RVWAP ENHANCED**Rolling VWAP with Alerts and Markers**

This Pine Script indicator enhances the traditional Rolling VWAP (Relative Volume Weighted Average Price) by adding dynamic features for improved visualization and alerting.

### Features:

1. **Dynamic VWAP Line Coloring**:

- The VWAP line changes color based on the relationship with the closing price:

- **Green** when the price is above the VWAP.

- **Red** when the price is below the VWAP.

2. **Candle and Background Coloring**:

- **Candles**: Colored green if the close is above the VWAP and red if below.

- **Background**: Subtle green or red shading indicates the price’s position relative to the VWAP.

3. **Alerts**:

- Alerts notify users when the VWAP changes direction:

- "VWAP Turned Green" for price crossing above the VWAP.

- "VWAP Turned Red" for price crossing below the VWAP.

4. **Small Dot Markers**:

- Tiny dots are plotted below the candles to mark VWAP state changes:

- **Green dot** for VWAP turning green.

- **Red dot** for VWAP turning red.

5. **Custom Time Period**:

- Users can select either a dynamic time period based on the chart's timeframe or a fixed time period (customizable in days, hours, and minutes).

6. **Standard Deviation Bands (Optional)**:

- Standard deviation bands around the VWAP can be enabled for further analysis.

This script is designed to provide clear and actionable insights into market trends using the RVWAP, making it an excellent tool for traders who rely on volume-based price action analysis.

חפש סקריפטים עבור "vwap"

MA Study: Different Types and More [NeoButane]A study of moving averages that utilizes different tricks I've learned to optimize them. Included is Bollinger Bands, Guppy (GMMA) and Super Guppy.

The method used to make it MtF should be more precise and smoother than regular MtF methods that use the security function. For intraday timeframes, each number represents each hour, with 24 equal to 1 day. For daily, 3 is 3 day, for weekly, 4 is the 4 weekly, etc. If you're on a higher timeframe than the one selected, the length will not change.

Log-space is used to make calculations work on many cryptos. The rules for color changing Guppy is changed to make it not as choppy on MAs other than EMA. Note that length does not affect SWMA and VWAP and source does not affect VWAP.

A short summary of each moving average can be found here: medium.com

List of included MAs:

ALMA: Arnaud Legoux

Double EMA

EMA: Exponential

Hull MA

KAMA: Kaufman Adaptive

Linear Regression Curve

LSMA: Least Squares

SMA: Simple

SMMA/RMA: Smoothed/Running

SWMA: Symm. Weighted

TMA: Triangular

Triple EMA

VWMA: Volume Weighted

WMA: Weighted

ZLEMA: Zero Lag

VWAP: Vol Weighted Average

Welles Wilder MA

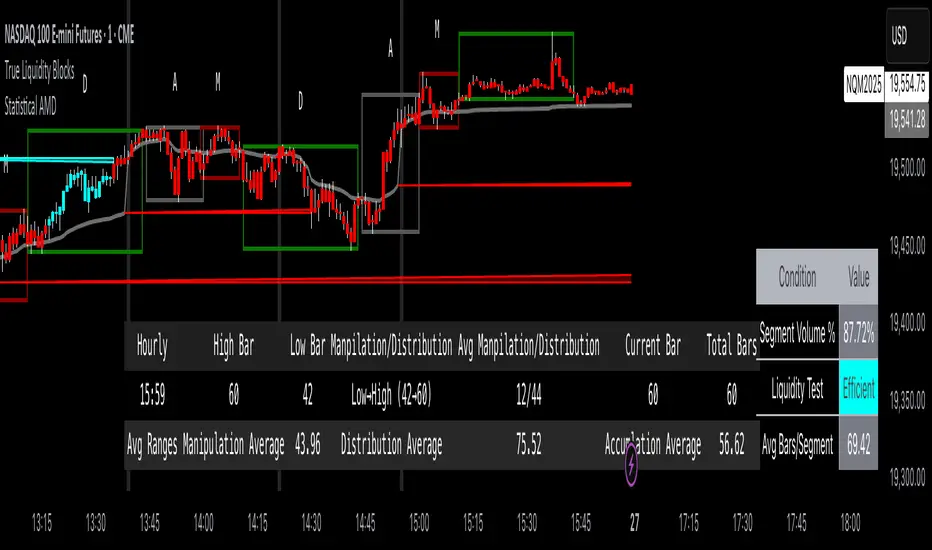

True Liquidity BlocksSo basically I've been deep diving into liquidity trading concepts similar to ICT (Inner Circle Trader) and developed an indicator that breaks down market movement through a volume-centric lens.

Key Concept:

Markets move not just by price, but by resolving trapped positions

Volume segments, not time intervals, show true market dynamics

VWAP (Volume Weighted Average Price) becomes a key structural reference

What Makes This Different:

Tracks volume segments instead of fixed time frames

Identifies "trapped" trader positions

Measures liquidity level efficiency

Color-codes bars based on nearest liquidity zone

Indicator Features:

Cyan/Red liquidity levels showing buy/sell pressure

Efficiency tracking for each level

Dynamic volume-based segmentation

Bar coloring to show nearest liquidity zone

Theoretical Inspiration: Viewed markets as energy systems where:

Positions create potential energy

Price movement resolves this energy

Trends form through systematic position liquidation

VWAP Recalculation in Each Segment:

Segment Start:

VWAP resets when volume threshold User Inputtable (600,000) is reached

Uses the last 4 price values (High, Low, Close, Close) for calculation

Weighted by volume traded during that segment

Calculation Method:

pineCopy = ta.vwap(hlcc4, na(segment_start) ? true : na, 1)

hlcc4: Combines high, low, close prices

na(segment_start): Ensures reset at new segment

Weighted by volume, not equal time intervals

Key Points:

Dynamic recalculation each segment

Reflects most recent trading activity

Provides real-time fair price reference

Tracks positioning

Essentially, VWAP resets and recalculates with each new volume segment, creating a rolling, volume-weighted average price that maps trader positioning.

BSL (Buy Side Liquidity) and SSL (Sell Side Liquidity) Explained:

When a volume segment closes relative to VWAP, it creates natural positioning traps:

BSL (Cyan) - Created when price closes BELOW THAT SEGMENT'S VWAP:

Bulls are positioned BELOW VWAP (trapped)

Shorts are positioned ABOVE VWAP (In Profit)

SSL (Red) - Created when price closes ABOVE THAT SEGMENT"S VWAP:

Bulls are positioned ABOVE VWAP (trapped)

Shorts are positioned BELOW VWAP (trapped)

Core Mechanism:

VWAP acts as a reference point for trader positioning

Trapped positions create inherent market tension

Levels expand to show accumulating pressure

Color-coded for quick identification of potential move direction

The goal: Visualize where traders are likely "stuck" and must eventually resolve their positions or liquidate other's, driving market movement.

It was just a fun experiment but If ya'll have any thoughts on it or what I could do to improve it, I would appreciate it.

Just a little note, It's optimized for futures, but if u uncheck the "Rest at Futures Open ?" setting, it allow full reign of any asset with volume data.

AI Trend Navigator [K-Neighbor]█ Overview

In the evolving landscape of trading and investment, the demand for sophisticated and reliable tools is ever-growing. The AI Trend Navigator is an indicator designed to meet this demand, providing valuable insights into market trends and potential future price movements. The AI Trend Navigator indicator is designed to predict market trends using the k-Nearest Neighbors (KNN) classifier.

By intelligently analyzing recent price actions and emphasizing similar values, it helps traders to navigate complex market conditions with confidence. It provides an advanced way to analyze trends, offering potentially more accurate predictions compared to simpler trend-following methods.

█ Calculations

KNN Moving Average Calculation: The core of the algorithm is a KNN Moving Average that computes the mean of the 'k' closest values to a target within a specified window size. It does this by iterating through the window, calculating the absolute differences between the target and each value, and then finding the mean of the closest values. The target and value are selected based on user preferences (e.g., using the VWAP or Volatility as a target).

KNN Classifier Function: This function applies the k-nearest neighbor algorithm to classify the price action into positive, negative, or neutral trends. It looks at the nearest 'k' bars, calculates the Euclidean distance between them, and categorizes them based on the relative movement. It then returns the prediction based on the highest count of positive, negative, or neutral categories.

█ How to use

Traders can use this indicator to identify potential trend directions in different markets.

Spotting Trends: Traders can use the KNN Moving Average to identify the underlying trend of an asset. By focusing on the k closest values, this component of the indicator offers a clearer view of the trend direction, filtering out market noise.

Trend Confirmation: The KNN Classifier component can confirm existing trends by predicting the future price direction. By aligning predictions with current trends, traders can gain more confidence in their trading decisions.

