Inside Bar SetupScript Details

- This script plots Inside Bar for given day in selected time-frame (applicable only for Timeframes < Day)

- Basis plotted inside bar, relevant targets are marked on the chart

- Targets can be customised from script settings. Example, if range of mother candle is 10 points, then T1 is 10 * x above/below mother candle and T2 is 10 * y above/below mother candle. This x & y are configured via script settings

How to use this script ?

- This script works well on 10-15 mins timeframe for stocks, 15/30 mins timeframe for nifty index and 30/60 mins time frame for bank nifty index

- If mother candle high is broken, take long trade with SL of mother candle low and if low is broken, take short trade with SL of mother candle high

Remember:

1. Above logic is to be combined with support/resistances i.e. price action. This script is an add-on to price action analysis giving you more conviction.

2. If range of mother candle is very high, it is recommended to avoid the trade.

3. Basis inside bar formed on higher time frame, take trade on basis of lower time frame i.e if inside bar is formed on 60 mins, take trade on the basis of 10-15 mins time frame

Example:

1. As seen in the chart, Nifty is near it's resistance and we are seeing Inside Bar being formed, In such scenario, even if High of Mother Candle is broken, we should be more interested to short as we are near resistance and probability of getting our targets in long side is less.

2. So, if I see breakdown of mother candle i.e. price going below low of mother candle, we will short with SL of high of mother candle.

3. As seen in the chart, both the targets are achieved.

Additional Info:

1. Targets on Long/Short Side can be configured via settings. For indices 1 times/1.5 times the range works well.

2. This script plots targets basis the first inside bar formed in the day for selected time frame.

3. Inside bars formed through out the day are coloured separately but lines are plotted only on the basis of 1st formed inside bar as this strategy works well for the first formed inside bar)

4. Don't forget to check volume in case of breakout/breakdown.

Note:

1. Mother Candle - First Candle of Inside Bar

2. Child Candle - Candle formed inside Mother Candle (Second Candle of Inside Bar)

Happy Trading :)

חפש סקריפטים עבור "股价站上60月线"

VIDYA Trend StrategyOne of the most common messages I get is people reaching out asking for quantitative strategies that trade cryptocurrency. This has compelled me to write this script and article, to help provide a quantitative/technical perspective on why I believe most strategies people write for crypto fail catastrophically, and how one might build measures within their strategies that help reduce the risk of that happening. For those that don't trade crypto, know that these approaches are applicable to any market.

I will start off by qualifying up that I mainly trade stocks and ETFs, and I believe that if you trade crypto, you should only be playing with money you are okay with losing. Most published crypto strategies I have seen "work" when the market is going up, and fail catastrophically when it is not. There are far more people trying to sell you a strategy than there are people providing 5-10+ year backtest results on their strategies, with slippage and commissions included, showing how they generated alpha and beat buy/hold. I understand that this community has some really talented people that can create some really awesome things, but I am saying that the vast majority of what you find on the internet will not be strategies that create alpha over the long term.

So, why do so many of these strategies fail?

There is an assumption many people make that cryptocurrency will act just like stocks and ETFs, and it does not. ETF returns have more of a Gaussian probability distribution. Because of this, ETFs have a short term mean reverting behavior that can be capitalized on consistently. Many technical indicators are built to take advantage of this on the equities market. Many people apply them to crypto. Many of those people are drawn down 60-70% right now while there are mean reversion strategies up YTD on equities, even though the equities market is down. Crypto has many more "tail events" that occur 3-4+ standard deviations from the mean.

There is a correlation in many equities and ETF markets for how long an asset continues to do well when it is currently doing well. This is known as momentum, and that correlation and time-horizon is different for different assets. Many technical indicators are built based on this behavior, and then people apply them to cryptocurrency with little risk management assuming they behave the same and and on the same time horizon, without pulling in the statistics to verify if that is actually the case. They do not.

People do not take into account the brokerage commissions and slippage. Brokerage commissions are particularly high with cryptocurrency. The irony here isn't lost to me. When you factor in trading costs, it blows up most short-term trading strategies that might otherwise look profitable.

There is an assumption that it will "always come back" and that you "HODL" through the crash and "buy more." This is why Three Arrows Capital, a $10 billion dollar crypto hedge fund is now in bankruptcy, and no one can find the owners. This is also why many that trade crypto are drawn down 60-70% right now. There are bad risk practices in place, like thinking the martingale gambling strategy is the same as dollar cost averaging while also using those terms interchangeably. They are not the same. The 1st will blow up your trade account, and the 2nd will reduce timing risk. Many people are systematically blowing up their trade accounts/strategies by using martingale and calling it dollar cost averaging. The more risk you are exposing yourself too, the more important your risk management strategy is.

There is an odd assumption some have that you can buy anything and win with technical/quantitative analysis. Technical analysis does not tell you what you should buy, it just tells you when. If you are running a strategy that is going long on an asset that lost 80% of its value in the last year, then your strategy is probably down. That same strategy might be up on a different asset. One might consider a different methodology on choosing assets to trade.

Lastly, most strategies are over-fit, or curve-fit. The more complicated and more parameters/settings you have in your model, the more likely it is just fit to historical data and will not perform similar in live trading. This is one of the reasons why I like simple models with few parameters. They are less likely to be over-fit to historical data. If the strategy only works with 1 set of parameters, and there isn't a range of parameters around it that create alpha, then your strategy is over-fit and is probably not suitable for live trading.

So, what can I do about all of this!?

I created the VIDYA Trend Strategy to provide an example of how one might create a basic model with a basic risk management strategy that might generate long term alpha on a volatile asset, like cryptocurrency. This is one (of many) risk management strategies that can reduce the volatility of your returns when trading any asset. I chose the Variable Index Dynamic Average (VIDYA) for this example because it's calculation filters out some market noise by taking into account the volatility of the underlying asset. I chose a trend following strategy because regressions are capturing behaviors that are not just specific to the equities market.

The more volatile an asset, the more you have to back-off the short term price movement to effectively trend-follow it. Otherwise, you are constantly buying into short term trends that don't represent the trend of the asset, then they reverse and loose money. This is why I am applying a trend following strategy to a 4 hour chart and not a 4 minute chart. It is also important to note that following these long term trends on a volatile asset exposes you to additional risk. So, how might one mitigate some of that risk?

One of the ways of reducing timing risk is scaling into a trade. This is different from "doubling down" or "trippling down." It is really a basic application of dollar cost averaging to reduce timing risk, although DCA would typically happen over a longer time period. If it is really a trend you are following, it will probably still be a trend tomorrow. Trend following strategies have lower win rates because the beginning of a trend often reverses. The more volatile the asset, the more likely that is to happen. However, we can reduce risk of buying into a reversal by slowly scaling into the trend with a small % of equity per trade.

Our example "VIDYA Trend Strategy" executes this by looking at a medium-term, volatility adjusted trend on a 4 hour chart. The script scales into it with 4% of the account equity every 4-hours that the trend is still up. This means you become fully invested after 25 trades/bars. It also means that early in the trade, when you might be more likely to experience a reversal, most of your account equity is not invested and those losses are much smaller. The script sells 100% of the position when it detects a trend reversal. The slower you scale into a trade, the less volatile your equity curve will be. This model also includes slippage and commissions that you can adjust under the "settings" menu.

This fundamental concept of reducing timing risk by scaling into a trade can be applied to any market.

Disclaimer: This is not financial advice. Open-source scripts I publish in the community are largely meant to spark ideas that can be used as building blocks for part of a more robust trade management strategy. If you would like to implement a version of any script, I would recommend making significant additions/modifications to the strategy & risk management functions. If you don’t know how to program in Pine, then hire a Pine-coder. We can help!

Cipher Twister - Long and ShortINTRO / NOTES:

This script is based on Market Cipher B Oscillator by Falcon

The difference in this script is that only the useful points are printed on the indicator, namely Long and Short Trade Execution signals to be used by a bot, namely the PT Bot.

The script also differs from the original that it has been upgraded to Pinescript v4

This oscillator can be used with ALL time frames, but generally works the best on 15 minute and 1 hour charts on ANY market, no matter, stock, forex, crypto, spot, futures, derivatives, Nasdaq etc...

