Multi Range VWAP PivotsMulti Range VWAP Pivots turned out to be one of my most accurate pivot indicators to date!

Multi Range VWAP Pivots works by recognizing the high and low of the timeframe selected (D, W, M, 6M, and 12M) and plotting range high to VWAP averages and range low to VWAP averages.

After further examination of each completed range, I came to the conclusion that due to the nature of averages, high and low respectively would need to be completed within the current range, for the averages to actually display pivots correctly. This means that if all averages appear to be "pivoting" correctly after or during a break lower of higher, then we can only assume the most recent break higher or lower could be exhaustion and price will be reverted to the mean (VWAP). OR, this could be the most accurate hindsight indicator on the planet.

*DISCLAIMER*: This indicator repaints. DO NOT backtest or set alerts with this indicator.

W-VWAP

High/Low Anchored VWAPHigh/Low Anchored VWAP simply plots an Anchored VWAP at High and Low, within a set range (D,W,M) , with a central "Basis" plot of the High and Low anchored VWAPs

*DISCLAMER* This indicator repaints. DO NOT set alerts or backtest using this indicator.

Musashi_HarmonicPricerMusashi HarmonicPricer was designed to my a tool for my personal trading strategy, and help me plot what I call ''Harmonic Structure', which is just a sophisticated way of using Fibonacci ratios based on the Elliott Wave Principle, Harmonic Patterns, and market structure.

- A distinctive element will be the integrated Fibonacci cluster tool, which plots automatically retracements and extensions of .272 (red) and .618 (purple) ratios, using the last two significant swings. For powerful usage, adjust the timeframes until they group into clusters or adjust the setup. You can also adjust the settings and select to plot only retracement, only extensions, both (default), the deviation (default = 7), and the historical approach.

- To be used wisely properly, you require multi-timeframe analysis, reason why you will find Monthly and Yearly VWAPs, as they won't change while you're switching timeframes, and fib-based EMAs to provide trend and dynamic support.

- Finally, the indicator will plot in price Hidden and Regular divergences for any oscillator you have on screen.

Have a good day.

VolumatrixVolumatrix is an enhanced volume weighted price indicator with advanced features

Created by CryptoJew & CryptoTiger on 04-06-2021

👋 Definition

Volumatrix turns current and historical price data into enhanced volume weighted price plots that allow you to visually grasp the momentum of any given market.

It’s easy to use and provides an accurate reading about an ongoing trend. This indicator is optimized to catch trend movements as soon as possible and to maximize certainty.

🙌 Overview

The Volumatrix indicator is based on an enhanced VWAP calculation, which serves as a present and upcoming price movement indication.

The further away the VWAP Wave is from the Zero Line, the more powerful the momentum is in that direction.

Conversely, the closer the VWAP Wave is to the Zero Line, the less momentum it has.

⭐️ Features

Volumatrix consists of the following features:

VWAP Waves: Visualizes the market's momentum in an easy-to-understand way by drawing colored waves.

VWAP Average: Acts as a calibration line for current wave movements.

Bearish & Bullish Dots: Indicates and confirms immediate trend changes by printing dual-colored dots.

E MA Backgrounds: Shows the general direction of the market, based on the exponential moving average (EMA).

In-depth alerts: Help traders discover potential trades with less time.

☝️ Basics

The Volume Weighted Average Price plays an essential role, as the Volumatrix indicator uses an enhanced VWAP calculation.

The volume weighted average price (VWAP) is a great technical trading indicator used by traders as it accounts for both price and volume.

VWAP signals the ratio of the cumulative share price to the cumulative volume traded over a given time.

It is essential because it provides traders with advanced insight into the trend and value of an asset.

Unlike moving averages, VWAP assigns more weight to price points with high volume.

This allows one to understand price points of interest, gauge relative strength, and identify prime entries/exits.

VWAP works with any interval: seconds, minutes, hours, days, weeks, months, years, etc...

However, keep in mind that VWAP can also experience some lag, much like a moving average.

Lag is inherent in the indicator because it's a calculation of an average using past data.

