Expected Intraday MovementThis indicator pretends to represent the "probable" maximum movement of an asset, for the rest of the day.

This indicator should be used "only" in intraday timeframe. You will not be able to see it if you select a longer timeframe.

To calculate the probable maximum movement, the indicator uses the VIX value for each minute.

On the first candle of the day, it also calculates the probable maximum movement for the whole day, and plots it in horizontal lines.

It also allows adding a couple of extra lines (for visual purposes only).

It also allows the creation of alerts, so that when the value of the asset is close to one of the limits, it can send you an alert using the Tradingview alert system.

Summary of parameters:

Intraday bands: allows you to show/hide the bands for each minute.

Intraday first candle projection: allows to show/hide the estimated projection from the first candle of the day.

Enable alert: allows to enable/disable alerts.

Upper and lower band offset: optional offset where alarms will be triggered (e.g. 10 points before the limit is reached).

Intraday Extra Projection: allows to show/hide extra levels (for visual purposes only)

Upper and lower extra: values for extra levels.

As always, no indicator is meant to provide a single, reliable strategy to your trading regimen and no indicator or group of indicators should be relied on solely. Be sure to do your own analysis and assessments of the stock prior to taking any trades.

Safe trades everyone!

חפש סקריפטים עבור "vix"

Correlational cyclesCorrelation is a statistical measure that expresses the extent to which two variables are linearly related (meaning they change together at a constant rate). It's a common tool for describing simple relationships without making a statement about cause and effect.

This script allows the user to input a multiplier to reverse the symbol input. This enables the user to look at a correlation measure between VIX and QQQ and the same time.. And get a better of understanding of what is not alligning and what is. the peaks in correlations usually signal a coming volatile period.

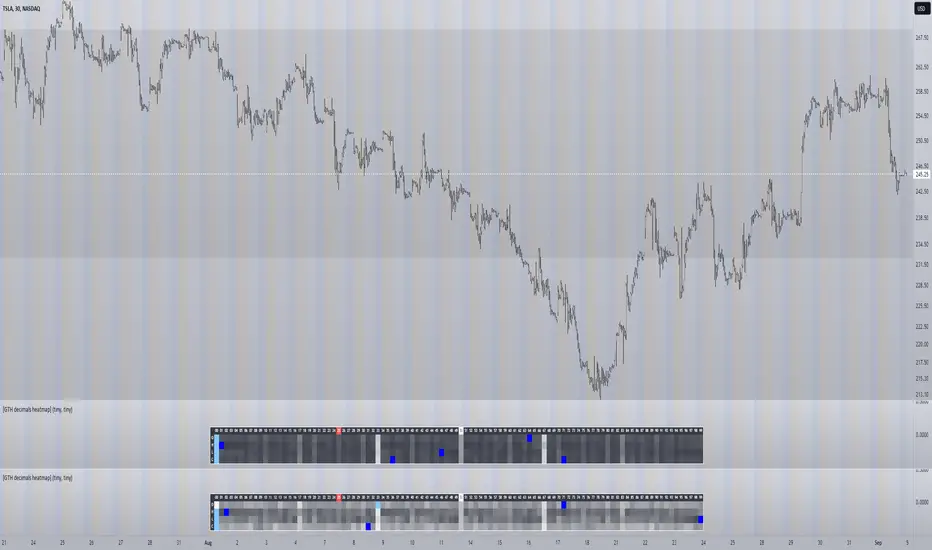

[GTH decimals heatmap] (wide screen advised)Preface

I share my personal general view on indicators below; skip ahead to the Description below if you are not interested.

It is my personal conviction that most - if not all - indicators rely mainly on trader's belief that they work, and in a feedback system like free markets they might become a self-fulfilling prophecy as a result, if (!) a big part of the traders believes in it, because some famous trader releases an indicator, or such person's public statement goes viral.

One of those voodoo indicators is the famous "follow-through day". There is zero statistical evidence for its validity, beyond the validity of a statement like "If it's bright at day it's usually the sun shining". The uselessness was proven exactly on its inventor's YT channel, Investors Business Daily. According to the examiner, its inventor William J. O'Neil himself could not explain the values used for this indicator. It might have been an incidental observation at some point without general validity. A.k.a "curve fitting". Still, it's being used by many today.

Another one of those indicators is the three points reversal on the S&P 500 Volatility Index (VIX) which allegedly might potentially maybe indicate a possible shift in trend. Both indicators share an immediately problematic feature: They use absolute values. Nothing is ever absolute in a highly subjective and emotionally driven game like the markets where a lot of money can be made and lost.

