Kairos BarakahTrade with precision during high-probability windows using this advanced Pine Script indicator, designed specifically for Indian Standard Time (IST). The tool identifies key reversal opportunities within a user-defined trading session, combining time-based reference levels, sequence-validated signals, and multi-factor win probability analysis for confident decision-making.

Key Features

1. Time-Based Reference Levels

Automatically sets high/low reference levels at a customizable start time (default: 19:00 IST).

Active trading window with adjustable duration (default: 135 minutes).

Clear visual reference lines for easy tracking.

2. Intelligent Signal Generation

Initial Signals:

Buy (B): Triggered when price closes above the reference high.

Sell (S): Triggered when price closes below the reference low.

Reversal Signals (R):

Valid only after an initial signal, ensuring proper sequence.

Buy Reversal: Price closes above reference high (after a Sell signal).

Sell Reversal: Price closes below reference low (after a Buy signal).

3. Multi-Dimensional Win Probability

Body Strength: Measures candle conviction (body size / total range).

Volume Confirmation: Compares current volume to 20-period average.

Trend Alignment: Uses EMA crosses (9/21) and RSI (14) for momentum.

Composite Score: Weighted blend of all factors, color-coded for quick interpretation:

🟢 >70%: High-confidence signal.

🟠 40-69%: Moderate confidence.

🔴 <40%: Weak signal.

4. Professional Visualization

Clean labels (B/S/R) at signal points.

Real-time reference table showing levels, active signal, and probabilities.

Customizable alerts for all signal types.

Why Use This Indicator?

IST-Optimized: Tailored for Indian market hours.

Rules-Based Reversals: Avoids false signals with strict sequence checks.

Data-Driven Confidence: Win probability metrics reduce guesswork.

Flexible Setup: Adjust time windows and parameters to fit your strategy.

חפש סקריפטים עבור "wind+芯片行业+市盈率+财经数据"

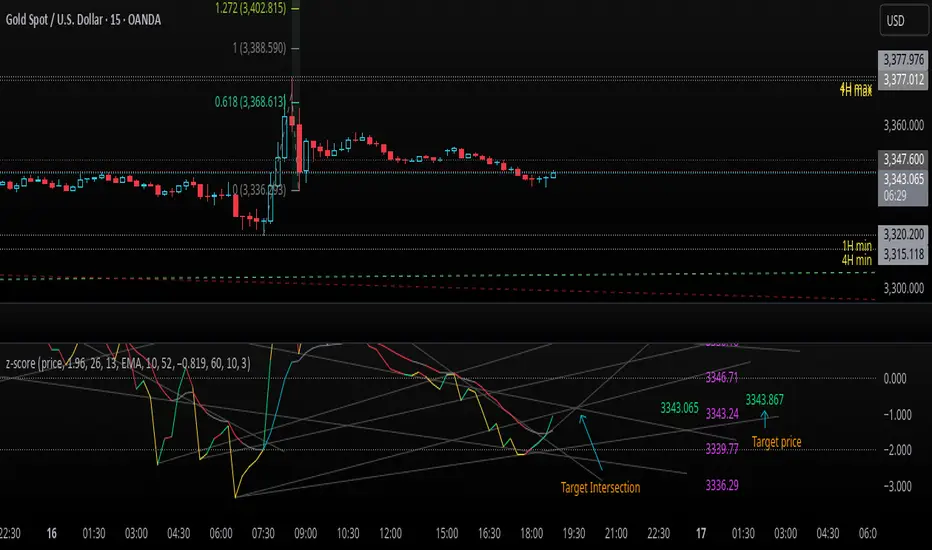

z-score-calkusi-v1.143z-scores incorporate the moment of N look-back bars to allow future price projection.

z-score = (X - mean)/std.deviation ; X = close

z-scores update with each new close print and with each new bar. Each new bar augments the mean and std.deviation for the N bars considered. The old Nth bar falls away from consideration with each new historical bar.

The indicator allows two other options for X: RSI or Moving Average.

NOTE: While trading use the "price" option only.

The other two options are provided for visualisation of RSI and Moving Average as z-score curves.

Use z-scores to identify tops and bottoms in the future as well as intermediate intersections through which a z-score will pass through with each new close and each new bar.

Draw lines from peaks and troughs in the past through intermediate peaks and troughs to identify projected intersections in the future. The most likely intersections are those that are formed from a line that comes from a peak in the past and another line that comes from a trough in the past. Try getting at least two lines from historical peaks and two lines from historical troughs to pass through a future intersection.

Compute the target intersection price in the future by clicking on the z-score indicator header to see a drag-able horizontal line to drag over the intersection. The target price is the last value displayed in the indicator's status bar after the closing price.

When the indicator header is clicked, a white horizontal drag-able line will appear to allow dragging the line over an intersection that has been drawn on the indicator for a future z-score projection and the associated future closing price.

With each new bar that appears, it is necessary to repeat the procedure of clicking the z-score indicator header to be able to drag the drag-able horizontal line to see the new target price for the selected intersection. The projected price will be different from the current close price providing a price arbitrage in time.

New intermediate peaks and troughs that appear require new lines be drawn from the past through the new intermediate peak to find a new intersection in the future and a new projected price. Since z-score curves are sort of cyclical in nature, it is possible to see where one has to locate a future intersection by drawing lines from past peaks and troughs.

Do not get fixated on any one projected price as the market decides which projected price will be realised. All prospective targets should be manually updated with each new bar.

When the z-score plot moves outside a channel comprised of lines that are drawn from the past, be ready to adjust to new market conditions.

z-score plots that move above the zero line indicate price action that is either rising or ranging. Similarly, z-score plots that move below the zero line indicate price action that is either falling or ranging. Be ready to adjust to new market conditions when z-scores move back and forth across the zero line.

A bar with highest absolute z-score for a cycle screams "reversal approaching" and is followed by a bar with a lower absolute z-score where close price tops and bottoms are realised. This can occur either on the next bar or a few bars later.

The indicator also displays the required N for a Normal(0,1) distribution that can be set for finer granularity for the z-score curve.This works with the Confidence Interval (CI) z-score setting. The default z-score is 1.96 for 95% CI.

Common Confidence Interval z-scores to find N for Normal(0,1) with a Margin of Error (MOE) of 1:

70% 1.036

75% 1.150

80% 1.282

85% 1.440

90% 1.645

95% 1.960

98% 2.326

99% 2.576

99.5% 2.807

99.9% 3.291

99.99% 3.891

99.999% 4.417

9-Jun-2025

Added a feature to display price projection labels at z-score levels 3, 2, 1, 0, -1, -2, 3.

This provides a range for prices available at the current time to help decide whether it is worth entering a trade. If the range of prices from say z=|2| to z=|1| is too narrow, then a trade at the current time may not be worth the risk.

Added plot for z-score moving average.

28-Jun-2025

Added Settings option for # of Std.Deviation level Price Labels to display. The default is 3. Min is 2. Max is 6.

This feature allows likelihood assessment for Fibonacci price projections from higher time frames at lower time frames. A Fibonacci price projection that falls outside |3.x| Std.Deviations is not likely.

Added Settings option for Chart Bar Count and Target Label Offset to allow placement of price labels for the standard z-score levels to the right of the window so that these are still visible in the window.

Target Label Offset allows adjustment of placement of Target Price Label in cases when the Target Price Label is either obscured by the price labels for the standard z-score levels or is too far right to be visible in the window.

9-Jul-2025

z-score 1.142 updates:

Displays in the status line before the close price the range for the selected Std. Deviation levels specified in Settings and |z-zMa|.

When |z-zMa| > |avg(z-zMa)| and zMa rising, |z-zMa| and zMa displays in aqua.

When |z-zMa| > |avg(z-zMa)| and zMa falling, |z-zMa| and zMa displays in red.

When |z-zMa| <= |avg(z-zMa)|, z and zMa display in gray.

z usually crosses over zMa when zMa is gray but not always. So if cross-over occurs when zMa is not gray, it implies a strong move in progress.

Practice makes perfect.

Use this indicator at your own risk

True Hour Open🧠 Why Count an Hour from 30th Minute to 30th Minute?

✅ Traditional Hour vs. Functional Hour

Traditional Time Logic: We’re used to viewing time in clean hourly chunks: 12:00 to 1:00, 1:00 to 2:00, and so on. This structure is fine for general purposes like clocks, meetings, and schedules.

Market Logic: Markets, however, don’t always respect these arbitrary human-made time divisions. Price action often develops momentum, structure, and transitions based on market participants' behavior, not on the clock.

🛠 What the Indicator Does

Marks the start of each hour at the 30th minute past the hour (e.g., 1:30, 2:30, 3:30).

Can highlight or segment candles that fall within a “30-to-30” hourly window.

Optionally draws background shading, lines, or boxes to visually group candles from one 30-minute mark to the next.

This helps you:

Visually align your trading with more accurate price behavior windows.

Anchor time blocks around actual market rhythm, not artificial time slots.

Backtest and strategize based on how candles behave in these alternative hourly segments.

📈 Summary

Trading is about timing. But great trading is about timing that makes sense.

By redefining the hour from 30 to 30, you’re not changing time—you’re aligning with how price moves in time.

Anomalous Holonomy Field Theory🌌 Anomalous Holonomy Field Theory (AHFT) - Revolutionary Quantum Market Analysis

Where Theoretical Physics Meets Trading Reality

A Groundbreaking Synthesis of Differential Geometry, Quantum Field Theory, and Market Dynamics

🔬 THEORETICAL FOUNDATION - THE MATHEMATICS OF MARKET REALITY

The Anomalous Holonomy Field Theory represents an unprecedented fusion of advanced mathematical physics with practical market analysis. This isn't merely another indicator repackaging old concepts - it's a fundamentally new lens through which to view and understand market structure .

1. HOLONOMY GROUPS (Differential Geometry)

In differential geometry, holonomy measures how vectors change when parallel transported around closed loops in curved space. Applied to markets:

Mathematical Formula:

H = P exp(∮_C A_μ dx^μ)

Where:

P = Path ordering operator

A_μ = Market connection (price-volume gauge field)

C = Closed price path

Market Implementation:

The holonomy calculation measures how price "remembers" its journey through market space. When price returns to a previous level, the holonomy captures what has changed in the market's internal geometry. This reveals:

Hidden curvature in the market manifold

Topological obstructions to arbitrage

Geometric phase accumulated during price cycles

2. ANOMALY DETECTION (Quantum Field Theory)

Drawing from the Adler-Bell-Jackiw anomaly in quantum field theory:

Mathematical Formula:

∂_μ j^μ = (e²/16π²)F_μν F̃^μν

Where:

j^μ = Market current (order flow)

F_μν = Field strength tensor (volatility structure)

F̃^μν = Dual field strength

Market Application:

Anomalies represent symmetry breaking in market structure - moments when normal patterns fail and extraordinary opportunities arise. The system detects:

Spontaneous symmetry breaking (trend reversals)

Vacuum fluctuations (volatility clusters)

Non-perturbative effects (market crashes/melt-ups)

3. GAUGE THEORY (Theoretical Physics)

Markets exhibit gauge invariance - the fundamental physics remains unchanged under certain transformations:

Mathematical Formula:

A'_μ = A_μ + ∂_μΛ

This ensures our signals are gauge-invariant observables , immune to arbitrary market "coordinate changes" like gaps or reference point shifts.

4. TOPOLOGICAL DATA ANALYSIS

Using persistent homology and Morse theory:

Mathematical Formula:

β_k = dim(H_k(X))

Where β_k are the Betti numbers describing topological features that persist across scales.

🎯 REVOLUTIONARY SIGNAL CONFIGURATION

Signal Sensitivity (0.5-12.0, default 2.5)

Controls the responsiveness of holonomy field calculations to market conditions. This parameter directly affects the threshold for detecting quantum phase transitions in price action.

Optimization by Timeframe:

Scalping (1-5min): 1.5-3.0 for rapid signal generation

Day Trading (15min-1H): 2.5-5.0 for balanced sensitivity

Swing Trading (4H-1D): 5.0-8.0 for high-quality signals only

Score Amplifier (10-200, default 50)

Scales the raw holonomy field strength to produce meaningful signal values. Higher values amplify weak signals in low-volatility environments.

Signal Confirmation Toggle

When enabled, enforces additional technical filters (EMA and RSI alignment) to reduce false positives. Essential for conservative strategies.

Minimum Bars Between Signals (1-20, default 5)

Prevents overtrading by enforcing quantum decoherence time between signals. Higher values reduce whipsaws in choppy markets.

👑 ELITE EXECUTION SYSTEM

Execution Modes:

Conservative Mode:

Stricter signal criteria

Higher quality thresholds

Ideal for stable market conditions

Adaptive Mode:

Self-adjusting parameters

Balances signal frequency with quality

Recommended for most traders

Aggressive Mode:

Maximum signal sensitivity

Captures rapid market moves

Best for experienced traders in volatile conditions

Dynamic Position Sizing:

When enabled, the system scales position size based on:

Holonomy field strength

Current volatility regime

Recent performance metrics

Advanced Exit Management:

Implements trailing stops based on ATR and signal strength, with mode-specific multipliers for optimal profit capture.

🧠 ADAPTIVE INTELLIGENCE ENGINE

Self-Learning System:

The strategy analyzes recent trade outcomes and adjusts:

Risk multipliers based on win/loss ratios

Signal weights according to performance

Market regime detection for environmental adaptation

Learning Speed (0.05-0.3):

Controls adaptation rate. Higher values = faster learning but potentially unstable. Lower values = stable but slower adaptation.

Performance Window (20-100 trades):

Number of recent trades analyzed for adaptation. Longer windows provide stability, shorter windows increase responsiveness.

🎨 REVOLUTIONARY VISUAL SYSTEM

1. Holonomy Field Visualization

What it shows: Multi-layer quantum field bands representing market resonance zones

How to interpret:

Blue/Purple bands = Primary holonomy field (strongest resonance)

Band width = Field strength and volatility

Price within bands = Normal quantum state

Price breaking bands = Quantum phase transition

Trading application: Trade reversals at band extremes, breakouts on band violations with strong signals.

2. Quantum Portals

What they show: Entry signals with recursive depth patterns indicating momentum strength

How to interpret:

Upward triangles with portals = Long entry signals

Downward triangles with portals = Short entry signals

Portal depth = Signal strength and expected momentum

Color intensity = Probability of success

Trading application: Enter on portal appearance, with size proportional to portal depth.

3. Field Resonance Bands

What they show: Fibonacci-based harmonic price zones where quantum resonance occurs

How to interpret:

Dotted circles = Minor resonance levels

Solid circles = Major resonance levels

Color coding = Resonance strength

Trading application: Use as dynamic support/resistance, expect reactions at resonance zones.

4. Anomaly Detection Grid

What it shows: Fractal-based support/resistance with anomaly strength calculations

How to interpret:

Triple-layer lines = Major fractal levels with high anomaly probability

Labels show: Period (H8-H55), Price, and Anomaly strength (φ)

⚡ symbol = Extreme anomaly detected

● symbol = Strong anomaly

○ symbol = Normal conditions

Trading application: Expect major moves when price approaches high anomaly levels. Use for precise entry/exit timing.

5. Phase Space Flow

What it shows: Background heatmap revealing market topology and energy

How to interpret:

Dark background = Low market energy, range-bound

Purple glow = Building energy, trend developing

Bright intensity = High energy, strong directional move

Trading application: Trade aggressively in bright phases, reduce activity in dark phases.

📊 PROFESSIONAL DASHBOARD METRICS

Holonomy Field Strength (-100 to +100)

What it measures: The Wilson loop integral around price paths

>70: Strong positive curvature (bullish vortex)

<-70: Strong negative curvature (bearish collapse)

Near 0: Flat connection (range-bound)

Anomaly Level (0-100%)

What it measures: Quantum vacuum expectation deviation

>70%: Major anomaly (phase transition imminent)

30-70%: Moderate anomaly (elevated volatility)

<30%: Normal quantum fluctuations

Quantum State (-1, 0, +1)

What it measures: Market wave function collapse

+1: Bullish eigenstate |↑⟩

0: Superposition (uncertain)

-1: Bearish eigenstate |↓⟩

Signal Quality Ratings

LEGENDARY: All quantum fields aligned, maximum probability

EXCEPTIONAL: Strong holonomy with anomaly confirmation

STRONG: Good field strength, moderate anomaly

MODERATE: Decent signals, some uncertainty

WEAK: Minimal edge, high quantum noise

Performance Metrics

Win Rate: Rolling performance with emoji indicators

Daily P&L: Real-time profit tracking

Adaptive Risk: Current risk multiplier status

Market Regime: Bull/Bear classification

🏆 WHY THIS CHANGES EVERYTHING

Traditional technical analysis operates on 100-year-old principles - moving averages, support/resistance, and pattern recognition. These work because many traders use them, creating self-fulfilling prophecies.

AHFT transcends this limitation by analyzing markets through the lens of fundamental physics:

Markets have geometry - The holonomy calculations reveal this hidden structure

Price has memory - The geometric phase captures path-dependent effects

Anomalies are predictable - Quantum field theory identifies symmetry breaking

Everything is connected - Gauge theory unifies disparate market phenomena

This isn't just a new indicator - it's a new way of thinking about markets . Just as Einstein's relativity revolutionized physics beyond Newton's mechanics, AHFT revolutionizes technical analysis beyond traditional methods.

🔧 OPTIMAL SETTINGS FOR MNQ 10-MINUTE

For the Micro E-mini Nasdaq-100 on 10-minute timeframe:

Signal Sensitivity: 2.5-3.5

Score Amplifier: 50-70

Execution Mode: Adaptive

Min Bars Between: 3-5

Theme: Quantum Nebula or Dark Matter

💭 THE JOURNEY - FROM IMPOSSIBLE THEORY TO TRADING REALITY

Creating AHFT was a mathematical odyssey that pushed the boundaries of what's possible in Pine Script. The journey began with a seemingly impossible question: Could the profound mathematical structures of theoretical physics be translated into practical trading tools?

The Theoretical Challenge:

Months were spent diving deep into differential geometry textbooks, studying the works of Chern, Simons, and Witten. The mathematics of holonomy groups and gauge theory had never been applied to financial markets. Translating abstract mathematical concepts like parallel transport and fiber bundles into discrete price calculations required novel approaches and countless failed attempts.

The Computational Nightmare:

Pine Script wasn't designed for quantum field theory calculations. Implementing the Wilson loop integral, managing complex array structures for anomaly detection, and maintaining computational efficiency while calculating geometric phases pushed the language to its limits. There were moments when the entire project seemed impossible - the script would timeout, produce nonsensical results, or simply refuse to compile.

The Breakthrough Moments:

After countless sleepless nights and thousands of lines of code, breakthrough came through elegant simplifications. The realization that market anomalies follow patterns similar to quantum vacuum fluctuations led to the revolutionary anomaly detection system. The discovery that price paths exhibit holonomic memory unlocked the geometric phase calculations.

The Visual Revolution:

Creating visualizations that could represent 4-dimensional quantum fields on a 2D chart required innovative approaches. The multi-layer holonomy field, recursive quantum portals, and phase space flow representations went through dozens of iterations before achieving the perfect balance of beauty and functionality.

The Balancing Act:

Perhaps the greatest challenge was maintaining mathematical rigor while ensuring practical trading utility. Every formula had to be both theoretically sound and computationally efficient. Every visual had to be both aesthetically pleasing and information-rich.

The result is more than a strategy - it's a synthesis of pure mathematics and market reality that reveals the hidden order within apparent chaos.

📚 INTEGRATED DOCUMENTATION

Once applied to your chart, AHFT includes comprehensive tooltips on every input parameter. The source code contains detailed explanations of the mathematical theory, practical applications, and optimization guidelines. This published description provides the overview - the indicator itself is a complete educational resource.

⚠️ RISK DISCLAIMER

While AHFT employs advanced mathematical models derived from theoretical physics, markets remain inherently unpredictable. No mathematical model, regardless of sophistication, can guarantee future results. This strategy uses realistic commission ($0.62 per contract) and slippage (1 tick) in all calculations. Past performance does not guarantee future results. Always use appropriate risk management and never risk more than you can afford to lose.

🌟 CONCLUSION

The Anomalous Holonomy Field Theory represents a quantum leap in technical analysis - literally. By applying the profound insights of differential geometry, quantum field theory, and gauge theory to market analysis, AHFT reveals structure and opportunities invisible to traditional methods.

From the holonomy calculations that capture market memory to the anomaly detection that identifies phase transitions, from the adaptive intelligence that learns and evolves to the stunning visualizations that make the invisible visible, every component works in mathematical harmony.

This is more than a trading strategy. It's a new lens through which to view market reality.

Trade with the precision of physics. Trade with the power of mathematics. Trade with AHFT.

I hope this serves as a good replacement for Quantum Edge Pro - Adaptive AI until I'm able to fix it.

— Dskyz, Trade with insight. Trade with anticipation.

Multi-Timeline 1.0Multi-TimeLines 1.0 - Comprehensive Description

WHAT IT DOES:

This indicator creates dynamic horizontal support/resistance lines based on opening prices captured at user-defined New York times. Unlike static horizontal lines, these levels automatically appear and disappear based on sophisticated session logic, providing traders with time-sensitive reference levels that adapt to market sessions.

HOW IT WORKS - TECHNICAL IMPLEMENTATION:

1.

Timezone Conversion Engine:

The script uses Pine Script's "America/New_York" timezone functions to ensure all time calculations are based on NY time, regardless of the user's chart timezone. This eliminates confusion and provides consistent behavior across global markets.

2.

Dual-Category Time Classification System:

The indicator employs a unique two-category classification system:

Category A (16:00-23:59 NY): Evening times that extend overnight until next day 15:59 NY

Category B (00:00-15:59 NY): Day times that extend until same day 15:59 NY

This classification handles the complex logic of overnight sessions and prevents lines from incorrectly resetting at midnight for evening times.

3. Price Capture Mechanism:

Uses precise time-hit detection with backup systems for edge cases (especially midnight 00:00). When a specified time occurs, the script captures the bar's opening price and stores it in persistent variables using Pine Script's var declarations.

4. Session-Aware Display Logic:

Lines only appear during their designated "display windows" - periods when the captured price level is relevant. The script uses conditional plotting with plot.style_linebr to create clean breaks when lines are inactive.

5. Smart Reset System:

Different reset behaviors based on time classification:

Category A times persist across midnight (for overnight analysis)

Category B times reset on day changes (except 00:00 which captures AT day change)

Automatic cleanup when display windows close

ORIGINALITY & UNIQUE FEATURES:

1. Overnight Session Handling:

Unlike basic horizontal line tools, this script properly handles overnight spans for evening times, making it invaluable for analyzing gaps and overnight price action.

2. Automatic Session Management:

No manual line drawing required - the script automatically manages when lines appear/disappear based on NY market sessions (15:59 close, 18:00 after-hours start).

3. Time-Window Display Logic:

Lines only show during relevant periods, reducing chart clutter and focusing attention on currently active levels.

TRADING CONCEPTS & APPLICATIONS:

1. Session-Based Analysis:

Capture opening prices at key session times:

00:00 NY: Sydney/Asian session start

03:00 NY: London pre-market

08:00 NY: London session open

09:30 NY: NYSE opening bell

18:00 NY: After-hours start

2. Gap Analysis:

Evening times (20:00-23:59) that extend overnight are particularly useful for:

Identifying potential gap-fill levels

Tracking overnight high/low breaks

Setting reference points for next-day trading

3. Support/Resistance Framework:

Opening prices at significant times often act as:

Intraday support/resistance levels

Reference points for breakout/breakdown analysis

Pivot levels for mean reversion strategies

HOW TO USE:

1. Time Input:

Enter times in "HH:MM" format using 24-hour NY time:

"09:30" for NYSE open

"15:30" for late-day reference

"20:00" for evening level (extends overnight)

2. Line Behavior:

Blue/Green/Cyan/Red lines: Your custom times

Yellow line: After-hours day open (18:00 NY start)

Lines appear with breaks during inactive periods

3. Strategic Setup:

Use 2-3 key session times for your trading style

Combine morning times (immediate reference) with evening times (overnight analysis)

Toggle after-hours line based on your market focus

CALCULATION METHOD:

The script uses direct opening price capture (no smoothing or averaging) at precise time hits, ensuring the most accurate representation of actual market levels at specified times. This raw price approach maintains the integrity of actual market opening prices rather than manipulated or calculated values.

This method is particularly effective because opening prices at significant times often represent institutional order flow and can act as magnetic levels throughout subsequent sessions.

AWR Pearsons R & LR Oscillator MTF1. Overview

This indicator is designed to analyze the correlation between a price series (or any custom indicator) and the bar index using Pearson’s correlation coefficient. It performs multiple linear regressions over shifted periods and then aggregates these results to create an oscillator. In addition, it integrates a multi-timeframe (MTF) analysis by retrieving the same calculations on 3 different time intervals, providing a more comprehensive view of the trend evolution.

2. User Parameters

The indicator offers several configurable parameters that allow the user to adjust both the calculations and the display:

Source (Linear Regression): The data source on which the regressions are applied (by default, the closing price).

Number of Linear Regressions (numOfLinReg): Allows choosing the number of correlation calculations (up to 10) to be carried out on different shifted periods.

Start Period (startPeriod) and Period Increment (periodIncrement): These parameters define the reference window for each regression. The calculation starts with a base period and then increases with each regression by a fixed increment, creating several time windows to assess the relationship between price evolution and time progression.

Deviation (def_deviation): Although defined, this parameter is intended to control the sensitivity of the calculations. It can be used in further developments of the indicator.

For Multi Time Frames analysis, three additional timeframes are provided through inputs in addition of the current period:

Sum up :

Timeframe 1 = current

Timeframe 2 = 30-minute (default settings)

Timeframe 3 = 1-hour (default settings)

Timeframe 4 = 4-hour (default settings)

These different timeframes allow you to obtain consistent or divergent signals over multiple resolutions, thereby enhancing the confidence of trading decisions.

3. Calculation Logic

At the core of the indicator is the f_calcConditions() function, which performs several essential tasks:

Calculating Pearson's Coefficients For each linear regression, the script uses ta.correlation() to measure the correlation between the chosen source (for example, the closing price) and the chronological index (bar_index). Up to 10 coefficients are computed over shifted windows, providing an evolving view of the linear relationship over different intervals.

Averaging the Results Once the coefficients are calculated, they are stored in an array and averaged to produce a global correlation value called avgPR_local.

Applying Moving Averages

The resulting average is then smoothed using several moving averages (SMA):

A short-term SMA (period of 14),

An intermediate SMA (period of 100),

A long-term SMA (period of 400).

These moving averages help to highlight the underlying trend of the oscillator by indicating the direction in which the correlation is moving.

Defining Trading Conditions Based on avgPR_local and its associated SMAs, multiple conditions are set to generate buy or sell signals:

Simple SMA Conditions :

Small signal :

Light blue below bar signal :

When the averaged coefficients lie between -1 and -0.63, are above the short-term SMA (14 periods), and are increasing, it may indicate a bullish dynamic (buy signal).

Orange above bar signal :

Conversely, when the value is higher (between 0.63 and 1) and below its SMA (14 periods), and are decreasing the trend is considered bearish (sell signal).

Medium signal :

Dark green signal

When the averaged coefficients lie between -1 and -0.45, are above the short-term SMA (14 periods), and are increasing, and also the average 100 is increasing. It may indicate a bullish dynamic (buy signal).

Light red signal :

Conversely, when the value is higher (between 0.45 and 1) and below its SMA (14 periods), the trend and are decreasing, and also the average 100 is decreasing. It may indicate a bearish dynamic(sell signal).

Light green signal :

When the averaged coefficients lie between -1 and -0.15, are above the short-term SMA (14 periods), and are increasing, and also the average 100 & 400 is increasing . It may indicate a bullish dynamic (buy signal).

Dark red signal :

Conversely, when the value is higher (between 0.45 and 1) and below its SMA (14 periods), the trend and are decreasing, and also the average 100 & 400 is decreasing. It may indicate a bearish dynamic(sell signal).

These additional conditions further refine the signals by verifying the consistency of the movement over longer periods. They check that the trends from the respective averages (intermediate and long-term) are in line with the direction indicated by the initial moving average.

These conditions are designed to capture moments when the oscillator's dynamics change, which can be interpreted as opportunities to enter or exit a trade.

4. Multi-Timeframes and Display

One of the main strengths of this indicator is its multi-timeframe approach.

This offers several advantages:

Comparative Analysis: Compare short-term dynamics with broader trends.

Enhanced Signal Reliability: A signal confirmed across multiple timeframes has a higher probability of success.

To visually highlight these signals on the chart, the indicator uses the plotchar() function with distinct symbols for each timeframe:

Current Timeframe: Signals are represented by the character "1"

30-Minute Timeframe: Displayed with the character "2".

1-Hour Timeframe: Displayed with the character "3".

4-Hour Timeframe: Displayed with the character "4".

The colors used are various shades of green for buy signals and shades of red/orange for sell signals, making it easy to distinguish between the different alerts.

5. Integrated Alerts

To avoid missing any trading opportunities, the indicator includes an alert condition via the alertcondition() function. This alert is triggered if any buy or sell signal is generated on any of the analyzed timeframes. The message "MTF valide" indicates that multiple timeframes are confirming the signal, enabling more informed decision-making.

6. How to Use This Indicator

Installation and Configuration: Copy the script into the TradingView Pine Script editor and add it to your chart. The default parameters can be tuned according to market behavior or personal preferences regarding sensitivity and responsiveness.

Interpreting the Signals:

Watch for the symbols on the chart corresponding to each timeframe.

A buy signal appears as a specific symbol below the bar (indicating a bullish condition based on a rising or less negative correlation), while a sell signal appears above the bar.

Multi-Timeframe Analysis: By comparing signals across timeframes, you can filter out false signals. For example, if the short-term timeframe shows a buy signal but the 4-hour timeframe indicates a bearish trend, you may need to reassess your position.

Adjusting the Settings: Depending on the asset type or market volatility, you might need to tweak the periods (startPeriod, periodIncrement) or the number of linear regressions to generate signals that better align with the price dynamics.

Using Alerts: Activate the built-in alert feature so that TradingView notifies you as soon as a multi-timeframe signal is detected. This ensures you stay informed even if you are not continuously monitoring the chart.

In Conclusion

The AWR Pearsons R & LR Oscillator MTF is a powerful tool for traders seeking a detailed understanding of market trends by combining statistical rigor (via Pearson's correlation coefficient) with a multi-timeframe approach. It is capable of generating clear entry and exit signals, visualized with specific symbols and colors depending on the timeframe. By adjusting the parameters to match your trading strategy and leveraging the alert system, you now have a robust instrument for making well-informed market decisions.

Feel free to dive deeper into each component and experiment with different configurations to see how the oscillator integrates with your overall technical analysis strategy. Enjoy exploring its potential and refining your trading approach!

ICT TIME ELEMENTS [KaninFX]## Overview

The ICT Time Elements indicator is a comprehensive trading tool designed to visualize the most critical market sessions and timeframes according to Inner Circle Trader (ICT) methodology. This indicator helps traders identify high-probability trading opportunities by highlighting key market sessions, killzones, and liquidity periods throughout the trading day.

## Key Features

### 🕐 Complete ICT Time Framework

- **Asian Range**: 8:00 PM - 12:00 AM (NY Time) - Evening consolidation period

- **London Killzone**: 2:00 AM - 5:00 AM (NY Time) - European market opening liquidity

- **NY Killzone**: 7:00 AM - 10:00 AM (NY Time) - US market opening with high volatility

- **Silver Bullet Sessions**:

- London Silver Bullet: 3:00 AM - 4:00 AM

- AM Silver Bullet: 10:00 AM - 11:00 AM

- PM Silver Bullet: 2:00 PM - 3:00 PM

- **Lunch Hours**: 5:00 AM - 7:00 AM & 12:00 PM - 1:00 PM (Lower volatility periods)

- **News Embargo**: 8:30 AM - 9:30 AM (High impact news release window)

- **20-Minute Macros**: :50 to :10 minutes of each hour (Short-term reversal periods)

- **True Day Close**: 4:00 PM - 4:30 PM (Official market close)

### 🎨 Visual Customization

- **Multiple Themes**: Dark, Light, and Custom color schemes

- **Adjustable Opacity**: Control zone transparency (0-100%)

- **Font Customization**: Tiny, Small, Normal, Large text sizes

- **Custom Colors**: Personalize each zone with your preferred colors

- **Professional Display**: Clean histogram visualization with zone labels

### 🌍 Multi-Timezone Support

Built-in support for major trading centers:

- America/New_York (Default)

- America/Chicago

- America/Los_Angeles

- Europe/London

- Asia/Tokyo

- Asia/Shanghai

- Australia/Sydney

### 📊 Smart Information Display

- **Real-time Zone Detection**: Automatically identifies current active session

- **Zone Labels**: Clear labeling at the center of each time period

- **Current Zone Indicator**: Arrow pointer showing the active session

- **Comprehensive Info Table**: Quick reference for all time zones and their schedules

- **Flexible Table Positioning**: Place info table in any corner of your chart

### ⚡ Performance Optimized

- **Memory Management**: Automatic cleanup of old labels to maintain performance

- **Efficient Processing**: Optimized time calculations for smooth operation

- **Resource Control**: Limited label generation to prevent system overload

## How It Works

The indicator continuously monitors the current time against predefined ICT session schedules. When price action enters a recognized time zone, the indicator:

1. **Highlights the Period**: Colors the histogram bar according to the active session

2. **Labels the Zone**: Places descriptive text identifying the current market condition

3. **Updates Info Table**: Shows current session status and complete schedule

4. **Tracks Macro Periods**: Identifies 20-minute reversal windows within major sessions

### Special Features

- **Macro Detection**: Automatically identifies when current time falls within a 20-minute macro period

- **Session Overlap Handling**: Properly manages overlapping time zones with priority logic

- **Dynamic Color Adjustment**: Theme-aware color selection for optimal visibility

## Best Use Cases

### For ICT Traders

- Identify optimal entry times during killzone sessions

- Recognize silver bullet opportunities for quick scalps

- Avoid trading during lunch hour consolidations

- Prepare for news embargo volatility

### For Session Traders

- Track major market session transitions

- Plan trading strategy around high-liquidity periods

- Understand global market flow and timing

### For Swing Traders

- Identify macro trend continuation points

- Time position entries during optimal sessions

- Understand market structure changes across sessions

## Installation & Setup

1. Add the indicator to your TradingView chart

2. Select your preferred timezone from the dropdown

3. Choose theme (Dark/Light) or customize colors

4. Adjust font size and table position to your preference

5. Enable/disable features as needed for your trading style

## Pro Tips

- **Combine with Price Action**: Use time zones alongside support/resistance levels

- **Focus on Killzones**: Highest probability setups occur during London and NY killzones

- **Watch Silver Bullets**: These 1-hour windows often provide excellent reversal opportunities

- **Respect Lunch Hours**: Lower volatility periods - consider smaller position sizes

- **News Embargo Awareness**: Prepare for potential whipsaws during 8:30-9:30 AM

## Conclusion

The ICT Time Elements indicator transforms complex ICT timing concepts into an easy-to-read visual tool. Whether you're a beginner learning ICT methodology or an experienced trader looking to optimize your timing, this indicator provides the essential market session awareness needed for successful trading.

*Compatible with all TradingView plans and timeframes. Works best on 1-minute to 1-hour charts for optimal session visualization.*

Casa_UtilsLibrary "Casa_Utils"

A collection of convenience and helper functions for indicator and library authors on TradingView

formatNumber(num)

My version of format number that doesn't have so many decimal places...

Parameters:

num (float) : The number to be formatted

Returns: The formatted number

getDateString(timestamp)

Convenience function returns timestamp in yyyy/MM/dd format.

Parameters:

timestamp (int) : The timestamp to stringify

Returns: The date string

getDateTimeString(timestamp)

Convenience function returns timestamp in yyyy/MM/dd hh:mm format.

Parameters:

timestamp (int) : The timestamp to stringify

Returns: The date string

getInsideBarCount()

Gets the number of inside bars for the current chart. Can also be passed to request.security to get the same for different timeframes.

Returns: The # of inside bars on the chart right now.

getLabelStyleFromString(styleString, acceptGivenIfNoMatch)

Tradingview doesn't give you a nice way to put the label styles into a dropdown for configuration settings. So, I specify them in the following format: "Center", "Left", "Lower Left", "Lower Right", "Right", "Up", "Upper Left", "Upper Right", "Plain Text", "No Labels". This function takes care of converting those custom strings back to the ones expected by tradingview scripts.

Parameters:

styleString (string)

acceptGivenIfNoMatch (bool) : If no match for styleString is found and this is true, the function will return styleString, otherwise it will return tradingview's preferred default

Returns: The string expected by tradingview functions

getTime(hourNumber, minuteNumber)

Given an hour number and minute number, adds them together and returns the sum. To be used by getLevelBetweenTimes when fetching specific price levels during a time window on the day.

Parameters:

hourNumber (int) : The hour number

minuteNumber (int) : The minute number

Returns: The sum of all the minutes

getHighAndLowBetweenTimes(start, end)

Given a start and end time, returns the high or low price during that time window.

Parameters:

start (int) : The timestamp to start with (# of seconds)

end (int) : The timestamp to end with (# of seconds)

Returns: The high or low value

getPremarketHighsAndLows()

Returns an expression that can be used by request.security to fetch the premarket high & low levels in a tuple.

Returns: (tuple)

getAfterHoursHighsAndLows()

Returns an expression that can be used by request.security to fetch the after hours high & low levels in a tuple.

Returns: (tuple)

getOvernightHighsAndLows()

Returns an expression that can be used by request.security to fetch the overnight high & low levels in a tuple.

Returns: (tuple)

getNonRthHighsAndLows()

Returns an expression that can be used by request.security to fetch the high & low levels for premarket, after hours and overnight in a tuple.

Returns: (tuple)

getLineStyleFromString(styleString, acceptGivenIfNoMatch)

Tradingview doesn't give you a nice way to put the line styles into a dropdown for configuration settings. So, I specify them in the following format: "Solid", "Dashed", "Dotted", "None/Hidden". This function takes care of converting those custom strings back to the ones expected by tradingview scripts.

Parameters:

styleString (string) : Plain english (or TV Standard) version of the style string

acceptGivenIfNoMatch (bool) : If no match for styleString is found and this is true, the function will return styleString, otherwise it will return tradingview's preferred default

Returns: The string expected by tradingview functions

getPercentFromPrice(price)

Get the % the current price is away from the given price.

Parameters:

price (float)

Returns: The % the current price is away from the given price.

getPositionFromString(position)

Tradingview doesn't give you a nice way to put the positions into a dropdown for configuration settings. So, I specify them in the following format: "Top Left", "Top Center", "Top Right", "Middle Left", "Middle Center", "Middle Right", "Bottom Left", "Bottom Center", "Bottom Right". This function takes care of converting those custom strings back to the ones expected by tradingview scripts.

Parameters:

position (string) : Plain english position string

Returns: The string expected by tradingview functions

getRsiAvgsExpression(rsiLength)

Call request.security with this as the expression to get the average up/down values that can be used with getRsiPrice (below) to calculate the price level where the supplied RSI level would be reached.

Parameters:

rsiLength (simple int) : The length of the RSI requested.

Returns: A tuple containing the avgUp and avgDown values required by the getRsiPrice function.

getRsiPrice(rsiLevel, rsiLength, avgUp, avgDown)

use the values returned by getRsiAvgsExpression() to calculate the price level when the provided RSI level would be reached.

Parameters:

rsiLevel (float) : The RSI level to find price at.

rsiLength (int) : The length of the RSI to calculate.

avgUp (float) : The average move up of RSI.

avgDown (float) : The average move down of RSI.

Returns: The price level where the provided RSI level would be met.

getSizeFromString(sizeString)

Tradingview doesn't give you a nice way to put the sizes into a dropdown for configuration settings. So, I specify them in the following format: "Auto", "Huge", "Large", "Normal", "Small", "Tiny". This function takes care of converting those custom strings back to the ones expected by tradingview scripts.

Parameters:

sizeString (string) : Plain english size string

Returns: The string expected by tradingview functions

getTimeframeOfChart()

Get the timeframe of the current chart for display

Returns: The string of the current chart timeframe

getTimeNowPlusOffset(candleOffset)

Helper function for drawings that use xloc.bar_time to help you know the time offset if you want to place the end of the drawing out into the future. This determines the time-size of one candle and then returns a time n candleOffsets into the future.

Parameters:

candleOffset (int) : The number of items to find singular/plural for.

Returns: The future time

getVolumeBetweenTimes(start, end)

Given a start and end time, returns the sum of all volume across bars during that time window.

Parameters:

start (int) : The timestamp to start with (# of seconds)

end (int) : The timestamp to end with (# of seconds)

Returns: The volume

isToday()

Returns true if the current bar occurs on today's date.

Returns: True if current bar is today

padLabelString(labelText, labelStyle)

Pads a label string so that it appears properly in or not in a label. When label.style_none is used, this will make sure it is left-aligned instead of center-aligned. When any other type is used, it adds a single space to the right so there is padding against the right end of the label.

Parameters:

labelText (string) : The string to be padded

labelStyle (string) : The style of the label being padded for.

Returns: The padded string

plural(num, singular, plural)

Helps format a string for plural/singular. By default, if you only provide num, it will just return "s" for plural and nothing for singular (eg. plural(numberOfCats)). But you can optionally specify the full singular/plural words for more complicated nomenclature (eg. plural(numberOfBenches, 'bench', 'benches'))

Parameters:

num (int) : The number of items to find singular/plural for.

singular (string) : The string to return if num is singular. Defaults to an empty string.

plural (string) : The string to return if num is plural. Defaults to 's' so you can just add 's' to the end of a word.

Returns: The singular or plural provided strings depending on the num provided.

timeframeInSeconds(timeframe)

Get the # of seconds in a given timeframe. Tradingview's timeframe.in_seconds() expects a simple string, and we often need to use series string, so this is an alternative to get you the value you need.

Parameters:

timeframe (string)

Returns: The number of secondsof that timeframe

timeframeOfChart()

Convert a timeframe string to a consistent standard.

Returns: The standard format for the string, or the unchanged value if it is unknown.

timeframeToString(timeframe)

Convert a timeframe string to a consistent standard.

Parameters:

timeframe (string)

Returns: (string) The standard format for the string, or the unchanged value if it is unknown.

stringToTimeframe(strTimeframe)

Convert an english-friendly timeframe string to a value that can be used by request.security. Specifically, this corrects hour strings (eg. 4h) to their numeric "minute" equivalent (eg. 240)

Parameters:

strTimeframe (string)

Returns: (string) The standard format for the string, or the unchanged value if it is unknown.

getPriceLabel(price, labelOffset, labelStyle, labelSize, labelColor, textColor)

Defines a label for the end of a price level line.

Parameters:

price (float) : The price level to render the label at.

labelOffset (int) : The number of candles to place the label to the right of price.

labelStyle (string) : A plain english string as defined in getLabelStyleFromString.

labelSize (string) : The size of the label.

labelColor (color) : The color of the label.

textColor (color) : The color of the label text (defaults to #ffffff)

Returns: The label that was created.

setPriceLabel(label, labelName, price, labelOffset, labelTemplate, labelStyle, labelColor, textColor)

Updates the label position & text based on price changes.

Parameters:

label (label) : The label to update.

labelName (string) : The name of the price level to be placed on the label.

price (float) : The price level to render the label at.

labelOffset (int) : The number of candles to place the label to the right of price.

labelTemplate (string) : The str.format template to use for the label. Defaults to: '{0}: {1} {2}{3,number,#.##}%' which means '{price}: {labelName} {+/-}{percentFromPrice}%'

labelStyle (string)

labelColor (color)

textColor (color)

getPriceLabelLine(price, labelOffset, labelColor, lineWidth)

Defines a line that will stretch from the plot line to the label.

Parameters:

price (float) : The price level to render the label at.

labelOffset (int) : The number of candles to place the label to the right of price.

labelColor (color)

lineWidth (int) : The width of the line. Defaults to 1.

setPriceLabelLine(line, price, labelOffset, lastTime, lineColor)

Updates the price label line based on price changes.

Parameters:

line (line) : The line to update.

price (float) : The price level to render the label at.

labelOffset (int) : The number of candles to place the label to the right of price.

lastTime (int) : The last time that the line should stretch from. Defaults to time.

lineColor (color)

SYMPL Reversal BandsThis is an expansion of the Hybrid moving average. It uses the same hybrid moving code from the hybrid moving average script with an additional layer using the ta.hma function for some slight additional smoothing. Colors of the bands change dynamically based of the long and short hybrid moving averages running in the background. This can be really helpful in identifying periods to short bounces or long dips.

Below is the explanation of the hybrid moving average

Hybrid Moving Average Market Trend System - , designed to visualize market trends using a combination of three moving averages: FRAMA (Fractal Adaptive Moving Average), VIDYA (Variable Index Dynamic Average), and a Hamming windowed Volume-Weighted Moving Average (VWMA).

Key Features:

FRAMA Calculation:

FRAMA adapts to market volatility by dynamically adjusting its smoothing factor based on the fractal dimension of price movement. This allows it to be more responsive during trending periods while filtering out noise in sideways markets. The FRAMA is calculated for both short and long periods

VIDYA with CMO:

The VIDYA (Variable Index Dynamic Average) is based on a Chande Momentum Oscillator (CMO), which adjusts the smoothing factor dynamically depending on the momentum of the market. Higher momentum periods result in more responsive averages, while low momentum periods lead to smoother averages. Like FRAMA, VIDYA is calculated for both short and long periods.

Hamming Windowed VWMA:

This VWMA variation applies a Hamming window to smooth the weighting of volume across the calculation period. This method emphasizes central data points and reduces noise, making the VWMA more adaptive to volume fluctuations. The Hamming VWMA is calculated for short and long periods, offering another layer of adaptability to the hybrid moving average.

Hybrid Moving Averages:

Dynamic Coloring and Filling:

The script uses dynamic color transitions to visually distinguish between bullish and bearish conditions:

Hybrid Moving Average - Market TrendHybrid Moving Average Market Trend System - , designed to visualize market trends using a combination of three moving averages: FRAMA (Fractal Adaptive Moving Average), VIDYA (Variable Index Dynamic Average), and a Hamming windowed Volume-Weighted Moving Average (VWMA).

Key Features:

FRAMA Calculation:

FRAMA adapts to market volatility by dynamically adjusting its smoothing factor based on the fractal dimension of price movement. This allows it to be more responsive during trending periods while filtering out noise in sideways markets. The FRAMA is calculated for both short and long periods

VIDYA with CMO:

The VIDYA (Variable Index Dynamic Average) is based on a Chande Momentum Oscillator (CMO), which adjusts the smoothing factor dynamically depending on the momentum of the market. Higher momentum periods result in more responsive averages, while low momentum periods lead to smoother averages. Like FRAMA, VIDYA is calculated for both short and long periods.

Hamming Windowed VWMA:

This VWMA variation applies a Hamming window to smooth the weighting of volume across the calculation period. This method emphasizes central data points and reduces noise, making the VWMA more adaptive to volume fluctuations. The Hamming VWMA is calculated for short and long periods, offering another layer of adaptability to the hybrid moving average.

Hybrid Moving Averages:

Dynamic Coloring and Filling:

The script uses dynamic color transitions to visually distinguish between bullish and bearish conditions:

Overnight vs Intra-day Performance█ STRATEGY OVERVIEW

The "Overnight vs Intra-day Performance" indicator quantifies price behaviour differences between trading hours and overnight periods. It calculates cumulative returns, compound growth rates, and visualizes performance components across user-defined time windows. Designed for analytical use, it helps identify whether returns are primarily generated during market hours or overnight sessions.

█ USAGE

Use this indicator on Stocks and ETFs to visualise and compare intra-day vs overnight performance

█ KEY FEATURES

Return Segmentation : Separates total returns into overnight (close-to-open) and intraday (open-to-close) components

Growth Tracking : Shows simple cumulative returns and compound annual growth rates (CAGR)

█ VISUALIZATION SYSTEM

1. Time-Series

Overnight Returns (Red)

Intraday Returns (Blue)

Total Returns (White)

2. Summary Table

Displays CAGR

3. Price Chart Labels

Floating annotations showing absolute returns and CAGR

Color-coded to match plot series

█ PURPOSE

Quantify market behaviour disparities between active trading sessions and overnight positioning

Provide institutional-grade attribution analysis for returns generation

Enable tactical adjustment of trading schedules based on historical performance patterns

Serve as foundational research for session-specific trading strategies

█ IDEAL USERS

1. Portfolio Managers

Analyse overnight risk exposure across holdings

Optimize execution timing based on return distributions

2. Quantitative Researchers

Study market microstructure through time-segmented returns

Develop alpha models leveraging session-specific anomalies

3. Market Microstructure Analysts

Identify liquidity patterns in overnight vs daytime sessions

Research ETF premium/discount mechanics

4. Day Traders

Align trading hours with highest probability return windows

Avoid overnight gaps through informed position sizing

mathLibrary "math"

It's a library of discrete aproximations of a price or Series float it uses Fourier Discrete transform, Laplace Discrete Original and Modified transform and Euler's Theoreum for Homogenus White noice operations. Calling functions without source value it automatically take close as the default source value.

Here is a picture of Laplace and Fourier approximated close prices from this library:

Copy this indicator and try it yourself:

import AutomatedTradingAlgorithms/math/1 as math

//@version=5

indicator("Close Price with Aproximations", shorttitle="Close and Aproximations", overlay=false)

// Sample input data (replace this with your own data)

inputData = close

// Plot Close Price

plot(inputData, color=color.blue, title="Close Price")

ltf32_result = math.LTF32(a=0.01)

plot(ltf32_result, color=color.green, title="LTF32 Aproximation")

fft_result = math.FFT()

plot(fft_result, color=color.red, title="Fourier Aproximation")

wavelet_result = math.Wavelet()

plot(wavelet_result, color=color.orange, title="Wavelet Aproximation")

wavelet_std_result = math.Wavelet_std()

plot(wavelet_std_result, color=color.yellow, title="Wavelet_std Aproximation")

DFT3(xval, _dir)

Discrete Fourier Transform with last 3 points

Parameters:

xval (float) : Source series

_dir (int) : Direction parameter

Returns: Aproxiated source value

DFT2(xval, _dir)

Discrete Fourier Transform with last 2 points

Parameters:

xval (float) : Source series

_dir (int) : Direction parameter

Returns: Aproxiated source value

FFT(xval)

Fast Fourier Transform once. It aproximates usig last 3 points.

Parameters:

xval (float) : Source series

Returns: Aproxiated source value

DFT32(xval)

Combined Discrete Fourier Transforms of DFT3 and DTF2 it aproximates last point by first

aproximating last 3 ponts and than using last 2 points of the previus.

Parameters:

xval (float) : Source series

Returns: Aproxiated source value

DTF32(xval)

Combined Discrete Fourier Transforms of DFT3 and DTF2 it aproximates last point by first

aproximating last 3 ponts and than using last 2 points of the previus.

Parameters:

xval (float) : Source series

Returns: Aproxiated source value

LFT3(xval, _dir, a)

Discrete Laplace Transform with last 3 points

Parameters:

xval (float) : Source series

_dir (int) : Direction parameter

a (float) : laplace coeficient

Returns: Aproxiated source value

LFT2(xval, _dir, a)

Discrete Laplace Transform with last 2 points

Parameters:

xval (float) : Source series

_dir (int) : Direction parameter

a (float) : laplace coeficient

Returns: Aproxiated source value

LFT(xval, a)

Fast Laplace Transform once. It aproximates usig last 3 points.

Parameters:

xval (float) : Source series

a (float) : laplace coeficient

Returns: Aproxiated source value

LFT32(xval, a)

Combined Discrete Laplace Transforms of LFT3 and LTF2 it aproximates last point by first

aproximating last 3 ponts and than using last 2 points of the previus.

Parameters:

xval (float) : Source series

a (float) : laplace coeficient

Returns: Aproxiated source value

LTF32(xval, a)

Combined Discrete Laplace Transforms of LFT3 and LTF2 it aproximates last point by first

aproximating last 3 ponts and than using last 2 points of the previus.

Parameters:

xval (float) : Source series

a (float) : laplace coeficient

Returns: Aproxiated source value

whitenoise(indic_, _devided, minEmaLength, maxEmaLength, src)

Ehler's Universal Oscillator with White Noise, without extra aproximated src.

It uses dinamic EMA to aproximate indicator and thus reducing noise.

Parameters:

indic_ (float) : Input series for the indicator values to be smoothed

_devided (int) : Divisor for oscillator calculations

minEmaLength (int) : Minimum EMA length

maxEmaLength (int) : Maximum EMA length

src (float) : Source series

Returns: Smoothed indicator value

whitenoise(indic_, dft1, _devided, minEmaLength, maxEmaLength, src)

Ehler's Universal Oscillator with White Noise and DFT1.

It uses src and sproxiated src (dft1) to clearly define white noice.

It uses dinamic EMA to aproximate indicator and thus reducing noise.

Parameters:

indic_ (float) : Input series for the indicator values to be smoothed

dft1 (float) : Aproximated src value for white noice calculation

_devided (int) : Divisor for oscillator calculations

minEmaLength (int) : Minimum EMA length

maxEmaLength (int) : Maximum EMA length

src (float) : Source series

Returns: Smoothed indicator value

smooth(dft1, indic__, _devided, minEmaLength, maxEmaLength, src)

Smoothing source value with help of indicator series and aproximated source value

It uses src and sproxiated src (dft1) to clearly define white noice.

It uses dinamic EMA to aproximate src and thus reducing noise.

Parameters:

dft1 (float) : Value to be smoothed.

indic__ (float) : Optional input for indicator to help smooth dft1 (default is FFT)

_devided (int) : Divisor for smoothing calculations

minEmaLength (int) : Minimum EMA length

maxEmaLength (int) : Maximum EMA length

src (float) : Source series

Returns: Smoothed source (src) series

smooth(indic__, _devided, minEmaLength, maxEmaLength, src)

Smoothing source value with help of indicator series

It uses dinamic EMA to aproximate src and thus reducing noise.

Parameters:

indic__ (float) : Optional input for indicator to help smooth dft1 (default is FFT)

_devided (int) : Divisor for smoothing calculations

minEmaLength (int) : Minimum EMA length

maxEmaLength (int) : Maximum EMA length

src (float) : Source series

Returns: Smoothed src series

vzo_ema(src, len)

Volume Zone Oscillator with EMA smoothing

Parameters:

src (float) : Source series

len (simple int) : Length parameter for EMA

Returns: VZO value

vzo_sma(src, len)

Volume Zone Oscillator with SMA smoothing

Parameters:

src (float) : Source series

len (int) : Length parameter for SMA

Returns: VZO value

vzo_wma(src, len)

Volume Zone Oscillator with WMA smoothing

Parameters:

src (float) : Source series

len (int) : Length parameter for WMA

Returns: VZO value

alma2(series, windowsize, offset, sigma)

Arnaud Legoux Moving Average 2 accepts sigma as series float

Parameters:

series (float) : Input series

windowsize (int) : Size of the moving average window

offset (float) : Offset parameter

sigma (float) : Sigma parameter

Returns: ALMA value

Wavelet(src, len, offset, sigma)

Aproxiates srt using Discrete wavelet transform.

Parameters:

src (float) : Source series

len (int) : Length parameter for ALMA

offset (simple float)

sigma (simple float)

Returns: Wavelet-transformed series

Wavelet_std(src, len, offset, mag)

Aproxiates srt using Discrete wavelet transform with standard deviation as a magnitude.

Parameters:

src (float) : Source series

len (int) : Length parameter for ALMA

offset (float) : Offset parameter for ALMA

mag (int) : Magnitude parameter for standard deviation

Returns: Wavelet-transformed series

LaplaceTransform(xval, N, a)

Original Laplace Transform over N set of close prices

Parameters:

xval (float) : series to aproximate

N (int) : number of close prices in calculations

a (float) : laplace coeficient

Returns: Aproxiated source value

NLaplaceTransform(xval, N, a, repeat)

Y repetirions on Original Laplace Transform over N set of close prices, each time N-k set of close prices

Parameters:

xval (float) : series to aproximate

N (int) : number of close prices in calculations

a (float) : laplace coeficient

repeat (int) : number of repetitions

Returns: Aproxiated source value

LaplaceTransformsum(xval, N, a, b)

Sum of 2 exponent coeficient of Laplace Transform over N set of close prices

Parameters:

xval (float) : series to aproximate

N (int) : number of close prices in calculations

a (float) : laplace coeficient

b (float) : second laplace coeficient

Returns: Aproxiated source value

NLaplaceTransformdiff(xval, N, a, b, repeat)

Difference of 2 exponent coeficient of Laplace Transform over N set of close prices

Parameters:

xval (float) : series to aproximate

N (int) : number of close prices in calculations

a (float) : laplace coeficient

b (float) : second laplace coeficient

repeat (int) : number of repetitions

Returns: Aproxiated source value

N_divLaplaceTransformdiff(xval, N, a, b, repeat)

N repetitions of Difference of 2 exponent coeficient of Laplace Transform over N set of close prices, with dynamic rotation

Parameters:

xval (float) : series to aproximate

N (int) : number of close prices in calculations

a (float) : laplace coeficient

b (float) : second laplace coeficient

repeat (int) : number of repetitions

Returns: Aproxiated source value

LaplaceTransformdiff(xval, N, a, b)

Difference of 2 exponent coeficient of Laplace Transform over N set of close prices

Parameters:

xval (float) : series to aproximate

N (int) : number of close prices in calculations

a (float) : laplace coeficient

b (float) : second laplace coeficient

Returns: Aproxiated source value

NLaplaceTransformdiffFrom2(xval, N, a, b, repeat)

N repetitions of Difference of 2 exponent coeficient of Laplace Transform over N set of close prices, second element has for 1 higher exponent factor

Parameters:

xval (float) : series to aproximate

N (int) : number of close prices in calculations

a (float) : laplace coeficient

b (float) : second laplace coeficient

repeat (int) : number of repetitions

Returns: Aproxiated source value

N_divLaplaceTransformdiffFrom2(xval, N, a, b, repeat)

N repetitions of Difference of 2 exponent coeficient of Laplace Transform over N set of close prices, second element has for 1 higher exponent factor, dynamic rotation

Parameters:

xval (float) : series to aproximate

N (int) : number of close prices in calculations

a (float) : laplace coeficient

b (float) : second laplace coeficient

repeat (int) : number of repetitions

Returns: Aproxiated source value

LaplaceTransformdiffFrom2(xval, N, a, b)

Difference of 2 exponent coeficient of Laplace Transform over N set of close prices, second element has for 1 higher exponent factor

Parameters:

xval (float) : series to aproximate

N (int) : number of close prices in calculations

a (float) : laplace coeficient

b (float) : second laplace coeficient

Returns: Aproxiated source value

Deep Volume [ChartPrime]Deep Volume is an indicator designed to give you high fidelity volume information. It does this by utilizing real time data provided by Tradingview to generate a wide range of metrics. We have included a convenient column chart to visualize the polarity of the volume, and a table to see the real time data. This works by utilizing pine script's varip feature to get information within candles. This is convenient as it allows users to get lower time frame information without the use of ltf functions. The result is seconds level data with out the need to be on a lower time frame chart. As a result, as you increase the time frame of the chart the updates will become slower. This is because Tradingview doesn't update the chart information as frequently on higher time frames as there isn't as much of a need.

This indicator works on real time data so to compensate for this we generate a simulated history based on candle structure. This helps in estimating the state of the moving average before the real time data starts. As a result the estimated history isn't as accurate and should be treated as such. That being said it is nice to have an estimation when the indicator is first loaded onto the chart.

Finally we have included a cumulative volume comparison that shows you how much volume there is compared to the average cumulative volume for the day. This metric utilizes a gradient to help you interpret the information at a glance. Low daily volume is represented with grays by default, while normal volume and greater is represented with a green color by default.

The table is partitioned into two sections; tick data, and average data. On the left you will see color coded information based on the direction of the move. On the left, the information is color coded based on the average movement direction. You can control how much information is displayed in the table within the indicators settings. This is defaulted to 20 but it can be as long or short as you like. Every new candle open the far left of the table you will see a 🗘 symbol and at the start of a new session you will see a 🗓 symbol.

The included metrics are as follows:

Time: This displays the time of the real time data update.

Time Delta: This displays the elapsed time between updates.

Order Size: This is the volume times the price change between updates.

Volume: This is the volume change for the update.

Price Change: This is the change in price since the last update.

Price: This is the price of the asset at the time of the update.

Speed of Tape: This is the average time delta. Use this to see how quickly the market is moving.

Average Order Size: This is the average order size.

Average Volume: This is the average volume

Volume Ratio: This the the ratio of bullish to bearish volume as expressed by a percent. 100% is all bullish within the window and -100% is all bearish within the window.

Average Price Change: This is the average price change within the window.

Sensitivity: This is a volatility metric designed to show you the price change per 1 volume unit.

Relative Sensitivity: This is a volatility metric designed to show you the average price change per average volume.

Enjoy

UtilsLibrary "Utils"

A collection of convenience and helper functions for indicator and library authors on TradingView

formatNumber(num)

My version of format number that doesn't have so many decimal places...

Parameters:

num (float) : (float) the number to be formatted

Returns: (string) The formatted number

getDateString(timestamp)

Convenience function returns timestamp in yyyy/MM/dd format.

Parameters:

timestamp (int) : (int) The timestamp to stringify

Returns: (int) The date string

getDateTimeString(timestamp)

Convenience function returns timestamp in yyyy/MM/dd hh:mm format.

Parameters:

timestamp (int) : (int) The timestamp to stringify

Returns: (int) The date string

getInsideBarCount()

Gets the number of inside bars for the current chart. Can also be passed to request.security to get the same for different timeframes.

Returns: (int) The # of inside bars on the chart right now.

getLabelStyleFromString(styleString, acceptGivenIfNoMatch)

Tradingview doesn't give you a nice way to put the label styles into a dropdown for configuration settings. So, I specify them in the following format: . This function takes care of converting those custom strings back to the ones expected by tradingview scripts.

Parameters:

styleString (string)

acceptGivenIfNoMatch (bool) : (bool) If no match for styleString is found and this is true, the function will return styleString, otherwise it will return tradingview's preferred default

Returns: (string) The string expected by tradingview functions

getTime(hourNumber, minuteNumber)

Given an hour number and minute number, adds them together and returns the sum. To be used by getLevelBetweenTimes when fetching specific price levels during a time window on the day.

Parameters:

hourNumber (int) : (int) The hour number

minuteNumber (int) : (int) The minute number

Returns: (int) The sum of all the minutes

getHighAndLowBetweenTimes(start, end)

Given a start and end time, returns the high or low price during that time window.

Parameters:

start (int) : The timestamp to start with (# of seconds)

end (int) : The timestamp to end with (# of seconds)

Returns: (float) The high or low value

getPremarketHighsAndLows()

Returns an expression that can be used by request.security to fetch the premarket high & low levels in a tuple.

Returns: (tuple)

getAfterHoursHighsAndLows()

Returns an expression that can be used by request.security to fetch the after hours high & low levels in a tuple.

Returns: (tuple)

getOvernightHighsAndLows()

Returns an expression that can be used by request.security to fetch the overnight high & low levels in a tuple.

Returns: (tuple)

getNonRthHighsAndLows()

Returns an expression that can be used by request.security to fetch the high & low levels for premarket, after hours and overnight in a tuple.

Returns: (tuple)

getLineStyleFromString(styleString, acceptGivenIfNoMatch)

Tradingview doesn't give you a nice way to put the line styles into a dropdown for configuration settings. So, I specify them in the following format: . This function takes care of converting those custom strings back to the ones expected by tradingview scripts.

Parameters:

styleString (string) : (string) Plain english (or TV Standard) version of the style string

acceptGivenIfNoMatch (bool) : (bool) If no match for styleString is found and this is true, the function will return styleString, otherwise it will return tradingview's preferred default

Returns: (string) The string expected by tradingview functions

getPercentFromPrice(price)

Get the % the current price is away from the given price.

Parameters:

price (float)

Returns: (float) The % the current price is away from the given price.

getPositionFromString(position)

Tradingview doesn't give you a nice way to put the positions into a dropdown for configuration settings. So, I specify them in the following format: . This function takes care of converting those custom strings back to the ones expected by tradingview scripts.

Parameters:

position (string) : (string) Plain english position string

Returns: (string) The string expected by tradingview functions

getTimeframeOfChart()

Get the timeframe of the current chart for display

Returns: (string) The string of the current chart timeframe

getTimeNowPlusOffset(candleOffset)

Helper function for drawings that use xloc.bar_time to help you know the time offset if you want to place the end of the drawing out into the future. This determines the time-size of one candle and then returns a time n candleOffsets into the future.

Parameters:

candleOffset (int) : (int) The number of items to find singular/plural for.

Returns: (int) The future time

getVolumeBetweenTimes(start, end)

Given a start and end time, returns the sum of all volume across bars during that time window.

Parameters:

start (int) : The timestamp to start with (# of seconds)

end (int) : The timestamp to end with (# of seconds)

Returns: (float) The volume

isToday()

Returns true if the current bar occurs on today's date.

Returns: (bool) True if current bar is today

padLabelString(labelText, labelStyle)