Hull Crossover Strategy no TP or SLWhat is it?

A simple yet effective strategy ran on the 30m chart.

This is a basic idea that can be expanded on using different indicator to either add signals or filter out certain bad signals!

The strategy consists of 1 fast moving average and 1 slow moving average.

Both of these moving averages are the Hull Moving Average

What is the Hull Moving Average?

The Hull Moving Average ( HMA ) is a directional trend indicator.

It captures the current market conditions and uses recent price action to determine if conditions are bullish or bearish relative to historical data.

The Hull is different from traditional trend indicators like the EMA and the SMA .

It is designed to reduce the lag often associated with other MAs by providing a faster signal on a smoother visual plane.

How it works?

When the fast HMA crosses over the slow HMA , we initiate a long signal, and

when the fast HMA crosses under the slow HMA , we initiate a short signal.

Conclusion

The power of simplicity is what makes this such a great core to use to build onto making something even better!

The results were optimised to suit the most common market conditions seen today.

******** Not financial advice! ********

Strategy

8 Whittle DownThe system is designed to short on directionally negative instruments like VXX & SQQQ

The system only shorts, no longs

It enters a pilot position if the system has no trades open at the time is in the late afternoon

It uses a 200-day moving average as a filter and will only short if the price is below the 200 day moving average

The pilot position will only enter with 1/3 ( one third ) of the total expected position size

StopLossPerc sets the stop loss, (1.15) means it is set to a 15% stop loss. -- The Red Line

The system will buy additional shares for a full position if the pilot piston profit target was not reached

The full shares position is set to purchase at a higher price. T2EntTrgPerc sets the buy percentage target for the additional shares. -- The Yellow Line

Each entry has different settable profit targets. T1ProfTrgPerc sets the profit target for the first trade (0.95) is basically set to a 5% profit.

T2ProfTrgPerc sets the profit target for the second trade (0.90) is basically set to a 10% profit. -- The White Line

RED LINE == STOP LOSS LINE

GREENLINE == PROFIT TARGET FOR THE 1ST TRADE

YELLOW LINE == ADD ON SHARES TO THE TRADE

WHITE LINE == PROFIT TARGET FOR THE 1st & 2nd TRADE COMBINED

Let me know if you have any questions and I'll try to clarify

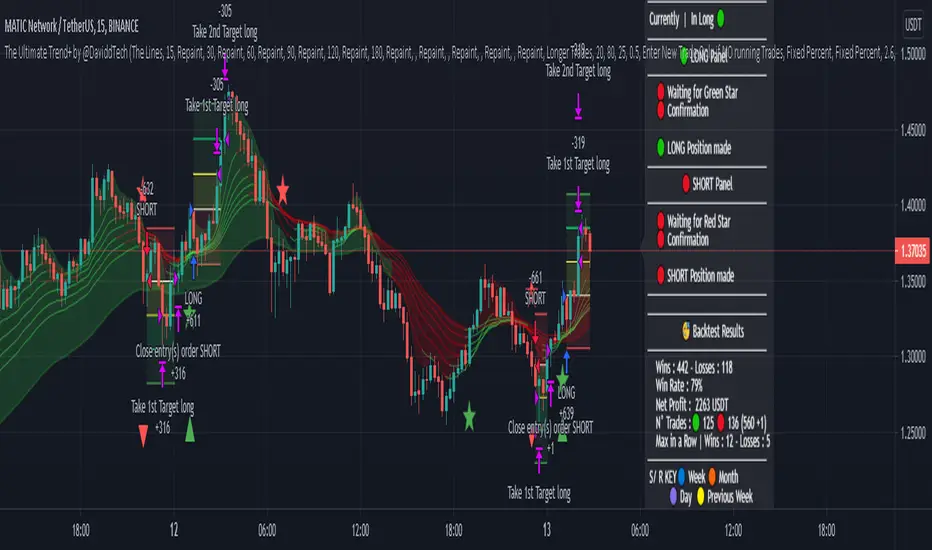

Multi Time Frame Heiken Ashi Candles by @DaviddTechMulti Time Frame Heiken Ashi Candles Visual Strategy.

Inspired by a video on YouTube by TradePro I decided to backtest this strategy.

The Strategy : This strategy waits for all the lines to cross green or red to look for a an entry.

It seems to give good results on the 15 minute timeframe.

