a 1-minute crypto chart (e.g., BTC/USDT).

Set thresholdPercent to 50 to catch only strong surges.

Position the table at the top left and reduce visible info for a clean layout.

Example 3: Long-Term Context

On a daily chart, use SMA and set lookbackPeriods to 50.

Helps identify breakout moves supported by strong volume.

How this is different from Trading View's Volume indicator:

The standard volume plot from trading view allows users to set a alert when the average line is crossed, but it does not allow you to set a custom percentage at which to trigger an alert. This indicator will allow you to set any percentage you wish to monitor and above that percentage threshold will trigger your alert.

===== ORIGINAL DESCRIPTION =====

Volume Spike Alert & Overlay

This indicator will display the following as an overlay on your chart:

Current volume

Average Volume

Threshold for Alert

Description:

This indicator will display the current bar volume based on the chart time frame,

display the average volume based on selected conditions,

allow user selectable threshold over the average volume to trigger an alert.

Options:

Average lookback period

Smoothing type

Alert Threshold %

Enable / Disable Each Value

Change Text Color

Change Background Color

Change Table location

Add/Remove extra row for placement in top corner

Usage Example:

I use this indicator to alert when the current volume exceeds the average volume by a specified percentage to alert to volume spikes.

Set the threshold to 25% in the settings

Create an alert by clicking on the 3 dots on the right of the indicator title on the chart

When the threshold is exceeded the alert will trigger

חפש סקריפטים עבור "text"

Intrabar DistributionThe Intrabar Distribution publication is an extension of the Intrabar BoxPlot publication. Besides a boxplot, it showcases price and volume distribution using intrabar Lower Timeframe (LTF) values (close) which can be displayed on the chart or in a separate pane.

🔶 USAGE

Intrabar Distribution has several features, users can display:

Recent candle for comparison against the other features

Boxplot of recent candle

Price distribution (optionally displayed as a curve)

Volume distribution

🔹 Recent candle / Boxplot

The middle 50% intrabar close values (Interquartile range, or IQR) are shown as a box, where the upper limit is percentile 75 (p75), and the lower limit is percentile 25 (p25). The dashed lines show the addition/subtraction of 1.5*IQR. All values out of range are considered outliers. They are displayed as white dots within the IQR*1.5 range or white X's when beyond the IQR*3 range (extreme outliers).

By showing the middle 50% intrabar values through a box, we can more easily see where the intrabar activity is mainly situated.

Note in the example above an upward-directed candle with a negative volume delta, displayed as a red box and dot (see further).

As seen in the following example, compared against the recent candle (grey candle at the left), most of the intrabar activity lies just beneath the opening price.

Note that results will be more accurate when more data is available, which can be done by making the difference between the current timeframe and the intrabar timeframe large enough.

🔹 Price / Volume distribution

The price and volume distribution can be helpful for highlighting areas of interest.

Here, we can see two areas where intrabar closing prices are mainly positioned.

The following example shows three successive bars. The recent bar is displayed on the left side, together with the volume distribution. The boxplot and price distribution are displayed on the right.

You can see the difference between volume and price distribution.

At the first bar, most price activity is at the top, while most of the volume was generated at the bottom; in other words, the price got briefly in the bottom region, with high volume before it returned.

At the second bar, price and volume are relatively equally distributed, which fits for indecisiveness.

The third bar shows more volume at a higher region; most intrabar closing prices are above the closing price.

Following example shows the same with 'Curve shaped' enabled (Settings: 'Price Distribution')

When 'Curve shaped' is enabled, lines/labels are shown with the standard deviation distance.

A blue 'guide line' can be enabled for easier interpretation.

🔹 Volume Delta

When there is a discrepancy between the delta volume and direction of the candle, this will be displayed as follows:

Red candle: when the sum of the volume of green intrabars is higher than the sum of the volume of red intrabars, the 'mean dot' will be coloured green.

Green candle: when the sum of the volume of red intrabars is higher than the sum of the volume of green intrabars, the 'mean dot' will be coloured red.

🔶 DETAILS

The intrabar values are sorted and split in parts/sections. The number of values in each section is displayed as a white line

The same principle applies to volume distribution, where the sum of volume per section is displayed as an orange area.

The boxplot displays several price values

Last close price

Highest / lowest intrabar close price

Median

p25 / p75

🔹 LTF settings

When 'Auto' is enabled (Settings, LTF), the LTF will be the nearest possible x times smaller TF than the current TF. When 'Premium' is disabled, the minimum TF will always be 1 minute to ensure TradingView plans lower than Premium don't get an error.

Examples with current Daily TF (when Premium is enabled):

500 : 3 minute LTF

1500 (default): 1 minute LTF

5000: 30 seconds LTF (1 minute if Premium is disabled)

🔶 SETTINGS

Location: Chart / Pane (when pane is opted, move the indicator to a separate pane as well)

Parts: divides the intrabar close values into parts/sections

Offset: offsets every drawing at once

Width: width of drawings, only applicable on "location: chart"

Label size: size of price labels

🔹 LTF

LTF: LTF setting

Auto + multiple: Adjusts the initial set LTF

Premium: Enable when your TradingView plan is Premium or higher

🔹 Current Bar

Display toggle + color setting

Offset: offsets only the 'Current Bar' drawing

🔹 Intrabar Boxplot

Display toggle + Colors, dependable on different circumstances.

Up: Price goes up, with more bullish than bearish intrabar volume.

Up-: Price goes up, with more bearish than bullish intrabar volume.

Down: Price goes down, with more bearish than bullish intrabar volume.

Down+: Price goes down, with more bullish than bearish intrabar volume.

Offset: offsets only the 'Boxplot' drawing

🔹 Price distribution

Display toggle + Color.

Curve Shaped

Guide Lines: Display 2 blue lines

Display Price: Show price of 'x' standard deviation

Offset: offsets only the 'Price distribution' drawing

Label size: size of price labels (standard deviation)

🔹 Volume distribution

Display toggle + Color.

Offset: offsets only the 'Volume distribution' drawing

🔹 Table

Show TF: Show intrabar Timeframe.

Textcolor

Size Table: Text Size

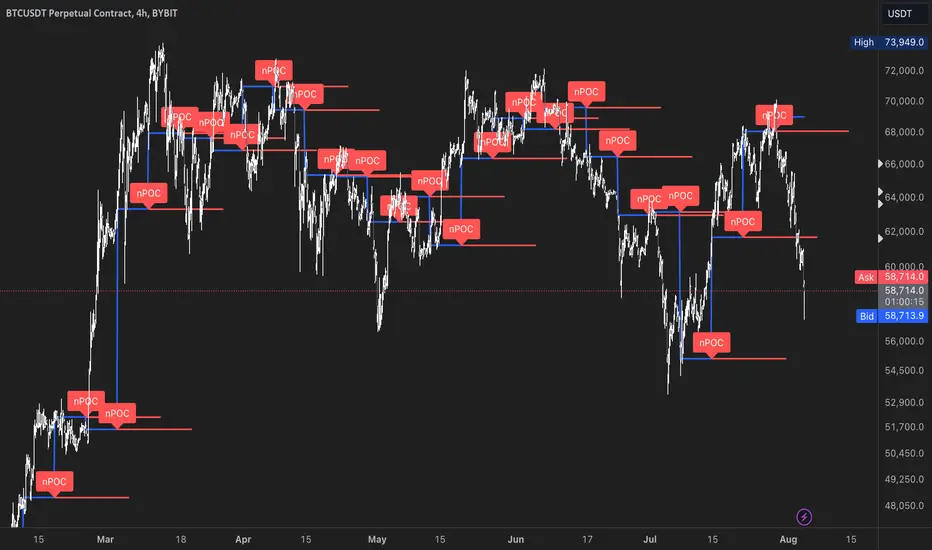

nPOC Levels by Tyler### Explanation of the Pine Script

This Pine Script identifies and displays weekly naked Points of Control (nPOCs) on a TradingView chart. An nPOC represents a Point of Control (POC) from a previous week that has not been revisited by price action in subsequent weeks. These nPOCs are extended to the right as horizontal lines, indicating potential support or resistance levels.

#### Script Overview

1. **Indicator Declaration:**

```pinescript

//@version=5

indicator("Weekly nPOCs", overlay=true)

```

- The script is defined as a version 5 Pine Script.

- The `indicator` function sets the script's name ("Weekly nPOCs") and specifies that the indicator should be overlaid on the price chart (`overlay=true`).

2. **Function to Calculate POC:**

```pinescript

f_poc(_hl2, _vol) =>

var float vol_profile = na

if (na(vol_profile))

vol_profile := array.new_float(100, 0.0)

_bin_size = (high - low) / 100

for i = 0 to 99

if _hl2 >= low + i * _bin_size and _hl2 < low + (i + 1) * _bin_size

array.set(vol_profile, i, array.get(vol_profile, i) + _vol)

max_volume = array.max(vol_profile)

poc_index = array.indexof(vol_profile, max_volume)

poc_price = low + poc_index * _bin_size + _bin_size / 2

poc_price

```

- The function `f_poc` calculates the Point of Control (POC) for a given period.

