Account GuardianAccount Guardian: Dynamic Risk/Reward Overlay

Introduction

Account Guardian is an open-source indicator for TradingView designed to help traders evaluate trade setups before entering positions. It automatically calculates Risk-to-Reward ratios based on market structure, displays visual Stop Loss and Take Profit zones, and provides real-time position sizing recommendations.

The indicator addresses a fundamental question every trader should ask before entering a trade: "Does this setup make mathematical sense?" Account Guardian answers this question visually and numerically, helping traders avoid impulsive entries with poor risk profiles.

Core Functionality

Account Guardian performs four primary functions:

Detects swing highs and swing lows to identify logical stop loss placement levels

Calculates Risk-to-Reward ratios for both long and short setups in real-time

Displays visual SL/TP zones on the chart for immediate trade planning

Computes position sizing based on your account size and risk tolerance

The goal is to provide traders with instant feedback on whether a potential trade meets their minimum risk/reward criteria before committing capital.

How It Works

Swing Detection

The indicator uses pivot point detection to identify recent swing highs and swing lows on the chart. These swing points serve as logical areas for stop loss placement:

For Long Trades: The most recent swing low becomes the stop loss level. Price breaking below this level would invalidate the bullish thesis.

For Short Trades: The most recent swing high becomes the stop loss level. Price breaking above this level would invalidate the bearish thesis.

The swing detection lookback period is configurable, allowing you to adjust sensitivity based on your trading timeframe and style.

It automatically adjusts the tp and sl when it is applied to your chart so it is always moving up and down!

Risk/Reward Calculation

Once swing levels are identified, the indicator calculates:

Entry Price: Current close price (where you would enter)

Stop Loss: Recent swing low (for longs) or swing high (for shorts)

Risk: Distance from entry to stop loss

Take Profit: Entry plus (Risk × Target Multiplier)

R:R Ratio: Reward divided by Risk

The R:R ratio is then evaluated against your configured thresholds to determine if the setup is valid, marginal, or poor.

Visual Elements

SL/TP Zones

When enabled, the indicator draws colored boxes on the chart showing:

Red Zone: Stop Loss area - the region between your entry and stop loss

Green/Gold/Red Zone: Take Profit area - colored based on R:R quality

The color coding provides instant visual feedback:

Green: R:R meets or exceeds your "Good R:R" threshold (default 3:1)

Gold: R:R meets minimum threshold but below "Good" (between 2:1 and 3:1)

Red: R:R below minimum threshold - setup should be avoided

Swing Point Markers

Small circles mark detected swing points on the chart:

Green circles: Swing lows (potential support / long SL levels)

Red circles: Swing highs (potential resistance / short SL levels)

Dashboard Panel

The dashboard in the top-right corner displays comprehensive trade planning information:

R:R Row: Current Risk-to-Reward ratio for long and short setups

Status Row: VALID, OK, BAD, or N/A based on R:R thresholds

Stop Loss Row: Exact price level for stop loss placement

Take Profit Row: Exact price level for take profit placement

Pos Size Row: Recommended position size based on your risk parameters

Risk $ Row: Dollar amount at risk per trade

Position Sizing Logic

The indicator calculates position size using the formula:

Position Size = Risk Amount / Risk per Unit

Where:

Risk Amount = Account Size × (Risk Percentage / 100)

Risk per Unit = Entry Price - Stop Loss Price

For example, with a $10,000 account risking 1% per trade ($100), if your entry is at 100 and stop loss at 98 (risk of 2 per unit), your position size would be 50 units.

Input Parameters

Swing Detection:

Swing Lookback: Number of bars to look back for pivot detection (default: 10). Higher values find more significant swing points but may be slower to update.

Target Multiplier: Multiplier applied to risk to calculate take profit distance (default: 2). A value of 2 means TP is 2× the distance of SL from entry.

Risk/Reward Thresholds:

Minimum R:R: Minimum acceptable Risk-to-Reward ratio (default: 2.0). Setups below this show as "BAD" in red.

Good R:R: Threshold for excellent setups (default: 3.0). Setups at or above this show as "VALID" in green.

Account Settings:

Account Size ($): Your trading account size in dollars (default: 10,000). Used for position sizing calculations.

Risk Per Trade (%): Percentage of account to risk per trade (default: 1.0%). Professional traders typically risk 0.5-2% per trade.

Display:

Show SL/TP Zones: Toggle visibility of the colored zone boxes on chart (default: enabled)

Show Dashboard: Toggle visibility of the information panel (default: enabled)

Analyze Direction: Choose to analyze Long only, Short only, or Both directions (default: Both)

How to Use This Indicator

Basic Workflow:

Add the indicator to your chart

Configure your account size and risk percentage in the settings

Set your minimum and good R:R thresholds based on your trading rules

Look at the dashboard to see current R:R for potential long and short entries

Only consider trades where the status shows "VALID" or at minimum "OK"

Use the displayed SL and TP levels for your order placement

Use the position size recommendation to determine lot/contract size

Interpreting the Dashboard:

VALID (Green): Excellent setup - R:R meets your "Good" threshold. This is the ideal scenario for taking a trade.

OK (Gold): Acceptable setup - R:R meets minimum but isn't optimal. Consider taking if other confluence factors align.

BAD (Red): Poor setup - R:R below minimum threshold. Avoid this trade or wait for better entry.

N/A (Gray): Cannot calculate - usually means no valid swing point detected yet.

Best Practices:

Use this indicator as a filter, not a signal generator. It tells you IF a trade makes sense, not WHEN to enter.

Combine with your existing entry strategy - use Account Guardian to validate setups from other analysis.

Adjust the swing lookback based on your timeframe. Lower timeframes may need smaller lookback values.

Be honest with your account size input - accurate position sizing requires accurate inputs.

Consider the target multiplier carefully. Higher multipliers mean larger potential reward but lower probability of hitting TP.

Alerts

The indicator includes four alert conditions:

Good Long Setup: Triggers when long R:R reaches or exceeds your "Good R:R" threshold

Good Short Setup: Triggers when short R:R reaches or exceeds your "Good R:R" threshold

Bad Long Setup: Triggers when long R:R falls below your minimum threshold

Bad Short Setup: Triggers when short R:R falls below your minimum threshold

These alerts can help you monitor multiple charts and get notified when favorable setups appear.

Technical Implementation

The indicator is built using Pine Script v6 and includes:

Pivot-based swing detection using ta.pivothigh() and ta.pivotlow()

Dynamic box drawing for visual SL/TP zones

Table-based dashboard for clean information display

Color-coded visual feedback system

Persistent variable tracking for swing levels

Code Structure:

// Swing Detection

float swingHi = ta.pivothigh(high, swingLen, swingLen)

float swingLo = ta.pivotlow(low, swingLen, swingLen)

// R:R Calculation for Long

float longSL = recentSwingLo

float longRisk = entry - longSL

float longTP = entry + (longRisk * targetMult)

float longRR = (longTP - entry) / longRisk

// Position Sizing

float riskAmount = accountSize * (riskPct / 100)

float posSize = riskAmount / longRisk

Limitations

The indicator uses historical swing points which may not always represent optimal SL placement for your specific strategy

Position sizing assumes you can trade fractional units - adjust accordingly for instruments with minimum lot sizes

R:R calculations assume linear price movement and don't account for gaps or slippage

The indicator doesn't predict price direction - it only evaluates the mathematical viability of a setup

Swing detection has inherent lag due to the lookback period required for pivot confirmation

Recommended Settings by Trading Style

Scalping (1-5 minute charts):

Swing Lookback: 5-8

Target Multiplier: 1-2

Minimum R:R: 1.5

Good R:R: 2.0

Day Trading (15-60 minute charts):

Swing Lookback: 8-12

Target Multiplier: 2

Minimum R:R: 2.0

Good R:R: 3.0

Swing Trading (4H-Daily charts):

Swing Lookback: 10-20

Target Multiplier: 2-3

Minimum R:R: 2.5

Good R:R: 4.0

Why Risk/Reward Matters

Many traders focus solely on win rate, but profitability depends on the combination of win rate AND risk/reward ratio. Consider these scenarios:

50% win rate with 1:1 R:R = Breakeven (before costs)

50% win rate with 2:1 R:R = Profitable

40% win rate with 3:1 R:R = Profitable

60% win rate with 1:2 R:R = Losing money

Account Guardian helps ensure you only take trades where the math works in your favor, even if you're wrong more often than you're right.