1. The Cloud - Confirmed with no repainting.

2. The Lines may repaint as the price movement changes.

Confluence with the RSI STOCHASTIC.

If you use the RSI STOCHASTIC you have 2 options.

1. Super Scalper - Where the strategy will enter on every cross <> the two levels.

2. Longer positions - One entry is made where the RSI STOCHASTIC the closest to the GREEN/RED Star.

WARNING:

- For purpose educate only

- Plots EMAs and other values on chart.

- This script to change bars colors.

Rosebud Trend Backtest [DepthHouse]*Past Performance Does Not Guarantee Future Results*

*Strategy created for backtesting purposes only.

*Backtesting assesses the viability of a trading strategy or pricing model by discovering how it would have played out retrospectively using historical data.

* Please be sure to read all updates below as the information below could change with future updates.

Rosebud Trend Indicator uses complex range calculations to easily detect trend changes, critical support and resistance levels, and even aid in spotting reversals. The Critical Support & Resistance Zones are plotted via the red and green cloud. This cloud not only visually displays the expected trend direction but often acts as major support and resistance zones. The outer band measures the expected range in which the assets trade over longer periods of time.

The Rosebud Trend Backtest combines the calculations of the ATR Auto Oscillator & the Rosebud Trend Indicator to demonstrate backtest performance.

// Settings //

Users can switch the ‘ Trend Sensitivity ’ between ‘ Low ', ' Med ', and ‘ High ’ to increase or decrease the rate at which the cloud changes.

By altering the S/R Band Thickness users can furthermore increase or decrease the rate at which a trend changes by altering the thickness of the cloud. Default is .50 however this can be lowered if needed.

Bar colors are generated by a combination of Rosebuds primary function and our ATR AUTO Oscillator base functions. Users have 3 bar color options to select from: Simple, Complex, and Off.

Simple: Bars colors alternate between shades of red and green based on the trend direction and the ATR Auto strength. The stronger the shade, the stronger the trend.

Complex: This adds a few extra variables to the script which generates a more complex bar color display. Using this option, Rosebud will generate light red bars in a bull trend if downward movement is strong and vice versa in a bear trend. It also will generate a purple bar if the candle successfully closes above or below the Top & Bottom Range Bands; We call this a range break, and it could be an early sign of strong upward or downward movement.

Off: In case you like to keep things even simpler, this option hides all overlay bar colors.

ATR Options: Used for Light & Strong Entries/Exits // Bar Colors also based on these settings

ATR Smoothed Signal Option: Turns advance smoothing on or off. On will reduce signal noise, while Off could land you that perfect bottom signal with a lower success rate.

ATR Candlestick Length: Default factor for bar color and shape generation, the higher the number the fewer signals that will generate.

ATR Candlestick Smoothing: Default smoothing for the Candlestick Length

Signal Lookback: Adjust the factor at which Bull, Bear, Up, and Down. Lower this to 2 for more signals.

// ⇅ BackTest Settings ⇅ //

Short Trading: Option to see backtest results for both long and short positions. Default is Long Only.

Strategy Entry Options:

Trend Only: Positions are entered right as there is a cloud trend change.

Light Entry: This enters a trade as soon as there is a breakout or breakdown signal generated from the ATR settings.

Strong Entry: Multiple conditions must be met; Price action must be near the Trend Base and must receive either a bullish or bearish crossover in the oversold or overbought range of the ATR Settings.

Strategy Exit Options:

Trend Only: Exits all positions after there is a primary trend change.

Light Exit: Exits a user set percentage of open positions when the ATR generates a breakdown or breakout. Will continue to do this at each occurrence. Presets are built in to keep these from triggering too often in volatile conditions.

Strong Exit: Exits a user set percentage of open positions when the ATR generates a bullish or bearish crossover in the overbought or oversold ranges. Will continue to do this with each occurrence. Presets are built in to keep these from triggering too often in volatile conditions.

Profit Points: Exits a set percentage of the position up to 3 times at a user set percentage gap from the entry. Any remaining amount in the position exits upon a trend change.

Profit QTY Percent: Percent of the position to exit when an exit condition triggers. This does not apply to the “Trend Only” exit option.

Profit Percent Gap: Percent gap for Profit Point Exits. Recommend adjusting based on timeframe. See example below.

Supertrend LSMA long StrategyThis is a long strategy which combines Super trend indicator with LSMA moving average.