DEFINITIONS:

This oscillator forms the foundation of Buy and Exit of Long and Short Trades.

There are 2 'Red' Lines at the top of the channel and 2 Green Lines at the bottom of the channel.

These two channels are set at default to be +53 / -53 and +60 / -60 respectively. These two lines will serve as the threshold point if one is to make cautious trades only.

There is a center line which divides the Oscillator into two parts. Above the center line, the market is in over bought territory and Below the center line is in over sold territory.

'Red' dots are drawn by the indicator to represent a potential Short (or a signal to exit from a Long position)

'Green' dots are drawn by the indicator to represent a potential Long (or a signal to exit from a Short position)

The 'Red' and 'Green' dots are draw when a Cross between both wt1 & wt2 cross, thus providing a fantastic indication of potential trend reversal and entry/exit of a position.

STRATEGY NOTES:

The strategy to use this indicator with for realistic and proper results would be to use it with an automated Trading Bot such as Profit Trailer (PT-BOT)

You could use this strategy manually, however it would mean you would need to sit in front of the screen all day and night long and activate the trades immediately after the 'red'/'green' dots are drawn. Usually this will result in non-optimal entries and exits as well as loss on various instances when a 'red' and 'green' dot are printed close together (which is usually when the market goes into correction/consolidation) and slow entries/exits will result in a loss rather than a small profit or exit at BE (Break Even)

ACTUAL STRATEGY (For use with automated bot)

To be used in conjunction with Heikin Ashi Candles for added cautionary measures

For LONGs ONLY

--------------------

1/ When 'Green' dot is drawn, ACTIVATE Long Position

(Use 1.5% Risk Management for each trade)

(Use Lot size based on 1.5% risk management and xLeverage (if any))

2/ Make sure bot Opens an SL (Stop Loss) value based on 1.5% Risk Management

3/ When 'Red' dot is drawn, CLOSE Long Position.

*If you want to add extra caution to your trade, only activate the trade if the 'Green' dot is BELOW the 'Green' Markers

*For added caution, use color coded Heikin Ashi candles to 'confirm' Activation and Closing of a trade in the bot configuration

---------------------------------------------------------------------------------------------------

For SHORTs ONLY

--------------------

1/ When 'Red' dot is drawn, ACTIVATE Short Position

(Use 1.5% Risk Management for each trade)

(Use Lot size based on 1.5% risk management and xLeverage (if any))

2/ Make sure bot Opens an SL (Stop Loss) value based on 1.5% Risk Management

3/ When 'Green' dot is drawn, CLOSE Short Position

*If you want to add extra caution to your trade, only activate the trade if the 'Red' dot is Above the Red Markers

*For added caution, use color coded Heikin Ashi candles to 'confirm' Activation and Closing of a trade in the bot configuration

---------------------------------------------------------------------------------------------------

Supplementary Notes:

Make sure that your bot configuration will only activate ONE TRADE when the 'Green'/'Red' dot appears.

Occasionally during high volatility , 'red'/'green' dots will appear intermittently before remaining drawn, thus the oscillator 'redraws' the dots during market movement.

There will be times where occasionally a 'green' dot or a 'red' dot will appear, the trade will be opened, but the trade will fail due to the market manipulation (algorithm/market maker bots/fake volume etc), to wipe out those trading on derivatives and futures markets using leverage. Do not worry about this, no bot can make 100% wins, no strategy will achieve 100% win ratio and one necessarily doesn't need a high win ratio when using strict money management practices with your trading for SL and lot size.

If you use this method, you will see great results, but again I must stress, using this method with a fully automated bot is the only way to achieve proper results.

Weighted Relative Strength IndexWRSI uses 3 different user defined time frames with user defined weight on each time frame to give a final RSI value

Default values:

RSI 1 = 5 minute timeframe with a weightage of 9:14

RSI 2 = 15 minute timeframe with a weightage of 4:14

RSI 1 = 60 minute timeframe with a weightage of 1:14

Works best on a 15 min chart.

Please note this indicator will show exactly same values on all time frame charts so if you are looking at a daily chart you may want to change to 60 min, Daily & Weekly RSI time frame in settings.

The weights used here are basically sqaures of 1,2,& 3, you may choose any numbers that work for you.

The RSI length taken here is 27 (count of nakshatras)

The RSI MA length taken here is 28 (count of nakshatras + Abhijit Nakshatra)

You can obviously change it to what works best for you.

MME MTF CCIHi All,

This is a Dual/Multi TF CCI script to be used for Intraday as well as positional system.

Intraday:

Chart TF : 5 mins

Underlying Trend CCI : CCI 34 of 30 mins TF

Immediate Trend CCI : CCI 34 of 5 mins TF

Execution CCI : CCI 8 of 5 mins TF

The CCIs are used for entry, exit during momentum breakouts or pullbacks.

General Long Setup:

Buy at CCI-8 5m below -135, when CCI-34 30 mins is > +100. Long exit when CCI 34 5 min < -60

General Short Setup:

Sell at CCI-8 5m above -135, when CCI-34 30 mins is < -100. Short exit when CCI 34 5 min > +60

The same CCI settings can be used for positional or investment per appropriate timeframes one is interested to trade, along with HTF above in ratio 1:5.

Hope its helpful!

Time█ OVERVIEW

This library is a Pine Script™ programmer’s tool containing a variety of time related functions to calculate or measure time, or format time into string variables.

█ CONCEPTS

`formattedTime()`, `formattedDate()` and `formattedDay()`

Pine Script™, like many other programming languages, uses timestamps in UNIX format, expressed as the number of milliseconds elapsed since 00:00:00 UTC, 1 January 1970. These three functions convert a UNIX timestamp to a formatted string for human consumption.

These are examples of ways you can call the functions, and the ensuing results:

CODE RESULT

formattedTime(timenow) >>> "00:40:35"

formattedTime(timenow, "short") >>> "12:40 AM"

formattedTime(timenow, "full") >>> "12:40:35 AM UTC"

formattedTime(1000 * 60 * 60 * 3.5, "HH:mm") >>> "03:30"

formattedDate(timenow, "short") >>> "4/30/22"

formattedDate(timenow, "medium") >>> "Apr 30, 2022"

formattedDate(timenow, "full") >>> "Saturday, April 30, 2022"

formattedDay(timenow, "E") >>> "Sat"

formattedDay(timenow, "dd.MM.yy") >>> "30.04.22"

formattedDay(timenow, "yyyy.MM.dd G 'at' hh:mm:ss z") >>> "2022.04.30 AD at 12:40:35 UTC"

These functions use str.format() and some of the special formatting codes it allows for. Pine Script™ documentation does not yet contain complete specifications on these codes, but in the meantime you can find some information in the The Java™ Tutorials and in Java documentation of its MessageFormat class . Note that str.format() implements only a subset of the MessageFormat features in Java.

`secondsSince()`

The introduction of varip variables in Pine Script™ has made it possible to track the time for which a condition is true when a script is executing on a realtime bar. One obvious use case that comes to mind is to enable trades to exit only when the exit condition has been true for a period of time, whether that period is shorter that the chart's timeframe, or spans across multiple realtime bars.

For more information on this function and varip please see our Using `varip` variables publication.

`timeFrom( )`

When plotting lines , boxes , and labels one often needs to calculate an offset for past or future end points relative to the time a condition or point occurs in history. Using xloc.bar_index is often the easiest solution, but some situations require the use of xloc.bar_time . We introduce `timeFrom()` to assist in calculating time-based offsets. The function calculates a timestamp using a negative (into the past) or positive (into the future) offset from the current bar's starting or closing time, or from the current time of day. The offset can be expressed in units of chart timeframe, or in seconds, minutes, hours, days, months or years. This function was ported from our Time Offset Calculation Framework .

`formattedNoOfPeriods()` and `secondsToTfString()`

Our final two offerings aim to confront two remaining issues:

How much time is represented in a given timestamp?

How can I produce a "simple string" timeframe usable with request.security() from a timeframe expressed in seconds?