Most indicators can not produce additional information since they can only re-pack price/volume action. Many times an interpretion of the distance between price and a moving average and/or the slope of a moving average deliver very similar - if not better - results than MACD, RSI etc., especially with standard settings, the origin of which are usually unknown (always a warning sign). Very few indicators can deliver information which is otherwise hard to quantify, e. g. market noise (Kaufman's Efficiency Ratio or Price Density) or volatility, standard deviation etc.

It is common knowledge that trading the markets is a game of probability. No indicator works all the time (or at all, see above). In order to make decisions based on any indicator, the probability for its validity and the conditions under which validity seemed to have occurred, must be known. Otherwise it is just coffee grounds reading under the illusion of adding to the edge, when in fact it is only adding to the trees, making it even harder to see the forest.

Description

A common belief is that whole or half-dollar prices tend to be attraction points in price action, so a number of traders include those into decision making. But are they really...?

Spoiler Alert:

Generally, it is safe to say that for the big majority of stocks there is very thin evidence for it. It depends vastly on the asset, the timeframe used and the market period (pre/post/main trading times). If at all, there seems to be an above random but still thin evidence for whole prices being significant attraction points. Interesting/surprising patterns are visible on many stocks/timeframes/session periods, though.

The screenshot shows TSLA, 30m timeframe, two heatmaps added. The top one shows pre/post-market data only, the bottom one main market data only. The cyan fields indicate the strongest occurrence, the dark blue fields indicate the weakest occurrence of open/high/low/close prices at the respective decimal. The red field indicates the current/last price decimal.

Clearly, TSLA displays a strong pre-market attraction for .00, followed by .33 and .67 and .50. This pattern of thirds seems to be a unique feature of TSLA. In the main trading session it is being diluted by a more random distribution.

Other interesting equities to examine:

SPY: No significant pattern on any timeframe!

META: Generally weak patterns on all timeframes, but interestingly on the 1D there is evidence for less randomness on O and H, more on L and most on C.

AAPL: 1D, foggy attraction areas around .35 and .12. Whole price is no attraction area at all! Very weak attraction around .73.

AMD: Strong pattern on D, W, M, attraction areas around 1/16th intervals. No patterns on lower timeframes.

AMZN: Significant differences between pre/post and main session. Strong 1/16th pattern below D in pre/post.

TAOP: Strong 1/5th pattern on all timeframes.

Read the tool tips and go explore!

Options Scalping NiftyThis Indicator is Owned by Team Option Scalping.

Top Right Corner TABLE ( 6 , 10 )

When you are trading in Nifty futures , we have to check major Stocks which is contributing to Nifty move. So we have given that in this tab.

This table consist of 5 Major Indices and 5 Stocks :

• BankNifty

• Nifty

•FinNifty

• Dow

• VIX

• RIL

• HDFCBANK

• INFY

• TCS

• ICICBANK

And following data of each stock has been provided:

• LTP

• Daily Change

• Daily Percentage Change

• 15-minute Change Percentage

• 1-Hour Change Percentage

This Table is completely different from Our other publish indicator named "Options Scalping V2". That consist of banking stocks data, and this consist of Nifty Stocks data. Data set are same but constituents are different.

Bull / Bear Market RegimeBull / Bear Market Regime

Instructions:

- A simple risk on or risk off indicator based on CBOE's Implied Correlation and VIX to highlight and indicate Bull / Bear Markets. To be used with the S&P500 index as that's the source from where the CBOE calculates and measures implied volatility & implied correlation. Can also be used with the other indices such as: Dow Jones, S&P 500, Nasdaq, & Nasdaq100, & Index ETF's such as DIA, SPY, QQQ, etc.

- Know the active regime, see the larger picture using the Daily or Weekly view, and visualize the current "Risk On (Bull) or Risk Off (Bear)" environment.

Description:

- Risk On and Risk Off simplified & visualized. Know if we are in a RISK ON or RISK OFF environment (Bull or Bear Market). (Absolute bottoms and tops will occur BEFORE a Risk On (Bull Market) or Risk Off (Bear Market) environment is confirmed!) This indicator is not meant to bottom tick or uptick market price action, but to show the active regime.

- Green: Bull Market, Risk On, low volatility, and low risk.

- Red: Bear Market, Risk Off, high volatility, and higher risk.

Buy & Sell Indicators (DAILY time frame)

- Nothing is 100% guaranteed! Can be used for short to medium term trades at the users discretion in BEAR MARKETS!!

- These signals are meant to be used during a RISK OFF / BEAR MARKET environment that tends to be accompanied with high volatility. A Risk on / Bull Market environment tends to have low volatility and endless rallies, so the signals will differ and in most instances not apply for Bull market / Risk on regime.

- The SELL signal will more often than not signal that a pullback is near in a BULL market and that a BMR-Bear Market Rally is almost over in a BEAR market.

- The BUY signal will have far more accuracy in a BEAR market-high volatility environment and can Identify short-term and major bottoms.

Always use proper sizing and risk management!

infoThis is a very simple script that i use to add useful info to my trading view charts.

specifically i track following :

1. VIX

2. RSI

3. ticker name and timeframe

Feel free to change, modify as per your requirements

Volatility Spike EstimatorPlots the Average True Range (ATR), its historical mean, the upper threshold for a volatility spike, and uses background color to show the likelihood of a volatility spike based on the current ATR value.

Green background indicates an increased likelihood of a volatility spike, while red background means a spike might have already occurred or be in progress.

Update: In this version, we added a short-term ATR calculation with an adjustable input parameter, shortTermATRLength. The likelihood of a volatility spike is now estimated based on the short-term ATR instead of the original ATR. This change makes the indicator more sensitive to recent market conditions and can help detect potential volatility spikes more quickly.

Negative Correlation SignalsThank you to Hendrik Fuchs who coded this for me - I highly recommend you...

The AUDUSD/EURUSD has a negative correlation with the DXY as does the GBPJPY/USDJPY have with the JPYX. This indicator is very simple and uses opposite candle pinbars (pinbar/doji structure can be set by you) of the two instruments on the chart whilst the stochastic RSI should be above 80 for overbought on the one but below 20 on the other for oversold (or vice versa) to generate a signal.

This indicator works as follow:

1. Choose an instrument that has an opposing negatively correlated instrument (EURUSD & DXY, GBPJPY & JPYX, US100 & VIX, etc.)

2. Add indicator to the chart and open settings.

3. Open the settings and add the correct instruments (default is set to GBPJPY & JPYX).

4. Enter your desired Stochastic RSI & candle formation settings.

You will see buy and sell signals appear on the charts. Alerts are possible (Any alert() function call). Does not repaint after close of candle. Better on higher timeframes but can also be used for scalping. Best used as confluence or as part of a trend trading system.

There are obviously many many variations that I have not even thought off - please let us know in the comment section if you find settings/timeframes/instruments that work particularly well.

CM_Williams_Vix_Fix - Market Top and Bottom with multi-timeframeThis is a modification of CM_Williams_Vix_Fix indicator to include both market tops and bottoms with multi-timeframe support. The original indicator only finds market bottoms.

All credits go to the original author ChrisMoody.

Original script link

Working:

The histogram above 0 signifies the trend of market going UP and the histogram below 0 signifies the trend of market going DOWN.

The histogram bar is calculated using "LookBack Period Standard Deviation High" number of candles. A threshold is calculated using bollinger bands and based on percentile of "Look Back Period Percentile High" number of candles.

If the histogram bar above 0 crosses the up threshold then we have market top which is signified by histogram bar having the color green. If the histogram bar below 0 crosses the down threshold then we have market bottom which is signified by histogram bar having the color red.

The market tops and bottoms can also be calculated across multiple timeframes.

Sample usage:

Suppose the market is in an uptrend and the indicator displays red market bottom bar, this might be an indication that the market has reached the end of a pullback. We can use additional indicators like stochastic or rsi to get additional confluence.

This indicator does not repaint but you need to wait for the candle to close.

Index_and_Commodity_PricesThis indicator shows real-time current day-to-day performance of 18 different indices and commodities . Here is the list of different sector ETFs that this indicator tracks

/////INDEX//////

1. BİST-100 - XU0100 - TR- Index

2. BİST-30 - XU030 - TR - Index

3. VİOP-30 - XU030D1! - Index

4. DJI - Dow Jones - Index

5. DAX - DAX Index

6. VIX - Volatilite S&P Index

//////FOREX MARKET/////

7. DXY - U.S. Dollar Index

8. EURUSD -

9. BTCUSD -

10. XAUUSD -

11. XAGUSD -

//////COMMODITY///////

12. BR1! - Brent

13. NG1! - Natural Gas

14. HRC1! -

15. ZW1! -

16. HG1! -

17. DJUSCL -

///////OTHER///////

18. US10Y -

Sigma Expected Movement [D/W/M]Based on the VIX, this indicator shows the expected movement of a stock, ETF or index.

This indicator has two standard deviations that you can set for better guidance.

You can also adjust it for a result in one day, one week or one month.

Settings

* Period

* 1st Deviation: Default 68%

* 2nd Deviation: Default 90%

*Round To Integer: If it checked, it will search for the nearest integer (+/-). Optimal for people who do Options.

*Table Position: refers to which corner you want to put the table with information.

SPX_Strikes_OpcionSigmaThis is a tool to know the strikes to use for Iron Condor.

You can change the colors for the lines.

It uses the VIX to estimate the movement of the SPX index.

VOLQ Sigma TableThis indicator replaces the implied volatility of VOLQ with the daily volatility and reflects that value into the price on the NDX chart to create the VOLQ standard deviation table.

It will only be useful for stocks related to the Nasdaq Index.

For example, NDX, QQQ or so.

And we want to predict the range of weekly fluctuations by plotting those values as a line in the future.

It is expressed as High 2σ by adding the standard deviation 2 sigma value of the VOLQ value from last week's closing price.

It is expressed as High 1σ by adding the standard deviation 1 sigma value of the VOLQ value from last week's closing price.

It is expressed as Low 1σ by subtracting the standard deviation 1 sigma value of the VOLQ value from the closing price of the previous week.

It is expressed as Low 2σ by subtracting the standard deviation 2 sigma value of the VOLQ value from last week's closing price.

1day predicts daily fluctuations.

2day predicts 2-day fluctuations.

3day predicts 3-day fluctuations.

4day predicts 4-day fluctuations.

5day predicts 5-day fluctuations.

In the settings you can select the start date to display the VOLQ line via input.

-----------------------------

What motivated me to create this indicator?

From my point of view, the reason for classifying vix volq historical volatility (realized volatility) is that the most important point is that VIXX and VolQ are calculated from implied volatility. It can be standardized as one-month volatility. There are many strike prices, but exchanges use the implied volatility of options traded on their own exchanges.

Because historical volatility depends on how the period is set, to compare with VIXX, we compare it with a month, that is, 20 business days. One-month implied volatility means (actually different depending on the strike price), because option traders expect that the one-month volatility will be this much, and it is the volatility created by volatility trading.

So we see it as the volatility expected by derivatives traders, especially volatility traders.

I'm trying to infer what the market thinks will fluctuate this much from the numbers generated there.

Willspread Chart + POIV & ADVolumen TrendColor sπThe Indicator is a combination of different types of measurements to the Price Action.

1. Spread: The Spread is set to measure your Symbol to another chosen Market like Dollar as Contra . But you can switch also between different markets.

2. Accumulation/Distribution with True Range of High or Low including OpenInterest. This only works with Futures .

--Energies, Metals, Bonds, Softs, Currencies, Livestock, live cattle , feeder cattle, lean hogs , index--

Open Interest for:

ZW, ZC, ZS, ZM, ZL, ZO, ZR, CL, RB, HO, NG, GC, SI, HG, PA, PL, ZN, ZB, ZT, ZF, CC, CT, KC, SB, JO, LB, AUDUSD, GBPUSD, USDCAD, EURUSD, USDJPY, USDCHF, USDMXN, NZDUSD, USDRUB, DX, BTC, ETH, LE, GF, HE, NQ, NDX, ES, SPX, RTY, VIX,

3. Accumulation/Distribution with True Range of High or Low including Volume .

4. The color shows if the Market has positive or negative (Willspread, Volume or Open Interest)

5. The Indicator also shows Divergences to Price and Willspread Movements.

If you want to have more information just give me a message.

Implied Volatility Estimator using Black Scholes [Loxx]Implied Volatility Estimator using Black Scholes derives a estimation of implied volatility using the Black Scholes options pricing model. The Bisection algorithm is used for our purposes here. This includes the ability to adjust for dividends.

Implied Volatility

The implied volatility (IV) of an option contract is that value of the volatility of the underlying instrument which, when input in an option pricing model (such as Black–Scholes), will return a theoretical value equal to the current market price of that option. The VIX , in contrast, is a model-free estimate of Implied Volatility. The latter is viewed as being important because it represents a measure of risk for the underlying asset. Elevated Implied Volatility suggests that risks to underlying are also elevated. Ordinarily, to estimate implied volatility we rely upon Black-Scholes (1973). This implies that we are prepared to accept the assumptions of Black Scholes (1973).

Inputs

Spot price: select from 33 different types of price inputs

Strike Price: the strike price of the option you're wishing to model

Market Price: this is the market price of the option; choose, last, bid, or ask to see different results

Historical Volatility Period: the input period for historical volatility ; historical volatility isn't used in the Bisection algo, this is to serve as a comparison, even though historical volatility is from price movement of the underlying asset where as implied volatility is the volatility of the option

Historical Volatility Type: choose from various types of implied volatility , search my indicators for details on each of these

Option Base Currency: this is to calculate the risk-free rate, this is used if you wish to automatically calculate the risk-free rate instead of using the manual input. this uses the 10 year bold yield of the corresponding country

% Manual Risk-free Rate: here you can manually enter the risk-free rate

Use manual input for Risk-free Rate? : choose manual or automatic for risk-free rate

% Manual Yearly Dividend Yield: here you can manually enter the yearly dividend yield

Adjust for Dividends?: choose if you even want to use use dividends

Automatically Calculate Yearly Dividend Yield? choose if you want to use automatic vs manual dividend yield calculation

Time Now Type: choose how you want to calculate time right now, see the tool tip

Days in Year: choose how many days in the year, 365 for all days, 252 for trading days, etc

Hours Per Day: how many hours per day? 24, 8 working hours, or 6.5 trading hours

Expiry date settings: here you can specify the exact time the option expires

*** the algorithm inputs for low and high aren't to be changed unless you're working through the mathematics of how Bisection works.

Included

Option pricing panel

Loxx's Expanded Source Types

Related Indicators

Cox-Ross-Rubinstein Binomial Tree Options Pricing Model

vol_coneDraws a volatility cone on the chart, using the contract's realized volatility (rv). The inputs are:

- window: the number of past periods to use for computing the realized volatility. VIX uses 30 calendar days, which is 21 trading days, so 21 is the default.

- stdevs: the number of standard deviations that the cone will cover.

- periods to project: the length of the volatility cone.

- periods per year: the number of periods in a year. for a daily chart, this is 252. for a thirty minute chart on a contract that trades 23 hours a day, this is 23 * 2 * 252 = 11592. for an accurate cone, this input must be set correctly, according to the chart's time frame.

- history: show the lagged projections. in other words, if the cone is set to project 21 periods in the future, the lines drawn show the top and bottom edges of the cone from 23 periods ago.

- rate: the current interest or discount rate. this is used to compute the forward price of the underlying contract. using an accurate forward price allows you to compare the realized volatility projection to the implied volatility projections derived from options prices.

Example settings for a 30 minute chart of a contract that trades 23 hours per day, with 1 standard deviation, a 21 day rv calculation, and half a day projected:

- stdevs: 1

- periods to project: 23

- window: 23 * 2 * 21 = 966

- periods per year: 23 * 2 * 252 = 11592

Additionally, a table is drawn in the upper right hand corner, with several values:

- rv: the contract's current realized volatility.

- rnk: the rv's percentile rank, compared to the rv values on past bars.

- acc: the proportion of times price settled inside, versus outside, the volatility cone, "periods to project" into the future. this should be around 65-70% for most contracts when the cone is set to 1 standard deviation.

- up: the upper bound of the cone for the projection period.

- dn: the lower bound of the cone for the projection period.

Limitations:

- pinescript only seems to be able to draw a limited distance into the future. If you choose too many "periods to project", the cone will start drawing vertically at some limit.

- the cone is not totally smooth owing to the facts a) it is comprised of a limited number of lines and b) each bar does not represent the same amount of time in pinescript, as some cross weekends, session gaps, etc.

vol_boxA simple script to draw a realized volatility forecast, in the form of a box. The script calculates realized volatility using the EWMA method, using a number of periods of your choosing. Using the "periods per year", you can adjust the script to work on any time frame. For example, if you are using an hourly chart with bitcoin, there are 24 periods * 365 = 8760 periods per year. This setting is essential for the realized volatility figure to be accurate as an annualized figure, like VIX.

By default, the settings are set to mimic CBOE volatility indices. That is, 252 days per year, and 20 period window on the daily timeframe (simulating a 30 trading day period).

Inside the box are three figures:

1. The current realized volatility.

2. The rank. E.g. "10%" means the current realized volatility is less than 90% of realized volatility measures.

3. The "accuracy": how often price has closed within the box, historically.

Inputs:

stdevs: the number of standard deviations for the box

periods to project: the number of periods to forecast

window: the number of periods for calculating realized volatility

periods per year: the number of periods in one year (e.g. 252 for the "D" timeframe)

Crude Oil: Backwardation Vs ContangoCrude Oil, CL

Plots Futures Curve: Futures contract prices over the next 3.5 years; to easily visualize Backwardation Vs Contango(carrying charge) markets.

Carrying charge (contract prices increasing into the future) = normal, representing the costs of carrying/storage of a commodity. When this is flipped to Backwardation(As the above; contract prices decreasing into the future): it's a bullish sign: Buyers want this commodity, and they want it NOW.

Note: indicator does not map to time axis in the same way as price; it simply plots the progression of contract months out into the future; left to right; so timeframe DOESN'T MATTER for this plot

TO UPDATE (every year or so): in REQUEST CONTRACTS section, delete old contracts (top) and add new ones (bottom). Then in PLOTTING section, Delete old contract labels (bottom); add new contract labels (top); adjust the X in 'bar_index-(X+_historical)' numbers accordingly

This is one of several similar Futures Curve indicators: Meats | Metals | Grains | VIX | Crude Oil

If you want to build from this; to work on other commodities; be aware that Tradingview limits the number of contract calls to 40 (hence the multiple indicators)

Tips:

-Right click and reset chart if you can't see the plot; or if you have trouble with the scaling.

-Right click and add to new scale if you prefer this not to overlay directly on price. Or move to new pane below.

-If this takes too long to load (due to so many security calls); comment out the more distant future half of the contracts; and their respective labels. Or comment out every other contract and every other label if you prefer.

--Added historical input: input days back in time; to see the historical shape of the Futures curve via selecting 'days back' snapshot

updated 20th June 2022

© twingall

Gap Reversion StrategyToday I am releasing to the community an original short-term, high-probability gap trading strategy, backed by a 20 year backtest. This strategy capitalizes on the mean reverting behavior of equity ETFs, which is largely driven by fear in the market. The strategy buys into that fear at a level that has historically mean reverted within ~5 days. Larry Connors has published useful research and variations of strategies based on this behavior that I would recommend any quantitative trader read.

What it does:

This strategy, for 1 day charts on equity ETFs, looks for an overnight gap down when the RSI is also in/near an oversold position. Then, it places a limit order further below the opening of the gapped-down day. It then exits the position based on a higher RSI level. The limit buy order is cancelled if the price doesn't reach your limit price that day. So, the larger you make the gap and limit %, the less signals you will have.

Features:

Inputs to allow the adjustment of the limit order %, the gap %, and the RSI entry/exit levels.

An option to have the limit order be based on a % of ATR instead of a % of asset price.

An optional filter that can turn-off trades when the VIX is unusually high.

A built in stop.

Built in alerts.

Disclaimer: This is not financial advice. Open-source scripts I publish in the community are largely meant to spark ideas that can be used as building blocks for part of a more robust trade management strategy. If you would like to implement a version of any script, I would recommend making significant additions/modifications to the strategy & risk management functions. If you don’t know how to program in Pine, then hire a Pine-coder. We can help!

PClose Levels 2.0This script plots the levels generated via a combination of SPX 2Y Quartiles for everyday, red days, and green days. It is intended for use solely with SPX.

These quartiles are also sorted by VIX averages into bands that expand and contract with VIX.

It gives us an idea of what levels to potentially expect resistance/support fairly well, but is designed to be used in conjunction with other indicators and macroeconomic information.

Green Dashed is your Expected Max Range (EMR+) based on Green Day averages.

Green Dotted is your Expected Range (ER+) based on full dataset averages.

Green solid lines are POS2 and POS1, based on Green Day averages.

White Dotted is your Expected Move (EM), based on full dataset averages.

Red solid lines are NEG1 and NEG2, based on Red Day averages.

Red Dotted is your Expected Range (ER-) based on full dataset averages.

Red Dashed is your Expected Max Range (EMR-) based on Red Day averages.

Relative Strength Volatility Adjusted Ema [CC]The Relative Strength Volatility Adjusted Exponential Moving Average was created by Vitali Apirine (Stocks and Commodities Mar 2022) and this is his final indicator of his recent Relative Strength series. I published both of the previous indicators, Relative Strength Volume Adjusted Exponential Moving Average and Relative Strength Exponential Moving Average

This indicator is particularly unique because it uses the Volatility Index (VIX) symbol as the default to determine volatility and uses this in place of the current stock's price into a typical relative strength calculation. As you can see in the chart, it follows the price much closer than the other two indicators and so of course this means that this indicator is best for choppy markets and the other two are better for trending markets. I would of course recommend to experiment with this one and see what works best for you.

I have included strong buy and sell signals in addition to normal ones so strong signals are darker in color and normal signals are lighter in color. Buy when the line turns green and sell when it turns red.

Let me know if there are any other indicators or scripts you would like to see me publish!

Nasdaq VXN Volatility Warning IndicatorToday I am sharing with the community a volatility indicator that uses the Nasdaq VXN Volatility Index to help you or your algorithms avoid black swan events. This is a similar the indicator I published last week that uses the SP500 VIX, but this indicator uses the Nasdaq VXN and can help inform strategies on the Nasdaq index or Nasdaq derivative instruments.

Variance is most commonly used in statistics to derive standard deviation (with its square root). It does have another practical application, and that is to identify outliers in a sample of data. Variance is defined as the squared difference between a value and its mean. Calculating that squared difference means that the farther away the value is from the mean, the more the variance will grow (exponentially). This exponential difference makes outliers in the variance data more apparent.

Why does this matter?

There are assets or indices that exist in the stock market that might make us adjust our trading strategy if they are behaving in an unusual way. In some instances, we can use variance to identify that behavior and inform our strategy.

Is that really possible?

Let’s look at the relationship between VXN and the Nasdaq100 as an example. If you trade a Nasdaq index with a mean reversion strategy or algorithm, you know that they typically do best in times of volatility . These strategies essentially attempt to “call bottom” on a pullback. Their downside is that sometimes a pullback turns into a regime change, or a black swan event. The other downside is that there is no logical tight stop that actually increases their performance, so when they lose they tend to lose big.

So that begs the question, how might one quantitatively identify if this dip could turn into a regime change or black swan event?

The Nasdaq Volatility Index ( VXN ) uses options data to identify, on a large scale, what investors overall expect the market to do in the near future. The Volatility Index spikes in times of uncertainty and when investors expect the market to go down. However, during a black swan event, historically the VXN has spiked a lot harder. We can use variance here to identify if a spike in the VXN exceeds our threshold for a normal market pullback, and potentially avoid entering trades for a period of time (I.e. maybe we don’t buy that dip).

Does this actually work?

In backtesting, this cut the drawdown of my index reversion strategies in half. It also cuts out some good trades (because high investor fear isn’t always indicative of a regime change or black swan event). But, I’ll happily lose out on some good trades in exchange for half the drawdown. Lets look at some examples of periods of time that trades could have been avoided using this strategy/indicator:

Example 1 – With the Volatility Warning Indicator, the mean reversion strategy could have avoided repeatedly buying this pullback that led to this asset losing over 75% of its value:

Example 2 - June 2018 to June 2019 - With the Volatility Warning Indicator, the drawdown during this period reduces from 22% to 11%, and the overall returns increase from -8% to +3%

How do you use this indicator?

This indicator determines the variance of VXN against a long term mean. If the variance of the VXN spikes over an input threshold, the indicator goes up. The indicator will remain up for a defined period of bars/time after the variance returns below the threshold. I have included default values I’ve found to be significant for a short-term mean-reversion strategy, but your inputs might depend on your risk tolerance and strategy time-horizon. The default values are for 1hr VXN data/charts. It will pull in variance data for the VXN regardless of which chart the indicator is applied to.

Disclaimer: Open-source scripts I publish in the community are largely meant to spark ideas or be used as building blocks for part of a more robust trade management strategy. If you would like to implement a version of any script, I would recommend making significant additions/modifications to the strategy & risk management functions. If you don’t know how to program in Pine, then hire a Pine-coder. We can help!

Commitment of Traders: Financial Metrics█ OVERVIEW

This indicator displays the Commitment of Traders (COT) financial data for futures markets.

█ CONCEPTS

Commitment of Traders (COT) data is tallied by the Commodity Futures Trading Commission (CFTC) , a US federal agency that oversees the trading of derivative markets such as futures in the US. It is weekly data that provides traders with information about open interest for an asset. The CFTC oversees derivative markets traded on different exchanges, so COT data is available for assets that can be traded on CBOT, CME, NYMEX, COMEX, and ICEUS.

A detailed description of the COT report can be found on the CFTC's website .

COT data is separated into three notable reports: Legacy, Disaggregated, and Financial. This indicator presents data from the COT Financial (Traders in Financial Futures) report. The Financial report includes financial contracts, such as currencies, US Treasury securities, Eurodollars, stocks, VIX and Bloomberg commodity index. As such, the TFF data is limited to financial-related tickers. The TFF report breaks down the reportable open interest positions into four classifications: Dealer/Intermediary, Asset Manager/Institutional, Leveraged Funds, and Other Reportables.

Our other COT indicators are:

• Commitment of Traders: Legacy Metrics

• Commitment of Traders: Disaggregated Metrics

• Commitment of Traders: Total

█ HOW TO USE IT

Load the indicator on an active chart (see here if you don't know how).

By default, the indicator uses the chart's symbol to derive the COT data it displays. You can also specify a CFTC code in the "CFTC code" field of the script's inputs to display COT data from a symbol different than the chart's.

The rest of this section documents the script's input fields.

Metric

Each metric represents a different column of the Commitment of Traders report. Details are available in the explanatory notes on the CFTC's website .

Here is a summary of the metrics:

• "Open Interest" is the total of all futures and/or option contracts entered into and not yet offset by a transaction, by delivery, by exercise, etc.

The aggregate of all long open interest is equal to the aggregate of all short open interest.

• "Traders Total" is the number of all unique reportable traders, regardless of the trading direction.

• "Traders Dealer" is the number of traders classified as a "Dealer/Intermediary" reported holding any position with the specified direction.

A "producer/merchant/processor/user" is an entity typically described as the “sell side” of the market.

Though they may not predominately sell futures, they do design and sell various financial assets to clients.

They tend to have matched books or offset their risk across markets and clients.

Futures contracts are part of the pricing and balancing of risk associated with the products they sell and their activities.

• "Traders Asset Manager" is the number of traders classified as "Asset Manager/Institutional" reported holding any position with the specified direction.

These are institutional investors, including pension funds, endowments, insurance companies,

mutual funds and those portfolio/investment managers whose clients are predominantly institutional.

• "Traders Leveraged Funds" is the number of traders classified as "Leveraged Funds" reported holding any position with the specified direction.

These are typically hedge funds and various types of money managers. The traders may be engaged in managing and

conducting proprietary futures trading and trading on behalf of speculative clients.

• "Traders Other Reportable" is the number of reportable traders that are not placed in any of the three categories specified above.

The traders in this category mostly are using markets to hedge business risk, whether that risk is related to foreign exchange, equities or interest rates.

This category includes corporate treasuries, central banks, smaller banks, mortgage originators, credit unions and any other reportable traders not assigned to the other three categories.

• "Traders Total Reportable" is the number of all traders reported holding any position with the specified direction.

To determine the total number of reportable traders in a market, a trader is counted only once whether or not the trader appears in more than one category.

As a result, the sum of the numbers of traders in each separate category typically exceeds the total number of reportable traders.

• "Dealer/Asset Manager/Leveraged Funds/Total Reportable/Other Reportable Positions -- all positions held by the traders of the specified category.

• "Nonreportable Positions" is the long and short open interest derived by subtracting the total long and short reportable positions from the total open interest.

Accordingly, the number of traders involved and the commercial/non-commercial classification of each trader are unknown.

• "Concentration Gross/Net LT 4/8 TDR" is the percentage of open interest held by 4/8 of the largest traders, by gross/net positions,

without regard to whether they are classified as commercial or non-commercial. The Net position ratios are computed after offsetting each trader’s equal long and short positions.

A reportable trader with relatively large, balanced long and short positions in a single market, therefore,

may be among the four and eight largest traders in both the gross long and gross short categories, but will probably not be included among the four and eight largest traders on a net basis.

Direction

Each metric is available for a particular set of directions. Valid directions for each metric are specified with its name in the "Metric" field's dropdown menu.

COT Selection Mode

This field's value determines how the script determines which COT data to return from the chart's symbol:

- "Root" uses the root of a futures symbol ("ES" for "ESH2020").

- "Base currency" uses the base currency in a forex pair ("EUR" for "EURUSD").

- "Currency" uses the quote currency, i.e., the currency the symbol is traded in ("JPY" for "TSE:9984" or "USDJPY").

- "Auto" tries all modes, in turn.

If no COT data can be found, a runtime error is generated.

Note that if the "CTFC Code" input field contains a code, it will override this input.

Futures/Options

Specifies the type of Commitment of Traders data to display: data concerning only Futures, only Options, or both.

CTFC Code

Instead of letting the script generate the CFTC COT code from the chart and the "COT Selection Mode" input when this field is empty, you can specify an unrelated CFTC COT code here, e.g., 001602 for wheat futures.

Look first. Then leap.