GKD-C STD-Filtered, Truncated Taylor FIR Filter [Loxx]Giga Kaleidoscope GKD-C STD-Filtered, Truncated Taylor Family FIR Filter is a Confirmation module included in Loxx's "Giga Kaleidoscope Modularized Trading System".

█ GKD-C STD-Filtered, Truncated Taylor Family FIR Filter

Exploring the Truncated Taylor Family FIR Filter with Standard Deviation Filtering

Filters play a vital role in signal processing, allowing us to extract valuable information from raw data by removing unwanted noise or highlighting specific features. In the context of financial data analysis, filtering techniques can help traders identify trends and make informed decisions. Below, we delve into the workings of a Truncated Taylor Family Finite Impulse Response (FIR) Filter with standard deviation filtering applied to the input and output signals. We will examine the code provided, breaking down the mathematical formulas and concepts behind it.

The code consists of two main sections: the design function that calculates the FIR filter coefficients and the stdFilter function that applies standard deviation filtering to the input signal.

design(int per, float taylorK)=>

float coeffs = array.new(per, 0)

float coeffsSum = 0

float _div = per + 1.0

float _coeff = 1

for i = 0 to per - 1

_coeff := (1 + taylorK) / 2 - (1 - taylorK) / 2 * math.cos(2.0 * math.pi * (i + 1) / _div)

array.set(coeffs,i, _coeff)

coeffsSum += _coeff

stdFilter(float src, int len, float filter)=>

float price = src

float filtdev = filter * ta.stdev(src, len)

price := math.abs(price - nz(price )) < filtdev ? nz(price ) : price

price

Design Function

The design function takes two arguments: an integer 'per' representing the number of coefficients for the FIR filter, and a floating-point number 'taylorK' to adjust the filter's characteristics. The function initializes an array 'coeffs' of length 'per' and sets all elements to 0. It also initializes variables 'coeffsSum', '_div', and '_coeff' to store the sum of the coefficients, a divisor for the cosine calculation, and the current coefficient, respectively.

A for loop iterates through the range of 0 to per-1, calculating the FIR filter coefficients using the formula:

_coeff := (1 + taylorK) / 2 - (1 - taylorK) / 2 * math.cos(2.0 * math.pi * (i + 1) / _div)

The calculated coefficients are stored in the 'coeffs' array, and their sum is stored in 'coeffsSum'. The function returns both 'coeffs' and 'coeffsSum' as a list.

stdFilter Function

The stdFilter function takes three arguments: a floating-point number 'src' representing the input signal, an integer 'len' for the standard deviation calculation period, and a floating-point number 'filter' to adjust the standard deviation filtering strength.

The function initializes a 'price' variable equal to 'src' and calculates the filtered standard deviation 'filtdev' using the formula:

filtdev = filter * ta.stdev(src, len)

The 'price' variable is then updated based on whether the absolute difference between the current price and the previous price is less than 'filtdev'. If true, 'price' is set to the previous price, effectively filtering out noise. Otherwise, 'price' remains unchanged.

Application of Design and stdFilter Functions

First, the input signal 'src' is filtered using the stdFilter function if the 'filterop' variable is set to "Both" or "Price", and 'filter' is greater than 0.

Next, the design function is called with the 'per' and 'taylorK' arguments to calculate the FIR filter coefficients and their sum. These values are stored in 'coeffs' and 'coeffsSum', respectively.

A for loop iterates through the range of 0 to per-1, calculating the filtered output 'dSum' using the formula:

dSum += nz(src ) * array.get(coeffs, k)

The output signal 'out' is then computed by dividing 'dSum' by 'coeffsSum' if 'coeffsSum' is not equal to 0; otherwise, 'out' is set to 0.

Finally, the output signal 'out' is filtered using the stdFilter function if the 'filterop' variable is set to "Both" or "Truncated Taylor FIR Filter", and 'filter' is greater than 0. The filtered signal is stored in the 'sig' variable.

The Truncated Taylor Family FIR Filter with Standard Deviation Filtering combines the strengths of two powerful filtering techniques to process financial data. By first designing the filter coefficients using the Taylor family FIR filter and then applying standard deviation filtering, the algorithm effectively removes noise and highlights relevant trends in the input signal. This approach allows traders and analysts to make more informed decisions based on the processed data.

In summary, the provided code effectively demonstrates how to create a custom FIR filter based on the Truncated Taylor family, along with standard deviation filtering applied to both input and output signals. This combination of filtering techniques enhances the overall filtering performance, making it a valuable tool for financial data analysis and decision-making processes. As the world of finance continues to evolve and generate increasingly complex data, the importance of robust and efficient filtering techniques cannot be overstated.

█ Giga Kaleidoscope Modularized Trading System

Core components of an NNFX algorithmic trading strategy

The NNFX algorithm is built on the principles of trend, momentum, and volatility. There are six core components in the NNFX trading algorithm:

1. Volatility - price volatility; e.g., Average True Range, True Range Double, Close-to-Close, etc.

2. Baseline - a moving average to identify price trend

3. Confirmation 1 - a technical indicator used to identify trends

4. Confirmation 2 - a technical indicator used to identify trends

5. Continuation - a technical indicator used to identify trends

6. Volatility/Volume - a technical indicator used to identify volatility/volume breakouts/breakdown

7. Exit - a technical indicator used to determine when a trend is exhausted

What is Volatility in the NNFX trading system?

In the NNFX (No Nonsense Forex) trading system, ATR (Average True Range) is typically used to measure the volatility of an asset. It is used as a part of the system to help determine the appropriate stop loss and take profit levels for a trade. ATR is calculated by taking the average of the true range values over a specified period.

True range is calculated as the maximum of the following values:

-Current high minus the current low

-Absolute value of the current high minus the previous close

-Absolute value of the current low minus the previous close

ATR is a dynamic indicator that changes with changes in volatility. As volatility increases, the value of ATR increases, and as volatility decreases, the value of ATR decreases. By using ATR in NNFX system, traders can adjust their stop loss and take profit levels according to the volatility of the asset being traded. This helps to ensure that the trade is given enough room to move, while also minimizing potential losses.

Other types of volatility include True Range Double (TRD), Close-to-Close, and Garman-Klass

What is a Baseline indicator?

The baseline is essentially a moving average, and is used to determine the overall direction of the market.

The baseline in the NNFX system is used to filter out trades that are not in line with the long-term trend of the market. The baseline is plotted on the chart along with other indicators, such as the Moving Average (MA), the Relative Strength Index (RSI), and the Average True Range (ATR).

Trades are only taken when the price is in the same direction as the baseline. For example, if the baseline is sloping upwards, only long trades are taken, and if the baseline is sloping downwards, only short trades are taken. This approach helps to ensure that trades are in line with the overall trend of the market, and reduces the risk of entering trades that are likely to fail.

By using a baseline in the NNFX system, traders can have a clear reference point for determining the overall trend of the market, and can make more informed trading decisions. The baseline helps to filter out noise and false signals, and ensures that trades are taken in the direction of the long-term trend.

What is a Confirmation indicator?

Confirmation indicators are technical indicators that are used to confirm the signals generated by primary indicators. Primary indicators are the core indicators used in the NNFX system, such as the Average True Range (ATR), the Moving Average (MA), and the Relative Strength Index (RSI).

The purpose of the confirmation indicators is to reduce false signals and improve the accuracy of the trading system. They are designed to confirm the signals generated by the primary indicators by providing additional information about the strength and direction of the trend.

Some examples of confirmation indicators that may be used in the NNFX system include the Bollinger Bands, the MACD (Moving Average Convergence Divergence), and the MACD Oscillator. These indicators can provide information about the volatility, momentum, and trend strength of the market, and can be used to confirm the signals generated by the primary indicators.

In the NNFX system, confirmation indicators are used in combination with primary indicators and other filters to create a trading system that is robust and reliable. By using multiple indicators to confirm trading signals, the system aims to reduce the risk of false signals and improve the overall profitability of the trades.

What is a Continuation indicator?

In the NNFX (No Nonsense Forex) trading system, a continuation indicator is a technical indicator that is used to confirm a current trend and predict that the trend is likely to continue in the same direction. A continuation indicator is typically used in conjunction with other indicators in the system, such as a baseline indicator, to provide a comprehensive trading strategy.

What is a Volatility/Volume indicator?

Volume indicators, such as the On Balance Volume (OBV), the Chaikin Money Flow (CMF), or the Volume Price Trend (VPT), are used to measure the amount of buying and selling activity in a market. They are based on the trading volume of the market, and can provide information about the strength of the trend. In the NNFX system, volume indicators are used to confirm trading signals generated by the Moving Average and the Relative Strength Index. Volatility indicators include Average Direction Index, Waddah Attar, and Volatility Ratio. In the NNFX trading system, volatility is a proxy for volume and vice versa.