- It takes two parameters: `_hl2` (the average of the high and low prices) and `_vol` (volume).

- A volume profile array (`vol_profile`) is initialized to store volume data across different price bins.

- The price range between the high and low is divided into 100 bins (`_bin_size`).

- The function iterates over each bin, accumulating the volumes for prices within each bin.

- The bin with the maximum volume is identified as the POC (`poc_price`).

3. **Variables to Store Weekly Data:**

```pinescript

var float poc = na

var float prev_poc = na

var line poc_lines = na

if na(poc_lines)

poc_lines := array.new_line(0)

```

- `poc` stores the current week's POC.

- `prev_poc` stores the previous week's POC.

- `poc_lines` is an array to store lines representing nPOCs. The array is initialized if it is `na` (not initialized).

4. **Calculate Weekly POC:**

```pinescript

is_new_week = ta.change(time('W')) != 0

if (is_new_week)

prev_poc := poc

poc := f_poc(hl2, volume)

if not na(prev_poc)

line new_poc_line = line.new(x1=bar_index, y1=prev_poc, x2=bar_index + 100, y2=prev_poc, color=color.red, width=2)

label.new(x=bar_index, y=prev_poc, text="nPOC", style=label.style_label_down, color=color.red, textcolor=color.white)

array.push(poc_lines, new_poc_line)

```

- `is_new_week` checks if the current bar is the start of a new week using the `ta.change(time('W'))` function.

- If it's a new week, the previous week's POC is stored in `prev_poc`, and the current week's POC is calculated using `f_poc`.

- If `prev_poc` is not `na`, a new line (`new_poc_line`) representing the nPOC is created, extending it to the right (for 100 bars).

- A label is created at the `prev_poc` level, marking it as "nPOC".

- The new line is added to the `poc_lines` array.

5. **Remove Old Lines:**

```pinescript

if array.size(poc_lines) > 52

line.delete(array.shift(poc_lines))

```

- This section ensures that only the last 52 weeks of nPOCs are kept to avoid cluttering the chart.

- If the `poc_lines` array contains more than 52 lines, the oldest line is deleted using `array.shift`.

6. **Plot the Current Week's POC as a Reference:**

```pinescript

plot(poc, title="Current Weekly POC", color=color.blue, linewidth=2, style=plot.style_line)

```

- The current week's POC is plotted as a blue line on the chart for reference.

#### Summary

This script calculates and identifies weekly Points of Control (POCs) and marks them as nPOCs if they remain untouched by subsequent price action. These nPOCs are displayed as horizontal lines extending to the right, providing traders with potential support or resistance levels. The script also manages the number of lines plotted to maintain a clear and uncluttered chart.

itradesize /\ Silver Bullet x Macro x KillzoneThis indicator shows the best way to annotate ICT Killzones, Silver Bullet and Macro times on the chart. With the help of a new pane, it will not distract your chart and will not cause any distractions to your eye, or brain but you can see when will they happen.

The indicator also draws everything beforehand when a proper new day starts.

You can customize them how you want to show up.

Collapsed or full view?

You can hide any of them and keep only the ones you would like to.

All the colors can be customized, texts & sizes or just use shortened texts and you are also able to hide those drawings which are older than the actual day.

You should minimize the pane where the script has been automatically drawn to therefore you will have the best experience and not show any distractions.

The script automatically shows the time-based boxes, based on the New York timezone.

Killzone Time windows ( for indices ):

London KZ 02:00 - 05:00

New York AM KZ 07:00 - 10:00

New York PM KZ 13:30 - 16:00

Silver Bullet times:

03:00 - 04:00

10:00 - 11:00

14:00 - 15:00

Macro times:

02:33 - 03:00

04:03 - 04:30

08:50 - 0910

09:50 - 10:10

10:50 - 11:10

11:50 - 12:50

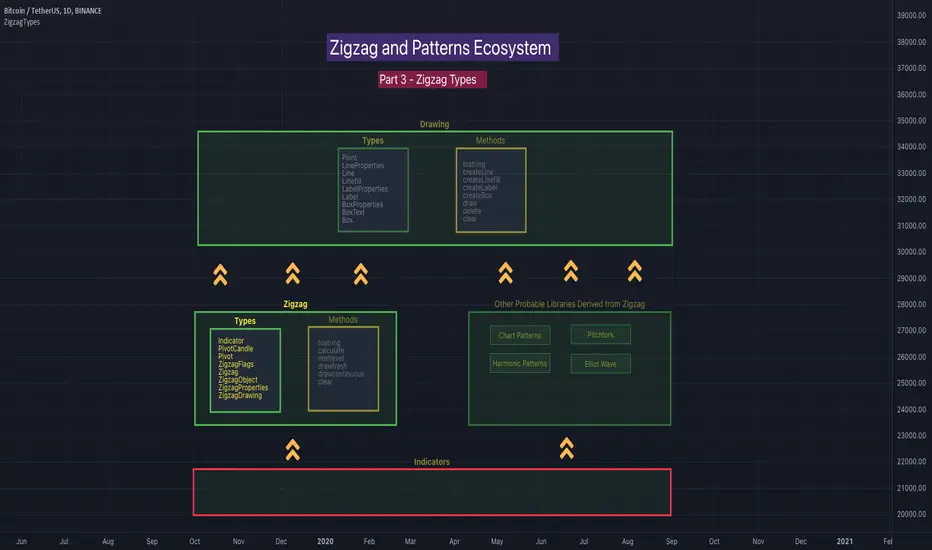

ZigzagLiteLibrary "ZigzagLite"

Lighter version of the Zigzag Library. Without indicators and sub-component divisions

method getPrices(pivots)

Gets the array of prices from array of Pivots

Namespace types: Pivot

Parameters:

pivots (Pivot ) : array array of Pivot objects

Returns: array array of pivot prices

method getBars(pivots)

Gets the array of bars from array of Pivots

Namespace types: Pivot

Parameters:

pivots (Pivot ) : array array of Pivot objects

Returns: array array of pivot bar indices

method getPoints(pivots)

Gets the array of chart.point from array of Pivots

Namespace types: Pivot

Parameters:

pivots (Pivot ) : array array of Pivot objects

Returns: array array of pivot points

method getPoints(this)

Namespace types: Zigzag

Parameters:

this (Zigzag)

method calculate(this, ohlc, ltfHighTime, ltfLowTime)

Calculate zigzag based on input values and indicator values

Namespace types: Zigzag

Parameters:

this (Zigzag) : Zigzag object

ohlc (float ) : Array containing OHLC values. Can also have custom values for which zigzag to be calculated

ltfHighTime (int) : Used for multi timeframe zigzags when called within request.security. Default value is current timeframe open time.

ltfLowTime (int) : Used for multi timeframe zigzags when called within request.security. Default value is current timeframe open time.

Returns: current Zigzag object

method calculate(this)

Calculate zigzag based on properties embedded within Zigzag object

Namespace types: Zigzag

Parameters:

this (Zigzag) : Zigzag object

Returns: current Zigzag object

method nextlevel(this)

Namespace types: Zigzag

Parameters:

this (Zigzag)

method clear(this)

Clears zigzag drawings array

Namespace types: ZigzagDrawing

Parameters:

this (ZigzagDrawing ) : array

Returns: void

method clear(this)

Clears zigzag drawings array

Namespace types: ZigzagDrawingPL

Parameters:

this (ZigzagDrawingPL ) : array

Returns: void

method drawplain(this)

draws fresh zigzag based on properties embedded in ZigzagDrawing object without trying to calculate

Namespace types: ZigzagDrawing

Parameters:

this (ZigzagDrawing) : ZigzagDrawing object

Returns: ZigzagDrawing object

method drawplain(this)

draws fresh zigzag based on properties embedded in ZigzagDrawingPL object without trying to calculate

Namespace types: ZigzagDrawingPL

Parameters:

this (ZigzagDrawingPL) : ZigzagDrawingPL object

Returns: ZigzagDrawingPL object

method drawfresh(this, ohlc)

draws fresh zigzag based on properties embedded in ZigzagDrawing object

Namespace types: ZigzagDrawing

Parameters:

this (ZigzagDrawing) : ZigzagDrawing object

ohlc (float ) : values on which the zigzag needs to be calculated and drawn. If not set will use regular OHLC

Returns: ZigzagDrawing object

method drawcontinuous(this, ohlc)

draws zigzag based on the zigzagmatrix input

Namespace types: ZigzagDrawing

Parameters:

this (ZigzagDrawing) : ZigzagDrawing object

ohlc (float ) : values on which the zigzag needs to be calculated and drawn. If not set will use regular OHLC

Returns:

PivotCandle

PivotCandle represents data of the candle which forms either pivot High or pivot low or both

Fields:

_high (series float) : High price of candle forming the pivot

_low (series float) : Low price of candle forming the pivot

length (series int) : Pivot length

pHighBar (series int) : represents number of bar back the pivot High occurred.

pLowBar (series int) : represents number of bar back the pivot Low occurred.

pHigh (series float) : Pivot High Price

pLow (series float) : Pivot Low Price

Pivot

Pivot refers to zigzag pivot. Each pivot can contain various data

Fields:

point (chart.point) : pivot point coordinates

dir (series int) : direction of the pivot. Valid values are 1, -1, 2, -2

level (series int) : is used for multi level zigzags. For single level, it will always be 0

ratio (series float) : Price Ratio based on previous two pivots

sizeRatio (series float)

ZigzagFlags

Flags required for drawing zigzag. Only used internally in zigzag calculation. Should not set the values explicitly

Fields:

newPivot (series bool) : true if the calculation resulted in new pivot

doublePivot (series bool) : true if the calculation resulted in two pivots on same bar

updateLastPivot (series bool) : true if new pivot calculated replaces the old one.

