TASC 2024.04 The Ultimate Smoother█ OVERVIEW

This script presents an implementation of the digital smoothing filter introduced by John Ehlers in his article "The Ultimate Smoother" from the April 2024 edition of TASC's Traders' Tips .

█ CONCEPTS

The UltimateSmoother preserves low-frequency swings in the input time series while attenuating high-frequency variations and noise. The defining input parameter of the UltimateSmoother is the critical period , which represents the minimum wavelength (highest frequency) in the filter's pass band. In other words, the filter attenuates or removes the amplitudes of oscillations at shorter periods than the critical period.

According to Ehlers, one primary advantage of the UltimateSmoother is that it maintains zero lag in its pass band and minimal lag in its transition band, distinguishing it from other conventional digital filters (e.g., moving averages ). One can apply this smoother to various input data series, including other indicators.

█ CALCULATIONS

Ehlers derived the UltimateSmoother using inspiration from the design principles he learned from his experience with analog filters , as described in the original publication. On a technical level, the UltimateSmoother's unique response involves subtracting a high-pass response from an all-pass response . At very low frequencies (lengthy periods), where the high-pass filter response has virtually no amplitude, the subtraction yields a frequency and phase response practically equivalent to the input data. At other frequencies, the subtraction achieves filtration through cancellation due to the close similarities in response between the high-pass filter and the input data.

חפש סקריפטים עבור "《中国区域创新能力评价报告2024》"

TASC 2024.03 Rate of Directional Change█ OVERVIEW

This script implements the Rate of Directional Change (RODC) indicator introduced by Richard Poster in the "Taming The Effects Of Whipsaw" article featured in the March 2024 edition of TASC's Traders' Tips .

█ CONCEPTS

In his article, Richard Poster discusses an approach to potentially reduce false trend-following strategy entry signals due to whipsaws in forex data. The RODC indicator is central to this approach. The idea behind RODC is that one can characterize market whipsaw as alternating up and down ZigZag segments. By counting the number of up and down segments within a lookback window, the RODC indicator aims to identify if the window contains a significant whipsaw pattern:

RODC = 100 * Segments / Window Size (bars)

Larger RODC values suggest elevated whipsaw in the calculation window, while smaller values signify trending price activity.

█ CALCULATIONS

• For each price bar, the script iterates through the lookback window to identify up and down segments.

• If the price change between subsequent bars within the window is in the direction opposite to the current segment and exceeds the specified threshold , the calculation interprets the condition as a reversal point and the start of a new segment.

• The script uses the number of segments within the window to calculate RODC according to the above formula.

• Finally, the script applies a simple moving average to smoothen the RODC data.

Users can change the length of the lookback window , the threshold value, and the smoothing length in the "Inputs" tab of the script's settings.

TASC 2024.02 Price-Time Filtering█ OVERVIEW

This script implements a price-time trend filter proposed by Alfred François Tagher in the “Trend Identification By Price And Time Filtering” article from the February 2024 edition of TASC's Traders' Tips .

█ CONCEPTS

In his article, Alfred François Tagher proposed a rule set designed to minimize the impact of stochastic price movements, facilitating the identification of larger-scale trends. The rules are:

• If the most recent week's close exceeds the previous week's high, the trend is up.

• If the most recent week's close is below the previous week's low, the trend is down.

• The trend remains unchanged until one of the above conditions occurs.

Similar rules can also apply to monthly bars.

The author argues that this approach integrates characteristics of conventional price action and time dynamics filters, so he refers to it as price-time filtering .

█ CALCULATIONS

This script applies the above price-time filtering rules and offers multiple ways to view the results on a chart:

• In the "Oscillator" view mode, the script counts and displays the number of bars in the uptrend and downtrend.

• In the "Linebreak" view mode, the trend filter is presented in a format resembling a point-and-figure (P&F) chart , with the length of each bar corresponding to the high-low range of the respective trend.

• In both view modes, the script offers bar coloring of the main chart based on the identified trend.

TASC 2024.01 Gap Momentum System█ OVERVIEW

TASC's January 2024 edition of Traders' Tips features an article titled “Gap Momentum” by Perry J. Kaufman. The article discusses how a trader might create a momentum strategy based on opening gap data. This script implements the Gap Momentum system presented therein.

█ CONCEPTS

In the article, Perry J. Kaufman introduces Gap Momentum as a cumulative series constructed in the same way as On-Balance Volume (OBV) , but using gap openings (today’s open minus yesterday’s close).

To smoothen the resulting time series (i.e., obtain the " signal line "), the author applies a simple moving average . Subsequently, he proposes the following two trading rules for a long-only trading system:

• Enter a long position when the signal line is moving higher.

• Exit when the signal line is moving lower.

█ CALCULATIONS

The calculation of Gap Momentum involves the following steps:

1. Calculate the ratio of the sum of positive gaps over the past N days to the sum of negative gaps (absolute values) over the same time period.

2. Add the resulting gap ratio to the cumulative time series. This time series is the Gap Momentum.

3. Keep moving forward, as in an N-day moving average.

#1 Vishal Toora Buy Sell Tablecopyright Vishal Toora

**“© 2025 Vishal Toora — counting volumes so you don’t have to. Buy, sell, or just stare at the screen.”**

Or a few more playful options:

1. **“© Vishal Toora — making deltas speak louder than your ex.”**

2. **“© Vishal Toora — one signal to rule them all (Buy/Sell/Neutral).”**

3. **“© Vishal Toora — because guessing markets is so 2024.”**

Disclaimer: This indicator is for educational and informational purposes only. I do not claim 100% accuracy, and you are responsible for your own trading decisions.

Fed Rate Change Impact📊 Fed Rate Change Impact — Macro Event-Driven Indicator

Fed Rate Change Impact is an advanced indicator designed to analyze the impact of Federal Reserve interest rate changes on financial markets. It integrates event-driven logic with dynamic visualization, percentage diagnostics, and multi-asset selection, offering a clear and customizable view of post-event effects.

🔍 Key Features 📅 Preloaded Fed Events : Includes over 30 historical rate cut (↓) and hike (↑) dates from 2008 to 2024.

📈 Post-Event Analysis : Calculates the percentage change of the selected asset 5, 10, and 30 days after each event.

📌 Vertical Chart Lines : Visually highlights each event directly on the chart, with dynamic coloring (red for hikes, green for cuts).

📋 Diagnostic Table : Displays real-time impact for each event, with color-coded values and a compact layout.

🧠 Interactive Filter: Choose to display only hikes, only cuts, or both.

🧭 Flexible Asset Selection : Analyze the current chart asset, pick from a predefined list, or manually input any ticker via input.symbol().

🎯 Contextual Highlighting : The table highlights the analyzed asset if it matches the active chart symbol.

⚙️ Customizable Parameters lookahead5, lookahead10, lookahead30: Define the time horizon for measuring post-event impact.

eventFilter : Choose which type of events to display.

presetAsset / customAsset : Select or input the asset to analyze.

🧪 Recommended Use Cases Macroeconomic analysis on indices, commodities, crypto, and forex

Studying delayed effects of rate changes on sensitive assets

Building event-driven strategies or diagnostic overlays

Visual backtesting and cross-asset comparison

🧠 Technical Notes The indicator is compatible with overlay=true and works best on Daily timeframe.

The table automatically adapts to the number of events and includes visual padding for improved readability.

All calculations are performed in real time and require no external data.

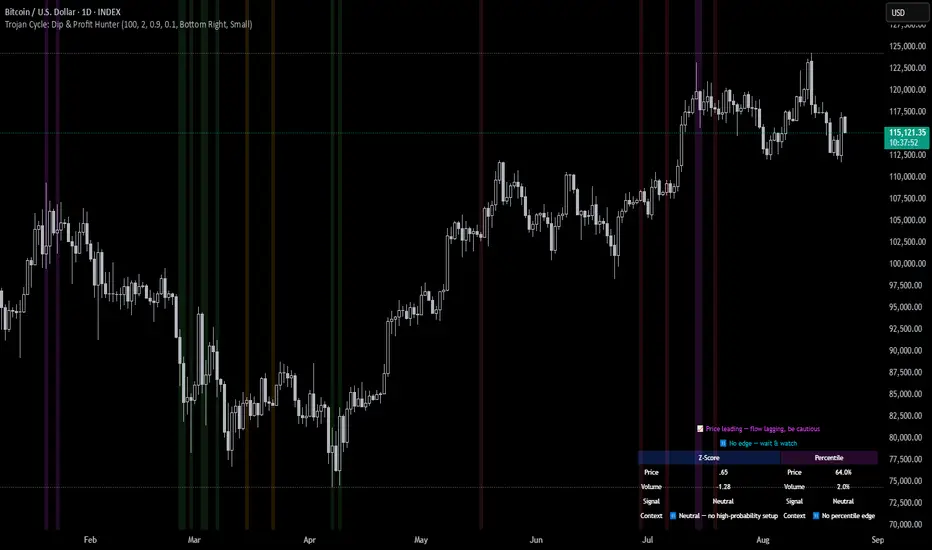

Trojan Cycle: Dip & Profit Hunter📉 Crypto is changing. Your signals should too.

