Bank Zones #PipGangHello Traders,

If you trade Forex and Indices this indicator will help you identify Buying and Selling levels that Banks are interested in. These levels are displayed on all time frames. Colors of the lines can be customized.

I also added code to show two EMA's, just uncomment the code to show them. :-)

How to use this indicator.

Show Bank Zones - this will enable/disable horizonal lines on the chart.

Price - enter bank zone price.

Increment By - plots three horizonal lines in pips above and below bank zone price.

Note: Decimal placement is KEY, this may vary by symbol.

Sample Settings:

US30USD

Price 35600.0

IncrementBy 50 (equals 50 pips)

XAUUSD

Price 1850.000

IncrementBy 5 (equals 50 pips)

GBPJPY

Price 152.500

IncrementBy .5 (equals 50 pips)

GBPUSD

Price 1.34100

IncrementBy .005 (equals 50 pips)

חפש סקריפטים עבור "科创50指数资金流向如何"

Forex scalper 2xEMA + SRSI + MACDThis is a forex scalping strategy designed for the most liquid pairs, like major forex pairs.

Its made of

1 EMA 50

1 EMA 100

Stochastic RSI

MACD

Rules

For long :close of the candle is above moving average 50, moving average 50> moving average 100, macd histogram is positive and cross over of stochastic rsi with the oversold level.

For short :close of the candle is below moving average 50, moving average 50 < moving average 100, macd histogram is negative and cross under of stochastic rsi with the overbought level.

Exit

For exit we have take profit and stop loss using fixed pip points.

For this example on EURUSD we use 20 pips for both tp and sl

IF you have any questions let me know !

EBB & Flow: a multi-EMA-based BB cloudIntro

This is an idea evolved out of the market maker method and EMA convergence, divergence, and mean reversion.

The market maker method informs us that the 5, 13, 50 and 200 EMAs are important to regulating price. Those EMA lengths are multiples of the 50 and 200 on lower major timeframes -- the 1 minute, 5, 15, 1H, 4H, 1D. I include the 21 because it is also a multiple and in crypto very often respected.

When market makers are testing price, they set their range and spike in the direction they test for liquidity. This can get chaotic. For instance, in a shorter time frame consolidation inside a bigger timeframe uptrend, it can be too easy to forget where you are in the many trends playing out.

When the EMAs are dragged over each other during normal price movement, you get these crisscrossing tracks of price, and the individual breaks can be hard to trace.

The range is what matters, ultimately, and the range is dynamic. In that case, the Bollinger Band is a great tool for detecting outliers in this case.

The Answer

So the answer this indicator seeks to give, is to look for outliers. This gives you a scalping strategy built on Traders Reality thinking and best put together with the PVSRA indicator, which I may include in this indicator just for the sake of concision, but they can work alongside each other or separately.

The key thing is the different EMA clouds, which are bollinger bands. Tight bands mean imminent breaks, favouring the trend. Vector candles out of a zone, pins to the low/high, etc. are all very relevant alongside this indicator.

You can also use it on its own and scalp the breaks of a cloud.

How it works

Each cloud is a standard deviation from their respective EMA, all in the same colour. The deviation multiple is 1.618 by default. Yes, fibonacci sequences are usually nonsense, but it works better with the BB than 2, 2.5 or 3.

Using just the clouds, you can see where each EMA is headed and how it behaves within the deviation of the others.

But that on its own isn't enough.

The indicator will also print snowflakes above and below the candle for notable outliers. It will be in the colour of the cloud it breaks, but only if that break is also breaking the smaller EMA clouds too.

The most snowflakes will be yellow because that's the 13 EMA. That one is dependent on nothing else and every break will print a snowflake. The 21 will be dependent on the 13. The 50 dependent on the 13 and 21 breaks. The 200 the most important.

For example, if the 200 EMA-BB or EBB is broken at the upper band, deviating by more than 162% of price over a 200 period EMA, and that break is not above the 50 EMA cloud, there will be no snowflake. However, if it exceeds the 13, 21, 50, and 200 clouds, then a purple snowflake will appear above the bar.

Any snowflake is an extreme in price. The purple is an especially good point of entry. That doesn't mean it is a perfect entry. You can build position from it, though, and be relatively certain of a price correction in the near future, because not only was this major EMA cloud violated, but all of the smaller ones too.

Reminder

You still need your PVSRA and candlesticks. This indicator on its own may have a nice hit rate for scalping and building position, as an alternative to the TDI or alongside it, but it is not enough on its own, just like the TDI.

Enjoy!

Quantitative Qualitative Estimation QQE

The QQE indicator is a momentum based indicator to determine trend and sideways.

The Qualitative Quantitative Estimation (QQE) indicator works like a smoother version of the popular Relative Strength Index (RSI) indicator. QQE expands on RSI by adding two volatility based trailing stop lines. These trailing stop lines are composed of a fast and a slow moving Average True Range (ATR). These ATR lines are smoothed making this indicator less susceptible to short term volatility.

The most common method of using QQE is to look for crosses of the fast and slow moving trailing stop lines during periods when the QQE line reflects overbought or oversold conditions

Qualitative Quantitative Estimation made up of a smoothed Relative Strength Index (RSI) indicator plus fast and slow volatility-based trailing levels.

Qualitative Quantitative Estimation can be used in two directions:

1.Determine the trend, i.e. if the line is above the 50 level, the trend is ascending, if below - descending;

2.Search for signals at the moment of crossing of the QQE FAST (maroon) and QQE SLOW (blue) lines.

The QQE itself is generally considered to indicate an up-trend ifQQE FAST is above QQE SLOW, and a down-trend if below QQE SLOW.

Often a middle-range between 40 and 60 is set and if the indicator is in that range, then the market is considered to be tracking sideways, or in no trend.

You will need to set only one parameter – “SF” "RSI SMoothing Factor", an analogue of the period in RSI.

By the way, judging from the open source information, the algorithm used the standard strength index with a period of 14 for calculations.

Various signals can be created from the indicator such as:

-Buy when QQE FAST crosses above QQE SLOW below 50 level or just buy when QQE lines crosses above 50 level.

-Sell when QQE FAST crosses below QQE SLOW above 50 level or just sell when QQE lines crosses below 50 level.

WARNING: QQE IS A RSI BASED INDICATOR SO THAT IT CAN TRIGGER FALSE SIGNALS DURING DIVERGENCES!

Kıvanç Özbilgiç

Nifty VolumeWhy this Script : Nifty 50 does not provide volume and some time it is really useful to understand the volume .

This is the pine script which calculate the nifty 50 volume .

Logic :

Take each stock contribute to nifty 50 and find it's volume .

Multiply the same with contribution percentage of the same on Nifty 50

Add up all of them and find the total volume .

There is a similar script by @daytraderph which is built for Bank Nifty (custom volume) . I took the same and built for Nfity.

Nifty has 50 stocks and you cant call security method more than 40 times from one Pine script, so this is the limitation of this script. It consider top 40 stocks and find the volume (which contribute pretty much around 95% of the volume) and convert the same to 100 %

Simple Moving Average Double HelixThis one is a mix of colour-coded moving averages and Ichimoku. It features two pairs of SMAs--default values of 9/20 and 50/200. Each SMA will be green when it rises and red when it falls. The spaces between each pair will fill with green or red depending on which line is on top. 9 over 20 or 50 over 200 makes a green cloud; if 9 or 50 falls below, the cloud will switch to green.

There's also the Ichimoku lagging span and a 35-period SMA (grey) that can be used as a trailing stop loss guideline.

Ideal long setup:

9, 20, 50, and 200 SMA are all green

both clouds are green

lagging span is above historic price action

Ideal short setup:

9, 20, 50, and 200 SMA are all red

both clouds are red

lagging span is below historic price action

RSI5_50 with DivergenceThis is variation of RSI Divergence strategy.

I have added a filter (long term RSI) to the Rules. strategy BUYs when RSI 50 period is above 50 line and there is divergence on the short term RSI

settings

=========

short term RSI period 5

long term RSI period 50

stopLoss is 8% --- if setting is enabled

BUY Rule

========

RSI 50 is above 50 line

short term RSI is showing divergence

Add to existing

==============

if already in position, BUY when shorTermRSI is crossing above 20

TakeProfit

=========

when longTermRSI reaches 60,65, 70 and 75 level , take partial profits .

(not when crossing down --- This may affect on profits , because when price goes down , it goes very fast )

Exit

=====

when longTermRSI is crossing down 30

OR stopLoss value hits

Note: When I tested this with GOOGL stock , I have got excellent results ... any experts there , please check everything is good with scripting ...

Happy Trading

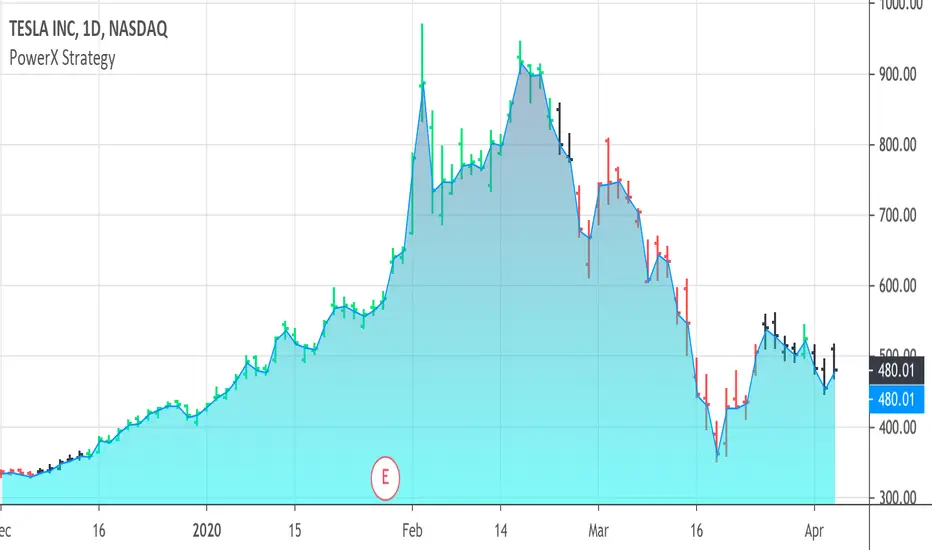

PowerX Strategy Bar Coloring [OFFICIAL VERSION]This script colors the bars according to the PowerX Strategy by Markus Heitkoetter:

The PowerX Strategy uses 3 indicators:

- RSI (7)

- Stochastics (14, 3, 3)

- MACD (12, 26 , 9)

The bars are colored GREEN if...

