Probability ConesA probability cone is an indicator that forecasts a statistical distribution from a set point in time into the future.

Features

Forecast a Standard or Laplace distribution.

Change the how many bars the cones will lookback and sample in their calculations.

Set how many bars to forecast the cones.

Let the cones follow price from a set number of bars back.

Anchor the cones and they will not update from their last location.

Show or hide any set of cones.

Change the deviation used of any cone's upper or lower line.

Change any line's color, style, or width.

Change or toggle the fill colors between any two cone lines.

Basic Interpretations

First, there is an assumption that the distribution starting from the cone's origin, based on the number of historical bars sampled, is likely to represent the distribution of future price.

Price typically hangs around the mean.

About 68% of price stays within the first deviation cones.

About 95% of price stays within the second deviation cones.

About 99.7% of price stays within the third deviation cones.

When price is between the first and second deviation cones, there is a higher probability for a reversal.

However, strong momentum while above or below the first deviation can indicate a trend where price maintains itself past the first deviation. For this reason it's recommended to use a momentum indicator alongside the cones.

There is no mean reversion assumption when price deviates. Price can continue to stay deviated.

It's recommended that the cones are placed at the beginning of calendar periods. Like the month, week, or day.

Be mindful when using the cones on various timeframes. As the lookback setting, which selects the number of bars back to load from the cone's origin, will load the number of bars back based on the current timeframe.

Second Deviation Strategy

How to react when price goes beyond the second deviation is contingent on your trading position.

If you are holding a losing trade and price has moved past the second deviation, it could be time to stop trading and exit.

If you are holding a winning trade and price has moved past the second deviation, it would be best to look at exit strategies to capitalize on the outperformance.

If price has moved beyond the second deviation and you hold no position, then do not open any new trades.

חפש סקריפטים עבור "ha溢价率"

vix_vx_regressionAn example of the linear regression library, showing the regression of VX futures on the VIX. The beta might help you weight VX futures when hedging SPX vega exposure. A VX future has point multiplier of 1000, whereas SPX options have a point multiplier of 100. Suppose the front month VX future has a beta of 0.6 and the front month SPX straddle has a vega of 8.5. Using these approximations, the VX future will underhedge the SPX straddle, since (0.6 * 1000) < (8.5 * 100). The position will have about 2.5 ($250) vega. Use the R^2 (coefficient of determination) to check how well the model fits the relationship between VX and VIX. The further from one this value, the less useful the model.

(Note that the mini, VXM futures also have a 100 point multiplier).

Trade Helper [Trading Nerd]Position Size Calculator / Lot Size Calculator

Disclaimer: I do my best to avoid wrong calculations and bugs. I provide this indicator without warranties of any kind. You bear all risks associated with the use of this indicator.

Inputs:

Market: Adds a name tag to the Table to keep track of the trades.

Entry Price: The entry Price of the Position.

Entry Time: The entry Time/Candle of the Position. If Stop Loss Type is 'ATR' or 'HH/LL' the Value for this is calculated by this Candle.

Stop Loss Type: Changes the Stop Loss Type.

Direction: Define if the trade direction is 'Long' or 'Short'. Has no effect on Stop Loss Type 'Custom'. For this you can just set the Stop Loss below/above the Entry Price .

ATR Multiplier: Multiplies the ATR Value by this number. Has only an effect on Stop Loss Type 'ATR'.

HH/LL Lookback Length: Lookback length for determine Highest High/Lowest Low value. Has only an effect on Stop Loss Type 'HH/LL'.

Custom SL Price: The Stop Loss Price if the Stop Loss Type is set to 'Custom'.

Risk Reward Ratio: The Risk is multiplied by this number to determine the Take Profit Price.

Balance: Balance Amount and Currency

Contract Size: The Position Size is divided by this number. E.G. in Forex one Lot is 100.000 Contracts. Change this Value depending on your Broker and Market.

Risk in %: Percent that is risked of the Balance for one Trade.

AveragesLibrary "Averages"

Contains utilities for generating averages from arrays. Useful for manipulated or cleaned data.

triangular(src, startingWeight) Calculates the triangular weighted average of a set of values where the last value has the highest weight.

Parameters:

src : The array to derive the average from.

startingWeight : The weight to begin with when calculating the average. Higher numbers will decrease the bias.

weighted(src, weights, weightDefault) Calculates the weighted average of a set of values.

Parameters:

src : The array to derive the average from.

weights : The array containing the weights for the source.

weightDefault : The default value to use when a weight is NA.

triangularWeighted(src, weights, startingWeight) Calculates the weighted average of a set of values where the last value has the highest triangular multiple.

Parameters:

src : The array to derive the average from.

weights : The array containing the weights for the source.

startingWeight : The multiple to begin with when calculating the average. Higher numbers will decrease the bias.

exponential(src) Calculates the exponential average of a set of values where the last value has the highest weight.

Parameters:

src : The array to derive the average from.

arrayFrom(src, len, omitNA) Creates an array from the provided series (oldest to newest).

Parameters:

src : The array to derive from.

len : The target length of the array.

omitNA : If true, NA values will not be added to the array and the resultant array may be shorter than the target length.

Currency Strength Meter [HeWhoMustNotBeNamed]⬜ Note: This is not the strength of currency pairs. But, in this script we are trying to derive strength of individual currencies by matching against single base currency.

⬜ Process

This is based on similar concept as that of Magic Numbers for stocks. Idea is simple.

▶ Calculate strength of each currency against USD. Derive the strength for both price movement and volume movement.

▶ Similarly calculate momentum of price and volume change.

▶ If USD is base currency, inverse momentum and strength index for the given symbol.

▶ Once these calculations are done, rank each currencies based on individual score on given things.

▶ Add up all the ranks to derive combined rank

▶ sort the currencies in the ascending order of overall rank.

⬜ USAGE

▶ Identify a base currency. In our case, we have used USD as base currency as it is easy to get pairs of all currencies with USD.