🧮 Calculation

Volume Weighted Average Price (VWAP) is constructed with two parameters, namely, price and volume, in 5 steps:

1. Calculate the Typical Price for the period.

((High + Low + Close)/3)

2. Multiply the Typical Price by the period Volume

(Typical Price x Volume)

3. Create a Cumulative Total of Typical Price

Cumulative(Typical Price x Volume)

4. Create a Cumulative Total of Volume

Cumulative(Volume)

5. Divide the Cumulative Totals

VWAP = Cumulative(Typical Price x Volume) / Cumulative(Volume)

🔍 Trend Identification - What to look for

VWAP is an excellent way to identify the trend of a market.

When using Volumatrix, you are looking for multiple confirmations that take place simultaneously.

The more confirmations that occur at the same time; the more certain the indicator will be.

You can identify the direction of a market by looking out for a few critical confirming signals.

📈 Bullish Trend Confirmations:

VWAP Wave overcrossing Zero Line :

When the VWAP Wave is crossing over the Zero Line, it indicates an immediate bullish trend.

This is one of the most certain moves that one can detect in Volumatrix.

This means that the price is about to change direction.

This is the case for any timeframe: seconds, minutes, hours, days, week, month, year, etc.

VWAP Wave color turning bullish:

When a bullish trend is about to happen, the VWAP Wave will change its color to yellow and finally to green.

That way, one can preemptively detect an upcoming bullish move.

In general, the VWAP Wave can change to 3 different colors.

Green means bullish.

Bullish Dots:

From time to time, bullish green dots will appear.

When combined with other indications, the Bullish Dots can be handy in confirming an upcoming or present uptrend.

That said, one should never solely rely on dots when deciding whether the trend is bullish or not.

Instead, if a trader sees a green dot, it should be taken as a hint to look for further bullish indications.

EMA Background:

One can identify the general trend of a market by looking at the background color of the indicator.

When the background is green, one can assume that a bullish trend is present.

The background color changes based on the exponential moving average (EMA).

By default, the 200 EMA is set. Change this value based on your timeframe preferences.

VWAP Average:

When the white VWAP Average line crosses above the Zero Line, it acts as an additional trend confirmation when combined with the VWAP waves.

As the VWAP average does not weigh in the short-term movements too heavily, it is less affected by immediate volatility.

Therefore, traders usually use the VWAP Average as a calibration tool to interpret the VWAP Waves more precisely.

📉 Bearish Trend Confirmations:

VWAP Wave under crossing Zero Line:

When the VWAP Wave is crossing under the Zero Line, it indicates an immediate bearish trend.

This is one of the most certain moves that one can detect in Volumatrix. This means that the price is about to change direction.

This is the case for any timeframe: seconds, minutes, hours, days, week, month, year, etc.

VWAP Wave turning bearish:

When a bearish trend is about to happen, the VWAP Wave will change its color to yellow and then finally to red.

That way, one can preemptively detect an upcoming bearish move. In general, the VWAP Wave can change to 3 different colors.

Red means bearish.

Bearish Dots:

From time to time, bearish red dots will appear.

When combined with other indications, the bearish dots can be handy in confirming an upcoming or present downtrend.

That said, one should never solely rely on dots when deciding whether the trend is bearish or not.

Instead, if a trader sees a red dot, it should be taken as a hint to look for further bearish indications.

EMA Background:

One can identify the general trend of a market by looking at the background color of the indicator.

When the background is red, one can assume that a bearish trend is present.

The background color changes based on the exponential moving average (EMA).

By default, the 200 EMA is set. Change this value based on your timeframe preferences.

VWAP Average:

When the white VWAP Average line crosses below the Zero Line, it acts as an additional trend confirmation if combined with the VWAP waves.

As the VWAP average does not weigh in the short-term movements too heavily, it is less affected by immediate volatility.

Therefore, traders usually use the VWAP Average as a calibration tool to interpret the VWAP Waves more precisely.

💤 Sideways Trend Confirmations:

VWAP Average:

When the VWAP Average is parallel and hovering around the Zero Line, either above or below it, that will indicate a sideways trend.

🚦 Usage - How and where to use it

The Volumatrix indicator is a universal indicator that works with any market capable of calculating a VWAP.

It’s currently being used in the following markets: cryptocurrency market, stock market, gold market and oil (just to name a few).

❗️ Requirements:

This indicator does not require any additional indicators as traders usually do in price action trading.