1.) The RSI (7) is above 50 AND

2.) The Stochastic (14, 3, 3) is above 50 AND

3.) The MACD (12, 26, 9) is above its Moving Average, i.e. MACD Histogram is positive.

The bars are colored RED if...

1.) The RSI (7) is below 50 AND

2.) The Stochastic (14, 3, 3) is below 50 AND

3.) The MACD (12, 26, 9) is below its Moving Average, i.e. MACD Histogram is negative.

If only 2 of these 3 conditions are met, then the bars are black (default color)

We highly recommend plotting the indicators mentioned above on your chart, too, so that you can see when bars are getting close to being "RED" or "GREEN", e.g. RSI is getting close to the 50 line.

BO - Bar's direction Signal - BacktestingBO - Bar's direction Signal - Backtesting Options:

A. Factors Calculate probability of x bars same direction

1. Periods Counting: Data to count From day/month/year To day/month/year

2. Trading Time: only cases occurred in trading time were counted.

B. Timezone

1. Trading time depend on Time zone and specified chart.

2. Enable Highlight Trading Time to check your period time is correct

C. Date Backtesting

* Only cases occurred in Date Backtesting were reported.

D. Setup Options & Rule

1. Reversal after 2 bars same direction

* Probability of 3 bars same direction < 50

* 2 bars same direction is start of series

2. Reversal after 3 bars same direction

* Probability of 4 bars same direction < 50

* 3 bars same direction is start of series

3. Reversal after 4 bars same direction

* Probability of 4 bars same direction < 50

* 3 bars same direction is start of series

4. Reversal after 5 bars same direction

* Probability of 5 bars same direction < 50

* 4 bars same direction is start of series

5. Reversal after 6 bars same direction

* Probability of 6 bars same direction < 50

* 5 bars same direction is start of series

Technical Analysis - Panel Info//A. Oscillators & B. Moving Averages base on TradingView's Technical Analysis by ThiagoSchmitz

//C.Pivot base on Ultimate Pivot Points Alerts by elbartt

//D. Summary & Panel info by anhnguyen14

Panel Info base on these indicators:

A. Oscillators

1. Rsi (14)

2. Stochastic (14,3,3)

3. CCI (20)

4. ADX (14)

5. AO

6. Momentum (10)

7. MACD (12,26)

8. Stoch RSI (3,3,14,14)

9. %R (14)

10. Bull bear

11. UO (7,14,28)

B. Moving Averages

1. SMA & EMA: 5-10-20-30-50-100-200

2. Ichimoku Cloud - Baseline (26)

3. Hull MA (9)

C. Pivot

1. Traditional

2. Fibonacci

3. Woodie

4. Camarilla

D. Summary

Sum_red=A_red+B_red+C_red

Sum_blue=A_blue+B_blue+C_blue

sell_point=(Sum_red/32)*100

buy_point=(Sum_blue/32)*100

sell =

Sum_red>Sum_blue

and sell_point>50

Strong_sell =

A_red>A_blue

and B_red>B_blue

and C_red>C_blue

and sell_point>50

and not crossunder(sell_point,75)

buy =

Sum_red>Sum_blue

and buy_point>50

Strong_buy =

A_red50

and not crossunder(buy_point,75)

neutral = not sell and not Strong_sell and not buy and not Strong_buy

Multi SMA EMA WMA HMA BB (5x8 MAs Bollinger Bands) MAX MTF - RRBMulti SMA EMA WMA HMA 4x7 Moving Averages with Bollinger Bands MAX MTF by RagingRocketBull 2019

Version 1.0

All available MAX MTF versions are listed below (They are very similar and I don't want to publish them as separate indicators):

ver 1.0: 4x7 = 28 MTF MAs + 28 Levels + 3 BB = 59 < 64

ver 2.0: 5x6 = 30 MTF MAs + 30 Levels + 3 BB = 63 < 64

ver 3.0: 3x10 = 30 MTF MAs + 30 Levels + 3 BB = 63 < 64

ver 4.0: 5(4+1)x8 = 8 CurTF MAs + 32 MTF MAs + 20 Levels + 3 BB = 63 < 64

ver 5.0: 6(5+1)x6 = 6 CurTF MAs + 30 MTF MAs + 24 Levels + 3 BB = 63 < 64

ver 6.0: 4(3+1)x10 = 10 CurTF MAs + 30 MTF MAs + 20 Levels + 3 BB = 63 < 64

Fib numbers: 8, 13, 21, 34, 55, 89, 144, 233, 377

This indicator shows multiple MAs of any type SMA EMA WMA HMA etc with BB and MTF support, can show MAs as dynamically moving levels.

There are 4 MA groups + 1 BB group, a total of 4 TFs * 7 MAs = 28 MAs. You can assign any type/timeframe combo to a group, for example:

- EMAs 9,12,26,50,100,200,400 x H1, H4, D1, W1 (4 TFs x 7 MAs x 1 type)

- EMAs 8,13,21,30,34,50,55,89,100,144,200,233,377,400 x M15, H1 (2 TFs x 14 MAs x 1 type)

- D1 EMAs and SMAs 8,13,21,30,34,50,55,89,100,144,200,233,377,400 (1 TF x 14 MAs x 2 types)

- H1 WMAs 13,21,34,55,89,144,233; H4 HMAs 9,12,26,50,100,200,400; D1 EMAs 12,26,89,144,169,233,377; W1 SMAs 9,12,26,50,100,200,400 (4 TFs x 7 MAs x 4 types)

- +1 extra MA type/timeframe for BB

There are several versions: Simple, MTF, Pro MTF, Advanced MTF, MAX MTF and Ultimate MTF. This is the MAX MTF version. The Differences are listed below. All versions have BB

- Simple: you have 2 groups of MAs that can be assigned any type (5+5)

- MTF: +2 custom Timeframes for each group (2x5 MTF) +1 TF for BB, TF XY smoothing

- Pro MTF: 4 custom Timeframes for each group (4x3 MTF), 1 TF for BB, MA levels and show max bars back options

- Advanced MTF: +4 extra MAs/group (4x7 MTF), custom Ticker/Symbols, Timeframe <>= filter, Remove Duplicates Option

- MAX MTF: +2 subtypes/group, packed to the limit with max possible MAs/TFs: 4x7, 5x6, 3x10, 4(3+1)x10, 5(4+1)x8, 6(5+1)x6

- Ultimate MTF: +individual settings for each MA, custom Ticker/Symbols

MAX MTF version tests the limits of Pinescript trying to squeeze as many MAs/TFs as possible into a single indicator.

It's basically a maxed out Advanced version with subtypes allowing for mixed types within a group (i.e. both emas and smas in a single group/TF)

Pinescript has the following limits:

- max 40 security calls (6 calls are reserved for dupe checks and smoothing, 2 are used for BB, so only 32 calls are available)

- max 64 plot outputs (BB uses 3 outputs, so only 61 plot outputs are available)

- max 50000 (50kb) size of the compiled code

Based on those limits, you can only have the following MAs/TFs combos in a single script:

1. 4x7, 5x6, 3x10 - total number of MTF MAs must always be <= 32, and you can still have BB and Num Levels = total MAs, without any compromises

2. 5(4+1)x8, 6(5+1)x6, 4(3+1)x10 - you can use the Current Symbol/Timeframe as an extra (+1) fixed TF with the same number of MTF MAs

- you don't need to call security to display MAs on the Current Symbol/Timeframe, so the total number of MTF MAs remains the same and is still <= 32

- to fit that many MAs into the max 64 plot outputs limit you need to reduce the number of levels (not every MA Group will have corresponding levels)

Features:

- 4x7 = 28 MAs of any type

- 4x MTF groups with XY step line smoothing

- +1 extra TF/type for BB MAs

- 2 MA subtypes within each group/TF

- 4x7 = 28 MA levels with adjustable group offsets, indents and shift

- supports any existing type of MA: SMA, EMA, WMA, Hull Moving Average (HMA)

- custom tickers/symbols for each group

- show max bars back option

- show/hide both groups of MAs/levels/BB and individual MAs

- timeframe filter: show only MAs/Levels with TFs <>= Current TF

- hide MAs/Levels with duplicate TFs

- support for custom TFs that are not available in free accounts: 2D, 3D etc

- support for timeframes in H: H, 2H, 4H etc

Notes:

- Uses timeframe textbox instead of input resolution dropdown to allow for 240 120 and other custom TFs

- Uses symbol textbox instead of input symbol to avoid establishing multiple dummy security connections to the current ticker - otherwise empty symbols will prevent script from running

- Possible reasons for missing MAs on a chart:

- there may not be enough bars in history to start plotting it. For example, W1 EMA200 needs at least 200 bars on a weekly chart.

- for charts with low/fractional prices i.e. 0.00002 << 0.001 (default Y smoothing step) decrease Y smoothing as needed (set Y = 0.0000001) or disable it completely (set X,Y to 0,0)

- for charts with high price values i.e. 20000 >> 0.001 increase Y smoothing as needed (set Y = 10-20). Higher values exceeding MAs point density will cause it to disappear as there will be no points to plot. Different TFs may require diff adjustments

- TradingView Replay Mode UI and Pinescript security calls are limited to TFs >= D (D,2D,W,MN...) for free accounts

- attempting to plot any TF < D1 in Replay Mode will only result in straight lines, but all TFs will work properly in history and real-time modes. This is not a bug.

- Max Bars Back (num_bars) is limited to 5000 for free accounts (10000 for paid), will show error when exceeded. To plot on all available history set to 0 (default)

- Slow load/redraw times. This indicator becomes slower, its UI less responsive when:

- Pinescript Node.js graphics library is too slow and inefficient at plotting bars/objects in a browser window. Code optimization doesn't help much - the graphics engine is the main reason for general slowness.

- the chart has a long history (10000+ bars) in a browser's cache (you have scrolled back a couple of screens in a max zoom mode).