By using volume indicators as confirmation tools, the NNFX trading system aims to reduce the risk of false signals and improve the overall profitability of trades. These indicators can provide additional information about the market that is not captured by the primary indicators, and can help traders to make more informed trading decisions. In addition, volume indicators can be used to identify potential changes in market trends and to confirm the strength of price movements.

What is an Exit indicator?

The exit indicator is used in conjunction with other indicators in the system, such as the Moving Average (MA), the Relative Strength Index (RSI), and the Average True Range (ATR), to provide a comprehensive trading strategy.

The exit indicator in the NNFX system can be any technical indicator that is deemed effective at identifying optimal exit points. Examples of exit indicators that are commonly used include the Parabolic SAR, the Average Directional Index (ADX), and the Chandelier Exit.

The purpose of the exit indicator is to identify when a trend is likely to reverse or when the market conditions have changed, signaling the need to exit a trade. By using an exit indicator, traders can manage their risk and prevent significant losses.

In the NNFX system, the exit indicator is used in conjunction with a stop loss and a take profit order to maximize profits and minimize losses. The stop loss order is used to limit the amount of loss that can be incurred if the trade goes against the trader, while the take profit order is used to lock in profits when the trade is moving in the trader's favor.

Overall, the use of an exit indicator in the NNFX trading system is an important component of a comprehensive trading strategy. It allows traders to manage their risk effectively and improve the profitability of their trades by exiting at the right time.

How does Loxx's GKD (Giga Kaleidoscope Modularized Trading System) implement the NNFX algorithm outlined above?

Loxx's GKD v1.0 system has five types of modules (indicators/strategies). These modules are:

1. GKD-BT - Backtesting module (Volatility, Number 1 in the NNFX algorithm)

2. GKD-B - Baseline module (Baseline and Volatility/Volume, Numbers 1 and 2 in the NNFX algorithm)

3. GKD-C - Confirmation 1/2 and Continuation module (Confirmation 1/2 and Continuation, Numbers 3, 4, and 5 in the NNFX algorithm)

4. GKD-V - Volatility/Volume module (Confirmation 1/2, Number 6 in the NNFX algorithm)

5. GKD-E - Exit module (Exit, Number 7 in the NNFX algorithm)

(additional module types will added in future releases)

Each module interacts with every module by passing data between modules. Data is passed between each module as described below:

GKD-B => GKD-V => GKD-C(1) => GKD-C(2) => GKD-C(Continuation) => GKD-E => GKD-BT

That is, the Baseline indicator passes its data to Volatility/Volume. The Volatility/Volume indicator passes its values to the Confirmation 1 indicator. The Confirmation 1 indicator passes its values to the Confirmation 2 indicator. The Confirmation 2 indicator passes its values to the Continuation indicator. The Continuation indicator passes its values to the Exit indicator, and finally, the Exit indicator passes its values to the Backtest strategy.

This chaining of indicators requires that each module conform to Loxx's GKD protocol, therefore allowing for the testing of every possible combination of technical indicators that make up the six components of the NNFX algorithm.

What does the application of the GKD trading system look like?

Example trading system:

Backtest: Strategy with 1-3 take profits, trailing stop loss, multiple types of PnL volatility, and 2 backtesting styles

Baseline: Hull Moving Average

Volatility/Volume: Hurst Exponent

Confirmation 1: STD-Filtered, Truncated Taylor Family FIR Filter as shown on the chart above

Confirmation 2: Williams Percent Range

Continuation: Fisher Transform

Exit: Rex Oscillator

Each GKD indicator is denoted with a module identifier of either: GKD-BT, GKD-B, GKD-C, GKD-V, or GKD-E. This allows traders to understand to which module each indicator belongs and where each indicator fits into the GKD protocol chain.

Giga Kaleidoscope Modularized Trading System Signals (based on the NNFX algorithm)

Standard Entry

1. GKD-C Confirmation 1 Signal

2. GKD-B Baseline agrees

3. Price is within a range of 0.2x Volatility and 1.0x Volatility of the Goldie Locks Mean

4. GKD-C Confirmation 2 agrees

5. GKD-V Volatility/Volume agrees

Baseline Entry

1. GKD-B Baseline signal

2. GKD-C Confirmation 1 agrees

3. Price is within a range of 0.2x Volatility and 1.0x Volatility of the Goldie Locks Mean

4. GKD-C Confirmation 2 agrees

5. GKD-V Volatility/Volume agrees

6. GKD-C Confirmation 1 signal was less than 7 candles prior

Volatility/Volume Entry

1. GKD-V Volatility/Volume signal

2. GKD-C Confirmation 1 agrees

3. Price is within a range of 0.2x Volatility and 1.0x Volatility of the Goldie Locks Mean

4. GKD-C Confirmation 2 agrees

5. GKD-B Baseline agrees

6. GKD-C Confirmation 1 signal was less than 7 candles prior

Continuation Entry

1. Standard Entry, Baseline Entry, or Pullback; entry triggered previously

2. GKD-B Baseline hasn't crossed since entry signal trigger

3. GKD-C Confirmation Continuation Indicator signals

4. GKD-C Confirmation 1 agrees

5. GKD-B Baseline agrees

6. GKD-C Confirmation 2 agrees

1-Candle Rule Standard Entry

1. GKD-C Confirmation 1 signal

2. GKD-B Baseline agrees

3. Price is within a range of 0.2x Volatility and 1.0x Volatility of the Goldie Locks Mean

Next Candle:

1. Price retraced (Long: close < close or Short: close > close )

2. GKD-B Baseline agrees

3. GKD-C Confirmation 1 agrees

4. GKD-C Confirmation 2 agrees

5. GKD-V Volatility/Volume agrees

1-Candle Rule Baseline Entry

1. GKD-B Baseline signal

2. GKD-C Confirmation 1 agrees

3. Price is within a range of 0.2x Volatility and 1.0x Volatility of the Goldie Locks Mean

4. GKD-C Confirmation 1 signal was less than 7 candles prior

Next Candle:

1. Price retraced (Long: close < close or Short: close > close )

2. GKD-B Baseline agrees

3. GKD-C Confirmation 1 agrees

4. GKD-C Confirmation 2 agrees

5. GKD-V Volatility/Volume Agrees

1-Candle Rule Volatility/Volume Entry

1. GKD-V Volatility/Volume signal

2. GKD-C Confirmation 1 agrees

3. Price is within a range of 0.2x Volatility and 1.0x Volatility of the Goldie Locks Mean

4. GKD-C Confirmation 1 signal was less than 7 candles prior

Next Candle:

1. Price retraced (Long: close < close or Short: close > close)

2. GKD-B Volatility/Volume agrees

3. GKD-C Confirmation 1 agrees

4. GKD-C Confirmation 2 agrees

5. GKD-B Baseline agrees

PullBack Entry

1. GKD-B Baseline signal

2. GKD-C Confirmation 1 agrees

3. Price is beyond 1.0x Volatility of Baseline

Next Candle:

1. Price is within a range of 0.2x Volatility and 1.0x Volatility of the Goldie Locks Mean

2. GKD-C Confirmation 1 agrees

3. GKD-C Confirmation 2 agrees

4. GKD-V Volatility/Volume Agrees

]█ Setting up the GKD

The GKD system involves chaining indicators together. These are the steps to set this up.

Use a GKD-C indicator alone on a chart

1. Inside the GKD-C indicator, change the "Confirmation Type" setting to "Solo Confirmation Simple"

Use a GKD-V indicator alone on a chart

**nothing, it's already useable on the chart without any settings changes

Use a GKD-B indicator alone on a chart

**nothing, it's already useable on the chart without any settings changes

Baseline (Baseline, Backtest)

1. Import the GKD-B Baseline into the GKD-BT Backtest: "Input into Volatility/Volume or Backtest (Baseline testing)"

2. Inside the GKD-BT Backtest, change the setting "Backtest Special" to "Baseline"

Volatility/Volume (Volatility/Volume, Backte st)

1. Inside the GKD-V indicator, change the "Testing Type" setting to "Solo"

2. Inside the GKD-V indicator, change the "Signal Type" setting to "Crossing" (neither traditional nor both can be backtested)

3. Import the GKD-V indicator into the GKD-BT Backtest: "Input into C1 or Backtest"

4. Inside the GKD-BT Backtest, change the setting "Backtest Special" to "Volatility/Volume"

5. Inside the GKD-BT Backtest, a) change the setting "Backtest Type" to "Trading" if using a directional GKD-V indicator; or, b) change the setting "Backtest Type" to "Full" if using a directional or non-directional GKD-V indicator (non-directional GKD-V can only test Longs and Shorts separately)

6. If "Backtest Type" is set to "Full": Inside the GKD-BT Backtest, change the setting "Backtest Side" to "Long" or "Short

7. If "Backtest Type" is set to "Full": To allow the system to open multiple orders at one time so you test all Longs or Shorts, open the GKD-BT Backtest, click the tab "Properties" and then insert a value of something like 10 orders into the "Pyramiding" settings. This will allow 10 orders to be opened at one time which should be enough to catch all possible Longs or Shorts.