In general it tends to works better with long trending markets such as stocks and cryptos using a big timeframe.

The rules are simple

Long entry:

Supertrend is telling us to go long and close of a candle is above moving average

Long exit:

Supertrend is telling us to go short

IF you have any questions, let me know !

Pivot Reversal strategy long onlyPivot Point Reversal Strategy

Pivot point reversal strategy is based on the first support level’s price action during the bullish trend and the first resistance level during the bearish trend . Traders follow the main trend and enter into the trade after reversal analyzing pivot point levels.

This version is an upgraded version, combining the initial pivot point reversal strategy together with one of the most accuracy moving average in my opinion for day trade, the Least square moving average.

At the same time I applied an option to backtest using a date range and a leverage calculator.

The default options are optimized for BTC /USDT 2H charts, using 0.1% comission fee.

If you have any questions, let me know

Extremely high win rate FOREX swing strategyTHis is a very simple yet extremely efficient FOREX strategy .

In general it tends to work the best against NZD and AUD pairs, however other major pairs and crosses can work as well.

It's made of a time management, together with MACD , moving average , a price action rule and a risk management.

THe logic behind is the next one :

For LONG:

We have 3 ascending candles.

Histogram of MACD is positive.

Last close of a candle is was above moving average.

If all those previous condition happened before 17/18 UTC time depending if its summer time or not, we enter the trade.

For Short:

We have 3 descending candles.

Histogram of MACD is negative.

Last close of a candle is was below moving average.

If all those previous condition happened before 17/18 UTC time depending if its summer time or not, we enter the trade.

RIsk management

For risk management, since we aim to have a 95%+ win rate, we aim to have a 5:1 or 10:1 risk to reward ratio. Meaning that for each $ we can win, we can lose 5-10$.

THats why I recommend to be extremely careful when playing with leverage with this strategy.

Full Forex scalper StrategyTHis is a FOREX scalping system that can be optimized with almost all majors and crosses pairs.

Its made of multiple elements such as :

MACD

Stochastic RSI

Fast VW moving average

Slow VW moving average

Time management( forex sessions as inputs)

Rules for entry

Long

Last 2 MACD values were ascending, fast moving average is below moving average and stochastic RSI is below 30 level. At the same time we are either into London or NY session.

Short

Last 2 MACD values were descending, fast moving average is above moving average and stochastic RSI is above 70 level. At the same time we are either into London or NY

Rules for exit

WE have 2 exit possibilities: we can exit either at the end of NY/London Session or based on a TP/SL risk management calculating % in movement.

If you have any questions let me know !

Crypto RSI with RVI StrategyThis is a long only strategy adapted for crypto market.

Its idea is to take the most juice out of a long trend and cut the losses as soon as possible.

For this , its components are RSI with a very big length - 100 or 200 preferably and RVI.

Rules for entry

If RVI is in the buy zone and we have a crossover from RSI with the overbought level.

Rules for exit

With change condition : If RVI is in the sell zone and we have a cross under from RSI with the oversold level.

With stop loss : we have a SL based on movement in % of the price, recommendable between 5-10%.

If you have any questions let me know !

3 RSI 6sma/ema ribbon crypto strategyThis is a very efficient swing trading strategy designed for crypto long timeframes like 2h+.

Initially we have 3 RSI .

AFter that we use them as source for 6 SMA/EMA for each RSI, 5, 30, 50, 70, 90, 100. With those we create a ribbon that we are going to use in order to check the direction of the trend.

Rules for entry:

For long : if either all the SMA/EMA's from the 2nd RSI are telling us to go long, or all the all SMA/EMA's from the 3rd rsi are telling us to go long F

For short : if either all the SMA/EMA's from the 2nd RSI are telling us to go short, or all the all SMA/EMA's from the 3rd rsi are telling us to go short

We exit when we get an opposite condition than the entry one.

Caution: this strategy has no risk management inside, so use it with caution. If you have any questions , let me know !

Forex bot full strategy with risk managementThis is a full strategy designed for forex major pairs, specially EUR/USD using 1h time frame chart.

Its components are

200 EMA

MACD

OBV

PSAR

RIsk management with tp and sl movements

Rules for entry

For long = Previous histogram from MACD was below 0 and current one is above 0. CLose of a candle is above EMA 200 , OBV oscillator is negative and we have an uptrend from PSAR

For short = Previous histogram from MACD was above 0 and current one is below 0. CLose of a candle is below EMA 200 , OBV oscillator is positive and we have an downtrend from PSAR

Rules for exit

For tp and sl values we calculate the distance from the close of candle until the psar values.

If you have any questions, let me know !

BTC Candle Correlation Strategy This is a special strategy adapted for crypto market, which instead of using the current chart candles, we use inside calculation a candle from different charts.

For best usage I recommend a big timeframe like 1-4h+.

In this case we take the high, low, open and close candles from different brokers for BTC, and with it we form up the candle that we are going to use for the logic of entry.

At the same time we are going to create an upper and lower bands using a moving average and the difference between high and low.

So in a way to put it, if BTC triggers a sell or buy order, we input instead these orders on the current chart, like in this example with ETH.

Rules for entry

For long : if we have a crossover of the btc source value with the upper band .

For short: if we have a crossunder of the btc source vale with the lower band.

For exit, we do it when we receive a different signal than the initial one.

This strategy does not have any other risk management inside, so use it with caution.

If you have any other questions, let me know !

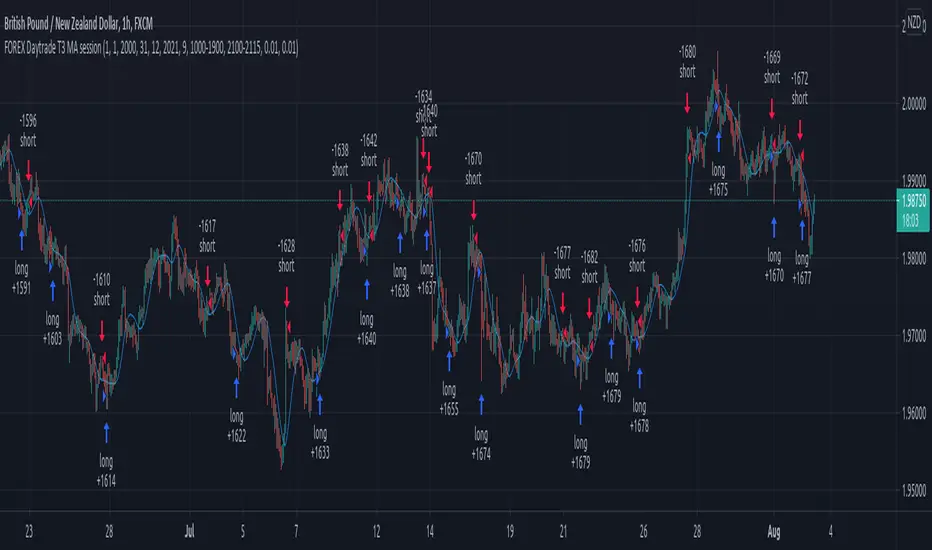

Forex Daytrade T3 MA sessionThis is a simple yet very efficient daytrading strategy for most crosses pairs, like EUR/NZD, EUR/AUD , GBP/NZD, GBP/AUD and so on.

It tends to works best with 1h and 15 min time frame charts.

Its components are :

Entry time = session that we want to trade, where we can combine for example half of London and all of NY using an hour system.

T3 Moving average

Price action.

Rules for entry

For long , we are during the hours we want to trade, current close is price is above previous high and at the same time is above moving average

For short , we are during the hours we want to trade, current close is price is below previous low and at the same time is below moving average

Rules for exit

We exit when either the opposite condition is triggered, if the hours of trading are off or based on a percentage TP/SL system movement.

For this example we use 1% movement both for TP and SL

If you have any questions, let me know !

xGhozt Consecutive Candle Count - BacktestxGhozt Consecutive Candle Count with Backtest simply counts consecutive positive or negative candles, and allows you to get the live statistics of how many times this consecutive candle series occurred in the past, with the probabilities of the next candle to be a reversal, and the average past gains from that reversal. You can select the number of consecutive candles you're tracking, and select a start and end date. When your desired pattern is met by the indicator, it will indicate you on the chart if it's worth shorting or longing the next candle.

You also have the possibility to set up alerts when your consecutive candles patterns are met. To do so, go into the indicator's settings, select your time frame, the consecutive number of candles you are tracking, your success rate, and the number this pattern occurred in the past. Once it's done, open the alerts box, and set up your alerts accordingly.

You will have 2 options:

- Green Candles Followed by Red = short next candle.

- Red Candles Followed by Green = long next candle

Now that the backtest is added, you can try different combinations and figure the best outcome to get the best returns!

One thing to note with the backtest: you cannot run the backtest with take profits / stop loss AND candle closing, it has to be one of the two.

[Advanced] Hilega-Milega IndicatorThis Indicator Name is Hilega Milega, and the original Idea given by Nitish Kumar, I just coded it and add some signals for backtesting.

it works on RSI + WMA and EMA plotted.

Default Values Used :

RSI = 9

WMA = 21

EMA = 3

But i added some extra, now everyone can change the Type of WMA and EMA, also SMA for trend confirmation,

How it works ??

Buy : When RSI crossover WMA or any Type of Moving Average you choose,

Sell : When RSI crossunder WMA or any Type of Moving Average you choose,

also:

Buy : When EMA crossover WMA or any Type of Moving Average you choose,

Sell : When EMA crossunder WMA or any Type of Moving Average you choose,

also:

Buy : When RSI + EMA crossover WMA or any Type of Moving Average you choose at the Same time,

Sell : When RSI + EMA crossunder WMA or any Type of Moving Average you choose at the Same time,

and Much More...! hope so you like it,

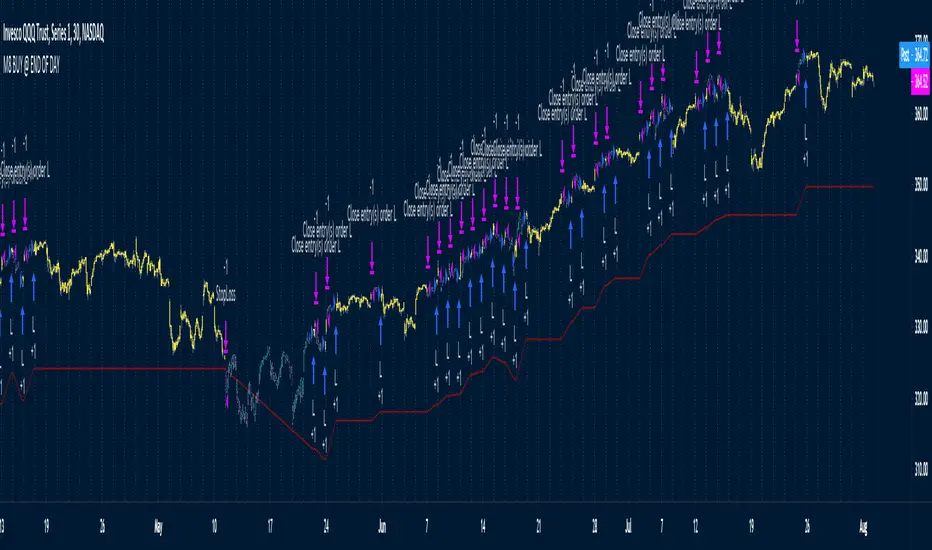

M8 BUY @ END OF DAYI've read a couple of times at a couple of different places that most of the move in the market happens after hours, meaning during non-standard trading hours.

After-market and pre-market hours and have seen data presented showing that systems which bought just before end normal market hours and sold the next morning had really amazing resutls.

But when testing those I found the results to be quite poor compared to the pretty graphs I saw, and after much tweaking and trying different ideas I gave up on the idea until I recently decided to try a new position management system.

The System

Buys at the end of the trading day before the close

Sells the next morning at the open IF THE CLOSE OF THE CURRENT BAR IS HIGHER THAN THE ENTRY PRICE

When the current price is not higher, the system will keep the position open until it EITHER gets stops out or closes on profit <<< this is WHY it has the high win %

The system has a high win ratio because it will keep that one position open until it either reaches profit or stops out

This "system" of waiting, and keeping the trade open, actually turned out to be a fantastic way to kind of put the complete trading strategy in a kind of limbo mode. It either waits for market failure or for a profit.

I don't really care about win % at all, almost always high win % ratio systems are just nonsense. What I look for is a PF -- profit factor of 1.5 or above, and a relatively smooth equity curve. -- This has both.

The Stop Loss setting is set @ .95, meaning a 5% stop loss. The Red Line on the chart is the stop loss line.

There is no set profit target -- it simply takes what the market gives.

Non-Repainting System

This does use a 200D Simple Moving Average as a filter. Like a Green Light / Red Light traffic light, the system will only trade long when the price is above its 200 Moving average.

Here is the code: "F1 = close > sma(security(syminfo.tickerid, "D", close ), MarketFilterLen) // HIGH OF OLD DATA -- SO NO REPAINTING"

I use "close ", so that's data from two days ago, it's fixed, confirmed, non-repainting data from the higher timeframe.

-- I would only suggest using this on direction tickers like SPY, QQQ, SSO, TQQQ, market sectors with additional filters in place.

Day of Week Custom Buy/Sell StrategyThis strategy was made for bitcoin and allows you to back test longing or shorting for various days of the week. The price may tend to go in one direction or another for each week day, and this strategy allows you to test days across a range of dates to capitalize on this.

Make sure you are on the daily time frame while viewing the performance and trade history to ensure the script works as intended and you have the most historical data as possible from Trading View.

Custom Date Buy/Sell StrategyThis strategy allows you to back test longing or shorting during a period of time between two dates.

Make sure you are in the daily time frame while viewing the performance and trade history to ensure you have the most historical data as possible from Trading View.

Finally, due to the way Trading View enters trades at the end of a candle, you must subtract one day from your starting and your end dates.

Three (3)-Bar and Four (4)-Bar Plays StrategyThis strategy analyzes the three and four-bar play which is when price action has a wide igniting bar that has a full body, then one or two narrow bars which have a relatively equal high for long plays and relatively equal low for short plays, then a continuation bar. You should not take plays that will encounter resistance. The stop loss is placed for long plays below the 2nd bar (or 3rd bar for 4-bar play).

This is commonly used on 1m, 2m, 5m, and 10m charts.

Jared Wesley is one of the more notable traders that use this setup. You can edit as an input the start date, end date, igniting bar size, the body percentage of the igniting bar, the relative equality of the 2nd bar (and 3rd bar for 4-bar play) compared to the igniting bar, and profit multiplier.

7-RSI strategyHello, I've only been trying to learn PineScript for two months on my own, here I am posting a version of the strategy for a grid bot with 20 orders, order size 5%, earlier I tried to find something similar, but could not. Perhaps others, those who, like me, are just starting to learn PineScript, will find something useful. In the process of using grid bots, I noticed that the RSI indicator is sufficient, so the strategy uses 7 RSI indicators on different timeframes, but it is not necessary to use all 7, usually 3 is enough, therefore, by default, the RSI values are set to limit so that there is no effect on the settings of others. The step between bot orders is set in the settings. The code can of course be simplified, but it's better for understanding, I think.

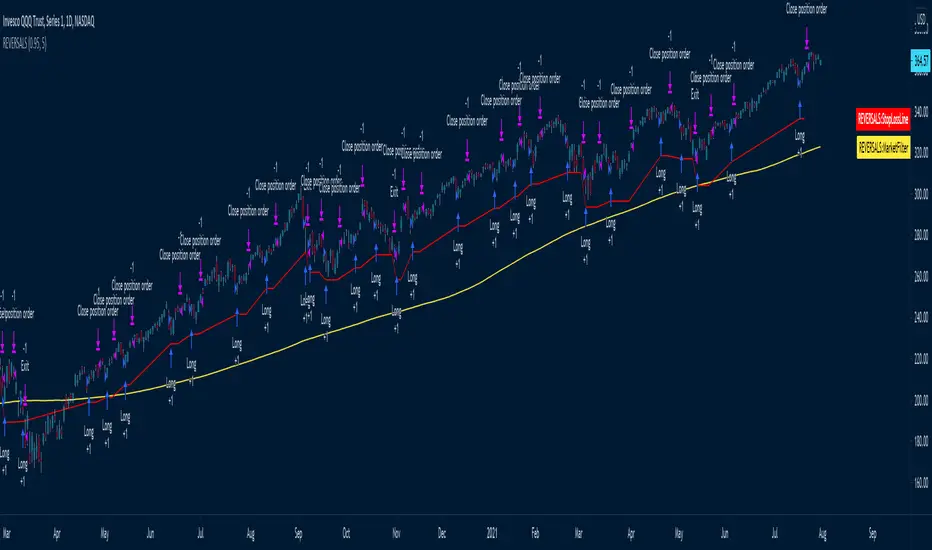

REVERSALS

The systems basically play reversals, it enters when the close is lower than its low of 5 bars ago to enter

It exits when the price is higher than the high of 5 days ago

Uses a 200 MA as a market filter, does not trade when the price is below its 200 Moving average

Uses a 5% stop, as per the red Stop Loss Line -- can be adjusted

The amount of bars it uses to look for reversals is set to 5 by default, but can be adjusted in settings.

Best to use on directional instruments where you know that the long term direction is up, for example:

TQQQ, SSO, SPX, SPY, or sector tickers -- but it would be best to include some more advanced filtering for sectors

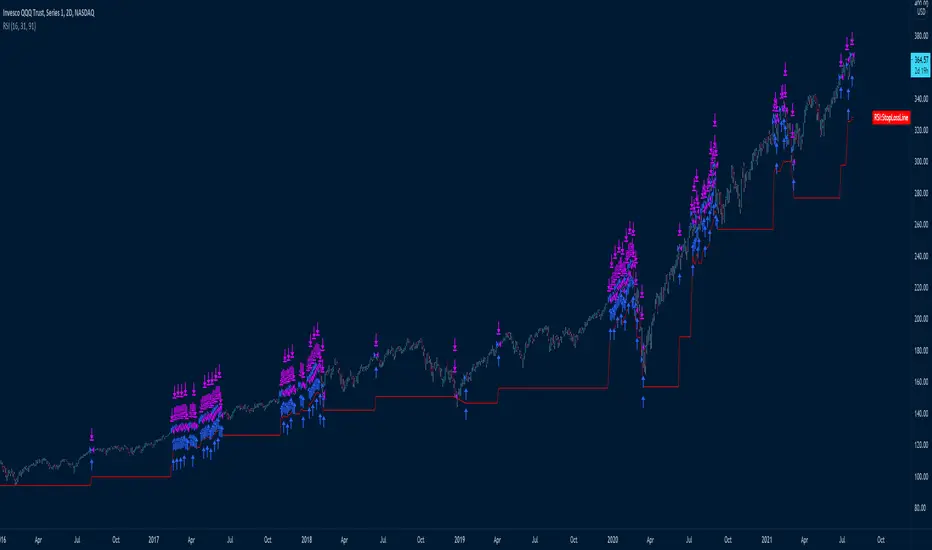

DUAL RSI

This system uses two RSI's with different settings

Fast RSI Lenght is 16, buys when RSI price is oversold @ 91 or lower, and sells when RSI price is overbought at 70

Slow RSI Lenght is 31, buys when RSI price is oversold @ 91 or lower, and sells when RSI price is overbought at 68

Pyramiding is set to 2 since each system should be able to trade in the same direction on the same day

The Red StopLine is a stop loss of 10% based on the combined strategic position average entry price.

I've used a 2D chart because I prefer longer-term charts for higher quality signals

The way I trade all the systems is to set up alerts to let me know when to look at what setups

The system also has a market filter and does not trade when the close is lower than its 200 days moving average

10PreBuyerQuite a simple system

Uses a moving average, the blue line to try and get filled at favorable prices

The MA is multiplied by a number (e.g. .90) which means the system tries to get filled at a 10% lower price (on the Blue MA line)

This means that stop limit buy orders have to be set in advance on the blue line and hope that they would get filled when there is a temporary drop in price

This obviously works best on tickers with a clear long-term up direction

The multiplier can be set to .95 to try and get in on 5% drops instead of 10% drops

"Prof TRG %" determines what profit target you'd like the system to use, default is 1.2 meaning a 20% target, but 1.05, 1.10, and 1.30 would also be good considerations

"Loss TRG %" determines what stop-loss target you'd like the system to use, default is 0.90, meaning 10% stop loss, but, .95, and .85 would also be good considerations

The Profit Target line is green

The Stop Loss target line is red

Using the combination of the Stop Loss inputs and Profit Target inputs you can determine your own RR (Risk to reward ratios), for example, 1:1, 2:1, 3:1, 5:1

Let me know if anything is unclear and I'll try to clarify.

Again, this system assumes that you'll have waiting stop limit orders that are trying to get filled on the blue line, is below price most of the time -- so it's trying to get in on temporary drops on instruments that have a long term uptrend.

1:1 RR ratio would mean high win %

1:5 RR ratios would mean low win %

Not that win % matters, the important things IMO to pay attention to is Profit Factor and a relatively smooth equity cruve