Basically, one just needs to follow the crossings, dots, and colors to get maximum certainty.

As a bonus, we recommend traders take advantage of TradingView’s multi-chart to catch more simultaneous confirmations.

🗣 Example Strategy: The 4 Timeframe Strategy

One can use the Volumatrix indicator along with the 4 timeframe strategy.

For example, open the 4 hour, 1 hour, 30 minute, and 5minute intervals simultaneously from left to right in a multi-chart layout.

Then lookout for the following conditions to meet:

OPEN LONG TRADE IF: On the 1-hour interval + 30-minute interval, Bullish Dots appear simultaneously

AND: On the 4-hour interval, the VWAP Wave is above the Zero Line

AND: On the 5-minute interval VWAP Wave is about to cross over the Zero Line or has already minimally crossed up.

OPEN SHORT TRADE IF: On the 1-hour interval + 30-minute interval, Bearish Dots appear simultaneously

AND: On the 4-hour interval VWAP Wave is below the Zero Line

AND: On the 5-minute interval VWAP Wave is about to cross under the Zero Line or has already minimally crossed down.

💡 Tips

Use TradingView’s 4-multi-chart layout to catch potential trades faster.

Use the indicator on a computer for optimal performance.

Set your computer screen to higher resolutions to get a better overview.

🔔 Alerts

With Volumatrix, you can use in-depth alerts like:

Bullish Dot

When a green dot at the bottom of the indicator appears

Bearish Dot

When a red dot at the bottom of the indicator appears

VWAP Wave Crossing Over Zero Line

When the VWAP Wave crosses over the Zero Line

VWAP Wave Crossing Under Zero Line

When the VWAP Wave crosses under the Zero Line

VWAP Wave Crossing Over Zero Line + Bullish Dot

When the VWAP Wave crosses over the Zero Line and a Bullish Dot appears

VWAP Wave Crossing Under Zero Line + Bearish Dot

When the VWAP Wave crosses over the Zero Line and a Bearish Dot appears

VWAP Average Crossing Over Zero Line

When the VWAP Average crosses over the Zero Line

VWAP Average Crossing Under Zero Line

When the VWAP Average crosses under the Zero Line

🔧 Settings

🔢 Inputs

These settings will change the behavior and outcome of the indicator.

EMA

Determines the number of previous candles that should be taken into calculation for the EMA background.

The value of the EMA can be changed to one's preferred value in accordance with the chosen interval.

The default value is 200.

🎨 Style

These settings will change the appearance of the indicator

VWAP Waves

Determines the color, opacity, thickness, and shape for the VWAP Waves.

The default shape is area.

The default colors are red, yellow & green.

VWAP Average

Determines the color, opacity, thickness, and shape for the VWAP Average.

The default shape is line.

The default color is white.

Zero Line

Determines the color, opacity, thickness, and shape for the Zero Line.

The default shape is a line.

The default color is white.

EMA Background

Determines the color & opacity for the Dynamic Background.

The default colors are black, red & green.

Bullish Dot

Determines the color, shape, opacity & location for the bullish dot.

The default shape is a circle.

The default color is green.

Bearish Dot

Determines the color, shape, opacity & location for the bearish dot.

The default shape is a circle.

The default color is red.

✅ Summary

Volumatrix is a unique indicator because, unlike many other VWAP tools, it's suited for simple as well as advanced analysis.

It’s a solid tool for immediately identifying the underlying trend of an asset.

Of course, this is true for any indicator based on the VWAP, which calculates an average using past data.

Still, Volumatrix is superior in this realm as it enhances the VWAP in its calculation and its visualization, while it comes with many advanced features.

❓ Questions

If you have any questions, just ask them here or in the Volumatrix community.

📚 Terminology

Bearish Dots: Red dots appearing at the bottom of the Volumatrix indicator.

Bullish Dots: Green dots appearing at the bottom of the Volumatrix indicator.

EMA: Exponential Moving Average - Tracks the price of an asset over time while giving more importance to recent price data.

Volume: A measure of how much of a given asset has traded in a period.

VWAP: Volume Weighted Average Price - The ratio of the value traded to total volume traded over time.

VWAP Average: Represents the average of the VWAP waves in the Volumatrix indicator.