█ Settings

PriceValue: This determines the type of price input used for distance calculation in the KNN algorithm.

hl2: Uses the average of the high and low prices.

VWAP: Uses the Volume Weighted Average Price.

VWAP: Uses the Volume Weighted Average Price.

Effect: Changing this input will modify the reference values used in the KNN classification, potentially altering the predictions.

TargetValue: This sets the target variable that the KNN classification will attempt to predict.

Price Action: Uses the moving average of the closing price.

VWAP: Uses the Volume Weighted Average Price.

Volatility: Uses the Average True Range (ATR).

Effect: Selecting different targets will affect what the KNN is trying to predict, altering the nature and intent of the predictions.

Number of Closest Values: Defines how many closest values will be considered when calculating the mean for the KNN Moving Average.

Effect: Increasing this value makes the algorithm consider more nearest neighbors, smoothing the indicator and potentially making it less reactive. Decreasing this value may make the indicator more sensitive but possibly more prone to noise.

Neighbors: This sets the number of neighbors that will be considered for the KNN Classifier part of the algorithm.

Effect: Adjusting the number of neighbors affects the sensitivity and smoothness of the KNN classifier.

Smoothing Period: Defines the smoothing period for the moving average used in the KNN classifier.

Effect: Increasing this value would make the KNN Moving Average smoother, potentially reducing noise. Decreasing it would make the indicator more reactive but possibly more prone to false signals.

█ What is K-Nearest Neighbors (K-NN) algorithm?

At its core, the K-NN algorithm recognizes patterns within market data and analyzes the relationships and similarities between data points. By considering the 'K' most similar instances (or neighbors) within a dataset, it predicts future price movements based on historical trends. The K-Nearest Neighbors (K-NN) algorithm is a type of instance-based or non-generalizing learning. While K-NN is considered a relatively simple machine-learning technique, it falls under the AI umbrella.

We can classify the K-Nearest Neighbors (K-NN) algorithm as a form of artificial intelligence (AI), and here's why:

Machine Learning Component: K-NN is a type of machine learning algorithm, and machine learning is a subset of AI. Machine learning is about building algorithms that allow computers to learn from and make predictions or decisions based on data. Since K-NN falls under this category, it is aligned with the principles of AI.

Instance-Based Learning: K-NN is an instance-based learning algorithm. This means that it makes decisions based on the entire training dataset rather than deriving a discriminative function from the dataset. It looks at the 'K' most similar instances (neighbors) when making a prediction, hence adapting to new information if the dataset changes. This adaptability is a hallmark of intelligent systems.

Pattern Recognition: The core of K-NN's functionality is recognizing patterns within data. It identifies relationships and similarities between data points, something akin to human pattern recognition, a key aspect of intelligence.

Classification and Regression: K-NN can be used for both classification and regression tasks, two fundamental problems in machine learning and AI. The indicator code is used for trend classification, a predictive task that aligns with the goals of AI.

Simplicity Doesn't Exclude AI: While K-NN is often considered a simpler algorithm compared to deep learning models, simplicity does not exclude something from being AI. Many AI systems are built on simple rules and can be combined or scaled to create complex behavior.

No Explicit Model Building: Unlike traditional statistical methods, K-NN does not build an explicit model during training. Instead, it waits until a prediction is required and then looks at the 'K' nearest neighbors from the training data to make that prediction. This lazy learning approach is another aspect of machine learning, part of the broader AI field.

-----------------

Disclaimer

The information contained in my Scripts/Indicators/Ideas/Algos/Systems does not constitute financial advice or a solicitation to buy or sell any securities of any type. I will not accept liability for any loss or damage, including without limitation any loss of profit, which may arise directly or indirectly from the use of or reliance on such information.

All investments involve risk, and the past performance of a security, industry, sector, market, financial product, trading strategy, backtest, or individual's trading does not guarantee future results or returns. Investors are fully responsible for any investment decisions they make. Such decisions should be based solely on an evaluation of their financial circumstances, investment objectives, risk tolerance, and liquidity needs.

My Scripts/Indicators/Ideas/Algos/Systems are only for educational purposes!

Daily AVWAPsDaily AVWAPs is designed for intraday and swing traders who track institutional volume benchmarks. Instead of a single "rolling" line that resets continuously, this indicator identifies the starting timestamp of the last 5 trading sessions and draws five distinct Anchored VWAPs from those exact moments.

This allows traders to see exactly where the average volume-weighted price stands for the current day (1D), yesterday (2D), and the three days prior (3D, 4D, 5D) simultaneously.

Key Features

Polyline Visualization: Unlike standard indicators that plot historical values for every bar (creating a messy "sawtooth" effect), this script uses Pine Script Polylines. It draws clean, static lines starting from the specific anchor point to the present price, mimicking the manual "Anchored VWAP" drawing tool.

Dynamic Session Detection: The script contains zero hardcoded dates. It automatically detects when a new trading day begins based on the chart data. It works seamlessly across all asset classes (Stocks, Crypto, Futures) and automatically adjusts for weekends, holidays, and irregular trading weeks without manual updates.

Unified Color Control: Input colors are synchronized. Changing a color in the settings menu updates both the chart line and the price scale label instantly.

Toggle Controls: Individual checkboxes allow you to toggle any specific VWAP (1D through 5D) on or off to keep your chart clean.

How to Use

Trend Strength: When the 1D, 2D, and 3D VWAPs are "fanning out" in alignment, the trend is strong.

Mean Reversion: In a sideways market, price often gravitates back to the 5-Day VWAP as a "value area."

Support & Resistance: Watch for price to respect the VWAP of a previous high-volume day (e.g., bouncing off the 3D VWAP during a pullback).

Settings

Source: Select the price data source (default is OHLC4) .

Colors & Toggles: Use the checkboxes to enable/disable specific lines. Customize the color for each specific day's AVWAP directly in the Inputs tab.

This indicator was adapted and repurposed from the original work by The_Last_Gentleman .

Technical Note: This indicator is optimized for intraday timeframes (1m, 5m, 15m, 1H). Because it uses polyline and array logic to scan specific session timestamps, it calculates exclusively on the most recent bar to maintain high performance.

Day Trader Trend & Triggers + Mini-Meter — v6**Day Trader Trend & Triggers — Intraday**

A fast, intraday trend and entry tool designed for **1m–15m charts**. It identifies **strong up/down trends** using:

* **MA ribbon:** EMA9 > EMA21 > EMA50 (or inverse) for directional bias.

* **Momentum:** RSI(50-line) and MACD histogram flips.

* **Volume & VWAP:** only confirms when volume expands above SMA(20) and price is above/below VWAP.

* **Higher-TF bias filter (optional):** e.g., align 1m/5m signals with the 15m trend.

When all align, the background highlights and the mini-meter shows UP/DOWN.

It also plots **entries**:

* **Pullbacks** to EMA21/EMA50 with a MACD re-cross,

* **Breakouts** of recent highs/lows on strong volume.

Built-in **alerts** for trend flips, pullbacks, and breakouts let you trade hands-off.

Best used on **5m for active day trades**, with 1m/3m for scalping and 15m for cleaner intraday swings.

Day Trader Trend & Triggers — v6**Day Trader Trend & Triggers — Intraday**

A fast, intraday trend and entry tool designed for **1m–15m charts**. It identifies **strong up/down trends** using:

* **MA ribbon:** EMA9 > EMA21 > EMA50 (or inverse) for directional bias.

* **Momentum:** RSI(50-line) and MACD histogram flips.

* **Volume & VWAP:** only confirms when volume expands above SMA(20) and price is above/below VWAP.

* **Higher-TF bias filter (optional):** e.g., align 1m/5m signals with the 15m trend.

When all align, the background highlights and the mini-meter shows UP/DOWN.

It also plots **entries**:

* **Pullbacks** to EMA21/EMA50 with a MACD re-cross,

* **Breakouts** of recent highs/lows on strong volume.

Built-in **alerts** for trend flips, pullbacks, and breakouts let you trade hands-off.

Best used on **5m for active day trades**, with 1m/3m for scalping and 15m for cleaner intraday swings.

Multiple (12) Strong Buy/Sell Signals + Momentum

Indicator Manual: "Multiple (12) Strong Buy/Sell Signals + Momentum"

This indicator is designed to identify strong buy and sell signals based on 12 configurable conditions, which include a variety of technical analysis methods such as trend-following indicators, pattern recognition, volume analysis, and momentum oscillators. It allows for customizable alerts and visual cues on the chart. The indicator helps traders spot potential entry and exit points by displaying buy and sell signals based on the selected conditions.