Disclaimer

This indicator is provided for educational and informational purposes only. It is not intended as financial, investment, trading, or any other type of advice or recommendation.

Trading involves substantial risk of loss and is not suitable for all investors. The calculations provided by this indicator are based on historical price data and mathematical formulas that may not accurately predict future price movements.

Position sizing recommendations are estimates based on user inputs and should be verified before placing actual trades. Always consider factors such as leverage, margin requirements, and broker-specific rules when determining actual position sizes.

The Risk-to-Reward ratios displayed are theoretical calculations based on swing point detection. Actual trade outcomes will vary based on market conditions, execution quality, and other factors not captured by this indicator.

Past performance does not guarantee future results. Users should thoroughly test any trading approach in a demo environment before risking real capital. The authors and publishers of this indicator are not responsible for any losses or damages arising from its use.

Always consult with a qualified financial advisor before making investment decisions.

Statistics

Session Opening Bar RangeSession Opening Bar Range (OBR) - Advanced Opening Range Indicator with Statistical Analysis

Overview

The Session First Bar Range (FBR) indicator is a comprehensive tool that captures and projects key levels based on the first bar of a user-defined trading session. Unlike traditional daily opening range indicators, this script allows traders to focus on specific session windows (New York RTH, London, Asia, etc.) and analyze price behavior relative to the initial momentum established in that session's opening bar.

What makes this indicator unique is its combination of three distinct projection methodologies: statistical analysis based on historical range data, Fibonacci extensions, and fixed-point rotation levels commonly used by institutional traders. To our knowledge, this is the only opening range indicator that incorporates statistical standard deviation levels calculated from historical first bar ranges, making it both a technical and probabilistic tool.

Core Concept

The opening range concept is based on the principle that the initial price action of a trading session often sets the tone for the remainder of that session.

Professional traders have long observed that:

The first bar's high and low act as key reference points

Price often respects or breaks these levels with significance

Expansion beyond the opening range tends to occur in measurable increments

This indicator takes these observations and enhances them with:

Historical probability analysis - "Based on the last 60 sessions, price typically extends X standard deviations beyond the opening range"

Proportional projections - Fibonacci-based extensions showing where measured moves typically target

Fixed-point rotations - Institutional rotation levels (e.g., 65 points for NQ, 15 points for ES)

How It Works

Session Detection & First Bar Capture

The indicator uses Pine Script's time() function with timezone support to precisely detect when a trading session begins. When the first bar of the selected timeframe occurs within the session window, the script captures:

High (H): The high of the first bar

Low (L): The low of the first bar

Mid (M): The midpoint (hl2) of the first bar

Critical Detail: These levels are fixed from the first bar only - they do not update as the session progresses. This differs from many "opening range" indicators that use a time period (e.g., first 30 minutes). Here, you select the bar timeframe (default 5-minute), and only that single first bar's range is captured.

Statistical Level Calculation

The indicator maintains a rolling array of the last N session's first bar ranges (default: 60 sessions). For each new session, it calculates:

Average Range: Mean of historical first bar ranges

Standard Deviation: Volatility of those ranges

Projection Levels: High/Low ± (Average Range + Std Dev × Multiplier)

This provides probability-based levels. For example, a +2σ level suggests: "Historically, price extending this far beyond the opening range is a 2-standard-deviation event (approximately 95th percentile)."

Fibonacci Extensions

Using the first bar range as the base unit (100%), the indicator projects Fibonacci levels:

100% extension: One full range above the high / below the low

1.618x extension: (Default) Golden ratio projection

2.618x, 3.618x extensions: Additional Fibonacci levels

Calculation: Range = H - L, then Target = H + (Range × Multiplier) for upside projections.

OR Rotation Levels

These are fixed-point increments from the first bar's high and low. Unlike percentage-based methods, rotations use absolute point values:

NQ traders often use 65-point increments

ES traders often use 15-point increments

Gold/bonds use different values

The indicator draws 5 levels above the high (R+1 through R+5) and 5 below the low (R-1 through R-5), each separated by your specified point increment.

Features:

Session Options

Pre-configured Sessions:

New York RTH (9:30am - 4:00pm)

New York Futures (8:00am - 5:00pm)

London (2:00am - 8:00am)

Asia (7:00pm - 2:00am)

Midnight to 5pm

ZB/Gold/Silver OR (8:20am - 4:00pm)

CL OR (9:00am - 4:00pm)

Custom Session: Define your own start/end times in HHMM format

Timezone Support: All sessions respect the selected timezone (default: America/New_York)

Customizable Timeframe

Select any timeframe for the first bar (1min, 5min, 15min, etc.)

Default: 5-minute bars

Important: This is the timeframe for the first bar capture, independent of your chart's timeframe

Display Options

Historical Ranges: Show/hide past session ranges (with configurable limit to manage performance)

Line Styles: Choose between Solid, Dashed, or Dotted for range lines and midline

Label Position: Left or Right side of range

Show Prices: Optionally display actual price values on labels

Custom Colors: Fully customizable colors for all components

Statistical Levels

Lookback Period: Number of historical sessions to analyze (default: 60)

Two Multiplier Levels: Default 1σ and 2σ, fully adjustable

Separate styling: Different line styles (dashed vs dotted) for each sigma level

Optional Labels: Show/hide sigma notation labels

Fibonacci Extensions

Four Extension Levels: 100%, 1.618x, 2.618x, 3.618x (all customizable)

Bidirectional: Projections both above and below the opening range

Optional Labels: Toggle percentage/multiplier labels

OR Rotation Levels

Configurable Increment: Set the point value for your instrument

Five Levels Each Direction: R±1 through R±5

Dynamic Labels: Show both rotation number and point value (e.g., "R+1 (65)")

Three Line Styles: Solid, Dashed, or Dotted

How to Use

Setup

Add the indicator to your chart

Select your trading session from the dropdown

Set the timeframe for first bar capture (typically 5-15 minutes)

Configure which projection methods you want to see (Statistical, Fibonacci, and/or Rotations)

For Day Traders

Scenario: Trading NQ during New York RTH

Session: Select "New York RTH (9:30am - 4:00pm)"

Timeframe: 5-minute (captures 9:30-9:35 bar)

Enable: OR Rotations with 65-point increments

Strategy:

Watch for acceptance/rejection at rotation levels

Use R+1/R-1 as initial profit targets

R+2/R-2 as extended targets

Statistical levels show when price is in "outlier" territory

and rotation levels

Performance Notes

The indicator limits objects to stay within TradingView's constraints (500 max)

If you enable all features, reduce "Maximum Historical Ranges" to prevent slowdown

Typical configuration: 10-20 historical ranges with all features enabled works well

Settings Guide

Session Settings

Session: Choose from pre-configured sessions or "Custom"

Custom Session Start/End: HHMM format (e.g., "0930" for 9:30am)

Timezone: Critical for accurate session detection

Opening Bar Format

Timeframe: The bar size for capturing the first bar's range

Show Midline: Toggle the mid-point line

Show Historical Ranges: Display previous sessions (recommended: leave ON)

Maximum Historical Ranges: Limit history to manage performance (1-500)

Range Style / MidLine Style: Solid, Dashed, or Dotted

Position: Label placement (Left or Right)

Show Prices: Include actual price values on labels

Statistical Levels

Lookback Periods: How many historical first bar ranges to analyze (default: 60)

Std Dev Multiplier 1/2: The sigma levels to project (default: 1.0 and 2.0)

All visual settings (colors, line width, label size)

Fibonacci Extensions

Show Fib Extensions: Enable/disable Fibonacci projections

Measured Move Extensions 1-4: The multipliers (default: 1.618, 2.618, 3.618, 4.618)

Visual customization options

OR Rotations

Rotation Increment: The point value for your instrument

NQ: 65 points

ES: 15 points

Adjust for other instruments based on their typical rotation behavior

Show Rotation Labels: Display level numbers and point values

Visual customization options

Use Cases

Gap Trading: When price gaps away from previous day's close, the first bar range shows the initial gap acceptance/rejection zone

Breakout Confirmation: Price breaking and holding above the first bar high with volume suggests trend day potential. Rotation levels provide measured targets.