This script doesn’t try to outguess price — it helps you track capital rotation and flow behavior in alignment with the evolving macro structure of the digital asset market.

Trojan Cycle: Dip & Profit Hunter is a signal engine built to support and validate the capital rotation models outlined in the Trojan Cycle and Synthetic Rotation theses — available via RWCS_LTD’s published charts

It is not a classic “buy low, sell high” tool. It is a structural filter that uses price/volume statistics to surface accumulation zones, synthetic traps, and macro context shifts — all aligned with the institutionalization of crypto post-2024.

🧠 Purpose & Value

Crypto no longer follows the retail-led, halving-driven pattern of 2017 or 2021.

Instead, institutional infrastructure, regulatory filters, and equity-market Trojan horses define the new path of capital.

This tool helps you visualize that path by interpreting behavior through statistical imbalances and real-time momentum signals.

Use it to:

Track where capital is accumulating or exiting

Identify signals consistent with true cycle rotation (vs. synthetic traps)

Validate your macro view with real-time statistical context

🔍 How It Works

The engine combines four signal layers:

1. Z-Score Logic

- Measures how far price and volume have deviated from their mean

- Detects dips, blowoffs, and exhaustion zones

2. Percentile Logic

- Compares current price and volume to historical rank distribution

- Flags statistically rare conditions (e.g. bottom 10% price, top 90% volume)

3. Combined Context Engine

- Integrates both models to generate one of 36 unique output states

- Each state provides a labeled market context (e.g., 🟢 Confluent Buy, 🔴 Confluent Sell, 🧨 Synthetic Trap )

4. Momentum Spread & Divergence

- Measures whether price is leading volume (trap risk) or volume is leading price (accumulation)

- Outputs intuitive momentum context with emoji-coded alerts

📋 What You See

🧠 Contextual Table UI with key Z-Scores, percentiles, signals, and market commentary

🎯 Emoji-coded signals to quickly grasp high-probability setups or risk zones

🌊 Optional overlays: price/volume divergence, momentum spread

🎨 Visual table customization (size, position) and chart highlights for signal clarity

🔔 Alert System

✅ Single dynamic alert using alert() that only fires when signal context changes

Prevents alert fatigue and allows clean webhook/automation integration

🧭 Use Cases

For macro cycle traders: Track where we are in the Trojan Cycle using statistical context

For thesis explorers: Use the 36-output signal map to match against your rotation thesis

For capital rotation watchers: Identify structural setups consistent with ETF-driven or compliance-filtered flow

For narrative skeptics: Avoid synthetic altseason traps where volume lags or flow dries up

🧪 Suggested Pairing for Thesis Validation

To use this tool as part of a thesis-confirmation framework , pair it with:

BTC.D — Bitcoin Dominance

ETH/BTC — Ethereum strength vs. Bitcoin

TOTALE100/ETH — Altcoin strength relative to ETH

RWCS_LTD’s published charts and macro cycle models

🏁 Final Note

Crypto has matured. So should your signals.

This tool doesn’t try to game the next 2 candles. It helps you understand the current phase in a compliance-filtered, institutionalized rotation model.

It’s not built for hype — it’s built for conviction.

Explore the thesis → Validate the structure → Trade with clarity.

🚨 Disclaimer

This script is not financial advice. It is an analytical tool designed to support market structure research and rotation thesis validation. Use this as part of a broader framework including technical structure, dominance charts, and macro data.

Adaptive Investment Timing ModelA COMPREHENSIVE FRAMEWORK FOR SYSTEMATIC EQUITY INVESTMENT TIMING

Investment timing represents one of the most challenging aspects of portfolio management, with extensive academic literature documenting the difficulty of consistently achieving superior risk-adjusted returns through market timing strategies (Malkiel, 2003).

Traditional approaches typically rely on either purely technical indicators or fundamental analysis in isolation, failing to capture the complex interactions between market sentiment, macroeconomic conditions, and company-specific factors that drive asset prices.

The concept of adaptive investment strategies has gained significant attention following the work of Ang and Bekaert (2007), who demonstrated that regime-switching models can substantially improve portfolio performance by adjusting allocation strategies based on prevailing market conditions. Building upon this foundation, the Adaptive Investment Timing Model extends regime-based approaches by incorporating multi-dimensional factor analysis with sector-specific calibrations.

Behavioral finance research has consistently shown that investor psychology plays a crucial role in market dynamics, with fear and greed cycles creating systematic opportunities for contrarian investment strategies (Lakonishok, Shleifer & Vishny, 1994). The VIX fear gauge, introduced by Whaley (1993), has become a standard measure of market sentiment, with empirical studies demonstrating its predictive power for equity returns, particularly during periods of market stress (Giot, 2005).

LITERATURE REVIEW AND THEORETICAL FOUNDATION

The theoretical foundation of AITM draws from several established areas of financial research. Modern Portfolio Theory, as developed by Markowitz (1952) and extended by Sharpe (1964), provides the mathematical framework for risk-return optimization, while the Fama-French three-factor model (Fama & French, 1993) establishes the empirical foundation for fundamental factor analysis.

Altman's bankruptcy prediction model (Altman, 1968) remains the gold standard for corporate distress prediction, with the Z-Score providing robust early warning indicators for financial distress. Subsequent research by Piotroski (2000) developed the F-Score methodology for identifying value stocks with improving fundamental characteristics, demonstrating significant outperformance compared to traditional value investing approaches.

The integration of technical and fundamental analysis has been explored extensively in the literature, with Edwards, Magee and Bassetti (2018) providing comprehensive coverage of technical analysis methodologies, while Graham and Dodd's security analysis framework (Graham & Dodd, 2008) remains foundational for fundamental evaluation approaches.

Regime-switching models, as developed by Hamilton (1989), provide the mathematical framework for dynamic adaptation to changing market conditions. Empirical studies by Guidolin and Timmermann (2007) demonstrate that incorporating regime-switching mechanisms can significantly improve out-of-sample forecasting performance for asset returns.

METHODOLOGY

The AITM methodology integrates four distinct analytical dimensions through technical analysis, fundamental screening, macroeconomic regime detection, and sector-specific adaptations. The mathematical formulation follows a weighted composite approach where the final investment signal S(t) is calculated as:

S(t) = α₁ × T(t) × W_regime(t) + α₂ × F(t) × (1 - W_regime(t)) + α₃ × M(t) + ε(t)

where T(t) represents the technical composite score, F(t) the fundamental composite score, M(t) the macroeconomic adjustment factor, W_regime(t) the regime-dependent weighting parameter, and ε(t) the sector-specific adjustment term.

Technical Analysis Component

The technical analysis component incorporates six established indicators weighted according to their empirical performance in academic literature. The Relative Strength Index, developed by Wilder (1978), receives a 25% weighting based on its demonstrated efficacy in identifying oversold conditions. Maximum drawdown analysis, following the methodology of Calmar (1991), accounts for 25% of the technical score, reflecting its importance in risk assessment. Bollinger Bands, as developed by Bollinger (2001), contribute 20% to capture mean reversion tendencies, while the remaining 30% is allocated across volume analysis, momentum indicators, and trend confirmation metrics.

Fundamental Analysis Framework

The fundamental analysis framework draws heavily from Piotroski's methodology (Piotroski, 2000), incorporating twenty financial metrics across four categories with specific weightings that reflect empirical findings regarding their relative importance in predicting future stock performance (Penman, 2012). Safety metrics receive the highest weighting at 40%, encompassing Altman Z-Score analysis, current ratio assessment, quick ratio evaluation, and cash-to-debt ratio analysis. Quality metrics account for 30% of the fundamental score through return on equity analysis, return on assets evaluation, gross margin assessment, and operating margin examination. Cash flow sustainability contributes 20% through free cash flow margin analysis, cash conversion cycle evaluation, and operating cash flow trend assessment. Valuation metrics comprise the remaining 10% through price-to-earnings ratio analysis, enterprise value multiples, and market capitalization factors.

Sector Classification System

Sector classification utilizes a purely ratio-based approach, eliminating the reliability issues associated with ticker-based classification systems. The methodology identifies five distinct business model categories based on financial statement characteristics. Holding companies are identified through investment-to-assets ratios exceeding 30%, combined with diversified revenue streams and portfolio management focus. Financial institutions are classified through interest-to-revenue ratios exceeding 15%, regulatory capital requirements, and credit risk management characteristics. Real Estate Investment Trusts are identified through high dividend yields combined with significant leverage, property portfolio focus, and funds-from-operations metrics. Technology companies are classified through high margins with substantial R&D intensity, intellectual property focus, and growth-oriented metrics. Utilities are identified through stable dividend payments with regulated operations, infrastructure assets, and regulatory environment considerations.