Key Observations:

• The script integrates multiple indicators and pattern recognition methods to provide comprehensive buy/sell signals.

• Trend-based indicators like EMAs and MACD are combined with pattern recognition (flags, triangles) and momentum-based signals (RSI, ADX, and volume analysis).

• User customization is a core feature, allowing adjustments to the conditions and thresholds for more tailored signals.

• The script is designed to be responsive to market conditions, with multiple conditions filtering out noise to generate reliable signals.

________________________________________

Key Features:

1. 12 Combined Buy/Sell Signal Conditions: This indicator incorporates a diverse set of conditions based on trend analysis, momentum, and price patterns.

2. Minimum Conditions Input: You can adjust the threshold of conditions that need to be met for the buy/sell signals to appear.

3. Alert Customization: Set alert thresholds for both buy and sell signals.

4. Dynamic Visualization: Buy and sell signals are shown as triangles on the chart, with momentum signals highlighted as circles.

________________________________________

Detailed Description of the 12 Conditions:

1. Exponential Moving Averages (EMA):

o Conditions: The indicator uses EMAs with periods 3, 8, and 13 for quick trend-following signals.

o Bullish Signal: EMA3 > EMA8 > EMA13 (Bullish stack).

o Bearish Signal: EMA3 < EMA8 < EMA13 (Bearish stack).

o Reversal Signal: The crossing over or under of these EMAs can signify trend reversals.

2. MACD (Moving Average Convergence Divergence):

o Fast MACD (2, 7, 3) is used to confirm trends quickly.

o Bullish Signal: When the MACD line crosses above the signal line.

o Bearish Signal: When the MACD line crosses below the signal line.

3. Donchian Channel:

o Tracks the highest high and lowest low over a given period (default 20).

o Breakout Signal: Price breaking above the upper band is bullish; breaking below the lower band is bearish.

4. VWAP (Volume-Weighted Average Price):

o Above VWAP: Bullish condition (price above VWAP).

o Below VWAP: Bearish condition (price below VWAP).

5. EMA Stacking & Reversal:

o Tracks the order of EMAs (3, 8, 13) to confirm strong trends and reversals.

o Bullish Reversal: EMA3 < EMA8 < EMA13 followed by a crossing to bullish.

o Bearish Reversal: EMA3 > EMA8 > EMA13 followed by a crossing to bearish.

6. Bull/Bear Flags:

o Bull Flag: Characterized by a strong price movement (flagpole) followed by a pullback and breakout.

o Bear Flag: Similar to Bull Flag but in the opposite direction.

7. Triangle Patterns (Ascending and Descending):

o Detects ascending and descending triangles using pivot highs and lows.

o Ascending Triangle: Higher lows and flat resistance.

o Descending Triangle: Lower highs and flat support.

8. Volume Sensitivity:

o Identifies price moves with significant volume increases.

o High Volume: When current volume is significantly above the moving average volume (set to 1.2x of the average).

9. Momentum Indicators:

o RSI (Relative Strength Index): Confirms overbought and oversold levels with thresholds set at 65 (overbought) and 35 (oversold).

o ADX (Average Directional Index): Confirms strong trends when ADX > 28.

o Momentum Up: Momentum is upward with strong volume and bullish RSI/ADX conditions.

o Momentum Down: Momentum is downward with strong volume and bearish RSI/ADX conditions.

10. Bollinger & Keltner Squeeze:

o Squeeze Condition: A contraction in both Bollinger Bands and Keltner Channels indicates low volatility, signaling a potential breakout.

o Squeeze Breakout: Price breaking above or below the squeeze bands.

11. 3 Consecutive Candles Condition:

o Bullish: Price rises for three consecutive candles with higher highs and lows.

o Bearish: Price falls for three consecutive candles with lower highs and lows.

12. Williams %R and Stochastic RSI:

o Williams %R: A momentum oscillator with signals when the line crosses certain levels.

o Stochastic RSI: Provides overbought/oversold levels with smoother signals.

o Combined Signals: You can choose whether to require both WPR and StochRSI to signal a buy/sell.

________________________________________

User Inputs (Inputs Tab):

1. Minimum Conditions for Buy/Sell:

o min_conditions: Number of conditions required to trigger a buy/sell signal on the chart (1 to 12).

o Alert_min_conditions: User-defined alert threshold (how many conditions must be met before an alert is triggered).

2. Donchian Channel Settings:

o Show Donchian: Toggle visibility of the Donchian channel.

o Donchian Length: The length of the Donchian Channel (default 20).

3. Bull/Bear Flag Settings:

o Bull Flag Flagpole Strength: ATR multiplier to define the strength of the flagpole.

o Bull Flag Pullback Length: Length of pullback for the bull flag pattern.

o Bull Flag EMA Length: EMA length used to confirm trend during bull flag pattern.

Similar settings exist for Bear Flag patterns.

4. Momentum Indicators:

o RSI Length: Period for calculating the RSI (default 9).

o RSI Overbought: Overbought threshold for the RSI (default 65).

o RSI Oversold: Oversold threshold for the RSI (default 35).

5. Bollinger/Keltner Squeeze Settings:

o Squeeze Width Threshold: The maximum width of the Bollinger and Keltner Bands for squeeze conditions.

6. Stochastic RSI Settings:

o Stochastic RSI Length: The period for calculating the Stochastic RSI.

7. WPR Settings:

o WPR Length: Period for calculating Williams %R (default 14).

________________________________________

User Inputs (Style Tab):

1. Signal Plotting:

o Control the display and colors of the buy/sell signals, momentum indicators, and pattern signals on the chart.

o Buy/Sell Signals: Can be customized with different colors and shapes (triangle up for buys, triangle down for sells).

o Momentum Signals: Custom circle placement for momentum-up or momentum-down signals.

2. Donchian Channel:

o Show Donchian: Toggle visibility of the Donchian upper, lower, and middle bands.

o Band Colors: Choose the color for each band (upper, lower, middle).

________________________________________

How to Use the Indicator:

1. Adjust Minimum Conditions: Set the minimum number of conditions that must be met for a signal to appear. For example, set it to 5 if you want only stronger signals.

2. Set Alert Threshold: Define the number of conditions needed to trigger an alert. This can be different from the minimum conditions for visual signals.

3. Customize Appearance: Modify the colors and styles of the signals to match your preferences.

________________________________________

Conclusion:

This comprehensive trading indicator uses a combination of trend-following, pattern recognition, and momentum-based conditions to help you spot potential buy and sell opportunities. By adjusting the input settings, you can fine-tune it to match your specific trading strategy, making it a versatile tool for different market conditions.

Signal Reliability Based on Condition Count

The reliability of the buy/sell signals increases as more conditions are met. Here's a breakdown of the probabilities:

1. 1-3 Conditions Met: Lower Probability

o Signals that meet only 1-3 conditions tend to have lower reliability and are considered less probable. These signals may represent false positives or weaker market movements, and traders should approach them with caution.

2. 4 Conditions Met: More Reliable Signal

o When 4 conditions are met, the signal becomes more reliable. This indicates that multiple indicators or market patterns are aligning, increasing the likelihood of a valid buy/sell opportunity. While not foolproof, it's a stronger indication that the market may be moving in a particular direction.

3. 5-6 Conditions Met: Strong Signal

o A signal meeting 5-6 conditions is considered a strong signal. This indicates a well-confirmed move, with several technical indicators and market factors aligning to suggest a higher probability of success. These are the signals that traders often prioritize.

4. 7+ Conditions Met: Rare and High-Confidence Signal

o Signals that meet 7 or more conditions are rare and should be considered high-confidence signals. These represent a significant alignment of multiple factors, and while they are less frequent, they are highly reliable when they do occur. Traders can be more confident in acting on these signals, but they should still monitor market conditions for confirmation.

________________________________________

You can adjust the number of conditions as needed, but this breakdown should give a clear structure on how the signal strength correlates with the number of conditions met!

Bull Bear Power With EMA FilterDescription of Indicator:

This Pine Script indicator colors price bars based on the open price in relation to custom moving averages (EMA/SMA), Bull/Bear Power (BBPower), and an optional VWAP filter. The bar colors help identify bullish and bearish conditions with added visual cues for price positioning relative to VWAP.

Key Features:

Customizable Moving Averages (EMA/SMA):

The user can select between EMA or SMA for both short-term and long-term moving averages.

Default moving averages are set to 5 (short-term) and 9 (long-term) but can be adjusted by the user.

Bullish Condition (Blue or Purple Bars):

A bar is colored blue if the following conditions are met:

The open price is above both the short-term and long-term moving averages.