Reversal Identification: Price reaching +2σ statistical level = rare event, potential exhaustion

Range Bound Days: Price oscillating between first bar high/low suggests range-bound session; trade reversals at extremes

Institutional Level Awareness: OR Rotations at 65 points (NQ) align with levels professional traders watch

Technical Notes

The indicator uses request.security() with lookahead=barmerge.lookahead_on to ensure the first bar levels are captured correctly

All drawing objects (lines, labels, fills) are managed in arrays with automatic cleanup to prevent memory issues

The statistical calculations use array.avg() and array.stdev() for accurate probability estimates

Rotation levels use individual line variables (like Fibonacci) rather than loops for reliability

Summary

This indicator is original in its combination of three distinct methodologies for projecting levels from a session's opening range:

Statistical Analysis - No other opening range indicator (to our knowledge) calculates standard deviation projections from historical first bar ranges

Time-Based Session Flexibility - Most OR indicators use only daily or fixed time periods; this allows any custom session window

Multiple Projection Methods - Traders can use statistical, Fibonacci, AND rotation levels together or separately

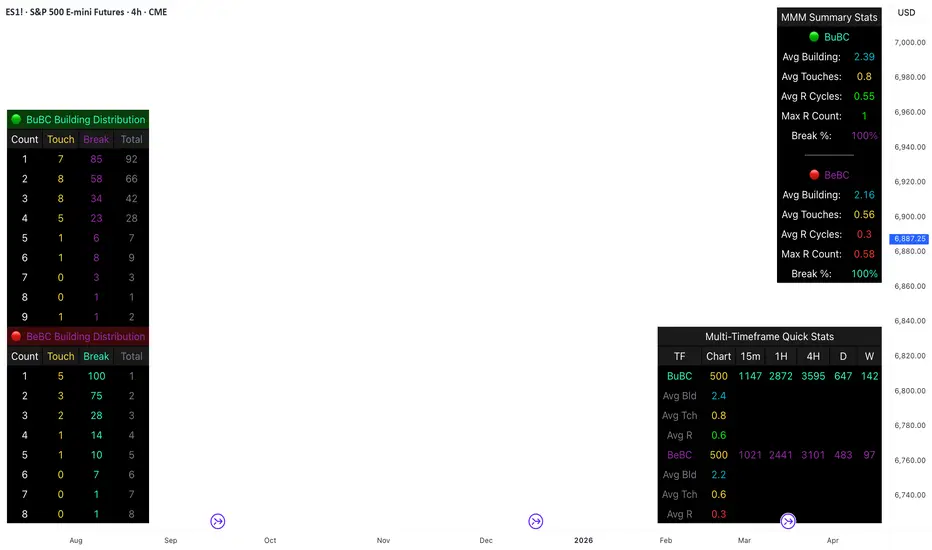

Body Close Continuity & failure Backtesting @MaxMaseratiThis indicator, is a highly advanced institutional-grade tool designed to track the "lifespan" of a trend based on Body Close (BC) sequences.

Unlike basic indicators that just show direction, this script analyzes the structural integrity of a trend by monitoring how many candles continue the move before a "Touch" (retest) or a "Break" (failure) occurs.

The Continuity & Failure Stats indicator tracks sequences of Bullish Body Closes (BuBC) and Bearish Body Closes (BeBC). It measures three critical phases: Building (pure momentum), Touching (price retesting the low/high of the sequence), and Resumption (price continuing the trend after a retest). It provides a statistical distribution of how long these "buildings" typically last before failing, allowing traders to know exactly when a trend is overextended.

This comprehensive analysis blends the statistical breakdown of the Continuity & Failure Stats indicator to provide a deep understanding of the structural momentum for the S&P 500 E-mini (ES1!) on a 4-hour timeframe.

1. Extensive Table Breakdown

A. Building Distribution (Left Table): The Fatigue Gauge

This table acts as a histogram of momentum, tracking the "Building Count"—the number of consecutive candles closing in a trend without price returning to its origin.

Count Column: Represents the streak length (e.g., 1, 2, or 3 candles).

Touch Column: Shows how many times a streak was interrupted by a retest ("touch") but remained structurally intact.

Break Column: Counts total structural failures where price closed beyond the sequence's anchor.

Data Insight: For BuBC, 92 sequences reached Count 1, but only 28 remained by Count 4. This reveals a steep momentum decay after the 3rd candle, establishing a "Statistical Wall" where only 2 sequences in history reached a count of 9.

B. MMM Summary Stats (Top Right): The Mathematical DNA

This table provides the "Expected Value" and behavior of a trend over the lookback period.

Avg Building (2.39 for BuBC): On average, a bullish move lasts ~2.4 candles of pure momentum before a retest or reversal occurs.

Avg Touches (0.8): This low number indicates "clean" trends that rarely wobble back to retest levels multiple times before reaching a conclusion.

Avg R Cycles (0.55): This suggests that once a bullish trend is interrupted, it only successfully resumes its momentum about half the time.

Max R Count (1): Typically, once a trend is "touched," it only manages one more push before failing.

C. Multi-Timeframe (MTF) Quick Stats (Bottom Right): Trend Weight

This compares the 4H chart against other layers of the market to identify "global" alignment.

Sample Comparison: There are 3,594 tracked BuBC sequences on the 4H compared to only 142 on the Weekly chart.

Fractal Law: The Avg Building (2.4) is consistent across several timeframes, implying that the "Rule of Three" (momentum fading after 3 candles) is a fractal characteristic of this asset.

2. Table Comparison: Synthesizing the Data

To trade effectively, you must compare Distribution (timing) against Summary Stats (averages):

Continuity vs. Failure: The Summary Stats show an average building of 2.39. When checking the Distribution table at Count 2, the "Break" count (58) is already high relative to the "Total". This confirms that the risk of failure increases exponentially the moment you exceed the average.

Momentum vs. Mean Reversion: Distribution tells you when a trend is "tired". If the 4H is at a "Building Count 4" (statistically overextended) while the Weekly chart is at "Building Count 1" (fresh momentum), you may choose to prioritize the higher timeframe's strength despite the local overextension.

3. Strategic Summary & Application

This indicator proves that market momentum follows a predictable "Building" cycle rather than an infinite streak.

The "Rule of Three" for ES1! 4H:

The Entry Zone (Momentum Start): The most profitable entries occur at Building Count 1. Statistically, you have a high probability of reaching a count of 2 or 3.

The Exit Zone (Momentum Limit): Take profits or tighten stops at Count 3. The data shows the sample size drops by nearly 50% between Count 3 and Count 4.

The "Touch" Rule (Retest Reliability): If price returns to the sequence low (a "Touch"), do not expect a massive continuation. The Max R Count of 1 tells us that resumptions are usually short-lived.

Danger Zone: Entering at Building Count 4 or higher is statistically dangerous, as the "Break" probability significantly outweighs the "Touch" or continuation probability.

CCI Standard DeviationCCI Standard Deviation – Asymmetric Volatility-Adjusted Trend Filter (CCI SD)

The Commodity Channel Index (CCI), created by Donald Lambert in 1980, measures how far the typical price deviates from its statistical average to identify cyclical momentum and trend strength.

The standard formula is:

CCI = (Typical Price − SMA(Typical Price, n)) / (0.015 × Mean Deviation)

where Typical Price = (High + Low + Close)/3.

CCI is unbounded and centered around zero: sustained readings above zero indicate bullish momentum, below zero bearish. Classic interpretations often use zero-line crosses or fixed levels (±100, ±200, ±250), but these can be unreliable when CCI volatility changes across market regimes.

This indicator was developed to create a more disciplined trend-following tool that aligns with my core risk principle: “always protect to the downside.”