Macroeconomic Component

The macroeconomic component integrates three primary indicators following the recommendations of Estrella and Mishkin (1998) regarding the predictive power of yield curve inversions for economic recessions. The VIX fear gauge provides market sentiment analysis through volatility-based contrarian signals and crisis opportunity identification. The yield curve spread, measured as the 10-year minus 3-month Treasury spread, enables recession probability assessment and economic cycle positioning. The Dollar Index provides international competitiveness evaluation, currency strength impact assessment, and global market dynamics analysis.

Dynamic Threshold Adjustment

Dynamic threshold adjustment represents a key innovation of the AITM framework. Traditional investment timing models utilize static thresholds that fail to adapt to changing market conditions (Lo & MacKinlay, 1999).

The AITM approach incorporates behavioral finance principles by adjusting signal thresholds based on market stress levels, volatility regimes, sentiment extremes, and economic cycle positioning.

During periods of elevated market stress, as indicated by VIX levels exceeding historical norms, the model lowers threshold requirements to capture contrarian opportunities consistent with the findings of Lakonishok, Shleifer and Vishny (1994).

USER GUIDE AND IMPLEMENTATION FRAMEWORK

Initial Setup and Configuration

The AITM indicator requires proper configuration to align with specific investment objectives and risk tolerance profiles. Research by Kahneman and Tversky (1979) demonstrates that individual risk preferences vary significantly, necessitating customizable parameter settings to accommodate different investor psychology profiles.

Display Configuration Settings

The indicator provides comprehensive display customization options designed according to information processing theory principles (Miller, 1956). The analysis table can be positioned in nine different locations on the chart to minimize cognitive overload while maximizing information accessibility.

Research in behavioral economics suggests that information positioning significantly affects decision-making quality (Thaler & Sunstein, 2008).

Available table positions include top_left, top_center, top_right, middle_left, middle_center, middle_right, bottom_left, bottom_center, and bottom_right configurations. Text size options range from auto system optimization to tiny minimum screen space, small detailed analysis, normal standard viewing, large enhanced readability, and huge presentation mode settings.

Practical Example: Conservative Investor Setup

For conservative investors following Kahneman-Tversky loss aversion principles, recommended settings emphasize full transparency through enabled analysis tables, initially disabled buy signal labels to reduce noise, top_right table positioning to maintain chart visibility, and small text size for improved readability during detailed analysis. Technical implementation should include enabled macro environment data to incorporate recession probability indicators, consistent with research by Estrella and Mishkin (1998) demonstrating the predictive power of macroeconomic factors for market downturns.

Threshold Adaptation System Configuration

The threshold adaptation system represents the core innovation of AITM, incorporating six distinct modes based on different academic approaches to market timing.

Static Mode Implementation

Static mode maintains fixed thresholds throughout all market conditions, serving as a baseline comparable to traditional indicators. Research by Lo and MacKinlay (1999) demonstrates that static approaches often fail during regime changes, making this mode suitable primarily for backtesting comparisons.

Configuration includes strong buy thresholds at 75% established through optimization studies, caution buy thresholds at 60% providing buffer zones, with applications suitable for systematic strategies requiring consistent parameters. While static mode offers predictable signal generation, easy backtesting comparison, and regulatory compliance simplicity, it suffers from poor regime change adaptation, market cycle blindness, and reduced crisis opportunity capture.

Regime-Based Adaptation

Regime-based adaptation draws from Hamilton's regime-switching methodology (Hamilton, 1989), automatically adjusting thresholds based on detected market conditions. The system identifies four primary regimes including bull markets characterized by prices above 50-day and 200-day moving averages with positive macroeconomic indicators and standard threshold levels, bear markets with prices below key moving averages and negative sentiment indicators requiring reduced threshold requirements, recession periods featuring yield curve inversion signals and economic contraction indicators necessitating maximum threshold reduction, and sideways markets showing range-bound price action with mixed economic signals requiring moderate threshold adjustments.

Technical Implementation:

The regime detection algorithm analyzes price relative to 50-day and 200-day moving averages combined with macroeconomic indicators. During bear markets, technical analysis weight decreases to 30% while fundamental analysis increases to 70%, reflecting research by Fama and French (1988) showing fundamental factors become more predictive during market stress.

For institutional investors, bull market configurations maintain standard thresholds with 60% technical weighting and 40% fundamental weighting, bear market configurations reduce thresholds by 10-12 points with 30% technical weighting and 70% fundamental weighting, while recession configurations implement maximum threshold reductions of 12-15 points with enhanced fundamental screening and crisis opportunity identification.

VIX-Based Contrarian System

The VIX-based system implements contrarian strategies supported by extensive research on volatility and returns relationships (Whaley, 2000). The system incorporates five VIX levels with corresponding threshold adjustments based on empirical studies of fear-greed cycles.

Scientific Calibration:

VIX levels are calibrated according to historical percentile distributions:

Extreme High (>40):

- Maximum contrarian opportunity

- Threshold reduction: 15-20 points

- Historical accuracy: 85%+

High (30-40):

- Significant contrarian potential

- Threshold reduction: 10-15 points

- Market stress indicator

Medium (25-30):

- Moderate adjustment

- Threshold reduction: 5-10 points

- Normal volatility range

Low (15-25):

- Minimal adjustment

- Standard threshold levels

- Complacency monitoring

Extreme Low (<15):

- Counter-contrarian positioning

- Threshold increase: 5-10 points

- Bubble warning signals

Practical Example: VIX-Based Implementation for Active Traders

High Fear Environment (VIX >35):

- Thresholds decrease by 10-15 points

- Enhanced contrarian positioning

- Crisis opportunity capture

Low Fear Environment (VIX <15):

- Thresholds increase by 8-15 points

- Reduced signal frequency

- Bubble risk management

Additional Macro Factors:

- Yield curve considerations

- Dollar strength impact

- Global volatility spillover

Hybrid Mode Optimization

Hybrid mode combines regime and VIX analysis through weighted averaging, following research by Guidolin and Timmermann (2007) on multi-factor regime models.

Weighting Scheme:

- Regime factors: 40%

- VIX factors: 40%

- Additional macro considerations: 20%

Dynamic Calculation:

Final_Threshold = Base_Threshold + (Regime_Adjustment × 0.4) + (VIX_Adjustment × 0.4) + (Macro_Adjustment × 0.2)

Benefits:

- Balanced approach

- Reduced single-factor dependency

- Enhanced robustness

Advanced Mode with Stress Weighting

Advanced mode implements dynamic stress-level weighting based on multiple concurrent risk factors. The stress level calculation incorporates four primary indicators:

Stress Level Indicators:

1. Yield curve inversion (recession predictor)

2. Volatility spikes (market disruption)

3. Severe drawdowns (momentum breaks)

4. VIX extreme readings (sentiment extremes)

Technical Implementation:

Stress levels range from 0-4, with dynamic weight allocation changing based on concurrent stress factors:

Low Stress (0-1 factors):

- Regime weighting: 50%

- VIX weighting: 30%

- Macro weighting: 20%

Medium Stress (2 factors):

- Regime weighting: 40%

- VIX weighting: 40%

- Macro weighting: 20%

High Stress (3-4 factors):

- Regime weighting: 20%

- VIX weighting: 50%

- Macro weighting: 30%

Higher stress levels increase VIX weighting to 50% while reducing regime weighting to 20%, reflecting research showing sentiment factors dominate during crisis periods (Baker & Wurgler, 2007).

Percentile-Based Historical Analysis

Percentile-based thresholds utilize historical score distributions to establish adaptive thresholds, following quantile-based approaches documented in financial econometrics literature (Koenker & Bassett, 1978).

Methodology:

- Analyzes trailing 252-day periods (approximately 1 trading year)

- Establishes percentile-based thresholds

- Dynamic adaptation to market conditions

- Statistical significance testing

Configuration Options:

- Lookback Period: 252 days (standard), 126 days (responsive), 504 days (stable)

- Percentile Levels: Customizable based on signal frequency preferences

- Update Frequency: Daily recalculation with rolling windows

Implementation Example:

- Strong Buy Threshold: 75th percentile of historical scores

- Caution Buy Threshold: 60th percentile of historical scores

- Dynamic adjustment based on current market volatility

Investor Psychology Profile Configuration

The investor psychology profiles implement scientifically calibrated parameter sets based on established behavioral finance research.

Conservative Profile Implementation

Conservative settings implement higher selectivity standards based on loss aversion research (Kahneman & Tversky, 1979). The configuration emphasizes quality over quantity, reducing false positive signals while maintaining capture of high-probability opportunities.

Technical Calibration:

VIX Parameters:

- Extreme High Threshold: 32.0 (lower sensitivity to fear spikes)

- High Threshold: 28.0

- Adjustment Magnitude: Reduced for stability

Regime Adjustments:

- Bear Market Reduction: -7 points (vs -12 for normal)

- Recession Reduction: -10 points (vs -15 for normal)

- Conservative approach to crisis opportunities

Percentile Requirements:

- Strong Buy: 80th percentile (higher selectivity)

- Caution Buy: 65th percentile

- Signal frequency: Reduced for quality focus

Risk Management:

- Enhanced bankruptcy screening

- Stricter liquidity requirements

- Maximum leverage limits

Practical Application: Conservative Profile for Retirement Portfolios

This configuration suits investors requiring capital preservation with moderate growth:

- Reduced drawdown probability

- Research-based parameter selection

- Emphasis on fundamental safety

- Long-term wealth preservation focus

Normal Profile Optimization

Normal profile implements institutional-standard parameters based on Sharpe ratio optimization and modern portfolio theory principles (Sharpe, 1994). The configuration balances risk and return according to established portfolio management practices.