The short-term moving average (MA 1) is above the long-term moving average (MA 2).

BBPower (open price minus the 13-period EMA) is positive, indicating bullish strength.

If the VWAP filter is enabled and the price opens below VWAP, the bullish bars will turn purple.

Bearish Condition (Yellow or Orange Bars):

A bar is colored yellow if the following conditions are met:

The open price is below both the short-term and long-term moving averages.

The short-term moving average (MA 1) is below the long-term moving average (MA 2).

BBPower is negative or zero, indicating bearish market conditions.

If the VWAP filter is enabled and the price opens above VWAP, the bearish bars will turn orange.

VWAP Filter (Optional):

An optional filter allows the user to add VWAP (Volume-Weighted Average Price) to the bar coloring logic.

When the VWAP filter is enabled, it provides additional information about price positioning relative to VWAP, turning bullish bars purple and bearish bars orange depending on whether the price opens above or below VWAP.

Usage:

Bullish Trend: Look for blue or purple bars to identify potential bullish momentum.

Bearish Trend: Look for yellow or orange bars to spot bearish conditions in the market.

The indicator allows users to customize the length and type of moving averages (EMA or SMA), as well as decide whether to apply the VWAP filter.

This indicator provides traders with clear visual signals to quickly assess the strength of bullish or bearish conditions based on the price's position relative to custom moving averages, BBPower, and VWAP, helping with trend identification and potential trade setups.

Depth of Market (DOM) [LuxAlgo]The Depth Of Market (DOM) tool allows traders to look under the hood of any market, taking price and volume analysis to the next level. The following features are included: DOM, Time & Sales, Volume Profile, Depth of Market, Imbalances, Buying Pressure, and up to 24 key intraday levels (it really packs a punch).

As a disclaimer, this tool does not use tick data, it is a DOM reconstruction from the provided real-time time series data (price and volume). So the volume you see is from filled orders only, this tool does not show unfilled limit orders.

Traders can enable or disable any of the features at will to avoid being overwhelmed with too much information and to make the tool perform faster.

The features that have the biggest impact on performance are Historical Data Collection, Key Levels (POC & VWAP), Time & Sales, Profile, and Imbalances. Disable these features to improve the indicator computational performance.

🔶 DOM

This is the simplest form of the tool, a simple DOM or ladder that displays the following columns:

PRICE: Price level

BID: Total number of market sell orders filled or limit buy orders filled.

SELL: Sell market orders

BUY: Buy market orders

ASK: Total number of market buy orders filled or limit sell orders filled.

The DOM only collects historical data from the last 24 hours and real-time data.

Traders can select a reset period for the DOM with two options:

DAILY: Resets at the beginning of each trading day

SESSIONS: Resets twice, as DAILY and 15.5 hours later, to coincide with the start of the RTH session for US tickers.

The DOM has two main modes, it can display price levels as ticks or points. The default is automatic based on the current daily volatility, but traders can manually force one mode or the other if they wish.

For convenience, traders have the option to set the number of lines (price levels), and the size of the text and to display only real-time data.

By default, the top price is set to 0 so that the DOM automatically adjusts the price levels to be displayed, but traders can set the top price manually so that the tool displays only the desired price levels in a fixed manner.

🔹 Volume Profile

As additional features to the basic DOM, traders have access to the volume profile histogram and the total volume per price level.

This helps traders identify at a glance key price areas where volume is accumulating (high volume nodes) or areas where volume is lacking (low volume nodes) - these areas are important to some traders who base their decision-making process on them.

🔹 Imbalances

Other added features are imbalances and buying pressure:

Interlevel Imbalance: volume delta between two different price levels

Intralevel Imbalance: delta between buy and sell volume at the same price level

Buying Pressure Percent: percentage of buy volume compared to total volume

Imbalances can help traders identify areas of interest in the price for possible support or resistance.

🔹 Depth

Depth allows traders to see at a glance how much supply is above the current price level or how much demand is below the current price level.

Above the current price level shows the cumulative ask volume (filled sell limit orders) and below the current price level shows the cumulative bid volume (filled buy limit orders).

🔶 KEY LEVELS

The tool includes up to 24 different key intraday levels of particular relevance:

Previous Week Levels

PWH: Previous week high

PWL: Previous week low

PWM: Previous week middle

PWS: Previous week settlement (close)

Previous Day Levels

PDH: Previous day high

PDL: Previous day low

PDM: Previous day middle

PDS: Previous day settlement (close)

Current Day Levels

OPEN: Open of day (or session)

HOD: High of day (or session)

LOD: Low of day (or session)

MOD: Middle of day (or session)

Opening Range

ORH: Open range high

ORL: Open range low

Initial Balance

IBH: Initial balance high

IBL: Initial balance low

VWAP

+3SD: Volume weighted average price plus 3 standard deviations

+2SD: Volume weighted average price plus 2 standard deviations

+1SD: Volume weighted average price plus 1 standard deviation

VWAP: Volume weighted average price

-1SD: Volume weighted average price minus 1 standard deviation

-2SD: Volume weighted average price minus 2 standard deviations

-3SD: Volume weighted average price minus 3 standard deviations

POC: Point of control

Different traders look at different levels, the key levels shown here are objective and specific areas of interest that traders can act on, providing us with potential areas of support or resistance in the price.

🔶 TIME & SALES

The tool also features a full-time and sales panel with time, price, and size columns, a size filter, and the ability to set the timezone to display time in the trader's local time.

The information shown here is what feeds the DOM and it can be useful in several ways, for example in detecting absorption. If a large number of orders are coming into the market but the price is barely moving, this indicates that there is enough liquidity at these levels to absorb all these orders, so if these orders stop coming into the market, the price may turn around.

🔶 SETTINGS

Period: Select the anchoring period to start data collection, DAILY will anchor at the start of the trading day, and SESSIONS will start as DAILY and 15.5 hours later (RTH for US tickers).

Mode: Select between AUTO and MANUAL modes for displaying TICKS or POINTS, in AUTO mode the tool will automatically select TICKS for tickers with a daily average volatility below 5000 ticks and POINTS for the rest of the tickers.

Rows: Select the number of price levels to display

Text Size: Select the text size

🔹 DOM

DOM: Enable/Disable DOM display

Realtime only: Enable/Disable real-time data only, historical data will be collected if disabled

Top Price: Specify the price to be displayed on the top row, set to 0 to enable dynamic DOM

Max updates: Specify how many times the values on the SELL and BUY columns are accumulated until reset.

Profile/Depth size: Maximum size of the histograms on the PROFILE and DEPTH columns.

Profile: Enable/Disable Profile column. High impact on performance.

Volume: Enable/Disable Volume column. Total volume traded at price level.

Interlevel Imbalance: Enable/Disable Interlevel Imbalance column. Total volume delta between the current price level and the price level above. High impact on performance.

Depth: Enable/Disable Depth, showing the cumulative supply above the current price and the cumulative demand below. Impact on performance.

Intralevel Imbalance: Enable/Disable Intralevel Imbalance column. Delta between total buy volume and total sell volume. High impact on performance.

Buying Pressure Percent: Enable/Disable Buy Percent column. Percentage of total buy volume compared to total volume.

Imbalance Threshold %: Threshold for highlighting imbalances. Set to 90 to highlight the top 10% of interlevel imbalances and the top and bottom 10% of intra-level imbalances.

Crypto volume precision: Specify the number of decimals to display on the volume of crypto assets

🔹 Key Levels

Key Levels: Enable/Disable KEY column. Very high performance impact.

Previous Week: Enable/Disable High, Low, Middle, and Close of the previous trading week.

Previous Day: Enable/Disable High, Low, Middle, and Settlement of the previous trading day.

Current Day/Session: Enable/Disable Open, High, Low and Middle of the current period.

Open Range: Enable/Disable High and Low of the first candle of the period.

Initial Balance: Enable/Disable High and Low of the first hour of the period.

VWAP: Enable/Disable Volume-weighted average price of the period with 1, 2, and 3 standard deviations.

POC: Enable/Disable Point of Control (price level with the highest volume traded) of the period.

🔹 Time & Sales

Time & Sales: Enable/Disable time and sales panel.

Timezone offset (hours): Enter your time zone\'s offset (+ or −), including a decimal fraction if needed.

Order Size: Set order size filter. Orders smaller than the value are not displayed.

🔶 THANKS

Hi, I'm makit0 coder of this tool and proud member of the LuxAlgo Opensource team, it's an honor to be part of the LuxAlgo family doing something I love as it's writing opensource code and sharing it with the world. I'd like to thank all of you who use, comment on, and vote for all of our open-source tools, and all of you who give us your support.