`formattedNoOfPeriods()` converts a time value in ms to a quantity of time units. This is useful for calculating a difference in time between 2 points and converting to a desired number of units of time. If no unit is supplied, the function automatically chooses a unit based on a predetermined time step.

`secondsToTfString()` converts an input time in seconds to a target timeframe string in timeframe.period string format. This is useful for implementing stepped timeframes relative to the chart time, or calculating multiples of a given chart timeframe. Results from this function are in simple form, which means they are useable as `timeframe` arguments in functions like request.security() .

█ NOTES

Although the example code is commented in detail, the size of the library justifies some further explanation as many concepts are demonstrated. Key points are as follows:

• Pivot points are used to draw lines from. `timeFrom( )` calculates the length of the lines in the specified unit of time.

By default the script uses 20 units of the charts timeframe. Example: a 1hr chart has arrows 20 hours in length.

• At the point of the arrows `formattedNoOfPeriods()` calculates the line length in the specified unit of time from the input menu.

If “Use Input Time” is disabled, a unit of time is automatically assigned.

• At each pivot point a label with a formatted date or time is placed with one of the three formatting helper functions to display the time or date the pivot occurred.

• A label on the last bar showcases `secondsSince()` . The label goes through three stages of detection for a timed alert.

If the difference between the high and the open in ticks exceeds the input value, a timer starts and will turn the label red once the input time is exceeded to simulate a time-delayed alert.

• In the bottom right of the screen `secondsToTfString()` posts the chart timeframe in a table. This can be multiplied from the input menu.

Look first. Then leap.

█ FUNCTIONS

formattedTime(timeInMs, format)

Converts a UNIX timestamp (in milliseconds) to a formatted time string.

Parameters:

timeInMs : (series float) Timestamp to be formatted.

format : (series string) Format for the time. Optional. The default value is "HH:mm:ss".

Returns: (string) A string containing the formatted time.

formattedDate(timeInMs, format)

Converts a UNIX timestamp (in milliseconds) to a formatted date string.

Parameters:

timeInMs : (series float) Timestamp to be formatted.

format : (series string) Format for the date. Optional. The default value is "yyyy-MM-dd".

Returns: (string) A string containing the formatted date.

formattedDay(timeInMs, format)

Converts a UNIX timestamp (in milliseconds) to the name of the day of the week.

Parameters:

timeInMs : (series float) Timestamp to be formatted.

format : (series string) Format for the day of the week. Optional. The default value is "EEEE" (complete day name).

Returns: (string) A string containing the day of the week.

secondsSince(cond, resetCond)

The duration in milliseconds that a condition has been true.

Parameters:

cond : (series bool) Condition to time.

resetCond : (series bool) When `true`, the duration resets.

Returns: The duration in seconds for which `cond` is continuously true.

timeFrom(from, qty, units)

Calculates a +/- time offset in variable units from the current bar's time or from the current time.

Parameters:

from : (series string) Starting time from where the offset is calculated: "bar" to start from the bar's starting time, "close" to start from the bar's closing time, "now" to start from the current time.

qty : (series int) The +/- qty of units of offset required. A "series float" can be used but it will be cast to a "series int".

units : (series string) String containing one of the seven allowed time units: "chart" (chart's timeframe), "seconds", "minutes", "hours", "days", "months", "years".

Returns: (int) The resultant time offset `from` the `qty` of time in the specified `units`.

formattedNoOfPeriods(ms, unit)

Converts a time value in ms to a quantity of time units.

Parameters:

ms : (series int) Value of time to be formatted.

unit : (series string) The target unit of time measurement. Options are "seconds", "minutes", "hours", "days", "weeks", "months". If not used one will be automatically assigned.

Returns: (string) A formatted string from the number of `ms` in the specified `unit` of time measurement

secondsToTfString(tfInSeconds, mult)

Convert an input time in seconds to target string TF in `timeframe.period` string format.

Parameters:

tfInSeconds : (simple int) a timeframe in seconds to convert to a string.

mult : (simple float) Multiple of `tfInSeconds` to be calculated. Optional. 1 (no multiplier) is default.

Returns: (string) The `tfInSeconds` in `timeframe.period` format usable with `request.security()`.

JaeRSI+What is JaeRSI++

🥇 It is an indicator that detects and displays the RSI of the upper frame one step at a time

- It is no different from normal RSI but, u can see the RSI of the upper frame together

- Works based on 5m 15m 1h 4h 1d 1w

🥇Also, if the RSI is (over 70↗️) or (less than 30↘️), changes the background color

- If the background color is continuous, it is recommended to check the frame one step higher

🥇 Meaning of table (table)

- "🌈", RSI, Main, Danger in order

- RSI: It is divided into 5, 15, 60, 240 and indicates the current RSI of each frame (the background color is different from RSI : 33.0 below / 67.0 above)

- Main: Estimate the mainframe

If the previous 14 candles have entered the Danger zone (RSI : below 33.0 / above 67.0) or oversold/number, the corresponding frame is marked as the main frame.

- Danger: If abnormal RSI motion is detected (beam shape) due to sudden surge/fall in a frame, it warns that the frame may be the main frame.

==================================================================================

JaeRSI++란?

🥇 상위 프레임의 RSI를 추가로 표시해 주는 RSI 지표입니다

- 일반 RSI와 알고리즘의 차이가 없으나 상위 프레임의 RSI를 함께 볼 수 있습니다 (빨간 선으로 표시)

- 5m 15m 1h 4h 1d 1w 기준으로 작동합니다

🥇또한 RSI가 (70 이상↗️) 또는 (30↘️)인 경우 배경색을 변경합니다

- 배경색이 연속적인 경우 프레임을 한 단계 높게 확인하는 것이 좋습니다

🥇표(테이블)의 의미

- 순서대로 시간프레임 , RSI , 메인 , 위험

- RSI : 5, 15, 60, 240으로 나뉘어져 각각 프레임의 현재 RSI를 나타낸다 (33.0 아래 / 67.0 위 부터 배경색이 달라짐)

- 메인 : 메인프레임을 추정한다

이전 14개 캔들안에 꺵판존(33.0 아래 / 67.0 위) or 과매도/수에 들어간 적이 있다면 해당 프레임을 메인프레임으로 표시한다

- 위험 : 어떤 프레임에서 급등/급락하여 비 정상적인 RSI의 움직임이 감지된다면(빔 형태) 해당 프레임이 메인 프레임일 수 있다고 경고한다

RSI Swing Trading Setup (2-Period)A simple script that adjusts the RSI visibly in order to better accommodate swing trading and certain swing trading setups/strategies.

--------------------------------------------------------------------------------------------------------------------------------------------------------

Best used in conjunction with "Linear Regression Channel by LonesomeTheBlue" with 2.2σ (std.dev) and Show Fib Levels.

^Click image for a redirect to that script.

--------------------------------------------------------------------------------------------------------------------------------------------------------

In certain price action patterns:

A bearish reversal from a previously bullish move can indicate tops of a rally if the RSI moves from 0-40 to 60 (1)

A bullish reversal from a previously bearish move can indicate bottoms of a pullback if the RSI moves from 60-100 to 40 (2)

(USE THE LINEAR REGRESSION CHANNEL TO VALIDIFY THE RETRACEMENTS)

--------------------------------------------------------------------------------------------------------------------------------------------------------

(1)

--------------------------------------------------------------------------------------------------------------------------------------------------------

(2)

--------------------------------------------------------------------------------------------------------------------------------------------------------