- Reload the page/Load a fresh chart and then apply the indicator or

- Switch to another Timeframe (old TF history will still remain in cache and that TF will be slow)

- in max possible zoom mode around 4500 bars can fit on 1 screen - this also slows down responsiveness. Reset Zoom level

- initial load and redraw times after a param change in UI also depend on TF. For example: D1/W1 - 2 sec, H1/H4 - 5-6 sec, M30 - 10 sec, M15/M5 - 4 sec, M1 - 5 sec. M30 usually has the longest history (up to 16000 bars) and W1 - the shortest (1000 bars).

- when indicator uses more MAs (plots) and timeframes it will redraw slower. Seems that up to 5 Timeframes is acceptable, but 6+ Timeframes can become very slow.

- show_last=last_bars plot limit doesn't affect load/redraw times, so it was removed from MA plot

- Max Bars Back (num_bars) default/custom set UI value doesn't seem to affect load/redraw times

- In max zoom mode all dynamic levels disappear (they behave like text)

- Dupe check includes symbol: symbol, tf, both subtypes - all must match for a duplicate group

- For the dupe check to work correctly a custom symbol must always include an exchange prefix. BB is not checked for dupes

Good Luck! Feel free to learn from/reuse the code to build your own indicators.

Multi SMA EMA WMA HMA BB (4x5 MAs Bollinger Bands) Adv MTF - RRBMulti SMA EMA WMA HMA 4x5 Moving Averages with Bollinger Bands Advanced MTF by RagingRocketBull 2019

Version 1.0

This indicator shows multiple MAs of any type SMA EMA WMA HMA etc with BB and MTF support, can show MAs as dynamically moving levels.

There are 4 MA groups + 1 BB group, a total of 4 TFs * 5 MAs = 20 MAs. You can assign any type/timeframe combo to a group, for example:

- EMAs 12,26,50,100,200 x H1, H4, D1, W1 (4 TFs x 5 MAs x 1 type)

- EMAs 8,10,13,21,30,50,55,100,200,400 x M15, H1 (2 TFs x 10 MAs x 1 type)

- D1 EMAs and SMAs 8,10,12,26,30,50,55,100,200,400 (1 TF x 10 MAs x 2 types)

- H1 WMAs 7,77,89,167,231; H4 HMAs 12,26,50,100,200; D1 EMAs 89,144,169,233,377; W1 SMAs 12,26,50,100,200 (4 TFs x 5 MAs x 4 types)

- +1 extra MA type/timeframe for BB

There are several versions: Simple, MTF, Pro MTF, Advanced MTF and Ultimate MTF. This is the Advanced MTF version. The Differences are listed below. All versions have BB

- Simple: you have 2 groups of MAs that can be assigned any type (5+5)

- MTF: +2 custom Timeframes for each group (2x5 MTF) +1 TF for BB, TF XY smoothing

- Pro MTF: 4 custom Timeframes for each group (4x3 MTF), 1 TF for BB, MA levels and show max bars back options

- Advanced MTF: +2 extra MAs/group (4x5 MTF), custom Ticker/Symbols, Timeframe <>= filter, Remove Duplicates Option

- Ultimate MTF: +individual settings for each MA, custom Ticker/Symbols

Features:

- 4x5 = 20 MAs of any type

- 4x MTF groups with XY step line smoothing

- +1 extra TF/type for BB MAs

- 4x5 = 20 MA levels with adjustable group offsets, indents and shift

- supports any existing type of MA: SMA, EMA, WMA, Hull Moving Average (HMA)

- custom tickers/symbols for each group - you can compare MAs of the same symbol across exchanges

- show max bars back option

- show/hide both groups of MAs/levels/BB and individual MAs

- timeframe filter: show only MAs/Levels with TFs <>= Current TF

- hide MAs/Levels with duplicate TFs

- support for custom TFs that are not available in free accounts: 2D, 3D etc

- support for timeframes in H: H, 2H, 4H etc

Notes:

- Uses timeframe textbox instead of input resolution dropdown to allow for 240 120 and other custom TFs

- Uses symbol textbox instead of input symbol to avoid establishing multiple dummy security connections to the current ticker - otherwise empty symbols will prevent script from running

- Possible reasons for missing MAs on a chart:

- there may not be enough bars in history to start plotting it. For example, W1 EMA200 needs at least 200 bars on a weekly chart.

- price << default Y smoothing step 5. For charts with low/fractional prices (i.e. 0.00002 << 5) adjust X Y smoothing as needed (set Y = 0.0000001) or disable it completely (set X,Y to 0,0)

- TradingView Replay Mode UI and Pinescript security calls are limited to TFs >= D (D,2D,W,MN...) for free accounts

- attempting to plot any TF < D1 in Replay Mode will only result in straight lines, but all TFs will work properly in history and real-time modes. This is not a bug.

- Max Bars Back (num_bars) is limited to 5000 for free accounts (10000 for paid), will show error when exceeded. To plot on all available history set to 0 (default)

- Slow load/redraw times. This indicator becomes slower, its UI less responsive when:

- Pinescript Node.js graphics library is too slow and inefficient at plotting bars/objects in a browser window. Code optimization doesn't help much - the graphics engine is the main reason for general slowness.

- the chart has a long history (10000+ bars) in a browser's cache (you have scrolled back a couple of screens in a max zoom mode).

- Reload the page/Load a fresh chart and then apply the indicator or

- Switch to another Timeframe (old TF history will still remain in cache and that TF will be slow)

- in max possible zoom mode around 4500 bars can fit on 1 screen - this also slows down responsiveness. Reset Zoom level

- initial load and redraw times after a param change in UI also depend on TF. For example:

D1/W1 - 2 sec, H1/H4 - 5-6 sec, M30 - 10 sec, M15/M5 - 4 sec, M1 - 5 sec.

M30 usually has the longest history (up to 16000 bars) and W1 - the shortest (1000 bars).

- when indicator uses more MAs (plots) and timeframes it will redraw slower. Seems that up to 5 Timeframes is acceptable, but 6+ Timeframes can become very slow.

- show_last=last_bars plot limit doesn't affect load/redraw times, so it was removed from MA plot

- Max Bars Back (num_bars) default/custom set UI value doesn't seem to affect load/redraw times

- In max zoom mode all dynamic levels disappear (they behave like text)

1. based on 3EmaBB, uses plot*, barssince and security functions

2. you can't set certain constants from input due to Pinescript limitations - change the code as needed, recompile and use as a private version

3. Levels = trackprice implementation

4. Show Max Bars Back = show_last implementation

5. swma has a fixed length = 4, alma and linreg have additional offset and smoothing params

6. Smoothing is applied by default for visual aesthetics on MTF. To use exact ma mtf values (lines with stair stepping) - disable it

Good Luck! You can explore, modify/reuse the code to build your own indicators.

BB Quick Fire5 Bollinger Bands in levels 50,2.0 | 50,2.5 |50,3.0 |50,3.5 |50,4.0

This is used to identify pullbakcs and future pitchfork's.

CM Stochastic POP Method 2-Jake Bernstein_V1Yesterday Jake Bernstein authorized me to post his updated results with the Stochastic Pop Trading System he developed many years ago.

You can take a look at the Original System with Updated Settings at

This indicator is a different set of rules Jake mentioned in the PDF he allowed me to post.

To view the PDF use this link:

dl.dropboxusercontent.com

Today we’re releasing the version described in the PDF that uses the StochK values of 55, 50, and 45. The rules are discussed in the PDF but here is a simple breakdown:

Enter Long when StochK is below 50 and Crosses Above 55

Exit Long on Cross Below 55

Enter Short when StochK is Above 50 and crosses Below 45

Exit Short on Cross Above 45

Two Important Items to understand about this method:

To code the rules Precisely we need a function that will be available when Strategy Capabilities are released on TradingView.

There is one of Jakes Profit Maximizing Strategies that needs to be integrated with this code…which again we need the Strategy based Function that will be coming soon.

To Compare this system to the Stochastic Pop Method 1 System shown yesterday at I used the same Symbol and dates for you to compare…but remember to give this Method 2 System a Fair Look/Evaluation…we need the Soon To Be Released…TradingView Strategy Capabilities.

BackTesting Results Example: EUR-USD Daily Chart Since 01/01/2005

Strategy 1 – Stochastic Pop Method 2 System:

Go Long When Stochasticis below 50 and Crosses Above 55. Go Short When Stochastic is above 50 and Crosses Below 45. Exit Long/Short When Stochastic has a Reverse Cross of Entry Value.

Results:

Total Trades = 151

Profit = 40,758 Pips

Win% = 37.1%

Profit Factor = 1.26

Avg Trade = 270 Pips Profit

***Most Consecutive Wins = 4 ... Most Consecutive Losses = 7

Strategy 2:

Rules - Proprietary Optimization Jake Will Teach. Only Added 1 Additional Exit Rule.

Results:

Total Trades = 151

Profit = 60.305 Pips

Win% = 37.1%

Profit Factor = 1.38

Avg Trade = 399 Pips Profit

***Most Consecutive Wins = 4 ... Most Consecutive Losses = 7

Indicator Includes:

-Ability to Color Candles (CheckBox In Inputs Tab)

Green = Long Trade

Blue = No Trade

Red = Short Trade

Jake Bernstein will be a contributor on TradingView when Backtesting/Strategies are released. Jake is one of the Top Trading System Developers in the world with 45+ years experience and he is going to teach TradingView.com’s community how to create Trading Systems and how to Optimize the correct way.

Link To PDF:

dl.dropboxusercontent.com

Link to Original Version of Indicator with Updated Settings.

RSI adaptive zones [AdaptiveRSI]This script introduces a unified mathematical framework that auto-scales oversold/overbought and support/resistance zones for any period length. It also adds true RSI candles for spotting intrabar signals.

Built on the Logit RSI foundation, this indicator converts RSI into a statistically normalized space, allowing all RSI lengths to share the same mathematical footing.

What was once based on experience and observation is now grounded in math.

✦ ✦ ✦ ✦ ✦

💡 Example Use Cases

RSI(14): Classic overbought/oversold signals + divergence

Support in an uptrend using RSI(14)

Range breakouts using RSI(21)

Short-term pullbacks using RSI(5)

✦ ✦ ✦ ✦ ✦

THE PAST: RSI Interpretation Required Multiple Rulebooks

Over decades, RSI practitioners discovered that RSI behaves differently depending on trend and lookback length:

• In uptrends, RSI tends to hold higher support zones (40–50)

• In downtrends, RSI tends to resist below 50–60

• Short RSIs (e.g., RSI(2)) require far more extreme threshold values

• Longer RSIs cluster near the center and rarely reach 70/30

These observations were correct — but lacked a unifying mathematical explanation.