▶ Identify most used combos for all other currencies which are paired with USD. Fx pair can either have USD as base currency or quote currency. It is desirable to use the pair which is most traded. For example, USDJPY is more traded pair than JPYUSD - hence it is advisable to use USDJPY instead of JPYUSD. Similarly AUDUSD is more traded than USDAUD - hence choosing AUDUSD for the purpose of this exercise is better approach. Notice that USDJPY has USD as base currency whereas AUDUSD has USD as quote currency. These calculations are handled internally to derive the right outcome irrespective of position of USD in the pair.

▶ Identify the forex broker which has all the selected forex tickers. All comparison is done against a single broker. Hence, choosing broker which does not wide range of forex pairs will show NAN for many rows.

▶ Once we set these, we get tabular output containing strength and oscillator based trend indexes for both price and volume indicator. Currencies are ordered in descending order of strength. Hence, top of the list can be considered as currency having highest strength and bottom of the table can be considered as currency having lowest strength. Please note that the calculation is valid only for selected timeframe and users can set other parameters such as moving average type, oscillator type, length etc which can alter the outcome.

▶ Use multiple timeframes to find out stronger and weaker currencies. Use directional indicators to understand where they are heading. Combine all these info to come up with currency pair you would like to trade :)

⬜ Settings

▶ Main settings and Currencies

Base Currency : This is set to USD by default as rest of the tickers used are paired with USD. Whatever the base currency is selected, rest of the tickers should follow the same combination.

Timeframe : Timeframe for which rankings need to be calculated.

Currencies : These should be the currency pair which involve base currency defined in the setting on either side.

▶ Display

Table : Allows users to set table location and size of the table. By default this is set to middle center and default size is normal. If user want to use multiple timeframes side by side, they can do so by changing these display settings.

Stat Type : To show either comparative ranking or actual indicator values

Jurik MacD & Leader NCMhey everyone,

While there are some Invite-Only Jurik MacDs, there are no free/open ones, so I thought I'd create one and publish it. It has most of the bells and whistles you'd want (I hope!).

You can see one with the bells and whistles all turned on in the first, and a 'quieter' one in the second.

//-----------------////-----------------////-----------------//

Why Jurik?

The Jurik MA is a quicker and smoother Exponential MA, and the best of all MAs, according to Jurik Research (lol). To be fair. I have found it to be excellent, and that is why I'm publishing this.

Power can be changed, recommended from 1-4: increasing it pulls it closer to the current price (almost like reducing the period), and decreasing: vice versa.

Phase increases the inertia of the line, how quickly it will respect price changes. It is usual to have less inertia on the fast JMA, and more on the slower (but remember the MACD line is the FastJMA minus the SlowJMA, so you may find adjusting power and phase on Signal line more effective). Search online for JurikRes (or Jurik Research) for more detailed information about the Jurik.

In the coding I have included a list of four different ways to set up the JMAs: however, you should probably tune this to your preferred asset (as with almost all indicators). If you find a good setup, please let me know!

You could trade with a MacD a number of ways. Entries could be:

- MacD crossing the zero line

- MacD crossing over the Signal line

- Histogram crossing above zero line.

Vice versa for exits. If this isn't enough, please google 'trading with a MacD'.

No indicator is perfect for trading, and that includes this one! Don't trade unless you know what you're doing.

//-----------------////-----------------////-----------------//

Please let me know if I can improve this script, or you have any other feedback. I can post code for colour palette as well if that is something anyone is keen on.

//-----------------////-----------------////-----------------//

Thanks to the many excellent coders that publish freely their code. I have learned so much from this community, and this code is based on the work of others (Chris Moody and everget).

Shout out to StevieMagg as well, who has helped me develop (and didn't want to charge me!). The Pine Script Community on Discord has been brilliant - lots of knowledge, ideas, support - thanks guys.

If you are new and interested in pine coding, I suggest you check out some of the masters (in no order):

ChrisMoody

Everget

RedKTrader

LonesomeDove

LazyBear

KivancOzbilgic

and more that I am missing. It is not necessarily the popular scripts that are the best.

//-----------------////-----------------////-----------------//

Kind regards,

Nelson

Vortex indicator cross support&resistance [LM]Hello traders,

I would like you to present Vortex indicator cross support&resistance script. The idea behind is same as my other S/R scripts to look for important S/R levels.

This time I have used little known and not that old Vortex Indicator that has been released in 2010. Vortex indicator has two plots that crosses each other and on the cross line is rendered. I have included smoothing with TEMA.

The indicator has following settings:

General control - here you can select period of vortex indicator and show/hide labels

Line control - where you can select type of line, colors...

Hope you will enjoy it,

Lukas

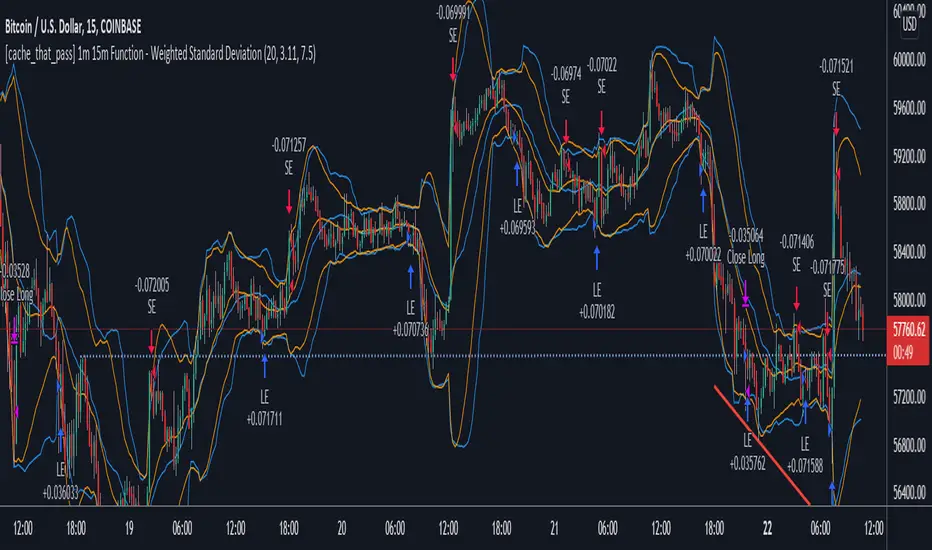

[cache_that_pass] 1m 15m Function - Weighted Standard DeviationTradingview Community,

As I progress through my journey, I have come to the realization that it is time to give back. This script isn't a life changer, but it has the building blocks for a motivated individual to optimize the parameters and have a production script ready to go.