Zigzag

Zigzag object which contains whole zigzag calculation parameters and pivots

Fields:

length (series int) : Zigzag length. Default value is 5

numberOfPivots (series int) : max number of pivots to hold in the calculation. Default value is 20

offset (series int) : Bar offset to be considered for calculation of zigzag. Default is 0 - which means calculation is done based on the latest bar.

level (series int) : Zigzag calculation level - used in multi level recursive zigzags

zigzagPivots (Pivot ) : array which holds the last n pivots calculated.

flags (ZigzagFlags) : ZigzagFlags object which is required for continuous drawing of zigzag lines.

ZigzagObject

Zigzag Drawing Object

Fields:

zigzagLine (series line) : Line joining two pivots

zigzagLabel (series label) : Label which can be used for drawing the values, ratios, directions etc.

ZigzagProperties

Object which holds properties of zigzag drawing. To be used along with ZigzagDrawing

Fields:

lineColor (series color) : Zigzag line color. Default is color.blue

lineWidth (series int) : Zigzag line width. Default is 1

lineStyle (series string) : Zigzag line style. Default is line.style_solid.

showLabel (series bool) : If set, the drawing will show labels on each pivot. Default is false

textColor (series color) : Text color of the labels. Only applicable if showLabel is set to true.

maxObjects (series int) : Max number of zigzag lines to display. Default is 300

xloc (series string) : Time/Bar reference to be used for zigzag drawing. Default is Time - xloc.bar_time.

curved (series bool) : Boolean field to print curved zigzag - used only with polyline implementation

ZigzagDrawing

Object which holds complete zigzag drawing objects and properties.

Fields:

zigzag (Zigzag) : Zigzag object which holds the calculations.

properties (ZigzagProperties) : ZigzagProperties object which is used for setting the display styles of zigzag

drawings (ZigzagObject ) : array which contains lines and labels of zigzag drawing.

ZigzagDrawingPL

Object which holds complete zigzag drawing objects and properties - polyline version

Fields:

zigzag (Zigzag) : Zigzag object which holds the calculations.

properties (ZigzagProperties) : ZigzagProperties object which is used for setting the display styles of zigzag

zigzagLabels (label )

zigzagLine (series polyline) : polyline object of zigzag lines

ZigzagLibrary "Zigzag"

Zigzag related user defined types. Depends on DrawingTypes library for basic types

method tostring(this, sortKeys, sortOrder, includeKeys)

Converts ZigzagTypes/Pivot object to string representation

Namespace types: Pivot

Parameters:

this (Pivot) : ZigzagTypes/Pivot

sortKeys (bool) : If set to true, string output is sorted by keys.

sortOrder (int) : Applicable only if sortKeys is set to true. Positive number will sort them in ascending order whreas negative numer will sort them in descending order. Passing 0 will not sort the keys

includeKeys (string ) : Array of string containing selective keys. Optional parmaeter. If not provided, all the keys are considered

Returns: string representation of ZigzagTypes/Pivot

method tostring(this, sortKeys, sortOrder, includeKeys)

Converts Array of Pivot objects to string representation

Namespace types: Pivot

Parameters:

this (Pivot ) : Pivot object array

sortKeys (bool) : If set to true, string output is sorted by keys.

sortOrder (int) : Applicable only if sortKeys is set to true. Positive number will sort them in ascending order whreas negative numer will sort them in descending order. Passing 0 will not sort the keys

includeKeys (string ) : Array of string containing selective keys. Optional parmaeter. If not provided, all the keys are considered

Returns: string representation of Pivot object array

method tostring(this)

Converts ZigzagFlags object to string representation

Namespace types: ZigzagFlags

Parameters:

this (ZigzagFlags) : ZigzagFlags object

Returns: string representation of ZigzagFlags

method tostring(this, sortKeys, sortOrder, includeKeys)

Converts ZigzagTypes/Zigzag object to string representation

Namespace types: Zigzag

Parameters:

this (Zigzag) : ZigzagTypes/Zigzagobject

sortKeys (bool) : If set to true, string output is sorted by keys.

sortOrder (int) : Applicable only if sortKeys is set to true. Positive number will sort them in ascending order whreas negative numer will sort them in descending order. Passing 0 will not sort the keys

includeKeys (string ) : Array of string containing selective keys. Optional parmaeter. If not provided, all the keys are considered

Returns: string representation of ZigzagTypes/Zigzag

method calculate(this, ohlc, indicators, indicatorNames)

Calculate zigzag based on input values and indicator values

Namespace types: Zigzag

Parameters:

this (Zigzag) : Zigzag object

ohlc (float ) : Array containing OHLC values. Can also have custom values for which zigzag to be calculated

indicators (matrix) : Array of indicator values

indicatorNames (string ) : Array of indicator names for which values are present. Size of indicators array should be equal to that of indicatorNames

Returns: current Zigzag object

method calculate(this)

Calculate zigzag based on properties embedded within Zigzag object

Namespace types: Zigzag

Parameters:

this (Zigzag) : Zigzag object

Returns: current Zigzag object

method nextlevel(this)

Calculate Next Level Zigzag based on the current calculated zigzag object

Namespace types: Zigzag

Parameters:

this (Zigzag) : Zigzag object

Returns: Next Level Zigzag object

method clear(this)

Clears zigzag drawings array

Namespace types: ZigzagDrawing

Parameters:

this (ZigzagDrawing ) : array

Returns: void

method drawplain(this)

draws fresh zigzag based on properties embedded in ZigzagDrawing object without trying to calculate

Namespace types: ZigzagDrawing

Parameters:

this (ZigzagDrawing) : ZigzagDrawing object

Returns: ZigzagDrawing object

method drawfresh(this, ohlc, indicators, indicatorNames)

draws fresh zigzag based on properties embedded in ZigzagDrawing object

Namespace types: ZigzagDrawing

Parameters:

this (ZigzagDrawing) : ZigzagDrawing object

ohlc (float ) : values on which the zigzag needs to be calculated and drawn. If not set will use regular OHLC

indicators (matrix) : Array of indicator values

indicatorNames (string ) : Array of indicator names for which values are present. Size of indicators array should be equal to that of indicatorNames

Returns: ZigzagDrawing object

method drawcontinuous(this, ohlc, indicators, indicatorNames)

draws zigzag based on the zigzagmatrix input

Namespace types: ZigzagDrawing

Parameters:

this (ZigzagDrawing) : ZigzagDrawing object

ohlc (float ) : values on which the zigzag needs to be calculated and drawn. If not set will use regular OHLC

indicators (matrix) : Array of indicator values

indicatorNames (string ) : Array of indicator names for which values are present. Size of indicators array should be equal to that of indicatorNames

Returns:

method getPrices(pivots)

Namespace types: Pivot

Parameters:

pivots (Pivot )

method getBars(pivots)

Namespace types: Pivot

Parameters:

pivots (Pivot )

Indicator

Indicator is collection of indicator values applied on high, low and close

Fields:

indicatorHigh (series float) : Indicator Value applied on High

indicatorLow (series float) : Indicator Value applied on Low

PivotCandle

PivotCandle represents data of the candle which forms either pivot High or pivot low or both

Fields:

_high (series float) : High price of candle forming the pivot

_low (series float) : Low price of candle forming the pivot

length (series int) : Pivot length

pHighBar (series int) : represents number of bar back the pivot High occurred.

pLowBar (series int) : represents number of bar back the pivot Low occurred.

pHigh (series float) : Pivot High Price

pLow (series float) : Pivot Low Price

indicators (Indicator ) : Array of Indicators - allows to add multiple

Pivot

Pivot refers to zigzag pivot. Each pivot can contain various data

Fields:

point (chart.point) : pivot point coordinates

dir (series int) : direction of the pivot. Valid values are 1, -1, 2, -2

level (series int) : is used for multi level zigzags. For single level, it will always be 0

componentIndex (series int) : is the lower level zigzag array index for given pivot. Used only in multi level Zigzag Pivots

subComponents (series int) : is the number of sub waves per each zigzag wave. Only applicable for multi level zigzags

microComponents (series int) : is the number of base zigzag components in a zigzag wave

ratio (series float) : Price Ratio based on previous two pivots

sizeRatio (series float)

subPivots (Pivot )

indicatorNames (string ) : Names of the indicators applied on zigzag

indicatorValues (float ) : Values of the indicators applied on zigzag

indicatorRatios (float ) : Ratios of the indicators applied on zigzag based on previous 2 pivots

ZigzagFlags

Flags required for drawing zigzag. Only used internally in zigzag calculation. Should not set the values explicitly

Fields:

newPivot (series bool) : true if the calculation resulted in new pivot

doublePivot (series bool) : true if the calculation resulted in two pivots on same bar

updateLastPivot (series bool) : true if new pivot calculated replaces the old one.