And of course thanks to the PineCoders family for all the work in front of and behind the scenes that makes the PineScript community what it is, simply the best.

Peace, Love & PineScript!

Overnight Bias: Net Long/Short with PercentOvernight bias can assist with NY session gap fades or gap and go trading once the NY session is open.

Some general gap rules are:

1. Gap Direction Aligned with Overnight Bias

Rule: If the NY session gaps up and the overnight bias is Net Long (e.g., >60% of bars above the overnight open), favor longs.

Confirmation: Look for price to hold above overnight open or VWAP.

Invalidation: If price re-enters the overnight range, reassess.

2. Gap Opposing Overnight Bias (Contrarian Setup)

Rule: If the NY opens opposite the overnight bias, expect potential gap fill or reversal.

Trade Bias: Look for retracement back toward the overnight open or VWAP.

Example: Overnight was Net Long, but NY gaps down → wait for reclaim of VWAP to go long, else fade strength.

3. Gap Into Prior Day Value Area (VAH to VAL)

Rule: If the NY session gaps into the prior day value area:

It implies mean reversion behavior.

Expect price to rotate toward the POC (point of control).

Trade Bias: Fade toward POC if overnight bias is balanced or opposite the gap direction.

4. Gap Outside Prior Day Value Area

Rule: A gap above VAH or below VAL suggests potential breakout or new trend day.

Trade Bias: If overnight bias aligns (e.g., gap above VAH + Net Long overnight), consider trend continuation.

Invalidation: If price breaks back inside the prior day value area, watch for failed breakout → fade trade possible.

5. Gap Above Prior Day High / Below Prior Day Low

Rule: This is a true breakout gap.

Above Prior High + Net Long Bias: Look for continuation.

Below Prior Low + Net Short Bias: Look for sell pressure continuation.

Trade Bias: Use pullbacks to the prior high/low or overnight open for continuation setups.

6. Gap Within Prior Day Range

Rule: If the NY open is within the prior day’s high and low, expect chop or balanced conditions.

Trade Bias: Use overnight VWAP and prior POC as decision zones. Be cautious unless a breakout occurs.

7. Failed Gap and Re-entry into Prior Day Range

Rule: If price gaps above prior high but re-enters the prior range, it's a failed breakout.

Trade Bias: Look for a fade back to VAH or POC.

Confirmation: Watch for breakdown below overnight VWAP or failure to hold overnight open.

8. Gap + Overnight VWAP Divergence

Rule: If price gaps opposite the direction of VWAP (e.g., VWAP rising, gap down), wait for confirmation.

Trade Bias: Be cautious with early trades. Bias may flip if VWAP is reclaimed.

9. Gap + Overnight Open Test

Rule: If price opens with a gap and then retests the overnight open, that level becomes a decision zone.

Trade Bias:

Hold above = trend continuation.

Rejection = gap fill or reversal.

10. Unfilled Gap = Trend Bias

Rule: If the gap remains unfilled for the first 30–60 minutes, it increases the odds of a trend day.

Trade Bias: Trade pullbacks in the direction of the gap and overnight bias.

Should anyone have suggestion to add please do so.

Constance Brown RSI with Composite IndexConstance Brown RSI with Composite Index

Overview

This indicator combines Constance Brown's RSI interpretation methodology with a Composite Index and ATR Distance to VWAP measurement to provide a comprehensive trading tool. It helps identify trends, momentum shifts, overbought/oversold conditions, and potential reversal points.

Key Features

Color-coded RSI zones for immediate trend identification

Composite Index for momentum analysis and divergence detection

ATR Distance to VWAP for identifying extreme price deviations

Automatic divergence detection for early reversal warnings

Pre-configured alerts for key trading signals

How to Use This Indicator

Trend Identification

The RSI line changes color based on its position:

Blue zone (RSI > 50): Bullish trend - look for buying opportunities

Purple zone (RSI < 50): Bearish trend - look for selling opportunities

Gray zone (RSI 40-60): Neutral/transitional market - prepare for potential breakout

The 40-50 area (light blue fill) acts as support during uptrends, while the 50-60 area (light purple fill) acts as resistance during downtrends.

// From the code:

upTrendZone = rsiValue > 50 and rsiValue <= 90

downTrendZone = rsiValue < 50 and rsiValue >= 10

neutralZone = rsiValue > 40 and rsiValue < 60

rsiColor = neutralZone ? neutralRSI : upTrendZone ? upTrendRSI : downTrendRSI

Momentum Analysis

The Composite Index (fuchsia line) provides momentum confirmation:

Values above 50 indicate positive momentum

Values below 40 indicate negative momentum

Crossing above/below these thresholds signals potential momentum shifts

// From the code:

compositeIndexRaw = rsiChange / ta.stdev(rsiValue, rsiLength)

compositeIndex = ta.sma(compositeIndexRaw, compositeSmoothing)

compositeScaled = compositeIndex * 10 + 50 // Scaled to fit 0-100 range

Overbought/Oversold Detection

The ATR Distance to VWAP table in the top-right corner shows how far price has moved from VWAP in terms of ATR units:

Extreme positive values (orange/red): Potentially overbought

Extreme negative values (purple/red): Potentially oversold

Near zero (gray): Price near average value

// From the code:

priceDistance = (close - vwapValue) / ta.atr(atrPeriod)

// Color coding based on distance value

Divergence Trading

The indicator automatically detects divergences between the Composite Index and price:

Bullish divergence: Price makes lower low but Composite Index makes higher low

Bearish divergence: Price makes higher high but Composite Index makes lower high

// From the code:

divergenceBullish = ta.lowest(compositeIndex, rsiLength) > ta.lowest(close, rsiLength)

divergenceBearish = ta.highest(compositeIndex, rsiLength) < ta.highest(close, rsiLength)

Trading Strategies

Trend Following

1. Identify the trend using RSI color:

Blue = Uptrend, Purple = Downtrend

2. Wait for pullbacks to support/resistance zones:

In uptrends: Buy when RSI pulls back to 40-50 zone and bounces

In downtrends: Sell when RSI rallies to 50-60 zone and rejects

3. Confirm with Composite Index:

Uptrends: Composite Index stays above 50 or quickly returns above it

Downtrends: Composite Index stays below 50 or quickly returns below it

4. Manage risk using ATR Distance:

Take profits when ATR Distance reaches extreme values

Place stops beyond recent swing points

Reversal Trading

1. Look for divergences

Bullish: Price makes lower low but Composite Index makes higher low

Bearish: Price makes higher high but Composite Index makes lower high

2. Confirm with ATR Distance:

Extreme readings suggest potential reversals

3. Wait for RSI zone transition:

Bullish: RSI crosses above 40 (purple to neutral/blue)

Bearish: RSI crosses below 60 (blue to neutral/purple)

4. Enter after confirmation:

Use candlestick patterns for precise entry

Place stops beyond the divergence point

Four pre-configured alerts are available:

Momentum High: Composite Index above 50

Momentum Low: Composite Index below 40

Bullish Divergence: Composite Index higher low

Bearish Divergence: Composite Index lower high

Customization

Adjust these parameters to optimize for your trading style:

RSI Length: Default 14, lower for more sensitivity, higher for fewer signals

Composite Index Smoothing: Default 10, lower for quicker signals, higher for less noise

ATR Period: Default 14, affects the ATR Distance to VWAP calculation

This indicator works well across various markets and timeframes, though the default settings are optimized for daily charts. Adjust parameters for shorter or longer timeframes as needed.

Happy trading!

Levels Of Interest------------------------------------------------------------------------------------

LEVELS OF INTEREST (LOI)

TRADING INDICATOR GUIDE

------------------------------------------------------------------------------------

Table of Contents:

1. Indicator Overview & Core Functionality

2. VWAP Foundation & Historical Context

3. Multi-Timeframe VWAP Analysis

4. Moving Average Integration System

5. Trend Direction Signal Detection

6. Visual Design & Display Features

7. Custom Level Integration

8. Repaint Protection Technology

9. Practical Trading Applications

10. Setup & Configuration Recommendations

------------------------------------------------------------------------------------

1. INDICATOR OVERVIEW & CORE FUNCTIONALITY

------------------------------------------------------------------------------------

The LOI indicator combines multiple VWAP calculations with moving averages across different timeframes. It's designed to show where institutional money is flowing and help identify key support and resistance levels that actually matter in today's markets.

Primary Functions:

- Multi-timeframe VWAP analysis (Daily, Weekly, Monthly, Yearly)

- Advanced moving average integration (EMA, SMA, HMA)

- Real-time trend direction detection

- Institutional flow analysis

- Dynamic support/resistance identification

Target Users: Day traders, swing traders, position traders, and institutional analysts seeking comprehensive market structure analysis.