Credit for the indicator is due to @rumpypumpydumpy

I adapted this indicator to a strategy for crypto markets. 15 minute time frame has worked best for me.

It is a standard deviation script that has 3 important user configured parameters. These 3 things are what the end user should tweak for optimum returns. They are....

1) Lookback Length - I have had luck with it set to 20, but any value from 1-1000 it will accept.

2) stopPer - Stop Loss percentage of each trade

3) takePer - Take Profit percentage of each trade

2 and 3 above are where you will see significant changes in returns by altering them and trying different percentages. An experienced pinescript programmer can take this and build on it even more. If you do, I ask that you please share the script with the community in an open-source fashion.

It also already accounts for the commission percentage of 0.075% that Binance.US uses for people who pay fees with BNB.

How it works...

It calculates a weighted standard deviation of the price for the lookback period set (so 20 candles is default). It recalculates each time a new candle is printed. It trades when price lows crossunder the bottom of that deviation channel, and sells when price highs crossover the top of that deviation channel. It works best in mid to long term sideways channels / Wyckoff accumulation periods.

40+ Coin Screener (workaround to 40 Security Limit Per Script) This is a far inferior method for a screener/scanner (compared to my first publication) but after looking at that script from a noobs eyes again, I could see how this form would be a lot easier to take in/understand so wanted to publish it. Everything that I could think of to mention about this is in my 1st pub so ill leave it to you to check it out...though I did include some comments in the script. It is pretty straight forward but if you have any questions don't hold them in. I'll answer them if I can. The only thing that is not in this one is setting up the alert feature so that you only have to create 1 alert per iteration of the script and it takes care of all of the coins for that iteration/set that is chosen in the settings (so please see previous script if would like to do this for your screener/scanner).

To be PERFECTLY CLEAR, the workaround is to the issue of not being able to scan but only 40 coins per script. You can scan more than 40 per script but only if you create "batches" or "sets" that the user can select within the settings which set to use for each iteration of the script on the chart. That being, you have to the script multiple times to the chart and merge them into 1 window and merge the scales (instructions in first publications). Here in this script I am scanning 72 different coins that are the Margin Coins on KUCOIN. I have split them up into 3 sets (24 coins per set). I could have made 2 sets but the script will be slower to load and to respond (like, when it comes to receiving alerts), thus I split them up the way I did. If you want to change any of this there are slightly more details in the previous script.

One great use-case that I LOVE about this particular version (and the way I use it) is right at the end of when I see a whole market dump/pump coming to an end and want to know which horse to bet on. Used to think whichever coin come out the fastest from the dump was the one to bet on but quickly learned that 1-2 (or even a few) hrs needs to go by first bc the ones that look the strongest in the beginning are NOT the ones to have performed the best when viewing the results 12 hrs later. IN FACT, many instances of using this exact script for reasons as such has taught me that the manipulators (I believe this to be the case as least) WANT everyone to bet on these that come out the gate the hardest and thus they make them move REALLY hard in the beginning then they QUICKLY become stagnant (moreso, they become WORSE than stagnant, they actually quickly retrace to put you into the negative so that you get out to get into the others now moving (to provide the market with more liquidity. They WANT you to get into a coin thats moving crazy hard so that they can then cease that movement once many fall for the trick just to then make that once strong looking coin now stagnant and make others move crazy hard. They wait for you to get out of the 1st and into the next set of movers just to do this time and time again bc hey, what are we sheep good for other than to provide the big guns with liquidity, am I right? Thats rhetorical, which you would know if you've ever had this happen to you (without a doubt MANY of you have). Let this script (above all other things) provide good evidence to back up this cynical way of viewing the markets to anyone that is questioning it.

This prolonged time between when the dump is over and when the ACTUAL movers REALLY start moving can actually be of great benefit to us sheep if used correctly, Firstly, it gives us some time to determine if when we thought was the bottom, ACTUALLY was the bottom. That bottom is easily determined if there are no (or very few) coins that went any lower than the point in time that the script began calculating on. Secondly, it allows us time to wait for the REAL movers and shakers to start moving and shaking.

One new feature that I LOVE that TV has implemented is the ability (once the script is added to the chart) to be able to click a point in time on the chart where you want the script to begin its calculations. If this point needs to be changed at any point in time then you can either go into the setting and input the time you wish or simply remove the script and add it again so that you are prompted to select another point in time. Ok, I think that everything I wanted to say. The next version that I will add will be probably my favorite and most used by yours truly...not to mention unique in a way that I have yet to see an implementation anything like it in all of TV's public library. Not to say its not there, but I have yet to come across it and I have DEFINITELY done my fair share of searching for it when I couldn't figure out how to code it for the longest time (though, I was and still am a noob so might get some great feedback on better ways to approach it, but we'll save that jabbering for the next of the publications.