Zigzag

Zigzag object which contains whole zigzag calculation parameters and pivots

Fields:

length (series int) : Zigzag length. Default value is 5

numberOfPivots (series int) : max number of pivots to hold in the calculation. Default value is 20

offset (series int) : Bar offset to be considered for calculation of zigzag. Default is 0 - which means calculation is done based on the latest bar.

level (series int) : Zigzag calculation level - used in multi level recursive zigzags

zigzagPivots (Pivot ) : array which holds the last n pivots calculated.

flags (ZigzagFlags) : ZigzagFlags object which is required for continuous drawing of zigzag lines.

ZigzagObject

Zigzag Drawing Object

Fields:

zigzagLine (series line) : Line joining two pivots

zigzagLabel (series label) : Label which can be used for drawing the values, ratios, directions etc.

ZigzagProperties

Object which holds properties of zigzag drawing. To be used along with ZigzagDrawing

Fields:

lineColor (series color) : Zigzag line color. Default is color.blue

lineWidth (series int) : Zigzag line width. Default is 1

lineStyle (series string) : Zigzag line style. Default is line.style_solid.

showLabel (series bool) : If set, the drawing will show labels on each pivot. Default is false

textColor (series color) : Text color of the labels. Only applicable if showLabel is set to true.

maxObjects (series int) : Max number of zigzag lines to display. Default is 300

xloc (series string) : Time/Bar reference to be used for zigzag drawing. Default is Time - xloc.bar_time.

ZigzagDrawing

Object which holds complete zigzag drawing objects and properties.

Fields:

zigzag (Zigzag) : Zigzag object which holds the calculations.

properties (ZigzagProperties) : ZigzagProperties object which is used for setting the display styles of zigzag

drawings (ZigzagObject ) : array which contains lines and labels of zigzag drawing.

ZigzagTypesLibrary "ZigzagTypes"

Zigzag related user defined types. Depends on DrawingTypes library for basic types

Indicator

Indicator is collection of indicator values applied on high, low and close

Fields:

indicatorHigh : Indicator Value applied on High

indicatorLow : Indicator Value applied on Low

PivotCandle

PivotCandle represents data of the candle which forms either pivot High or pivot low or both

Fields:

_high : High price of candle forming the pivot

_low : Low price of candle forming the pivot

length : Pivot length

pHighBar : represents number of bar back the pivot High occurred.

pLowBar : represents number of bar back the pivot Low occurred.

pHigh : Pivot High Price

pLow : Pivot Low Price

indicators : Array of Indicators - allows to add multiple

Pivot

Pivot refers to zigzag pivot. Each pivot can contain various data

Fields:

point : pivot point coordinates

dir : direction of the pivot. Valid values are 1, -1, 2, -2

level : is used for multi level zigzags. For single level, it will always be 0

ratio : Price Ratio based on previous two pivots

indicatorNames : Names of the indicators applied on zigzag

indicatorValues : Values of the indicators applied on zigzag

indicatorRatios : Ratios of the indicators applied on zigzag based on previous 2 pivots

ZigzagFlags

Flags required for drawing zigzag. Only used internally in zigzag calculation. Should not set the values explicitly

Fields:

newPivot : true if the calculation resulted in new pivot

doublePivot : true if the calculation resulted in two pivots on same bar

updateLastPivot : true if new pivot calculated replaces the old one.

Zigzag

Zigzag object which contains whole zigzag calculation parameters and pivots

Fields:

length : Zigzag length. Default value is 5

numberOfPivots : max number of pivots to hold in the calculation. Default value is 20

offset : Bar offset to be considered for calculation of zigzag. Default is 0 - which means calculation is done based on the latest bar.

level : Zigzag calculation level - used in multi level recursive zigzags

zigzagPivots : array which holds the last n pivots calculated.

flags : ZigzagFlags object which is required for continuous drawing of zigzag lines.

ZigzagObject

Zigzag Drawing Object

Fields:

zigzagLine : Line joining two pivots

zigzagLabel : Label which can be used for drawing the values, ratios, directions etc.

ZigzagProperties

Object which holds properties of zigzag drawing. To be used along with ZigzagDrawing

Fields:

lineColor : Zigzag line color. Default is color.blue

lineWidth : Zigzag line width. Default is 1

lineStyle : Zigzag line style. Default is line.style_solid.

showLabel : If set, the drawing will show labels on each pivot. Default is false

textColor : Text color of the labels. Only applicable if showLabel is set to true.

maxObjects : Max number of zigzag lines to display. Default is 300

xloc : Time/Bar reference to be used for zigzag drawing. Default is Time - xloc.bar_time.

ZigzagDrawing

Object which holds complete zigzag drawing objects and properties.

Fields:

properties : ZigzagProperties object which is used for setting the display styles of zigzag

drawings : array which contains lines and labels of zigzag drawing.

zigzag : Zigzag object which holds the calculations.

Chart Info & Signature## Overview

Chart Info & Signature displays customizable information tables on your TradingView chart. It consists of two independent tables that can be positioned anywhere on the chart and fully customized to match your branding and preferences.

---

## Table 1: Market Info Table

### What It Displays

The Market Info Table shows essential trading information:

1. **Exchange** - The exchange name (e.g., "BINANCE", "NASDAQ")

2. **Trading Pair** - The symbol pair (e.g., "BTC/USD", "EUR/USD") with optional timeframe

3. **Date** - Current date in DD/MM/YYYY format

4. **Signature** (optional) - Custom text that appears below the date

### Positioning

- **Vertical Position**: Top, Middle, or Bottom of the chart

- **Horizontal Position**: Left, Center, or Right of the chart

- **Exchange Position**: Can be placed at the top or bottom of the table

### Customization Options

#### Exchange Settings

- Show/Hide exchange name

- Text size (tiny, small, normal, large, huge, auto)

- Text color

- Background color

- Position (top or bottom of table)

#### Pair Settings

- Pair delimiter (default: "/")

- Text size

- Text color

- Background color

#### Timeframe Settings

- Show/Hide timeframe (displays current chart timeframe like "1h", "15m", "1D")

#### Date Settings

- Show/Hide date

- Text size

- Text color

- Background color

#### Signature Settings (Below Date)

- Show/Hide signature

- Custom text

- Text size

- Text color

- Background color

- Spacing before signature (with adjustable size)

---

## Table 2: Signature Table

### What It Displays

The Signature Table displays up to 3 customizable text lines, perfect for contact information or any custom text you want to display.

### Positioning

- **Vertical Position**: Top, Middle, or Bottom of the chart

- **Horizontal Position**: Left, Center, or Right of the chart

### Customization Options

#### Line 1 (Top Line)

- Show/Hide line

- Custom text

- Text size

- Text color

- Background color

- Spacing after line (with adjustable size)

#### Line 2 (Middle Line)

- Show/Hide line

- Custom text

- Text size

- Text color

- Background color

- Spacing after line (with adjustable size)

#### Line 3 (Bottom Line)

- Show/Hide line

- Custom text

- Text size

- Text color

- Background color

### Smart Positioning

The table automatically adjusts the spacing between lines based on which lines are visible, ensuring proper alignment regardless of which lines you choose to display.

---

## Key Features

### ✅ Fully Customizable

- Every element can be shown or hidden

- Individual text sizes for each element

- Custom colors for text and backgrounds

- Adjustable spacing between elements

### ✅ Flexible Positioning

- Each table can be positioned independently

- 9 possible positions per table (3 vertical × 3 horizontal)

- Tables can overlap or be placed separately

### ✅ Organized Settings

- Settings are organized into logical groups and subgroups

- Easy to find and modify specific elements

- Clean, intuitive settings panel

### ✅ Dynamic Content

- Trading pair automatically updates based on chart symbol

- Timeframe automatically matches current chart timeframe

- Date updates in real-time

- Exchange name pulled from symbol information

---

## Text Size Options

All text size settings support the following options:

- **tiny** - Smallest fixed size

- **small** - Small fixed size

- **normal** - Standard fixed size

- **large** - Large fixed size

- **huge** - Largest fixed size

- **auto** - Automatically adjusts based on chart zoom and screen size

---

## Default Configuration

- **Market Info Table**: Positioned at top-right, showing exchange, pair with timeframe, and date. Signature row in Market Info Table is hidden by default.