✦ ✦ ✦ ✦ ✦

THE PRESENT: One Framework Handles RSI(2) to RSI(200)

Instead of using fixed thresholds (70/30, 90/10, etc.), this indicator maps RSI into a normalized statistical space using:

• The Logit transformation to remove 0–100 scale distortion

• A universal scaling based on 2/√(n−1) scaling factor to equalize distribution shapes

As a result, RSI values become directly comparable across all lookback periods.

✦ ✦ ✦ ✦ ✦

💡 How the Adaptive Zones Are Calculated

The adaptive framework defines RSI zones as statistical regimes derived from the Logit-transformed RSI .

Each boundary corresponds to a standard deviation (σ) threshold, scaled by 2/√(n−1), making RSI distributions comparable across periods.

This structure was inspired by Nassim Nicholas Taleb’s body–shoulders–tails regime model:

Body (±0.66σ) — consolidation / equilibrium

Shoulders (±1σ to ±2.14σ) — trending region

Tails (outside of ±2.14σ) — rare, high-volatility behavior

Transitions between these regimes are defined by the derivatives of the position (CDF) function :

• ±1σ → shift from consolidation to trend

• ±√3σ → shift from trend to exhaustion

Adaptive Zone Summary

Consolidation: −0.66σ to +0.66σ

Support/Resistance: ±0.66σ to ±1σ

Uptrend/Downtrend: ±1σ to ±√3σ

Overbought/Oversold: ±√3σ to ±2.14σ

Tails: outside of ±2.14σ

✦ ✦ ✦ ✦ ✦

📌 Inverse Transformation: From σ-Space Back to RSI

A final step is required to return these statistically normalized boundaries back into the familiar 0–100 RSI scale. Because the Logit transform maps RSI into an unbounded real-number domain, the inverse operation uses the hyperbolic tangent function to compress σ-space back into the bounded RSI range.

RSI(n) = 50 + 50 · tanh(z / √(n − 1))

The result is a smooth, mathematically consistent conversion where the same statistical thresholds maintain identical meaning across all RSI lengths, while still expressing themselves as intuitive RSI values traders already understand.

✦ ✦ ✦ ✦ ✦

Key Features

Mathematically derived adaptive zones for any RSI period

Support/resistance zone identification for trend-aligned reversals

Optional OHLC RSI bars/candles for intrabar zone interactions

Fully customizable zone visibility and colors

Statistically consistent interpretation across all markets and timeframes

Inputs

RSI Length — core parameter controlling zone scaling

RSI Display : Line / Bar / Candle visualization modes

✦ ✦ ✦ ✦ ✦

💡 How to Use

This indicator is a framework , not a binary signal generator.

Start by defining the question you want answered, e.g.:

• Where is the breakout?

• Is price overextended or still trending?

• Is the correction ending, or is trend reversing?

Then:

Choose the RSI length that matches your timeframe

Observe which adaptive zone price is interacting with

Interpret market behavior accordingly

Example: Long-Term Trend Assesment using RSI(200)

A trader may ask: "Is this a long term top?"

Unlikely, because RSI(200) holds above Resistance zone , therefore the trend remains strong.

✦ ✦ ✦ ✦ ✦

👉 Practical tip:

If you used to overlay weekly RSI(14) on a daily chart (getting a line that waits 5 sessions to recalculate), you can now read the same long-horizon state continuously : set RSI(70) on the daily chart (~14 weeks × 5 days/week = 70 days) and let the adaptive zones update every bar .

Note: It won’t be numerically identical to the weekly RSI due to lookback period used, but it tracks the same regime on a standardized scale with bar-by-bar updates.

✦ ✦ ✦ ✦ ✦

Note: This framework describes statistical structure, not prediction. Use as part of a complete trading approach. Past behavior does not guarantee future outcomes.

framework ≠ guaranteed signal

---

Attribution & License

This indicator incorporates:

• Logit transformation of RSI

• Variance scaling using 2/√(n−1)

• Zone placement derived from Taleb’s body–shoulders–tails regime model and CDF derivatives

• Inverse TANH(z) transform for mapping z-scores back into bounded RSI space

Released under CC BY-NC-SA 4.0 — free for non-commercial use with credit.

© AdaptiveRSI

GRA v5 SNIPER# GRA v5 SNIPER - Documentation & Cheatsheet

## 🎯 Get Rich Aggressively v5 - SNIPER Edition

**Precision Futures Scalping | NQ • ES • YM • GC • BTC**

> **Philosophy:** *Quality over quantity. One sniper shot beats ten spray-and-pray attempts.*

---

## ⚡ QUICK CHEATSHEET

```

┌─────────────────────────────────────────────────────────────────────────────┐

│ GRA v5 SNIPER - QUICK REFERENCE │

├─────────────────────────────────────────────────────────────────────────────┤

│ │

│ 🎯 SIGNAL REQUIREMENTS (ALL MUST BE TRUE): │

│ ═══════════════════════════════════════════ │

│ ✓ Tier → B minimum (20+ pts NQ) │

│ ✓ Volume → 1.5x+ average │

│ ✓ Delta → 60%+ dominance (buyers OR sellers) │

│ ✓ Body → 70%+ of candle range │

│ ✓ Range → 1.3x+ average candle size │

│ ✓ Wicks → Small opposite wick (<50% of body) │

│ ✓ CVD → Trending with signal direction │

│ ✓ Session → London (3-5am ET) OR NY (9:30-11:30am ET) │

│ │

├─────────────────────────────────────────────────────────────────────────────┤

│ │

│ 📊 TIER ACTIONS: │

│ ════════════════ │

│ S-TIER (100+ pts) → 🥇 HOLD position, ride the wave │

│ A-TIER (50-99 pts) → 🥈 SWING for 2-3 minutes │

│ B-TIER (20-49 pts) → 🥉 SCALP quick, 30-60 seconds │

│ │

├─────────────────────────────────────────────────────────────────────────────┤

│ │

│ 🚨 ENTRY CHECKLIST: │

│ ═══════════════════ │

│ □ Signal appears (S🎯, A🎯, or B🎯) │

│ □ Table shows: Vol GREEN, Delta colored, Body GREEN │

│ □ CVD arrow matches direction (▲ for long, ▼ for short) │

│ □ Session active (LDN! or NY! in yellow) │

│ □ Enter at close of signal candle │

│ │

├─────────────────────────────────────────────────────────────────────────────┤

│ │

│ ⛔ DO NOT TRADE WHEN: │

│ ════════════════════ │

│ ✗ Session shows "---" (outside key hours) │

│ ✗ Vol shows RED (below 1.5x) │

│ ✗ Body shows RED (weak candle structure) │

│ ✗ Delta below 60% (no clear dominance) │

│ ✗ Multiple conflicting signals │

│ │

├─────────────────────────────────────────────────────────────────────────────┤

│ │

│ 📈 INSTRUMENT SETTINGS: │

│ ════════════════════════ │

│ NQ/ES (1-3 min): S=100, A=50, B=20 pts │

│ YM (1-5 min): S=100, A=50, B=25 pts │

│ GC (5-15 min): S=15, A=8, B=4 pts │

│ BTC (1-15 min): S=500, A=250, B=100 pts │

│ │

└─────────────────────────────────────────────────────────────────────────────┘

```

---

## 📋 DETAILED DOCUMENTATION

### What Makes SNIPER Different?

The SNIPER edition eliminates 80%+ of signals compared to standard GRA. Every signal that passes through has been validated by **8 independent filters**:

| Filter | Standard GRA | SNIPER GRA | Why It Matters |

|--------|-------------|------------|----------------|

| Volume | 1.3x avg | **1.5x avg** | Institutional participation |

| Delta | 55% | **60%** | Clear buyer/seller control |

| Body Ratio | None | **70%+** | No dojis or spinners |

| Range | None | **1.3x avg** | Significant price movement |

| Wicks | None | **<50% body** | Conviction in direction |

| CVD | None | **Required** | Trend confirmation |

| B-Tier Min | 10 pts | **20 pts** | Filter noise |

| Session | Optional | **Required** | Institutional hours |

---

### Signal Anatomy

When you see a signal like `A🎯`, here's what passed validation:

```

Signal: A🎯 LONG at 21,450.00

Validation Breakdown:

├── Points: 67.5 pts ✓ (A-Tier = 50-99)

├── Volume: 2.1x avg ✓ (≥1.5x required)

├── Delta: 68% Buyers ✓ (≥60% required)

├── Body: 78% of range ✓ (≥70% required)

├── Range: 1.6x avg ✓ (≥1.3x required)

├── Wick: Upper 15% ✓ (<50% of body)

├── CVD: ▲ Rising ✓ (Matches LONG)

└── Session: NY! ✓ (Active session)

RESULT: VALID SNIPER SIGNAL

```

---

### Table Legend

| Field | Reading | Color Meaning |

|-------|---------|---------------|

| **Pts** | Point movement | Gold/Green/Yellow = Tiered |

| **Tier** | S/A/B/X | Gold/Green/Yellow/White |

| **Vol** | Volume ratio | 🟢 ≥1.5x, 🔴 <1.5x |

| **Delta** | Buy/Sell % | 🟢 Buy dom, 🔴 Sell dom, ⚪ Neutral |

| **Body** | Body % of range | 🟢 ≥70%, 🔴 <70% |

| **CVD** | Cumulative delta | ▲ Bullish trend, ▼ Bearish trend |

| **Sess** | Session status | 🟡 Active, ⚫ Inactive |

---

### Trading Rules

#### Entry Rules

1. **Wait for signal** - Don't anticipate

2. **Verify table** - All conditions GREEN

3. **Enter at candle close** - Not during formation

4. **Position size by tier:**

- S-Tier: Full size

- A-Tier: 75% size

- B-Tier: 50% size

#### Exit Rules

| Tier | Target | Max Hold Time |

|------|--------|---------------|

| S | Let it run | 5-10 minutes |

| A | 1:1.5 R:R | 2-3 minutes |

| B | 1:1 R:R | 30-60 seconds |

#### Stop Loss

- Place at **opposite end of signal candle**

- For S-Tier: Allow 50% retracement

- For B-Tier: Tight stop, quick exit

---

### Session Priority

```

LONDON OPEN (3:00-5:00 AM ET)

════════════════════════════

• Best for: GC, European indices

• Characteristics: Stop hunts, reversals

• Look for: Sweeps of Asian session levels

NY OPEN (9:30-11:30 AM ET)

════════════════════════════

• Best for: NQ, ES, YM

• Characteristics: High volume, trends

• Look for: Continuation after 10 AM

```

---

### Common Mistakes to Avoid

| Mistake | Why It's Bad | Solution |

|---------|-------------|----------|

| Trading outside sessions | Low volume = fake moves | Wait for LDN! or NY! |

| Ignoring weak body | Dojis reverse | Body must be 70%+ |

| Fighting CVD | Swimming upstream | CVD must confirm |

| Oversizing B-Tier | Small moves = small size | 50% max on B |

| Chasing missed signals | FOMO loses money | Wait for next setup |

---

### Alert Setup

Configure these alerts in TradingView:

| Alert | Priority | Action |

|-------|----------|--------|

| 🎯 S-TIER LONG/SHORT | 🔴 High | Drop everything, check chart |

| 🎯 A-TIER LONG/SHORT | 🟠 Medium | Evaluate within 30 seconds |

| 🎯 B-TIER LONG/SHORT | 🟢 Low | Quick glance if available |

| LONDON/NY OPEN | 🔵 Info | Prepare for action |

---

### Pine Script v6 Notes

This indicator uses Pine Script v6 features:

- `request.security_lower_tf()` for intrabar delta

- Type inference for cleaner code

- Array operations for CVD calculation

**Minimum TradingView Plan:** Pro (for intrabar data)

---

## 🏆 Golden Rule

> **"If you have to convince yourself it's a good signal, it's not a good signal."**

The SNIPER edition is designed so that when a signal appears, there's nothing to think about. If all conditions are met, you trade. If any condition fails, you wait.

**Leave every trade with money. That's the goal.**

---

*© Alexandro Disla - Get Rich Aggressively v5 SNIPER*

*Pine Script v6 | TradingView*

BTC Dashboard D / 4H / 1H (simple)//@version=5

indicator("BTC Dashboard D / 4H / 1H (simple)", overlay = true)

// ---------- Réglages ----------

rsiLen = 14

emaLen50 = 50

emaLen200 = 200

// Petite fonction pour formater les nombres

f_fmt(float v) =>

str.tostring(v, format.mintick)

// ---------- TIMEFRAMES ----------

tfD = "D"

tf4H = "240"

tf1H = "60"

// ---------- DAILY ----------

closeD = request.security(syminfo.tickerid, tfD, close)

ema50D = request.security(syminfo.tickerid, tfD, ta.ema(close, emaLen50))

ema200D = request.security(syminfo.tickerid, tfD, ta.ema(close, emaLen200))

rsiD = request.security(syminfo.tickerid, tfD, ta.rsi(close, rsiLen))

// ---------- 4H ----------

close4H = request.security(syminfo.tickerid, tf4H, close)

ema504H = request.security(syminfo.tickerid, tf4H, ta.ema(close, emaLen50))

ema2004H = request.security(syminfo.tickerid, tf4H, ta.ema(close, emaLen200))

rsi4H = request.security(syminfo.tickerid, tf4H, ta.rsi(close, rsiLen))

// ---------- 1H ----------

close1H = request.security(syminfo.tickerid, tf1H, close)

ema501H = request.security(syminfo.tickerid, tf1H, ta.ema(close, emaLen50))

ema2001H = request.security(syminfo.tickerid, tf1H, ta.ema(close, emaLen200))

rsi1H = request.security(syminfo.tickerid, tf1H, ta.rsi(close, rsiLen))

// ---------- TABLE ----------

var table t = table.new(position.top_right, 4, 4, border_width = 1)

if barstate.islast

// Ligne d’en-tête

table.cell(t, 0, 0, "TF", text_color = color.white, bgcolor = color.new(color.black, 0))

table.cell(t, 0, 1, "Close", text_color = color.white, bgcolor = color.new(color.black, 0))

table.cell(t, 0, 2, "EMA50 / EMA200", text_color = color.white, bgcolor = color.new(color.black, 0))

table.cell(t, 0, 3, "RSI", text_color = color.white, bgcolor = color.new(color.black, 0))

// ----- DAILY -----

rowD = 1

table.cell(t, rowD, 0, "D", text_color = color.yellow, bgcolor = color.new(color.blue, 70))

table.cell(t, rowD, 1, f_fmt(closeD))

table.cell(t, rowD, 2, "50: " + f_fmt(ema50D) + "\n200: " + f_fmt(ema200D))

table.cell(t, rowD, 3, f_fmt(rsiD))

// ----- 4H -----

row4 = 2

table.cell(t, row4, 0, "4H", text_color = color.white, bgcolor = color.new(color.teal, 70))

table.cell(t, row4, 1, f_fmt(close4H))

table.cell(t, row4, 2, "50: " + f_fmt(ema504H) + "\n200: " + f_fmt(ema2004H))

table.cell(t, row4, 3, f_fmt(rsi4H))

// ----- 1H -----

row1 = 3

table.cell(t, row1, 0, "1H", text_color = color.white, bgcolor = color.new(color.green, 70))

table.cell(t, row1, 1, f_fmt(close1H))

table.cell(t, row1, 2, "50: " + f_fmt(ema501H) + "\n200: " + f_fmt(ema2001H))

table.cell(t, row1, 3, f_fmt(rsi1H))

Dynamic Equity Allocation Model//@version=6

indicator('Dynamic Equity Allocation Model', shorttitle = 'DEAM', overlay = false, precision = 1, scale = scale.right, max_bars_back = 500)

// DYNAMIC EQUITY ALLOCATION MODEL

// Quantitative framework for dynamic portfolio allocation between stocks and cash.

// Analyzes five dimensions: market regime, risk metrics, valuation, sentiment,

// and macro conditions to generate allocation recommendations (0-100% equity).

//

// Uses real-time data from TradingView including fundamentals (P/E, ROE, ERP),

// volatility indicators (VIX), credit spreads, yield curves, and market structure.

// INPUT PARAMETERS

group1 = 'Model Configuration'

model_type = input.string('Adaptive', 'Allocation Model Type', options = , group = group1, tooltip = 'Conservative: Slower to increase equity, Aggressive: Faster allocation changes, Adaptive: Dynamic based on regime')

use_crisis_detection = input.bool(true, 'Enable Crisis Detection System', group = group1, tooltip = 'Automatic detection and response to crisis conditions')

use_regime_model = input.bool(true, 'Use Market Regime Detection', group = group1, tooltip = 'Identify Bull/Bear/Crisis regimes for dynamic allocation')

group2 = 'Portfolio Risk Management'

target_portfolio_volatility = input.float(12.0, 'Target Portfolio Volatility (%)', minval = 3, maxval = 20, step = 0.5, group = group2, tooltip = 'Target portfolio volatility (Cash reduces volatility: 50% Equity = ~10% vol, 100% Equity = ~20% vol)')

max_portfolio_drawdown = input.float(15.0, 'Maximum Portfolio Drawdown (%)', minval = 5, maxval = 35, step = 2.5, group = group2, tooltip = 'Maximum acceptable PORTFOLIO drawdown (not market drawdown - portfolio with cash has lower drawdown)')

enable_portfolio_risk_scaling = input.bool(true, 'Enable Portfolio Risk Scaling', group = group2, tooltip = 'Scale allocation based on actual portfolio risk characteristics (recommended)')

risk_lookback = input.int(252, 'Risk Calculation Period (Days)', minval = 60, maxval = 504, group = group2, tooltip = 'Period for calculating volatility and risk metrics')

group3 = 'Component Weights (Total = 100%)'

w_regime = input.float(35.0, 'Market Regime Weight (%)', minval = 0, maxval = 100, step = 5, group = group3)

w_risk = input.float(25.0, 'Risk Metrics Weight (%)', minval = 0, maxval = 100, step = 5, group = group3)

w_valuation = input.float(20.0, 'Valuation Weight (%)', minval = 0, maxval = 100, step = 5, group = group3)

w_sentiment = input.float(15.0, 'Sentiment Weight (%)', minval = 0, maxval = 100, step = 5, group = group3)

w_macro = input.float(5.0, 'Macro Weight (%)', minval = 0, maxval = 100, step = 5, group = group3)

group4 = 'Crisis Detection Thresholds'

crisis_vix_threshold = input.float(40, 'Crisis VIX Level', minval = 30, maxval = 80, group = group4, tooltip = 'VIX level indicating crisis conditions (COVID peaked at 82)')

crisis_drawdown_threshold = input.float(15, 'Crisis Drawdown Threshold (%)', minval = 10, maxval = 30, group = group4, tooltip = 'Market drawdown indicating crisis conditions')

crisis_credit_spread = input.float(500, 'Crisis Credit Spread (bps)', minval = 300, maxval = 1000, group = group4, tooltip = 'High yield spread indicating crisis conditions')

group5 = 'Display Settings'

show_components = input.bool(false, 'Show Component Breakdown', group = group5, tooltip = 'Display individual component analysis lines')

show_regime_background = input.bool(true, 'Show Dynamic Background', group = group5, tooltip = 'Color background based on allocation signals')

show_reference_lines = input.bool(false, 'Show Reference Lines', group = group5, tooltip = 'Display allocation percentage reference lines')

show_dashboard = input.bool(true, 'Show Analytics Dashboard', group = group5, tooltip = 'Display comprehensive analytics table')

show_confidence_bands = input.bool(false, 'Show Confidence Bands', group = group5, tooltip = 'Display uncertainty quantification bands')

smoothing_period = input.int(3, 'Smoothing Period', minval = 1, maxval = 10, group = group5, tooltip = 'Smoothing to reduce allocation noise')

background_intensity = input.int(95, 'Background Intensity (%)', minval = 90, maxval = 99, group = group5, tooltip = 'Higher values = more transparent background')

// Styling Options

color_scheme = input.string('EdgeTools', 'Color Theme', options = , group = 'Appearance', tooltip = 'Professional color themes')

use_dark_mode = input.bool(true, 'Optimize for Dark Theme', group = 'Appearance')

main_line_width = input.int(3, 'Main Line Width', minval = 1, maxval = 5, group = 'Appearance')

// DATA RETRIEVAL

// Market Data

sp500 = request.security('SPY', timeframe.period, close)

sp500_high = request.security('SPY', timeframe.period, high)

sp500_low = request.security('SPY', timeframe.period, low)

sp500_volume = request.security('SPY', timeframe.period, volume)

// Volatility Indicators

vix = request.security('VIX', timeframe.period, close)

vix9d = request.security('VIX9D', timeframe.period, close)

vxn = request.security('VXN', timeframe.period, close)

// Fixed Income and Credit

us2y = request.security('US02Y', timeframe.period, close)

us10y = request.security('US10Y', timeframe.period, close)

us3m = request.security('US03MY', timeframe.period, close)

hyg = request.security('HYG', timeframe.period, close)

lqd = request.security('LQD', timeframe.period, close)

tlt = request.security('TLT', timeframe.period, close)

// Safe Haven Assets

gold = request.security('GLD', timeframe.period, close)

usd = request.security('DXY', timeframe.period, close)

yen = request.security('JPYUSD', timeframe.period, close)

// Financial data with fallback values

get_financial_data(symbol, fin_id, period, fallback) =>

data = request.financial(symbol, fin_id, period, ignore_invalid_symbol = true)

na(data) ? fallback : data

// SPY fundamental metrics

spy_earnings_per_share = get_financial_data('AMEX:SPY', 'EARNINGS_PER_SHARE_BASIC', 'TTM', 20.0)

spy_operating_earnings_yield = get_financial_data('AMEX:SPY', 'OPERATING_EARNINGS_YIELD', 'FY', 4.5)

spy_dividend_yield = get_financial_data('AMEX:SPY', 'DIVIDENDS_YIELD', 'FY', 1.8)

spy_buyback_yield = get_financial_data('AMEX:SPY', 'BUYBACK_YIELD', 'FY', 2.0)

spy_net_margin = get_financial_data('AMEX:SPY', 'NET_MARGIN', 'TTM', 12.0)

spy_debt_to_equity = get_financial_data('AMEX:SPY', 'DEBT_TO_EQUITY', 'FY', 0.5)

spy_return_on_equity = get_financial_data('AMEX:SPY', 'RETURN_ON_EQUITY', 'FY', 15.0)

spy_free_cash_flow = get_financial_data('AMEX:SPY', 'FREE_CASH_FLOW', 'TTM', 100000000)

spy_ebitda = get_financial_data('AMEX:SPY', 'EBITDA', 'TTM', 200000000)

spy_pe_forward = get_financial_data('AMEX:SPY', 'PRICE_EARNINGS_FORWARD', 'FY', 18.0)

spy_total_debt = get_financial_data('AMEX:SPY', 'TOTAL_DEBT', 'FY', 500000000)

spy_total_equity = get_financial_data('AMEX:SPY', 'TOTAL_EQUITY', 'FY', 1000000000)

spy_enterprise_value = get_financial_data('AMEX:SPY', 'ENTERPRISE_VALUE', 'FY', 30000000000)

spy_revenue_growth = get_financial_data('AMEX:SPY', 'REVENUE_ONE_YEAR_GROWTH', 'TTM', 5.0)

// Market Breadth Indicators

nya = request.security('NYA', timeframe.period, close)

rut = request.security('IWM', timeframe.period, close)

// Sector Performance

xlk = request.security('XLK', timeframe.period, close)

xlu = request.security('XLU', timeframe.period, close)

xlf = request.security('XLF', timeframe.period, close)

// MARKET REGIME DETECTION

// Calculate Market Trend

sma_20 = ta.sma(sp500, 20)

sma_50 = ta.sma(sp500, 50)

sma_200 = ta.sma(sp500, 200)

ema_10 = ta.ema(sp500, 10)

// Market Structure Score

trend_strength = 0.0

trend_strength := trend_strength + (sp500 > sma_20 ? 1 : -1)

trend_strength := trend_strength + (sp500 > sma_50 ? 1 : -1)

trend_strength := trend_strength + (sp500 > sma_200 ? 2 : -2)

trend_strength := trend_strength + (sma_50 > sma_200 ? 2 : -2)

// Volatility Regime

returns = math.log(sp500 / sp500 )

realized_vol_20d = ta.stdev(returns, 20) * math.sqrt(252) * 100

realized_vol_60d = ta.stdev(returns, 60) * math.sqrt(252) * 100

ewma_vol = ta.ema(math.pow(returns, 2), 20)

realized_vol = math.sqrt(ewma_vol * 252) * 100

vol_premium = vix - realized_vol

// Drawdown Calculation

running_max = ta.highest(sp500, risk_lookback)

current_drawdown = (running_max - sp500) / running_max * 100

// Regime Score

regime_score = 0.0

// Trend Component (40%)

if trend_strength >= 4

regime_score := regime_score + 40

regime_score

else if trend_strength >= 2

regime_score := regime_score + 30

regime_score

else if trend_strength >= 0

regime_score := regime_score + 20

regime_score

else if trend_strength >= -2

regime_score := regime_score + 10

regime_score

else

regime_score := regime_score + 0

regime_score

// Volatility Component (30%)

if vix < 15

regime_score := regime_score + 30

regime_score

else if vix < 20

regime_score := regime_score + 25

regime_score

else if vix < 25

regime_score := regime_score + 15

regime_score

else if vix < 35

regime_score := regime_score + 5

regime_score

else

regime_score := regime_score + 0

regime_score

// Drawdown Component (30%)

if current_drawdown < 3

regime_score := regime_score + 30

regime_score

else if current_drawdown < 7

regime_score := regime_score + 20

regime_score

else if current_drawdown < 12

regime_score := regime_score + 10

regime_score

else if current_drawdown < 20

regime_score := regime_score + 5

regime_score

else

regime_score := regime_score + 0

regime_score

// Classify Regime

market_regime = regime_score >= 80 ? 'Strong Bull' : regime_score >= 60 ? 'Bull Market' : regime_score >= 40 ? 'Neutral' : regime_score >= 20 ? 'Correction' : regime_score >= 10 ? 'Bear Market' : 'Crisis'

// RISK-BASED ALLOCATION

// Calculate Market Risk

parkinson_hl = math.log(sp500_high / sp500_low)

parkinson_vol = parkinson_hl / (2 * math.sqrt(math.log(2))) * math.sqrt(252) * 100

garman_klass_vol = math.sqrt((0.5 * math.pow(math.log(sp500_high / sp500_low), 2) - (2 * math.log(2) - 1) * math.pow(math.log(sp500 / sp500 ), 2)) * 252) * 100

market_volatility_20d = math.max(ta.stdev(returns, 20) * math.sqrt(252) * 100, parkinson_vol)

market_volatility_60d = ta.stdev(returns, 60) * math.sqrt(252) * 100

market_drawdown = current_drawdown

// Initialize risk allocation

risk_allocation = 50.0

if enable_portfolio_risk_scaling

// Volatility-based allocation

vol_based_allocation = target_portfolio_volatility / math.max(market_volatility_20d, 5.0) * 100

vol_based_allocation := math.max(0, math.min(100, vol_based_allocation))

// Drawdown-based allocation

dd_based_allocation = 100.0

if market_drawdown > 1.0

dd_based_allocation := max_portfolio_drawdown / market_drawdown * 100

dd_based_allocation := math.max(0, math.min(100, dd_based_allocation))

dd_based_allocation

// Combine (conservative)

risk_allocation := math.min(vol_based_allocation, dd_based_allocation)

// Dynamic adjustment

current_equity_estimate = 50.0

estimated_portfolio_vol = current_equity_estimate / 100 * market_volatility_20d

estimated_portfolio_dd = current_equity_estimate / 100 * market_drawdown

vol_utilization = estimated_portfolio_vol / target_portfolio_volatility

dd_utilization = estimated_portfolio_dd / max_portfolio_drawdown

risk_utilization = math.max(vol_utilization, dd_utilization)

risk_adjustment_factor = 1.0

if risk_utilization > 1.0

risk_adjustment_factor := math.exp(-0.5 * (risk_utilization - 1.0))

risk_adjustment_factor := math.max(0.5, risk_adjustment_factor)

risk_adjustment_factor

else if risk_utilization < 0.9

risk_adjustment_factor := 1.0 + 0.2 * math.log(1.0 / risk_utilization)

risk_adjustment_factor := math.min(1.3, risk_adjustment_factor)

risk_adjustment_factor

risk_allocation := risk_allocation * risk_adjustment_factor

risk_allocation

else

vol_scalar = target_portfolio_volatility / math.max(market_volatility_20d, 10)

vol_scalar := math.min(1.5, math.max(0.2, vol_scalar))

drawdown_penalty = 0.0

if current_drawdown > max_portfolio_drawdown

drawdown_penalty := (current_drawdown - max_portfolio_drawdown) / max_portfolio_drawdown

drawdown_penalty := math.min(1.0, drawdown_penalty)

drawdown_penalty

risk_allocation := 100 * vol_scalar * (1 - drawdown_penalty)

risk_allocation

risk_allocation := math.max(0, math.min(100, risk_allocation))

// VALUATION ANALYSIS

// Valuation Metrics

actual_pe_ratio = spy_earnings_per_share > 0 ? sp500 / spy_earnings_per_share : spy_pe_forward

actual_earnings_yield = nz(spy_operating_earnings_yield, 0) > 0 ? spy_operating_earnings_yield : 100 / actual_pe_ratio

total_shareholder_yield = spy_dividend_yield + spy_buyback_yield

// Equity Risk Premium (multi-method calculation)

method1_erp = actual_earnings_yield - us10y

method2_erp = actual_earnings_yield + spy_buyback_yield - us10y

payout_ratio = spy_dividend_yield > 0 and actual_earnings_yield > 0 ? spy_dividend_yield / actual_earnings_yield : 0.4

sustainable_growth = spy_return_on_equity * (1 - payout_ratio) / 100

method3_erp = spy_dividend_yield + sustainable_growth * 100 - us10y

implied_growth = spy_revenue_growth * 0.7

method4_erp = total_shareholder_yield + implied_growth - us10y

equity_risk_premium = method1_erp * 0.35 + method2_erp * 0.30 + method3_erp * 0.20 + method4_erp * 0.15

ev_ebitda_ratio = spy_enterprise_value > 0 and spy_ebitda > 0 ? spy_enterprise_value / spy_ebitda : 15.0

debt_equity_health = spy_debt_to_equity < 1.0 ? 1.2 : spy_debt_to_equity < 2.0 ? 1.0 : 0.8

// Valuation Score

base_valuation_score = 50.0

if equity_risk_premium > 4

base_valuation_score := 95

base_valuation_score

else if equity_risk_premium > 3

base_valuation_score := 85

base_valuation_score

else if equity_risk_premium > 2

base_valuation_score := 70

base_valuation_score

else if equity_risk_premium > 1

base_valuation_score := 55

base_valuation_score

else if equity_risk_premium > 0

base_valuation_score := 40

base_valuation_score

else if equity_risk_premium > -1

base_valuation_score := 25

base_valuation_score

else

base_valuation_score := 10

base_valuation_score

growth_adjustment = spy_revenue_growth > 10 ? 10 : spy_revenue_growth > 5 ? 5 : 0

margin_adjustment = spy_net_margin > 15 ? 5 : spy_net_margin < 8 ? -5 : 0

roe_adjustment = spy_return_on_equity > 20 ? 5 : spy_return_on_equity < 10 ? -5 : 0

valuation_score = base_valuation_score + growth_adjustment + margin_adjustment + roe_adjustment

valuation_score := math.max(0, math.min(100, valuation_score * debt_equity_health))

// SENTIMENT ANALYSIS

// VIX Term Structure

vix_term_structure = vix9d > 0 ? vix / vix9d : 1

backwardation = vix_term_structure > 1.05

steep_backwardation = vix_term_structure > 1.15

// Safe Haven Flows

gold_momentum = ta.roc(gold, 20)

dollar_momentum = ta.roc(usd, 20)

yen_momentum = ta.roc(yen, 20)

treasury_momentum = ta.roc(tlt, 20)

safe_haven_flow = gold_momentum * 0.3 + treasury_momentum * 0.3 + dollar_momentum * 0.25 + yen_momentum * 0.15

// Advanced Sentiment Analysis

vix_percentile = ta.percentrank(vix, 252)

vix_zscore = (vix - ta.sma(vix, 252)) / ta.stdev(vix, 252)

vix_momentum = ta.roc(vix, 5)

vvix_proxy = ta.stdev(vix_momentum, 20) * math.sqrt(252)

risk_reversal_proxy = (vix - realized_vol) / realized_vol

// Sentiment Score

base_sentiment = 50.0

vix_adjustment = 0.0

if vix_zscore < -1.5

vix_adjustment := 40

vix_adjustment

else if vix_zscore < -0.5

vix_adjustment := 20

vix_adjustment

else if vix_zscore < 0.5

vix_adjustment := 0

vix_adjustment

else if vix_zscore < 1.5

vix_adjustment := -20

vix_adjustment

else

vix_adjustment := -40

vix_adjustment

term_structure_adjustment = backwardation ? -15 : steep_backwardation ? -30 : 5

vvix_adjustment = vvix_proxy > 2.0 ? -10 : vvix_proxy < 1.0 ? 10 : 0

sentiment_score = base_sentiment + vix_adjustment + term_structure_adjustment + vvix_adjustment

sentiment_score := math.max(0, math.min(100, sentiment_score))

// MACRO ANALYSIS

// Yield Curve

yield_spread_2_10 = us10y - us2y

yield_spread_3m_10 = us10y - us3m

// Credit Conditions

hyg_return = ta.roc(hyg, 20)

lqd_return = ta.roc(lqd, 20)

tlt_return = ta.roc(tlt, 20)

hyg_duration = 4.0

lqd_duration = 8.0

tlt_duration = 17.0

hyg_log_returns = math.log(hyg / hyg )

lqd_log_returns = math.log(lqd / lqd )

hyg_volatility = ta.stdev(hyg_log_returns, 20) * math.sqrt(252)

lqd_volatility = ta.stdev(lqd_log_returns, 20) * math.sqrt(252)

hyg_yield_proxy = -math.log(hyg / hyg ) * 100

lqd_yield_proxy = -math.log(lqd / lqd ) * 100

tlt_yield = us10y

hyg_spread = (hyg_yield_proxy - tlt_yield) * 100

lqd_spread = (lqd_yield_proxy - tlt_yield) * 100

hyg_distance = (hyg - ta.lowest(hyg, 252)) / (ta.highest(hyg, 252) - ta.lowest(hyg, 252))

lqd_distance = (lqd - ta.lowest(lqd, 252)) / (ta.highest(lqd, 252) - ta.lowest(lqd, 252))

default_risk_proxy = 2.0 - (hyg_distance + lqd_distance)

credit_spread = hyg_spread * 0.5 + (hyg_volatility - lqd_volatility) * 1000 * 0.3 + default_risk_proxy * 200 * 0.2

credit_spread := math.max(50, credit_spread)

credit_market_health = hyg_return > lqd_return ? 1 : -1

flight_to_quality = tlt_return > (hyg_return + lqd_return) / 2

// Macro Score

macro_score = 50.0

yield_curve_score = 0

if yield_spread_2_10 > 1.5 and yield_spread_3m_10 > 2

yield_curve_score := 40

yield_curve_score

else if yield_spread_2_10 > 0.5 and yield_spread_3m_10 > 1

yield_curve_score := 30

yield_curve_score

else if yield_spread_2_10 > 0 and yield_spread_3m_10 > 0

yield_curve_score := 20

yield_curve_score

else if yield_spread_2_10 < 0 or yield_spread_3m_10 < 0

yield_curve_score := 10

yield_curve_score

else

yield_curve_score := 5

yield_curve_score

credit_conditions_score = 0

if credit_spread < 200 and not flight_to_quality

credit_conditions_score := 30

credit_conditions_score

else if credit_spread < 400 and credit_market_health > 0

credit_conditions_score := 20

credit_conditions_score

else if credit_spread < 600

credit_conditions_score := 15

credit_conditions_score

else if credit_spread < 1000

credit_conditions_score := 10

credit_conditions_score

else

credit_conditions_score := 0

credit_conditions_score

financial_stability_score = 0

if spy_debt_to_equity < 0.5 and spy_return_on_equity > 15

financial_stability_score := 20

financial_stability_score

else if spy_debt_to_equity < 1.0 and spy_return_on_equity > 10

financial_stability_score := 15

financial_stability_score

else if spy_debt_to_equity < 1.5

financial_stability_score := 10

financial_stability_score

else

financial_stability_score := 5

financial_stability_score

macro_score := yield_curve_score + credit_conditions_score + financial_stability_score

macro_score := math.max(0, math.min(100, macro_score))

// CRISIS DETECTION

crisis_indicators = 0

if vix > crisis_vix_threshold

crisis_indicators := crisis_indicators + 1

crisis_indicators

if vix > 60

crisis_indicators := crisis_indicators + 2

crisis_indicators

if current_drawdown > crisis_drawdown_threshold

crisis_indicators := crisis_indicators + 1

crisis_indicators

if current_drawdown > 25

crisis_indicators := crisis_indicators + 1

crisis_indicators

if credit_spread > crisis_credit_spread

crisis_indicators := crisis_indicators + 1

crisis_indicators

sp500_roc_5 = ta.roc(sp500, 5)

tlt_roc_5 = ta.roc(tlt, 5)

if sp500_roc_5 < -10 and tlt_roc_5 < -5

crisis_indicators := crisis_indicators + 2

crisis_indicators

volume_spike = sp500_volume > ta.sma(sp500_volume, 20) * 2

sp500_roc_1 = ta.roc(sp500, 1)

if volume_spike and sp500_roc_1 < -3

crisis_indicators := crisis_indicators + 1

crisis_indicators

is_crisis = crisis_indicators >= 3

is_severe_crisis = crisis_indicators >= 5

// FINAL ALLOCATION CALCULATION

// Convert regime to base allocation

regime_allocation = market_regime == 'Strong Bull' ? 100 : market_regime == 'Bull Market' ? 80 : market_regime == 'Neutral' ? 60 : market_regime == 'Correction' ? 40 : market_regime == 'Bear Market' ? 20 : 0

// Normalize weights

total_weight = w_regime + w_risk + w_valuation + w_sentiment + w_macro

w_regime_norm = w_regime / total_weight

w_risk_norm = w_risk / total_weight

w_valuation_norm = w_valuation / total_weight

w_sentiment_norm = w_sentiment / total_weight

w_macro_norm = w_macro / total_weight

// Calculate Weighted Allocation

weighted_allocation = regime_allocation * w_regime_norm + risk_allocation * w_risk_norm + valuation_score * w_valuation_norm + sentiment_score * w_sentiment_norm + macro_score * w_macro_norm

// Apply Crisis Override

if use_crisis_detection

if is_severe_crisis

weighted_allocation := math.min(weighted_allocation, 10)

weighted_allocation

else if is_crisis

weighted_allocation := math.min(weighted_allocation, 25)

weighted_allocation

// Model Type Adjustment

model_adjustment = 0.0

if model_type == 'Conservative'

model_adjustment := -10

model_adjustment

else if model_type == 'Aggressive'

model_adjustment := 10

model_adjustment

else if model_type == 'Adaptive'

recent_return = (sp500 - sp500 ) / sp500 * 100

if recent_return > 5

model_adjustment := 5

model_adjustment

else if recent_return < -5

model_adjustment := -5

model_adjustment

// Apply adjustment and bounds

final_allocation = weighted_allocation + model_adjustment

final_allocation := math.max(0, math.min(100, final_allocation))

// Smooth allocation

smoothed_allocation = ta.sma(final_allocation, smoothing_period)

// Calculate portfolio risk metrics (only for internal alerts)

actual_portfolio_volatility = smoothed_allocation / 100 * market_volatility_20d

actual_portfolio_drawdown = smoothed_allocation / 100 * current_drawdown

// VISUALIZATION

// Color definitions

var color primary_color = #2196F3

var color bullish_color = #4CAF50

var color bearish_color = #FF5252

var color neutral_color = #808080

var color text_color = color.white

var color bg_color = #000000

var color table_bg_color = #1E1E1E

var color header_bg_color = #2D2D2D

switch color_scheme // Apply color scheme

'Gold' =>

primary_color := use_dark_mode ? #FFD700 : #DAA520

bullish_color := use_dark_mode ? #FFA500 : #FF8C00

bearish_color := use_dark_mode ? #FF5252 : #D32F2F

neutral_color := use_dark_mode ? #C0C0C0 : #808080

text_color := use_dark_mode ? color.white : color.black

bg_color := use_dark_mode ? #000000 : #FFFFFF

table_bg_color := use_dark_mode ? #1A1A00 : #FFFEF0

header_bg_color := use_dark_mode ? #2D2600 : #F5F5DC

header_bg_color

'EdgeTools' =>

primary_color := use_dark_mode ? #4682B4 : #1E90FF

bullish_color := use_dark_mode ? #4CAF50 : #388E3C

bearish_color := use_dark_mode ? #FF5252 : #D32F2F

neutral_color := use_dark_mode ? #708090 : #696969

text_color := use_dark_mode ? color.white : color.black

bg_color := use_dark_mode ? #000000 : #FFFFFF

table_bg_color := use_dark_mode ? #0F1419 : #F0F8FF

header_bg_color := use_dark_mode ? #1E2A3A : #E6F3FF

header_bg_color

'Behavioral' =>

primary_color := #808080

bullish_color := #00FF00

bearish_color := #8B0000

neutral_color := #FFBF00

text_color := use_dark_mode ? color.white : color.black

bg_color := use_dark_mode ? #000000 : #FFFFFF

table_bg_color := use_dark_mode ? #1A1A1A : #F8F8F8

header_bg_color := use_dark_mode ? #2D2D2D : #E8E8E8

header_bg_color

'Quant' =>

primary_color := #808080

bullish_color := #FFA500

bearish_color := #8B0000

neutral_color := #4682B4

text_color := use_dark_mode ? color.white : color.black

bg_color := use_dark_mode ? #000000 : #FFFFFF

table_bg_color := use_dark_mode ? #0D0D0D : #FAFAFA

header_bg_color := use_dark_mode ? #1A1A1A : #F0F0F0

header_bg_color

'Ocean' =>

primary_color := use_dark_mode ? #20B2AA : #008B8B

bullish_color := use_dark_mode ? #00CED1 : #4682B4

bearish_color := use_dark_mode ? #FF4500 : #B22222

neutral_color := use_dark_mode ? #87CEEB : #2F4F4F

text_color := use_dark_mode ? #F0F8FF : #191970

bg_color := use_dark_mode ? #001F3F : #F0F8FF

table_bg_color := use_dark_mode ? #001A2E : #E6F7FF

header_bg_color := use_dark_mode ? #002A47 : #CCF2FF

header_bg_color

'Fire' =>

primary_color := use_dark_mode ? #FF6347 : #DC143C

bullish_color := use_dark_mode ? #FFD700 : #FF8C00

bearish_color := use_dark_mode ? #8B0000 : #800000

neutral_color := use_dark_mode ? #FFA500 : #CD853F

text_color := use_dark_mode ? #FFFAF0 : #2F1B14

bg_color := use_dark_mode ? #2F1B14 : #FFFAF0

table_bg_color := use_dark_mode ? #261611 : #FFF8F0

header_bg_color := use_dark_mode ? #3D241A : #FFE4CC

header_bg_color

'Matrix' =>

primary_color := use_dark_mode ? #00FF41 : #006400

bullish_color := use_dark_mode ? #39FF14 : #228B22

bearish_color := use_dark_mode ? #FF073A : #8B0000

neutral_color := use_dark_mode ? #00FFFF : #008B8B

text_color := use_dark_mode ? #C0FF8C : #003300

bg_color := use_dark_mode ? #0D1B0D : #F0FFF0

table_bg_color := use_dark_mode ? #0A1A0A : #E8FFF0

header_bg_color := use_dark_mode ? #112B11 : #CCFFCC

header_bg_color

'Arctic' =>

primary_color := use_dark_mode ? #87CEFA : #4169E1

bullish_color := use_dark_mode ? #00BFFF : #0000CD

bearish_color := use_dark_mode ? #FF1493 : #8B008B

neutral_color := use_dark_mode ? #B0E0E6 : #483D8B

text_color := use_dark_mode ? #F8F8FF : #191970

bg_color := use_dark_mode ? #191970 : #F8F8FF

table_bg_color := use_dark_mode ? #141B47 : #F0F8FF

header_bg_color := use_dark_mode ? #1E2A5C : #E0F0FF

header_bg_color

// Transparency settings

bg_transparency = use_dark_mode ? 85 : 92

zone_transparency = use_dark_mode ? 90 : 95

band_transparency = use_dark_mode ? 70 : 85

table_transparency = use_dark_mode ? 80 : 15

// Allocation color

alloc_color = smoothed_allocation >= 80 ? bullish_color : smoothed_allocation >= 60 ? color.new(bullish_color, 30) : smoothed_allocation >= 40 ? primary_color : smoothed_allocation >= 20 ? color.new(bearish_color, 30) : bearish_color

// Dynamic background

var color dynamic_bg_color = na

if show_regime_background

if smoothed_allocation >= 70

dynamic_bg_color := color.new(bullish_color, background_intensity)

dynamic_bg_color

else if smoothed_allocation <= 30

dynamic_bg_color := color.new(bearish_color, background_intensity)

dynamic_bg_color

else if smoothed_allocation > 60 or smoothed_allocation < 40

dynamic_bg_color := color.new(primary_color, math.min(99, background_intensity + 2))

dynamic_bg_color

bgcolor(dynamic_bg_color, title = 'Allocation Signal Background')

// Plot main allocation line

plot(smoothed_allocation, 'Equity Allocation %', color = alloc_color, linewidth = math.max(1, main_line_width))

// Reference lines (static colors for hline)

hline_bullish_color = color_scheme == 'Gold' ? use_dark_mode ? #FFA500 : #FF8C00 : color_scheme == 'EdgeTools' ? use_dark_mode ? #4CAF50 : #388E3C : color_scheme == 'Behavioral' ? #00FF00 : color_scheme == 'Quant' ? #FFA500 : color_scheme == 'Ocean' ? use_dark_mode ? #00CED1 : #4682B4 : color_scheme == 'Fire' ? use_dark_mode ? #FFD700 : #FF8C00 : color_scheme == 'Matrix' ? use_dark_mode ? #39FF14 : #228B22 : color_scheme == 'Arctic' ? use_dark_mode ? #00BFFF : #0000CD : #4CAF50

hline_bearish_color = color_scheme == 'Gold' ? use_dark_mode ? #FF5252 : #D32F2F : color_scheme == 'EdgeTools' ? use_dark_mode ? #FF5252 : #D32F2F : color_scheme == 'Behavioral' ? #8B0000 : color_scheme == 'Quant' ? #8B0000 : color_scheme == 'Ocean' ? use_dark_mode ? #FF4500 : #B22222 : color_scheme == 'Fire' ? use_dark_mode ? #8B0000 : #800000 : color_scheme == 'Matrix' ? use_dark_mode ? #FF073A : #8B0000 : color_scheme == 'Arctic' ? use_dark_mode ? #FF1493 : #8B008B : #FF5252

hline_primary_color = color_scheme == 'Gold' ? use_dark_mode ? #FFD700 : #DAA520 : color_scheme == 'EdgeTools' ? use_dark_mode ? #4682B4 : #1E90FF : color_scheme == 'Behavioral' ? #808080 : color_scheme == 'Quant' ? #808080 : color_scheme == 'Ocean' ? use_dark_mode ? #20B2AA : #008B8B : color_scheme == 'Fire' ? use_dark_mode ? #FF6347 : #DC143C : color_scheme == 'Matrix' ? use_dark_mode ? #00FF41 : #006400 : color_scheme == 'Arctic' ? use_dark_mode ? #87CEFA : #4169E1 : #2196F3

hline(show_reference_lines ? 100 : na, '100% Equity', color = color.new(hline_bullish_color, 70), linestyle = hline.style_dotted, linewidth = 1)

hline(show_reference_lines ? 80 : na, '80% Equity', color = color.new(hline_bullish_color, 40), linestyle = hline.style_dashed, linewidth = 1)

hline(show_reference_lines ? 60 : na, '60% Equity', color = color.new(hline_bullish_color, 60), linestyle = hline.style_dotted, linewidth = 1)

hline(50, '50% Balanced', color = color.new(hline_primary_color, 50), linestyle = hline.style_solid, linewidth = 2)

hline(show_reference_lines ? 40 : na, '40% Equity', color = color.new(hline_bearish_color, 60), linestyle = hline.style_dotted, linewidth = 1)

hline(show_reference_lines ? 20 : na, '20% Equity', color = color.new(hline_bearish_color, 40), linestyle = hline.style_dashed, linewidth = 1)

hline(show_reference_lines ? 0 : na, '0% Equity', color = color.new(hline_bearish_color, 70), linestyle = hline.style_dotted, linewidth = 1)

// Component plots

plot(show_components ? regime_allocation : na, 'Regime', color = color.new(#4ECDC4, 70), linewidth = 1)

plot(show_components ? risk_allocation : na, 'Risk', color = color.new(#FF6B6B, 70), linewidth = 1)

plot(show_components ? valuation_score : na, 'Valuation', color = color.new(#45B7D1, 70), linewidth = 1)

plot(show_components ? sentiment_score : na, 'Sentiment', color = color.new(#FFD93D, 70), linewidth = 1)

plot(show_components ? macro_score : na, 'Macro', color = color.new(#6BCF7F, 70), linewidth = 1)

// Confidence bands

upper_band = plot(show_confidence_bands ? math.min(100, smoothed_allocation + ta.stdev(smoothed_allocation, 20)) : na, color = color.new(neutral_color, band_transparency), display = display.none, title = 'Upper Band')

lower_band = plot(show_confidence_bands ? math.max(0, smoothed_allocation - ta.stdev(smoothed_allocation, 20)) : na, color = color.new(neutral_color, band_transparency), display = display.none, title = 'Lower Band')

fill(upper_band, lower_band, color = show_confidence_bands ? color.new(neutral_color, zone_transparency) : na, title = 'Uncertainty')

// DASHBOARD

if show_dashboard and barstate.islast

var table dashboard = table.new(position.top_right, 2, 20, border_width = 1, bgcolor = color.new(table_bg_color, table_transparency))

table.clear(dashboard, 0, 0, 1, 19)

// Header

header_color = color.new(header_bg_color, 20)

dashboard_text_color = text_color

table.cell(dashboard, 0, 0, 'DEAM', text_color = dashboard_text_color, bgcolor = header_color, text_size = size.normal)

table.cell(dashboard, 1, 0, model_type, text_color = dashboard_text_color, bgcolor = header_color, text_size = size.normal)

// Core metrics