I hope each and every one of ya'll (yes, Im from the South) have the GREATEST of Thanksgivings (if in the US that is...I graced my parents with the best gift anyone could have given them 35 years ago on Thanksgiving....MEEEE ;) So I will sure as hell be having a great holiday. Thanks for checking out my script...you can "like" and leave a comment if you so feel the urge to...or not. Im not doing this for me, but rather to stretch my arms out as far as possible to benefit the most people as possible and more people would see the script if it has more likes/comments/traffic pointing towards it...not to mention as other publishers have...it IS gratifying to see a few likes in my side window, which btw, I have MANY more variations and completely diff types of scanners/screeners Ill be publishing in the future and to know that they've become of use....I"VE become of use to the community is very....pleasing to me and does (as I've also seen many publishers mention as well) drive me to want to publish ones that I originally thought I would keep for myself. Peace out people.

Ripple (XRP) Model PriceAn article titled Bitcoin Stock-to-Flow Model was published in March 2019 by "PlanB" with mathematical model used to calculate Bitcoin model price during the time. We know that Ripple has a strong correlation with Bitcoin. But does this correlation have a definite rule?

In this study, we examine the relationship between bitcoin's stock-to-flow ratio and the ripple(XRP) price.

The Halving and the stock-to-flow ratio

Stock-to-flow is defined as a relationship between production and current stock that is out there.

SF = stock / flow

The term "halving" as it relates to Bitcoin has to do with how many Bitcoin tokens are found in a newly created block. Back in 2009, when Bitcoin launched, each block contained 50 BTC, but this amount was set to be reduced by 50% every 210,000 blocks (about 4 years). Today, there have been three halving events, and a block now only contains 6.25 BTC. When the next halving occurs, a block will only contain 3.125 BTC. Halving events will continue until the reward for minors reaches 0 BTC.

With each halving, the stock-to-flow ratio increased and Bitcoin experienced a huge bull market that absolutely crushed its previous all-time high. But what exactly does this affect the price of Ripple?

Price Model

I have used Bitcoin's stock-to-flow ratio and Ripple's price data from April 1, 2014 to November 3, 2021 (Daily Close-Price) as the statistical population.

Then I used linear regression to determine the relationship between the natural logarithm of the Ripple price and the natural logarithm of the Bitcoin's stock-to-flow (BSF).

You can see the results in the image below:

Basic Equation : ln(Model Price) = 3.2977 * ln(BSF) - 12.13

The high R-Squared value (R2 = 0.83) indicates a large positive linear association.

Then I "winsorized" the statistical data to limit extreme values to reduce the effect of possibly spurious outliers (This process affected less than 4.5% of the total price data).

ln(Model Price) = 3.3297 * ln(BSF) - 12.214

If we raise the both sides of the equation to the power of e, we will have:

============================================

Final Equation:

■ Model Price = Exp(- 12.214) * BSF ^ 3.3297

Where BSF is Bitcoin's stock-to-flow

============================================

If we put current Bitcoin's stock-to-flow value (54.2) into this equation we get value of 2.95USD. This is the price which is indicated by the model.

There is a power law relationship between the market price and Bitcoin's stock-to-flow (BSF). Power laws are interesting because they reveal an underlying regularity in the properties of seemingly random complex systems.

I plotted XRP model price (black) over time on the chart.

Estimating the range of price movements

I also used several bands to estimate the range of price movements and used the residual standard deviation to determine the equation for those bands.

Residual STDEV = 0.82188

ln(First-Upper-Band) = 3.3297 * ln(BSF) - 12.214 + Residual STDEV =>

ln(First-Upper-Band) = 3.3297 * ln(BSF) – 11.392 =>

■ First-Upper-Band = Exp(-11.392) * BSF ^ 3.3297

In the same way:

■ First-Lower-Band = Exp(-13.036) * BSF ^ 3.3297

I also used twice the residual standard deviation to define two extra bands:

■ Second-Upper-Band = Exp(-10.570) * BSF ^ 3.3297

■ Second-Lower-Band = Exp(-13.858) * BSF ^ 3.3297

These bands can be used to determine overbought and oversold levels.

Estimating of the future price movements

Because we know that every four years the stock-to-flow ratio, or current circulation relative to new supply, doubles, this metric can be plotted into the future.

At the time of the next halving event, Bitcoins will be produced at a rate of 450 BTC / day. There will be around 19,900,000 coins in circulation by August 2025

It is estimated that during first year of Bitcoin (2009) Satoshi Nakamoto (Bitcoin creator) mined around 1 million Bitcoins and did not move them until today. It can be debated if those coins might be lost or Satoshi is just waiting still to sell them but the fact is that they are not moving at all ever since. We simply decrease stock amount for 1 million BTC so stock to flow value would be:

BSF = (19,900,000 – 1.000.000) / (450 * 365) =115.07

Thus, Bitcoin's stock-to-flow will increase to around 115 until AUG 2025. If we put this number in the equation:

Model Price = Exp(- 12.214) * 114 ^ 3.3297 = 36.06$

Ripple has a fixed supply rate. In AUG 2025, the total number of coins in circulation will be about 56,000,000,000. According to the equation, Ripple's market cap will reach $2 trillion.

Note that these studies have been conducted only to better understand price movements and are not a financial advice.

LA_Crpyto_Pirate Modifie VuManChu B Script with Scalping FiltersI added the following filters for entry signals to the VuManChu B with divergences for use as a scalping indicator. You will need to load the 50 EMA and this indicator to trade this per the rules below

The rules for trading this are as follows; You can only take a long or short entry when all of these requirements match

The wave cross is under the zero line (long) or over the zero line (short)

The money flow indicator is green (long) or red (short)

The closing price is above the 200 EMA (long) or below the 200 EMA (short)

price has pulled back to the 50 EMA

Here are the filters I employed in the script to help you trade this

Zero Line Filter: Only signal longs under the zero line and shorts over the zero line will fire off a signal

Money Flow Indicator Filter: Only signal longs when money flow is green and only shorts when money flow is red

200 MA filter: Only longs when price is closing above the 200 EMA and only shorts when price is closing below the 200 EMA

When you get an alert, simply check to see that price has pulled back to the 50 EMA before entering. Place long and short orders when the indicator signals and you confirm price has pulled back to the 50 ema before entering the long or short. Set your Stop Loss above or below the pervious pullback and set a reward ratio of your choice. Good luck!