- **Signature Table**: Positioned at bottom-right, showing 3 signature lines with added spacing between line 1 and line 2

- All text uses semi-transparent white (#ffffff77) by default

- All backgrounds are transparent by default

---

## Tips

1. Use **auto** text size for elements that need to scale with chart zoom

2. Use transparent backgrounds for a clean, minimal look

3. Position tables in corners to avoid interfering with price action

4. Customize colors to match your chart theme

5. Hide elements you don't need to keep the display clean

Michael's Custom Watermark🔷 MICHAEL'S CUSTOM WATERMARK INDICATOR

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

📊 OVERVIEW

A comprehensive chart watermark overlay that displays essential fundamental and technical information for stocks in a clean, customizable table format. Perfect for traders who want quick access to key metrics without cluttering their charts.

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

✨ KEY FEATURES

📊 Fundamental Data Display — Shows Industry, Sector, Market Cap, and P/E Ratio

📅 Earnings Information — Displays next earnings date with countdown timer

📈 ATR Volatility Indicator — 14-day ATR with color-coded visual alerts (🔴🟡🟢)

🎨 Auto Theme Detection — Automatically adjusts text color based on chart background

⚙️ Fully Customizable — Position, colors, size, and displayed metrics all adjustable

🏢 GICS Sector Mapping — Heuristic-based sector classification aligned with industry standards

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

🎯 WHAT MAKES THIS INDICATOR UNIQUE?

Unlike basic watermarks, this indicator provides:

Real-time fundamental data integration

Smart theme-aware color adaptation for both light and dark charts

Configurable volatility alerts using ATR thresholds

Earnings countdown feature to never miss important dates

Optimized display that only shows relevant data for the current symbol type

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

📖 HOW TO USE

1. BASIC SETUP

Add the indicator to your chart. By default, it displays in the top-left corner with all features enabled.

2. POSITIONING

Vertical Location: Top, Middle, or Bottom

Horizontal Location: Left, Center, or Right

Vertical Offset: Fine-tune position with 0-50 pixel offset from top

3. CUSTOMIZATION OPTIONS

TEXT APPEARANCE:

Auto Text Color — Enable to automatically adapt text color to your chart theme

Manual Color — Set a fixed text color if auto-color is disabled

Text Size — Choose from Huge, Large, Normal, or Small

Theme Colors — Customize text color for light and dark backgrounds separately

DATA DISPLAY TOGGLES:

Show Industry & Sector — Display heuristic-based GICS-aligned sector and industry classification

Show Market Cap — View market capitalization in T/B/M format

Show P/E Ratio — Display Price-to-Earnings ratio (stocks only)

Show ATR (14-Day) — Display Average True Range with percentage and visual indicator

Show Next Earnings — Display upcoming earnings information

Show Earnings Countdown — Show days remaining until next earnings (requires earnings display)

4. ATR VOLATILITY ALERTS

Configure custom thresholds to monitor volatility:

Red Threshold — ATR percentage that triggers red alert 🔴 (default: 6%)

Yellow Threshold — ATR percentage that triggers yellow alert 🟡 (default: 3%)

Green — Shows automatically when ATR is below yellow threshold 🟢

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

📐 UNDERSTANDING THE DISPLAY

🏢 SECTOR & INDUSTRY

Shows the GICS sector classification followed by the specific industry. The indicator uses heuristic-based mapping to align TradingView sectors with standard GICS classifications. Note that this mapping is based on keyword detection and industry analysis, so while generally accurate, it may not perfectly match official GICS classifications in all cases.

💰 MARKET CAP

Displays market capitalization using standard abbreviations:

T = Trillion

B = Billion

M = Million

📊 P/E RATIO

Shows the trailing twelve-month Price-to-Earnings ratio. Only displayed for stocks when enabled. Shows "N/A" if data is unavailable.

📈 ATR (14-DAY)

Displays the 14-period Average True Range in both absolute value and percentage terms, with a color-coded indicator:

🔴 Red: High volatility (above red threshold)

🟡 Yellow: Moderate volatility (between yellow and red thresholds)

🟢 Green: Low volatility (below yellow threshold)

📅 EARNINGS

Shows earnings information in three formats:

"X days remaining" — When countdown is enabled and earnings date is known

"Upcoming" — When date is in the future but countdown is disabled

"Recently Reported" — When earnings just occurred

"N/A" — When no earnings data is available

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

⚙️ TECHNICAL DETAILS

SUPPORTED INSTRUMENTS:

Optimized for stocks with full fundamental data

Works with other instruments (crypto, forex, futures) but only displays applicable metrics

Automatically suppresses irrelevant data (e.g., P/E for non-stocks)

PERFORMANCE:

Lightweight overlay with minimal resource usage

Updates only on last bar for efficiency

No historical recalculation needed

COMPATIBILITY:

Pine Script v6

Works on all timeframes

Compatible with all chart types

Auto-adapts to theme changes

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

💡 TIPS & BEST PRACTICES

Enable Auto Text Color for seamless theme switching between light and dark modes

Adjust vertical offset to avoid overlap with price action in high-volatility periods

Use ATR thresholds appropriate to your trading style and asset class

Disable features you don't use to keep the watermark clean and focused

Position in corners to maximize chart viewing space

Use smaller text size for multi-panel layouts

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

🔧 TROUBLESHOOTING

"N/A" SHOWING FOR P/E RATIO:

This is normal for non-stock instruments

May occur for stocks with negative earnings

Check if fundamental data is available for the symbol

EARNINGS SHOWING "N/A":

Earnings data may not be available for all stocks

Check TradingView's data coverage for your symbol

TEXT COLOR NOT VISIBLE:

Enable Auto Text Color feature

Manually set text color to contrast with your chart background

Adjust custom light/dark text colors in settings

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

⚠️ DISCLAIMER

This indicator is for informational purposes only. The fundamental data displayed is sourced from TradingView's data providers. Always verify critical information before making trading decisions. Past performance is not indicative of future results.

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

If you find this indicator helpful, please give it a boost 🚀 and share your feedback in the comments!

Version: 1.0

Pine Script Version: v6

Created by: Michael

Adaptive Volume‐Demand‐Index (AVDI)Demand Index (according to James Sibbet) – Short Description

The Demand Index (DI) was developed by James Sibbet to measure real “buying” vs. “selling” strength (Demand vs. Supply) using price and volume data. It is not a standalone trading signal, but rather a filter and trend confirmer that should always be used together with chart structure and additional indicators.

---

\ 1. Calculation Basis\

1. Volume Normalization

$$

\text{normVol}_t

= \frac{\text{Volume}_t}{\mathrm{EMA}(\text{Volume},\,n_{\text{Vol}})_t}

\quad(\text{e.g., }n_{\text{Vol}} = 13)

$$

This smooths out extremely high volume spikes and compares them to the average (≈ 1 means “average volume”).

2. Price Factor

$$

\text{priceFactor}_t

= \frac{\text{Close}_t - \text{Open}_t}{\text{Open}_t}.

$$

Positive values for bullish bars, negative for bearish bars.

3. Component per Bar

$$

\text{component}_t

= \text{normVol}_t \times \text{priceFactor}_t.

$$

If volume is above average (> 1) and the price rises slightly, this yields a noticeably positive value; conversely if the price falls.

4. Raw DI (Rolling Sum)

Over a window of \$w\$ bars (e.g., 20):

$$

\text{RawDI}_t

= \sum_{i=0}^{w-1} \text{component}_{\,t-i}.

$$

Alternatively, recursively for \$t \ge w\$:

$$

\text{RawDI}_t

= \text{RawDI}_{t-1}

+ \text{component}_t

- \text{component}_{\,t-w}.

$$

5. Optional EMA Smoothing

An EMA over RawDI (e.g., \$n\_{\text{DI}} = 50\$) reduces short-term fluctuations and highlights medium-term trends:

$$

\text{EMA\_DI}_t

= \mathrm{EMA}(\text{RawDI},\,n_{\text{DI}})_t.

$$

6.Zero Line

Handy guideline:

RawDI > 0: Accumulated buying power dominates.

RawDI < 0: Accumulated selling power dominates.

2. Interpretation & Application

Crossing Zero

RawDI above zero → Indication of increasing buying pressure (potential long signal).

RawDI below zero → Indication of increasing selling pressure (potential short signal).

Not to be used alone for entry—always confirm with price action.

RawDI vs. EMA_DI

RawDI > EMA\_DI → Acceleration of demand.

RawDI < EMA\_DI → Weakening of demand.

Divergences

Price makes a new high, RawDI does not make a higher high → potential weakness in the uptrend.

Price makes a new low, RawDI does not make a lower low → potential exhaustion of the downtrend.

3. Typical Signals (for Beginners)

\ 1. Long Setup\

RawDI crosses zero from below,

RawDI > EMA\_DI (acceleration),

Price closes above a short-term swing high or resistance.

Stop-Loss: just below the last swing low, Take-Profit/Trailing: on reversal signals or fixed R\:R.

2. Short Setup

RawDI crosses zero from above,

RawDI < EMA\_DI (increased selling pressure),

Price closes below a short-term swing low or support.

Stop-Loss: just above the last swing high.