------------------------------------------------------------------------------------

2. VWAP FOUNDATION & HISTORICAL CONTEXT

------------------------------------------------------------------------------------

Historical Development: VWAP started in the 1980s when big institutional traders needed a way to measure if they were getting good fills on their massive orders. Unlike regular price averages, VWAP weighs each price by the volume traded at that level. This makes it incredibly useful because it shows you where most of the real money changed hands.

Mathematical Foundation: The basic math is simple: you take each price, multiply it by the volume at that price, add them all up, then divide by total volume. What you get is the true "average" price that reflects actual trading activity, not just random price movements.

Formula: VWAP = Σ(Price × Volume) / Σ(Volume)

Where typical price = (High + Low + Close) / 3

Institutional Behavior Patterns:

- When price trades above VWAP, institutions often look to sell

- When it's below, they're usually buying

- Creates natural support and resistance that you can actually trade against

- Serves as benchmark for execution quality assessment

------------------------------------------------------------------------------------

3. MULTI-TIMEFRAME VWAP ANALYSIS

------------------------------------------------------------------------------------

Core Innovation: Here's where LOI gets interesting. Instead of just showing daily VWAP like most indicators, it displays four different timeframes simultaneously:

**Daily VWAP Implementation**:

- Resets every morning at market open

- Provides clearest picture of intraday institutional sentiment

- Primary tool for day trading strategies

- Most responsive to immediate market conditions

**Weekly VWAP System**:

- Resets each Monday (or first trading day)

- Smooths out daily noise and volatility

- Perfect for swing trades lasting several days to weeks

- Captures weekly institutional positioning

**Monthly VWAP Analysis**:

- Resets at beginning of each calendar month

- Captures bigger institutional rebalancing at month-end

- Fund managers often operate on monthly mandates

- Significant weight in intermediate-term analysis

**Yearly VWAP Perspective**:

- Resets annually for full-year institutional view

- Shows long-term institutional positioning

- Where pension funds and sovereign wealth funds operate

- Critical for major trend identification

Confluence Zone Theory: The magic happens when multiple VWAP levels cluster together. These confluence zones often become major turning points because different types of institutional money all see value at the same price.

------------------------------------------------------------------------------------

4. MOVING AVERAGE INTEGRATION SYSTEM

------------------------------------------------------------------------------------

Multi-Type Implementation: The indicator includes three types of moving averages, each with its own personality and application:

**Exponential Moving Averages (EMAs)**:

- React quickly to recent price changes

- Displayed as solid lines for easy identification

- Optimal performance in trending market conditions

- Higher sensitivity to current price action

**Simple Moving Averages (SMAs)**:

- Treat all historical data points equally

- Appear as dashed lines in visual display

- Slower response but more reliable in choppy conditions

- Traditional approach favored by institutional traders

**Hull Moving Averages (HMAs)**:

- Newest addition to the system (dotted line display)

- Created by Alan Hull in 2005

- Solves classic moving average dilemma: speed vs. accuracy

- Manages to be both responsive and smooth simultaneously

Technical Innovation: Alan Hull's solution addresses the fundamental problem where moving averages are either too slow (missing moves) or too fast (generating false signals). HMAs achieve optimal balance through weighted calculation methodology.

Period Configuration:

- 5-period: Short-term momentum assessment

- 50-period: Intermediate trend identification

- 200-period: Long-term directional confirmation

------------------------------------------------------------------------------------

5. TREND DIRECTION SIGNAL DETECTION

------------------------------------------------------------------------------------

Real-Time Momentum Analysis: One of LOI's best features is its real-time trend detection system. Next to each moving average, visual symbols provide immediate trend assessment:

Symbol System:

- ▲ Rising average (bullish momentum confirmation)

- ▼ Falling average (bearish momentum indication)

- ► Flat average (consolidation or indecision period)

Update Frequency: These signals update in real-time with each new price tick and function across all configured timeframes. Traders can quickly scan daily and weekly trends to assess alignment or conflicting signals.

Multi-Timeframe Trend Analysis:

- Simultaneous daily and weekly trend comparison

- Immediate identification of trend alignment

- Early warning system for potential reversals

- Momentum confirmation for entry decisions

------------------------------------------------------------------------------------

6. VISUAL DESIGN & DISPLAY FEATURES

------------------------------------------------------------------------------------

Color Psychology Framework: The color scheme isn't random but based on psychological associations and trading conventions:

- **Blue Tones**: Institutional neutrality (VWAP levels)

- **Green Spectrum**: Growth and stability (weekly timeframes)

- **Purple Range**: Longer-term sophistication (monthly analysis)

- **Orange Hues**: Importance and attention (yearly perspective)

- **Red Tones**: User-defined significance (custom levels)

Adaptive Display Technology: The indicator automatically adjusts decimal places based on the instrument you're trading. High-priced stocks show 2 decimals, while penny stocks might show 8. This keeps the display incredibly clean regardless of what you're analyzing - no cluttered charts or overwhelming information overload.

Smart Labeling System: Advanced positioning algorithm automatically spaces all elements to prevent overlap, even during extreme zoom levels or multiple timeframe analysis. Every level stays clearly readable without any visual chaos disrupting your analysis.

------------------------------------------------------------------------------------

7. CUSTOM LEVEL INTEGRATION

------------------------------------------------------------------------------------

User-Defined Level System: Beyond the calculated VWAP and moving average levels, traders can add custom horizontal lines at any price point for personalized analysis.

Strategic Applications:

- **Psychological Levels**: Round numbers, previous significant highs/lows

- **Technical Levels**: Fibonacci retracements, pivot points

- **Fundamental Targets**: Analyst price targets, earnings estimates

- **Risk Management**: Stop-loss and take-profit zones

Integration Features:

- Seamless incorporation with smart labeling system

- Custom color selection for visual organization

- Extension capabilities across all chart timeframes

- Maintains display clarity with existing indicators

------------------------------------------------------------------------------------

8. REPAINT PROTECTION TECHNOLOGY

------------------------------------------------------------------------------------

Critical Trading Feature: This addresses one of the most significant issues in live trading applications. Most multi-timeframe indicators "repaint," meaning they display different signals when viewing historical data versus real-time analysis.

Protection Benefits:

- Ensures every displayed signal could have been traded when it appeared

- Eliminates discrepancies between historical and live analysis

- Provides realistic performance expectations

- Maintains signal integrity across chart refreshes

Configuration Options:

- **Protection Enabled**: Default setting for live trading

- **Protection Disabled**: Available for backtesting analysis

- User-selectable toggle based on analysis requirements

- Applies to all multi-timeframe calculations

Implementation Note: With protection enabled, signals may appear one bar later than without protection, but this ensures all signals represent actionable opportunities that could have been executed in real-time market conditions.

------------------------------------------------------------------------------------

9. PRACTICAL TRADING APPLICATIONS

------------------------------------------------------------------------------------

**Day Trading Strategy**:

Focus on daily VWAP with 5-period moving averages. Look for bounces off VWAP or breaks through it with volume. Short-term momentum signals provide entry and exit timing.

**Swing Trading Approach**:

Weekly VWAP becomes your primary anchor point, with 50-period averages showing intermediate trends. Position sizing based on weekly VWAP distance.

**Position Trading Method**:

Monthly and yearly VWAP provide broad market context, while 200-period averages confirm long-term directional bias. Suitable for multi-week to multi-month holdings.

**Multi-Timeframe Confluence Strategy**:

The highest-probability setups occur when daily, weekly, and monthly VWAPs cluster together, especially when multiple moving averages confirm the same direction. These represent institutional consensus zones.

Risk Management Integration:

- VWAP levels serve as dynamic stop-loss references

- Multiple timeframe confirmation reduces false signals

- Institutional flow analysis improves position sizing decisions

- Trend direction signals optimize entry and exit timing

------------------------------------------------------------------------------------

10. SETUP & CONFIGURATION RECOMMENDATIONS

------------------------------------------------------------------------------------

Initial Configuration: Start with default settings and adjust based on individual trading style and market focus. Short-term traders should emphasize daily and weekly timeframes, while longer-term investors benefit from monthly and yearly level analysis.

Transparency Optimization: The transparency settings allow clear price action visibility while maintaining level reference points. Most traders find 70-80% transparency optimal - it provides a clean, unobstructed view of price movement while maintaining all critical reference levels needed for analysis.

Integration Strategy: Remember that no indicator functions effectively in isolation. LOI provides excellent context for institutional flow and trend direction analysis, but should be combined with complementary analysis tools for optimal results.