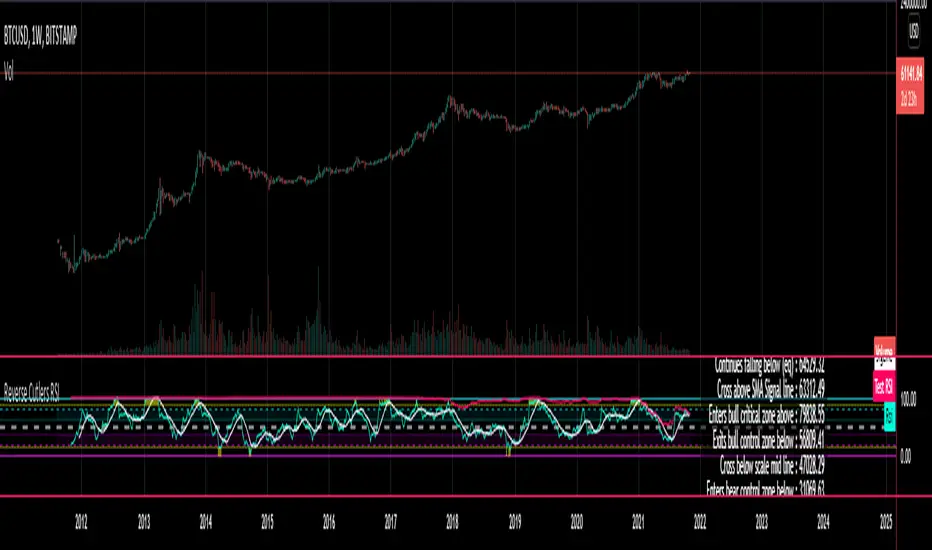

Reverse Cutlers Relative Strength Index On ChartIntroduction

The Reverse Cutlers Relative Strength Index (RCRSI) OC is an indicator which tells the user what price is required to give a particular Cutlers Relative Strength Index ( RSI ) value, or cross its Moving Average (MA) signal line.

Overview

Background & Credits:

The relative strength index ( RSI ) is a momentum indicator used in technical analysis that was originally developed by J. Welles Wilder Jr. and introduced in his seminal 1978 book, “New Concepts in Technical Trading Systems.”.

Cutler created a variation of the RSI known as “Cutlers RSI” using a different formulation to avoid an inherent accuracy problem which arises when using Wilders method of smoothing.

Further developments in the use, and more nuanced interpretations of the RSI have been developed by Cardwell, and also by well-known chartered market technician, Constance Brown C.M.T., in her acclaimed book "Technical Analysis for the Trading Professional” 1999 where she described the idea of bull and bear market ranges for RSI , and while she did not actually reveal the formulas, she introduced the concept of “reverse engineering” the RSI to give price level outputs.

Renowned financial software developer, co-author of academic books on finance, and scientific fellow to the Department of Finance and Insurance at the Technological Educational Institute of Crete, Giorgos Siligardos PHD . brought a new perspective to Wilder’s RSI when he published his excellent and well-received articles "Reverse Engineering RSI " and "Reverse Engineering RSI II " in the June 2003, and August 2003 issues of Stocks & Commodities magazine, where he described his methods of reverse engineering Wilders RSI .

Several excellent Implementations of the Reverse Wilders Relative Strength Index have been published here on Tradingview and elsewhere.

My utmost respect, and all due credits to authors of related prior works.

Introduction

It is worth noting that while the general RSI formula, and the logic dictating the UpMove and DownMove data series has remained the same as the Wilders original formulation, it has been interpreted in a different way by using a different method of averaging the upward, and downward moves.

Cutler recognized the issue of data length dependency when using wilders smoothing method of calculating RSI which means that wilders standard RSI will have a potential initialization error which reduces with every new data point calculated meaning early results should be regarded as unreliable until enough calculation iterations have occurred for convergence.

Hence Cutler proposed using Simple Moving Averaging for gain and loss data which this Indicator is based on.

Having "Reverse engineered" prices for any oscillator makes the planning, and execution of strategies around that oscillator far simpler, more timely and effective.

Introducing the Reverse Cutlers RSI which consists of plotted lines on a scale of 0 to 100, and an optional infobox.

The RSI scale is divided into zones:

• Scale high (100)

• Bull critical zone (80 - 100)

• Bull control zone (62 - 80)

• Scale midline (50)

• Bear control zone (20 - 38)

• Bear critical zone (0 - 20)

• Scale low (0)

The RSI plots which graphically display output closing price levels where Cutlers RSI value will crossover:

• RSI (eq) (previous RSI value)

• RSI MA signal line

• RSI Test price

• Alert level high

• Alert level low

The info box displays output closing price levels where Cutlers RSI value will crossover:

• Its previous value. ( RSI )

• Bull critical zone.

• Bull control zone.

• Mid-Line.

• Bear control zone.

• Bear critical zone.

• RSI MA signal line

• Alert level High

• Alert level low

And also displays the resultant RSI for a user defined closing price:

• Test price RSI

The infobox outputs can be shown for the current bar close, or the next bar close.

The user can easily select which information they want in the infobox from the setttings

Importantly:

All info box price levels for the current bar are calculated immediately upon the current bar closing and a new bar opening, they will not change until the current bar closes.

All info box price levels for the next bar are projections which are continually recalculated as the current price changes, and therefore fluctuate as the current price changes.

Understanding the Relative Strength Index

At its simplest the RSI is a measure of how quickly traders are bidding the price of an asset up or down.

It does this by calculating the difference in magnitude of price gains and losses over a specific lookback period to evaluate market conditions.

The RSI is displayed as an oscillator (a line graph that can move between two extremes) and outputs a value limited between 0 and 100.

It is typically accompanied by a moving average signal line.

Traditional interpretations

Overbought and oversold:

An RSI value of 70 or above indicates that an asset is becoming overbought (overvalued condition), and may be may be ready for a trend reversal or corrective pullback in price.

An RSI value of 30 or below indicates that an asset is becoming oversold (undervalued condition), and may be may be primed for a trend reversal or corrective pullback in price.

Midline Crossovers:

When the RSI crosses above its midline ( RSI > 50%) a bullish bias signal is generated. (only take long trades)

When the RSI crosses below its midline ( RSI < 50%) a bearish bias signal is generated. (only take short trades)

Bullish and bearish moving average signal Line crossovers:

When the RSI line crosses above its signal line, a bullish buy signal is generated

When the RSI line crosses below its signal line, a bearish sell signal is generated.

Swing Failures and classic rejection patterns:

If the RSI makes a lower high, and then follows with a downside move below the previous low, a Top Swing Failure has occurred.

If the RSI makes a higher low, and then follows with an upside move above the previous high, a Bottom Swing Failure has occurred.

Examples of classic swing rejection patterns

Bullish swing rejection pattern:

The RSI moves into oversold zone (below 30%).

The RSI rejects back out of the oversold zone (above 30%)

The RSI forms another dip without crossing back into oversold zone.

The RSI then continues the bounce to break up above the previous high.

Bearish swing rejection pattern:

The RSI moves into overbought zone (above 70%).

The RSI rejects back out of the overbought zone (below 70%)

The RSI forms another peak without crossing back into overbought zone.

The RSI then continues to break down below the previous low.

Divergences:

A regular bullish RSI divergence is when the price makes lower lows in a downtrend and the RSI indicator makes higher lows.

A regular bearish RSI divergence is when the price makes higher highs in an uptrend and the RSI indicator makes lower highs.

A hidden bullish RSI divergence is when the price makes higher lows in an uptrend and the RSI indicator makes lower lows.

A hidden bearish RSI divergence is when the price makes lower highs in a downtrend and the RSI indicator makes higher highs.

Regular divergences can signal a reversal of the trending direction.

Hidden divergences can signal a continuation in the direction of the trend.

Chart Patterns:

RSI regularly forms classic chart patterns that may not show on the underlying price chart, such as ascending and descending triangles & wedges , double tops, bottoms and trend lines etc.

Support and Resistance:

It is very often easier to define support or resistance levels on the RSI itself rather than the price chart.

Modern interpretations in trending markets:

Modern interpretations of the RSI stress the context of the greater trend when using RSI signals such as crossovers, overbought/oversold conditions, divergences and patterns.

Constance Brown, CMT , was one of the first who promoted the idea that an oversold reading on the RSI in an uptrend is likely much higher than 30%, and that an overbought reading on the RSI during a downtrend is much lower than the 70% level.

In an uptrend or bull market, the RSI tends to remain in the 40 to 90 range, with the 40-50 zone acting as support.

During a downtrend or bear market, the RSI tends to stay between the 10 to 60 range, with the 50-60 zone acting as resistance.

For ease of executing more modern and nuanced interpretations of RSI it is very useful to break the RSI scale into bull and bear control and critical zones.

These ranges will vary depending on the RSI settings and the strength of the specific market’s underlying trend.

Limitations of the RSI

Like most technical indicators, its signals are most reliable when they conform to the long-term trend.

True trend reversal signals are rare, and can be difficult to separate from false signals.

False signals or “fake-outs”, e.g. a bullish crossover, followed by a sudden decline in price, are common.

Since the indicator displays momentum, it can stay overbought or oversold for a long time when an asset has significant sustained momentum in either direction.

Data Length Dependency when using wilders smoothing method of calculating RSI means that wilders standard RSI will have a potential initialization error which reduces with every new data point calculated meaning early results should be regarded as unreliable until calculation iterations have occurred for convergence.

Reverse Cutlers Relative Strength IndexIntroduction

The Reverse Cutlers Relative Strength Index (RCRSI) is an indicator which tells the user what price is required to give a particular Cutlers Relative Strength Index (RSI) value, or cross its Moving Average (MA) signal line.

Overview

Background & Credits:

The relative strength index (RSI) is a momentum indicator used in technical analysis that was originally developed by J. Welles Wilder Jr. and introduced in his seminal 1978 book, “New Concepts in Technical Trading Systems.”.

Cutler created a variation of the RSI known as “Cutlers RSI” using a different formulation to avoid an inherent accuracy problem which arises when using Wilders method of smoothing.

Further developments in the use, and more nuanced interpretations of the RSI have been developed by Cardwell, and also by well-known chartered market technician, Constance Brown C.M.T., in her acclaimed book "Technical Analysis for the Trading Professional” 1999 where she described the idea of bull and bear market ranges for RSI, and while she did not actually reveal the formulas, she introduced the concept of “reverse engineering” the RSI to give price level outputs.

Renowned financial software developer, co-author of academic books on finance, and scientific fellow to the Department of Finance and Insurance at the Technological Educational Institute of Crete, Giorgos Siligardos PHD. brought a new perspective to Wilder’s RSI when he published his excellent and well-received articles "Reverse Engineering RSI " and "Reverse Engineering RSI II " in the June 2003, and August 2003 issues of Stocks & Commodities magazine, where he described his methods of reverse engineering Wilders RSI.

Several excellent Implementations of the Reverse Wilders Relative Strength Index have been published here on Tradingview and elsewhere.

My utmost respect, and all due credits to authors of related prior works.

Introduction

It is worth noting that while the general RSI formula, and the logic dictating the UpMove and DownMove data series as described above has remained the same as the Wilders original formulation, it has been interpreted in a different way by using a different method of averaging the upward, and downward moves.

Cutler recognized the issue of data length dependency when using wilders smoothing method of calculating RSI which means that wilders standard RSI will have a potential initialization error which reduces with every new data point calculated meaning early results should be regarded as unreliable until enough calculation iterations have occurred for convergence.

Hence Cutler proposed using Simple Moving Averaging for gain and loss data which this Indicator is based on.

Having "Reverse engineered" prices for any oscillator makes the planning, and execution of strategies around that oscillator far simpler, more timely and effective.

Introducing the Reverse Cutlers RSI which consists of plotted lines on a scale of 0 to 100, and an optional infobox.

The RSI scale is divided into zones:

• Scale high (100)

• Bull critical zone (80 - 100)

• Bull control zone (62 - 80)

• Scale midline (50)

• Bear critical zone (20 - 38)

• Bear control zone (0 - 20)

• Scale low (0)

The RSI plots are:

• Cutlers RSI

• RSI MA signal line

• Test price RSI

• Alert level high

• Alert level low

The info box displays output closing price levels where Cutlers RSI value will crossover:

• Its previous value. (RSI )

• Bull critical zone.

• Bull control zone.

• Mid-Line.

• Bear control zone.

• Bear critical zone.

• RSI MA signal line

• Alert level High

• Alert level low

And also displays the resultant RSI for a user defined closing price:

• Test price RSI

The infobox outputs can be shown for the current bar close, or the next bar close.

The user can easily select which information they want in the infobox from the setttings

Importantly:

All info box price levels for the current bar are calculated immediately upon the current bar closing and a new bar opening, they will not change until the current bar closes.

All info box price levels for the next bar are projections which are continually recalculated as the current price changes, and therefore fluctuate as the current price changes.

Understanding the Relative Strength Index

At its simplest the RSI is a measure of how quickly traders are bidding the price of an asset up or down.

It does this by calculating the difference in magnitude of price gains and losses over a specific lookback period to evaluate market conditions.

The RSI is displayed as an oscillator (a line graph that can move between two extremes) and outputs a value limited between 0 and 100.

It is typically accompanied by a moving average signal line.

Traditional interpretations

Overbought and oversold:

An RSI value of 70 or above indicates that an asset is becoming overbought (overvalued condition), and may be may be ready for a trend reversal or corrective pullback in price.

An RSI value of 30 or below indicates that an asset is becoming oversold (undervalued condition), and may be may be primed for a trend reversal or corrective pullback in price.

Midline Crossovers:

When the RSI crosses above its midline (RSI > 50%) a bullish bias signal is generated. (only take long trades)

When the RSI crosses below its midline (RSI < 50%) a bearish bias signal is generated. (only take short trades)

Bullish and bearish moving average signal Line crossovers:

When the RSI line crosses above its signal line, a bullish buy signal is generated

When the RSI line crosses below its signal line, a bearish sell signal is generated.

Swing Failures and classic rejection patterns:

If the RSI makes a lower high, and then follows with a downside move below the previous low, a Top Swing Failure has occurred.

If the RSI makes a higher low, and then follows with an upside move above the previous high, a Bottom Swing Failure has occurred.

Examples of classic swing rejection patterns

Bullish swing rejection pattern:

The RSI moves into oversold zone (below 30%).

The RSI rejects back out of the oversold zone (above 30%)

The RSI forms another dip without crossing back into oversold zone.

The RSI then continues the bounce to break up above the previous high.

Bearish swing rejection pattern:

The RSI moves into overbought zone (above 70%).

The RSI rejects back out of the overbought zone (below 70%)

The RSI forms another peak without crossing back into overbought zone.

The RSI then continues to break down below the previous low.

Divergences:

A regular bullish RSI divergence is when the price makes lower lows in a downtrend and the RSI indicator makes higher lows.

A regular bearish RSI divergence is when the price makes higher highs in an uptrend and the RSI indicator makes lower highs.

A hidden bullish RSI divergence is when the price makes higher lows in an uptrend and the RSI indicator makes lower lows.

A hidden bearish RSI divergence is when the price makes lower highs in a downtrend and the RSI indicator makes higher highs.

Regular divergences can signal a reversal of the trending direction.

Hidden divergences can signal a continuation in the direction of the trend.

Chart Patterns:

RSI regularly forms classic chart patterns that may not show on the underlying price chart, such as ascending and descending triangles & wedges, double tops, bottoms and trend lines etc.

Support and Resistance:

It is very often easier to define support or resistance levels on the RSI itself rather than the price chart.

Modern interpretations in trending markets:

Modern interpretations of the RSI stress the context of the greater trend when using RSI signals such as crossovers, overbought/oversold conditions, divergences and patterns.

Constance Brown, CMT, was one of the first who promoted the idea that an oversold reading on the RSI in an uptrend is likely much higher than 30%, and that an overbought reading on the RSI during a downtrend is much lower than the 70% level.

In an uptrend or bull market, the RSI tends to remain in the 40 to 90 range, with the 40-50 zone acting as support.

During a downtrend or bear market, the RSI tends to stay between the 10 to 60 range, with the 50-60 zone acting as resistance.

For ease of executing more modern and nuanced interpretations of RSI it is very useful to break the RSI scale into bull and bear control and critical zones.

These ranges will vary depending on the RSI settings and the strength of the specific market’s underlying trend.

Limitations of the RSI

Like most technical indicators, its signals are most reliable when they conform to the long-term trend.

True trend reversal signals are rare, and can be difficult to separate from false signals.

False signals or “fake-outs”, e.g. a bullish crossover, followed by a sudden decline in price, are common.

Since the indicator displays momentum, it can stay overbought or oversold for a long time when an asset has significant sustained momentum in either direction.

Data Length Dependency when using wilders smoothing method of calculating RSI means that wilders standard RSI will have a potential initialization error which reduces with every new data point calculated meaning early results should be regarded as unreliable until calculation iterations have occurred for convergence.

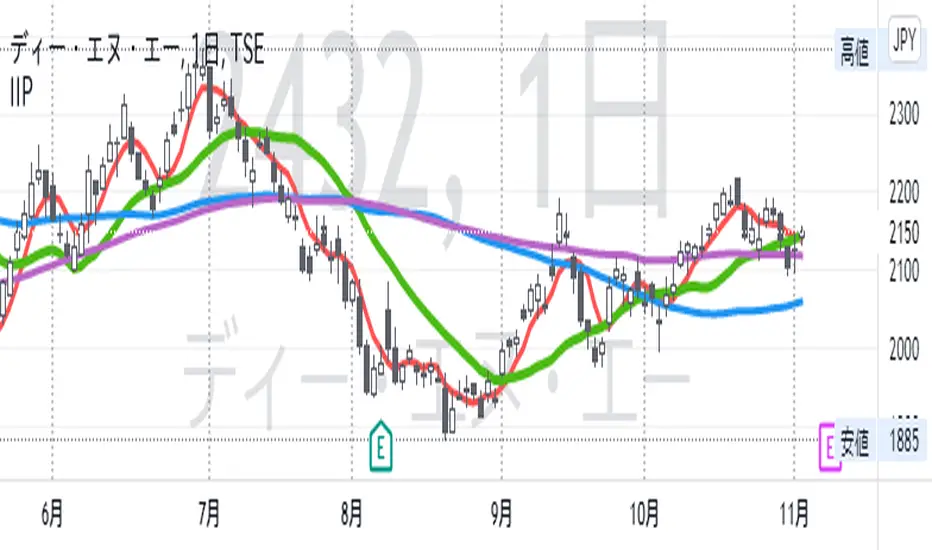

IIPThis indicator includes followings functions,

1. Close and SMA

Show 8 SMA (default: 3, 5, 7, 9, 20, 100, 300: each can be adjustable.)

2. Background color in Perfect Order (5, 20 ,60)

Perfect Order: Red

Reverse Perfect Order: Blue

3. Golden Cross and Dead Cross between SMA 5 and SMA 20

Golden Cross(GC):▲ with Green

Dead Cross(DC):▼ with Red

4. Show labels on 5 days, 20 days, 60 days and 100 days before today

5. Put dotted vertical line on first day in every month.

TradingGroundhog - Fundamental Analysis - Multiple RSI Ema(Script Available Version of my previous Fundamental Analysis - Multiple RSI Ema )

As the number of crypto currencies is expanding, we need to find the one which will boom in the next months, weeks or even days.

Therefore, I present to you a Fundamental Analysis tool based on RSI built in order to compare the RSI between the diverse cryptocurrencies.

When cryptocurrencies start to trend, become active, minable and especially "buyable", people are investing their money into them.

As a result,the Daily RSI rises and the price of the crypto in question increases steadily.

With "Fundamental Analysis - Multiple RSI EMA" you can :

Follow up to 20 RSI from different exchanges at the same time.

Find easily Increasing/Decreasing RSI as the lines get transparent if their RSI decrease.

You can also select market with high potential of booming as :

Booming Market : 60 < Daily RSI <= 100 (Strong green background)

Potent Market : 55 < Daily RSI <= 60 (Light green background)

Sleepy Market : 50 < Daily RSI <= 55 (Light red background)

Dying Market : 0 < Daily RSI <= 50 (Strong red background)

Futur booming crypto will go from the Potent Market to the Booming Market

Can be used with the following time frames depending on the necessity:

4H

Daily (Preferred)

Weekly

Monthly

Good trades !

Disclaimer (As it should always be one to any script)

***

This script is intended for and only to be used for personal purposes only. No such information provided by it constitutes advice or a recommendation for any investment or trading strategy for any specific person. There is no guarantee presented or implied as to the accuracy of specific forecasts, projections, or predictive statements offered by the script. Users of the script agree that its original developer does not take responsibility for any of your investment decisions. Please seek professional advice before trading.

***

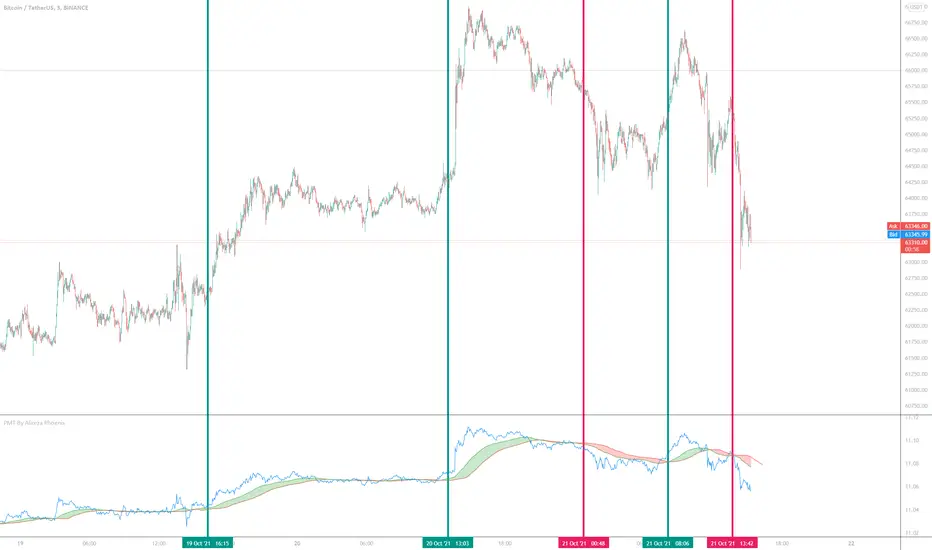

Price Movement Trend By Alireza Phoenix (Logarithmic)hi Traders

This logarithmic indicator shows the price movement trend, which is designed based on logarithmic functions and moving averages.

The Price Movement Trend Display Composed By :

A leading line consisting of the natural logarithm of Running Moving Average with length 60 and Offset 20 , and is displayed in red line.

A signal line consisting of a natural logarithm of an exponential moving average of length 90 , and is displayed in green line.

A price line consisting of the natural logarithm of a simple moving average along 1 whose source is price close , and is displayed in blue line.

A hidden price line consisting of the natural logarithm of a simple moving average along 1 and its source being the highest and lowest average prices , and is displayed in maroon line.

Learning how to get a signal from the price Movement trend indicator:

Moving the signal line and breaking the leading line upwards to form a green cloud is a buy signal.

Moving the signal line and breaking the leading line downwards that forms a red cloud is a sell signal.

Moving the price line and breaking the trend cloud upward , is a buy signal

Moving the price line and breaking the trend cloud downwards , is a sell signal

My instagram id : @pnxf6

ترجمه فارسی :

سلام تریدرها

این اندیکاتور لگاریتمی ، نمایش دهنده روند حرکتی قیمت است ، که بر اساس توابع لگاریتمی و میانگین های متحرک قیمت طراحی شده است

این اندیکاتور تشکیل شده از :

یک خط پیشرو متشکل از لگاریتم طبیعی متحرک وزنی نمایی مورد استفاده درآر اس آی به طول 60 و انحراف 20 است

یک خط سیگنال متشکل از لگاریتم طبیعی میانگین متحرک نمایی با طول 90

یک خط قیمت که متشکل از لگاریتم طبیعی میانگین متحرک ساده در طول 1 که منبع آن بسته شدن قیمت است.

یک خط قیمت مخفی که متشکل از لگاریتم طبیعی میانگین متحرک ساده در طول 1 و منبع آن میانگین بالاترین و پایین ترین قیمت است

یک فضای ابری مابین خط پیشرو و خط سیگنال که که با "نمایش روند حرکت قیمت" مشخص شده و در رنگ های سبز و قرمز قابل مشاهده میباشد.

آموزش گرفتن سیگنال ازاندیکاتور نمایش روند قیمت :

حرکت خط سیگنال و شکستن خط پیشرو رو به بالا که تشکیل ابر سبز رنگ میدهد یک سیگنال خرید میباشد .

حرکت خط سیگنال و شکستن خط پیشرو رو به پایین که تشکیل ابر قرمز رنگ میدهد یک سیگنال فروش میباشد .

حرکت خط قیمت و شکستن ابر روند حرکت قیمت رو به بالا سیگنال خرید میباشد

حرکت خط قیمت و شکستن ابر روند حرکت قیمت رو به پایین سیگنال فروش میباشد.

Special Time PeriodWith this indicator, you can choose candles in the period you want on your chart.

How ?

• If your chart is 5 minutes, the duration should be greater than 5 on this indicator.

If you do not do it this way, there will be gaps in the price, it will not give the right result.

• If you want to see it in minutes, you must enter a direct numerical value. For example, to see 2 hours, you must enter the number 120. Because 2 hours is 120 minutes.

Like the warning above, if you want to plot a 2-hour chart with this indicator, a maximum of 1 hour should be selected on your main chart.

• Resolution, eg. '60' - 60 minutes, 'D' - daily, 'W' - weekly, 'M' - monthly, '5D' - 5 days, '12M' - one year, '3M' - one quarter

• For example, if you want to see the 2-day chart, you should have a maximum of 1 day chart open on your home screen and write "2D" to the indicator value.

• You will get much better results if the period on your main chart and the period on this indicator are multiples of each other.

• In the image below, the period on the main chart is 30 minutes, but the period on the indicator is 90

• Click on the facing brackets at the top right of the legend and your chart will enlarge.

[VJ] Hulk Smash IntraThis is a simple intraday strategy for working on Stocks or commodities based out on Super Trend and ever reliable ADX . You can modify the start time and end time based on your timezones. Session value should be from market start to the time you want to square-off

Important: The end time should be at least 2 minutes before the intraday square-off time set by your broker

Comment below if you get good returns

Strategy: Supertrend and ADX strength (Hulk Smash)

Indicators used :

Super trend is simple and easy to use indicator and gives a precise reading about an on going trend.It is built with two parameters, namely period and multiplier.The Buy and Sell signal modifies once the indicator tosses over the closing price. When the Super trend closes above the Price, a Buy signal is generated, and when the Super trend closes below the Price, a Sell signal is generated. In this case we use it only for direction .

ADX informs a trader when the market is trending.It filters out anti trend trades to help trend chasing indicators from frequent whipsaws

Multiplier is a vital input for Super trend. If the multiplier value is too high, then lesser number of signals is made.

Buying/Selling

• If the price is going UP, and the ADX indicator is also going UP, then we have the case for a bullish trend.

• The same is true if the price is going down and the ADX indicator is going UP. Then we have the case for a bearish trend.

• Value of ADX below 20 is called trading zone which implies non-trending market

• Trade with Strength only if the Super trend is validating

ADX Values

0 - 20 : Non Trending (Range bound market, phase of Accumulation/Distribution)

20-45 : Strong Signal (helpful for traders)

45-60 : Very strong trend (occur rarely, indicate exhaustion)

60 - 100 : Extremely strong trend (very rare, unsustainable trends, be ready for reversals)

Usage & Best setting :

Choose a good volatile stock and a time frame - 5m.

ADX Factor : vary as per info above

ST multiplier : 3

There is stop loss and take profit that can be used to optimise your trade

The template also includes daily square off based on your time.

Strat Assistant Alerts and Highs/LowsStrat Assistant FTC Only

----------------------------

█ OVERVIEW

This script is intended to highlight/draw lines for the prior high/low of 30, 60, day, week, month, quarter, as well as create the alerts for when these thresholds get crossed

Input

----------

The script has inputs for every time frame plotted - 30, 60, day, week, month, quarter. All of the following items below can be "modified"

is the high line active? (for the corresponding time frame, will plot the line yes or no - by default only the DAY is displayed)

is the low line active? (for the corresponding time frame, will plot the line yes or no - by default only the DAY is displayed))

The high line color - modify the color of the corresponding time frame high line to your liking

The low line color - modify the color of the corresponding time frame low line to your liking

The time frame line width - make some lines wider than others for easier distinction

Output

----------

Lines for each corresponding time frame activated in the selected color and width.

Custom alerts - open a stock, select the Alerts button at the top, click the condition as the name of this script. The next drop down will show you all the corresponding alerts you can set for the current price crossing above the prior timelines high or below the prior timelines low (the bracket number is just for sorting purposes).

Best Practices

----------

What's not mapped? - Style (you can't drive this by an input, by default day is dashed, the rest are a solid line)

What's not mapped? - Price on the Y axis. I'm still trying to figure this out, not sure you can do it. I can add a label, just gets cluttered fast

Played with this a little bit using crypto, but obviously I can't test out all these alerts without a lot of things moving. Please do your due diligence.

I know a million people are going to want a million things. I can create more alerts coming soon, for now I wanted to start with this. Please and comments or suggestions or feedback and I'll see what I can do. I can create labels (for price) randomly, but it will clutter the screen. Or I can create one big box or table with prices shown.

Strat Assistant Hour FlipStrat Assistant Hour Flip

----------------------------

█ OVERVIEW

This script is intended to provide a vertical line indicator for the hourly "flips" to easily indicate when the hour turns. Ideally used in timeframes less than an hour.

Input

----------

Hour Color: the color of the line and the text for the hourly indicator

Four Hour Color: the color of the line and the text for the four hour indicator

Show Label Text?: an on/off (active/inactive) flag to display the text (new 30s/60s). I can't figure out how to get a label vertical, so sometimes it gets in the way.

Output

----------

Vertical Dotted Line Indicator: vertical lines that allow a user to quickly see when the hour flips

Hour Flip Labels: quick visual labels with the same color as the lines that will display new 4h/60s/30s

Best Practices

----------

Trading view may limit the number of lines drawn, so probably not best to be use in larger time frames (like days/month worth of data on the chart) for smaller intervals

Best if used for intervals under 30 minutes

Strat Assistant FTC OnlyStrat Assistant FTC Only

----------------------------

█ OVERVIEW

This script is intended to provide full time frame continuity information for almost all time frames (3, 5, 15, 30, 60, 4H, Day, Week, Month, Quarter)

When added, the script provides a visual indicator to the right at the current price level with indicators for the various time frames in terms of price action and candle type.

█ DETAIL

----------

Output

Time Frames: 3min, 5min, 15min, 30min, 60min, 4 Hour, Day, Week, Month Quarter

Time Frame Labels: 3, 5, 15, 30, 60, H, 4H, D, W, M, Q

Current Candle Time Frame Price Action: displayed below time frame labels. RED + Arrow Down (open > close) or GREEN + Arrow Up (open =< close)

Time Frame Compare: displayed above time frame labels. Current high/low vs prior high/low are compared. IN = Inside/Yellow (current high/low inside prior), O = Outside/Fuchsia (current high/low both greater and less than prior high/low), 2U = Up/Green (current high higher than prior, and low not lower), 2D = Down/Red (current lows lower than prior lows, and high not higher)

Will not show time frames lower than the one currently selected

Best Practices

----------

Had to decouple this from the other scripts because Trading View limits how much you can plot/show

May be a little slow at times, analyzing a lot of time periods/data be patient.

Volume Zone Oscillator and Price Zone Oscillator (VZO/PZO)Credits go to @NeoButane as basis is taken from his open-source code and I modified it - changes described below.

Usage:

Positive -> bullish, negative -> bearish

-60/60 is seen as the limit of the oscillator range, and a pullback should be expected from there

-40/40 are in general Oversold/Overbought levels

Modifications:

added alerts

added Divergences formula

added additional types of smoothing

added signal display based on described above usage (extreme levels of oscillations and bounce back)

Tenkansen&Kijunsen LinesYou can see 2 sections on this script

1. Kijunsen Lines Section

Basicly calculated by adding the highest high and the lowest low over the past 26 periods and dividing the result by two.

Kijunsen Lines section has 4 lines

a. 60 Minutes Kijunsen

b. 240 Minutes Kijunsen

c. 1 Day Kijunsen

d. 1 Week Kijunsen

You can see all 4 kijunsen at all periods.

2. Tenkansen Lines Section

Basicly calculated by adding the highest high and the highest low over the past nine periods and then dividing the result by two

Tenkansen Lines section has 4 lines

a. 60 Minutes Tenkansen

b. 240 Minutes Tenkansen

c. 1 Day Tenkansen

d. 1 Week Tenkansen

You can see all 4 tenkansen at all periods.

With this you can see 4 kijunsen and 4 tenkansen lines without changing periods. (May have some calculating problems. Because of different candle systems.)

This indicator has 2 functions

A. Support Function

All kijunsen and all tenkansen lines has support function.

B. Resistance Function

All kijunsen and all tenkansen lines has resistance function.

Chart Champions - Part 3 - SessionsThank you for sparing you time to read my indicator.

This indicator has been created as a suite of 3. This was to ensure that those with only the Free Trading View account could benefit (with their restriction to 3 indicators). Please ensure you install each indicator and read each indicator write up to fully understand what has tried to achieved.

Chart Champions – Part 1 –Lvls nPOC VWAPS

This indicator is broken down into:

• Levels

• VWAPS

• Naked Point of Control

Levels

It displays the levels to the right of the price Axis to enable the user to have a cleaner chart.

The below levels will automatically appear:

dOpen – pdHigh – pdLow – pdEQ – pwEQ

Optional Levels include:

mOpen – pmOpen – pdOpen – dbyOpen – wOpen – pwOpen

VWAPs

Optional VWAPs

Daily (including pdVWAP close) – Weekly – Monthly

Naked Points of Control (nPOC)

To view the nPOC move the chart back in time to pick up the nPOCs.

Chart Champions – Part 2 – CCV IBs POC

This indicator is broken down into:

• Chart Champions Value

• Initial Balance

• Points of Control

Chart Champions Value (CCV)

CCV is based on the 80% rule of the dOpen opening outside of the pdVAH/pdVAL. Please do you own research to fully understand how this trading strategy works (readily avaliable online).

Initial Balance (IB)

IB is based on the first 60 minutes of the market opening. It captures the highest and lowest points within that 60 minutes. Please do you own research to fully understand how this trading strategy works (readily avaliable online).

Points of Control (POCs)

POC are the price levels where the most volume was traded.

Developing POC (dPOC) will constantly move with volume/price action through out the day.

Optional POCs

Previous Day POC (pdPOC) – Day Before Yesterday POC (dbyPOC)

Chart Champions – Part 3 – Sessions - Manual Input

This indicator is broken down into:

• Manual Inputs (daily, weekly, monthly)

• IGOR SessionsTtimes

• Pre + Market Openings

Manual Input

Daily x3

Weekly x 3

Monthly x 3

This allows the trader to put in specific levels.

IGOR Session Times

This is a user specific requirement to highlight cetain times during the day, displayed at the bottom of the chart in the colour strip.

Pre + Market Openings

This allows the user to see when pre market trading has started and with the live maket has started, displayed at the top of the chart in colours.

A huge thank you goes out to:

Stackoverflow users AnyDozer and Bjorn.

TV user ahancock for allow me use of this code.

Disclaimer the lower the timeframe the more information it processes.

Chart Champions - Part 2 - CCV IBs POCsThank you for sparing you time to read my indicator.

This indicator has been created as a suite of 3. This was to ensure that those with only the Free Trading View account could benefit (with their restriction to 3 indicators). Please ensure you install each indicator and read each indicator write up to fully understand what has tried to achieved.

Chart Champions – Part 1 –Lvls nPOC VWAPS

This indicator is broken down into:

• Levels

• VWAPS

• Naked Point of Control

Levels

It displays the levels to the right of the price Axis to enable the user to have a cleaner chart.

The below levels will automatically appear:

dOpen – pdHigh – pdLow – pdEQ – pwEQ

Optional Levels include:

mOpen – pmOpen – pdOpen – dbyOpen – wOpen – pwOpen

VWAPs

Optional VWAPs

Daily (including pdVWAP close) – Weekly – Monthly

Naked Points of Control (nPOC)

To view the nPOC move the chart back in time to pick up the nPOCs.

Chart Champions – Part 2 – CCV IBs POC

This indicator is broken down into:

• Chart Champions Value

• Initial Balance

• Points of Control

Chart Champions Value (CCV)

CCV is based on the 80% rule of the dOpen opening outside of the pdVAH/pdVAL. Please do you own research to fully understand how this trading strategy works (readily avaliable online).

Initial Balance (IB)

IB is based on the first 60 minutes of the market opening. It captures the highest and lowest points within that 60 minutes. Please do you own research to fully understand how this trading strategy works (readily avaliable online).

Points of Control (POCs)

POC are the price levels where the most volume was traded.

Developing POC (dPOC) will constantly move with volume/price action through out the day.

Optional POCs

Previous Day POC (pdPOC) – Day Before Yesterday POC (dbyPOC)

Chart Champions – Part 3 – Sessions - Manual Input

This indicator is broken down into:

• Manual Inputs (daily, weekly, monthly)

• IGOR SessionsTtimes

• Pre + Market Openings

Manual Input

Daily x3

Weekly x 3

Monthly x 3

This allows the trader to put in specific levels.

IGOR Session Times

This is a user specific requirement to highlight cetain times during the day, displayed at the bottom of the chart in the colour strip.

Pre + Market Openings

This allows the user to see when pre market trading has started and with the live maket has started, displayed at the top of the chart in colours.

A huge thank you goes out to:

Stackoverflow users AnyDozer and Bjorn.

TV user ahancock for allow me use of this code.

Disclaimer the lower the timeframe the more information it processes.

Chart Champions - Part 1 - nPOC - Levels - VWAPsThank you for sparing you time to read my indicator.

This indicator has been created as a suite of 3. This was to ensure that those with only the Free Trading View account could benefit (with their restriction to 3 indicators). Please ensure you install each indicator and read each indicator write up to fully understand what has tried to achieved.

Chart Champions – Part 1 –Lvls nPOC VWAPS

This indicator is broken down into:

• Levels

• VWAPS

• Naked Point of Control

Levels

It displays the levels to the right of the price Axis to enable the user to have a cleaner chart.

The below levels will automatically appear:

dOpen – pdHigh – pdLow – pdEQ – pwEQ

Optional Levels include:

mOpen – pmOpen – pdOpen – dbyOpen – wOpen – pwOpen

VWAPs

Optional VWAPs

Daily (including pdVWAP close) – Weekly – Monthly

Naked Points of Control (nPOC)

To view the nPOC move the chart back in time to pick up the nPOCs.

Chart Champions – Part 2 – CCV IBs POC

This indicator is broken down into:

• Chart Champions Value

• Initial Balance

• Points of Control

Chart Champions Value (CCV)

CCV is based on the 80% rule of the dOpen opening outside of the pdVAH/pdVAL. Please do you own research to fully understand how this trading strategy works (readily avaliable online).

Initial Balance (IB)

IB is based on the first 60 minutes of the market opening. It captures the highest and lowest points within that 60 minutes. Please do you own research to fully understand how this trading strategy works (readily avaliable online).

Points of Control (POCs)

POC are the price levels where the most volume was traded.

Developing POC (dPOC) will constantly move with volume/price action through out the day.

Optional POCs

Previous Day POC (pdPOC) – Day Before Yesterday POC (dbyPOC)

Chart Champions – Part 3 – Sessions - Manual Input

This indicator is broken down into:

• Manual Inputs (daily, weekly, monthly)

• IGOR SessionsTtimes

• Pre + Market Openings

Manual Input

Daily x3

Weekly x 3

Monthly x 3

This allows the trader to put in specific levels.

IGOR Session Times

This is a user specific requirement to highlight cetain times during the day, displayed at the bottom of the chart in the colour strip.

Pre + Market Openings

This allows the user to see when pre market trading has started and with the live maket has started, displayed at the top of the chart in colours.

A huge thank you goes out to:

Stackoverflow users AnyDozer and Bjorn.

TV user ahancock for allow me use of this code.

Disclaimer the lower the timeframe the more information it processes.