Starting from the standard CCI zero-line concept for trend direction, I experimented with standard deviation bands to make the oscillator volatility-adjusted. I then applied deliberate asymmetry: requiring the lower 1σ envelope (CCI − stdev) to cross above a positive threshold for bullish confirmation (high-probability entry only in robust trends), while exiting immediately on any raw CCI weakness below a negative threshold (quick downside protection). User inputs for both thresholds were added to allow fine-tuning and adaptability across different assets and timeframes.

An optional DEMA-smoothed version of the lower envelope provides additional clarity when desired.

Extreme zones

raw CCI ±240 and lower envelope > 200 or < –200 - are highlighted with background shading to flag rare acceleration or capitulation phases.

How it works

Standard CCI calculated on typical price (default length 38).

Rolling standard deviation of the CCI itself (default length 13) measures the oscillator’s recent volatility.

Lower envelope = CCI − stdev (dn).

Optional DEMA smoothing (default length 12) can be toggled.

Trend logic:

Bullish regime only when lower envelope

→ Long Threshold (default +10)

→ statistical proof of strength

Bearish/neutral immediately when raw CCI

→ Short Threshold (default –25)

→ fast downside protection

Origin and development

The indicator emerged from wanting a cleaner, more reliable CCI for trend direction. After testing volatility-adjusted versions, the asymmetric design proved superior:

it enters only high-conviction uptrends and exits rapidly on weakness, significantly reducing whipsaws while preserving trend capture.

Parameters were optimized through extensive backtests on major assets (BTC, ETH, SOL and many more Cryptos; Magnificent 7 stocks, QQQ, SPX, gold).

The defaults were selected for the best average Sortino ratio and lowest maximum drawdown across this broad universe, ensuring robustness and avoiding single-asset overfitting.

How to use it

Green triangle below bar

→ lower envelope crosses above Long Threshold

→ high-conviction bullish trend confirmed

→ enter or add to longs

Magenta triangle above bar

→ CCI crosses below Short Threshold

→ exit longs or go cash/short

While lower envelope remains above Long Threshold

→ hold bullish positions

Extreme background shading (dn >200 or CCI ±240)

→ rare high-attention zones (potential acceleration or exhaustion)

Recommended defaults

CCI length: 38

SD length: 13

Long threshold: +10

Short threshold: –25

Optional MA length: 12 (DEMA of lower envelope)

All visual elements (bar coloring, signals, background, smoothed line) are toggleable for personal preference.

This indicator is designed as a trend-strength and risk-management filter and is not intended as a standalone trading system.

Disclaimer:

This is not financial advice. Backtests are based on past results and are not indicative of future performance.

Xbirch_Turtle_ Crypto_CalcМодернизированная стратегия Черепах.

Вход/выход по каналу Дончиана, стопы по величине ATR, возможность выбора лонг/шорт/всё. Имеется пирамидинг - добавление по +0,5ATR от первого бая, не более 4х входов. Модернизированный стоп - по ATR от первого бая.

Не финансовый совет.

A modernized Turtle strategy.

Entry/exit based on the Donchian Channel, stops based on the ATR value, and the ability to choose long/short/all options. Pyramiding is available – adding +0.5 ATR from the first buy, with a maximum of four entries. The modernized stop is based on the ATR value from the first buy.

This is not financial advice.

SMC Post-Analysis Lab [PhenLabs]📊 SMC Post-Analysis Lab

Version: PineScript™ v6

📌 Description

The SMC Post-Analysis Lab is a dedicated hindsight analysis tool built for traders who want to understand what really happened during any historical trading period. Unlike forward-looking indicators, this tool lets you scroll back through time and instantly receive algorithmic classification of market states using Smart Money Concepts methodology.

Whether you’re reviewing a losing trade, studying a successful session, or building your pattern recognition skills, this indicator provides immediate context. The expansion-aware algorithm processes price action within your selected window and outputs clear, actionable classifications ranging from Parabolic Expansion to Consolidation Inducements.

Stop relying on subjective post-trade analysis. Let the algorithm objectively tell you whether institutional players were accumulating, distributing, or running inducements during your trades.

🚀 Points of Innovation

First indicator specifically designed for SMC-based post-trade review rather than live signal generation

Dual-mode analysis system allowing both dynamic scrollback and precise date selection

Expansion-aware classification algorithm that weighs range position against net displacement

Real-time efficiency metrics calculating directional quality of price movement

Integrated visual FVG detection within the analysis window only

Interactive table with clickable date range adjustment via chart interface

🔧 Core Components

Pivot Detection Engine: Uses configurable pivot length to identify significant swing highs and lows for structure break detection

Window Calculator: Determines active analysis zone based on either bar offset or timestamp boundaries

Data Aggregator: Tracks window open, high, low, close and counts bullish/bearish structure break events

State Classification Algorithm: Applies hierarchical logic to determine market state from six possible classifications

Visual Renderer: Draws structure breaks, FVG boxes, and window highlighting within the active zone

🔥 Key Features

Sliding Window Mode: Use the Scroll Back slider to dynamically move your analysis zone backwards through history bar-by-bar

Date Range Mode: Select specific start and end timestamps for precise session or trade review

Six Market State Classifications: Parabolic Expansion (Bull/Bear), Bullish/Bearish Order Flow, Accumulation/Distribution Reversal, and Consolidation/Inducement

Range Position Percentile: See exactly where price closed relative to the window’s high-low range as a percentage

Bull/Bear Event Counter: Quantified count of structure breaks in each direction during the analysis period

Efficiency Calculation: Net move divided by total range reveals trending quality versus chop

🎨 Visualization

Blue Window Highlight: Active analysis zone is clearly marked with blue background shading on the chart

Structure Break Lines: Dashed lines appear at each bullish or bearish structure break within the window

FVG Boxes: Fair Value Gaps automatically render as semi-transparent boxes in bullish or bearish colors

Dashboard Table: Top-right positioned table displays State, Analysis description, and Metrics in real-time

Color-Coded States: Each classification uses distinct coloring for immediate visual recognition

Interactive Tip Row: Optional help text guides users on clicking the table to adjust date range

📖 Usage Guidelines

General Configuration

Analysis Mode: Default is Sliding Window. Choose Date Range for specific timestamp analysis.

Sliding Window Settings

Scroll Back (Bars): Default 0. Increase to move window backwards into history.

Window Width (Bars): Default 100. Range 20-50 for scalping, 100+ for swing analysis.

Date Range Settings

Start Date: Select the beginning timestamp for your analysis period.

End Date: Select the ending timestamp for your analysis period.

Visual Settings

Show Help Tip: Default true. Toggle to hide instructional row in dashboard.

Bullish Color: Default teal. Customize for bullish elements.

Bearish Color: Default red. Customize for bearish elements.

SMC Parameters

Pivot Length: Default 5. Lower values (3-5) catch minor breaks. Higher values (10+) focus on major swings.

✅ Best Use Cases

Post-trade review to understand why entries succeeded or failed

Session analysis to identify institutional activity patterns

Trade journaling with objective algorithmic classifications

Pattern recognition training through historical scrollback

Identifying whether stop hunts were inducements or legitimate breaks

Comparing your real-time read versus what the algorithm detected

⚠️ Limitations

Designed for historical analysis only, not live trade signals

Classification accuracy depends on appropriate pivot length for the timeframe

FVG detection uses simple gap logic without mitigation tracking

State classification is based on window data only, not broader context

Requires manual scrolling or date input to review different periods

💡 What Makes This Unique

Purpose-Built for Review: Unlike most indicators focused on live signals, this is designed specifically for post-trade analysis

Expansion-Aware Logic: Algorithm weighs both position in range AND directional efficiency for accurate state detection

Interactive Date Control: Click the dashboard table to reveal draggable anchors for window adjustment directly on chart

🔬 How It Works

1. Window Definition:

User selects either Sliding Window or Date Range mode

System calculates which bars fall within the active analysis zone

Active zone receives blue background highlighting

2. Data Collection:

Algorithm captures window open, running high, running low, and current close

Structure breaks are detected when price crosses above last pivot high or below last pivot low

Bullish and bearish events are counted separately

3. State Classification:

Range Position calculates where close sits as percentage of high-low range

Efficiency calculates net move divided by total range

Hierarchical logic applies priority rules from Parabolic states down to Consolidation

4. Output Rendering:

Dashboard table updates with State title, Analysis description, and Metrics

Visual elements render within window only to keep chart clean

Colors reflect bullish, bearish, or neutral classification

💡 Note:

This indicator is intended for educational and review purposes. Use it to develop your understanding of Smart Money Concepts by analyzing what institutional order flow looked like during historical periods. Combine insights with your own analysis methodology for best results.