Performance Considerations:

- Multiple timeframe calculations may impact chart loading speed

- Adjust displayed timeframes based on trading frequency

- Customize color schemes for different market sessions

- Regular review and adjustment of custom levels

------------------------------------------------------------------------------------

FINAL ANALYSIS

------------------------------------------------------------------------------------

Competitive Advantage: What makes LOI different is its focus on where real money actually trades. By combining volume-weighted calculations with multiple timeframes and trend detection, it cuts through market noise to show you what institutions are really doing.

Key Success Factor: Understanding that different timeframes serve different purposes is essential. Use them together to build a complete picture of market structure, then execute trades accordingly.

The integration of institutional flow analysis with technical trend detection creates a comprehensive trading tool that addresses both short-term tactical decisions and longer-term strategic positioning.

------------------------------------------------------------------------------------

END OF DOCUMENTATION

------------------------------------------------------------------------------------

Ind-Suite: The Ultimate Strategic Dashboard [Gap/Dow/MA/SR]概要 Ind-Suiteは、トレードに必要な4つの重要な要素(窓、市場構造、移動平均線、水平線)を1つのインジケーターに統合した包括的なトレーディング・スイートです。 このツールの目的は、単一のサインに頼るのではなく、複数の根拠が重なる「コンフルエンス(Confluence)」を視覚的に発見することにあります。

機能モジュール 設定画面の「⚡ MODULE TOGGLES ⚡」から、各モジュールのON/OFFを瞬時に切り替えられます。

Module A: Gaps (窓)

未埋めの窓(Gap)をボックスで表示します。

価格が引き寄せられるターゲットとして機能します。一定期間経過した窓は自動的に非表示になります。

Module B: Dow Structure (ダウ理論と構造)

ZigZagラインによる波の描画と、トレンド状態の判定。

BOS (Break of Structure): トレンド継続のブレイクポイントにラベルを表示。

下落トレンド時は背景色が変化し、視覚的にトレンドを把握できます。

Module C: Safe Scaffold (足場と勢い)

EMA (9/20) & VWAP: トレンドフォローのための主要な移動平均線。

Bollinger Bands: ボラティリティの確認用(ON/OFF可能)。

Signal: EMAクロスとバンド幅拡大(スクイーズからのエクスパンション)を検知したロングサインを表示。

Module D: S/R Guardian (水平線)

過去のPivot点をベースに、意識されやすいサポート・レジスタンスラインを自動描画します。

強度に基づいてラインが統合され、重要度が高い価格帯を可視化します。

推奨される使い方 すべてのモジュールを常にONにする必要はありません。チャートが情報過多にならないよう、必要な機能だけを選択して表示してください。 例えば、「S/Rライン」での反発、「Dow Structure」でのBOS、「Gap」の埋め完了など、3つ以上の根拠が重なるポイントは、優位性の高いエントリーポイントとなります。

--------------

Overview Ind-Suite is a comprehensive trading suite that integrates four essential elements (Gaps, Market Structure, Moving Averages, and Support/Resistance) into a single indicator. The goal of this tool is not to rely on a single signal, but to visually identify "Confluence" where multiple factors align.

Feature Modules You can instantly toggle each module ON/OFF via the "⚡ MODULE TOGGLES ⚡" in the settings.

Module A: Gaps

Highlights unclosed gaps with boxes.

These act as price magnets/targets. Old gaps are automatically hidden after a set period.

Module B: Dow Structure (Trend & Market Structure)

Draws ZigZag waves and determines trend status based on pivot points.

BOS (Break of Structure): Labels are displayed at key breakout points confirming trend continuation.

Background color changes during downtrends for instant visual recognition.

Module C: Safe Scaffold (Momentum & MAs)

EMA (9/20) & VWAP: Key moving averages for trend following.

Bollinger Bands: For volatility analysis (Toggle available).

Signal: Displays Long signals upon EMA crossover combined with BBW expansion (volatility breakout).

Module D: S/R Guardian (Support & Resistance)

Automatically draws S/R zones based on historical pivot points.

Levels are merged based on proximity, visualizing significant price zones.

Recommended Usage It is not necessary to keep all modules ON at all times. Toggle features as needed to keep your chart clean. High-probability setups are often found where multiple factors converge (Confluence). For example: A bounce off an "S/R Line," confirmed by a "BOS" in Dow Structure, coinciding with a "Gap" fill.

X AVWAP DSOA powerful, non-overlay momentum indicator designed to measure the relationship between current price action and key Volume Weighted Average Price (VWAP) structures. It provides traders with a refined, configurable view of momentum by combining the **magnitude of price separation** with the **trend momentum** of the volume anchor.

---

### Core Calculation and Principle

This oscillator moves beyond simple price-vs-average separation by integrating the momentum (slope) of the volume average itself. The indicator is built around two primary components:

1. **Distance (D):** This is the magnitude of separation, calculated as the difference between the **closing price** and the selected **AVWAP Anchor Source** ($D = \text{Close} - \text{AVWAP}$).

2. **Slope (S):** This represents the **trend momentum** of the VWAP, calculated as the change in the smoothed AVWAP over a defined lookback period.

The final oscillator value is determined by the selected **Combination Method**, giving the user control over how these two factors interact:

* **Addition (Baseline):** The oscillator value is $D + S$. This provides a balanced view where the price separation is slightly adjusted by the VWAP's momentum.

* **Weighted Addition:** The oscillator value is $D + (S \times \text{Weight})$. This is a powerful feature that **allows the user to prioritize the impact of the Slope (trend momentum) over the Distance (magnitude)** using a customizable multiplier called the **Slope Weight**.

---

### Customization and Flexibility

The indicator's value lies in its deep configurability, allowing it to adapt to different trading strategies and timeframes:

* **AVWAP Anchor Source:** You can toggle between two critical VWAP reset structures for context:

* **4H Session VWAP:** Uses fixed, sequential 4-hour VWAP segments (e.g., 18:00, 22:00 NY Time) for tracking short-term structural shifts.

* **Daily AVWAP (ETH 18:00):** Uses a single, continuous VWAP anchored from the Electronic Trading Hours (ETH) open at 18:00 NY Time, providing a broader, sustained volume-weighted average context.

* **VWAP Price Source:** The underlying price used to calculate the VWAP itself is selectable (options include Close, OHLC4, HLC3, Open, High, and Low).

* **Plot Style:** Toggle between a continuous **Line** plot (for tracking fine movements) and a color-coded **Histogram** (for clear magnitude and directional reading, with Blue for positive and Red for negative).

### Trading Application

The AVWAP Distance & Slope Oscillator is a sophisticated tool best used to identify:

* **Zero-Line Crosses:** Signifying price crossing the underlying volume anchor while accounting for the anchor's own momentum.

* **Momentum Confirmation:** A high positive reading indicates price is strongly above the VWAP, and the VWAP itself is actively rising (strong bullish momentum).

* **Filtered Signals:** By adjusting the **Slope Weight** (in the Weighted Addition method), traders can amplify signals when the structural trend (VWAP slope) is strong, helping to filter out minor price fluctuations that occur when the VWAP is relatively flat.

X Tail that Wagsintraday session-framework and ETH-anchored VWAP tool for TradingView. It draws today’s OVN (ETH) high/mid/low, today’s RTH-day open, previous day open/high/low, and a carried ETH VWAP handle (yesterday’s 4:00 PM NY VWAP, projected forward) to give you a clean, non-repainting scaffold for bias, structure, and execution. All timestamps are New York–local with DST handled explicitly, so historical sessions align correctly across time changes.

Key Capabilities

ETH OVN Range (18:00 → 09:30 NY)

Captures the rolling overnight high/low and computes the mid; at 09:30 NY it locks those levels and extends them to 16:00 NY (same day).

Optional labels (size/color configurable) placed slightly to the right of the 4 PM timestamp for readability.

Daily Handles (Today & Previous Day)

Today’s open line starts at the ETH open (anchor preserved) and extends toward 4 PM NY (or up to the “current bar + 5 bars” cap), with label control.

Previous day open/high/low plotted as discrete reference lines for carry-over structure.

ETH-Anchored VWAP (Live) + Bands

ETH-anchored VWAP runs only during the active ETH session (DST-aware).

Optional VWAP bands (0.5×, 1.0×, 2.0× multipliers) plotted as line-break series.

Carried ETH VWAP Handle (PD 4 PM Snapshot)

At 16:00 NY, the script snapshots the final ETH VWAP value.

On the next ETH open, it projects that value as a static dashed line through the session (non-mutating, non-repainting), with optional label.

Labeling & Styling

Single-toggle label system with color and five sizes.

Per-line color/width controls for quick visual hierarchy.