VWAP Wave: The colorful waves representing the enhanced VWAP in the Volumatrix indicator.

Zero Line: It’s the indicator’s baseline and determines the beginning and end of a certain trend.

🙏 Acknowledgments

First, we would like to thank TradingView & PineCoders for this fantastic platform and technology.

We are also very grateful to our loyal trading community for constantly supporting our efforts.

We are looking forward to continuously improving this indicator for you.

CCI & EMA strategy by TradeswithashishThis strategy is extremely useful for positional traders or traders using timeframe 15-minute of higher. It uses following combo of values:

VWAP, CCI, Volume and Moving average (simple and exponential)

Caution:

Avoid taking trade if candle size is greater than twice the average candle size. for that wait for the retracement to near trailing stoploss

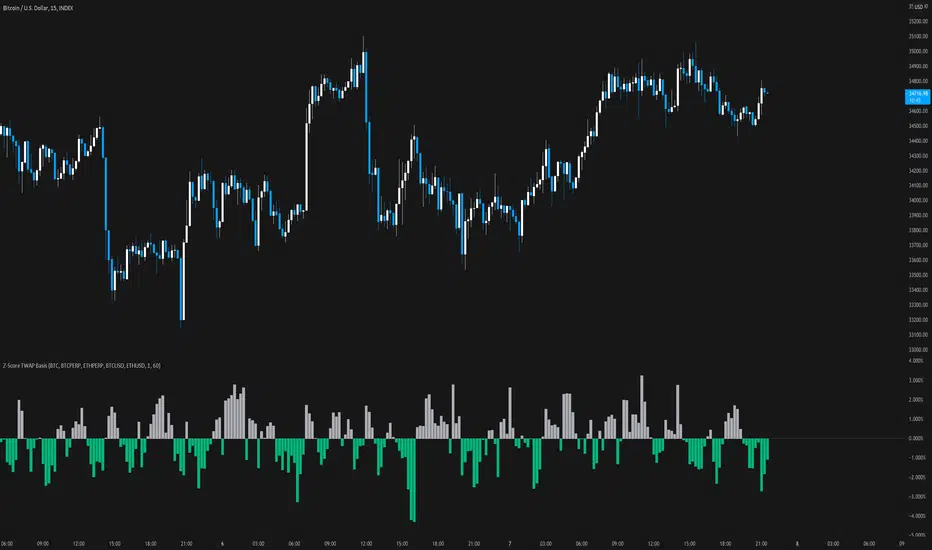

Z-Score TWAP BasisCONCEPT

Z-Score TWAP Basis shows the basis between spot and perpetual contracts, with the integration of the Z-Score algorithm.

FEATURES

In addition to the usual TWAP basis, the indicator uses the Z-Score.

BankNifty - VWAP + StdDev Bands- By Default the script draws Daily VWAP for Bank Nifty based on Futures Volume or underlying Index Stocks based on user input

- Optionally one may Anchor it to Week/Month etc or anchor it from a particular Time.

- It also draws 3 Standard Deviation Bands from the VWAP based on User Input.

- Optionally draws Previous VWAP Close for and Bullish or Bearish Move.

- It works with NIFTY 50 as well but only using Futures Volume(Pine limitation to number of security calls) . Please change the Symbol and Futures Volume symbol to "NSE:NIFTY" and "NSE:NIFTY1!" NSE:BANKNIFTY NSE:NIFTY

HYE Mean Reversion VWAPIndicator version of the strategy "HYE Mean Reversion VWAP"

"Long", "Short", "Exit Long" and "Exit Short" alarms added.

Use with "Once Per Bar Close".

*** I used the "VWAP with period" indicator code of @neolao. Special thanks to @neolao.

Indicator Link:

HYE Mean Reversion VWAP [Strategy]An RSI filtered version of PJ Sutherland's Jaws Mean Reversion algorithm using volume weighted average price (VWAP) instead of simple moving average (SMA).

"Long" on the close when;

1-) 2 period VWAP closes 3% or more below the 5 period VWAP ,

2-) 5 period exponential average of the 2 period RSI is below 30.

"Exit Long" on the close when;

1-) 2 period VWAP closes above the 5 period VWAP.

"Short" on the close when;

1-) 2 period VWAP closes 3% or more above the 5 period VWAP ,

2-) 5 period exponential average of the 2 period RSI is above 70.