Solo Confirmation Simple (Confirmation, Backtest)

1. Inside the GKD-C indicator, change the "Confirmation Type" setting to "Solo Confirmation Simple"

1. Import the GKD-C indicator into the GKD-BT Backtest: "Input into Backtest"

2. Inside the GKD-BT Backtest, change the setting "Backtest Special" to "Solo Confirmation Simple"

Solo Confirmation Complex without Exits (Baseline, Volatility/Volume, Confirmation, Backtest)

1. Inside the GKD-V indicator, change the "Testing Type" setting to "Chained"

2. Import the GKD-B Baseline into the GKD-V indicator: "Input into Volatility/Volume or Backtest (Baseline testing)"

3. Inside the GKD-C indicator, change the "Confirmation Type" setting to "Solo Confirmation Complex"

4. Import the GKD-V indicator into the GKD-C indicator: "Input into C1 or Backtest"

5. Inside the GKD-BT Backtest, change the setting "Backtest Special" to "GKD Full wo/ Exits"

6. Import the GKD-C into the GKD-BT Backtest: "Input into Exit or Backtest"

Solo Confirmation Complex with Exits (Baseline, Volatility/Volume, Confirmation, Exit, Backtest)

1. Inside the GKD-V indicator, change the "Testing Type" setting to "Chained"

2. Import the GKD-B Baseline into the GKD-V indicator: "Input into Volatility/Volume or Backtest (Baseline testing)"

3. Inside the GKD-C indicator, change the "Confirmation Type" setting to "Solo Confirmation Complex"

4. Import the GKD-V indicator into the GKD-C indicator: "Input into C1 or Backtest"

5. Import the GKD-C indicator into the GKD-E indicator: "Input into Exit"

6. Inside the GKD-BT Backtest, change the setting "Backtest Special" to "GKD Full w/ Exits"

7. Import the GKD-E into the GKD-BT Backtest: "Input into Backtest"

Full GKD without Exits (Baseline, Volatility/Volume, Confirmation 1, Confirmation 2, Continuation, Backtest)

1. Inside the GKD-V indicator, change the "Testing Type" setting to "Chained"

2. Import the GKD-B Baseline into the GKD-V indicator: "Input into Volatility/Volume or Backtest (Baseline testing)"

3. Inside the GKD-C 1 indicator, change the "Confirmation Type" setting to "Confirmation 1"

4. Import the GKD-V indicator into the GKD-C 1 indicator: "Input into C1 or Backtest"

5. Inside the GKD-C 2 indicator, change the "Confirmation Type" setting to "Confirmation 2"

6. Import the GKD-C 1 indicator into the GKD-C 2 indicator: "Input into C2"

7. Inside the GKD-C Continuation indicator, change the "Confirmation Type" setting to "Continuation"

8. Inside the GKD-BT Backtest, change the setting "Backtest Special" to "GKD Full wo/ Exits"

9. Import the GKD-E into the GKD-BT Backtest: "Input into Exit or Backtest"

Full GKD with Exits (Baseline, Volatility/Volume, Confirmation 1, Confirmation 2, Continuation, Exit, Backtest)

1. Inside the GKD-V indicator, change the "Testing Type" setting to "Chained"

2. Import the GKD-B Baseline into the GKD-V indicator: "Input into Volatility/Volume or Backtest (Baseline testing)"

3. Inside the GKD-C 1 indicator, change the "Confirmation Type" setting to "Confirmation 1"

4. Import the GKD-V indicator into the GKD-C 1 indicator: "Input into C1 or Backtest"

5. Inside the GKD-C 2 indicator, change the "Confirmation Type" setting to "Confirmation 2"

6. Import the GKD-C 1 indicator into the GKD-C 2 indicator: "Input into C2"

7. Inside the GKD-C Continuation indicator, change the "Confirmation Type" setting to "Continuation"

8. Import the GKD-C Continuation indicator into the GKD-E indicator: "Input into Exit"

9. Inside the GKD-BT Backtest, change the setting "Backtest Special" to "GKD Full w/ Exits"

10. Import the GKD-E into the GKD-BT Backtest: "Input into Backtest"

Baseline + Volatility/Volume (Baseline, Volatility/Volume, Backtest)

1. Inside the GKD-V indicator, change the "Testing Type" setting to "Baseline + Volatility/Volume"

2. Inside the GKD-V indicator, make sure the "Signal Type" setting is set to "Traditional"

3. Import the GKD-B Baseline into the GKD-V indicator: "Input into Volatility/Volume or Backtest (Baseline testing)"

4. Inside the GKD-BT Backtest, change the setting "Backtest Special" to "Baseline + Volatility/Volume"

5. Import the GKD-V into the GKD-BT Backtest: "Input into C1 or Backtest"

6. Inside the GKD-BT Backtest, change the setting "Backtest Type" to "Full". For this backtest, you must test Longs and Shorts separately

7. To allow the system to open multiple orders at one time so you can test all Longs or Shorts, open the GKD-BT Backtest, click the tab "Properties" and then insert a value of something like 10 orders into the "Pyramiding" settings. This will allow 10 orders to be opened at one time which should be enough to catch all possible Longs or Shorts.

Requirements

Inputs

Confirmation 1: GKD-V Volatility / Volume indicator

Confirmation 2: GKD-C Confirmation indicator

Continuation: GKD-C Confirmation indicator

Solo Confirmation Simple: GKD-B Baseline

Solo Confirmation Complex: GKD-V Volatility / Volume indicator

Solo Confirmation Super Complex: GKD-V Volatility / Volume indicator

Stacked 1: None

Stacked 2+: GKD-C, GKD-V, or GKD-B Stacked 1

Outputs

Confirmation 1: GKD-C Confirmation 2 indicator

Confirmation 2: GKD-C Continuation indicator

Continuation: GKD-E Exit indicator

Solo Confirmation Simple: GKD-BT Backtest

Solo Confirmation Complex: GKD-BT Backtest or GKD-E Exit indicator

Solo Confirmation Super Complex: GKD-C Continuation indicator

Stacked 1: GKD-C, GKD-V, or GKD-B Stacked 2+

Stacked 2+: GKD-C, GKD-V, or GKD-B Stacked 2+ or GKD-BT Backtest

Additional features will be added in future releases.

חפש סקריפטים עבור "algo"

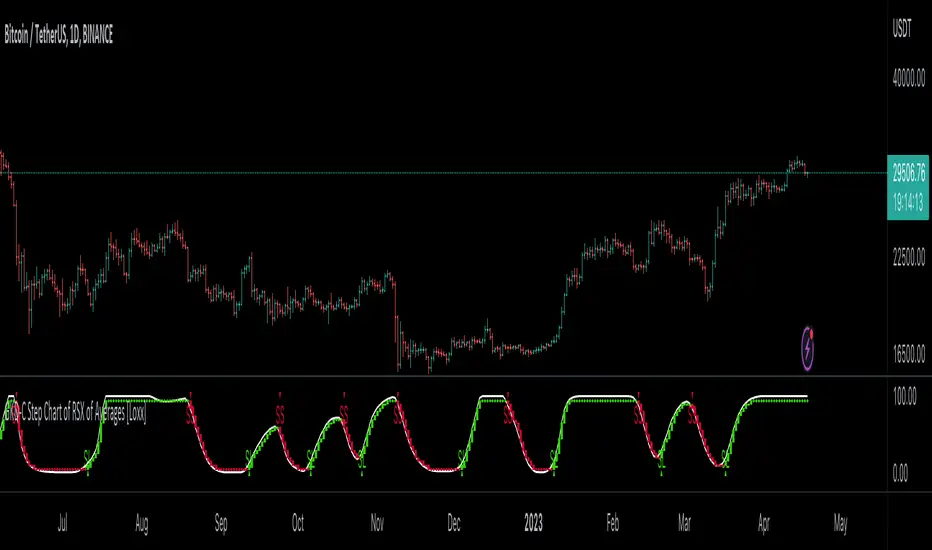

GKD-C Step Chart of RSX of Averages [Loxx]Giga Kaleidoscope GKD-C Step Chart of RSX of Averages is a Confirmation module included in Loxx's "Giga Kaleidoscope Modularized Trading System".

█ GKD-C Step Chart of RSX of Averages

What is the RSX?

The Jurik RSX is a technical indicator developed by Mark Jurik to measure the momentum and strength of price movements in financial markets, such as stocks, commodities, and currencies. It is an advanced version of the traditional Relative Strength Index (RSI), designed to offer smoother and less lagging signals compared to the standard RSI.