ETF-Futures Opening Ratio (Table)This indicator calculates the opening price ratio between an ETF and its corresponding futures contract using the 9:30 AM New York (RTH) opening price.

The ratio is locked at the official market open and remains fixed throughout the session, providing a stable reference for:

Translating ETF price levels into futures equivalents

Comparing relative value and premium/discount behavior

Maintaining consistent cross-instrument analysis during the trading day

The output is displayed in a simple on-chart table for quick reference and minimal chart clutter.

Universal Moving Average🙏🏻 UMA (Universal Moving Average) represents the most natural and prolly ‘the’ final general universal entity for calculating rolling typical value for any type of time-series. Simply via different weighting schemes applied together, it encodes:

Location of each datapoint in corresponding fields (price, time, volume)

Informational relevance of each datapoint via using windowing functions that are fundamental in nature and go beyond DSP inventions & approximations

Innovation in state space (in our case = volatility)

The real beauty of this development: being simply a weighting scheme that can be applied to anything: be it weighted median , weighted quantile regression, or weighted KDE , or a simple weighted mean (like in this script). As long as a method accepts weights, you can harness the power of this entity. It means that final algorithmic complexity will match your initial tool.

As a moving ‘average’ it beats ALMA, KAMA, MAMA, VIDYA and all others because it is a simple and general entity, and all it does is encoding ‘all’ available information. I think that post might anger a lot of people, because lotta things will be realized as legacy and many paywalls gonna be ignored, specially for the followers of DSP cult, the ones who yet don’t understand that aggregated tick data is not a signal omg, it’s a completely different type of time series where your methods simply don’t fit even closely. I am also sorry to inform y’all, that spectral analysis is much closer to state-space methods in spirit than to DSP. But in fact DSP is cool and I love it, well for actual signals xD

...

Weights explained & how to use them: as I already said, the whole thing is based on combining different set of weights, and you can turn them on/off in script settings. Btw I've set em up defaults so you can use the thing on price data out of the box right away.

Price, Time, Volume weights: encode location of every datapoint in Price & TIme & Volume field

Howtouse: u have to disable one weight that corresponds to the field you apply UMA to. E.g if you apply UMA to prices, you turn off price weighting And turn on time and volume weighting. Or if you apply UMA to volume delta, you turn off volume weighting And turn on price and time weighting.

Higher prices are more important, this asymmetry is confirmed and even proved by the fact that prices can’t be negative (don’t even mention that incorrect rollover on CL contract in 2k20...).

Signal weights: encode actuality/importance/relevance of datapoints.

Howtouse: in DSP terms, it provides smoothing, but also compensates for the lag it introduces. This smoothness is useful if you use slope reversals for signal generation aka watching peaks and valleys in a moving average shape. It's also better to perturb smoothed outputs with this , this way you inject high freq content back, But in controlled way!

Signal = information.

The fundamental universal entity behind so-called “smoothing” in DSP has nothing to do with signals and goes eons beyond DSP. This is simply about measuring the relevance of data in time.

First, new datapoints need some time to be “embedded” into the timeline, you can think of it as time proof, kinda stuff needs time to be proved, accepted; while earliest datapoints lose relevance in time.

Second, along with the first notion, at the same time there’s the counter notion that simply weights new data more, acting as a counterweight from the down-weighting of the latest datapoints introduced by the first notion.

The first part can be represented as PDF of beta(2, 2) window (a set of weights in our case). It’s actually well known as the Welch window, that lives in between so called statistical and DSP worlds, emerges in multiple contexts. Mainstream DSP users tho mostly don’t use this one, they use primitive legacy windowing function, you can find all kinds on this wiki page.

Now the second part, where DSP adepts usually stop, is to introduce the second compensating windowing function. Instead they try to reduce window size, or introduce other kinds of volatility weights, do some tricks, but it ain’t provides obviously. The natural step here is to simply use the integral of the initial window; if the initial window is beta(2, 2) then what we simply need is CDF of beta(2, 2), in fact the vertically inverted shape of it aka survival function . That’s it bros. Simply as that.

When both of these are applied you have smth magical, your output becomes smooth and yet not lagging. No arbitrary windowing functions, tricks with data modification etc

Why beta(2, 2)? It naturally arises in many contexts, it’s based on one of the most fundamental functions in the universe: x^2. It has finite support. I can talk more bout it on request, but I am absolutely sure this is it.

^^ impulse response of the resulting weighs together (green) compared with uniform weights aka boxcar (red). Made with this script .

Weighing by state: encodes state-space innovation of each datapoint, basically magnitude of changes, strength of these changes, aka volatility.

Howtouse: this makes your moving average volatility aware in proper math ways. The influence of datapoints will be stronger when changes are stronger. This is weighting by innovations, or weighting by volatility by using squared returns.

Why squared returns? They encode state‑space innovations properly because the innovation of any continuous‑time semimartingale is about its quadratic variation, and quadratic variation is built from squared increments, not absolute increments.

Adaptive length is not the right way to introduce adaptivity by volatility xD. When you weight datapoints by squared returns you’re already dynamically varying ‘effective’ data size, you don’t need anything else.

...

It’s all good, progress happens, that’s how the Universe works, that's how Universal Moving Average works. Time to evolve. I might update other scripts with this complete weighting scheme, either by my own desire or your request.

...

∞

Portfolio P&L Table 10 SlotsOverview

This indicator displays a compact, Excel-style position P&L table directly on your TradingView chart. It is designed to help traders track unrealized profit/loss for a manually-entered position and ensure the calculations only apply to the symbols you actually trade, preventing confusion when switching between tickers.

The script is symbol-aware: it checks the current chart symbol against up to 10 user-defined position slots and shows P&L only when a match is found.

Core Concept

Most P&L scripts on TradingView rely on a single set of inputs (average price, quantity), which remains active even when the user changes chart symbols. That can lead to incorrect P&L displays on instruments where no position exists.

This indicator solves that by combining:

Symbol matching logic (ticker / exchange:ticker / base ticker normalization)

Slot-based position storage (up to 10 positions)

Dynamic real-time P&L calculations driven by the chart’s live price

As a result, the table behaves like a “position panel” that follows the chart, while respecting your actual holdings list.

Matching & Display Logic

Symbol Detection

The indicator compares the current chart symbol to each slot’s symbol using multiple matching methods to reduce false mismatches:

Full symbol (EXCHANGE:TICKER)

Ticker only (TICKER)

Normalized “base ticker” extraction (useful when your chart format differs from inputs)

Position Selection

The first matching slot is selected and displayed.

If no slot matches, the table shows “No position for this symbol” and does not output P&L values.

P&L Calculation Logic

When a valid slot is matched and its values are valid:

Unrealized Gross P&L

Long: (Last Price − Avg Price) × Quantity

Short: (Avg Price − Last Price) × Quantity (handled via direction multiplier)

Unrealized Net P&L (optional)

If fees are enabled, the script subtracts the slot’s total fees from gross P&L.

P&L %

Calculated relative to average price, direction-adjusted for long/short positions.

Breakeven Price

Without fees: breakeven = average price

With fees: breakeven is adjusted using fees / quantity and direction.

The table updates automatically with market movement because all values are recalculated from the chart’s current price.

Inputs and Defaults

General

Include Fees? (default: Off)

Text Size

Table Position (Top/Bottom, Left/Right)

Slots (1 → 10)

Each slot contains:

Symbol (example formats: NVTS, NASDAQ:NVTS, NYSE:PATH)

Side (Long / Short)

Average Price

Quantity

Total Fees (optional; applied only when “Include Fees” is enabled)

Colors (Fully Customizable)

The table supports user-defined colors for:

Header text/background

Body text/background

Positive P&L color

Negative P&L color

Neutral/no-position color

This allows you to match the table visually to any chart theme.