"Exit Short" on the close when;

1-) 2 period VWAP closes below the 5 period VWAP.

*** You can change the needed percentage for long and short trades, periods of VWAPs and RSI levels.

*** You can select the trend direction: "Long Only" , "Short Only" or "Both". Default is "Long Only".

I used the "VWAP with period" indicator code of @neolao. Special thanks to @neolao.

Indicator Link:

VWAP AverageThe VWAP Average does NOT reset on a singular timeframe ie. daily, weekly etc. "Newsession" is based on input length on current session timeframe, just like any other moving average.

VWAP High/Low ChannelIn short, the VWAP High/Low Channel is based on VWAP "newsession" on swing high/low, with a basis of the two.

The VWAP High/Low channel seems to act like Bollinger bands or Donchain Channels when squeezing for a breakout, while also acting as a pivot after a breakout.

Trade Vertex - Bank Nifty Volume IndicatorNSE:BANKNIFTY

We all know that the value of an Bank Nifty is derived from top banking sector underlying stocks.

The value of Bank Nifty is calculated from free float market capitalization.

Using the same formula, I made an indicator on the bases of weighted volume of each stock.

This indicator will help you to plot Volume on Bank Nifty.

TurboVWAPVWAP indicator based in the built-in one but completely rewritten. Features:

- more standard deviation bands, up to 3.

- added the possibility to not anchor the VWAP but make it a rolling one instead, like a VWMA, being in this case able to specify days, hours or minutes for the rolling VWAP.

- for rolling VWAPs, the indicator doesn't count bars but real days, hours or minutes instead, so regardless of the chart timeframe the indicator will always show the correct values.

- for rolling VWAPs, if you specify x days as the rolling time, the indicator will always count exactly 24 hours from the current time backwards - so, from the same time yesterday or x days ago.

- in rolling VWAPs, although the indicator counts real time elapsed as per your settings and not chart bars, it will automatically skip holidays, so you needn't worry about that.

- for the anchored VWAP, added the possibility to specify custom session times (for example, for ES 0830-1500, instead of Globex, which is the Tradingview default as of today)

- complete customization of all fills and linetypes

For illustration purposes in the attached 1min chart I have:

- a 30min rolling VWAP in BLUE with no standard deviation plots,

- a 1 day rolling VWAP in RED with standard deviations in light red and green (these are the default settings)

- a RTH-session-anchored VWAP in ORANGE with standard deviations in light orange and light blue

EmperorBTC's VWAP StrategyEmperorBTC's VWAP Indicator & Strategy

v2.1

coded by Bogdan Vaida

This indicator was created after EmperorBTC's conditions.

Good timeframes for it: 30', 15', 5'

To convert from strategy to study switch the commented lines in the beginning

and at the end of the script and vice versa.

What this indicator does is to check if:

o Pivot Point was crossed

o Stoch-RSI and VWAP were crossed in current or previous candle

o Candle (or previous candle) close is in the trend direction

If all these are true then it will go long or short based on direction.

VWAPS MTF (Multi Timeframe) + candles color on crossingVolume weighted average price Multi Timeframe

Description:

Vwaps in 3 different types of time: Daily, weekly and monthly

This indicator has a built-in option that paints the price bars if they are above or below the daily vwap.

Features:

1 - Add or remove timeframe (unchecking colors).

2 - Edit the colors according to the price crossing up or down each vwap.

3 - Option that colored candles on Daily Vwap crossing.

GMS: GW-VWAPAlright, as per usual with these, I end up adapting an existing indicator to what I want to accomplish. So this is based off the built in VWAP indicator. I added in the gummy worm to easily identify the trend, as well as the related bands to identify potential areas to either reverse position or to trim an existing one.

The middle part of the bands are the gummy worm version of VWAP. It is the VWAP using the high and another VWAP using the low. The black line is HL2 VWAP (technically 3 VWAPs).

The bands follow what I was mentioning above. So the outer most part of the bands are the high & low VWAP (with the same multiplier) and the inner bands are the HL2 VWAP.

Of course you can set whatever input source you want for these. The default is how I use it. If you want to get rid of the bar color just go to the indicator settings and un-select it at the bottom.