The main advantage of the Jurik RSX is that it provides more accurate and timely signals for traders and analysts, thanks to its improved calculation methods that reduce noise and lag in the indicator's output. This enables better decision-making when analyzing market trends and potential trading opportunities.

A Comprehensive Analysis of the stepChart() Algorithm for Financial Technical Analysis

Technical analysis is a widely adopted method for forecasting financial market trends by evaluating historical price data and utilizing various statistical tools. We examine an algorithm that implements the stepChart() function, a custom indicator designed to assist traders in identifying trends and making more informed decisions. We will provide an in-depth analysis of the code, exploring its structure, purpose, and functionality.

The code can be divided into two main sections: the stepChart() function definition and its application to charting data. We will first examine the stepChart() function definition, followed by its application.

stepChart() Function Definition

The stepChart() function takes two arguments: a floating-point number 'srcprice' representing the source price and a simple integer 'stepSize' to determine the increment for evaluating trends.

Within the function, five floating-point variables are initialized: steps, trend, rtrend, rbar_high, and rbar_low. These variables will be used to compute the step chart values and store the trends and bar high/low values.

The 'bar_index' variable is employed to identify the current bar in the price chart. If the current bar is the first one (bar_index == 0), the function initializes the steps, rbar_high, rbar_low, trend, and rtrend variables using the source price and step size. If stepSize is greater than 0, the variables are initialized using the rounded value of srcprice divided by stepSize, multiplied by stepSize. Otherwise, they are initialized to srcprice.

In the following part of the function, the code checks if the absolute difference between the source price and the previous steps value is less than the step size. If true, the current steps value remains unchanged. If not, the code enters a while loop that continues incrementing or decrementing the steps value by the step size until the absolute difference between the source price and the steps value is less than or equal to the step size.

Next, the trend variable is calculated based on the relationship between the current steps value and the previous steps value. The rbar_high, rbar_low, and rtrend variables are updated accordingly.

Finally, the function returns a list containing rbar_high, rbar_low, and rtrend values.

Application of the stepChart() Function

In this section, the stepChart() function is applied to the RSX of the smoothed moving average of the closing prices of a financial instrument. The moving average and RSX functions are used to calculate the moving average and RSX, respectively.

The stepChart() function is called with the RSX values and the user-defined step size. The resulting values are stored in the rbar_high, rbar_low, and rtrend variables.

Next, the bar_high, bar_low, bar_close, and bar_open variables are set based on the values of rbar_high, rbar_low, and rtrend. These variables will be used to plot the stepChart() on the price chart. The bar_high variable is set to rbar_high, and the bar_low variable is set to rbar_high if rbar_high is equal to rbar_low, or to rbar_low otherwise. The bar_close variable is set to bar_high if rtrend equals 1, and to bar_low otherwise. Lastly, the bar_open variable is set to bar_low if rtrend equals 1, and to bar_high otherwise.

Finally, we use the built in Pine function plotcandle to plot the candles on the chart.

The stepChart() function is an innovative technical analysis tool designed to help traders identify trends in financial markets. By combining the RSX and moving average indicators and utilizing the step chart approach, this custom indicator provides a visually appealing and intuitive representation of price trends. Understanding the intricacies of this code can prove invaluable for traders looking to make well-informed decisions

Core components of an NNFX algorithmic trading strategy

The NNFX algorithm is built on the principles of trend, momentum, and volatility. There are six core components in the NNFX trading algorithm:

1. Volatility - price volatility; e.g., Average True Range, True Range Double, Close-to-Close, etc.

2. Baseline - a moving average to identify price trend

3. Confirmation 1 - a technical indicator used to identify trends

4. Confirmation 2 - a technical indicator used to identify trends

5. Continuation - a technical indicator used to identify trends

6. Volatility/Volume - a technical indicator used to identify volatility/volume breakouts/breakdown

7. Exit - a technical indicator used to determine when a trend is exhausted

What is Volatility in the NNFX trading system?

In the NNFX (No Nonsense Forex) trading system, ATR (Average True Range) is typically used to measure the volatility of an asset. It is used as a part of the system to help determine the appropriate stop loss and take profit levels for a trade. ATR is calculated by taking the average of the true range values over a specified period.

True range is calculated as the maximum of the following values:

-Current high minus the current low

-Absolute value of the current high minus the previous close

-Absolute value of the current low minus the previous close

ATR is a dynamic indicator that changes with changes in volatility. As volatility increases, the value of ATR increases, and as volatility decreases, the value of ATR decreases. By using ATR in NNFX system, traders can adjust their stop loss and take profit levels according to the volatility of the asset being traded. This helps to ensure that the trade is given enough room to move, while also minimizing potential losses.

Other types of volatility include True Range Double (TRD), Close-to-Close, and Garman-Klass

What is a Baseline indicator?

The baseline is essentially a moving average, and is used to determine the overall direction of the market.

The baseline in the NNFX system is used to filter out trades that are not in line with the long-term trend of the market. The baseline is plotted on the chart along with other indicators, such as the Moving Average (MA), the Relative Strength Index (RSI), and the Average True Range (ATR).

Trades are only taken when the price is in the same direction as the baseline. For example, if the baseline is sloping upwards, only long trades are taken, and if the baseline is sloping downwards, only short trades are taken. This approach helps to ensure that trades are in line with the overall trend of the market, and reduces the risk of entering trades that are likely to fail.

By using a baseline in the NNFX system, traders can have a clear reference point for determining the overall trend of the market, and can make more informed trading decisions. The baseline helps to filter out noise and false signals, and ensures that trades are taken in the direction of the long-term trend.

What is a Confirmation indicator?

Confirmation indicators are technical indicators that are used to confirm the signals generated by primary indicators. Primary indicators are the core indicators used in the NNFX system, such as the Average True Range (ATR), the Moving Average (MA), and the Relative Strength Index (RSI).

The purpose of the confirmation indicators is to reduce false signals and improve the accuracy of the trading system. They are designed to confirm the signals generated by the primary indicators by providing additional information about the strength and direction of the trend.

Some examples of confirmation indicators that may be used in the NNFX system include the Bollinger Bands, the MACD (Moving Average Convergence Divergence), and the MACD Oscillator. These indicators can provide information about the volatility, momentum, and trend strength of the market, and can be used to confirm the signals generated by the primary indicators.

In the NNFX system, confirmation indicators are used in combination with primary indicators and other filters to create a trading system that is robust and reliable. By using multiple indicators to confirm trading signals, the system aims to reduce the risk of false signals and improve the overall profitability of the trades.

What is a Continuation indicator?

In the NNFX (No Nonsense Forex) trading system, a continuation indicator is a technical indicator that is used to confirm a current trend and predict that the trend is likely to continue in the same direction. A continuation indicator is typically used in conjunction with other indicators in the system, such as a baseline indicator, to provide a comprehensive trading strategy.

What is a Volatility/Volume indicator?

Volume indicators, such as the On Balance Volume (OBV), the Chaikin Money Flow (CMF), or the Volume Price Trend (VPT), are used to measure the amount of buying and selling activity in a market. They are based on the trading volume of the market, and can provide information about the strength of the trend. In the NNFX system, volume indicators are used to confirm trading signals generated by the Moving Average and the Relative Strength Index. Volatility indicators include Average Direction Index, Waddah Attar, and Volatility Ratio. In the NNFX trading system, volatility is a proxy for volume and vice versa.

By using volume indicators as confirmation tools, the NNFX trading system aims to reduce the risk of false signals and improve the overall profitability of trades. These indicators can provide additional information about the market that is not captured by the primary indicators, and can help traders to make more informed trading decisions. In addition, volume indicators can be used to identify potential changes in market trends and to confirm the strength of price movements.

What is an Exit indicator?

The exit indicator is used in conjunction with other indicators in the system, such as the Moving Average (MA), the Relative Strength Index (RSI), and the Average True Range (ATR), to provide a comprehensive trading strategy.

The exit indicator in the NNFX system can be any technical indicator that is deemed effective at identifying optimal exit points. Examples of exit indicators that are commonly used include the Parabolic SAR, the Average Directional Index (ADX), and the Chandelier Exit.

The purpose of the exit indicator is to identify when a trend is likely to reverse or when the market conditions have changed, signaling the need to exit a trade. By using an exit indicator, traders can manage their risk and prevent significant losses.

In the NNFX system, the exit indicator is used in conjunction with a stop loss and a take profit order to maximize profits and minimize losses. The stop loss order is used to limit the amount of loss that can be incurred if the trade goes against the trader, while the take profit order is used to lock in profits when the trade is moving in the trader's favor.

Overall, the use of an exit indicator in the NNFX trading system is an important component of a comprehensive trading strategy. It allows traders to manage their risk effectively and improve the profitability of their trades by exiting at the right time.