---

4. Notes and Parameters

Recommended Values (Beginners):

Volume EMA (n₍Vol₎) = 13

RawDI window (w) = 20

EMA over DI (n₍DI₎) = 50 (medium-term) or 1 (no smoothing)

Attention:\

NEVER use in isolation. Always in combination with price action analysis (trendlines, support/resistance, candlestick patterns).

Especially during volatile news phases, RawDI can fluctuate strongly → EMA\_DI helps to avoid false signals.

---

Conclusion The Demand Index by James Sibbet is a powerful filter to assess price movements by their volume backing. It shows whether a rally is truly driven by demand or merely a short-term volume anomaly. In combination with classic chart analysis and risk management, it helps to identify robust entry points and potential trend reversals earlier.

ADR% Extension Levels from SMA 50I created this indicator inspired by RealSimpleAriel (a swing trader I recommend following on X) who does not buy stocks extended beyond 4 ADR% from the 50 SMA and uses extensions from the 50 SMA at 7-8-9-10-11-12-13 ADR% to take profits with a 20% position trimming.

RealSimpleAriel's strategy (as I understood it):

-> Focuses on leading stocks from leading groups and industries, i.e., those that have grown the most in the last 1-3-6 months (see on Finviz groups and then select sector-industry).

-> Targets stocks with the best technical setup for a breakout, above the 200 SMA in a bear market and above both the 50 SMA and 200 SMA in a bull market, selecting those with growing Earnings and Sales.

-> Buys stocks on breakout with a stop loss set at the day's low of the breakout and ensures they are not extended beyond 4 ADR% from the 50 SMA.

-> 3-5 day momentum burst: After a breakout, takes profits by selling 1/2 or 1/3 of the position after a 3-5 day upward move.

-> 20% trimming on extension from the 50 SMA: At 7 ADR% (ADR% calculated over 20 days) extension from the 50 SMA, takes profits by selling 20% of the remaining position. Continues to trim 20% of the remaining position based on the stock price extension from the 50 SMA, calculated using the 20-period ADR%, thus trimming 20% at 8-9-10-11 ADR% extension from the 50 SMA. Upon reaching 12-13 ADR% extension from the 50 SMA, considers the stock overextended, closes the remaining position, and evaluates a short.

-> Trailing stop with ascending SMA: Uses a chosen SMA (10, 20, or 50) as the definitive stop loss for the position, depending on the stock's movement speed (preferring larger SMAs for slower-moving stocks or for long-term theses). If the stock's closing price falls below the chosen SMA, the entire position is closed.

In summary:

-->Buy a breakout using the day's low of the breakout as the stop loss (this stop loss is the most critical).

--> Do not buy stocks extended beyond 4 ADR% from the 50 SMA.

--> Sell 1/2 or 1/3 of the position after 3-5 days of upward movement.

--> Trim 20% of the position at each 7-8-9-10-11-12-13 ADR% extension from the 50 SMA.

--> Close the entire position if the breakout fails and the day's low of the breakout is reached.

--> Close the entire position if the price, during the rise, falls below a chosen SMA (10, 20, or 50, depending on your preference).

--> Definitively close the position if it reaches 12-13 ADR% extension from the 50 SMA.

I used Grok from X to create this indicator. I am not a programmer, but based on the ADR% I use, it works.

Below is Grok from X's description of the indicator:

Script Description

The script is a custom indicator for TradingView that displays extension levels based on ADR% relative to the 50-period Simple Moving Average (SMA). Below is a detailed description of its features, structure, and behavior:

1. Purpose of the Indicator

Name: "ADR% Extension Levels from SMA 50".

Objective: Draw horizontal blue lines above and below the 50-period SMA, corresponding to specific ADR% multiples (4, 7, 8, 9, 10, 11, 12, 13). These levels represent potential price extension zones based on the average daily percentage volatility.

Overlay: The indicator is overlaid on the price chart (overlay=true), so the lines and SMA appear directly on the price graph.

2. Configurable Inputs

The indicator allows users to customize parameters through TradingView settings:

SMA Length (smaLength):

Default: 50 periods.

Description: Specifies the number of periods for calculating the Simple Moving Average (SMA). The 50-period SMA serves as the reference point for extension levels.

Constraint: Minimum 1 period.

ADR% Length (adrLength):

Default: 20 periods.

Description: Specifies the number of days to calculate the moving average of the daily high/low ratio, used to determine ADR%.

Constraint: Minimum 1 period.

Scale Factor (scaleFactor):

Default: 1.0.

Description: An optional multiplier to adjust the distance of extension levels from the SMA. Useful if levels are too close or too far due to an overly small or large ADR%.

Constraint: Minimum 0.1, increments of 0.1.

Tooltip: "Adjust if levels are too close or far from SMA".

3. Main Calculations

50-period SMA:

Calculated with ta.sma(close, smaLength) using the closing price (close).

Serves as the central line around which extension levels are drawn.

ADR% (Average Daily Range Percentage):

Formula: 100 * (ta.sma(dhigh / dlow, adrLength) - 1).

Details:

dhigh and dlow are the daily high and low prices, obtained via request.security(syminfo.tickerid, "D", high/low) to ensure data is daily-based, regardless of the chart's timeframe.

The dhigh / dlow ratio represents the daily percentage change.

The simple moving average (ta.sma) of this ratio over 20 days (adrLength) is subtracted by 1 and multiplied by 100 to obtain ADR% as a percentage.

The result is multiplied by scaleFactor for manual adjustments.

Extension Levels:

Defined as ADR% multiples: 4, 7, 8, 9, 10, 11, 12, 13.

Stored in an array (levels) for easy iteration.

For each level, prices above and below the SMA are calculated as:

Above: sma50 * (1 + (level * adrPercent / 100))

Below: sma50 * (1 - (level * adrPercent / 100))

These represent price levels corresponding to a percentage change from the SMA equal to level * ADR%.

4. Visualization

Horizontal Blue Lines:

For each level (4, 7, 8, 9, 10, 11, 12, 13 ADR%), two lines are drawn:

One above the SMA (e.g., +4 ADR%).

One below the SMA (e.g., -4 ADR%).

Color: Blue (color.blue).

Style: Solid (style=line.style_solid).

Management:

Each level has dedicated variables for upper and lower lines (e.g., upperLine1, lowerLine1 for 4 ADR%).

Previous lines are deleted with line.delete before drawing new ones to avoid overlaps.

Lines are updated at each bar with line.new(bar_index , level, bar_index, level), covering the range from the previous bar to the current one.

Labels:

Displayed only on the last bar (barstate.islast) to avoid clutter.

For each level, two labels:

Above: E.g., "4 ADR%", positioned above the upper line (style=label.style_label_down).

Below: E.g., "-4 ADR%", positioned below the lower line (style=label.style_label_up).

Color: Blue background, white text.

50-period SMA:

Drawn as a gray line (color.gray) for visual reference.

Diagnostics:

ADR% Plot: ADR% is plotted in the status line (orange, histogram style) to verify the value.

ADR% Label: A label on the last bar near the SMA shows the exact ADR% value (e.g., "ADR%: 2.34%"), with a gray background and white text.

5. Behavior

Dynamic Updating:

Lines update with each new bar to reflect new SMA 50 and ADR% values.

Since ADR% uses daily data ("D"), it remains constant within the same day but changes day-to-day.

Visibility Across All Bars:

Lines are drawn on every bar, not just the last one, ensuring visibility on historical data as well.

Adaptability:

The scaleFactor allows level adjustments if ADR% is too small (e.g., for low-volatility symbols) or too large (e.g., for cryptocurrencies).

Compatibility:

Works on any timeframe since ADR% is calculated from daily data.

Suitable for symbols with varying volatility (e.g., stocks, forex, cryptocurrencies).

6. Intended Use

Technical Analysis: Extension levels represent significant price zones based on average daily volatility. They can be used to:

Identify potential price targets (e.g., take profit at +7 ADR%).

Assess support/resistance zones (e.g., -4 ADR% as support).

Measure price extension relative to the 50 SMA.

Trading: Useful for strategies based on breakouts or mean reversion, where ADR% levels indicate reversal or continuation points.

Debugging: Labels and ADR% plot help verify that values align with the symbol’s volatility.

7. Limitations

Dependence on Daily Data: ADR% is based on daily dhigh/dlow, so it may not reflect intraday volatility on short timeframes (e.g., 1 minute).

Extreme ADR% Values: For low-volatility symbols (e.g., bonds) or high-volatility symbols (e.g., meme stocks), ADR% may require adjustments via scaleFactor.

Graphical Load: Drawing 16 lines (8 upper, 8 lower) on every bar may slow the chart for very long historical periods, though line management is optimized.

ADR% Formula: The formula 100 * (sma(dhigh/dlow, Length) - 1) may produce different values compared to other ADR% definitions (e.g., (high - low) / close * 100), so users should be aware of the context.

8. Visual Example

On a chart of a stock like TSLA (daily timeframe):

The 50 SMA is a gray line tracking the average trend.

Assuming an ADR% of 3%:

At +4 ADR% (12%), a blue line appears at sma50 * 1.12.