Internal “tail” logic keeps right endpoints near price (open-anchored lines extend to min(4 PM, now + 5 bars)), avoiding chart-wide overdraw.

Robust Session Logic

All session boundaries computed in NY local time; DST rules applied for historical bars.

Cross-midnight windows handled safely (no gaps or misalignment around day rolls).

Primary Use Cases

Session Bias & Context

Use OVN H/M/L and today’s open to define structural bias zones before RTH begins. A break-and-hold above OVN mid, for example, can filter long ideas; conversely, rejection at OVN high can warn of mean reversion.

Carry-Forward Mean/Value Reference

The carried ETH VWAP (PD 4 PM) acts as a “value memory” line for the next day. Traders can:

Fade tests away from it in balanced conditions,

Use it as a pullback/acceptance gauge during trends,

Track liquidity grabs when price spikes through and reclaims.

Execution Planning & Risk

Anchor stops/targets around PD H/L and OVN H/M/L for well-defined invalidation.

Combine with your entry model (order-flow, momentum, or pattern) to time fades at range extremes or momentum breaks from OVN mid.

Confluence Mapping

Layer the tool with opening range tools, HTF zones, or profile/VWAPs (weekly/daily) to spot high-quality confluence where multiple references cluster.

Regime & Day-Type Read

Quickly see whether RTH accepts/rejects the OVN range or gravitates to PD VWAP handle, helping classify the day (trend, balanced, double-distribution, etc.).

Quick Start

Apply to your intraday chart (any instrument supported by TradingView; best on ≤15m for live intraday context).

In Current Day group, keep Open and OVN HL on; optionally display the mid.

In Previous Day group, enable PD Open/HL for carry-over levels.

Enable AVWAP if you want live ETH-anchored VWAP and its Bands for distance context.

Keep PD VWAP on to project yesterday’s 4 PM ETH VWAP as a static dashed line into today.

Use the Label group to size/color the on-chart tags.

Settings Overview (Plain-English)

Label: Toggle labels on/off; choose label text color and size.

Current Day:

Open (color/width) — daily open line anchored at ETH open.

OVN HL (and Mid) — overnight high/low and midpoint, locked at 09:30 and extended to 16:00.

AVWAP + Bands — ETH-anchored VWAP with optional 0.5×/1×/2× bands.

Previous Day:

PD Open/HL — yesterday’s daily handles.

PD VWAP — the carried snapshot of yesterday’s 4 PM ETH VWAP projected forward (dashed).

Notes & Best Practices

Time Zone: All session logic is hard-coded to America/New_York and DST-robust. No manual DST tweaks required.

Non-Repainting: The carried PD VWAP line is a snapshot; once drawn, it does not back-fill or mutate.

Intraday Use: Designed for intraday execution. It will display on higher TFs, but the session granularity is most informative at ≤15m.

Performance: Script caps lines/labels (500) and uses short “tails” to keep charts responsive.

Compatibility: Uses request.security(..., "D", series, lookahead_on) intentionally to lock daily handles early for planning; this is by design.

Typical Playbook Examples

Fade Extremes in Balance: As RTH opens inside OVN, look for rejection wicks at OVN High with confluence from PD VWAP handle overhead; risk above OVN High.

Trend Continuation: In directional sessions, acceptances above OVN Mid with price pulling back to the live ETH VWAP can offer continuation entries.

Reversion to Value: Sharp extensions away from the carried PD VWAP that quickly stall often revert to that handle; use it as a target or as an acceptance test.

RightFlow Universal Volume Profile - Any Market Any TimeframeSummary in one paragraph

RightFlow is a right anchored microstructure volume profile for stocks, futures, FX, and liquid crypto on intraday and daily timeframes. It acts only when several conditions align inside a session window and presents the result as a compact right side profile with value area, POC, a bull bear mix by price bin, and a HUD of profile VWAP and pressure shares. It is original because it distributes each bar’s weight into multiple mid price slices, blends bull bear pressure per bin with a CLV based split, and grows the profile to the right so price action stays readable. Add to a clean chart, read the table, and use the visuals. For conservative workflows read on bar close.

Scope and intent

• Markets. Major FX pairs, index futures, large cap equities and ETFs, liquid crypto.

• Timeframes. One minute to daily.

• Default demo used in the publication. SPY on 15 minute.

• Purpose. See where participation concentrates, which side dominated by price level, and how far price sits from VA and POC.

Originality and usefulness

• Unique fusion. Right anchored growth plus per bar slicing and CLV split, with weight modes Raw, Notional, and DeltaProxy.

• Failure mode addressed. False reads from single bar direction and coarse binning.

• Testability. All parts sit in Inputs and the HUD.

• Portable yardstick. Value Area percent and POC are universal across symbols.

• Protected scripts. Not applicable. Method and use are fully disclosed.

Method overview in plain language

Pick a scope Rolling or Today or This Week. Define a window and number of price bins. For each bar, split its range into small slices, assign each slice a weight from the selected mode, and split that weight by CLV or by bar direction. Accumulate totals per bin. Find the bin with the highest total as POC. Expand left and right until the chosen share of total volume is covered to form the value area. Compute profile VWAP for all, buyers, and sellers and show them with pressure shares.

Base measures

Range basis. High minus low and mid price samples across the bar window.

Return basis. Not used. VWAP trio is price weighted by weights.

Components

• RightFlow Bins. Price histogram that grows to the right.

• Bull Bear Split. CLV based 0 to 1 share or pure bar direction.

• Weight Mode. Raw volume, notional volume times close, or DeltaProxy focus.

• Value Area Engine. POC then outward expansion to target share.

• HUD. Profile VWAP, Buy and Sell percent, winner delta, split and weight mode.

• Session windows optional. Scope resets on day or week.

Fusion rule

Color of each bin is the convex blend of bull and bear shares. Value area shading is lighter inside and darker outside.

Signal rule

This is context, not a trade signal. A strong separation between buy and sell percent with price holding inside VA often confirms balance. Price outside VA with skewed pressure often marks initiative moves.

What you will see on the chart

• Right side bins with blended colors.

• A POC line across the profile width.

• Labels for POC, VAH, and VAL.

• A compact HUD table in the top right.

Table fields and quick reading guide

• VWAP. Profile VWAP.

• Buy and Sell. Pressure shares in percent.

• Delta Winner. Winner side and margin in percent.

• Split and Weight. The active modes.

Reading tip. When Session scope is Today or This Week and Buy minus Sell is clearly positive or negative, that side often controls the day’s narrative.

Inputs with guidance

Setup

• Profile scope. Rolling or session reset. Rolling uses window bars.

• Rolling window bars. Typical 100 to 300. Larger is smoother.

Binning

• Price bins. Typical 32 to 128. More bins increase detail.

• Slices per bar. Typical 3 to 7. Raising it smooths distribution.

Weighting

• Weight mode. Raw, Notional, DeltaProxy. Notional emphasizes expensive prints.

• Bull Bear split. CLV or BarDir. CLV is more nuanced.

• Value Area percent. Typical 68 to 75.

View

• Profile width in bars, color split toggle, value area shading, opacities, POC line, VA labels.

Usage recipes

Intraday trend focus

• Scope Today, bins 64, slices 5, Value Area 70.

• Split CLV, Weight Notional.

Intraday mean reversion

• Scope Today, bins 96, Value Area 75.

• Watch fades back to POC after initiative pushes.

Swing continuation

• Scope Rolling 200 bars, bins 48.

• Use Buy Sell skew with price relative to VA.

Realism and responsible publication

No performance claims. Shapes can move while a bar forms and settle on close. Education only.

Honest limitations and failure modes

Thin liquidity and data gaps can distort bin weights. Very quiet regimes reduce contrast. Session time is the chart venue time.

Open source reuse and credits

None.

Legal

Education and research only. Not investment advice. Test on history and simulation before live use.

_mr_beach Sunday Entwicklung Version 1_mr_beach Sunday Development Version 1

Short Description (for TradingView publication):

This indicator combines EMA crossovers, VWAP with standard deviation bands, gap detection, pivot-based support & resistance, and VWAP distance labels in a single overlay. Perfect for discretionary traders aiming to efficiently identify gap fills, trend reversals, and key price levels. All components can be toggled on/off via the settings menu.

Full Indicator Description:

🧠 Purpose of the Indicator:

This all-in-one tool merges several analytical features to visualize trend direction, market structure, key price levels (e.g., gaps, VWAP distance, pivot support), and entry signals at a glance.

🔧 Integrated Features:

EMA20 / EMA50: Trend detection via moving averages. Crossover signals indicate potential entries.

VWAP + Band: Volume-weighted average price with visual deviation bands.