How does Loxx's GKD (Giga Kaleidoscope Modularized Trading System) implement the NNFX algorithm outlined above?

Loxx's GKD v1.0 system has five types of modules (indicators/strategies). These modules are:

1. GKD-BT - Backtesting module (Volatility, Number 1 in the NNFX algorithm)

2. GKD-B - Baseline module (Baseline and Volatility/Volume, Numbers 1 and 2 in the NNFX algorithm)

3. GKD-C - Confirmation 1/2 and Continuation module (Confirmation 1/2 and Continuation, Numbers 3, 4, and 5 in the NNFX algorithm)

4. GKD-V - Volatility/Volume module (Confirmation 1/2, Number 6 in the NNFX algorithm)

5. GKD-E - Exit module (Exit, Number 7 in the NNFX algorithm)

(additional module types will added in future releases)

Each module interacts with every module by passing data between modules. Data is passed between each module as described below:

GKD-B => GKD-V => GKD-C(1) => GKD-C(2) => GKD-C(Continuation) => GKD-E => GKD-BT

That is, the Baseline indicator passes its data to Volatility/Volume. The Volatility/Volume indicator passes its values to the Confirmation 1 indicator. The Confirmation 1 indicator passes its values to the Confirmation 2 indicator. The Confirmation 2 indicator passes its values to the Continuation indicator. The Continuation indicator passes its values to the Exit indicator, and finally, the Exit indicator passes its values to the Backtest strategy.

This chaining of indicators requires that each module conform to Loxx's GKD protocol, therefore allowing for the testing of every possible combination of technical indicators that make up the six components of the NNFX algorithm.

What does the application of the GKD trading system look like?

Example trading system:

Backtest: Strategy with 1-3 take profits, trailing stop loss, multiple types of PnL volatility, and 2 backtesting styles

Baseline: Hull Moving Average

Volatility/Volume: Hurst Exponent

Confirmation 1: Step Chart of RSX of Averages as shown on the chart above

Confirmation 2: Williams Percent Range

Continuation: Fisher Transform

Exit: Rex Oscillator

Each GKD indicator is denoted with a module identifier of either: GKD-BT, GKD-B, GKD-C, GKD-V, or GKD-E. This allows traders to understand to which module each indicator belongs and where each indicator fits into the GKD protocol chain.

Giga Kaleidoscope Modularized Trading System Signals (based on the NNFX algorithm)

Standard Entry

1. GKD-C Confirmation 1 Signal

2. GKD-B Baseline agrees

3. Price is within a range of 0.2x Volatility and 1.0x Volatility of the Goldie Locks Mean

4. GKD-C Confirmation 2 agrees

5. GKD-V Volatility/Volume agrees

Baseline Entry

1. GKD-B Baseline signal

2. GKD-C Confirmation 1 agrees

3. Price is within a range of 0.2x Volatility and 1.0x Volatility of the Goldie Locks Mean

4. GKD-C Confirmation 2 agrees

5. GKD-V Volatility/Volume agrees

6. GKD-C Confirmation 1 signal was less than 7 candles prior

Volatility/Volume Entry

1. GKD-V Volatility/Volume signal

2. GKD-C Confirmation 1 agrees

3. Price is within a range of 0.2x Volatility and 1.0x Volatility of the Goldie Locks Mean

4. GKD-C Confirmation 2 agrees

5. GKD-B Baseline agrees

6. GKD-C Confirmation 1 signal was less than 7 candles prior

Continuation Entry

1. Standard Entry, Baseline Entry, or Pullback; entry triggered previously

2. GKD-B Baseline hasn't crossed since entry signal trigger

3. GKD-C Confirmation Continuation Indicator signals

4. GKD-C Confirmation 1 agrees

5. GKD-B Baseline agrees

6. GKD-C Confirmation 2 agrees

1-Candle Rule Standard Entry

1. GKD-C Confirmation 1 signal

2. GKD-B Baseline agrees

3. Price is within a range of 0.2x Volatility and 1.0x Volatility of the Goldie Locks Mean

Next Candle:

1. Price retraced (Long: close < close or Short: close > close )

2. GKD-B Baseline agrees

3. GKD-C Confirmation 1 agrees

4. GKD-C Confirmation 2 agrees

5. GKD-V Volatility/Volume agrees

1-Candle Rule Baseline Entry

1. GKD-B Baseline signal

2. GKD-C Confirmation 1 agrees

3. Price is within a range of 0.2x Volatility and 1.0x Volatility of the Goldie Locks Mean

4. GKD-C Confirmation 1 signal was less than 7 candles prior

Next Candle:

1. Price retraced (Long: close < close or Short: close > close )

2. GKD-B Baseline agrees

3. GKD-C Confirmation 1 agrees

4. GKD-C Confirmation 2 agrees

5. GKD-V Volatility/Volume Agrees

1-Candle Rule Volatility/Volume Entry

1. GKD-V Volatility/Volume signal

2. GKD-C Confirmation 1 agrees

3. Price is within a range of 0.2x Volatility and 1.0x Volatility of the Goldie Locks Mean

4. GKD-C Confirmation 1 signal was less than 7 candles prior

Next Candle:

1. Price retraced (Long: close < close or Short: close > close)

2. GKD-B Volatility/Volume agrees

3. GKD-C Confirmation 1 agrees

4. GKD-C Confirmation 2 agrees

5. GKD-B Baseline agrees

PullBack Entry

1. GKD-B Baseline signal

2. GKD-C Confirmation 1 agrees

3. Price is beyond 1.0x Volatility of Baseline

Next Candle:

1. Price is within a range of 0.2x Volatility and 1.0x Volatility of the Goldie Locks Mean

2. GKD-C Confirmation 1 agrees

3. GKD-C Confirmation 2 agrees

4. GKD-V Volatility/Volume Agrees

]█ Setting up the GKD

The GKD system involves chaining indicators together. These are the steps to set this up.

Use a GKD-C indicator alone on a chart

1. Inside the GKD-C indicator, change the "Confirmation Type" setting to "Solo Confirmation Simple"

Use a GKD-V indicator alone on a chart

**nothing, it's already useable on the chart without any settings changes

Use a GKD-B indicator alone on a chart

**nothing, it's already useable on the chart without any settings changes

Baseline (Baseline, Backtest)

1. Import the GKD-B Baseline into the GKD-BT Backtest: "Input into Volatility/Volume or Backtest (Baseline testing)"

2. Inside the GKD-BT Backtest, change the setting "Backtest Special" to "Baseline"

Volatility/Volume (Volatility/Volume, Backte st)

1. Inside the GKD-V indicator, change the "Testing Type" setting to "Solo"

2. Inside the GKD-V indicator, change the "Signal Type" setting to "Crossing" (neither traditional nor both can be backtested)

3. Import the GKD-V indicator into the GKD-BT Backtest: "Input into C1 or Backtest"

4. Inside the GKD-BT Backtest, change the setting "Backtest Special" to "Volatility/Volume"

5. Inside the GKD-BT Backtest, a) change the setting "Backtest Type" to "Trading" if using a directional GKD-V indicator; or, b) change the setting "Backtest Type" to "Full" if using a directional or non-directional GKD-V indicator (non-directional GKD-V can only test Longs and Shorts separately)

6. If "Backtest Type" is set to "Full": Inside the GKD-BT Backtest, change the setting "Backtest Side" to "Long" or "Short

7. If "Backtest Type" is set to "Full": To allow the system to open multiple orders at one time so you test all Longs or Shorts, open the GKD-BT Backtest, click the tab "Properties" and then insert a value of something like 10 orders into the "Pyramiding" settings. This will allow 10 orders to be opened at one time which should be enough to catch all possible Longs or Shorts.