At -4 ADR% (-12%), a blue line appears at sma50 * 0.88.

Other lines appear at ±7, ±8, ±9, ±10, ±11, ±12, ±13 ADR%.

On the last bar, labels show "4 ADR%", "-4 ADR%", etc., and a gray label shows "ADR%: 3.00%".

ADR% is visible in the status line as an orange histogram.

9. Code: Technical Structure

Language: Pine Script @version=5.

Inputs: Three configurable parameters (smaLength, adrLength, scaleFactor).

Calculations:

SMA: ta.sma(close, smaLength).

ADR%: 100 * (ta.sma(dhigh / dlow, adrLength) - 1) * scaleFactor.

Levels: sma50 * (1 ± (level * adrPercent / 100)).

Graphics:

Lines: Created with line.new, deleted with line.delete to avoid overlaps.

Labels: Created with label.new only on the last bar.

Plots: plot(sma50) for the SMA, plot(adrPercent) for debugging.

Optimization: Uses dedicated variables for each line (e.g., upperLine1, lowerLine1) for clear management and to respect TradingView’s graphical object limits.

10. Possible Improvements

Option to show lines only on the last bar: Would reduce visual clutter.

Customizable line styles: Allow users to choose color or style (e.g., dashed).

Alert for anomalous ADR%: A message if ADR% is too small or large.

Dynamic levels: Allow users to specify ADR% multiples via input.

Optimization for short timeframes: Adapt ADR% for intraday timeframes.

Conclusion

The script creates a visual indicator that helps traders identify price extension levels based on daily volatility (ADR%) relative to the 50 SMA. It is robust, configurable, and includes debugging tools (ADR% plot and labels) to verify values. The ADR% formula based on dhigh/dlow

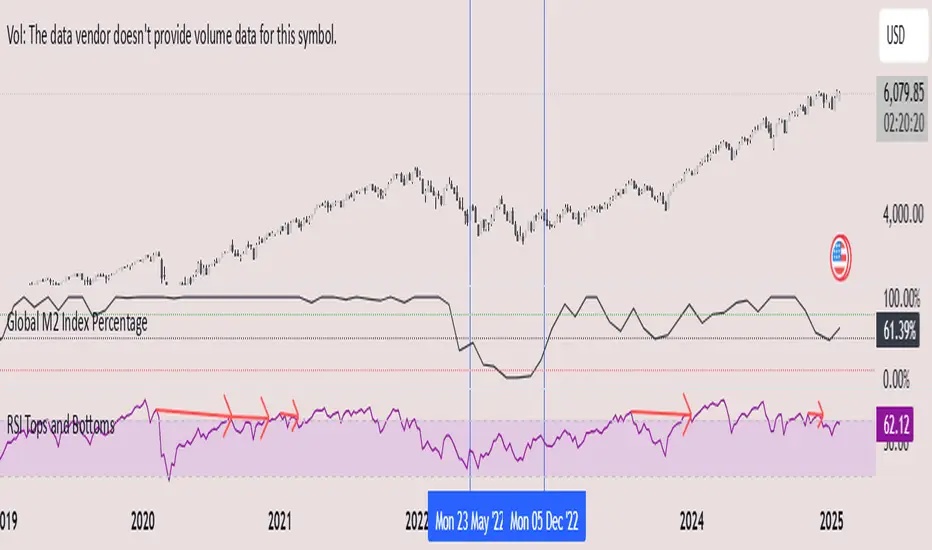

Global M2 Index Percentage### **Global M2 Index Percentage**

**Description:**

The **Global M2 Index Percentage** is a custom indicator designed to track and visualize the global money supply (M2) in a normalized percentage format. It aggregates M2 data from major economies (e.g., the US, EU, China, Japan, and the UK) and adjusts for exchange rates to provide a comprehensive view of global liquidity. This indicator helps traders and investors understand the broader macroeconomic environment, identify trends in money supply, and make informed decisions based on global liquidity conditions.

---

### **How It Works:**

1. **Data Aggregation**:

- The indicator collects M2 data from key economies and adjusts it using exchange rates to calculate a global M2 value.

- The formula for global M2 is:

\

2. **Normalization**:

- The global M2 value is normalized into a percentage (0% to 100%) based on its range over a user-defined period (default: 13 weeks).

- The formula for normalization is:

\

3. **Visualization**:

- The indicator plots the M2 Index as a line chart.

- Key reference levels are highlighted:

- **10% (Red Line)**: Oversold level (low liquidity).

- **50% (Black Line)**: Neutral level.

- **80% (Green Line)**: Overbought level (high liquidity).

---

### **How to Use the Indicator:**

#### **1. Understanding the M2 Index:**

- **Below 10%**: Indicates extremely low liquidity, which may signal economic contraction or tight monetary policy.

- **Above 80%**: Indicates high liquidity, which may signal loose monetary policy or potential inflationary pressures.

- **Between 10% and 80%**: Represents a neutral to moderate liquidity environment.

#### **2. Trading Strategies:**

- **Long-Term Investing**:

- Use the M2 Index to assess global liquidity trends.

- **High M2 Index (e.g., >80%)**: Consider investing in risk assets (stocks, commodities) as liquidity supports growth.

- **Low M2 Index (e.g., <10%)**: Shift to defensive assets (bonds, gold) as liquidity tightens.

- **Short-Term Trading**:

- Combine the M2 Index with technical indicators (e.g., RSI, MACD) for timing entries and exits.

- **M2 Index Rising + RSI Oversold**: Potential buying opportunity.

- **M2 Index Falling + RSI Overbought**: Potential selling opportunity.

#### **3. Macroeconomic Analysis**:

- Use the M2 Index to monitor the impact of central bank policies (e.g., quantitative easing, rate hikes).

- Correlate the M2 Index with inflation data (CPI, PPI) to anticipate inflationary or deflationary trends.

---

### **Key Features:**

- **Customizable Timeframe**: Adjust the lookback period (e.g., 13 weeks, 26 weeks) to suit your trading style.

- **Multi-Economy Data**: Aggregates M2 data from the US, EU, China, Japan, and the UK for a global perspective.

- **Normalized Output**: Converts raw M2 data into an easy-to-interpret percentage format.

- **Reference Levels**: Includes key levels (10%, 50%, 80%) for quick analysis.

---

### **Example Use Case:**

- **Scenario**: The M2 Index rises from 49% to 62% over two weeks.

- **Interpretation**: Global liquidity is increasing, potentially due to central bank stimulus.

- **Action**:

- **Long-Term**: Increase exposure to equities and commodities.

- **Short-Term**: Look for buying opportunities in oversold assets (e.g., RSI < 30).

---

### **Why Use the Global M2 Index Percentage?**

- **Macro Insights**: Understand the broader economic environment and its impact on financial markets.

- **Risk Management**: Identify periods of high or low liquidity to adjust your portfolio accordingly.

- **Enhanced Timing**: Combine with technical analysis for better entry and exit points.

---

### **Conclusion:**

The **Global M2 Index Percentage** is a powerful tool for traders and investors seeking to incorporate macroeconomic data into their strategies. By tracking global liquidity trends, this indicator helps you make informed decisions, whether you're trading short-term or planning long-term investments. Add it to your TradingView charts today and gain a deeper understanding of the global money supply!

---

**Disclaimer**: This indicator is for informational purposes only and should not be considered financial advice. Always conduct your own research and consult with a professional before making investment decisions.

Visible and Anchored OTE chart [SYNC & TRADE]Thanks for the start @twingall

Visible and Anchored OTE chart

Indicator for visualizing price levels and optimal trading zones (OTE - Optimal Trading Entry) using Fibonacci levels.

Main features

Visualization of price ranges using two OTE zones:

OTE 70% (79-62 Fibonacci levels)

OTE 30% (21-38 Fibonacci levels)

Setting up time periods:

Ability to use a custom date range

Option to work with a higher time frame

Flexible display settings:

Choose between using candle bodies or the full range for binding

Customizable appearance of OTE boxes

Customizable text labels

Additional levels:

Middle line (50.5%)

Optional levels of 29.5%, 70.5% and 88%

Customizable Fibonacci extensions

Indicator settings

Main parameters

Use Custom Dates - enable a custom date range

Start Date/End Date - set a time range

Use Higher Timeframe - use a higher time frame

Higher Timeframe - select a higher timeframe

Setting up OTE zones

Show Fib Box - displaying OTE zones

Enable Fib Box 79-62 - enabling OTE zone 70%

Enable Fib Box 21-38 - enabling OTE zone 30%

Show Text - displaying text labels in zones

Visual design

Text Size - text size (tiny/small/medium/large)

Text Color - text color

Text Alignment - text alignment

Line Thickness - line thickness (1-4)

Line Style - line style (Solid/Dashed/Dotted)

Fibonacci levels

High/Low Lines - displaying extreme levels

Midline - displaying the middle line (50.5%)

Show 29.5 Line - additional level 29.5%

Show 70.5 Line - additional level 70.5%

Show 88 Line - additional level 88%

Extensions Fibonacci

There are 6 customizable extension levels available:

Ext#1 (default 1.0)

Ext#2 (default 1.27)

Ext#3 (default 1.62)

Ext#4 (default 2.0)

Ext#5 (default 2.62)

Ext#6 (default 3.62)

For each level, you can configure:

On/Off

Color

Meaning

Alerts

The indicator provides the following types of alerts:

Entering/Exiting OTE Zones:

Entering 70% OTE Zone

Exiting 70% OTE Zone

Entering 30% OTE Zone

Exiting 30% OTE Zone

Crossing Additional Levels:

Crossing 29.5% Level

Crossing 70.5% Level

Crossing 88% Level

Reaching Extension Levels Fibonacci:

Alerts for each configured extension level

Support for both positive and negative extensions

Usage

Add the indicator to the chart

Configure the required display parameters

Set alerts if necessary

Use OTE zones to identify potential entry points into the market

Notes

The indicator automatically updates when the visible area of the chart changes

When using a custom date range, make sure the selected period contains data

For correct operation with a higher time frame, make sure that historical data is available

Visible and Anchored OTE chart

Индикатор для визуализации ценовых уровней и зон оптимальной торговли (OTE - Optimal Trading Entry) с использованием уровней Фибоначчи.