Compression support&resistance [LM]Hello traders,

I would like to present you Compression support&resistance script. The idea behind is to look for areas of price compression(inside bar candles). Basically the S/R lines are created after three candles that are formed in certain pattern and volume conditions. First candle of pattern is usually the most volatile and fist inside bar after volatile candle high and low creates S/R lines in order to look for breakouts or for future bounces of the S/R line. Also by default volume has to be decreasing from candle to candle, although this condition can be controlled by setting.

It has various settings as my other S/R scripts for multi timeframe analysis. The current timeframe uses line API but for multi timeframe I use plot lines. There are two filters. Volume filter for declining volume of the pattern candles and volatility filter which renders line only in case that pattern occurs after some % change has happened within some lookback period.

Credit also for this indicator goes to @berkek as he took time to explain it to me.

Hope you will enjoy it,

Lukas

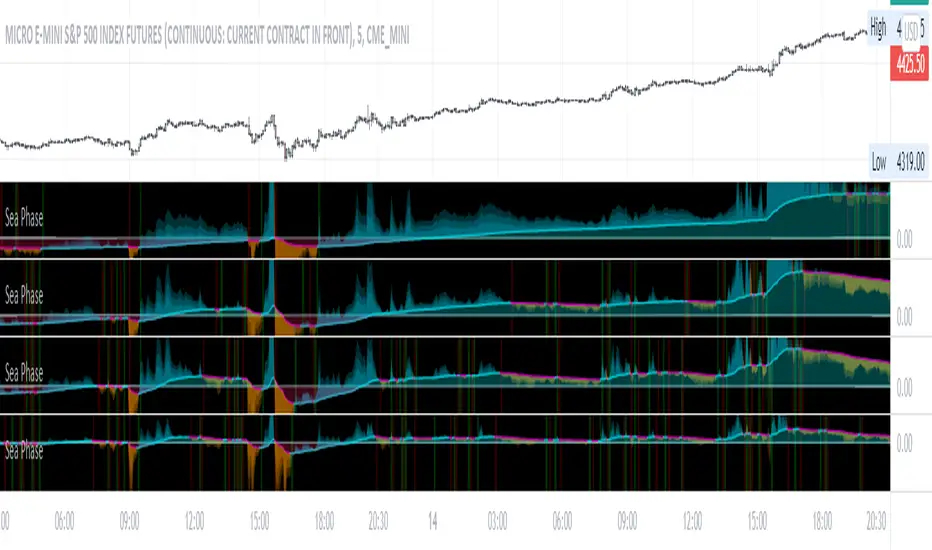

Sea Phase [DM]Greetings Colleagues

I share a simple indicator

Follow the progression of:

1. Development of the range of the daily bars

2. Development of the "Normalized" daily volume difference

3. Difference of closing price with closing of the previous bar instead of with the opening price because it is more effective.

4. It also has a background with the crossing of the signal with its own moving average.

The set has been simplified with three lengths that if you want you do not have to adjust it has a selector that multiplies the lengths to make the signal smoother

Enjoy!!!

TASC 2021.11 MADH Moving Average Difference, Hann█ OVERVIEW

Presented here is code for the "Moving Average Difference, Hann" indicator originally conceived by John Ehlers. The code is also published in the November 2021 issue of Trader's Tips by Technical Analysis of Stocks & Commodities (TASC) magazine.

█ CONCEPTS

By employing a Hann windowed finite impulse response filter (FIR), John Ehlers has enhanced the Moving Average Difference (MAD) to provide an oscillator with exceptional smoothness.

Of notable mention, the wave form of MADH resembles Ehlers' "Reverse EMA" Indicator, formerly revealed in the September 2017 issue of TASC. Many variations of the "Reverse EMA" were published in TradingView's Public Library.

█ FEATURES

Three values in the script's "Settings/Inputs" provide control over the oscillators behavior:

• The price source

• A "Short Length" with a default of 8, to manage the lower band edge of the oscillator

• The "Dominant Cycle", originally set at 27, which appears to be a placeholder for an adaptive control mechanism

Two coloring options are provided for the line's fill:

• "ZeroCross", the default, uses the line's position above/below the zero level. This is the mode used in the top version of MADH on this chart.

• "Momentum" uses the line's up/down state, as shown in the bottom version of the indicator on the chart.

█ NOTES

Calculations

The source price is used in two independent Hann windowed FIR filters having two different periods (lengths) of historical observation for calculation, one being a "Short Length" and the other termed "Dominant Cycle". These are then passed to a "rate of change" calculation and then returned by the reusable function. The secret sauce is that a "windowed Hann FIR filter" is superior tp a generic SMA filter, and that ultimately reveals Ehlers' clever enhancement. We'll have to wait and see what ingenuities Ehlers has next to unleash. Stay tuned...

The `madh()` function code was optimized for computational efficiency in Pine, differing visibly from Ehlers' original formula, but yielding the same results as Ehlers' version.

Background

This indicator has a sibling indicator discussed in the "The MAD Indicator, Enhanced" article by Ehlers. MADH is an evolutionary update from the prior MAD indicator code published in the October 2021 issue of TASC.

Sibling Indicators

• Moving Average Difference (MAD)

• Cycle/Trend Analytics

Related Information

• Cycle/Trend Analytics And The MAD Indicator

• The Reverse EMA Indicator

• Hann Window

• ROC

Join TradingView!

MACD PlusMoving Average Convergence Divergence – MACD

The MACD is an extremely popular indicator used in technical analysis. It can be used to identify aspects of a security's overall trend. Most notably these aspects are momentum, as well as trend direction and duration. What makes the MACD so informative is that it is actually the combination of two different types of indicators. First, the MACD employs two Moving Averages of varying lengths (which are lagging indicators) to identify trend direction and duration. Then, it takes the difference in values between those two Moving Averages (MACD Line) and an EMA of those Moving Averages (Signal Line) and plots that difference between the two lines as a histogram which oscillates above and below a center Zero Line. The histogram is used as a good indication of a security's momentum.

Added Color Plots to Settings Pane.

Switched MTF Logic to turn ON/OFF automatically w/ TradingView's Built in Feature.

Added Ability to Turn ON/OFF Show MacD & Signal Line.

Added Ability to Turn ON/OFF Show Histogram.

Added Ability to Change MACD Line Colors Based on Trend.

Added Ability to Highlight Price Bars Based on Trend.

Added Alerts to Settings Pane.

Customized Alerts to Show Symbol, TimeFrame, Closing Price, MACD Crosses Up & MACD Crosses Down Signals in Alert.

Alerts are Pre-Set to only Alert on Bar Close.

Added ability to show Dots when MACD Crosses.

Added Ability to Change Plot Widths in Settings Pane.

Added in Alert Feature where Cross Up if above 0 or cross down if below 0 (OFF By Default).

Squeeze Pro

Traditionally, John Carter's version uses 20 period SMAs as the basis lines on both the BB and the KC.

In this version, I've given the freedom to change this and try out different types of moving averages.

The original squeeze indicator had only one Squeeze setting, though this new one has three.

The gray dot Squeeze, call it a "low squeeze" or an "early squeeze" - this is the easiest Squeeze to form based on its settings.

The orange dot Squeeze is the original from the first Squeeze indicator.

And finally, the yellow dot squeeze, call it a "high squeeze" or "power squeeze" - is the most difficult to form and suggests price is under extreme levels of compression.

Colored Directional Movement Index (CDMI) , a custom interpretation of J. Welles Wilder’s Directional Movement Index (DMI), where :

DMI is a collection of three separate indicators ( ADX , +DI , -DI ) combined into one and measures the trend’s strength as well as its direction

CDMI is a custom interpretation of DMI which presents ( ADX , +DI , -DI ) with a color scale - representing the trend’s strength, color density - representing momentum/slope of the trend’s strength, and triangle up/down shapes - representing the trend’s direction. CDMI provides all the information in a single line with colored triangle shapes plotted on the bottom. DMI can provide quality information and even trading signals but it is not an easy indicator to master, whereus CDMI simplifies its usage. The CDMI adds additional insight of verifying/confirming the trend as well as its strength

Label :

Displaying the trend strength and direction

Displaying adx and di+/di- values

Displaying adx's momentum (growing or falling)

Where tooltip label describes "howto read colored dmi line"

Ability to display historical values of DMI readings displayed in the label.

Added "Expert Trend Locator - XTL"

The XTL was developed by Tom Joseph (in his book Applying Technical Analysis ) to identify major trends, similar to Elliott Wave 3 type swings.

Blue bars are bullish and indicate a potential upwards impulse.

Red bars are bearish and indicate a potential downwards impulse.

White bars indicate no trend is detected at the moment.

Added "Williams Vix Fix" signal. The Vix is one of the most reliable indicators in history for finding market bottoms. The Williams Vix Fix is simply a code from Larry Williams creating almost identical results for creating the same ability the Vix has to all assets.

The VIX has always been much better at signaling bottoms than tops. Simple reason is when market falls retail traders panic and increase volatility , and professionals come in and capitalize on the situation. At market tops there is no one panicking... just liquidity drying up.

The FE green triangles are "Filtered Entries"

The AE green triangles are "Aggressive Filtered Entries"

DCA Bot Long/Short Thanks to @TheTradingParrot for the inspiration and knowledge shared.

Thanks to @ericlin0122 for the original DCA Bot Emulator which is the backbone of this strategy.

The script simulates DCA strategy with parameters used in 3commas DCA bots for futures trading. Experiment with parameters

to find your trading setup.

Beware how large your total leveraged position is and how far can market go before you get liquidated!

Do that with the help of futures liquidation calculators you can find online!

I`ve added:

1) an internal average price and profit calculating, instead of TV`s native one, which is subject to severe slippage.

2) I`ve built a graphic interface, so levels are clearly visible and back-test analyzing made easier.

3) now both Long & Short direction of the strategy exist.

4) trailing TP which was featured in the initial script has been removed because TV`s execution model makes

it impossible to know how the real world trailing would have unfolded.

5) the table is self explanatory, and it is there to help you discover what happened and where.

6) vertical colored lines appear when the new maximum deviation from the original price has

been reached

All the trading happens with total account capital, and all order sizes inputs are expressed in percent.

Known issues:

When deviation is small, and the same candle triggers safety AND the close order, the initial orders are closed, but a

new one opens on the next candle. This is "resolved" by closing the unwanted trade forcefully on the next candle, affecting

profit calculating minimally and guaranteeing that what should be closed has been closed.

The code could be improved through use of arrays, making the table flexible so the number of rows should be dynamic depending

on the number of SOs.

!!!!! IMPORTANT!!!!!

This strategy script is made to receive a signal from an exterior study script, which should plot +100 for long or -100 for short

entry (that is by default - values can be changed in the strategy settings menu). That plot should be found in "Enter Trigger" input

dropdown menu at the bottom of strategy settings menu. Removing the "and trigger == long/short_trigger" condition from strategy entry

conditions makes the strategy open trades ASAP.

Cheers!

Vigia blai5VIGÍA is the latest and current version of this weighted indicator that collects, combines and harmonizes the values of four other classic indicators: RSI, MFI, Bollinger Bands and Stochastic.

It is a 2nd Generation indicator, as it does not base its algorithm on pure price data, but on its evolution (volatility, volume differences, power variations, cycle phase ...) working from first generation indicators included and mixed in the algorithm.

With the RSI we detect current power or depletion; the MFI adds the harmonization between price and volume; Bollinger Bands warn us of positions in areas close to support and resistance, and Stochastic informs us of the favorable and unfavorable phases of its cycle. VIGÍA tries to gather all this information in a single value and signal. This is how the curve of this indicator emerges.

The layout of this curve is its own and different from that of the other four separately. But the key idea of this complex indicator is to harmonize the signals.

By "harmonizing" we mean that an exaggerated value of one of the individual indicators, being part of a set, is nuanced. On the other hand, a simultaneous good look in two or more, enhances the resulting signal making it more visible and clear for trading.

One of the main effects that I have tried to enhance in the various versions of VIGÍA is its geometry, so one of the best ways to operate the indicator is divergences, which are generally quite reliable.

But, unlike so many conventional indicators, VIGÍA allows us a relatively large number of operations, which can satisfy both lovers of the most daring techniques and those who are more prudent in their trading.

In the first place, the black line is properly the Watch Signal (SV), the soul and central element of this entire invention.

On it you will see that a red line is oscillating. It is an Exponential Average of the indicator itself (by default, value 20). It is of enormous interest for trading since the SV cuts on its Average can be taken as entry and exit signals. (To check it, you just have to check it on the history of any value or index).

But there are more elements. An important change is the transformation of fixed levels into variable trading bands. This system allows the environment to adapt to changes in the asset price, recognizing and transforming itself according to the trend or laterality phases through which it runs. The signal moves above and below a central zero value and (as always) with no extreme limits, because it is important to remember that VIGÍA is not an oscillator and that prevents it from reaching a predefined extreme and being 'keyed in'.

On the upper variable band, we enter the overload zone, in Vigía's own jargon, while under the lower variable band, the situation of the indicator is on discharge. It is interesting to observe how, precisely the crossing of these variable bands by Vigía coincides on many occasions with the fastest and most productive phase of the entire price shift, far from concepts that in this phase we should already abandon as outdated and unreliable such as "overbought" or "oversold."

The last two elements remain to be described: a timid blue dashed line and that flickering central area of color called the Astro.

The blue dashed line is named Filter. It is a much more useful element than its smooth and modest journey appears. The Filter has some really fascinating features. Notice, for example, that it is the only line that I keep in visible numerical value, to know exactly when it has a positive and negative value. In periods of laterality, it is a good ally to help us make decisions. It does more things, but that is a prize reserved for whoever pays some attention to it… :-))

We will finish by Astro. Astro is an indicator with its own personality that I designed separately, it is available independently, but I ended up incorporating it into Watcher, which also happens with the Medium Proportional Volume (MPV). Both can be presented or hidden, according to the tastes or needs of the user.

Astro is an adjustable trend indicator, a very useful little tool that will help us identify the critical points where we must consider entries or changes in position. Its default value is 8 cycles, which is a good fit for daily stocks, but I have left open the possibility of modifying its period to be able to take advantage of all its power in intraday temporalities. Once again, I invite you to DO NOT believe me, but to launch the indicator on any asset and evaluate the signals that Astro has offered on its history.

Exponential MA Channel, Daily Timeframe (Crypto)Moving averages are some of the most common tools for traders. Some of the most widely used ones are simple moving averages (e.g. 20SMA, 50 SMA, 100 SMA, 200SMA,...). There are endless combinations of moving averages that can be used. I prefer to use exponential moving averages because they react more quickly to price data (essentially they filter back through the data over a discrete number of timesteps, with more recent history receiving the highest weighting in the final calculation).

This script uses a combination of the 21EMA, 53 EMA, and 100EMA. The idea of this script is to provide insight into when an asset might be close to a local top/bottom by monitoring price within the middle channel (yellow, blue, and orange lines), as well as identifying longer timeframe opportunities to buy/sell by examining the upper (green) and lower (red) bands. Disclaimer: this is not a guarantee that if price enters a region, that it will be a top or bottom, it is simply an indicator to get an idea based on price history.

As far as I know, this particular combination of exponential moving averages has not yet been published. I do not have an infinite amount of time to check through the entire library of published scripts. If someone else has already done this, I was unaware. Numerical computations were performed on ETHBTC price data in order to find the coefficients used in this script. Essentially, each EMA has a multiplier of either 1, a fraction of 1, or a number larger than 1 (these are the numbers in the script being multiplied by 'out1', 'out2', 'out3'; feel free to change these and see how this changes the indicator). I have found it to be useful for myself, and hope other people can tinker with this idea. My only wish is to allow other people to use this starting point to explore for themselves. I hope that I am allowed to publish this script without it being taken down so that others can freely use it.

Recommendations: although this was fit specifically for ETHBTC, it appears useful for many crypto pairs, specifically alt-BTC pairs and crypto-USD pairs. For example, I have found it useful for BTCUSD, ETHUSD, LINKUSD, LINKBTC, ETHBTC, ADABTC, etc. Only use on the DAILY timeframe.

TASC 2021.10 - MAD Moving Average DifferencePresented here is code for the "Moving Average Difference" indicator originally conceived by John Ehlers, also referred to as MAD. This is one of TradingView's first code releases published in the October 2021 issue of Trader's Tips by Technical Analysis of Stocks & Commodities (TASC) magazine.

This indicator has a companion indicator that is discussed in the article entitled Cycle/Trend Analytics And The MAD Indicator , authored by John Ehlers. He's providing an innovative double dose of indicator code for the month of October 2021.

John Ehlers generally describes it as a "thinking man's" MACD . MAD has similar, yet distinct, intended operation. For those of you familiar with the MACD indicator operation, you will find MACD adjustments having defaults of 12 and 26, while MAD has comparable adjustments with defaults of 8 and 23. These are intended for adjustment, same as any other oscillator.

The MAD indicator can be basically described as two simple moving averages applied within a "rate of change" (ROC) calculation.