The indicator is intended for :

Quick P&L visibility while charting

Avoiding accidental P&L “carry over” when switching symbols

Tracking a shortlist of positions without external spreadsheets

If you trade more than 10 tickers regularly, the script can be extended further using the same slot architecture.

Limitations

Values are unrealized and based on the chart’s price (close/last available feed).

The script does not track multiple lots per symbol automatically; each slot represents a single consolidated position (avg + total qty).

Disclaimer

This script is provided for educational and analytical purposes only. It does not constitute financial advice, investment recommendations, or an invitation to trade. Trading involves risk, and past performance does not guarantee future results. Always verify your position data and calculations independently before making trading decisions.

Binance futures Funding Rate Sentiment ZonesHello,

This script is pretty much self explanatory.

Instead of having to have Binance open to check the Funding rate for futures USDT coins, it is shown in TradingView.

There are multiple colors that are shown:

-0.05% to 0.05% = neutral funding, no color on background

-+0.05% to -+0.1% = transition zone, long/short population increasing/decreasing

-+0.1% to -+ 2% = extreme positive / negative funding, red color

Dynamic EMA Trend Table [Customizable]Overview

The Dynamic EMA Trend Table is a comprehensive dashboard designed to give traders an instant overview of the market trend across five distinct Exponential Moving Averages (EMAs). Instead of cluttering your chart with multiple lines, this script organizes the data into a clean, customizable table, allowing you to assess trend alignment at a glance.

How It Works

This indicator calculates five user-defined EMAs (defaulting to the popular 5, 20, 50, 100, and 200 periods). It then compares the Current Price against each EMA value to determine the immediate trend status:

Bullish State: When the current price is above the specific EMA, the table cell turns Green (customizable).

Bearish State: When the current price is below the specific EMA, the table cell turns Red (customizable).

This logic allows swing traders and scalpers to instantly see if the asset is in a strong uptrend (all cells Green), a strong downtrend (all cells Red), or a consolidation phase (mixed colors).

Key Features

Fully Customizable Periods: Change the length of all 5 EMAs to fit your specific strategy (e.g., Fibonacci numbers or standard Swing Trading settings).

Dynamic UI: Position the table anywhere on the screen (Top/Bottom/Left/Right) and adjust the size to fit your screen resolution.

Visual Cleanliness: You can choose to show the table only, or toggle the "Show EMAs on Chart" option to plot the actual lines on your chart.

Smart Coloring: The lines on the chart (if enabled) inherit the same color logic as the table—turning Green when price is above them and Red when price is below.

Settings & Configuration

Price Source: Select Close, High, Low, etc. (Default is Close).

Table Position & Size: Customize where the dashboard appears.

EMA Lengths: Set your 5 preferred lookback periods.

Color Theme: Fully adjustable colors for Bullish, Bearish, Neutral, and Background elements to match your chart theme (Dark/Light mode friendly).

Use Case Example

Trend Confirmation: A trader looking for a "Buy" entry might wait for the short-term EMAs (5 and 20) and the medium-term EMA (50) to all turn Green in the table before entering.

Support/Resistance Watch: By quickly glancing at the values in the table, you can see exactly where the 200 EMA sits without needing to scroll back on your chart to find the line.

Daily candle separation + NY open + First hour open Daily candle separation + NY open + First hour open

High/Low Tracker ARDR/ADR V4High and lows in 2 timeframes

16:00 -> 03:55

19:30 -> 02:55

Toggle on/off of

- Auto extending untill 09:25

- Live updating during price action

Configure linestyles, box styles

It is now displaying correctly for both CL and ES

Position Avg Line + P/L Table - SightLine LabsPosition Avg – SLL is a lightweight position-tracking indicator designed to display a persistent average price level on the chart along with a real-time position summary table.

This script is non-trading and does not generate signals, entries, or exits. It is intended strictly for position awareness and visual reference.

What this indicator does:

Plots a persistent horizontal average price line (dashed by default)

Displays a live position statistics table showing:

Shares owned

Average price

Current price

Unrealized profit/loss in dollars

Unrealized profit/loss in percent

Updates automatically as price changes

Works across all timeframes

Does not depend on broker integration or strategy logic

Key features:

Average Price Line:

User-defined average price input

Persistent across the entire chart

Adjustable color and width

Visibility toggle

Position Table:

Six selectable table positions:

Top Left, Top Center, Top Right, Bottom Left, Bottom Center, Bottom Right

Adjustable text size (Tiny through Huge)

Optional table background fill

Optional inner grid lines

Optional outer frame border

Independent color control for:

Header background

Header text

Value text

Positive and negative P/L values

Chart Overlay Options:

Optional chart background tint

Does not modify the global chart theme

Inputs overview:

Position Settings:

Shares Owned

Average Price

Visual Settings:

Show or hide average price line

Line color and width

Table Settings:

Table position

Table text size

Color Settings:

Header background and text colors

Value text color

Positive and negative P/L colors

Optional table background, grid, and frame colors

How to use:

Add the indicator to a chart

Open the settings panel

Enter the number of shares and the average price

Adjust table position, size, and colors as desired

Use the average price line and table as a visual reference for trade and risk management

Notes and limitations:

This indicator does not place trades

It does not connect to any broker

All values are manually entered

Unrealized P/L is calculated using the chart’s current price

Commissions, fees, and slippage are not included

Disclaimer:

This script is provided for educational and informational purposes only. It does not constitute financial advice, investment recommendations, or trade signals. All trading decisions are the sole responsibility of the user.

Developed by SightLine Labs.

Luis-Enrico Mag7 PerformanceTracks daily & weekly performance (1-4W) of Magnificent 7 stocks (GOOG, AAPL, AMZN, META, MSFT, NVDA, TSLA) in a compact table.

Key Features:

Daily chart only (uses 5 trading days = 1 week)

Day % + 1/2/3/4 Week returns

Color-coded (green/red)

Bottom-left position

Optimized (7 security calls only)

Quantum Elasticity Overview: Quantum Elasticity is a sophisticated Mean Reversion Engine based on the law of statistical probability. It models market price action as an elastic system that revolves around a dynamic equilibrium point (Linear Regression).

The Core Logic: Markets are rarely efficient. When price deviates significantly from its historical mean, it creates "Statistical Tension." This script measures that tension using dynamic standard deviation envelopes (Sigma Bands).

Equilibrium: The center line represents the fair value of the asset.

Elasticity Zones: When price enters the "Extreme" bands, the probability of a snap-back towards the mean increases exponentially.

Unique Features:

Non-Lagging Linear Regression: Unlike SMA/EMA, our equilibrium line adapts to the slope of the trend without the heavy lag of traditional indicators.

Dynamic Tension Index: The built-in HUD displays the real-time elasticity of the market, helping traders identify exhaustion points.

Reversion Alerts: "REVERT" signals appear when the market reaches a 1.5x Sigma deviation, indicating a critical oversold/overbought state.

How to obtain access: This is an "Invite-only" script. To gain access, please visit my profile or send a private message for subscription details.

Vol BO/BD + Profitsthis is basis Profit line crossover above Volume basis VWAP.

Long at crossover and exit at crossunder

Trade responsibly

StratyPro Signal + ExitStratyPro Signal + Exit — Description

StratyPro is an intraday market-flow framework built around liquidity behavior, session timing and structural shifts. Instead of combining public indicators, StratyPro uses its own unified engine that monitors:

• Accumulation ranges formed during the early session

• Liquidity events when price reaches key levels and rejects

• Structural shifts based on pivot swings

• Momentum confirmation after structural breaks

• Higher-timeframe inefficiency zones (price speed / imbalance areas)

• Session-specific conditions for Core Session and Expansion Session

The objective is to provide a logical roadmap of how price transitions from accumulation → manipulation → expansion during the trading day.

--------------------------------------------------------------------

1. Session Framework

StratyPro operates using three phases:

1. Asia Accumulation Phase

- Builds the core accumulation range

- Builds an extended reference range used later by the Expansion Session

2. Pre-Core Phase

- Tracks a local intraday range before the main session

- Detects liquidity taps or sweeps of this range

3. Core Session (London)

- Primary signal window where the engine evaluates directional intent

4. Expansion Session (New York)

- Secondary session logic for continuation or reversal during the afternoon

--------------------------------------------------------------------

2. Liquidity Events and Key Levels

StartyPro identifies multiple types of liquidity behavior:

• Sweeps of the Asia accumulation range

• Sweeps of the extended reference range

• Sweeps of the pre-session intraday range

• Equal-high and equal-low clusters that attract price and later reject

A liquidity event is confirmed when price trades beyond a key level and then returns back into the range.

Users can decide whether:

• Liquidity events are required for signals

• Only the side where liquidity was taken should be traded

• Both sides can be considered

--------------------------------------------------------------------

3. Structural Shifts and Momentum Confirmation

The engine monitors local structure using pivot-based swing points. A directional shift occurs when price closes beyond a previous swing level.

This shift is validated only if accompanied by a momentum candle (a body significantly larger than recent average).

The user can select aggressive, standard, or defensive confirmation modes.

These momentum-based signals are independent from zone-based signals.

--------------------------------------------------------------------

4. Inefficiency / Imbalance Zones (Higher Timeframe Mapping)

StratyPro maps areas where price moved too quickly (inefficiency zones) on a higher timeframe.

These zones:

• Are detected using multiple gap-based models

• Have a maximum lifetime

• Are invalidated if price fully trades through

• Are visualized with dynamic boxes extended forward

Optional signal conditions allow:

• Tap + rejection within an active zone

• Session window confirmation

• Liquidity-based directional filters

--------------------------------------------------------------------

5. Equilibrium

StratyPro calculates an equilibrium level for each session based on the midpoint of either:

• The Asia accumulation range, or

• The most recent structural swing range

Users can restrict signals so that:

• Shorts only trigger above equilibrium

• Longs only trigger below equilibrium

This helps avoid entries in the inefficient half of the range.

--------------------------------------------------------------------

6. Signal Types

There are two main signal types inside each session:

1. Zone-Based Signals

- Price interacts with an active inefficiency zone

- Liquidity event is confirmed

- Price rejects the zone

- Session window is active

2. Momentum-Based Signals

- A structural shift is confirmed

- A momentum candle supports the move

- Liquidity/equilibrium conditions are met

- Session window is active

Long and short signals are plotted clearly on the chart with directional labels.

--------------------------------------------------------------------

7. Alerts

SP includes alerts for:

• Zone-based long/short signals

• Momentum-based long/short signals

• Core Session events

• Expansion Session events

Each alert matches the exact visual signal on chart.

--------------------------------------------------------------------

Recommended workflow:

1. Observe how the Asia range forms initial liquidity.

2. Watch for liquidity grabs before the main session.

3. Use inefficiency zones as primary interest areas.

4. Use session timing as the main filter.

5. Apply your own risk management alongside the signals.

Stratypro is a structural mapping tool intended for experienced traders. It does not constitute financial advice.

R Factor Advanced Stock Activity Ranking (Experimental) R Factor (relative factor) is a custom logic based 'momentum ranking' parameter, which measures intensity of intraday momentum and volatility. This parameter compared today's activity from last 20 days activity and ranks the stocks according to the intensity of the momentum.

Why momentum ranker?

Because traditional %change sorts intraday stock which show momentum in ascending order of value of % change, for example 3%, 2.5 %, 1% etc. But momentum ranker does not use % change as a sorting parameter for top gainers, or losers. It ranks the stocks, regardless of the direction, according to the intensity it is showing. The value of the momentum ranking has no meaning of itself, just understand that higher the value of momentum ranker, the more intensity the stock is showing.

In this indicator we can only scan 40 F&O stock of Indian Stock Market. This indicator is to be used only on 5 min timeframe.

Tip: Do not change any values in the settings otherwise, the indicator won't work as expected.

Also after applying the indicator, your canvas will shrink, manually fix it by stretching from Y axis, a table will appear showing top 20 stocks. Some times the indicator will glitch & show incorrect names of stocks, refresh the Tradingview website to fix this. Best used on a PC.

Disclaimer/Warning:

This parameter is inspired by TradeFinder and is an attempt to study the momentum of the stocks. This indicator in no way attempts to copy features of the TradeFinder software, this is purely an experimental Indicator, for the people who cannot afford to buy a trading software. This indicator does not provide Buy/Sell signals or nor is an investment advice. This indicator solely for the purpose of study of price and its momentum. Users are responsible for their own actions, profit/loss of the users is not the liability of author.

Elite Net Cash by Mashrab🚀 Elite Net Cash Dashboard code by Mashrab

Stop switching tabs. Get the full fundamental picture instantly.

This dual-panel dashboard puts institutional-grade data right on your chart. It splits the "heavy math" from the "market context," giving you a clean, professional view of a company's true value and trading personality.

🔥 Why You’ll Love It

Two Smart Tables:

Financials: See the health check immediately—Net Cash, Cash Backed %, Free Cash Flow, and Revenue Growth.

Profile: Know who you are trading—Market Cap (with auto-class like "Mega" or "Small"), Volatility (ADR), and Sector.

Auto-ETF Mapping: It automatically tags the sector with its matching ETF (e.g., Technology (XLK)). Perfect for quickly checking relative strength!

Volatility Alerts: The ADR (Average Daily Range) turns Yellow if the stock moves more than 5% a day. Know the risk before you size your position.

Minimalist Mode: Want a clean chart? Uncheck the "Borders" box in settings for a sleek, text-only floating display.

🎯 How to Trade It

Check the Green: Look at the Financials table. Green numbers mean the company is cash-rich and growing.

Check the Moves: Look at the Profile table. High ADR means expect wild swings; Mega Cap means steady stability.

Check the Sector: Use the ETF tag to see if the whole industry is moving or just this stock.

⚙️ Make It Yours

Split the View: Put Financials top-right and Profile bottom-right (or anywhere else).

Style It: Toggle borders on/off and pick your colors.

[iQ]PRO Pricing Levels+PRO Pricing Levels+ Analysis

Summary

A comprehensive institutional-grade market profile and liquidity analysis tool designed for professional traders who focus on price delivery and volume distribution. It identifies high-probability reaction zones by blending historical interaction density with advanced mathematical modeling.

How It Works

The script utilizes a proprietary multi-layered engine to map the "DNA" of recent price action. It functions by scanning a user-defined lookback window to identify specific price coordinates where the market has historically shown significant interest or exhaustion.

Methodology: The core logic evaluates "Price-Density" It doesn't just look at where price has been, but calculates the quality of those interactions by weighing them against volume intensity and recency. This creates a "Heatmap" of structural importance.

Model Engine: The tool incorporates a sophisticated classification system that identifies the current "Market Model" (such as Expansion, Reversion, or Compression). This helps traders distinguish between a trending market and a mean-reverting one.

Statistical Deviations: Beyond standard support and resistance, the script projects dynamic expansion levels based on the volatility of the analyzed range, identifying potential "statistical exhaustion" points.

Liquidity Mapping: It automatically detects internal and external liquidity sweeps, providing real-time feedback on whether the current move is a genuine breakout or a sophisticated stop-hunt.

Key Features

Dynamic PD Heatmap: Visually represents price density and interaction quality through a color-coded histogram.

Advanced Model Engine: Automatically classifies market phases (e.g., "MM Reversal" or "Expansion") to align your bias.

Volume-Weighted Weighting: Filters out "fake" price movements that occurred on low participation.

Premium/Discount Zones: Integrated equilibrium mapping to ensure you are never buying at the top of a range or selling at the bottom.

Chaos Filtering: An advanced algorithmic filter designed to minimize noise and highlight only the most structurally sound levels.

How to Use

Step 1: Define the Range: Adjust the Lookback Length to match your trading style (shorter for scalping, longer for swing trading).

Step 2: Identify the POC: Look for the "Point of Control" (POC) markers. These levels represent the highest density of historical interaction and often act as "magnets" for price.

Step 3: Monitor the Model Label: Use the Market Model label to determine if you should be looking for trend-following entries or reversal setups.