Source code is open so feel free to poke around.

Hope this helps,

Andre

Multi-VWAPVolume Weighted Average Price (VWAP) Definition

What is the Volume Weighted Average Price (VWAP)?

The volume weighted average price (VWAP) is a trading benchmark used by traders that gives the average price a security has traded at throughout the day,

based on both volume and price. It is important because it provides traders with insight into both the trend and value of a security.

-Investopedia By JASON FERNANDO Reviewed by SOMER ANDERSON Updated Feb 24, 2021

-Choose from 5 different Timeframes (lower or higher)

Hull Suite by InSilico Extended 2x VersionJust an extended version of InSilicos great Hull Suite

Added Functions

- Second Hull Indicator with all options

- HTF color fix for the bands and barcolors

Vwap Comp [Auto+Osc] [Intromoto]This script compares the spot or USDT vwaps to the perpetuals, or USDTPERP, specifically for Binance.

This script will only work properly on binance perpetual charts. It auto detects which chart you're on and shows the appropriate comparison.

I made this due to the volume discrepancies between the derivative and spot markets.When the oscillator is below zero, the perpetual vwap is below the spot vwap, if it's above, the perpetual vwap is above the spot vwap.

Colors become more extreme the further away the vwaps are. Bright green increase the odds of a bullish reversal, red or pink columns indicate a potential for bearish reversal.

For example. If I'm on the BINANCE:ETHUSDTPERP chart, the script will compare the BINANCE:ETHUSDT to the BINANCE:ETHUSDTPERP vwaps with the input metrics.

Users can change the thresholds that determine the colors of the plots on the oscillator. Users can also input the time frame observed. The default is set to 'D' or daily Vwaps. If you change the time frame you'll likely have to tweak the thresholds to give reasonable color indication.

DM for access.

Thanks.

D/W/M VWAPsPlot Daily, Weekly and Monthly VWAPs

Preferences:

- Enable/Disable Daily, Weekly or Monthly VWAPs

- Color

- Hide in own Time Frame (i.e. Daily VWAP is hidden on 1D TF and above)

RSI Div at Daily VWAP StDevMean Reversion indicator based on RSI Divergences at Overbought/Oversold conditions with Price above/below a Standard Deviation from Daily VWAP. Useful for intra-day trading.

Signal criteria:

1. RSI is at Overbought/Oversold

2. RSI Divergence present (not hidden)

3. RSI has not reached Neutral level (i.e. 50)

4. Price has crossed above/below a Standard Deviation from Daily VWAP

Config Options:

- RSI length (default:14)

- Divergence Lookback Period (default:14)

- RSI Oversold/Overbought tresholds (default: 70/30)

- RSI Reset Level (default: 55/45)

- Use VWAP Std Dev (default: yes)

- Standard Deviation from Daily VWAP (default: 1.51)

Use with discretion.

EmperorBTC's VWAP IndicatorThis indicator was created after EmperorBTC's conditions. Conditions displayed below:

Good timeframes for it: 30', 15', 5'

To convert from strategy to study switch the commented lines in the beginning and at the end of the script

What this indicator does is:

1) Check if Pivot Point was crossed

2) Stoch-RSI and VWAP were crossed up in current or previous candle

3) Candle (or previous candle) is green

Then, it will plot a Long opportunity.

FUTURE IDEAS:

- Volume Expansion

- Candle Stick patterns

(JS) Interchanging ATR & VWAP BandsOkay so this is pretty simple, but I think it's a great tool for day trading especially. I just took the default VWAP and Keltner channel scripts and combined them together.

The top option allows you to choose which one you'd prefer to use, "Use ATR instead of VWAP" .

The next options, "ATR Source", "KC Length", and "ATR Length" are the parameters for the ATR Bands.

"Number of Bands" allows you to choose how many bands you'd like to be on display (you can choose 1-8).

"Use Expoential MA" and "Band Style" are more default parameters from Keltner Channels used to set up the ATR Bands.

The "ATR Bands" are just stacked Keltner Channels separated by 1 ATR each, whereas the "VWAP Bands" are separated by standard deviation just like the default script from Trading View.

In these example chart, you can see the weekly VWAP with 8 deviation bands and 5 ATR bands with Keltner Channels.