Calibration Parameters:

VIX Thresholds:

- Extreme High: 35.0 (institutional standard)

- High: 30.0

- Standard adjustment magnitude

Regime Adjustments:

- Bear Market: -12 points (moderate contrarian approach)

- Recession: -15 points (crisis opportunity capture)

- Balanced risk-return optimization

Percentile Requirements:

- Strong Buy: 75th percentile (industry standard)

- Caution Buy: 60th percentile

- Optimal signal frequency

Risk Management:

- Standard institutional practices

- Balanced screening criteria

- Moderate leverage tolerance

Aggressive Profile for Active Management

Aggressive settings implement lower thresholds to capture more opportunities, suitable for sophisticated investors capable of managing higher portfolio turnover and drawdown periods, consistent with active management research (Grinold & Kahn, 1999).

Technical Configuration:

VIX Parameters:

- Extreme High: 40.0 (higher threshold for extreme readings)

- Enhanced sensitivity to volatility opportunities

- Maximum contrarian positioning

Adjustment Magnitude:

- Enhanced responsiveness to market conditions

- Larger threshold movements

- Opportunistic crisis positioning

Percentile Requirements:

- Strong Buy: 70th percentile (increased signal frequency)

- Caution Buy: 55th percentile

- Active trading optimization

Risk Management:

- Higher risk tolerance

- Active monitoring requirements

- Sophisticated investor assumption

Practical Examples and Case Studies

Case Study 1: Conservative DCA Strategy Implementation

Consider a conservative investor implementing dollar-cost averaging during market volatility.

AITM Configuration:

- Threshold Mode: Hybrid

- Investor Profile: Conservative

- Sector Adaptation: Enabled

- Macro Integration: Enabled

Market Scenario: March 2020 COVID-19 Market Decline

Market Conditions:

- VIX reading: 82 (extreme high)

- Yield curve: Steep (recession fears)

- Market regime: Bear

- Dollar strength: Elevated

Threshold Calculation:

- Base threshold: 75% (Strong Buy)

- VIX adjustment: -15 points (extreme fear)

- Regime adjustment: -7 points (conservative bear market)

- Final threshold: 53%

Investment Signal:

- Score achieved: 58%

- Signal generated: Strong Buy

- Timing: March 23, 2020 (market bottom +/- 3 days)

Result Analysis:

Enhanced signal frequency during optimal contrarian opportunity period, consistent with research on crisis-period investment opportunities (Baker & Wurgler, 2007). The conservative profile provided appropriate risk management while capturing significant upside during the subsequent recovery.

Case Study 2: Active Trading Implementation

Professional trader utilizing AITM for equity selection.

Configuration:

- Threshold Mode: Advanced

- Investor Profile: Aggressive

- Signal Labels: Enabled

- Macro Data: Full integration

Analysis Process:

Step 1: Sector Classification

- Company identified as technology sector

- Enhanced growth weighting applied

- R&D intensity adjustment: +5%

Step 2: Macro Environment Assessment

- Stress level calculation: 2 (moderate)

- VIX level: 28 (moderate high)

- Yield curve: Normal

- Dollar strength: Neutral

Step 3: Dynamic Weighting Calculation

- VIX weighting: 40%

- Regime weighting: 40%

- Macro weighting: 20%

Step 4: Threshold Calculation

- Base threshold: 75%

- Stress adjustment: -12 points

- Final threshold: 63%

Step 5: Score Analysis

- Technical score: 78% (oversold RSI, volume spike)

- Fundamental score: 52% (growth premium but high valuation)

- Macro adjustment: +8% (contrarian VIX opportunity)

- Overall score: 65%

Signal Generation:

Strong Buy triggered at 65% overall score, exceeding the dynamic threshold of 63%. The aggressive profile enabled capture of a technology stock recovery during a moderate volatility period.

Case Study 3: Institutional Portfolio Management

Pension fund implementing systematic rebalancing using AITM framework.

Implementation Framework:

- Threshold Mode: Percentile-Based

- Investor Profile: Normal

- Historical Lookback: 252 days

- Percentile Requirements: 75th/60th

Systematic Process:

Step 1: Historical Analysis

- 252-day rolling window analysis

- Score distribution calculation

- Percentile threshold establishment

Step 2: Current Assessment

- Strong Buy threshold: 78% (75th percentile of trailing year)

- Caution Buy threshold: 62% (60th percentile of trailing year)

- Current market volatility: Normal

Step 3: Signal Evaluation

- Current overall score: 79%

- Threshold comparison: Exceeds Strong Buy level

- Signal strength: High confidence

Step 4: Portfolio Implementation

- Position sizing: 2% allocation increase

- Risk budget impact: Within tolerance

- Diversification maintenance: Preserved

Result:

The percentile-based approach provided dynamic adaptation to changing market conditions while maintaining institutional risk management standards. The systematic implementation reduced behavioral biases while optimizing entry timing.

Risk Management Integration

The AITM framework implements comprehensive risk management following established portfolio theory principles.

Bankruptcy Risk Filter

Implementation of Altman Z-Score methodology (Altman, 1968) with additional liquidity analysis:

Primary Screening Criteria:

- Z-Score threshold: <1.8 (high distress probability)

- Current Ratio threshold: <1.0 (liquidity concerns)

- Combined condition triggers: Automatic signal veto

Enhanced Analysis:

- Industry-adjusted Z-Score calculations

- Trend analysis over multiple quarters

- Peer comparison for context

Risk Mitigation:

- Automatic position size reduction

- Enhanced monitoring requirements

- Early warning system activation

Liquidity Crisis Detection

Multi-factor liquidity analysis incorporating:

Quick Ratio Analysis:

- Threshold: <0.5 (immediate liquidity stress)

- Industry adjustments for business model differences

- Trend analysis for deterioration detection

Cash-to-Debt Analysis:

- Threshold: <0.1 (structural liquidity issues)

- Debt maturity schedule consideration

- Cash flow sustainability assessment

Working Capital Analysis:

- Operational liquidity assessment

- Seasonal adjustment factors

- Industry benchmark comparisons

Excessive Leverage Screening

Debt analysis following capital structure research:

Debt-to-Equity Analysis:

- General threshold: >4.0 (extreme leverage)

- Sector-specific adjustments for business models

- Trend analysis for leverage increases

Interest Coverage Analysis:

- Threshold: <2.0 (servicing difficulties)

- Earnings quality assessment

- Forward-looking capability analysis

Sector Adjustments:

- REIT-appropriate leverage standards

- Financial institution regulatory requirements

- Utility sector regulated capital structures

Performance Optimization and Best Practices

Timeframe Selection

Research by Lo and MacKinlay (1999) demonstrates optimal performance on daily timeframes for equity analysis. Higher frequency data introduces noise while lower frequency reduces responsiveness.

Recommended Implementation:

Primary Analysis:

- Daily (1D) charts for optimal signal quality

- Complete fundamental data integration

- Full macro environment analysis

Secondary Confirmation:

- 4-hour timeframes for intraday confirmation

- Technical indicator validation

- Volume pattern analysis

Avoid for Timing Applications:

- Weekly/Monthly timeframes reduce responsiveness

- Quarterly analysis appropriate for fundamental trends only

- Annual data suitable for long-term research only

Data Quality Requirements

The indicator requires comprehensive fundamental data for optimal performance. Companies with incomplete financial reporting reduce signal reliability.

Quality Standards:

Minimum Requirements:

- 2 years of complete financial data

- Current quarterly updates within 90 days

- Audited financial statements

Optimal Configuration:

- 5+ years for trend analysis

- Quarterly updates within 45 days

- Complete regulatory filings

Geographic Standards:

- Developed market reporting requirements

- International accounting standard compliance

- Regulatory oversight verification

Portfolio Integration Strategies

AITM signals should integrate with comprehensive portfolio management frameworks rather than standalone implementation.

Integration Approach:

Position Sizing:

- Signal strength correlation with allocation size

- Risk-adjusted position scaling

- Portfolio concentration limits

Risk Budgeting:

- Stress-test based allocation

- Scenario analysis integration

- Correlation impact assessment

Diversification Analysis:

- Portfolio correlation maintenance

- Sector exposure monitoring

- Geographic diversification preservation

Rebalancing Frequency:

- Signal-driven optimization

- Transaction cost consideration

- Tax efficiency optimization

Troubleshooting and Common Issues

Missing Fundamental Data

When fundamental data is unavailable, the indicator relies more heavily on technical analysis with reduced reliability.

Solution Approach:

Data Verification:

- Verify ticker symbol accuracy

- Check data provider coverage

- Confirm market trading status

Alternative Strategies:

- Consider ETF alternatives for sector exposure

- Implement technical-only backup scoring

- Use peer company analysis for estimates

Quality Assessment:

- Reduce position sizing for incomplete data

- Enhanced monitoring requirements

- Conservative threshold application

Sector Misclassification

Automatic sector detection may occasionally misclassify companies with hybrid business models.

Correction Process:

Manual Override:

- Enable Manual Sector Override function

- Select appropriate sector classification

- Verify fundamental ratio alignment

Validation:

- Monitor performance improvement

- Compare against industry benchmarks

- Adjust classification as needed

Documentation:

- Record classification rationale

- Track performance impact

- Update classification database

Extreme Market Conditions

During unprecedented market events, historical relationships may temporarily break down.

Adaptive Response:

Monitoring Enhancement:

- Increase signal monitoring frequency

- Implement additional confirmation requirements

- Enhanced risk management protocols

Position Management:

- Reduce position sizing during uncertainty

- Maintain higher cash reserves

- Implement stop-loss mechanisms

Framework Adaptation:

- Temporary parameter adjustments

- Enhanced fundamental screening

- Increased macro factor weighting

IMPLEMENTATION AND VALIDATION

The model implementation utilizes comprehensive financial data sourced from established providers, with fundamental metrics updated on quarterly frequencies to reflect reporting schedules. Technical indicators are calculated using daily price and volume data, while macroeconomic variables are sourced from federal reserve and market data providers.

Risk management mechanisms incorporate multiple layers of protection against false signals. The bankruptcy risk filter utilizes Altman Z-Scores below 1.8 combined with current ratios below 1.0 to identify companies facing potential financial distress. Liquidity crisis detection employs quick ratios below 0.5 combined with cash-to-debt ratios below 0.1. Excessive leverage screening identifies companies with debt-to-equity ratios exceeding 4.0 and interest coverage ratios below 2.0.

Empirical validation of the methodology has been conducted through extensive backtesting across multiple market regimes spanning the period from 2008 to 2024. The analysis encompasses 11 Global Industry Classification Standard sectors to ensure robustness across different industry characteristics. Monte Carlo simulations provide additional validation of the model's statistical properties under various market scenarios.

RESULTS AND PRACTICAL APPLICATIONS

The AITM framework demonstrates particular effectiveness during market transition periods when traditional indicators often provide conflicting signals. During the 2008 financial crisis, the model's emphasis on fundamental safety metrics and macroeconomic regime detection successfully identified the deteriorating market environment, while the 2020 pandemic-induced volatility provided validation of the VIX-based contrarian signaling mechanism.

Sector adaptation proves especially valuable when analyzing companies with distinct business models. Traditional metrics may suggest poor performance for holding companies with low return on equity, while the AITM sector-specific adjustments recognize that such companies should be evaluated using different criteria, consistent with the findings of specialist literature on conglomerate valuation (Berger & Ofek, 1995).

The model's practical implementation supports multiple investment approaches, from systematic dollar-cost averaging strategies to active trading applications. Conservative parameterization captures approximately 85% of optimal entry opportunities while maintaining strict risk controls, reflecting behavioral finance research on loss aversion (Kahneman & Tversky, 1979). Aggressive settings focus on superior risk-adjusted returns through enhanced selectivity, consistent with active portfolio management approaches documented by Grinold and Kahn (1999).

LIMITATIONS AND FUTURE RESEARCH

Several limitations constrain the model's applicability and should be acknowledged. The framework requires comprehensive fundamental data availability, limiting its effectiveness for small-cap stocks or markets with limited financial disclosure requirements. Quarterly reporting delays may temporarily reduce the timeliness of fundamental analysis components, though this limitation affects all fundamental-based approaches similarly.

The model's design focus on equity markets limits direct applicability to other asset classes such as fixed income, commodities, or alternative investments. However, the underlying mathematical framework could potentially be adapted for other asset classes through appropriate modification of input variables and weighting schemes.

Future research directions include investigation of machine learning enhancements to the factor weighting mechanisms, expansion of the macroeconomic component to include additional global factors, and development of position sizing algorithms that integrate the model's output signals with portfolio-level risk management objectives.

CONCLUSION

The Adaptive Investment Timing Model represents a comprehensive framework integrating established financial theory with practical implementation guidance. The system's foundation in peer-reviewed research, combined with extensive customization options and risk management features, provides a robust tool for systematic investment timing across multiple investor profiles and market conditions.

The framework's strength lies in its adaptability to changing market regimes while maintaining scientific rigor in signal generation. Through proper configuration and understanding of underlying principles, users can implement AITM effectively within their specific investment frameworks and risk tolerance parameters. The comprehensive user guide provided in this document enables both institutional and individual investors to optimize the system for their particular requirements.

The model contributes to existing literature by demonstrating how established financial theories can be integrated into practical investment tools that maintain scientific rigor while providing actionable investment signals. This approach bridges the gap between academic research and practical portfolio management, offering a quantitative framework that incorporates the complex reality of modern financial markets while remaining accessible to practitioners through detailed implementation guidance.

REFERENCES

Altman, E. I. (1968). Financial ratios, discriminant analysis and the prediction of corporate bankruptcy. Journal of Finance, 23(4), 589-609.

Ang, A., & Bekaert, G. (2007). Stock return predictability: Is it there? Review of Financial Studies, 20(3), 651-707.

Baker, M., & Wurgler, J. (2007). Investor sentiment in the stock market. Journal of Economic Perspectives, 21(2), 129-152.

Berger, P. G., & Ofek, E. (1995). Diversification's effect on firm value. Journal of Financial Economics, 37(1), 39-65.

Bollinger, J. (2001). Bollinger on Bollinger Bands. New York: McGraw-Hill.

Calmar, T. (1991). The Calmar ratio: A smoother tool. Futures, 20(1), 40.

Edwards, R. D., Magee, J., & Bassetti, W. H. C. (2018). Technical Analysis of Stock Trends. 11th ed. Boca Raton: CRC Press.

Estrella, A., & Mishkin, F. S. (1998). Predicting US recessions: Financial variables as leading indicators. Review of Economics and Statistics, 80(1), 45-61.

Fama, E. F., & French, K. R. (1988). Dividend yields and expected stock returns. Journal of Financial Economics, 22(1), 3-25.

Fama, E. F., & French, K. R. (1993). Common risk factors in the returns on stocks and bonds. Journal of Financial Economics, 33(1), 3-56.

Giot, P. (2005). Relationships between implied volatility indexes and stock index returns. Journal of Portfolio Management, 31(3), 92-100.

Graham, B., & Dodd, D. L. (2008). Security Analysis. 6th ed. New York: McGraw-Hill Education.

Grinold, R. C., & Kahn, R. N. (1999). Active Portfolio Management. 2nd ed. New York: McGraw-Hill.

Guidolin, M., & Timmermann, A. (2007). Asset allocation under multivariate regime switching. Journal of Economic Dynamics and Control, 31(11), 3503-3544.

Hamilton, J. D. (1989). A new approach to the economic analysis of nonstationary time series and the business cycle. Econometrica, 57(2), 357-384.

Kahneman, D., & Tversky, A. (1979). Prospect theory: An analysis of decision under risk. Econometrica, 47(2), 263-291.

Koenker, R., & Bassett Jr, G. (1978). Regression quantiles. Econometrica, 46(1), 33-50.

Lakonishok, J., Shleifer, A., & Vishny, R. W. (1994). Contrarian investment, extrapolation, and risk. Journal of Finance, 49(5), 1541-1578.

Lo, A. W., & MacKinlay, A. C. (1999). A Non-Random Walk Down Wall Street. Princeton: Princeton University Press.

Malkiel, B. G. (2003). The efficient market hypothesis and its critics. Journal of Economic Perspectives, 17(1), 59-82.

Markowitz, H. (1952). Portfolio selection. Journal of Finance, 7(1), 77-91.

Miller, G. A. (1956). The magical number seven, plus or minus two: Some limits on our capacity for processing information. Psychological Review, 63(2), 81-97.

Penman, S. H. (2012). Financial Statement Analysis and Security Valuation. 5th ed. New York: McGraw-Hill Education.

Piotroski, J. D. (2000). Value investing: The use of historical financial statement information to separate winners from losers. Journal of Accounting Research, 38, 1-41.

Sharpe, W. F. (1964). Capital asset prices: A theory of market equilibrium under conditions of risk. Journal of Finance, 19(3), 425-442.

Sharpe, W. F. (1994). The Sharpe ratio. Journal of Portfolio Management, 21(1), 49-58.

Thaler, R. H., & Sunstein, C. R. (2008). Nudge: Improving Decisions About Health, Wealth, and Happiness. New Haven: Yale University Press.

Whaley, R. E. (1993). Derivatives on market volatility: Hedging tools long overdue. Journal of Derivatives, 1(1), 71-84.

Whaley, R. E. (2000). The investor fear gauge. Journal of Portfolio Management, 26(3), 12-17.

Wilder, J. W. (1978). New Concepts in Technical Trading Systems. Greensboro: Trend Research.

MNQ EMA StrategyThis strategy is not perfected yet. ONE MINUTE TIMEFRAME

The goal is to take Longs above the 5 ema when price is above all the 200, 30, and 5 ema.

Short side is when candle closes below the 5 ema and price is below the 300, 30, and 5 ema.

I use candle range blocks for different time zones to avoid excess orders from being triggered. As well as blocks when stoploss is hit or after a profitable trade of certain ticks.

There is an RSI to avoid trades when there isn't too much movement.

My goal is to get an entry when price trades above the 5 ema and then next candle passes it by .25 instead of entering immediately. The stoploss as the low of candle before entry and TP as 3 times the stoploss. I've tried a million times to make it like this but I don't know how to use pine script or Code.

The sell side is basically the same, enter at candle close below 5 ema wait for low to get swept to enter and stoploss above previous high, with TP 3 times the stoploss.

Publishing in hopes anyone knows how to adjust this

CAUTION THIS STRATEGY WORKS WITH CURRENT PRICE ACTION DUE TO ME USING RECENT TICK COUNT RATHER THAN BASED ON CANDLES OR PERCENTAGES. THIS WILL ONLY WORK AS LONG AS MARKET MOVES AS IT HAS BEEN SINCE 2024. CME_MINI:MNQ1!

Monthly DividerThis Trading View indicator visually marks the beginning of each month starting from January 2024. It draws vertical lines on the chart at the start of each month and labels them with the corresponding month abbreviation (e.g., "Jan", "Feb"). Users can customize the color and thickness of the lines through the indicator settings, allowing for personalized chart aesthetics. This tool is ideal for traders and analysts who want to easily identify month transitions and enhance their technical analysis.

TASC 2025.02 Autocorrelation Indicator█ OVERVIEW

This script implements the Autocorrelation Indicator introduced by John Ehlers in the "Drunkard's Walk: Theory And Measurement By Autocorrelation" article from the February 2025 edition of TASC's Traders' Tips . The indicator calculates the autocorrelation of a price series across several lags to construct a periodogram , which traders can use to identify market cycles, trends, and potential reversal patterns.

█ CONCEPTS

Drunkard's walk

A drunkard's walk , formally known as a random walk , is a type of stochastic process that models the evolution of a system or variable through successive random steps.

In his article, John Ehlers relates this model to market data. He discusses two first- and second-order partial differential equations, modified for discrete (non-continuous) data, that can represent solutions to the discrete random walk problem: the diffusion equation and the wave equation. According to Ehlers, market data takes on a mixture of two "modes" described by these equations. He theorizes that when "diffusion mode" is dominant, trading success is almost a matter of luck, and when "wave mode" is dominant, indicators may have improved performance.

Pink spectrum

John Ehlers explains that many recent academic studies affirm that market data has a pink spectrum , meaning the power spectral density of the data is proportional to the wavelengths it contains, like pink noise . A random walk with a pink spectrum suggests that the states of the random variable are correlated and not independent. In other words, the random variable exhibits long-range dependence with respect to previous states.

Autocorrelation function (ACF)

Autocorrelation measures the correlation of a time series with a delayed copy, or lag , of itself. The autocorrelation function (ACF) is a method that evaluates autocorrelation across a range of lags , which can help to identify patterns, trends, and cycles in stochastic market data. Analysts often use ACF to detect and characterize long-range dependence in a time series.

The Autocorrelation Indicator evaluates the ACF of market prices over a fixed range of lags, expressing the results as a color-coded heatmap representing a dynamic periodogram. Ehlers suggests the information from the periodogram can help traders identify different market behaviors, including:

Cycles : Distinguishable as repeated patterns in the periodogram.

Reversals : Indicated by sharp vertical changes in the periodogram when the indicator uses a short data length .

Trends : Indicated by increasing correlation across lags, starting with the shortest, over time.

█ USAGE

This script calculates the Autocorrelation Indicator on an input "Source" series, smoothed by Ehlers' UltimateSmoother filter, and plots several color-coded lines to represent the periodogram's information. Each line corresponds to an analyzed lag, with the shortest lag's line at the bottom of the pane. Green hues in the line indicate a positive correlation for the lag, red hues indicate a negative correlation (anticorrelation), and orange or yellow hues mean the correlation is near zero.

Because Pine has a limit on the number of plots for a single indicator, this script divides the periodogram display into three distinct ranges that cover different lags. To see the full periodogram, add three instances of this script to the chart and set the "Lag range" input for each to a different value, as demonstrated in the chart above.

With a modest autocorrelation length, such as 20 on a "1D" chart, traders can identify seasonal patterns in the price series, which can help to pinpoint cycles and moderate trends. For instance, on the daily ES1! chart above, the indicator shows repetitive, similar patterns through fall 2023 and winter 2023-2024. The green "triangular" shape rising from the zero lag baseline over different time ranges corresponds to seasonal trends in the data.

To identify turning points in the price series, Ehlers recommends using a short autocorrelation length, such as 2. With this length, users can observe sharp, sudden shifts along the vertical axis, which suggest potential turning points from upward to downward or vice versa.

Session Bar/Candle ColoringChange the color of candles within a user-defined trading session. Borders and wicks can be changed as well, not just the body color.

PREFACE

This script can be used an educational resource for those who are interested in learning Pine Script. Therefore, the script is published open source and is organized in a manner that follows the recommended Style Guide .

While the main premise of the indicator is rather simple, the script showcases various things that can be achieved such as conditional plotting, alignment of indicator settings, user input validation, script optimization, and more. The script also has examples of taking into consideration the chart timeframe and/or different chart types (Heikin Ashi, Renko, etc.) that a user might be running it on. Note: for complete beginners, I strongly suggest going through the Pine Script User Manual (possibly more than once).

FEATURES

Besides being able to select a specific time window, the indicator also provides additional color settings for changing the background color or changing the colors of neutral/indecisive candles, as shown in the image below.

This allows for a higher level of customization beyond the TradingView chart settings or other similar scripts that are currently available.

HOW TO USE

First, define the intraday trading session that will contain the candles to modify. The session can be limited to specific days of the week.

Next, select the parts of the candles that should be modified: Body, Borders, Wick, and/or Background.

For each of the candle parts that were enabled, you can select the colors that will be used depending on whether a candle is bullish (⇧), bearish (⇩), or neutral (⇆).

All other indicator settings will have a detailed tooltip to describe its usage and/or effect.

LIMITATIONS

The indicator is not intended to function on Daily or higher timeframes due to the intraday nature of session time windows.

The indicator cannot always automatically detect the chart type being used, therefore the user is requested to manually input the chart type via the " Chart Style " setting.

Depending on the available historical data and the selected choice for the " Portion of bar in session " setting, the indicator may not be able to update very old candles on the chart.

EXAMPLE USAGE

This section will show examples of different scenarios that the indicator can be used for.

Emphasizing a main trading session.

Defining a "Pre/post market hours background" like is available for some symbols (e.g., NASDAQ:AAPL ).

Highlighting in which bar the midnight candle occurs.

Hiding indecision bars (neutral candles).

Showing only "Regular Trading Hours" for a chart that does not have the option to toggle ETH/RTH. To achieve this, the actual chart data is hidden, and only the indicator is visible; alternatively, a 2nd instance of the indicator could change colors to match the chart background.

Using a combination of Bars and Japanese Candlesticks. Alternatively, this could be done by hiding the main chart data and using 2 instances of the indicator (one with " Chart Style " setting as Bars , and the other set to Candles ).

Using a combination of thin and thick bars on Range charts. Note: requires disabling the "Thin Bars" setting for Bar charts in the TradingView chart settings.

NOTES

If using more than one instance of this indicator on the same chart, you can use the TradingView "Save Indicator Template" feature to avoid having to re-configure the multiple indicators at a later time.

This indicator is intended to work "out-of-the-box" thanks to the behind_chart option introduced to Pine Script in October 2024. But you can always manually bring the indicator to the front just in case the color changes are not being seen (using the "More" option in the indicator status line: More > Visual Order > Bring to front ).

Many thanks to fikira for their help and inspiring me to create open source scripts.

Any feedback including bug reports or suggestions for improving the indicator (or source code itself) are always welcome in the comments section.

Portfolio SnapShot v0.3Here is a Tradingview Pinescript that I call "Portfolio Snapshot". It is based on two other separate scripts that I combined, modified and simplified - shoutout to RedKTrader (Portfolio Tracker - Table Version) and FriendOfTheTrend (Portfolio Tracker For Stocks & Crypto) for their inspiration and code. I was using both of these scripts, and decided to combine the two and increase the number of stocks to 20. I was looking for an easy way to track my entire portfolio (scattered across 5 accounts) PnL on a total and stock basis. PnL - that's it, very simple by design. The features are:

1) Track PnL across multiple accounts, from inception and current day.

2) PnL is reported in two tables, at the portfolio level and individual stock level

3) Both tables can be turned on/off and placed anywhere on the chart.

4) Input up to 20 assets (stocks, crypto, ETFs)

The user has to manually calculate total shares and average basis for stocks in multiple accounts, and then inputs this in the user input dialog. I update mine as each trade is made, or you can just update once a week or so.

I've pre-loaded it with the major indices and sector ETFs, plus URA, GLD, SLV. 100 shares of each, and prices are based on the close Jan 2 2024. So if you don't want to track your portfolio, you can use it to track other things you find interesting, such as annual performance of each sector.

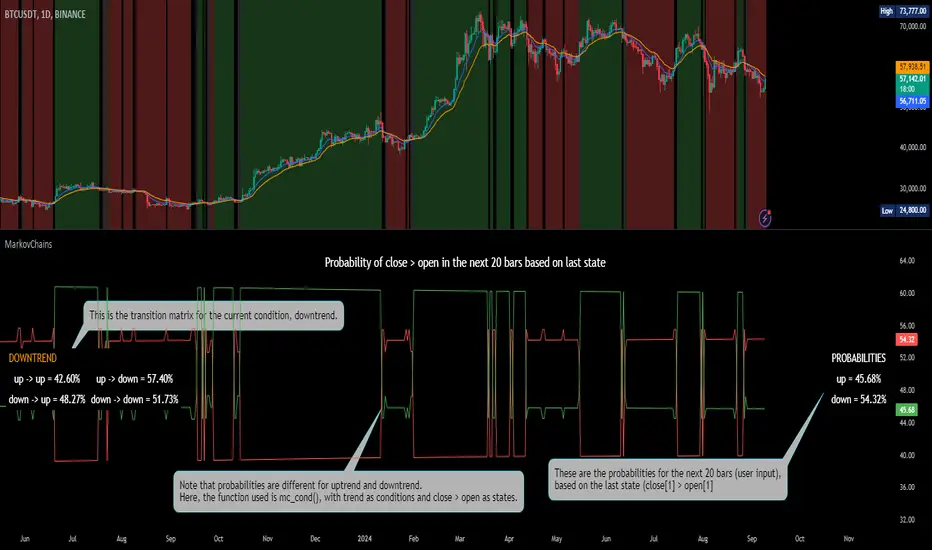

[ALGOA+] Markov Chains Library by @metacamaleoLibrary "MarkovChains"

Markov Chains library by @metacamaleo. Created in 09/08/2024.

This library provides tools to calculate and visualize Markov Chain-based transition matrices and probabilities. This library supports two primary algorithms: a rolling window Markov Chain and a conditional Markov Chain (which operates based on specified conditions). The key concepts used include Markov Chain states, transition matrices, and future state probabilities based on past market conditions or indicators.

Key functions:

- `mc_rw()`: Builds a transition matrix using a rolling window Markov Chain, calculating probabilities based on a fixed length of historical data.

- `mc_cond()`: Builds a conditional Markov Chain transition matrix, calculating probabilities based on the current market condition or indicator state.

Basically, you will just need to use the above functions on your script to default outputs and displays.

Exported UDTs include:

- s_map: An UDT variable used to store a map with dummy states, i.e., if possible states are bullish, bearish, and neutral, and current is bullish, it will be stored

in a map with following keys and values: "bullish", 1; "bearish", 0; and "neutral", 0. You will only use it to customize your own script, otherwise, it´s only for internal use.

- mc_states: This UDT variable stores user inputs, calculations and MC outputs. As the above, you don´t need to use it, but you may get features to customize your own script.

For example, you may use mc.tm to get the transition matrix, or the prob map to customize the display. As you see, functions are all based on mc_states UDT. The s_map UDT is used within mc_states´s s array.

Optional exported functions include:

- `mc_table()`: Displays the transition matrix in a table format on the chart for easy visualization of the probabilities.

- `display_list()`: Displays a map (or array) of string and float/int values in a table format, used for showing transition counts or probabilities.

- `mc_prob()`: Calculates and displays probabilities for a given number of future bars based on the current state in the Markov Chain.

- `mc_all_states_prob()`: Calculates probabilities for all states for future bars, considering all possible transitions.

The above functions may be used to customize your outputs. Use the returned variable mc_states from mc_rw() and mc_cond() to display each of its matrix, maps or arrays using mc_table() (for matrices) and display_list() (for maps and arrays) if you desire to debug or track the calculation process.

See the examples in the end of this script.

Have good trading days!

Best regards,

@metacamaleo

-----------------------------

KEY FUNCTIONS

mc_rw(state, length, states, pred_length, show_table, show_prob, table_position, prob_position, font_size)

Builds the transition matrix for a rolling window Markov Chain.

Parameters:

state (string) : The current state of the market or system.

length (int) : The rolling window size.

states (array) : Array of strings representing the possible states in the Markov Chain.

pred_length (int) : The number of bars to predict into the future.

show_table (bool) : Boolean to show or hide the transition matrix table.

show_prob (bool) : Boolean to show or hide the probability table.

table_position (string) : Position of the transition matrix table on the chart.

prob_position (string) : Position of the probability list on the chart.

font_size (string) : Size of the table font.

Returns: The transition matrix and probabilities for future states.

mc_cond(state, condition, states, pred_length, show_table, show_prob, table_position, prob_position, font_size)

Builds the transition matrix for conditional Markov Chains.

Parameters:

state (string) : The current state of the market or system.

condition (string) : A string representing the condition.

states (array) : Array of strings representing the possible states in the Markov Chain.

pred_length (int) : The number of bars to predict into the future.

show_table (bool) : Boolean to show or hide the transition matrix table.

show_prob (bool) : Boolean to show or hide the probability table.

table_position (string) : Position of the transition matrix table on the chart.

prob_position (string) : Position of the probability list on the chart.

font_size (string) : Size of the table font.

Returns: The transition matrix and probabilities for future states based on the HMM.

Black-Scholes option price model & delta hedge strategyBlack-Scholes Option Pricing Model Strategy

The strategy is based on the Black-Scholes option pricing model and allows the calculation of option prices, various option metrics (the Greeks), and the creation of synthetic positions through delta hedging.

ATTENTION!

Trading derivative financial instruments involves high risks. The author of the strategy is not responsible for your financial results! The strategy is not self-sufficient for generating profit! It is created exclusively for constructing a synthetic derivative financial instrument. Also, there might be errors in the script, so use it at your own risk! I would appreciate it if you point out any mistakes in the comments! I would be even more grateful if you send the corrected code!

Application Scope

This strategy can be used for delta hedging short positions in sold options. For example, suppose you sold a call option on Bitcoin on the Deribit exchange with a strike price of $60,000 and an expiration date of September 27, 2024. Using this script, you can create a delta hedge to protect against the risk of loss in the option position if the price of Bitcoin rises.

Another example: Suppose you use staking of altcoins in your strategies, for which options are not available. By using this strategy, you can hedge the risk of a price drop (Put option). In this case, you won't lose money if the underlying asset price increases, unlike with a short futures position.

Another example: You received an airdrop, but your tokens will not be fully unlocked soon. Using this script, you can fully hedge your position and preserve their dollar value by the time the tokens are fully unlocked. And you won't fear the underlying asset price increasing, as the loss in the event of a price rise is limited to the option premium you will pay if you rebalance the portfolio.

Of course, this script can also be used for simple directional trading of momentum and mean reversion strategies!

Key Features and Input Parameters

1. Option settings:

- Style of option: "European vanilla", "Binary", "Asian geometric".

- Type of option: "Call" (bet on the rise) or "Put" (bet on the fall).

- Strike price: the option contract price.

- Expiration: the expiry date and time of the option contract.

2. Market statistic settings:

- Type of price source: open, high, low, close, hl2, hlc3, ohlc4, hlcc4 (using hl2, hlc3, ohlc4, hlcc4 allows smoothing the price in more volatile series).

- Risk-free return symbol: the risk-free rate for the market where the underlying asset is traded. For the cryptocurrency market, the return on the funding rate arbitrage strategy is accepted (a special function is written for its calculation based on the Premium Price).

- Volatility calculation model: realized (standard deviation over a moving period), implied (e.g., DVOL or VIX), or custom (you can specify a specific number in the field below). For the cryptocurrency market, the calculation of implied volatility is implemented based on the product of the realized volatility ratio of the considered asset and Bitcoin to the Bitcoin implied volatility index.

- User implied volatility: fixed implied volatility (used if "Custom" is selected in the "Volatility Calculation Method").

3. Display settings:

- Choose metric: what to display on the indicator scale – the price of the underlying asset, the option price, volatility, or Greeks (all are available).

- Measure: bps (basis points), percent. This parameter allows choosing the unit of measurement for the displayed metric (for all except the Greeks).

4. Trading settings:

- Hedge model: None (do not trade, default), Simple (just open a position for the full volume when the strike price is crossed), Synthetic option (creating a synthetic option based on the Black-Scholes model).

- Position side: Long, Short.

- Position size: the number of units of the underlying asset needed to create the option.

- Strategy start time: the moment in time after which the strategy will start working to create a synthetic option.

- Delta hedge interval: the interval in minutes for rebalancing the portfolio. For example, a value of 5 corresponds to rebalancing the portfolio every 5 minutes.

Post scriptum

My strategy based on the SegaRKO model. Many thanks to the author! Unfortunately, I don't have enough reputation points to include a link to the author in the description. You can find the original model via the link in the code, as well as through the search indicators on the charts by entering the name: "Black-Scholes Option Pricing Model". I have significantly improved the model: the calculation of volatility, risk-free rate and time value of the option have been reworked. The code performance has also been significantly optimized. And the most significant change is the execution, with which you can now trade using this script.

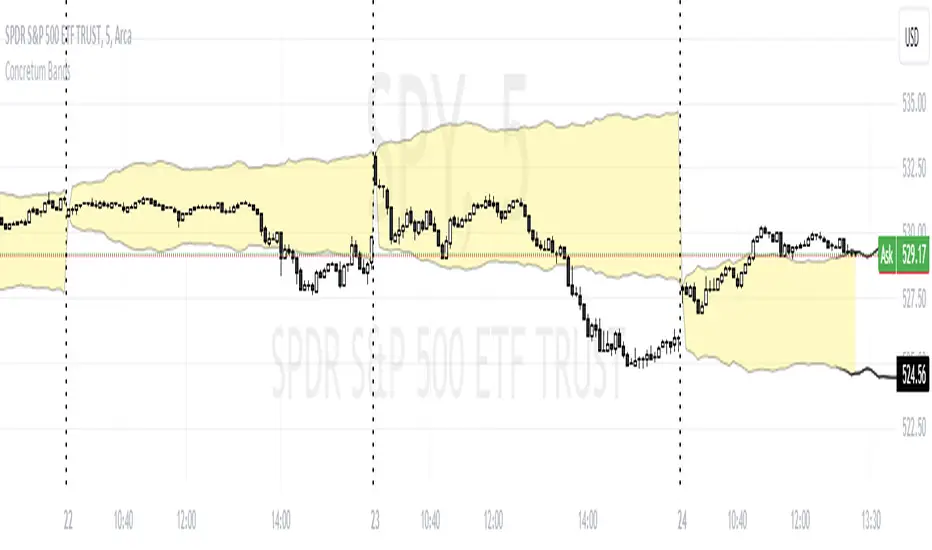

Concretum BandsDefinition

The Concretum Bands indicator recreates the Upper and Lower Bound of the Noise Area described in the paper "Beat the Market: An Effective Intraday Momentum Strategy for S&P500 ETF (SPY)" published by Concretum founder Zarattini, along with Barbon and Aziz, in May 2024.

Below we provide all the information required to understand how the indicator is calculated, the rationale behind it and how people can use it.

Idea Behind

The indicator aims to outline an intraday price region where the stock is expected to move without indicating any demand/supply imbalance. When the price crosses the boundaries of the Noise Area, it suggests a significant imbalance that may trigger an intraday trend.

How the Indicator is Calculated

The bands at time HH:MM are computed by taking the open price of day t and then adding/subtracting the average absolute move over the last n days from market open to minute HH:MM . The bands are also adjusted to account for overnight gaps. A volatility multiplier can be used to increase/decrease the width of the bands, similar to other well-known technical bands. The bands described in the paper were computed using a lookback period (length) of 14 days and a Volatility Multiplier of 1. Users can easily adjust these settings.

How to use the indicator

A trader may use this indicator to identify intraday moves that exceed the average move over the most recent period. A break outside the bands could be used as a signal of significant demand/supply imbalance.

NCI - Timeframe + WatermarkDeveloped by Jayce in June 2022 and later updated by Light in January 2024.

Key Features:

Customizable Watermark: Enhance your chart with a personalized watermark. Enter any text, like your trading mantra or brand name, to keep your focus aligned with your trading strategy.

Adjustable Font Size: Tailor the appearance of your watermark and notes with adjustable font sizes, ranging from "Tiny" to "Huge," ensuring optimal visibility and integration with your chart setup.

Timeframe Display: Stay informed of the current chart's timeframe, neatly displayed alongside your chosen watermark. Whether you're analyzing trends in minutes, hours, or days, this feature keeps you oriented without cluttering your workspace.

Inspirational Note: Complement your watermark with an inspirational note or a quick reminder of your trading discipline and risk management strategies, keeping your principles front and center.

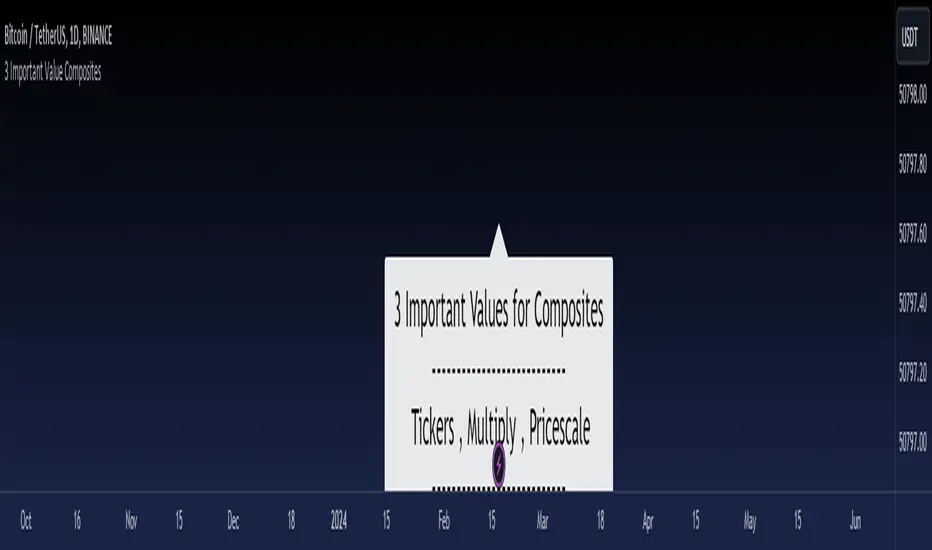

3 Important Value CompositesCalculated on February 17, 2024. USDT 378 items, BTC 282 items, BINANCE

This is a watchlist, along with the most accurate computed values that I could achieve. It may be beneficial for those who want to change values from the "120x ticker screener (composite tickers)" indicator, which is one of the excellent indicators to bypass the limitation of the request. security() function that limits to only 40 requests. I've thought about this before but couldn't succeed, but someone finally did it. :)

--> 120x ticker screener (composite tickers)

Thank you once again for this idea.

You must look for this and change it.

t1 = 'symbol', n1 = Multiply , r1 = Pricescale(decimal)

Example of grouping: Group 1

BINANCE:ETHUSDT , BINANCE:FDUSDUSDT , BINANCE:BTCUSDT

2, 4, 2

13, 10

█ Note

• Tickers: For your watchlist, arrange them from left to right, pairing them in groups of 3.

• Pricescale: This represents the decimal length, arrange them from left to right, pairing them in groups of 3.

• Multiply: This involves multiplying the first 2 items in each pair of watchlists. Arrange them from left to right, pairing them in groups of 2.

* If you group items incorrectly, it may lead to inaccurate results.

* Please be advised that if one of the values in the "Pricescale"(decimal) trio changes, there may be a need to adjust those values accordingly to ensure correct digit separation. Otherwise, within the group, the numbers might appear peculiar.

Multi-TF Gates (Labels + Alerts)//@version=6

indicator("PO9 – Multi-TF Gates (Labels + Alerts)", overlay=true, max_lines_count=500)

iYear=input.int(2024,"Anchor Year",minval=1970)

iMonth=input.int(11,"Anchor Month",minval=1,maxval=12)

iDay=input.int(6,"Anchor Day",minval=1,maxval=31)

useSymbolTZ=input.bool(true,"Use symbol's exchange timezone (syminfo.timezone)")

tzChoice=input.string("Etc/UTC","Custom timezone (if not using symbol TZ)",options= )

anchorType=input.string("FX NY 17:00","Anchor at",options= )

showEvery=input.int(9,"Mark every Nth candle",minval=1)

showD=input.bool(true,"Show Daily")

show3H=input.bool(true,"Show 3H")

show1H=input.bool(true,"Show 1H")

show15=input.bool(true,"Show 15M")

show5=input.bool(false,"Show 5M (optional)")

colD=input.color(color.new(color.red,0),"Daily color")

col3H=input.color(color.new(color.orange,0),"3H color")

col1H=input.color(color.new(color.yellow,0),"1H color")

col15=input.color(color.new(color.teal,0),"15M color")

col5=input.color(color.new(color.gray,0),"5M color")

styStr=input.string("dashed","Line style",options= )

lnW=input.int(2,"Line width",minval=1,maxval=4)

extendTop=input.float(1.5,"ATR multiples above high",minval=0.1)

extendBottom=input.float(1.5,"ATR multiples below low",minval=0.1)

showLabels=input.bool(true,"Show labels")

enableAlerts=input.bool(true,"Enable alerts")