Основные возможности

Визуализация ценовых диапазонов с помощью двух OTE зон:

OTE 70% (79-62 уровни Фибоначчи)

OTE 30% (21-38 уровни Фибоначчи)

Настройка временных периодов:

Возможность использования пользовательского диапазона дат

Опция работы с высшим таймфреймом

Гибкая настройка отображения:

Выбор между использованием тел свечей или полного диапазона для привязки

Настраиваемый внешний вид боксов OTE

Настраиваемые текстовые метки

Дополнительные уровни:

Средняя линия (50.5%)

Опциональные уровни 29.5%, 70.5% и 88%

Настраиваемые расширения Фибоначчи

Настройка индикатора

Основные параметры

Use Custom Dates - включение пользовательского диапазона дат

Start Date/End Date - установка временного диапазона

Use Higher Timeframe - использование высшего таймфрейма

Higher Timeframe - выбор высшего таймфрейма

Настройка OTE зон

Show Fib Box - отображение зон OTE

Enable Fib Box 79-62 - включение зоны OTE 70%

Enable Fib Box 21-38 - включение зоны OTE 30%

Show Text - отображение текстовых меток в зонах

Визуальное оформление

Text Size - размер текста (tiny/small/medium/large)

Text Color - цвет текста

Text Alignment - выравнивание текста

Line Thickness - толщина линий (1-4)

Line Style - стиль линий (Solid/Dashed/Dotted)

Уровни Фибоначчи

High/Low Lines - отображение крайних уровней

Midline - отображение средней линии (50.5%)

Show 29.5 Line - дополнительный уровень 29.5%

Show 70.5 Line - дополнительный уровень 70.5%

Show 88 Line - дополнительный уровень 88%

Расширения Фибоначчи

Доступно 6 настраиваемых уровней расширения:

Ext#1 (по умолчанию 1.0)

Ext#2 (по умолчанию 1.27)

Ext#3 (по умолчанию 1.62)

Ext#4 (по умолчанию 2.0)

Ext#5 (по умолчанию 2.62)

Ext#6 (по умолчанию 3.62)

Для каждого уровня можно настроить:

Включение/выключение

Цвет

Значение

Оповещения

Индикатор предоставляет следующие типы оповещений:

Вход/выход из зон OTE:

Вход в зону OTE 70%

Выход из зоны OTE 70%

Вход в зону OTE 30%

Выход из зоны OTE 30%

Пересечение дополнительных уровней:

Пересечение уровня 29.5%

Пересечение уровня 70.5%

Пересечение уровня 88%

Достижение уровней расширения Фибоначчи:

Оповещения для каждого настроенного уровня расширения

Поддержка как положительных, так и отрицательных расширений

Использование

Добавьте индикатор на график

Настройте необходимые параметры отображения

При необходимости установите оповещения

Используйте зоны OTE для определения потенциальных точек входа в рынок

Примечания

Индикатор автоматически обновляется при изменении видимой области графика

При использовании пользовательского диапазона дат убедитесь, что выбранный период содержит данные

Для корректной работы с высшим таймфреймом убедитесь в доступности исторических данных

analytics_tablesLibrary "analytics_tables"

📝 Description

This library provides the implementation of several performance-related statistics and metrics, presented in the form of tables.

The metrics shown in the afforementioned tables where developed during the past years of my in-depth analalysis of various strategies in an atempt to reason about the performance of each strategy.

The visualization and some statistics where inspired by the existing implementations of the "Seasonality" script, and the performance matrix implementations of @QuantNomad and @ZenAndTheArtOfTrading scripts.

While this library is meant to be used by my strategy framework "Template Trailing Strategy (Backtester)" script, I wrapped it in a library hoping this can be usefull for other community strategy scripts that will be released in the future.

🤔 How to Guide

To use the functionality this library provides in your script you have to import it first!

Copy the import statement of the latest release by pressing the copy button below and then paste it into your script. Give a short name to this library so you can refer to it later on. The import statement should look like this:

import jason5480/analytics_tables/1 as ant

There are three types of tables provided by this library in the initial release. The stats table the metrics table and the seasonality table.

Each one shows different kinds of performance statistics.

The table UDT shall be initialized once using the `init()` method.

They can be updated using the `update()` method where the updated data UDT object shall be passed.

The data UDT can also initialized and get updated on demend depending on the use case

A code example for the StatsTable is the following:

var ant.StatsData statsData = ant.StatsData.new()

statsData.update(SideStats.new(), SideStats.new(), 0)

if (barstate.islastconfirmedhistory or (barstate.isrealtime and barstate.isconfirmed))

var statsTable = ant.StatsTable.new().init(ant.getTablePos('TOP', 'RIGHT'))

statsTable.update(statsData)

A code example for the MetricsTable is the following:

var ant.StatsData statsData = ant.StatsData.new()

statsData.update(ant.SideStats.new(), ant.SideStats.new(), 0)

if (barstate.islastconfirmedhistory or (barstate.isrealtime and barstate.isconfirmed))

var metricsTable = ant.MetricsTable.new().init(ant.getTablePos('BOTTOM', 'RIGHT'))

metricsTable.update(statsData, 10)

A code example for the SeasonalityTable is the following:

var ant.SeasonalData seasonalData = ant.SeasonalData.new().init(Seasonality.monthOfYear)

seasonalData.update()

if (barstate.islastconfirmedhistory or (barstate.isrealtime and barstate.isconfirmed))

var seasonalTable = ant.SeasonalTable.new().init(seasonalData, ant.getTablePos('BOTTOM', 'LEFT'))

seasonalTable.update(seasonalData)

🏋️♂️ Please refer to the "EXAMPLE" regions of the script for more advanced and up to date code examples!

Special thanks to @Mrcrbw for the proposal to develop this library and @DCNeu for the constructive feedback 🏆.

getTablePos(ypos, xpos)

Get table position compatible string

Parameters:

ypos (simple string) : The position on y axise

xpos (simple string) : The position on x axise

Returns: The position to be passed to the table

method init(this, pos, height, width, positiveTxtColor, negativeTxtColor, neutralTxtColor, positiveBgColor, negativeBgColor, neutralBgColor)

Initialize the stats table object with the given colors in the given position

Namespace types: StatsTable

Parameters:

this (StatsTable) : The stats table object

pos (simple string) : The table position string

height (simple float) : The height of the table as a percentage of the charts height. By default, 0 auto-adjusts the height based on the text inside the cells

width (simple float) : The width of the table as a percentage of the charts height. By default, 0 auto-adjusts the width based on the text inside the cells

positiveTxtColor (simple color) : The text color when positive

negativeTxtColor (simple color) : The text color when negative

neutralTxtColor (simple color) : The text color when neutral

positiveBgColor (simple color) : The background color with transparency when positive

negativeBgColor (simple color) : The background color with transparency when negative

neutralBgColor (simple color) : The background color with transparency when neutral

method init(this, pos, height, width, neutralBgColor)

Initialize the metrics table object with the given colors in the given position

Namespace types: MetricsTable

Parameters:

this (MetricsTable) : The metrics table object

pos (simple string) : The table position string

height (simple float) : The height of the table as a percentage of the charts height. By default, 0 auto-adjusts the height based on the text inside the cells

width (simple float) : The width of the table as a percentage of the charts width. By default, 0 auto-adjusts the width based on the text inside the cells

neutralBgColor (simple color) : The background color with transparency when neutral

method init(this, seas)

Initialize the seasonal data

Namespace types: SeasonalData

Parameters:

this (SeasonalData) : The seasonal data object

seas (simple Seasonality) : The seasonality of the matrix data

method init(this, data, pos, maxNumOfYears, height, width, extended, neutralTxtColor, neutralBgColor)

Initialize the seasonal table object with the given colors in the given position

Namespace types: SeasonalTable

Parameters: