Global M2 Money Supply // Days Offset =This is the original version.. there is no update... just needed to re-install the script.

Forecasting

ATR % Line from LoD/HoDATR % Line Trading Indicator - Entry Filter Tool

This Pine Script creates a sophisticated ATR (Average True Range) percentage-based entry filter indicator for TradingView that helps traders avoid buying overextended stocks and identify optimal entry zones based on volatility.

Core Functionality - Entry Discipline

The script calculates a maximum entry threshold by taking a percentage of the Average True Range (ATR) and projecting it from the current day's low. This creates a dynamic "no-buy zone" that adapts to market volatility, helping traders avoid purchasing stocks that have already moved too far from their daily base.

Key Calculation:

Measures the ATR over a specified period (default: 14 bars)

Takes a user-defined percentage of that ATR (default: 25%)

Projects this distance from the day's low to establish a maximum entry threshold

Entry Rule: Avoid buying when price exceeds this ATR% level from the daily low or high.

Visual Features

Entry Threshold Line:

Draws a horizontal line at the calculated maximum entry level

Line extends forward for clear visualization of the "no-buy zone"

Red zones above this line indicate overextended conditions

Fully customizable appearance with color, width, and style options

Smart Entry Alerts:

Optional labels show the ATR percentage threshold and exact price level

Visual confirmation when stocks are trading in acceptable entry zones vs. extended areas

Real-Time Monitoring Table:

Displays current distance from daily low as ATR percentage

Shows whether current price is in "safe entry zone" or "extended territory"

Customizable display options for clean chart analysis

Practical Applications for Entry Management

Avoiding Extended Entries:

Primary Use: Don't initiate long positions when price is more than X% ATR from the daily low

Prevents buying stocks that have already made their daily move

Reduces risk of buying at temporary tops within the trading session

Entry Zone Identification:

Price trading below the ATR% line = potential entry opportunity

Price trading above the ATR% line = wait for pullback or skip the trade

Combines volatility analysis with momentum discipline

Risk Management Benefits:

Improved Entry Timing: Enter closer to daily support levels

Better Risk/Reward: Shorter distance to stop loss (daily low)

Reduced Chasing: Systematic approach prevents FOMO-driven entries

Volatility Awareness: Higher volatility stocks get wider acceptable entry ranges

Configuration for Entry Filtering

Key Settings for Entry Management:

ATR Percentage: Set your maximum acceptable extension (15-30% common for day trading)

Reference Point: Use "Low" to measure extension from daily base

Line Style: Make highly visible to clearly see entry threshold

Alert Integration: Visual confirmation of entry-friendly zones

Typical Usage Scenarios:

Conservative Entries: 15-20% ATR from daily low

Moderate Extensions: 25-35% ATR for stronger momentum plays

Aggressive Setups: 40%+ ATR for breakout situations (use with caution)

Entry Strategy Integration

Pre-Market Planning:

Set ATR% threshold based on stock's typical volatility

Identify key levels where entries become unfavorable

Plan alternative entry strategies for extended stocks

Intraday Execution:

Monitor real-time ATR% extension from daily low

Avoid new long positions when threshold is exceeded

Wait for pullbacks to re-enter acceptable entry zones

This tool transforms volatility analysis into practical entry discipline, helping traders maintain consistent entry standards and avoid the costly mistake of chasing overextended stocks. By respecting ATR-based extension limits, traders can improve their entry timing and overall trade profitability.

Market Energy – Trend vs Retest (with Saturation %)Market Energy – Trend vs Retest Indicator

This indicator measures the bullish and bearish energy in the market based on volume-weighted price changes.

It calculates two smoothed energy waves — bullish energy and bearish energy — using exponential moving averages of volume-adjusted price movements.

The indicator detects trend changes and retests by comparing the relative strength of these waves.

A saturation percentage quantifies the intensity of the current dominant side (bulls or bears) relative to recent highs.

- High saturation (>70%) indicates strong momentum and dominance by bulls or bears.

- Low saturation (<30%) suggests weak momentum and possible market indecision or consolidation.

The background color highlights the current control: green for bulls, red for bears, with transparency indicating the saturation level.

A label shows which side is currently in control along with the saturation percentage for quick interpretation.

Use this tool to identify strong trends, possible retests, and momentum strength to support your trading decisions.

Market Energy – Trend vs RetestShows who is in control of the market. The red lines are sellers in control and the green are the buyers in control

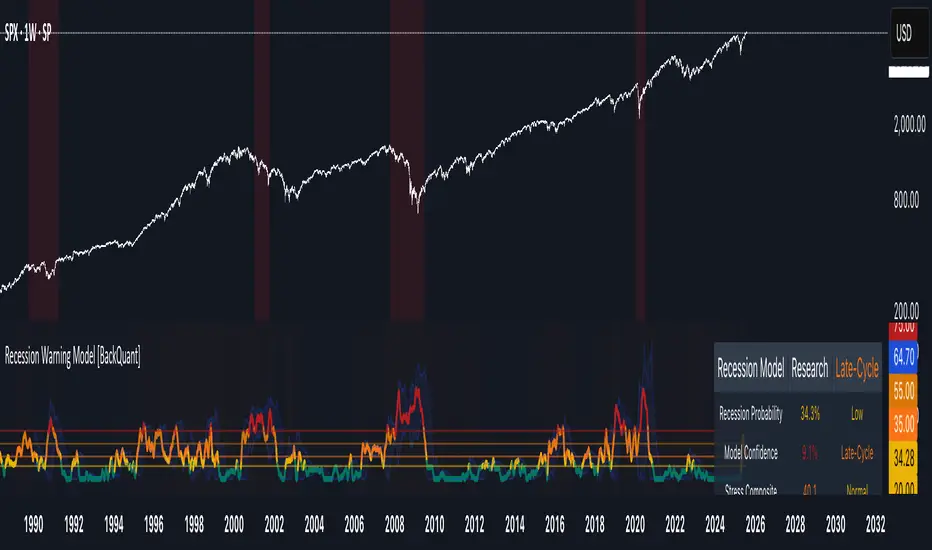

Recession Warning Model [BackQuant]Recession Warning Model

Overview

The Recession Warning Model (RWM) is a Pine Script® indicator designed to estimate the probability of an economic recession by integrating multiple macroeconomic, market sentiment, and labor market indicators. It combines over a dozen data series into a transparent, adaptive, and actionable tool for traders, portfolio managers, and researchers. The model provides customizable complexity levels, display modes, and data processing options to accommodate various analytical requirements while ensuring robustness through dynamic weighting and regime-aware adjustments.

Purpose

The RWM fulfills the need for a concise yet comprehensive tool to monitor recession risk. Unlike approaches relying on a single metric, such as yield-curve inversion, or extensive economic reports, it consolidates multiple data sources into a single probability output. The model identifies active indicators, their confidence levels, and the current economic regime, enabling users to anticipate downturns and adjust strategies accordingly.

Core Features

- Indicator Families : Incorporates 13 indicators across five categories: Yield, Labor, Sentiment, Production, and Financial Stress.

- Dynamic Weighting : Adjusts indicator weights based on recent predictive accuracy, constrained within user-defined boundaries.

- Leading and Coincident Split : Separates early-warning (leading) and confirmatory (coincident) signals, with adjustable weighting (default 60/40 mix).

- Economic Regime Sensitivity : Modulates output sensitivity based on market conditions (Expansion, Late-Cycle, Stress, Crisis), using a composite of VIX, yield-curve, financial conditions, and credit spreads.

- Display Options : Supports four modes—Probability (0-100%), Binary (four risk bins), Lead/Coincident, and Ensemble (blended probability).

- Confidence Intervals : Reflects model stability, widening during high volatility or conflicting signals.

- Alerts : Configurable thresholds (Watch, Caution, Warning, Alert) with persistence filters to minimize false signals.

- Data Export : Enables CSV output for probabilities, signals, and regimes, facilitating external analysis in Python or R.

Model Complexity Levels

Users can select from four tiers to balance simplicity and depth:

1. Essential : Focuses on three core indicators—yield-curve spread, jobless claims, and unemployment change—for minimalistic monitoring.

2. Standard : Expands to nine indicators, adding consumer confidence, PMI, VIX, S&P 500 trend, money supply vs. GDP, and the Sahm Rule.

3. Professional : Includes all 13 indicators, incorporating financial conditions, credit spreads, JOLTS vacancies, and wage growth.

4. Research : Unlocks all indicators plus experimental settings for advanced users.

Key Indicators

Below is a summary of the 13 indicators, their data sources, and economic significance:

- Yield-Curve Spread : Difference between 10-year and 3-month Treasury yields. Negative spreads signal banking sector stress.

- Jobless Claims : Four-week moving average of unemployment claims. Sustained increases indicate rising layoffs.

- Unemployment Change : Three-month change in unemployment rate. Sharp rises often precede recessions.

- Sahm Rule : Triggers when unemployment rises 0.5% above its 12-month low, a reliable recession indicator.

- Consumer Confidence : University of Michigan survey. Declines reflect household pessimism, impacting spending.

- PMI : Purchasing Managers’ Index. Values below 50 indicate manufacturing contraction.

- VIX : CBOE Volatility Index. Elevated levels suggest market anticipation of economic distress.

- S&P 500 Growth : Weekly moving average trend. Declines reduce wealth effects, curbing consumption.

- M2 + GDP Trend : Monitors money supply and real GDP. Simultaneous declines signal credit contraction.

- NFCI : Chicago Fed’s National Financial Conditions Index. Positive values indicate tighter conditions.

- Credit Spreads : Proxy for corporate bond spreads using 10-year vs. 2-year Treasury yields. Widening spreads reflect stress.

- JOLTS Vacancies : Job openings data. Significant drops precede hiring slowdowns.

- Wage Growth : Year-over-year change in average hourly earnings. Late-cycle spikes often signal economic overheating.

Data Processing

- Rate of Change (ROC) : Optionally applied to capture momentum in data series (default: 21-bar period).

- Z-Score Normalization : Standardizes indicators to a common scale (default: 252-bar lookback).

- Smoothing : Applies a short moving average to final signals (default: 5-bar period) to reduce noise.

- Binary Signals : Generated for each indicator (e.g., yield-curve inverted or PMI below 50) based on thresholds or Z-score deviations.

Probability Calculation

1. Each indicator’s binary signal is weighted according to user settings or dynamic performance.

2. Weights are normalized to sum to 100% across active indicators.

3. Leading and coincident signals are aggregated separately (if split mode is enabled) and combined using the specified mix.

4. The probability is adjusted by a regime multiplier, amplifying risk during Stress or Crisis regimes.

5. Optional smoothing ensures stable outputs.

Display and Visualization

- Probability Mode : Plots a continuous 0-100% recession probability with color gradients and confidence bands.

- Binary Mode : Categorizes risk into four levels (Minimal, Watch, Caution, Alert) for simplified dashboards.

- Lead/Coincident Mode : Displays leading and coincident probabilities separately to track signal divergence.

- Ensemble Mode : Averages traditional and split probabilities for a balanced view.

- Regime Background : Color-coded overlays (green for Expansion, orange for Late-Cycle, amber for Stress, red for Crisis).

- Analytics Table : Optional dashboard showing probability, confidence, regime, and top indicator statuses.

Practical Applications

- Asset Allocation : Adjust equity or bond exposures based on sustained probability increases.

- Risk Management : Hedge portfolios with VIX futures or options during regime shifts to Stress or Crisis.

- Sector Rotation : Shift toward defensive sectors when coincident signals rise above 50%.

- Trading Filters : Disable short-term strategies during high-risk regimes.

- Event Timing : Scale positions ahead of high-impact data releases when probability and VIX are elevated.

Configuration Guidelines

- Enable ROC and Z-score for consistent indicator comparison unless raw data is preferred.

- Use dynamic weighting with at least one economic cycle of data for optimal performance.

- Monitor stress composite scores above 80 alongside probabilities above 70 for critical risk signals.

- Adjust adaptation speed (default: 0.1) to 0.2 during Crisis regimes for faster indicator prioritization.

- Combine RWM with complementary tools (e.g., liquidity metrics) for intraday or short-term trading.

Limitations

- Macro indicators lag intraday market moves, making RWM better suited for strategic rather than tactical trading.

- Historical data availability may constrain dynamic weighting on shorter timeframes.

- Model accuracy depends on the quality and timeliness of economic data feeds.

Final Note

The Recession Warning Model provides a disciplined framework for monitoring economic downturn risks. By integrating diverse indicators with transparent weighting and regime-aware adjustments, it empowers users to make informed decisions in portfolio management, risk hedging, or macroeconomic research. Regular review of model outputs alongside market-specific tools ensures its effective application across varying market conditions.

Official USD Staggered Bands - ArgentinaOfficial USD Staggered Bands - Argentina

The Central Bank, under the administration of Javier Milei (La Libertad Avanza), announced on Friday, April 11, 2025, a series of measures to eliminate the so-called "exchange rate restriction."

In this new phase, the dollar's exchange rate on the Free Exchange Market (MLC) will be able to fluctuate within a band between $1,000 and $1,400 , the limits of which will be expanded at a rate of 1% monthly.

The lines evolve daily, increasing as the public administration predicts. This way, you can know the likelihood of a Central Bank intervention to correct the variation and return the peso to a price within the band.

The script runs under the ticker USDARS

ATR Plots + OverlayATR Plots + Overlay

This tool calculates and displays Average True Range (ATR)-based levels on your chart for any selected timeframe, giving traders a quick visual reference for expected price movement relative to the most recent bar’s open price. It plots guide levels above and below that open and shows how much of the typical ATR-based range has already been covered—all in one interactive table and on-chart overlay.

What It Does

ATR Calculation:

Uses true range data over a user-defined period (default 14), smoothed via RMA, SMA, EMA, or WMA, on the selected timeframe (e.g., 1h, 4h, daily) to calculate the ATR value.

Projected Levels:

Plots four reference levels relative to the open price of the most recent bar on the chosen timeframe:

+100% ATR: Open + ATR

+50% ATR: Open + 50% of ATR

−50% ATR: Open − 50% of ATR

−100% ATR: Open − ATR

Coverage %:

Tracks high and low prices for the current session on the selected timeframe and calculates what percentage of the ATR has already been covered:

Coverage % = (High − Low) ÷ ATR × 100

Interactive Table:

Shows the ATR value and current coverage percentage in a customizable table overlay. Position, color scheme, borders, transparency, and an optional empty top row are all adjustable via settings.

Customization Options

Table Settings:

Position the table (top/bottom × left/right).

Customize background color, text color, border color, and thickness.

Optionally add an empty top row for spacing.

Line Settings:

Choose color, line style (solid/dotted/dashed), and width.

Lines automatically update with each new bar on the selected timeframe, anchored to that bar’s open price.

General Inputs:

ATR length (number of bars).

Smoothing method (RMA, SMA, EMA, WMA).

Timeframe selection for ATR calculations (e.g., 15m, 1h, Daily).

How to Use It for Trading

Measure Volatility: Quickly gauge the expected price movement based on ATR for any timeframe.

Identify Overextension: Use the coverage % to see how much of the expected ATR range is already consumed.

Plan Entries & Exits: Align trade targets and stops with ATR levels for more objective planning.

Visual Reference: Horizontal guide lines and table update automatically as new bars form, keeping information clear and actionable.

Ideal For

Intraday traders using ATR levels to frame trades.

Swing traders wanting ATR-based reference points for larger timeframes.

Anyone seeking a volatility-based framework for planning stops, targets, or identifying overextended conditions.

Taylor Rule (Styled by Mongoose) + Macro Action PlanMethodology:

This indicator implements the standard Taylor Rule to estimate a theoretically neutral federal funds rate (FFR) based on economic conditions.

Taylor Rule Formula:

FFR = r* + π + 0.5(π - π*) + 0.5 × Output Gap

π = current inflation rate

π* = inflation target

r* = natural real interest rate

Output Gap = 100 × (u* - u) / u*

u = actual unemployment rate

u* = natural unemployment rate

Visuals:

Teal Line = Taylor Rule Rate

Orange Line = Manual Fed Funds Rate (custom input)

Color Zone Highlight

Red = policy rate far below Taylor estimate (gap > +1.0)

Green = policy rate far above Taylor estimate (gap < -1.0)

Reference Lines:

0% (Zero Bound)

2% (Neutral Rate)

5% (Hawkish Zone)

How to Use:

A Taylor Rate above the actual Fed Funds Rate may imply accommodative conditions.

A Taylor Rate below the actual Fed Funds Rate may imply restrictive or tight policy.

The gap between the Taylor estimate and actual rate helps assess potential macro pressure on markets, yields, and risk assets.

Trader Application:

Helps forecast shifts in Fed stance and macro policy inflection points

Use as a regime filter for positioning in equities, bonds, FX, and commodities

Can support long/short macro strategies based on rate gap and inflation dynamics

Inputs (Editable):

Inflation rate

Inflation target

Neutral real rate (r*)

Actual and natural unemployment rate

Manual FFR value

Bracket PreviewThe Bracket Preview indicator allows the user to set their intended bracket order distance (distance, in ticks, to take-profit and stop-loss) from the current live price so that a preview is generated and updated in real-time as price moves. This gives the trader a quick reference of where the bracket orders would be placed if a position were entered at that specific moment in time. This can be helpful by making it more obvious to the trader before a trade is placed exactly where these levels would be in relation to previous price action or if it would be better to wait for price to move to a more favorable level or accept a different Risk-Reward (RR) from this specific trade.

• “If I entered a long position now, would my target be in front of or beyond a recent consolidation area where it is likely to run into resistance and potentially reverse before hitting my take-profit?”

• “Would this bracket order place my stop-loss above or below a previous pivot or would I need to move it after entering the trade and potentially increase the risk on this trade to have it in a more logical level?”

• “If price is in a range and I enter now, would my stop be in the middle of the range while my target is outside the top of the range? Maybe I should wait for price to move to an area where my target would be inside but near the top of the range while my stop loss is below the range so that I’m not taking unnecessary risk or being forced to take an unfavorable RR.”

BUY in HASH RibbonsHash Ribbons Indicator (BUY Signal)

A TradingView Pine Script v6 implementation for identifying Bitcoin miner capitulation (“Springs”) and recovery phases based on hash rate data. It marks potential low-risk buying opportunities by tracking short- and long-term moving averages of the network hash rate.

⸻

Key Features

• Hash Rate SMAs

• Short-term SMA (default: 30 days)

• Long-term SMA (default: 60 days)

• Phase Markers

• Gray circle: Short SMA crosses below long SMA (start of capitulation)

• White circles: Ongoing capitulation, with brighter white when the short SMA turns upward

• Yellow circle: Short SMA crosses back above long SMA (end of capitulation)

• Orange circle: Buy signal once hash rate recovery aligns with bullish price momentum (10-day price SMA crosses above 20-day price SMA)

• Display Modes

• Ribbons: Plots the two SMAs as colored bands—red for capitulation, green for recovery

• Oscillator: Shows the percentage difference between SMAs as a histogram (red for negative, blue for positive)

• Optional Overlays

• Bitcoin halving dates (2012, 2016, 2020, 2024) with dashed lines and labels

• Raw hash rate data in EH/s

• Alerts

• Configurable alerts for capitulation start, recovery, and buy signals

⸻

How It Works

1. Data Source: Fetches daily hash rate values from a selected provider (e.g., IntoTheBlock, Quandl).

2. Capitulation Detection: When the 30-day SMA falls below the 60-day SMA, miners are likely capitulating.

3. Recovery Identification: A rising 30-day SMA during capitulation signals miner recovery.

4. Buy Signal: Confirmed when the hash rate recovery coincides with a bullish shift in price momentum (10-day price SMA > 20-day price SMA).

⸻

Inputs

Hash Rate Short SMA: 30 days

Hash Rate Long SMA: 60 days

Plot Signals: On

Plot Halvings: Off

Plot Raw Hash Rate: Off

⸻

Considerations

• Timeframe: Best applied on daily charts to capture meaningful miner behavior.

• Data Reliability: Ensure the chosen hash rate source provides consistent, gap-free data.

• Risk Management: Use alongside other technical indicators (e.g., RSI, MACD) and fundamental analysis.

• Backtesting: Evaluate performance over different market cycles before live deployment.

Combined Predictive Indicator### Combined Predictive Zones & Levels

This indicator is a powerful hybrid tool designed to provide a comprehensive map of potential future price action. It merges two distinct predictive models into a single, cohesive view, helping traders identify key levels of support, resistance, and areas of high confluence.

#### How It Works: Two Models in One

This script is built on two core components that you can use together or analyze separately:

**Part 1: Classic Range & Fibonacci Prediction**

This model uses classic technical analysis principles to project a potential range for the upcoming price action.

* **Highest High / Lowest Low:** It identifies the significant trading range over a user-defined lookback period.

* **Fibonacci Levels:** It automatically plots key Fibonacci retracement levels (e.g., 38.2% and 61.8%) within this range, which often act as critical support or resistance.

* **ATR & Average Range:** It calculates a "predicted" upper and lower boundary based on the average historical range and current volatility (ATR).

**Part 2: Advanced Predictive Ranges (Self-Adjusting Channels)**

This is a dynamic model that creates adaptive support and resistance zones based on a smoothed average price and volatility.

* **Dynamic Average:** It uses a unique moving average that only adjusts when the price moves significantly, creating a stable baseline.

* **ATR-Based Zones:** It projects multiple levels of support (S1, S2) and resistance (R1, R2) around this average, which widen and narrow based on market volatility. These zones often signal areas where price might stall or reverse.

#### Key Features:

* **Hybrid Model for Confluence:** The true power of this indicator lies in finding where the levels from both models overlap. A Fibonacci level aligning with a Predictive Range support zone is a much stronger signal.

* **Comprehensive Data Table:** A clean, on-chart table displays the precise values of all key predictive levels, allowing for quick reference and precise trade planning.

* **Multi-Timeframe (MTF) Capability:** The Advanced Predictive Ranges can be calculated on a higher timeframe, giving you a broader market context.

* **Fully Customizable:** All lengths, multipliers, and levels for both models are fully adjustable in the settings to fit any asset or trading style.

* **Clear Visuals:** All zones and levels are color-coded for intuitive and easy-to-read analysis.

#### How to Use:

1. Look for areas of **confluence** where multiple levels from both models cluster together. These are high-probability zones for price reactions.

2. Use the Predictive Range zones (S1/S2 and R1/R2) as potential targets for trades or as areas to watch for entries and exits.

3. Pay attention to the on-chart table for exact price levels to set limit orders or stop-losses.

**Disclaimer:** This script is an analytical tool for educational purposes and should not be considered financial advice. All trading involves risk. Past performance is not indicative of future results. Always use this indicator as part of a comprehensive trading strategy with proper risk management.

Feedback is welcome! If you find this tool useful, please leave a like.

3 EMA Pullback Strategy with ATRThis script will not only plot the moving averages but also identify potential trade setups by highlighting trend conditions, marking entry points, and dynamically plotting the corresponding Stop Loss and Take Profit levels directly on your chart.

Here is the Pine Script code for your strategy.

Multi timeframe trendDESCRIPTION

This indicator, Multi Timeframe Trend, is a powerful tool designed to give traders a comprehensive overview of market trends across multiple timeframes using a single, customizable Exponential Moving Average (EMA). It visually displays whether the price is trading above or below the EMA on each timeframe, helping traders quickly determine the dominant trend at a glance.

The real-time dashboard is plotted directly on your chart and color-coded to show bullish (green) or bearish (red) conditions per timeframe, from 15 minutes to 1 week. It is especially helpful for identifying trend alignment across multiple timeframes—an essential component of many professional trading strategies.

USER INPUTS

* Enter the EMA length – Adjust the EMA period used in the trend calculation (default: 200)

* Table Size – Choose how large the on-chart table appears: "tiny", "small", "normal", or "large"

INDICATOR LOGIC

* The indicator calculates the EMA for each of the following timeframes: 1W, 1D, 4H, 1H, 30M, and 15M

* It checks whether the current close is above or below each EMA and labels it as:

* Bullish if close > EMA

* Bearish if close < EMA

* Each timeframe’s trend is displayed in a dynamic table in the top-right corner of the chart

* The background color of each cell changes according to trend condition for quick visual interpretation

* Real-time responsiveness: handles both historical and live bars to maintain accurate, flicker-free updates

WHY IT IS UNIQUE

* Combines multiple timeframe trend analysis into a single glance

* Clean and color-coded dashboard overlay for real-time trading decisions

* Avoids repainting using barstate logic for accurate trend updates

* Fully customizable table size and EMA length

* Works on any chart, including stocks, crypto, forex, indices

HOW USERS CAN BENEFIT FROM IT

* Multi-timeframe confirmation: Easily confirm alignment across timeframes before entering a trade

* Avoid false signals by ensuring higher timeframe trends agree with lower timeframe setups

* Enhance strategy filters: Use as a trend filter in combination with your existing entry indicators

* Quick market analysis: No need to switch between charts or manually calculate EMAs

* Visual clarity: Trend conditions are easy to read and interpret in real-time

ATR as % of CloseATR 14day period in % terms

the Normal ATR indicator by TV helps but this gives a clear idea as to the range in percentage terms as and when market rises to newer and newer highs

better than an absolute value

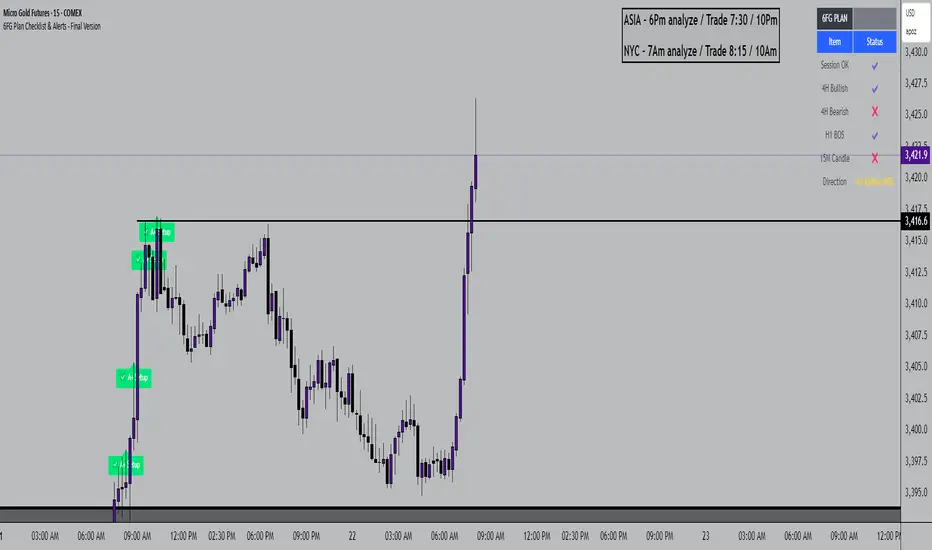

6FG Plan Checklist & Alerts - Final Version🧠 SCRIPT OVERVIEW: "6FG A+ SETUP - Simplified"

This script is designed to identify high-probability A+ trade setups in alignment with your personal 6FG trading plan, based on:

H1 Break of Structure (required)

4H trend confirmation

15M candle confirmation

Session filter

A+ Label & Visual Table Checklist

✅ KEY COMPONENTS

1. Toggle Inputs

These allow you to customize your view and filters without changing the code:

showSession: Only allow alerts inside Asian or NY sessions

show4hTrend: Include or ignore 4H directional bias

show15mConfirm: Include or ignore confirmation from 15M candles

showTable: Display checklist table on chart

showLabel: Display the “✅ A+” label on qualifying bars

2. Session Filter

Defines valid timeframes for trading (Asian or New York)

Helps avoid setups during low-liquidity hours

Controlled by showSession

3. 4H Trend (Confirmation Only)

Uses a 20-period SMA on 4H to detect general bias:

Bullish = Price above SMA

Bearish = Price below SMA

This trend is not mandatory for an alert if toggle is off

4. H1 Break of Structure (REQUIRED)

Looks at the highest high and lowest low of the last 10 candles on the 1H timeframe

Detects either:

Bullish BOS = Current close > highest high

Bearish BOS = Current close < lowest low

This is the core trigger for the A+ setup

If BOS doesn't happen, no entry is valid

5. 15M Confirmation Candles

(Optional - controlled by show15mConfirm)

Checks for one of three confirmation patterns:

Bullish Engulfing

Bearish Engulfing

Pin Bar

This adds confidence but can be toggled off

6. Entry Conditions (A+ Setup)

All the following must be true for entryOK = true:

✅ H1 BOS (required)

✅ Session is valid (if toggle is on)

✅ 15M confirmation pattern (if toggle is on)

✅ 4H trend (if toggle is on)

7. Visual Output

If entryOK = true:

✅ A green "A+" label appears below price

✅ A checklist table on the top-right shows:

Session status ✔️❌

4H bullish/bearish ✔️❌

H1 BOS ✔️❌

15M confirmation ✔️❌

Final Direction: Bullish / Bearish / —

A+ Setup: ✔️❌

8. Alerts

You will receive a TradingView alert when an A+ Setup is detected:

FTM → SONIC Combined Candlesticksthis script combines the chart of FTM and SONIC to get a better overview of the entire price action

Markov Chain Trend ProbabilityA Markov Chain is a mathematical model that predicts future states based on the current state, assuming that the future depends only on the present (not the past). Originally developed by Russian mathematician Andrey Markov, this concept is widely used in:

Finance: Risk modeling, portfolio optimization, credit scoring, algorithmic trading

Weather Forecasting: Predicting sunny/rainy days, temperature patterns, storm tracking

Here's an example of a Markov chain: If the weather is sunny, the probability that will be sunny 30 min later is say 90%. However, if the state changes, i.e. it starts raining, how the probability that will be raining 30 min later is say 70% and only 30% sunny.

Similar concept can be applied to markets price action and trends.

Mathematical Foundation

The core principle follows the Markov Property: P(X_{t+1}|X_t, X_{t-1}, ..., X_0) = P(X_{t+1}|X_t)

Transition Matrix :

-------------Next State

Current----

--------P11 P12

-----P21 P22

Probability Calculations:

P(Up→Up) = Count(Up→Up) / Count(Up states)

P(Down→Down) = Count(Down→Down) / Count(Down states)

Steady-state probability: π = πP (where π is the stationary distribution)

State Definition:

State = UPTREND if (Price_t - Price_{t-n})/ATR > threshold

State = DOWNTREND if (Price_t - Price_{t-n})/ATR < -threshold

How It Works in Trading

This indicator applies Markov Chain theory to market trends by:

Defining States: Classifies market conditions as UPTREND or DOWNTREND based on price movement relative to ATR (Average True Range)

Learning Transitions: Analyzes historical data to calculate probabilities of moving from one state to another

Predicting Probabilities: Estimates the likelihood of future trend continuation or reversal

How to Use

Parameters:

Lookback Period: Number of bars to analyze for trend detection (default: 14)

ATR Threshold: Sensitivity multiplier for state changes (default: 0.5)

Historical Periods: Sample size for probability calculations (default: 33)

Trading Applications:

Trend confirmation for entry/exit decisions

Risk assessment through probability analysis

Market regime identification

Early warning system for potential trend reversals

The indicator works on any timeframe and asset class. Enjoy!

Clarix 5m Scalping Breakout StrategyPurpose

A 5-minute scalping breakout strategy designed to capture fast 3-5 pip moves, using premium/discount zone filters and market bias conditions.

How It Works

The script monitors price action in 5-minute intervals, forming a 15-minute high and low range by tracking the highs and lows of the first 3 consecutive 5-minute candles starting from a custom time. In the next 3 candles, it waits for a breakout above the 15m high or below the 15m low while confirming market bias using custom equilibrium zones.

Buy signals trigger when price breaks the 15m high while in a discount zone

Sell signals trigger when price breaks the 15m low while in a premium zone

The strategy simulates trades with fixed 3-5 pip take profit and stop loss values (configurable). All trades are recorded in a backtest table with live trade results and an automatically updated win rate.

Features

Designed exclusively for the 5-minute timeframe

Custom 15-minute high/low breakout logic

Premium, Discount, and Equilibrium zone display

Built-in backtest tracker with live trade results, statistics, and win rate

Customizable start time, take profit, and stop loss settings

Real-time alerts on breakout signals

Visual markers for trade entries and failed trades

Consistent win rate exceeding 90–95% on average when following market conditions

Usage Tips

Use strictly on 5-minute charts for accurate signal performance. Avoid during high-impact news releases.

Important: Once a trade is opened, manually set your take profit at +3 to +5 pips immediately to secure the move, as these quick scalps often hit the target within a single candle. This prevents missed exits during rapid price action.

30s OR ProjectionsThis script gets the opening range for NQ,ES, and YM. It then created deviations based on this range as targets to take profit from. You may also use the deviations to enter into trades looking for the other side of the range. You have the ability to shade areas of the range.

Date Marker GPTDate Marker GPT

By Jimmy Dimos (corrected by ChatGPT-o3)

Description

This overlay indicator automatically plots vertical lines at each weekly option-expiration timestamp (Friday at 3 PM CST) for both historical and upcoming periods, helping you visualize key expiration dates alongside your price action and regression tools. Shown is my Date Maker GPT vertical blue Lines, Linear Regression Channel(not part of my script) and zigzag++ also not part of my script.

⸻

Key Features

• Past Expirations: Draws 12 past Friday markers at 3 PM CST

• Future Expirations: Projects 12 upcoming Friday markers at 3 PM CST

• Timezone Handling: Uses UTC internally (21:00 UTC = 3 PM CST)

• Customizable: num_fridays_past and num_fridays_future inputs let you adjust how many weeks to display

⸻

How It Works

1. Timestamp Calculation

• Uses Pine Script’s dayofweek() and timestamp() functions to find each Friday at the target hour.

• Two helper functions, get_previous_friday() and get_next_friday(), compute offsets in days/weeks based on the current bar’s date.

2. Drawing Lines

• Loops through the specified number of weeks in the past and future.

• Calls line.new() for each expiration timestamp, extending lines across the entire chart.

⸻

Usage Tips

• Overlay this script on any OHLC chart to see how price tends to cluster around option expirations.

• Combine with a linear regression or trend-channel indicator to anticipate likely trading ranges leading into expiration.

• Tweak the num_fridays_past and num_fridays_future parameters to focus on shorter or longer horizons.

⸻

Disclaimer: This tool is provided for educational and analytical purposes only. It is not financial advice. Always conduct your own research and risk management.