Further Related Information

• SMA

• ROC

Join TradingView!

TASC 2021.10 - Cycle/Trend AnalyticsPresented here is code for the "Cycle/Trend Analytics" indicator originally conceived by John Ehlers. This is another one of TradingView's first code releases published in the October 2021 issue of Trader's Tips by Technical Analysis of Stocks & Commodities (TASC) magazine.

This indicator, referred to as "CTA" in later explanations, has a companion indicator that is discussed in the article entitled MAD Moving Average Difference , authored by John Ehlers. He's providing an innovative double dose of indicator code for the month of October 2021.

Modes of Operation

CTA has two modes defined as "trend" and "cycle". Ehlers' intention from what can be gathered from the article is to portray "the strength of the trend" in trend mode on real data. Cycle mode exhibits the response of the bank of calculations when a hypothetical sine wave is utilized as price. When cycle mode is chosen, two other lines will be displayed that are not shown in trend mode. A more detailed explanation of the indicator's technical functionality and intention can be found in the original Cycle/Trend Analytics And The MAD Indicator article, which requires a subscription.

Computational Functionality

The CTA indicator only has one adjustment in the indicator "Settings" for choice of modes. The default mode of operation is "trend". Trend mode applies raw price data to the bank of plots, while the cycle mode employs a sinusoidal oscillator set to a cycle period of 30 bars. These are passed to multiple SMAs, which are then subtracted from the original source data. The result is a fascinating display of plots embellished with vivid array of gradient color on real data or the hypothetical sine wave.

Related Information

• SMA

• color.rgb()

Join TradingView

[blackcat] L1 Trend Detection Index (TDI)Level: 1

Background

The trend detection index (TDI), which can be used to help detect when a trend has begun and when it has come to an end.

Function

The Trend Detection Index (TDI) is used to identify when a trend has started and when it ends. The TDI can be used as a stand-alone indicator or combined with others; It will work well when it comes to spotting the beginning of trends. However, this does not mean that its signals are absolutely accurate.

Inputs

Price --> Price source as input.

Length --> Length input can be adjusted to tune TDI performance.

Key Signal

MktPos --> 1 for long and -1 for short

Remarks

This is a Level 1 free but closed source indicator.

Feedbacks are appreciated.

Multi ZZ - Support/ResistenceExperimental and probably can be improved further.

Method of deriving support/resistence is as follows:

Calculate Zigzags and start pushing them to SR array as and when they form

If any of the existing item is within the small distance - merge them. ATR is used to find if the prices are close by.

Whenever we merge two pivots, strength of support keeps increasing. This means, price has bounced off this point more time. Hence, keep track of number of pivots merged together.

Keep removing old pivots which are far away based on Loopback input

And that's all we got the full list of support and resistence points.

Now, to filter insignificant pivots, chose only those points which has been merged by more than Min Pivots input. Width of the support/resistence lines also will be thicker for the pivots which has more count. Hence thicker line imply strong support and resistence whereas the thinner ones are minor ones.

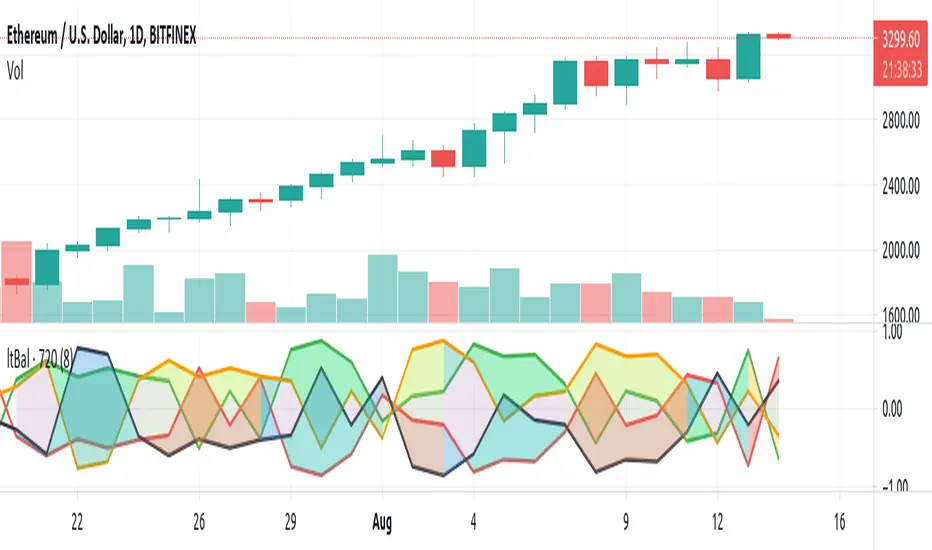

Light BalanceThe script is simple, going for a color scheme logic which tenderly avoids rigorous signals processing.

For the script to remain simple, logical derivatives are also out; as such, there are no secondary relations built off of primary ones. And it also ignores (unless you do this yourself) the logic in a varying order of lines.

Coloring has been done according to a limited set of relations between the four (4) plotted lines.

Quite a bit of information is capture, as you'll see when looking at line order, crossings, and transparency transitions and their patterns.

The approach makes the relations ones which can be learned over time; you become the algorithm to sort out signals. Ha ha. I know that sounds like a cop out doesn't it. Did I mention it's a simple script?

One thing you might want to play with right away are fills having red and green, and lime and fuchsia. It would be cool to reduce it all down to two (2) colors, but all the boolean relations might have to be listed, and it also may not be possible to cumulatively combine transparency overlays of the same value. Visually, that approach may not result to awaken a useful feature anyway. Also, fill() has its limitations in that it cannot be in a local scope; this includes function wrapped calls to fill(), or calls made using branching logic statements if/elseif, iff(), and var = (cond) ? t_val/exp : f_val/exp. So, to my knowledge, a fill() can not be made to be logically on/off.

Please, enjoy getting some use out of it.