Step 4: Execute at Liquidity Zones: Look for price to interact with the "💧" markers or high-multiplier deviation lines for potential exhaustion-based entries.

Settings & Configuration

Core & Range Definition: Customize the lookback period and price source for level generation.

PRD Level Calculation: Switch between ATR, Percentage, or Fixed Point steps to determine how granular the price map should be.

Range Deviations: Configure multiple multipliers to project potential overextension zones.

Model Engine: Toggle the advanced "Chaos Filter" and "RAV Weighting" to adjust the sensitivity of the probability calculations.

Visualization: Enable or disable the Heatmap, Summary Table, and Regression Channels to suit your chart layout.

Past does not guarantee future results.

For Research and study!

Enjoy, MMiQ.

Stochastic Oscillator (Arrows 20/80)Arrows added to study to indicate when the D line is crosses the 20 and 80 line

MartinGale Average Simulator - By LowisOriginality and Utility

This script is not a traditional indicator nor a cosmetic variation of existing tools such as moving averages, oscillators, or common indicator combinations. It is a deterministic averaging and risk modeling engine, specifically designed to simulate, analyze, and validate multi-order averaging (DCA) structures under fully configurable conditions.

The originality of this script lies in the fact that it does not generate trade signals and does not attempt to predict market direction. Instead, it models the mathematical behavior of an entire chained order structure, allowing the user to quantitatively evaluate how an averaging strategy behaves as price evolves.

The script continuously computes and displays:

The dynamic average entry price after each additional order.

The progressive position size growth as orders are added.

The total capital committed, factoring in leverage.

The individual PnL per order and the aggregated PnL of the entire structure, both in absolute and percentage terms.

The real account usage percentage as the averaging sequence progresses.

The sensitivity of the structure to changes in the current or simulated price.

Unlike classic indicators that operate on historical price data to infer probabilities, this tool functions as a deterministic planning and risk-audit system. Its purpose is to help traders answer structural questions that standard indicators do not address, such as:

How much capital is actually committed by the time the Nth order is reached.

The exact resulting average price given a custom percentage distribution across orders.

The structural drawdown required before an averaging strategy becomes profitable.

How changes in leverage, number of orders, or percentage distribution affect overall risk exposure.

The script allows full user control over key parameters, including:

Number of averaging orders.

Custom percentage offsets per order.

Account capital and leverage.

Entry price and current/simulated price.

Decimal precision for price and asset quantity.

Clear visualization through tables and price-level graphics.

This makes the script a trade engineering and risk modeling tool, rather than a signal-based indicator. Its value lies in structural analysis and execution planning, a category not covered by standard open-source scripts in the public library.

The source code is intentionally kept private because the internal averaging, position-sizing, and risk-accumulation engine represents proprietary logic that can be directly reused for commercial products or automated systems. Disclosing this implementation would allow immediate replication without providing additional educational or functional value to the end user, who already has full operational control through exposed inputs.

For these reasons, the script is functionally original, technically useful, and fully justifies closed-source protection, in compliance with TradingView’s publication guidelines.

🔧 How the Indicator Works (Technical Overview)

This indicator implements a deterministic averaging (DCA) simulation engine designed to accurately model the mathematical, financial, and percentage-based behavior of a leveraged position composed of multiple sequential orders.

Unlike traditional indicators that only display static levels or visual signals, this script reconstructs the full internal structure of a position, order by order, allowing the user to analyze its complete evolution under different price scenarios.

📌 Entry Price Calculation per Order

Starting from an initial entry price, the user defines a set of percentage-based distances for each averaging order.

Each new entry price is calculated as:

A percentage deviation relative to the original entry price

Adjusted by trade direction (long or short)

Dynamically rounded according to user-defined price precision

As a result, each order has an independent, deterministic, and reproducible price, without relying on external data or real trade execution.

📌 Position Size and Capital Usage Calculation

For every order, the engine computes:

Asset quantity acquired based on allocated capital and leverage

Actual margin used considering leverage

Progressive accumulation of total deployed capital

Account capital usage percentage per order and in total

This allows the trader to clearly visualize how real account exposure grows as additional averaging orders are added — something that is not evident in standard DCA tools.

📌 Average Entry Price Recalculation

After each new order, the indicator recalculates the weighted average entry price of the entire position by combining:

The previous average price

The new entry price

The updated total asset quantity

This accurately reflects how the real break-even level evolves as the position is averaged, which is critical for aggressive averaging or martingale-style strategies.

📌 Individual and Cumulative PnL Computation

The script supports two evaluation modes:

Current market price

User-defined simulated price, intended for hypothetical or stress-test scenarios

Using the selected price, the indicator calculates:

Individual PnL per order

Total cumulative PnL of the position

PnL percentage relative to the capital used in each order

PnL percentage relative to total deployed capital

Each order maintains its own mathematical identity, avoiding common errors where PnL is diluted or calculated solely against the averaged price.

📌 Structured and Objective Visualization

All calculations are represented through:

Independent horizontal price lines per order

Informational labels anchored to their corresponding price levels

Tabular summaries displaying the exact state of each order, row by row

No classical indicators, predictive signals, or discretionary filters are used.

The system is 100% mathematical, deterministic, and reproducible.

📌 Purpose and Practical Utility

This indicator is designed to:

Evaluate the mathematical viability of averaging schemes

Analyze real leverage-based risk exposure

Compare price scenarios before execution

Understand how small price movements affect large accumulated positions

Identify points where capital usage becomes inefficient or dangerous

It does not execute trades and does not generate trading signals.

Its purpose is structural position analysis, not prediction.

🧭 How to Use the Indicator (Step-by-Step Guide)

This indicator does not require prior trading experience to be used.

It operates entirely through configurable parameters and updates automatically in real time.

1️⃣ Define the Initial Entry Parameters

Start by setting the initial entry price.

This value represents the price at which the first position entry is opened.

Next, define:

Account capital: the total available capital

Entry percentage: the percentage of the account used in the first order

The indicator automatically calculates:

Capital invested

Asset quantity acquired

Real position exposure

2️⃣ Select the Position Direction

Choose whether the position is:

Long (benefits from price increases), or

Short (benefits from price decreases)

This selection automatically adjusts:

Price movement direction

PnL calculations

Averaging percentage behavior

No additional configuration is required.

3️⃣ Configure Leverage and Number of Orders

Set the leverage used for the position.

This value is applied to calculate:

Required margin per order

Total exposure relative to account capital

Then, specify the number of averaging orders.

Each order represents an additional entry that would be placed if price moves against the position.

4️⃣ Define Averaging Percentages

Enter the percentage offsets for each averaging order, separated by commas.

Example:

4, 8, 13, 19, 39, 54

Each value represents how far (in percentage terms) price must move from the original entry before adding a new order.

The indicator automatically calculates:

Exact price level of each order

Updated average entry price

Capital deployed per order

Total capital usage

5️⃣ (Optional) Set a Simulated Price

Optionally, a simulated price can be defined.

This allows users to:

Evaluate hypothetical market scenarios

Analyze deep drawdowns

Simulate price recoveries

Study PnL behavior without waiting for live market movement

Any change to this value instantly recalculates all results.

6️⃣ Interpreting the Results

Once configured, the indicator displays in real time:

Individual order prices

Updated average entry price

Capital invested per order and in total

Individual and cumulative PnL

PnL percentage relative to deployed capital

No buttons or manual refresh are required.

Any parameter change updates the entire simulation automatically.

🎯 Important Notes

The indicator does not execute trades

No buy or sell signals are generated

All calculations are purely mathematical and deterministic

Its purpose is to visualize, analyze, and understand how a multi-entry averaging position behaves under different market conditions.

🔒 Closed-Source Justification

This script is published as closed-source because it implements a custom multi-order position simulation engine that goes beyond standard indicator calculations.

Internally, the script relies on a structured calculation framework that manages:

Order-to-order dependency

Cumulative capital usage across multiple entries

Dynamic average price recalculation

Individual and aggregated PnL modeling

State-aware recalculation logic tied to user-defined parameters

The value of the script resides not in isolated formulas, but in the overall architecture and calculation flow that coordinates these elements into a coherent position analysis model.