Solo Confirmation Simple (Confirmation, Backtest)

1. Inside the GKD-C indicator, change the "Confirmation Type" setting to "Solo Confirmation Simple"

1. Import the GKD-C indicator into the GKD-BT Backtest: "Input into Backtest"

2. Inside the GKD-BT Backtest, change the setting "Backtest Special" to "Solo Confirmation Simple"

Solo Confirmation Complex without Exits (Baseline, Volatility/Volume, Confirmation, Backtest)

1. Inside the GKD-V indicator, change the "Testing Type" setting to "Chained"

2. Import the GKD-B Baseline into the GKD-V indicator: "Input into Volatility/Volume or Backtest (Baseline testing)"

3. Inside the GKD-C indicator, change the "Confirmation Type" setting to "Solo Confirmation Complex"

4. Import the GKD-V indicator into the GKD-C indicator: "Input into C1 or Backtest"

5. Inside the GKD-BT Backtest, change the setting "Backtest Special" to "GKD Full wo/ Exits"

6. Import the GKD-C into the GKD-BT Backtest: "Input into Exit or Backtest"

Solo Confirmation Complex with Exits (Baseline, Volatility/Volume, Confirmation, Exit, Backtest)

1. Inside the GKD-V indicator, change the "Testing Type" setting to "Chained"

2. Import the GKD-B Baseline into the GKD-V indicator: "Input into Volatility/Volume or Backtest (Baseline testing)"

3. Inside the GKD-C indicator, change the "Confirmation Type" setting to "Solo Confirmation Complex"

4. Import the GKD-V indicator into the GKD-C indicator: "Input into C1 or Backtest"

5. Import the GKD-C indicator into the GKD-E indicator: "Input into Exit"

6. Inside the GKD-BT Backtest, change the setting "Backtest Special" to "GKD Full w/ Exits"

7. Import the GKD-E into the GKD-BT Backtest: "Input into Backtest"

Full GKD without Exits (Baseline, Volatility/Volume, Confirmation 1, Confirmation 2, Continuation, Backtest)

1. Inside the GKD-V indicator, change the "Testing Type" setting to "Chained"

2. Import the GKD-B Baseline into the GKD-V indicator: "Input into Volatility/Volume or Backtest (Baseline testing)"

3. Inside the GKD-C 1 indicator, change the "Confirmation Type" setting to "Confirmation 1"

4. Import the GKD-V indicator into the GKD-C 1 indicator: "Input into C1 or Backtest"

5. Inside the GKD-C 2 indicator, change the "Confirmation Type" setting to "Confirmation 2"

6. Import the GKD-C 1 indicator into the GKD-C 2 indicator: "Input into C2"

7. Inside the GKD-C Continuation indicator, change the "Confirmation Type" setting to "Continuation"

8. Inside the GKD-BT Backtest, change the setting "Backtest Special" to "GKD Full wo/ Exits"

9. Import the GKD-E into the GKD-BT Backtest: "Input into Exit or Backtest"

Full GKD with Exits (Baseline, Volatility/Volume, Confirmation 1, Confirmation 2, Continuation, Exit, Backtest)

1. Inside the GKD-V indicator, change the "Testing Type" setting to "Chained"

2. Import the GKD-B Baseline into the GKD-V indicator: "Input into Volatility/Volume or Backtest (Baseline testing)"

3. Inside the GKD-C 1 indicator, change the "Confirmation Type" setting to "Confirmation 1"

4. Import the GKD-V indicator into the GKD-C 1 indicator: "Input into C1 or Backtest"

5. Inside the GKD-C 2 indicator, change the "Confirmation Type" setting to "Confirmation 2"

6. Import the GKD-C 1 indicator into the GKD-C 2 indicator: "Input into C2"

7. Inside the GKD-C Continuation indicator, change the "Confirmation Type" setting to "Continuation"

8. Import the GKD-C Continuation indicator into the GKD-E indicator: "Input into Exit"

9. Inside the GKD-BT Backtest, change the setting "Backtest Special" to "GKD Full w/ Exits"

10. Import the GKD-E into the GKD-BT Backtest: "Input into Backtest"

Baseline + Volatility/Volume (Baseline, Volatility/Volume, Backtest)

1. Inside the GKD-V indicator, change the "Testing Type" setting to "Baseline + Volatility/Volume"

2. Inside the GKD-V indicator, make sure the "Signal Type" setting is set to "Traditional"

3. Import the GKD-B Baseline into the GKD-V indicator: "Input into Volatility/Volume or Backtest (Baseline testing)"

4. Inside the GKD-BT Backtest, change the setting "Backtest Special" to "Baseline + Volatility/Volume"

5. Import the GKD-V into the GKD-BT Backtest: "Input into C1 or Backtest"

6. Inside the GKD-BT Backtest, change the setting "Backtest Type" to "Full". For this backtest, you must test Longs and Shorts separately

7. To allow the system to open multiple orders at one time so you can test all Longs or Shorts, open the GKD-BT Backtest, click the tab "Properties" and then insert a value of something like 10 orders into the "Pyramiding" settings. This will allow 10 orders to be opened at one time which should be enough to catch all possible Longs or Shorts.

Requirements

Inputs

Confirmation 1: GKD-V Volatility / Volume indicator

Confirmation 2: GKD-C Confirmation indicator

Continuation: GKD-C Confirmation indicator

Solo Confirmation Simple: GKD-B Baseline

Solo Confirmation Complex: GKD-V Volatility / Volume indicator

Solo Confirmation Super Complex: GKD-V Volatility / Volume indicator

Stacked 1: None

Stacked 2+: GKD-C, GKD-V, or GKD-B Stacked 1

Outputs

Confirmation 1: GKD-C Confirmation 2 indicator

Confirmation 2: GKD-C Continuation indicator

Continuation: GKD-E Exit indicator

Solo Confirmation Simple: GKD-BT Backtest

Solo Confirmation Complex: GKD-BT Backtest or GKD-E Exit indicator

Solo Confirmation Super Complex: GKD-C Continuation indicator

Stacked 1: GKD-C, GKD-V, or GKD-B Stacked 2+

Stacked 2+: GKD-C, GKD-V, or GKD-B Stacked 2+ or GKD-BT Backtest

Additional features will be added in future releases.

loxxfftLibrary "loxxfft"

This code is a library for performing Fast Fourier Transform (FFT) operations. FFT is an algorithm that can quickly compute the discrete Fourier transform (DFT) of a sequence. The library includes functions for performing FFTs on both real and complex data. It also includes functions for fast correlation and convolution, which are operations that can be performed efficiently using FFTs. Additionally, the library includes functions for fast sine and cosine transforms.

Reference:

www.alglib.net

fastfouriertransform(a, nn, inversefft)

Returns Fast Fourier Transform

Parameters:

a (float ) : float , An array of real and imaginary parts of the function values. The real part is stored at even indices, and the imaginary part is stored at odd indices.

nn (int) : int, The number of function values. It must be a power of two, but the algorithm does not validate this.

inversefft (bool) : bool, A boolean value that indicates the direction of the transformation. If True, it performs the inverse FFT; if False, it performs the direct FFT.

Returns: float , Modifies the input array a in-place, which means that the transformed data (the FFT result for direct transformation or the inverse FFT result for inverse transformation) will be stored in the same array a after the function execution. The transformed data will have real and imaginary parts interleaved, with the real parts at even indices and the imaginary parts at odd indices.

realfastfouriertransform(a, tnn, inversefft)

Returns Real Fast Fourier Transform

Parameters:

a (float ) : float , A float array containing the real-valued function samples.

tnn (int) : int, The number of function values (must be a power of 2, but the algorithm does not validate this condition).

inversefft (bool) : bool, A boolean flag that indicates the direction of the transformation (True for inverse, False for direct).

Returns: float , Modifies the input array a in-place, meaning that the transformed data (the FFT result for direct transformation or the inverse FFT result for inverse transformation) will be stored in the same array a after the function execution.

fastsinetransform(a, tnn, inversefst)

Returns Fast Discrete Sine Conversion

Parameters:

a (float ) : float , An array of real numbers representing the function values.

tnn (int) : int, Number of function values (must be a power of two, but the code doesn't validate this).

inversefst (bool) : bool, A boolean flag indicating the direction of the transformation. If True, it performs the inverse FST, and if False, it performs the direct FST.

Returns: float , The output is the transformed array 'a', which will contain the result of the transformation.

fastcosinetransform(a, tnn, inversefct)

Returns Fast Discrete Cosine Transform

Parameters:

a (float ) : float , This is a floating-point array representing the sequence of values (time-domain) that you want to transform. The function will perform the Fast Cosine Transform (FCT) or the inverse FCT on this input array, depending on the value of the inversefct parameter. The transformed result will also be stored in this same array, which means the function modifies the input array in-place.

tnn (int) : int, This is an integer value representing the number of data points in the input array a. It is used to determine the size of the input array and control the loops in the algorithm. Note that the size of the input array should be a power of 2 for the Fast Cosine Transform algorithm to work correctly.

inversefct (bool) : bool, This is a boolean value that controls whether the function performs the regular Fast Cosine Transform or the inverse FCT. If inversefct is set to true, the function will perform the inverse FCT, and if set to false, the regular FCT will be performed. The inverse FCT can be used to transform data back into its original form (time-domain) after the regular FCT has been applied.

Returns: float , The resulting transformed array is stored in the input array a. This means that the function modifies the input array in-place and does not return a new array.

fastconvolution(signal, signallen, response, negativelen, positivelen)

Convolution using FFT

Parameters:

signal (float ) : float , This is an array of real numbers representing the input signal that will be convolved with the response function. The elements are numbered from 0 to SignalLen-1.

signallen (int) : int, This is an integer representing the length of the input signal array. It specifies the number of elements in the signal array.

response (float ) : float , This is an array of real numbers representing the response function used for convolution. The response function consists of two parts: one corresponding to positive argument values and the other to negative argument values. Array elements with numbers from 0 to NegativeLen match the response values at points from -NegativeLen to 0, respectively. Array elements with numbers from NegativeLen+1 to NegativeLen+PositiveLen correspond to the response values in points from 1 to PositiveLen, respectively.

negativelen (int) : int, This is an integer representing the "negative length" of the response function. It indicates the number of elements in the response function array that correspond to negative argument values. Outside the range , the response function is considered zero.

positivelen (int) : int, This is an integer representing the "positive length" of the response function. It indicates the number of elements in the response function array that correspond to positive argument values. Similar to negativelen, outside the range , the response function is considered zero.

Returns: float , The resulting convolved values are stored back in the input signal array.

fastcorrelation(signal, signallen, pattern, patternlen)

Returns Correlation using FFT

Parameters:

signal (float ) : float ,This is an array of real numbers representing the signal to be correlated with the pattern. The elements are numbered from 0 to SignalLen-1.

signallen (int) : int, This is an integer representing the length of the input signal array.

pattern (float ) : float , This is an array of real numbers representing the pattern to be correlated with the signal. The elements are numbered from 0 to PatternLen-1.

patternlen (int) : int, This is an integer representing the length of the pattern array.

Returns: float , The signal array containing the correlation values at points from 0 to SignalLen-1.

tworealffts(a1, a2, a, b, tn)

Returns Fast Fourier Transform of Two Real Functions

Parameters:

a1 (float ) : float , An array of real numbers, representing the values of the first function.

a2 (float ) : float , An array of real numbers, representing the values of the second function.

a (float ) : float , An output array to store the Fourier transform of the first function.

b (float ) : float , An output array to store the Fourier transform of the second function.

tn (int) : float , An integer representing the number of function values. It must be a power of two, but the algorithm doesn't validate this condition.

Returns: float , The a and b arrays will contain the Fourier transform of the first and second functions, respectively. Note that the function overwrites the input arrays a and b.

█ Detailed explaination of each function

Fast Fourier Transform

The fastfouriertransform() function takes three input parameters:

1. a: An array of real and imaginary parts of the function values. The real part is stored at even indices, and the imaginary part is stored at odd indices.

2. nn: The number of function values. It must be a power of two, but the algorithm does not validate this.

3. inversefft: A boolean value that indicates the direction of the transformation. If True, it performs the inverse FFT; if False, it performs the direct FFT.

The function performs the FFT using the Cooley-Tukey algorithm, which is an efficient algorithm for computing the discrete Fourier transform (DFT) and its inverse. The Cooley-Tukey algorithm recursively breaks down the DFT of a sequence into smaller DFTs of subsequences, leading to a significant reduction in computational complexity. The algorithm's time complexity is O(n log n), where n is the number of samples.

The fastfouriertransform() function first initializes variables and determines the direction of the transformation based on the inversefft parameter. If inversefft is True, the isign variable is set to -1; otherwise, it is set to 1.

Next, the function performs the bit-reversal operation. This is a necessary step before calculating the FFT, as it rearranges the input data in a specific order required by the Cooley-Tukey algorithm. The bit-reversal is performed using a loop that iterates through the nn samples, swapping the data elements according to their bit-reversed index.

After the bit-reversal operation, the function iteratively computes the FFT using the Cooley-Tukey algorithm. It performs calculations in a loop that goes through different stages, doubling the size of the sub-FFT at each stage. Within each stage, the Cooley-Tukey algorithm calculates the butterfly operations, which are mathematical operations that combine the results of smaller DFTs into the final DFT. The butterfly operations involve complex number multiplication and addition, updating the input array a with the computed values.

The loop also calculates the twiddle factors, which are complex exponential factors used in the butterfly operations. The twiddle factors are calculated using trigonometric functions, such as sine and cosine, based on the angle theta. The variables wpr, wpi, wr, and wi are used to store intermediate values of the twiddle factors, which are updated in each iteration of the loop.

Finally, if the inversefft parameter is True, the function divides the result by the number of samples nn to obtain the correct inverse FFT result. This normalization step is performed using a loop that iterates through the array a and divides each element by nn.

In summary, the fastfouriertransform() function is an implementation of the Cooley-Tukey FFT algorithm, which is an efficient algorithm for computing the DFT and its inverse. This FFT library can be used for a variety of applications, such as signal processing, image processing, audio processing, and more.

Feal Fast Fourier Transform

The realfastfouriertransform() function performs a fast Fourier transform (FFT) specifically for real-valued functions. The FFT is an efficient algorithm used to compute the discrete Fourier transform (DFT) and its inverse, which are fundamental tools in signal processing, image processing, and other related fields.

This function takes three input parameters:

1. a - A float array containing the real-valued function samples.

2. tnn - The number of function values (must be a power of 2, but the algorithm does not validate this condition).

3. inversefft - A boolean flag that indicates the direction of the transformation (True for inverse, False for direct).

The function modifies the input array a in-place, meaning that the transformed data (the FFT result for direct transformation or the inverse FFT result for inverse transformation) will be stored in the same array a after the function execution.

The algorithm uses a combination of complex-to-complex FFT and additional transformations specific to real-valued data to optimize the computation. It takes into account the symmetry properties of the real-valued input data to reduce the computational complexity.

Here's a detailed walkthrough of the algorithm:

1. Depending on the inversefft flag, the initial values for ttheta, c1, and c2 are determined. These values are used for the initial data preprocessing and post-processing steps specific to the real-valued FFT.

2. The preprocessing step computes the initial real and imaginary parts of the data using a combination of sine and cosine terms with the input data. This step effectively converts the real-valued input data into complex-valued data suitable for the complex-to-complex FFT.

3. The complex-to-complex FFT is then performed on the preprocessed complex data. This involves bit-reversal reordering, followed by the Cooley-Tukey radix-2 decimation-in-time algorithm. This part of the code is similar to the fastfouriertransform() function you provided earlier.

4. After the complex-to-complex FFT, a post-processing step is performed to obtain the final real-valued output data. This involves updating the real and imaginary parts of the transformed data using sine and cosine terms, as well as the values c1 and c2.

5. Finally, if the inversefft flag is True, the output data is divided by the number of samples (nn) to obtain the inverse DFT.

The function does not return a value explicitly. Instead, the transformed data is stored in the input array a. After the function execution, you can access the transformed data in the a array, which will have the real part at even indices and the imaginary part at odd indices.

Fast Sine Transform

This code defines a function called fastsinetransform that performs a Fast Discrete Sine Transform (FST) on an array of real numbers. The function takes three input parameters:

1. a (float array): An array of real numbers representing the function values.

2. tnn (int): Number of function values (must be a power of two, but the code doesn't validate this).

3. inversefst (bool): A boolean flag indicating the direction of the transformation. If True, it performs the inverse FST, and if False, it performs the direct FST.

The output is the transformed array 'a', which will contain the result of the transformation.

The code starts by initializing several variables, including trigonometric constants for the sine transform. It then sets the first value of the array 'a' to 0 and calculates the initial values of 'y1' and 'y2', which are used to update the input array 'a' in the following loop.

The first loop (with index 'jx') iterates from 2 to (tm + 1), where 'tm' is half of the number of input samples 'tnn'. This loop is responsible for calculating the initial sine transform of the input data.

The second loop (with index 'ii') is a bit-reversal loop. It reorders the elements in the array 'a' based on the bit-reversed indices of the original order.

The third loop (with index 'ii') iterates while 'n' is greater than 'mmax', which starts at 2 and doubles each iteration. This loop performs the actual Fast Discrete Sine Transform. It calculates the sine transform using the Danielson-Lanczos lemma, which is a divide-and-conquer strategy for calculating Discrete Fourier Transforms (DFTs) efficiently.

The fourth loop (with index 'ix') is responsible for the final phase adjustments needed for the sine transform, updating the array 'a' accordingly.

The fifth loop (with index 'jj') updates the array 'a' one more time by dividing each element by 2 and calculating the sum of the even-indexed elements.

Finally, if the 'inversefst' flag is True, the code scales the transformed data by a factor of 2/tnn to get the inverse Fast Sine Transform.

In summary, the code performs a Fast Discrete Sine Transform on an input array of real numbers, either in the direct or inverse direction, and returns the transformed array. The algorithm is based on the Danielson-Lanczos lemma and uses a divide-and-conquer strategy for efficient computation.

Fast Cosine Transform

This code defines a function called fastcosinetransform that takes three parameters: a floating-point array a, an integer tnn, and a boolean inversefct. The function calculates the Fast Cosine Transform (FCT) or the inverse FCT of the input array, depending on the value of the inversefct parameter.

The Fast Cosine Transform is an algorithm that converts a sequence of values (time-domain) into a frequency domain representation. It is closely related to the Fast Fourier Transform (FFT) and can be used in various applications, such as signal processing and image compression.

Here's a detailed explanation of the code:

1. The function starts by initializing a number of variables, including counters, intermediate values, and constants.

2. The initial steps of the algorithm are performed. This includes calculating some trigonometric values and updating the input array a with the help of intermediate variables.

3. The code then enters a loop (from jx = 2 to tnn / 2). Within this loop, the algorithm computes and updates the elements of the input array a.

4. After the loop, the function prepares some variables for the next stage of the algorithm.

5. The next part of the algorithm is a series of nested loops that perform the bit-reversal permutation and apply the FCT to the input array a.

6. The code then calculates some additional trigonometric values, which are used in the next loop.

7. The following loop (from ix = 2 to tnn / 4 + 1) computes and updates the elements of the input array a using the previously calculated trigonometric values.

8. The input array a is further updated with the final calculations.

9. In the last loop (from j = 4 to tnn), the algorithm computes and updates the sum of elements in the input array a.

10. Finally, if the inversefct parameter is set to true, the function scales the input array a to obtain the inverse FCT.

The resulting transformed array is stored in the input array a. This means that the function modifies the input array in-place and does not return a new array.

Fast Convolution

This code defines a function called fastconvolution that performs the convolution of a given signal with a response function using the Fast Fourier Transform (FFT) technique. Convolution is a mathematical operation used in signal processing to combine two signals, producing a third signal representing how the shape of one signal is modified by the other.

The fastconvolution function takes the following input parameters:

1. float signal: This is an array of real numbers representing the input signal that will be convolved with the response function. The elements are numbered from 0 to SignalLen-1.

2. int signallen: This is an integer representing the length of the input signal array. It specifies the number of elements in the signal array.

3. float response: This is an array of real numbers representing the response function used for convolution. The response function consists of two parts: one corresponding to positive argument values and the other to negative argument values. Array elements with numbers from 0 to NegativeLen match the response values at points from -NegativeLen to 0, respectively. Array elements with numbers from NegativeLen+1 to NegativeLen+PositiveLen correspond to the response values in points from 1 to PositiveLen, respectively.

4. int negativelen: This is an integer representing the "negative length" of the response function. It indicates the number of elements in the response function array that correspond to negative argument values. Outside the range , the response function is considered zero.

5. int positivelen: This is an integer representing the "positive length" of the response function. It indicates the number of elements in the response function array that correspond to positive argument values. Similar to negativelen, outside the range , the response function is considered zero.

The function works by:

1. Calculating the length nl of the arrays used for FFT, ensuring it's a power of 2 and large enough to hold the signal and response.

2. Creating two new arrays, a1 and a2, of length nl and initializing them with the input signal and response function, respectively.

3. Applying the forward FFT (realfastfouriertransform) to both arrays, a1 and a2.

4. Performing element-wise multiplication of the FFT results in the frequency domain.

5. Applying the inverse FFT (realfastfouriertransform) to the multiplied results in a1.

6. Updating the original signal array with the convolution result, which is stored in the a1 array.

The result of the convolution is stored in the input signal array at the function exit.

Fast Correlation

This code defines a function called fastcorrelation that computes the correlation between a signal and a pattern using the Fast Fourier Transform (FFT) method. The function takes four input arguments and modifies the input signal array to store the correlation values.

Input arguments:

1. float signal: This is an array of real numbers representing the signal to be correlated with the pattern. The elements are numbered from 0 to SignalLen-1.

2. int signallen: This is an integer representing the length of the input signal array.

3. float pattern: This is an array of real numbers representing the pattern to be correlated with the signal. The elements are numbered from 0 to PatternLen-1.

4. int patternlen: This is an integer representing the length of the pattern array.

The function performs the following steps:

1. Calculate the required size nl for the FFT by finding the smallest power of 2 that is greater than or equal to the sum of the lengths of the signal and the pattern.

2. Create two new arrays a1 and a2 with the length nl and initialize them to 0.

3. Copy the signal array into a1 and pad it with zeros up to the length nl.

4. Copy the pattern array into a2 and pad it with zeros up to the length nl.

5. Compute the FFT of both a1 and a2.

6. Perform element-wise multiplication of the frequency-domain representation of a1 and the complex conjugate of the frequency-domain representation of a2.

7. Compute the inverse FFT of the result obtained in step 6.

8. Store the resulting correlation values in the original signal array.

At the end of the function, the signal array contains the correlation values at points from 0 to SignalLen-1.

Fast Fourier Transform of Two Real Functions

This code defines a function called tworealffts that computes the Fast Fourier Transform (FFT) of two real-valued functions (a1 and a2) using a Cooley-Tukey-based radix-2 Decimation in Time (DIT) algorithm. The FFT is a widely used algorithm for computing the discrete Fourier transform (DFT) and its inverse.

Input parameters:

1. float a1: an array of real numbers, representing the values of the first function.

2. float a2: an array of real numbers, representing the values of the second function.

3. float a: an output array to store the Fourier transform of the first function.

4. float b: an output array to store the Fourier transform of the second function.

5. int tn: an integer representing the number of function values. It must be a power of two, but the algorithm doesn't validate this condition.

The function performs the following steps:

1. Combine the two input arrays, a1 and a2, into a single array a by interleaving their elements.

2. Perform a 1D FFT on the combined array a using the radix-2 DIT algorithm.

3. Separate the FFT results of the two input functions from the combined array a and store them in output arrays a and b.

Here is a detailed breakdown of the radix-2 DIT algorithm used in this code:

1. Bit-reverse the order of the elements in the combined array a.

2. Initialize the loop variables mmax, istep, and theta.

3. Enter the main loop that iterates through different stages of the FFT.

a. Compute the sine and cosine values for the current stage using the theta variable.

b. Initialize the loop variables wr and wi for the current stage.

c. Enter the inner loop that iterates through the butterfly operations within each stage.

i. Perform the butterfly operation on the elements of array a.

ii. Update the loop variables wr and wi for the next butterfly operation.

d. Update the loop variables mmax, istep, and theta for the next stage.

4. Separate the FFT results of the two input functions from the combined array a and store them in output arrays a and b.

At the end of the function, the a and b arrays will contain the Fourier transform of the first and second functions, respectively. Note that the function overwrites the input arrays a and b.

█ Example scripts using functions contained in loxxfft

Real-Fast Fourier Transform of Price w/ Linear Regression

Real-Fast Fourier Transform of Price Oscillator

Normalized, Variety, Fast Fourier Transform Explorer

Variety RSI of Fast Discrete Cosine Transform

STD-Stepped Fast Cosine Transform Moving Average

Stochastic Enhanced [DCAUT]█ Stochastic Enhanced

📊 ORIGINALITY & INNOVATION

The Stochastic Enhanced indicator builds upon George Lane's classic momentum oscillator (developed in the late 1950s) by providing comprehensive smoothing algorithm flexibility. While traditional implementations limit users to Simple Moving Average (SMA) smoothing, this enhanced version offers 21 advanced smoothing algorithms, allowing traders to optimize the indicator's characteristics for different market conditions and trading styles.

Key Improvements:

Extended from single SMA smoothing to 21 professional-grade algorithms including adaptive filters (KAMA, FRAMA), zero-lag methods (ZLEMA, T3), and advanced digital filters (Kalman, Laguerre)

Maintains backward compatibility with traditional Stochastic calculations through SMA default setting

Unified smoothing algorithm applies to both %K and %D lines for consistent signal processing characteristics

Enhanced visual feedback with clear color distinction and background fill highlighting for intuitive signal recognition

Comprehensive alert system covering crossovers and zone entries for systematic trade management

Differentiation from Traditional Stochastic:

Traditional Stochastic indicators use fixed SMA smoothing, which introduces consistent lag regardless of market volatility. This enhanced version addresses the limitation by offering adaptive algorithms that adjust to market conditions (KAMA, FRAMA), reduce lag without sacrificing smoothness (ZLEMA, T3, HMA), or provide superior noise filtering (Kalman Filter, Laguerre filters). The flexibility helps traders balance responsiveness and stability according to their specific needs.

📐 MATHEMATICAL FOUNDATION

Core Stochastic Calculation:

The Stochastic Oscillator measures the position of the current close relative to the high-low range over a specified period:

Step 1: Raw %K Calculation

%K_raw = 100 × (Close - Lowest Low) / (Highest High - Lowest Low)

Where:

Close = Current closing price

Lowest Low = Lowest low over the %K Length period

Highest High = Highest high over the %K Length period

Result ranges from 0 (close at period low) to 100 (close at period high)

Step 2: Smoothed %K Calculation

%K = MA(%K_raw, K Smoothing Period, MA Type)

Where:

MA = Selected moving average algorithm (SMA, EMA, etc.)